Research Proposal: Online Accounting System Impact on Small Businesses

VerifiedAdded on 2023/04/23

|14

|6104

|460

Report

AI Summary

This research proposal investigates the economic impact of online accounting systems on small-scale organizations in Australia. It begins by outlining the research problem, highlighting the increasing prevalence and challenges of online accounting software for small businesses. The study aims to evaluate the impact of these systems on economic growth, compare available options, and identify preferred software choices. The proposal includes a literature review covering cloud computing, intellectual capital, and the relationship between cloud-based accounting and business performance, identifying gaps for further research. The methodology section details the research philosophy, approach, design, data collection, analysis methods, sampling techniques, and ethical considerations for conducting the study. This proposal seeks to understand how online accounting systems contribute to the economic success of small and medium-scale businesses in the competitive Australian market. Desklib provides access to past papers and solved assignments to aid students in their studies.

Running head: RESEARCH PROPOSAL

Research Proposal

Name of the student

Name of the university

Author note

Research Proposal

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1RESEARCH PROPOSAL

Abstract

This report had proposed to examine the impact of online accounting system on the economic

performance of small-scale organization in Australia. The research had developed the

research question and hypothesis based on the objective in the research. The literature review

had identified the gap in previous literature to develop a research design suitable for

addressing the literature gap. The report had also developed effective research methodology

consisting research instruments and methods critical for conducting the data collection and

analysis.

Abstract

This report had proposed to examine the impact of online accounting system on the economic

performance of small-scale organization in Australia. The research had developed the

research question and hypothesis based on the objective in the research. The literature review

had identified the gap in previous literature to develop a research design suitable for

addressing the literature gap. The report had also developed effective research methodology

consisting research instruments and methods critical for conducting the data collection and

analysis.

2RESEARCH PROPOSAL

Table of Contents

1.0 Introduction..........................................................................................................................3

1.1 Research Problem.............................................................................................................3

1.2 Background of the study..................................................................................................3

1.3 Objective of the research..................................................................................................4

1.4 Research question.............................................................................................................4

1.5 Research hypothesis.........................................................................................................4

2.0 Literature review..................................................................................................................5

2.1 Introduction......................................................................................................................5

2.2 Cloud Computing.............................................................................................................5

2.3 Intellectual Capital...........................................................................................................5

2.4 Cloud based accounting and business performance.........................................................6

2.5 Conceptual framework.....................................................................................................7

2.6 Literature gap...................................................................................................................7

3.0 Research methodology.........................................................................................................7

3.1 Research philosophy........................................................................................................8

3.2 Research approach...........................................................................................................8

3.3 Research design................................................................................................................8

3.4 Data collection and Analysis............................................................................................9

3.5 Sampling..........................................................................................................................9

3.6 Reliability and Validity..................................................................................................10

3.7 Ethical consideration......................................................................................................10

4.0 References..........................................................................................................................11

Table of Contents

1.0 Introduction..........................................................................................................................3

1.1 Research Problem.............................................................................................................3

1.2 Background of the study..................................................................................................3

1.3 Objective of the research..................................................................................................4

1.4 Research question.............................................................................................................4

1.5 Research hypothesis.........................................................................................................4

2.0 Literature review..................................................................................................................5

2.1 Introduction......................................................................................................................5

2.2 Cloud Computing.............................................................................................................5

2.3 Intellectual Capital...........................................................................................................5

2.4 Cloud based accounting and business performance.........................................................6

2.5 Conceptual framework.....................................................................................................7

2.6 Literature gap...................................................................................................................7

3.0 Research methodology.........................................................................................................7

3.1 Research philosophy........................................................................................................8

3.2 Research approach...........................................................................................................8

3.3 Research design................................................................................................................8

3.4 Data collection and Analysis............................................................................................9

3.5 Sampling..........................................................................................................................9

3.6 Reliability and Validity..................................................................................................10

3.7 Ethical consideration......................................................................................................10

4.0 References..........................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3RESEARCH PROPOSAL

Title: Economic Impact of Online Accounting System on Small Business in Australia

1.0 Introduction

This research had aimed to critically evaluate the impact of online accounting systems

on economic aspect of small-scale organizations. The use of accounting software has become

one of the most necessary things for the small-scale businesses in Australia. Xero, Intuit and

Sage have increased their number of subscriptions from small scale business organizations.

The online accounting system have reduced the time spent on manual drudge work in

accounting. The small-scale businesses have to go through many issues due to the changing

nature of the political and economic environment of the country in the past decade. The most

significant pain point for these organizations were the availability of online technology at

affordable prices. Emergence of new technologies in the field of cloud accounting have

reduced these issues significantly and the study will examine the nature and direction of

relationship between the online accounting systems and economic impact on small scale

organizations.

1.1 Research Problem

Online accounting has reached the notable benchmark when maturity is taken into

account. The power of desktop accounting systems has been replicated through huge

ecosystems of online applications that are compatible to each other. Amazon Web Services is

one of the most popular platforms for executing SaaS (software as a service) and many

companies have opted for these services which reduced the subscription of major companies

like Sage, Intuit and Xero. These organizations have all lost their CEO’s in the past year

which have increased the problems for these organizations. The majority of the companies

are attempting to automate the reconciliation processes. The availability of large number of

organizations have provided the businesses in Australia with excess options and the market

has become overcrowded which made the choice of platform quite difficult for small scale

business organizations. Therefore, the research would aim to understand and identify the

software that is best suitable and preferred by the small-scale organizations and the rationale

of their choice.

1.2 Background of the study

Cloud accounting system has become the trend in the last five years and has become

mainstream for the small-scale companies in Australia. Cloud accounting systems are

dominating the market and it has become dominant as it can be accessed from anywhere if

internet facilities are available. Moreover, there has been increase in connectivity in cloud

accounting systems which includes automated transactions, payment gateway support,

lodgements for tax offices and SuperStream payments (Macpherson, 2015). Connectivity is

one of the most positive feature of cloud accounting systems and can be augmented

effortlessly by other cloud computing applications such as ecommerce, debt chasing, business

intelligence and point-of scale (Withers, 2018). This facilitates in selecting the customer

relationship management system ideal to the needs of the business. The effective integration

of both the systems facilitates in accessing same contact details for both the linked systems.

In Australia, the third-party application ecosystems have matured significantly which

is a critical factor in deciding upon the suitable accounting software. Moreover, the core

functions, its convenience and usability are other key factors for choosing an appropriate

cloud-based accounting system. The six most significant cloud accounting system are Saasu,

Xero, Sage, QuickBooks Online Plus, Reckon One and MYOB Essentials (Macpherson,

2018). The use of new global accounting software is basic necessity of the organizations for

dealing with multiple currencies and accounting rules and regulations in different countries.

Title: Economic Impact of Online Accounting System on Small Business in Australia

1.0 Introduction

This research had aimed to critically evaluate the impact of online accounting systems

on economic aspect of small-scale organizations. The use of accounting software has become

one of the most necessary things for the small-scale businesses in Australia. Xero, Intuit and

Sage have increased their number of subscriptions from small scale business organizations.

The online accounting system have reduced the time spent on manual drudge work in

accounting. The small-scale businesses have to go through many issues due to the changing

nature of the political and economic environment of the country in the past decade. The most

significant pain point for these organizations were the availability of online technology at

affordable prices. Emergence of new technologies in the field of cloud accounting have

reduced these issues significantly and the study will examine the nature and direction of

relationship between the online accounting systems and economic impact on small scale

organizations.

1.1 Research Problem

Online accounting has reached the notable benchmark when maturity is taken into

account. The power of desktop accounting systems has been replicated through huge

ecosystems of online applications that are compatible to each other. Amazon Web Services is

one of the most popular platforms for executing SaaS (software as a service) and many

companies have opted for these services which reduced the subscription of major companies

like Sage, Intuit and Xero. These organizations have all lost their CEO’s in the past year

which have increased the problems for these organizations. The majority of the companies

are attempting to automate the reconciliation processes. The availability of large number of

organizations have provided the businesses in Australia with excess options and the market

has become overcrowded which made the choice of platform quite difficult for small scale

business organizations. Therefore, the research would aim to understand and identify the

software that is best suitable and preferred by the small-scale organizations and the rationale

of their choice.

1.2 Background of the study

Cloud accounting system has become the trend in the last five years and has become

mainstream for the small-scale companies in Australia. Cloud accounting systems are

dominating the market and it has become dominant as it can be accessed from anywhere if

internet facilities are available. Moreover, there has been increase in connectivity in cloud

accounting systems which includes automated transactions, payment gateway support,

lodgements for tax offices and SuperStream payments (Macpherson, 2015). Connectivity is

one of the most positive feature of cloud accounting systems and can be augmented

effortlessly by other cloud computing applications such as ecommerce, debt chasing, business

intelligence and point-of scale (Withers, 2018). This facilitates in selecting the customer

relationship management system ideal to the needs of the business. The effective integration

of both the systems facilitates in accessing same contact details for both the linked systems.

In Australia, the third-party application ecosystems have matured significantly which

is a critical factor in deciding upon the suitable accounting software. Moreover, the core

functions, its convenience and usability are other key factors for choosing an appropriate

cloud-based accounting system. The six most significant cloud accounting system are Saasu,

Xero, Sage, QuickBooks Online Plus, Reckon One and MYOB Essentials (Macpherson,

2018). The use of new global accounting software is basic necessity of the organizations for

dealing with multiple currencies and accounting rules and regulations in different countries.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4RESEARCH PROPOSAL

The use of effective accounting tool has been one of the key elements of managing

sustainability of organizations as companies require information, both non-financial and

financial to survive in markets where the level of competition is very high (Myob.com,

2017).

The significant change in the market can be understood from the fact that it has

changed from being a duopoly to one of most competitive environments. The market is

highly competitive and consists of different types of competitors and can be divided in to

groups. The first group is the incumbents consisting of MYOB and Reckon that have been the

big players in Australia. These companies have been late in developing the online version of

their existing software. However, they have made steady progress since 2015 where they

have managed to rebrand their image and provide consumers with online version of their

software. The next category consists of the global giants and consists of Intuit, Sage and

QuickBooks Online which has intensified the competition in the market (Macpherson, 2018).

These companies have the potential of competing with Xero at par. The third category are

insurgents and consists of companies such as Xero and Saasu which has revolutionized this

market and were the early movers in the market. The next category consists of the new

companies in the accounting software business and consists of company such as NetSuite.

NetSuite had been providing ERP services to small and medium scale organization that were

growing rapidly but have entered the market of accounting systems with JCurve

(Macpherson, 2018).

This shows that the market of accounting systems for small and medium scale

companies have changed rapidly in the last five years due to the emergence of large number

of players in the market. The research would address this topic to understand the most

preferred accounting software for the companies and how it helps in improving the economic

growth of small and medium scale businesses.

1.3 Objective of the research

The objective of the research are as follows:

To examine the impact of online accounting systems on the economic growth of

small- scale organizations

To critically evaluate the different options available for small scale organizations in

terms of online accounting systems

To identify the most preferred online accounting software among small scale

businesses

1.4 Research question

What is the impact of online accounting systems on the economic aspect of small-

scale organizations?

What are the different options available for small scale organizations in terms of

online accounting systems?

What is the most preferred online accounting software among small scale businesses

in Australia?

1.5 Research hypothesis

H0: There is no significant impact of cloud based accounting system on the economic growth

of small scale organizations

H1: There is significant impact of cloud based accounting system on the economic growth of

small scale organizations

The use of effective accounting tool has been one of the key elements of managing

sustainability of organizations as companies require information, both non-financial and

financial to survive in markets where the level of competition is very high (Myob.com,

2017).

The significant change in the market can be understood from the fact that it has

changed from being a duopoly to one of most competitive environments. The market is

highly competitive and consists of different types of competitors and can be divided in to

groups. The first group is the incumbents consisting of MYOB and Reckon that have been the

big players in Australia. These companies have been late in developing the online version of

their existing software. However, they have made steady progress since 2015 where they

have managed to rebrand their image and provide consumers with online version of their

software. The next category consists of the global giants and consists of Intuit, Sage and

QuickBooks Online which has intensified the competition in the market (Macpherson, 2018).

These companies have the potential of competing with Xero at par. The third category are

insurgents and consists of companies such as Xero and Saasu which has revolutionized this

market and were the early movers in the market. The next category consists of the new

companies in the accounting software business and consists of company such as NetSuite.

NetSuite had been providing ERP services to small and medium scale organization that were

growing rapidly but have entered the market of accounting systems with JCurve

(Macpherson, 2018).

This shows that the market of accounting systems for small and medium scale

companies have changed rapidly in the last five years due to the emergence of large number

of players in the market. The research would address this topic to understand the most

preferred accounting software for the companies and how it helps in improving the economic

growth of small and medium scale businesses.

1.3 Objective of the research

The objective of the research are as follows:

To examine the impact of online accounting systems on the economic growth of

small- scale organizations

To critically evaluate the different options available for small scale organizations in

terms of online accounting systems

To identify the most preferred online accounting software among small scale

businesses

1.4 Research question

What is the impact of online accounting systems on the economic aspect of small-

scale organizations?

What are the different options available for small scale organizations in terms of

online accounting systems?

What is the most preferred online accounting software among small scale businesses

in Australia?

1.5 Research hypothesis

H0: There is no significant impact of cloud based accounting system on the economic growth

of small scale organizations

H1: There is significant impact of cloud based accounting system on the economic growth of

small scale organizations

5RESEARCH PROPOSAL

2.0 Literature review

2.1 Introduction

As stated by Fatima, (2016), there has been drastic changes in the modern business

environment due to the advancement of business technology. The development of business

functions and operations have reached the highest possible level where accounting has a

special role to play. Rogers, (2016) states that even though, the overall process of accounting

has changed but the purpose has remained the same for organizations. The financial

performance of companies is measured using accounting tools. According to Fatima, (2016),

accounting facilities in recording, reporting and analysing the business transactions.

Managers and owners use financial data such as ratios to examine the health and performance

of the organizations. Informational technology has brought about quantitative and qualitative

changes to accounting management systems. The development of informational technology

has provided different dimension to the development of online accounting systems.

2.2 Cloud Computing

According to Armitage, Webb and Glynn, (2016), cloud computing is the method of

centralizing data of a firm via shared providers and it can only be accessed through internet

enabled devices and limited users. There are generally three basic models of cloud computing

and they are Software as a Service (SaaS), Platform as a Service (PaaS) and Infrastructure as

a Service (IaaS). SaaS facilitates a cloud user to run software on cloud platforms and majority

of the accounting companies are providing these facilities (Cleary and Quinn, 2016). PaaS

facilities in deploying and developing a software or application using infrastructure and tools

provided by cloud service providers. IaaS provides hardware and storage services with

maximum control over the computing resources.

Cleary and Quinn, (2016) states that cloud computing provides multiple benefits to

firms such as reduction in information technology cost, reduces the barrier to innovation,

availability of global systems, automatic access to updates for systems and software and

ability to scale informational technology requirements. Brandas, Megan and Didraga, (2015)

opined that introduction to cloud computing has reduced the cost of powerful information

technology infrastructure quite less and small-scale companies are able to readily access

technology which was only available to large scale companies due to huge capital

investments. Moreover, cloud computing facilitates in freeing up space in different

functional areas such as in financial accounting. Desai et al., (2018) argued that even though

there are many advantages of using cloud-based accounting software but there are problems

of reliability privacy and data protection. On the contrary, Dimitriu and Matei (2015) states

that cloud-based applications have reached maturity in the market and companies need cloud-

based accounting systems for surviving in the industry. Leach, Zhang and Weimer, (2017)

states that cloud-based applications are more secure than organizational systems as IT

personnel support them at all times. Desai et al., (2018) argued that it is not feasible to use

cloud-based accounting systems as it a primary repository for data which I critical in nature.

Therefore, it might be suitable to try put other functions at first before moving on to the

accounting function. As stated by Cleary and Quinn, (2016), cloud-based computing can

provide better flow of information and improve the accessibility of data. This would

definitely improve decision making at different levels of hierarchy which would enhance the

performance of the organization.

2.0 Literature review

2.1 Introduction

As stated by Fatima, (2016), there has been drastic changes in the modern business

environment due to the advancement of business technology. The development of business

functions and operations have reached the highest possible level where accounting has a

special role to play. Rogers, (2016) states that even though, the overall process of accounting

has changed but the purpose has remained the same for organizations. The financial

performance of companies is measured using accounting tools. According to Fatima, (2016),

accounting facilities in recording, reporting and analysing the business transactions.

Managers and owners use financial data such as ratios to examine the health and performance

of the organizations. Informational technology has brought about quantitative and qualitative

changes to accounting management systems. The development of informational technology

has provided different dimension to the development of online accounting systems.

2.2 Cloud Computing

According to Armitage, Webb and Glynn, (2016), cloud computing is the method of

centralizing data of a firm via shared providers and it can only be accessed through internet

enabled devices and limited users. There are generally three basic models of cloud computing

and they are Software as a Service (SaaS), Platform as a Service (PaaS) and Infrastructure as

a Service (IaaS). SaaS facilitates a cloud user to run software on cloud platforms and majority

of the accounting companies are providing these facilities (Cleary and Quinn, 2016). PaaS

facilities in deploying and developing a software or application using infrastructure and tools

provided by cloud service providers. IaaS provides hardware and storage services with

maximum control over the computing resources.

Cleary and Quinn, (2016) states that cloud computing provides multiple benefits to

firms such as reduction in information technology cost, reduces the barrier to innovation,

availability of global systems, automatic access to updates for systems and software and

ability to scale informational technology requirements. Brandas, Megan and Didraga, (2015)

opined that introduction to cloud computing has reduced the cost of powerful information

technology infrastructure quite less and small-scale companies are able to readily access

technology which was only available to large scale companies due to huge capital

investments. Moreover, cloud computing facilitates in freeing up space in different

functional areas such as in financial accounting. Desai et al., (2018) argued that even though

there are many advantages of using cloud-based accounting software but there are problems

of reliability privacy and data protection. On the contrary, Dimitriu and Matei (2015) states

that cloud-based applications have reached maturity in the market and companies need cloud-

based accounting systems for surviving in the industry. Leach, Zhang and Weimer, (2017)

states that cloud-based applications are more secure than organizational systems as IT

personnel support them at all times. Desai et al., (2018) argued that it is not feasible to use

cloud-based accounting systems as it a primary repository for data which I critical in nature.

Therefore, it might be suitable to try put other functions at first before moving on to the

accounting function. As stated by Cleary and Quinn, (2016), cloud-based computing can

provide better flow of information and improve the accessibility of data. This would

definitely improve decision making at different levels of hierarchy which would enhance the

performance of the organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6RESEARCH PROPOSAL

2.3 Intellectual Capital

Cleary and Quinn, (2016) states that it is essential to use intellectual capital to its

fullest potential to increase their competitiveness in the market. Intellectual capital consists

of structural capital, relational capital and human capital. Knowledge management is a key

aspect for companies as effective utilization of resources is necessity. Human capital includes

explicit and tacit knowledge acquired by the employees within the organization. Structural

capital consists of different rules, norms, procedures and rules that form the core of the firm.

Relational capital consists of the knowledge developed by establishing relationship with key

stakeholders. These factors help firms in maintaining their competitive position in the

market. Organization value creation for firms requires their unique sets of intellectual capital.

Melo and Machado, (2018) states that non-physical resources are key value drivers for

organizations and firms require extensive control over their systems to realise their full

potential.

Asiaei, Jusoh and Bontis, (2018) states that management of intellectual property leads

to superiority in financial performance and driving factor for value creation within the

company. However, it is difficult to understand the impact of only one resource on value

creation as they act in bundles. Secundo et al., (2017) states, it is safe to say that there is inter

dependency between the resources for creating value. In terms of value creation, structural

capital can be considered as one of the most valuable assets for companies. This means that

accounting is one of the critical component of structural capital. Novas, Alves and Sousa,

(2017) states that majority of the value is generated from the past experiences of the

employees and it is difficult to transfer this knowledge effectively to enhance the financial

performance of the organization.

2.4 Cloud based accounting and business performance

Dimitriu and Matei, (2015) states that it is easier for the small-scale companies to

utilize their scarce resources effectively by adopting accounting software based on cloud

computing. This will create strategic purpose and add more value to the organization.

Khomonenko and Gindin, (2016) opined, small-scale organizations are switching to these

software as traditional ways of accounting is time consuming and expensive from the

perspective of the firm. Small scale and Start-up companies have been eager to adapt to cloud

based information technology systems and cloud computing to check their cost. On the

contrary, Cleary and Quinn, (2016) states that medium scale organizations are reluctant to

switch as they have spent considerable amount of capital for developing their own

information technology infrastructure. Larger companies also use their own cloud

infrastructure as using off shared space is less beneficial to such organizations. Al-Aqrabi et

al., (2015) states that cloud based accounting has the ability to impact all the three aspects of

intellectual component by enhancing knowledge sharing practices. This effects the process of

value creation and positively impacts the performance of the business.

Inggarsono et al., (2018) states that organizational performance is enhanced by the

incorporation of innovation strategy which is either process orientated or product oriented. It

is obvious that small-scale organizations having better alignment in information technology

systems will have a competitive advantage over other companies in the industry. Secundo et

al., (2017) opined that characteristics of accounting software are essential for improving the

performance of the organization and they are efficiency, reliability, data quality, accuracy and

ease of use. These factors are crucial factors for improving the economic aspect of the firm.

The ability of the firm to gain more outputs by using minimum amount of input is known as

efficiency. Asiaei, Jusoh and Bontis, (2018) opined that small-scale firms aim to improve

their business performance by reaching economies of scale where efficiency is a key criteria.

2.3 Intellectual Capital

Cleary and Quinn, (2016) states that it is essential to use intellectual capital to its

fullest potential to increase their competitiveness in the market. Intellectual capital consists

of structural capital, relational capital and human capital. Knowledge management is a key

aspect for companies as effective utilization of resources is necessity. Human capital includes

explicit and tacit knowledge acquired by the employees within the organization. Structural

capital consists of different rules, norms, procedures and rules that form the core of the firm.

Relational capital consists of the knowledge developed by establishing relationship with key

stakeholders. These factors help firms in maintaining their competitive position in the

market. Organization value creation for firms requires their unique sets of intellectual capital.

Melo and Machado, (2018) states that non-physical resources are key value drivers for

organizations and firms require extensive control over their systems to realise their full

potential.

Asiaei, Jusoh and Bontis, (2018) states that management of intellectual property leads

to superiority in financial performance and driving factor for value creation within the

company. However, it is difficult to understand the impact of only one resource on value

creation as they act in bundles. Secundo et al., (2017) states, it is safe to say that there is inter

dependency between the resources for creating value. In terms of value creation, structural

capital can be considered as one of the most valuable assets for companies. This means that

accounting is one of the critical component of structural capital. Novas, Alves and Sousa,

(2017) states that majority of the value is generated from the past experiences of the

employees and it is difficult to transfer this knowledge effectively to enhance the financial

performance of the organization.

2.4 Cloud based accounting and business performance

Dimitriu and Matei, (2015) states that it is easier for the small-scale companies to

utilize their scarce resources effectively by adopting accounting software based on cloud

computing. This will create strategic purpose and add more value to the organization.

Khomonenko and Gindin, (2016) opined, small-scale organizations are switching to these

software as traditional ways of accounting is time consuming and expensive from the

perspective of the firm. Small scale and Start-up companies have been eager to adapt to cloud

based information technology systems and cloud computing to check their cost. On the

contrary, Cleary and Quinn, (2016) states that medium scale organizations are reluctant to

switch as they have spent considerable amount of capital for developing their own

information technology infrastructure. Larger companies also use their own cloud

infrastructure as using off shared space is less beneficial to such organizations. Al-Aqrabi et

al., (2015) states that cloud based accounting has the ability to impact all the three aspects of

intellectual component by enhancing knowledge sharing practices. This effects the process of

value creation and positively impacts the performance of the business.

Inggarsono et al., (2018) states that organizational performance is enhanced by the

incorporation of innovation strategy which is either process orientated or product oriented. It

is obvious that small-scale organizations having better alignment in information technology

systems will have a competitive advantage over other companies in the industry. Secundo et

al., (2017) opined that characteristics of accounting software are essential for improving the

performance of the organization and they are efficiency, reliability, data quality, accuracy and

ease of use. These factors are crucial factors for improving the economic aspect of the firm.

The ability of the firm to gain more outputs by using minimum amount of input is known as

efficiency. Asiaei, Jusoh and Bontis, (2018) opined that small-scale firms aim to improve

their business performance by reaching economies of scale where efficiency is a key criteria.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7RESEARCH PROPOSAL

Reliability of the information gathered is significant as it impacts the overall decision making

process of the company. Accounting systems provide information that are reliable and free of

error which enhances the decision making capabilities of the organization which increases the

internal efficiency of the organization. The usability of the software is one of the major

factors as software need to be user friendly but these aspect has not been considered in

majority of the studies. Online accounting software has to be easy to use so that it can used

any person having minimum knowledge of the subject. The data quality is also a key factor in

improving the performance of the business. Khomonenko and Gindin, (2016) states that

quality of data inputted and outputted from the systems have to be of highest quality to

enhance the decision making process. Internal auditing is always required to maintain the

quality of the data and the use of online accounting software makes the quality of the data

high and relevant for evaluation. Leach, Zhang and Weimer, (2017) states that precision and

accuracy are two critical aspect of accounting data and online accounting software provides

the data with highest accuracy and precision. The credibility of the information makes the

decision making for the companies accurate and online accounting software adds credibility

to the data as there is significant reduction in chances of human error. The business

achievement of any organization depend on their operational and financial performance and

the consistency of the financial data drives these factors.

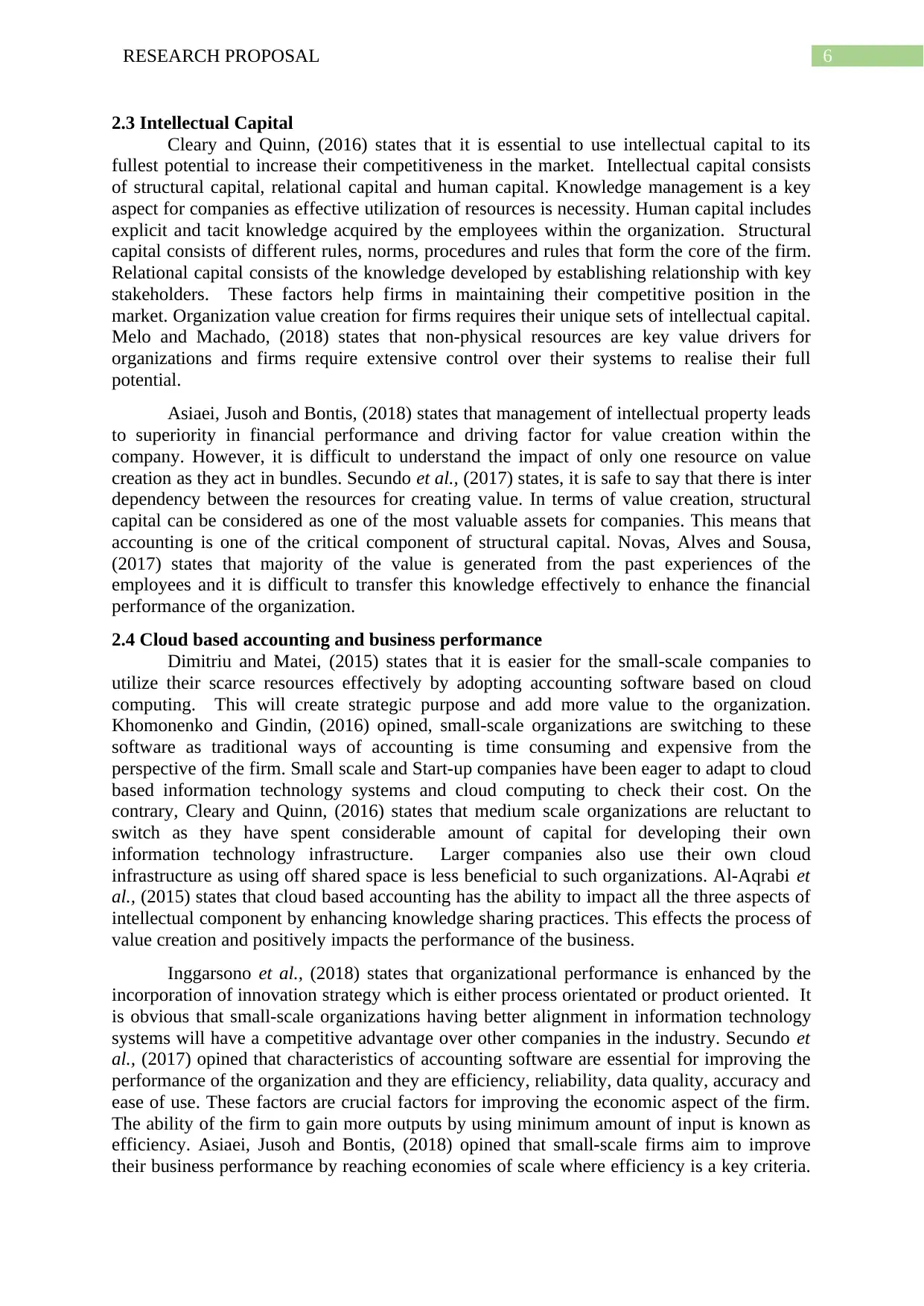

2.5 Conceptual framework

Figure 1: Conceptual Framework

Source:

2.6 Literature gap

The majority of the literature has failed to identify the impact of online accounting

system on business and economic performances of small-scale organizations. The concept of

online accounting software and cloud computing is relatively new and most of the literature

has not addressed the characteristics of the different cloud accounting software and the way it

impacts the economic performance of small scale organizations. However, even though it is a

broad topic, Australia is one of the major markets where the competition and use of online

Reliability of the information gathered is significant as it impacts the overall decision making

process of the company. Accounting systems provide information that are reliable and free of

error which enhances the decision making capabilities of the organization which increases the

internal efficiency of the organization. The usability of the software is one of the major

factors as software need to be user friendly but these aspect has not been considered in

majority of the studies. Online accounting software has to be easy to use so that it can used

any person having minimum knowledge of the subject. The data quality is also a key factor in

improving the performance of the business. Khomonenko and Gindin, (2016) states that

quality of data inputted and outputted from the systems have to be of highest quality to

enhance the decision making process. Internal auditing is always required to maintain the

quality of the data and the use of online accounting software makes the quality of the data

high and relevant for evaluation. Leach, Zhang and Weimer, (2017) states that precision and

accuracy are two critical aspect of accounting data and online accounting software provides

the data with highest accuracy and precision. The credibility of the information makes the

decision making for the companies accurate and online accounting software adds credibility

to the data as there is significant reduction in chances of human error. The business

achievement of any organization depend on their operational and financial performance and

the consistency of the financial data drives these factors.

2.5 Conceptual framework

Figure 1: Conceptual Framework

Source:

2.6 Literature gap

The majority of the literature has failed to identify the impact of online accounting

system on business and economic performances of small-scale organizations. The concept of

online accounting software and cloud computing is relatively new and most of the literature

has not addressed the characteristics of the different cloud accounting software and the way it

impacts the economic performance of small scale organizations. However, even though it is a

broad topic, Australia is one of the major markets where the competition and use of online

8RESEARCH PROPOSAL

accounting system has intensified. The impact of online accounting systems on economic

performance will be evaluated in context to the Australian small-scale companies.

3.0 Research methodology

Research methodology is the systematic way of collecting data and analysing based

on the objective of the research. Research methodology will be developed based on the

objective of the research. The research will follow Saunders research onion to define the

philosophy, approach, design, validity, reliability, data collection, analysis and sampling

methods. The three main purpose of conducting a research are description of behaviour,

reliable predictions and cause and effect relationship between variables (Taylor, Bogdan and

DeVault, 2015). In this current study, all the above-mentioned points are crucial aspect of the

research. This is the reason that the study will use experimental method which will facilitate

explanation of the overall phenomenon and will include description, prediction and causal

relationship. This is a fundamental research as the findings of the research does not have any

practical implication attached to it. However, this research will assist in generalization the

change and facilitate in generating more knowledge regarding the topic.

3.1 Research philosophy

Research philosophy consists of the beliefs and assumptions made by the research

based on the research questions in the research. The nature, source and development of

knowledge is considered in the research which facilitates in understanding the way the data

needs to be collected to derive effective results in the research. The different research

philosophies are interpretivism, positivism, realism and pragmatism. However, in this study

pragmatism will be chosen as the philosophy (Flick, 2015). Pragmatism accepts theories if

they have valid actions supporting them and it chooses different data collection methods

based on each question in the research. Therefore, it can be used for conducting a mixed

method analysis where both qualitative and quantitative data analysis can be used.

Pragmatism facilities in modifying philosophical assumptions as it considers that multiple

viewpoints exist to a research problem and multiple realities can co-exist (Kennedy, 2017).

Therefore, as research question is the most critical determinant in the research, pragmatism

will use suitable methods based on the questions.

3.2 Research approach

The three different research approaches used in the research are inductive, deductive

and abductive approach. The significance of hypothesis in the research defines the

appropriate approach to be used. The inductive approach is used to conducting exploratory

studies where new paradigms, theories and generalizations are developed. This means that in

inductive approach, the hypothesis is developed after the data has been collected. On the

contrary, in case of deductive approach, the hypothesis is developed based on the existing

theories and critical review of literature (Sekaran and Bougie, 2016). Abductive approach is

used to meet the limitations of both inductive and deductive approach where surprising facts

are stated at the initial phase of the research and the remaining research focuses on proving

that fact. In this current research, deductive approach will be used to test the hypothesis

developed based on the literature review and will facilitate in evaluating the relationship

between online accounting systems and economic growth for different companies.

3.3 Research design

Research design has been used to defined differently by different authors where some

consider it as the choice between qualitative and quantitative methods while other consider it

as the method of choosing the appropriate method for data analysis and collection. However,

in general terms, research design can be defined as the plan for collecting data and analysing

accounting system has intensified. The impact of online accounting systems on economic

performance will be evaluated in context to the Australian small-scale companies.

3.0 Research methodology

Research methodology is the systematic way of collecting data and analysing based

on the objective of the research. Research methodology will be developed based on the

objective of the research. The research will follow Saunders research onion to define the

philosophy, approach, design, validity, reliability, data collection, analysis and sampling

methods. The three main purpose of conducting a research are description of behaviour,

reliable predictions and cause and effect relationship between variables (Taylor, Bogdan and

DeVault, 2015). In this current study, all the above-mentioned points are crucial aspect of the

research. This is the reason that the study will use experimental method which will facilitate

explanation of the overall phenomenon and will include description, prediction and causal

relationship. This is a fundamental research as the findings of the research does not have any

practical implication attached to it. However, this research will assist in generalization the

change and facilitate in generating more knowledge regarding the topic.

3.1 Research philosophy

Research philosophy consists of the beliefs and assumptions made by the research

based on the research questions in the research. The nature, source and development of

knowledge is considered in the research which facilitates in understanding the way the data

needs to be collected to derive effective results in the research. The different research

philosophies are interpretivism, positivism, realism and pragmatism. However, in this study

pragmatism will be chosen as the philosophy (Flick, 2015). Pragmatism accepts theories if

they have valid actions supporting them and it chooses different data collection methods

based on each question in the research. Therefore, it can be used for conducting a mixed

method analysis where both qualitative and quantitative data analysis can be used.

Pragmatism facilities in modifying philosophical assumptions as it considers that multiple

viewpoints exist to a research problem and multiple realities can co-exist (Kennedy, 2017).

Therefore, as research question is the most critical determinant in the research, pragmatism

will use suitable methods based on the questions.

3.2 Research approach

The three different research approaches used in the research are inductive, deductive

and abductive approach. The significance of hypothesis in the research defines the

appropriate approach to be used. The inductive approach is used to conducting exploratory

studies where new paradigms, theories and generalizations are developed. This means that in

inductive approach, the hypothesis is developed after the data has been collected. On the

contrary, in case of deductive approach, the hypothesis is developed based on the existing

theories and critical review of literature (Sekaran and Bougie, 2016). Abductive approach is

used to meet the limitations of both inductive and deductive approach where surprising facts

are stated at the initial phase of the research and the remaining research focuses on proving

that fact. In this current research, deductive approach will be used to test the hypothesis

developed based on the literature review and will facilitate in evaluating the relationship

between online accounting systems and economic growth for different companies.

3.3 Research design

Research design has been used to defined differently by different authors where some

consider it as the choice between qualitative and quantitative methods while other consider it

as the method of choosing the appropriate method for data analysis and collection. However,

in general terms, research design can be defined as the plan for collecting data and analysing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9RESEARCH PROPOSAL

it based on the research questions and objectives. Research design can be divided into three

groups and they are exploratory, explanatory and conclusive (Morse, 2016). However, in this

study, explanatory research design has been used to facilitate the mixed method analysis.

Explanatory research design is used for studies which lacks in depth analysis from previous

researches. This will facilitate in explaining the phenomenon for the study. In this study, the

sequential explanatory design will be used which will consist of conducting both quantitative

and qualitative data analysis. In sequential explanatory research design, quantitative data

analysis will be conducted to analyse the data collected and then qualitative analysis will be

used to compare and explain the results obtained from the quantitative data analysis in the

research (Maxwell, Chmiel and Rogers, 2015). This will facilitate in overcoming the

weakness of single research design and assists in addressing questions at different levels and

layers.

3.4 Data collection and Analysis

Data is collected using primary and secondary data collection methods. In this study,

the data collection will be collected through primary data collection method where

quantitative data will be collected through online survey questionnaires which will be asked

to accountants working in different organizations (Palinkas et al., 2015). The qualitative data

will be collected through interview questionnaire which will be asked to the financial

managers of small scale companies. The quantitative questionnaire will consist of close

ended question so that relevant answers can be obtained from the research. The qualitative

questionnaire will consist of open-ended questions which will provide in depth answers to the

research question.

The quantitative data will be analysed using SPSS (Statistical tool for social sciences)

which is a statistical tool for conducting inferential statistics in the research. The responses

from the participants will be represented through frequency tables and graphs. The study will

also conduct regression analysis, correlation and cross tabulation to examine the relationship

between online accounting software and economic growth of small and medium scale

organizations. The correlation analysis and hypothesis testing will facilitate in understanding

the nature and direction of relationship between the variables (Smith, Cannata and Haynes,

2016). The regression analysis will be conducted to develop a linear model for representation

the degree of relationship. The qualitative data will be analysed using coding where initially

open coding will be executed. Open coding will examine the statements and remarks made by

the participants to identify key words and theories in the answers. Axial coding will be used

to examine these codes and identify the pattern in the answers collected from the respondents.

The qualitative analysis will facilitate in comparing with the data collected from the

quantitative analysis and explaining the phenomenon in detail.

3.5 Sampling

Sampling is the method of choosing the elements from the overall sample population.

Sampling is used to reduce the complexity of the study and manage cost associated with it.

The process of sampling in primary data analysis consists of five steps. The first step is

choosing the target population where the best segment of the population is chosen that would

provide effective data in primary analysis (Etikan, Musa and Alkassim, 2016). The next step

is choosing the sampling frame in the research which will determine the participants within

the chosen population. The third step is choosing the sample size of the population. The four

step is choosing the sampling technique to be used based on the needs of the research and

finally, the last step is implementing the sampling method. There are basically two types of

sampling method, one is probabilistic sampling and another is non-probabilistic sampling.

Probabilistic sampling consists of methods such as simple random sampling, cluster

it based on the research questions and objectives. Research design can be divided into three

groups and they are exploratory, explanatory and conclusive (Morse, 2016). However, in this

study, explanatory research design has been used to facilitate the mixed method analysis.

Explanatory research design is used for studies which lacks in depth analysis from previous

researches. This will facilitate in explaining the phenomenon for the study. In this study, the

sequential explanatory design will be used which will consist of conducting both quantitative

and qualitative data analysis. In sequential explanatory research design, quantitative data

analysis will be conducted to analyse the data collected and then qualitative analysis will be

used to compare and explain the results obtained from the quantitative data analysis in the

research (Maxwell, Chmiel and Rogers, 2015). This will facilitate in overcoming the

weakness of single research design and assists in addressing questions at different levels and

layers.

3.4 Data collection and Analysis

Data is collected using primary and secondary data collection methods. In this study,

the data collection will be collected through primary data collection method where

quantitative data will be collected through online survey questionnaires which will be asked

to accountants working in different organizations (Palinkas et al., 2015). The qualitative data

will be collected through interview questionnaire which will be asked to the financial

managers of small scale companies. The quantitative questionnaire will consist of close

ended question so that relevant answers can be obtained from the research. The qualitative

questionnaire will consist of open-ended questions which will provide in depth answers to the

research question.

The quantitative data will be analysed using SPSS (Statistical tool for social sciences)

which is a statistical tool for conducting inferential statistics in the research. The responses

from the participants will be represented through frequency tables and graphs. The study will

also conduct regression analysis, correlation and cross tabulation to examine the relationship

between online accounting software and economic growth of small and medium scale

organizations. The correlation analysis and hypothesis testing will facilitate in understanding

the nature and direction of relationship between the variables (Smith, Cannata and Haynes,

2016). The regression analysis will be conducted to develop a linear model for representation

the degree of relationship. The qualitative data will be analysed using coding where initially

open coding will be executed. Open coding will examine the statements and remarks made by

the participants to identify key words and theories in the answers. Axial coding will be used

to examine these codes and identify the pattern in the answers collected from the respondents.

The qualitative analysis will facilitate in comparing with the data collected from the

quantitative analysis and explaining the phenomenon in detail.

3.5 Sampling

Sampling is the method of choosing the elements from the overall sample population.

Sampling is used to reduce the complexity of the study and manage cost associated with it.

The process of sampling in primary data analysis consists of five steps. The first step is

choosing the target population where the best segment of the population is chosen that would

provide effective data in primary analysis (Etikan, Musa and Alkassim, 2016). The next step

is choosing the sampling frame in the research which will determine the participants within

the chosen population. The third step is choosing the sample size of the population. The four

step is choosing the sampling technique to be used based on the needs of the research and

finally, the last step is implementing the sampling method. There are basically two types of

sampling method, one is probabilistic sampling and another is non-probabilistic sampling.

Probabilistic sampling consists of methods such as simple random sampling, cluster

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10RESEARCH PROPOSAL

sampling, stratified sampling and systematic sampling (Emerson, 2015). On the other hand,

non-probabilistic sampling consists of methods such as quota sampling, purposive sampling,

volunteer sampling and haphazard sampling.

In this given study, the target population consist of the all the people working in small

and medium scale businesses in Australia. The sampling frame will consist of all the

accountants and managers working in small and medium scale businesses. The sample size

will consist of 100 participants for the quantitative analysis and 5 managers for qualitative

analysis. The study will choose simple random sampling as the method of the selecting

elements from the overall population for the quantitative data collection and the study will

use purposive sampling as the method of selecting managers for interviews.

3.6 Reliability and Validity

Reliability is the ability of the study to replicate the results using different datasets

using same instruments. The study will use Cronbach’s Alpha test to measure the reliability

of the data collected. In this method, the insignificant questions that do not have any

significance to this research will be eliminated. It will be measuring the internal consistency

of the data collected in the research (Noble and Smith, 2015). The study will use test rated

reliability to compare the results using different data sets for the qualitative analysis. Validity

measures the appropriateness of the different methods used in the research. In this research,

construct validity will be used to measure the appropriateness of the instruments used.

3.7 Ethical consideration

This study will maintain their ethical aspect of the research by providing adequate

information to the participants about the research. The privacy of the participants of the

research will maintained by keeping anonymity of the participants. The participants’ data will

be stored till the study is complete and will not be shared for any other purpose. The three-

cardinal sin of research, falsification, fabrication and plagiarism will be kept in mind. The

data collected from secondary sources would consist of proper citations, none of the data will

be falsified and fabricated to develop significant results in the research (Quinlan et al., 2019).

The researchers will be provided information regarding the purpose of conducting the

research and none of them would be forced to take part in the research. The research will

protect the interest of the respondents and none of them will be harmed. None of the

respondents will be forced to take part in the research and the questions will not use

discriminatory language which may offend the respondents in any way.

sampling, stratified sampling and systematic sampling (Emerson, 2015). On the other hand,

non-probabilistic sampling consists of methods such as quota sampling, purposive sampling,

volunteer sampling and haphazard sampling.

In this given study, the target population consist of the all the people working in small

and medium scale businesses in Australia. The sampling frame will consist of all the

accountants and managers working in small and medium scale businesses. The sample size

will consist of 100 participants for the quantitative analysis and 5 managers for qualitative

analysis. The study will choose simple random sampling as the method of the selecting

elements from the overall population for the quantitative data collection and the study will

use purposive sampling as the method of selecting managers for interviews.

3.6 Reliability and Validity

Reliability is the ability of the study to replicate the results using different datasets

using same instruments. The study will use Cronbach’s Alpha test to measure the reliability

of the data collected. In this method, the insignificant questions that do not have any

significance to this research will be eliminated. It will be measuring the internal consistency

of the data collected in the research (Noble and Smith, 2015). The study will use test rated

reliability to compare the results using different data sets for the qualitative analysis. Validity

measures the appropriateness of the different methods used in the research. In this research,

construct validity will be used to measure the appropriateness of the instruments used.

3.7 Ethical consideration

This study will maintain their ethical aspect of the research by providing adequate

information to the participants about the research. The privacy of the participants of the

research will maintained by keeping anonymity of the participants. The participants’ data will

be stored till the study is complete and will not be shared for any other purpose. The three-

cardinal sin of research, falsification, fabrication and plagiarism will be kept in mind. The

data collected from secondary sources would consist of proper citations, none of the data will

be falsified and fabricated to develop significant results in the research (Quinlan et al., 2019).

The researchers will be provided information regarding the purpose of conducting the

research and none of them would be forced to take part in the research. The research will

protect the interest of the respondents and none of them will be harmed. None of the

respondents will be forced to take part in the research and the questions will not use

discriminatory language which may offend the respondents in any way.

11RESEARCH PROPOSAL

4.0 References

Al-Aqrabi, H., Liu, L., Hill, R. and Antonopoulos, N., 2015. Cloud BI: Future of business

intelligence in the Cloud. Journal of Computer and System Sciences, 81(1), pp.85-96.

Armitage, H.M., Webb, A. and Glynn, J., 2016. The use of management accounting

techniques by small and medium‐sized enterprises: a field study of Canadian and Australian

practice. Accounting Perspectives, 15(1), pp.31-69.

Asiaei, K., Jusoh, R. and Bontis, N., 2018. Intellectual capital and performance measurement

systems in Iran. Journal of Intellectual Capital, 19(2), pp.294-320.

Brandas, C., Megan, O. and Didraga, O., 2015. Global perspectives on accounting

information systems: mobile and cloud approach. Procedia Economics and Finance, 20,

pp.88-93.

Cleary, P. and Quinn, M., 2016. Intellectual capital and business performance: An

exploratory study of the impact of cloud-based accounting and finance infrastructure. Journal

of Intellectual Capital, 17(2), pp.255-278.

Desai, S., Motamarri, T.R., Solanki, V. and Mishra, R., 2018, March. Cloud ERP for Small

and Medium Enterprises. In 2018 Second International Conference on Electronics,

Communication and Aerospace Technology (ICECA) (pp. 1-3). IEEE.

Dimitriu, O. and Matei, M., 2015. Cloud accounting: a new business model in a challenging

context. Procedia Economics and Finance, 32, pp.665-671.

Dimitriu, O. and Matei, M., 2015. Cloud accounting: a new business model in a challenging

context. Procedia Economics and Finance, 32, pp.665-671.

Emerson, R.W., 2015. Convenience sampling, random sampling, and snowball sampling:

How does sampling affect the validity of research?. Journal of Visual Impairment &

Blindness, 109(2), pp.164-168.

Etikan, I., Musa, S.A. and Alkassim, R.S., 2016. Comparison of convenience sampling and

purposive sampling. American Journal of Theoretical and Applied Statistics, 5(1), pp.1-4.

Fatima, H., 2016. Impact of E-Accounting in Today’s Scenario. International Journal of

Engineering and Management Research (IJEMR), 6(1), pp.260-264.

Flick, U., 2015. Introducing research methodology: A beginner's guide to doing a research

project. Sage.

Inggarsono, Y., Goman, M., Paembonan, A.P. and Asri, M., 2018. Literature Review on

Cloud Computing Technology Integration in Small and Medium Sized Enterprise’s

Accounting System. Available at SSRN 3298094.

Kennedy, A.M., 2017. Macro-Social Marketing Research: Philosophy, Methodology and

Methods. Journal of Macromarketing, 37(4), pp.347-355.

Khomonenko, A. and Gindin, S., 2016, April. Performance evaluation of cloud computing

accounting for expenses on information security. In Proceedings of the 18th Conference of

Open Innovations Association FRUCT (pp. 100-105). FRUCT Oy.

4.0 References

Al-Aqrabi, H., Liu, L., Hill, R. and Antonopoulos, N., 2015. Cloud BI: Future of business

intelligence in the Cloud. Journal of Computer and System Sciences, 81(1), pp.85-96.

Armitage, H.M., Webb, A. and Glynn, J., 2016. The use of management accounting

techniques by small and medium‐sized enterprises: a field study of Canadian and Australian

practice. Accounting Perspectives, 15(1), pp.31-69.

Asiaei, K., Jusoh, R. and Bontis, N., 2018. Intellectual capital and performance measurement

systems in Iran. Journal of Intellectual Capital, 19(2), pp.294-320.

Brandas, C., Megan, O. and Didraga, O., 2015. Global perspectives on accounting

information systems: mobile and cloud approach. Procedia Economics and Finance, 20,

pp.88-93.

Cleary, P. and Quinn, M., 2016. Intellectual capital and business performance: An

exploratory study of the impact of cloud-based accounting and finance infrastructure. Journal

of Intellectual Capital, 17(2), pp.255-278.

Desai, S., Motamarri, T.R., Solanki, V. and Mishra, R., 2018, March. Cloud ERP for Small

and Medium Enterprises. In 2018 Second International Conference on Electronics,

Communication and Aerospace Technology (ICECA) (pp. 1-3). IEEE.

Dimitriu, O. and Matei, M., 2015. Cloud accounting: a new business model in a challenging

context. Procedia Economics and Finance, 32, pp.665-671.

Dimitriu, O. and Matei, M., 2015. Cloud accounting: a new business model in a challenging

context. Procedia Economics and Finance, 32, pp.665-671.

Emerson, R.W., 2015. Convenience sampling, random sampling, and snowball sampling:

How does sampling affect the validity of research?. Journal of Visual Impairment &

Blindness, 109(2), pp.164-168.

Etikan, I., Musa, S.A. and Alkassim, R.S., 2016. Comparison of convenience sampling and

purposive sampling. American Journal of Theoretical and Applied Statistics, 5(1), pp.1-4.

Fatima, H., 2016. Impact of E-Accounting in Today’s Scenario. International Journal of

Engineering and Management Research (IJEMR), 6(1), pp.260-264.

Flick, U., 2015. Introducing research methodology: A beginner's guide to doing a research

project. Sage.

Inggarsono, Y., Goman, M., Paembonan, A.P. and Asri, M., 2018. Literature Review on

Cloud Computing Technology Integration in Small and Medium Sized Enterprise’s

Accounting System. Available at SSRN 3298094.

Kennedy, A.M., 2017. Macro-Social Marketing Research: Philosophy, Methodology and

Methods. Journal of Macromarketing, 37(4), pp.347-355.

Khomonenko, A. and Gindin, S., 2016, April. Performance evaluation of cloud computing

accounting for expenses on information security. In Proceedings of the 18th Conference of

Open Innovations Association FRUCT (pp. 100-105). FRUCT Oy.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.