Research in IT 20: Online Banking Impact on Cooperative Bank, India

VerifiedAdded on 2021/11/01

|22

|4996

|208

Report

AI Summary

This research paper investigates the impact of online facilities on the Cooperative Bank in Amritsar, India, comparing its performance to other commercial organizations. The study employs both qualitative and quantitative data analysis to determine the need for online facilities within the bank. The findings highlight the central role of online banking applications in financial institutions' operations and performance. The research also addresses ethical considerations and outlines the project's timeline and budget. The paper reviews literature on internet and mobile banking, discussing security issues and the evolution of online banking services. The methodology includes a survey research design, targeting commercial institutions and employing questionnaires for data collection. The study aims to determine the significance of online banking applications on the performance of commercial organizations and the impact of the absence of such facilities on customer retention at the Cooperative Bank.

Running head: RESEARCH IN IT 1

Research in IT

Name

Institution Affiliation

Research in IT

Name

Institution Affiliation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RESEARCH IN IT 2

Online Banking Application (Cooperative Bank Amritsar, India)

Abstract

The research paper discuss the need to implement the online facilities in Cooperative Bank in Amritsar

(India). Accordingly the primary goal of this paper is to investigate the impact of online facilities towards

the functioning of commercial organisations in comparison to Cooperative bank, Amritsar (India) which

does not have these online facilities in the modern era. Therefore, this paper uses qualitative and quantitative

data analysis approach to conduct the research. After carrying out the research it is found that online banking

applications play a central role in the operation and performance of financial institutions. It is also found that

ethical approval was also undertaken to decline issues associated with ethics. Additionally, it was realised

that the entire project required 254 days and a budget of approximately $10,000 to successfully complete the

research.

Keywords: mobile banking, Internet banking, commercial institutions.

Table of Contents

Online Banking Application (Cooperative Bank Amritsar, India)

Abstract

The research paper discuss the need to implement the online facilities in Cooperative Bank in Amritsar

(India). Accordingly the primary goal of this paper is to investigate the impact of online facilities towards

the functioning of commercial organisations in comparison to Cooperative bank, Amritsar (India) which

does not have these online facilities in the modern era. Therefore, this paper uses qualitative and quantitative

data analysis approach to conduct the research. After carrying out the research it is found that online banking

applications play a central role in the operation and performance of financial institutions. It is also found that

ethical approval was also undertaken to decline issues associated with ethics. Additionally, it was realised

that the entire project required 254 days and a budget of approximately $10,000 to successfully complete the

research.

Keywords: mobile banking, Internet banking, commercial institutions.

Table of Contents

RESEARCH IN IT 3

Introduction..................................................................................................................................................................... 4

Problem statement...........................................................................................................................................................5

Research questions..........................................................................................................................................................5

Research Question and Hypothesis..................................................................................................................................5

Literature review.............................................................................................................................................................6

Internet Banking..........................................................................................................................................................6

Mobile banking security issues....................................................................................................................................8

Methodology................................................................................................................................................................... 8

Introduction.................................................................................................................................................................8

Research design...........................................................................................................................................................9

Population target..........................................................................................................................................................9

Sampling frame...........................................................................................................................................................9

Sample and sampling tactic.......................................................................................................................................10

Research contribution................................................................................................................................................10

Ethics approval..........................................................................................................................................................11

Data collection Process..................................................................................................................................................11

Instruments for data collection..................................................................................................................................11

Data processing and analysis.....................................................................................................................................11

Evaluation metrics/Analysis......................................................................................................................................11

Timeline and costs.....................................................................................................................................................12

Timeline................................................................................................................................................................12

Budget cost............................................................................................................................................................14

References..................................................................................................................................................................... 15

Appendes....................................................................................................................................................................... 18

Appendix A: Ethics application screening questionnaire ..........................................................................................18

Appendix B: Online banking application...................................................................................................................22

Introduction..................................................................................................................................................................... 4

Problem statement...........................................................................................................................................................5

Research questions..........................................................................................................................................................5

Research Question and Hypothesis..................................................................................................................................5

Literature review.............................................................................................................................................................6

Internet Banking..........................................................................................................................................................6

Mobile banking security issues....................................................................................................................................8

Methodology................................................................................................................................................................... 8

Introduction.................................................................................................................................................................8

Research design...........................................................................................................................................................9

Population target..........................................................................................................................................................9

Sampling frame...........................................................................................................................................................9

Sample and sampling tactic.......................................................................................................................................10

Research contribution................................................................................................................................................10

Ethics approval..........................................................................................................................................................11

Data collection Process..................................................................................................................................................11

Instruments for data collection..................................................................................................................................11

Data processing and analysis.....................................................................................................................................11

Evaluation metrics/Analysis......................................................................................................................................11

Timeline and costs.....................................................................................................................................................12

Timeline................................................................................................................................................................12

Budget cost............................................................................................................................................................14

References..................................................................................................................................................................... 15

Appendes....................................................................................................................................................................... 18

Appendix A: Ethics application screening questionnaire ..........................................................................................18

Appendix B: Online banking application...................................................................................................................22

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RESEARCH IN IT 4

Introduction

Mobile banking is an invention which has progressively condensed itself in passive ways cutting

across different financial organisations as well as other economic sectors. In the 21st century mobile banking

had progressed from merely offering text messaging services to that of pseudo online banking which not

simply allow its customers to view their balances but also be in the position to set up a range of alerts (Beck,

Chen, Lin, & Song, 2016). In addition to that, online banking has made it possible for customers to transact

different activities like redeem loyalty coupons, money transfers, and deposit cheques using their cell phones

and instructing payroll based transactions. Indeed, the globe has revolutionised and it is increasingly getting

addicted to transacting businesses across the internet and through the cyber space in addition to the World

Wide Web (Frame, & White, 2014). Accordingly, in respect to internet commerce it has enlarged into

diverse forms of money as well as built on digital data which is offered by the private market actors

(Romānova, & Kudinska, 2016). Subsequently, these transaction have in one way or other replaced the state

authorised bank records and inspecting accounts as the accustomed payment means.

Technology has greatly revolutionised and it is playing a chief part in enhancing the principles of

service provision in the banking industry. Long are days gone when clients would queue in the banking halls

waiting to make payment for their utility bills, school fees as well as other monetary dealings (Sharma,

Govindaluri, & Al Balushi, 2015). Certainly, with the stride and advents taking place in the field of

information technology customers are no capable of doing all these transaction at the comfort of their houses

using their cell phones or by use of ATM cards (Jeucken, & Bouma, 2017). Moreover, as a result of the

tremendous development and growth of the mobile phone sector a majority of the financial organisations are

immensely venturing in the untapped opportunities. Therefore, financial institutions have partnered with the

mobile phone cycle providers to provide online banking services to their customers. Significantly, the ATM

banking is regarded as the primary as well as expansively adopted retail internet banking service in India.

Nevertheless, based on the recent statistics from Cooperative bank limited, Amritsar India indicate that the

adoption and use of mobile banking services has overshadowed the ATM banking in the last few years

Introduction

Mobile banking is an invention which has progressively condensed itself in passive ways cutting

across different financial organisations as well as other economic sectors. In the 21st century mobile banking

had progressed from merely offering text messaging services to that of pseudo online banking which not

simply allow its customers to view their balances but also be in the position to set up a range of alerts (Beck,

Chen, Lin, & Song, 2016). In addition to that, online banking has made it possible for customers to transact

different activities like redeem loyalty coupons, money transfers, and deposit cheques using their cell phones

and instructing payroll based transactions. Indeed, the globe has revolutionised and it is increasingly getting

addicted to transacting businesses across the internet and through the cyber space in addition to the World

Wide Web (Frame, & White, 2014). Accordingly, in respect to internet commerce it has enlarged into

diverse forms of money as well as built on digital data which is offered by the private market actors

(Romānova, & Kudinska, 2016). Subsequently, these transaction have in one way or other replaced the state

authorised bank records and inspecting accounts as the accustomed payment means.

Technology has greatly revolutionised and it is playing a chief part in enhancing the principles of

service provision in the banking industry. Long are days gone when clients would queue in the banking halls

waiting to make payment for their utility bills, school fees as well as other monetary dealings (Sharma,

Govindaluri, & Al Balushi, 2015). Certainly, with the stride and advents taking place in the field of

information technology customers are no capable of doing all these transaction at the comfort of their houses

using their cell phones or by use of ATM cards (Jeucken, & Bouma, 2017). Moreover, as a result of the

tremendous development and growth of the mobile phone sector a majority of the financial organisations are

immensely venturing in the untapped opportunities. Therefore, financial institutions have partnered with the

mobile phone cycle providers to provide online banking services to their customers. Significantly, the ATM

banking is regarded as the primary as well as expansively adopted retail internet banking service in India.

Nevertheless, based on the recent statistics from Cooperative bank limited, Amritsar India indicate that the

adoption and use of mobile banking services has overshadowed the ATM banking in the last few years

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RESEARCH IN IT 5

(Martins, Oliveira, & Popovič, 2014). Accordingly, the studies have shown that the major reason for the

rapid adoption and growth of the mobile banking system is that most of the low income earners currently

have access to cell phones (Shaikh, & Karjaluoto, 2015). The optimistic feature of mobile banking is that

cell phones are currently available even in the remote areas and at a cost effective price.

Problem statement

The major problem in this study is to determine the impact of online facilities towards the

functioning of commercial organisations in comparison to Cooperative bank, Amritsar (India) which does

not have these online facilities. The major assumption of many recent studies in operations enhancement as

well as set-ups learning has been that technology invention has a straight significance towards enhancing

performance (Al-Ajam, & Md Nor, 2015). Accordingly, premeditated management in the commercial sector

mandate that they should have efficient system in place to fight against capricious events which can endure

their operations and at the same time reduce the involved risks using technological inventions. Therefore,

only financial organisation that have the capacity to adapt the changing setting and adoption of novel

concepts as well as business approaches can survive (Safeena, Kammani, & Date, 2018).

Research questions

The study objectives include:

To determine the need to implement the online facilities in Cooperative Bank in Amritsar (India).

Research Question and Hypothesis

What is the need to implement the online facilities in Cooperative Bank in Amritsar, India?

H1: Online banking applications have a great significance towards the performance of commercial

organisations.

(Martins, Oliveira, & Popovič, 2014). Accordingly, the studies have shown that the major reason for the

rapid adoption and growth of the mobile banking system is that most of the low income earners currently

have access to cell phones (Shaikh, & Karjaluoto, 2015). The optimistic feature of mobile banking is that

cell phones are currently available even in the remote areas and at a cost effective price.

Problem statement

The major problem in this study is to determine the impact of online facilities towards the

functioning of commercial organisations in comparison to Cooperative bank, Amritsar (India) which does

not have these online facilities. The major assumption of many recent studies in operations enhancement as

well as set-ups learning has been that technology invention has a straight significance towards enhancing

performance (Al-Ajam, & Md Nor, 2015). Accordingly, premeditated management in the commercial sector

mandate that they should have efficient system in place to fight against capricious events which can endure

their operations and at the same time reduce the involved risks using technological inventions. Therefore,

only financial organisation that have the capacity to adapt the changing setting and adoption of novel

concepts as well as business approaches can survive (Safeena, Kammani, & Date, 2018).

Research questions

The study objectives include:

To determine the need to implement the online facilities in Cooperative Bank in Amritsar (India).

Research Question and Hypothesis

What is the need to implement the online facilities in Cooperative Bank in Amritsar, India?

H1: Online banking applications have a great significance towards the performance of commercial

organisations.

RESEARCH IN IT 6

H2: The absence of online banking facilities at Cooperative Bank, Amritsar India is cause for losing its

customers.

Literature review

This part intents to discover the in depth idea in relation to mobile and internet banking by reviewing

a range of past studies on the subject matter.

Internet Banking

As a result of massive innovation happening in the field of technology and communication it has led

to modern financial distribution channels growing rapidly both in figures and form like mobile banking,

ATMs, PC banking and Internet banking as the most recent (Hanafizadeh, Keating, & Khedmatgozar, 2014).

Following the dawn of the Interne, financial institutions have significantly accepted the net because of the

fast growth of the World Wide Web. At the same time in the commercial industry the internet was a signal

of a revolution in the banking distribution Arenas (Gaitán, Peral & Ramón 2015). Therefore, commercial

businesses especially banks massively invested in the development of the internet channels. Consequently,

internet banking has faced rapid development in most nations and has transformed the banking activities

(Shaikh, & Karjaluoto, 2015). It is inevitable that the internet banking has been continuously revolutionising

hence giving the present banking sector more and more offers and opportunities to serve their customers in a

better way (Yu, Balaji, & Khong, 2015). For instance, online banking started more than three decades ago

where customers were offered with application software programs which operate on personal computers

which can only be dialled into the bank through a telephone line, modem and run the programs remotely on

the user PC.

Conversely, the absence of internet as well as the expenses related with the usage of online banking

inhibited its growth. Nonetheless, towards the end of the 1990s the internet banking boomed as a result of

the internet explosion made users more comfortable with undertaking transactions across the web (Alalwan

et al, 2015). With the advent of the dotcom it became ostensible that the internet banking was not the

H2: The absence of online banking facilities at Cooperative Bank, Amritsar India is cause for losing its

customers.

Literature review

This part intents to discover the in depth idea in relation to mobile and internet banking by reviewing

a range of past studies on the subject matter.

Internet Banking

As a result of massive innovation happening in the field of technology and communication it has led

to modern financial distribution channels growing rapidly both in figures and form like mobile banking,

ATMs, PC banking and Internet banking as the most recent (Hanafizadeh, Keating, & Khedmatgozar, 2014).

Following the dawn of the Interne, financial institutions have significantly accepted the net because of the

fast growth of the World Wide Web. At the same time in the commercial industry the internet was a signal

of a revolution in the banking distribution Arenas (Gaitán, Peral & Ramón 2015). Therefore, commercial

businesses especially banks massively invested in the development of the internet channels. Consequently,

internet banking has faced rapid development in most nations and has transformed the banking activities

(Shaikh, & Karjaluoto, 2015). It is inevitable that the internet banking has been continuously revolutionising

hence giving the present banking sector more and more offers and opportunities to serve their customers in a

better way (Yu, Balaji, & Khong, 2015). For instance, online banking started more than three decades ago

where customers were offered with application software programs which operate on personal computers

which can only be dialled into the bank through a telephone line, modem and run the programs remotely on

the user PC.

Conversely, the absence of internet as well as the expenses related with the usage of online banking

inhibited its growth. Nonetheless, towards the end of the 1990s the internet banking boomed as a result of

the internet explosion made users more comfortable with undertaking transactions across the web (Alalwan

et al, 2015). With the advent of the dotcom it became ostensible that the internet banking was not the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RESEARCH IN IT 7

solution that financial institutions had anticipate to be. At the commencement of the millennium the

investment in internet banking development faced a relatively slowdown. However, the base of internet

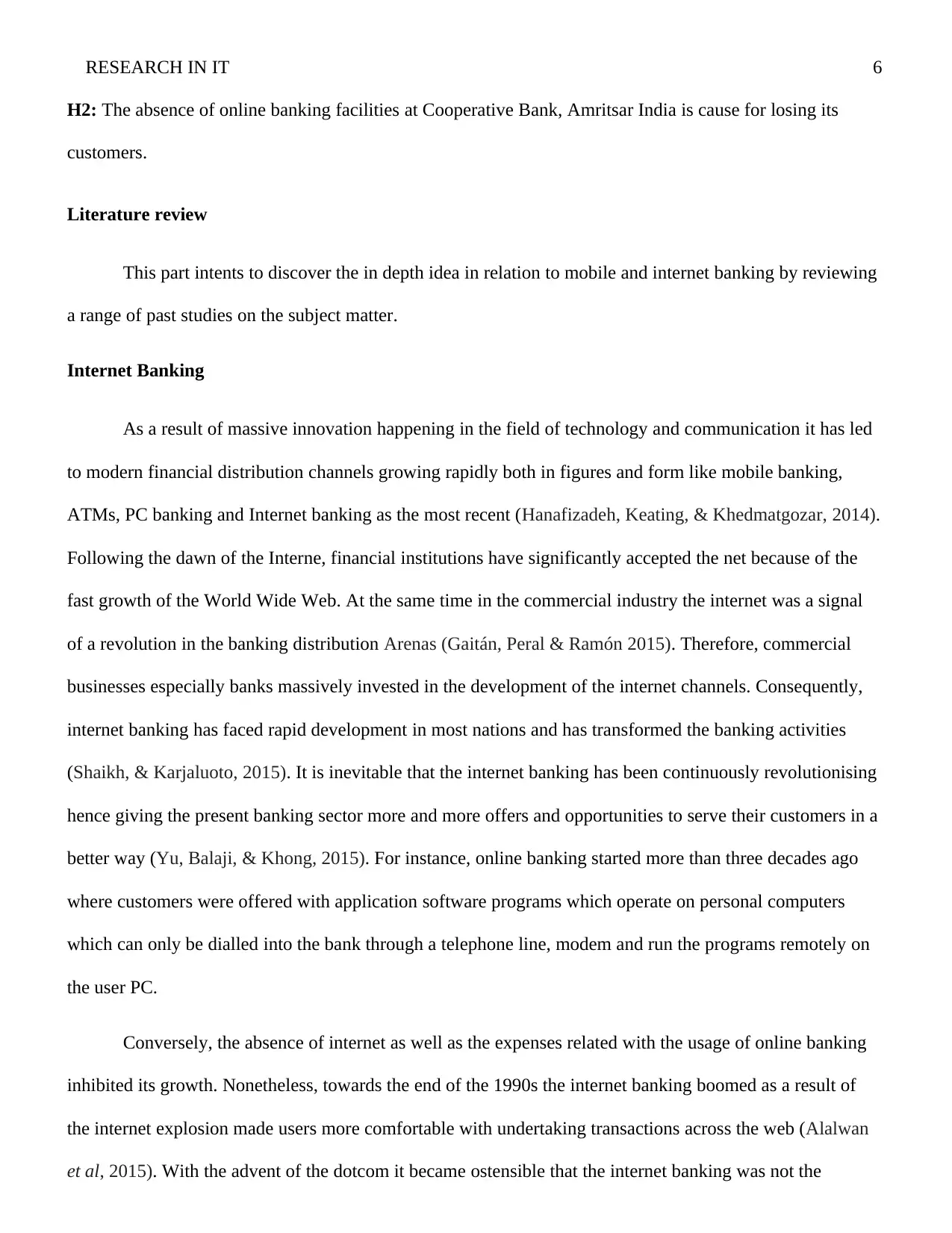

banking customers was increasing steadily. According to Forrester Research, besides branch Internet was a

dominant channel in 2007 as illustrated in figure 2.1 bellow.

Figure 1: Primary Retail Banking Channel 2007

When it comes to internet banking there has been always existence of a common confusion between

the terms internet banking, PC banking and online banking. The terms online banking and internet banking

are commonly used in the literature to refer to the same things. According to Oruç, & Tatar, (2017) online

banking is another terms which refers to internet banking and they share the same meaning. Online banking

or Internet banking refers to the services which allow customers to perform banking transactions with the

use of a computer which is connected to the internet. On the other hand, Takieddine, & Sun, (2015) claims

that online banking are systems which allow customers to financial institutions to gain access to their

accounts as well as the general information regarding its services and products via the bank’s website minus

the intervention of sending faxes, letters, telephones and email confirmations. Accordingly, internet banking

is the kind of service in which bank users are capable of making information requests and conducting most

of the traditional retail banking services like transferring money to dissimilar accounts and banking services

solution that financial institutions had anticipate to be. At the commencement of the millennium the

investment in internet banking development faced a relatively slowdown. However, the base of internet

banking customers was increasing steadily. According to Forrester Research, besides branch Internet was a

dominant channel in 2007 as illustrated in figure 2.1 bellow.

Figure 1: Primary Retail Banking Channel 2007

When it comes to internet banking there has been always existence of a common confusion between

the terms internet banking, PC banking and online banking. The terms online banking and internet banking

are commonly used in the literature to refer to the same things. According to Oruç, & Tatar, (2017) online

banking is another terms which refers to internet banking and they share the same meaning. Online banking

or Internet banking refers to the services which allow customers to perform banking transactions with the

use of a computer which is connected to the internet. On the other hand, Takieddine, & Sun, (2015) claims

that online banking are systems which allow customers to financial institutions to gain access to their

accounts as well as the general information regarding its services and products via the bank’s website minus

the intervention of sending faxes, letters, telephones and email confirmations. Accordingly, internet banking

is the kind of service in which bank users are capable of making information requests and conducting most

of the traditional retail banking services like transferring money to dissimilar accounts and banking services

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RESEARCH IN IT 8

like electronic online payments at the comfort of their houses (Khedmatgozar, & Shahnazi, 2018).

Therefore, online banking offers customers a universal connection from any region across the world and it is

universally accessible from any internet connected computer device.

Mobile banking security issues

According to Martins, Oliveira, & Popovič, (2014) commercial facilities offering banking services

using mobile devices are at the moment facing a number of hard choices regarding the right solution. These

challenges include balancing both short-term and long-term strategies for the mobile channel, the capacities

of banks end-to-end transactions monitoring as well as risk-scoring architecture, creation of security vendors

as well as their abilities (Alwan, & Al-Zubi, 2016). As a result of clients demanding for swift online

experiences particularly on mobile gadgets financial institutions are required to match the role out of

functionality to undertake risker practices with the capability to authenticate the applications, devices and

consumers in approached that are preferred by users (Boateng, Adam, Okoe, & Anning-Dorson, 2016).

Therefore, fraud controls are matched to risk of particular clients actions which dependent on the integrity,

authentication and secrecy of the consumer’s identity and credentials. Similarly, other essential aspects

impacting the strategy used in mobile security and its architecture come up during the overlapping, complex,

interrelated, and dynamic environment involving mobile platforms and services, banking, digital and online

identity service providers and payment providers.

Methodology

Introduction

In the case of this part it deals with data gathering, processing, and analysis approaches. Accordingly,

research methodology help to describe the technical processes in a way that is suitable for the audience

(Taylor, Bogdan, & DeVault, 2015). Certainly, research methodology realise this by addressing the sample

designs employed in the research, the gathered data as well as the fieldwork undertaken for the study and

like electronic online payments at the comfort of their houses (Khedmatgozar, & Shahnazi, 2018).

Therefore, online banking offers customers a universal connection from any region across the world and it is

universally accessible from any internet connected computer device.

Mobile banking security issues

According to Martins, Oliveira, & Popovič, (2014) commercial facilities offering banking services

using mobile devices are at the moment facing a number of hard choices regarding the right solution. These

challenges include balancing both short-term and long-term strategies for the mobile channel, the capacities

of banks end-to-end transactions monitoring as well as risk-scoring architecture, creation of security vendors

as well as their abilities (Alwan, & Al-Zubi, 2016). As a result of clients demanding for swift online

experiences particularly on mobile gadgets financial institutions are required to match the role out of

functionality to undertake risker practices with the capability to authenticate the applications, devices and

consumers in approached that are preferred by users (Boateng, Adam, Okoe, & Anning-Dorson, 2016).

Therefore, fraud controls are matched to risk of particular clients actions which dependent on the integrity,

authentication and secrecy of the consumer’s identity and credentials. Similarly, other essential aspects

impacting the strategy used in mobile security and its architecture come up during the overlapping, complex,

interrelated, and dynamic environment involving mobile platforms and services, banking, digital and online

identity service providers and payment providers.

Methodology

Introduction

In the case of this part it deals with data gathering, processing, and analysis approaches. Accordingly,

research methodology help to describe the technical processes in a way that is suitable for the audience

(Taylor, Bogdan, & DeVault, 2015). Certainly, research methodology realise this by addressing the sample

designs employed in the research, the gathered data as well as the fieldwork undertaken for the study and

RESEARCH IN IT 9

analysis on the gathered data. Simonsohn, Nelson, & Simmons, (2017) asserts that research methodology is

an overall standard that directs the researcher.

Research design

According to Merriam, & Tisdell, (2015) the target of this part is to set out a description of and the

justification for the selected methodology and research approaches. Accordingly, research design is the

general plan for obtaining responses to the questions under research as well as for managing various

challenges experienced at the time of the study process. Therefore selecting the suitable research design is

based on the research questions, sample of participants, data gathering method and analysis method. In this

study it employed an expressive survey research design. According to Glesne, (2015) the scholar define

expressive survey research design as a sequential study approach for gathering data from representative

sample population with the help of instruments that consist of observations, closed-ended or open-ended

questions as well as interviews. Indeed, this is one of the common and widely used non-experimental study

designs for collecting massive survey data from representative sample of participants

Population target

Population is defined a finite or infinite group of individual components. The population target used

for this study was divided into two levels. The first population involved commercial institutions in which the

study targeted commercial organizations in India. The second target group population comprised top

management leaders of commercial financial institutions. The primary reason for selecting the top

management employees was because they have the responsibility for performance of their particular banks

(Quinlan, Babin, Carr, & Griffin, 2019). On the same note they have greater appreciation on the manner in

which innovation impact financial performance. These employees also have a responsibility of managing

performance of their respective departmental budgets and action plans.

Sampling frame

analysis on the gathered data. Simonsohn, Nelson, & Simmons, (2017) asserts that research methodology is

an overall standard that directs the researcher.

Research design

According to Merriam, & Tisdell, (2015) the target of this part is to set out a description of and the

justification for the selected methodology and research approaches. Accordingly, research design is the

general plan for obtaining responses to the questions under research as well as for managing various

challenges experienced at the time of the study process. Therefore selecting the suitable research design is

based on the research questions, sample of participants, data gathering method and analysis method. In this

study it employed an expressive survey research design. According to Glesne, (2015) the scholar define

expressive survey research design as a sequential study approach for gathering data from representative

sample population with the help of instruments that consist of observations, closed-ended or open-ended

questions as well as interviews. Indeed, this is one of the common and widely used non-experimental study

designs for collecting massive survey data from representative sample of participants

Population target

Population is defined a finite or infinite group of individual components. The population target used

for this study was divided into two levels. The first population involved commercial institutions in which the

study targeted commercial organizations in India. The second target group population comprised top

management leaders of commercial financial institutions. The primary reason for selecting the top

management employees was because they have the responsibility for performance of their particular banks

(Quinlan, Babin, Carr, & Griffin, 2019). On the same note they have greater appreciation on the manner in

which innovation impact financial performance. These employees also have a responsibility of managing

performance of their respective departmental budgets and action plans.

Sampling frame

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RESEARCH IN IT 10

The sampling frame for this researched comprised all the licensed financial institution in India. Therefore,

the focus of this research was based on the management of the team. Describe a sampling frame as a list of

the target people in which a sample is chosen in which the expressive survey designs the sampling frame

normally comprises a finite population.

Sample and sampling tactic

According to a sample in a survey study refers to a subset of features that are drawn from the entire

population. As a result, prior to data collection it is significant to identify the sample size specifications of a

study. Accordingly, this research made use of a purposive process to determine the sample units.

Simonsohn, Nelson, & Simmons, (2017) argue that purposive sample is a judgemental sample which is a

non-probability. The primary goal of a purposive sample is to generate a sample which is rationally assumed

as the representative of the entire populace which is completed by applying the expert understanding of the

people to choose in a non-random way a sample of components which is a representation of the cross-

section of the population. Therefore, the sample unit used were five commercial organisations. The selected

banks were picked because they have extensively invested in different inventions built on information

existing in their yearly reports. Also, these banks are responsible for a relatively big portion of

approximately 70% of the banking industry in India in terms of market share index of the net resources,

stakeholders’ money, number of deposits, and number of loan accounts as well as deposit accounts.

Research contribution

Accordingly, this research is significant in the sense that it allow the commercial sector to strive to

leverage on technology to develop the financial service industry to improve access to financial services. The

key propeller to such change in the commercial industry is invention and information technology. Based on

the findings, the commercial sector has the capacity to appreciate the areas of innovation to uplift the

banking industry.

The sampling frame for this researched comprised all the licensed financial institution in India. Therefore,

the focus of this research was based on the management of the team. Describe a sampling frame as a list of

the target people in which a sample is chosen in which the expressive survey designs the sampling frame

normally comprises a finite population.

Sample and sampling tactic

According to a sample in a survey study refers to a subset of features that are drawn from the entire

population. As a result, prior to data collection it is significant to identify the sample size specifications of a

study. Accordingly, this research made use of a purposive process to determine the sample units.

Simonsohn, Nelson, & Simmons, (2017) argue that purposive sample is a judgemental sample which is a

non-probability. The primary goal of a purposive sample is to generate a sample which is rationally assumed

as the representative of the entire populace which is completed by applying the expert understanding of the

people to choose in a non-random way a sample of components which is a representation of the cross-

section of the population. Therefore, the sample unit used were five commercial organisations. The selected

banks were picked because they have extensively invested in different inventions built on information

existing in their yearly reports. Also, these banks are responsible for a relatively big portion of

approximately 70% of the banking industry in India in terms of market share index of the net resources,

stakeholders’ money, number of deposits, and number of loan accounts as well as deposit accounts.

Research contribution

Accordingly, this research is significant in the sense that it allow the commercial sector to strive to

leverage on technology to develop the financial service industry to improve access to financial services. The

key propeller to such change in the commercial industry is invention and information technology. Based on

the findings, the commercial sector has the capacity to appreciate the areas of innovation to uplift the

banking industry.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RESEARCH IN IT 11

Ethics approval

The study reviews past research undertaken on the research topic and online journals. Therefore, with

the aid of such research types there is high possibility that the banking industry within Amritsar and

particularly Cooperative Bank need to embrace online application in their customer service delivery.

Certainly, to be able to collect this type of data and information, it is necessary for the research team to get

permission from the ethics committee Merriam, & Tisdell, (2015). Accordingly, this is significant as it will

help them not to experiencing finance issues while undertaking the research.

Data collection Process

Instruments for data collection

The researcher made use of questionnaires to get qualitative data for analysis. The questionnaires

consisted of both open-ended and closed-ended questions to produce the qualitative data (Glesne, 2015). The

investigator used questionnaires as they are cost effective, have the capacity to cover a huge geographical

region and free from the interviewer’s bias. Additionally, responses are in respondent’s words and enough

time is provided which enable for well-thought out responses. Additionally the researcher used qualitative

measure to analyse the collected data. The qualitative data was used to measure clients’ level of satisfaction,

services offered, challenges experienced to measure the semantic contents of the response. The qualitative

data was analysed using statistical data analysis.

Data processing and analysis

Generally, the amount of data gathered in this study was huge because the research questions cannot

be responded to using simple read-through of numeric information. Thus, the data required to be processed

and analysed in a systematic and coherent manner.

Evaluation metrics/Analysis

Ethics approval

The study reviews past research undertaken on the research topic and online journals. Therefore, with

the aid of such research types there is high possibility that the banking industry within Amritsar and

particularly Cooperative Bank need to embrace online application in their customer service delivery.

Certainly, to be able to collect this type of data and information, it is necessary for the research team to get

permission from the ethics committee Merriam, & Tisdell, (2015). Accordingly, this is significant as it will

help them not to experiencing finance issues while undertaking the research.

Data collection Process

Instruments for data collection

The researcher made use of questionnaires to get qualitative data for analysis. The questionnaires

consisted of both open-ended and closed-ended questions to produce the qualitative data (Glesne, 2015). The

investigator used questionnaires as they are cost effective, have the capacity to cover a huge geographical

region and free from the interviewer’s bias. Additionally, responses are in respondent’s words and enough

time is provided which enable for well-thought out responses. Additionally the researcher used qualitative

measure to analyse the collected data. The qualitative data was used to measure clients’ level of satisfaction,

services offered, challenges experienced to measure the semantic contents of the response. The qualitative

data was analysed using statistical data analysis.

Data processing and analysis

Generally, the amount of data gathered in this study was huge because the research questions cannot

be responded to using simple read-through of numeric information. Thus, the data required to be processed

and analysed in a systematic and coherent manner.

Evaluation metrics/Analysis

RESEARCH IN IT 12

The collected data was evaluated on the number of responses given on every question and the highest

responses with a similar argument and response was taken as the most probable answer to the question.

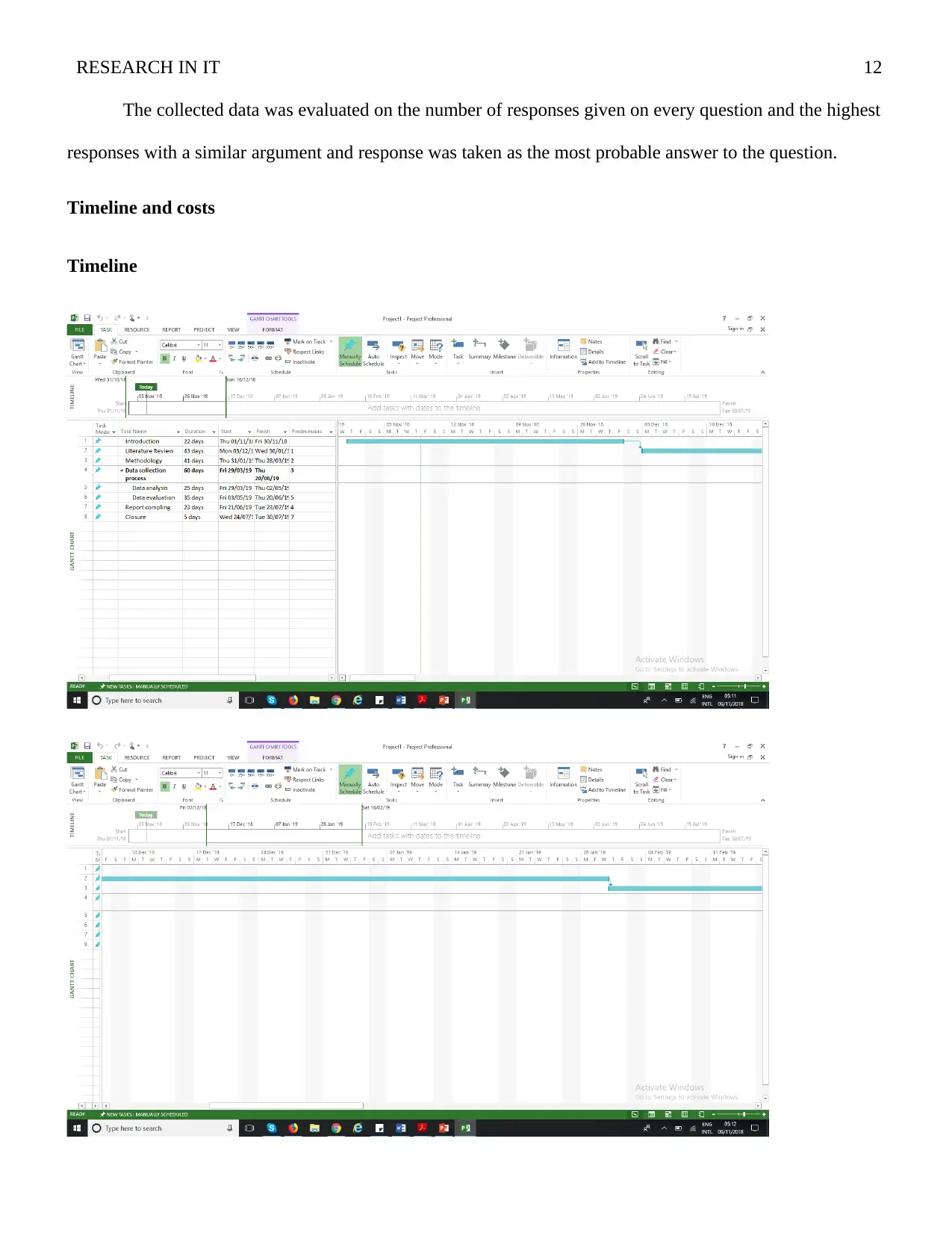

Timeline and costs

Timeline

The collected data was evaluated on the number of responses given on every question and the highest

responses with a similar argument and response was taken as the most probable answer to the question.

Timeline and costs

Timeline

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.