Detailed Report: Preparation and Analysis of an Operational Budget

VerifiedAdded on 2020/07/23

|17

|2872

|45

Report

AI Summary

This report provides a comprehensive overview of operational budgeting, encompassing various assessment activities. It begins with an introduction to budgets, different types (operating, production, sales, master), and budgetary control principles. The report emphasizes the importance of communicating budget planning and includes detailed examples of an annual budget for 2016, a monthly profit and loss estimate, purchase budgets, and worksheet examples. Key elements such as budget variance analysis, forecasting techniques, and double-entry accounting are discussed. The report further delves into the preparation of budget objectives, sales and production budgets, cash budgets, and budgeted income statements and balance sheets. Stakeholder consultation, key performance indicators (KPIs), and budgetary reports are also covered. The significance of preparing budgets and their role in creating goodwill are highlighted, concluding with references.

Prepare Operational Budget

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Assessment Activity 1 .....................................................................................................................1

TASK 1.1 ........................................................................................................................................1

What is budget........................................................................................................................1

Different types of budgets......................................................................................................1

Budgetary control principles..................................................................................................1

TASK 1.2 ........................................................................................................................................2

Importance of communicating budget planning to peers.......................................................2

TASK 1.3 ........................................................................................................................................2

Preparation of annual budget for 2016...................................................................................2

TASK 1.4.........................................................................................................................................2

Monthly budgeted Profit and Loss estimate for 2015............................................................2

TASK 1.5.........................................................................................................................................3

Purchase budget......................................................................................................................3

TASK 1.6.........................................................................................................................................3

Worksheet...............................................................................................................................3

TASK 1.7 ........................................................................................................................................4

TASK 1.8.........................................................................................................................................5

Budget variance......................................................................................................................5

TASK 1.9.........................................................................................................................................6

Discuss forecasting techniques...............................................................................................6

Double-entry accounting........................................................................................................7

Variance analysis....................................................................................................................7

Assessment Activity 2......................................................................................................................7

TASK 2.1.........................................................................................................................................7

Preparation of budget objectives............................................................................................7

TASK 2.2.........................................................................................................................................7

Sales budget............................................................................................................................7

TASK 2.3.........................................................................................................................................8

INTRODUCTION...........................................................................................................................1

Assessment Activity 1 .....................................................................................................................1

TASK 1.1 ........................................................................................................................................1

What is budget........................................................................................................................1

Different types of budgets......................................................................................................1

Budgetary control principles..................................................................................................1

TASK 1.2 ........................................................................................................................................2

Importance of communicating budget planning to peers.......................................................2

TASK 1.3 ........................................................................................................................................2

Preparation of annual budget for 2016...................................................................................2

TASK 1.4.........................................................................................................................................2

Monthly budgeted Profit and Loss estimate for 2015............................................................2

TASK 1.5.........................................................................................................................................3

Purchase budget......................................................................................................................3

TASK 1.6.........................................................................................................................................3

Worksheet...............................................................................................................................3

TASK 1.7 ........................................................................................................................................4

TASK 1.8.........................................................................................................................................5

Budget variance......................................................................................................................5

TASK 1.9.........................................................................................................................................6

Discuss forecasting techniques...............................................................................................6

Double-entry accounting........................................................................................................7

Variance analysis....................................................................................................................7

Assessment Activity 2......................................................................................................................7

TASK 2.1.........................................................................................................................................7

Preparation of budget objectives............................................................................................7

TASK 2.2.........................................................................................................................................7

Sales budget............................................................................................................................7

TASK 2.3.........................................................................................................................................8

Production budget...................................................................................................................8

TASK 2.4.........................................................................................................................................8

Cash budget............................................................................................................................8

TASK 2.5.........................................................................................................................................9

Budgeted income statement....................................................................................................9

TASK 2.6.......................................................................................................................................11

Budgeted balance sheet........................................................................................................11

TASK 2.7.......................................................................................................................................12

Stakeholders and consultation methods................................................................................12

TASK 2.8.......................................................................................................................................13

KPI (Key Performance Indicators).......................................................................................13

TASK 2.9.......................................................................................................................................13

Budgetary reports.................................................................................................................13

Assessment Activity 3....................................................................................................................13

Budget Objectives................................................................................................................13

Significance of preparing budgets........................................................................................13

Budgets creates goodwill......................................................................................................14

Convince stakeholders before budget implementation.........................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................14

TASK 2.4.........................................................................................................................................8

Cash budget............................................................................................................................8

TASK 2.5.........................................................................................................................................9

Budgeted income statement....................................................................................................9

TASK 2.6.......................................................................................................................................11

Budgeted balance sheet........................................................................................................11

TASK 2.7.......................................................................................................................................12

Stakeholders and consultation methods................................................................................12

TASK 2.8.......................................................................................................................................13

KPI (Key Performance Indicators).......................................................................................13

TASK 2.9.......................................................................................................................................13

Budgetary reports.................................................................................................................13

Assessment Activity 3....................................................................................................................13

Budget Objectives................................................................................................................13

Significance of preparing budgets........................................................................................13

Budgets creates goodwill......................................................................................................14

Convince stakeholders before budget implementation.........................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Operational budgets are crucial for business to prepare so that forecasting about future

can be made easily. The present report deals with various assessments engaged in preparation of

operational budgets so that meaningful results may be obtained.

Assessment Activity 1

TASK 1.1

What is budget

Budget is a document containing financial plan of company for the coming period

including anticipating sales and estimated expenses.

Different types of budgets

Operating budget

This budget is prepared for estimating income and expenses for the coming year. All

costs should be forecasted to prepare budget (Pal, 2018 ).

Production budget

Production budget is prepared for maintaining level of production so that adequate units

may be manufactured with much ease having estimation of sales and inventory of finished

goods.

Sales budget

Sales budget is prepared to analyse expected units to be sold in a particular period.

Master budget

It is complete segregation of all the budgets so that overall picture of financial health may

be assessed.

Budgetary control principles

Budgetary control principles are used to record actual performance and then compare the

same with planned performance so that variances can be easily found out. Corrective action can

be taken to remove variances.

1

Operational budgets are crucial for business to prepare so that forecasting about future

can be made easily. The present report deals with various assessments engaged in preparation of

operational budgets so that meaningful results may be obtained.

Assessment Activity 1

TASK 1.1

What is budget

Budget is a document containing financial plan of company for the coming period

including anticipating sales and estimated expenses.

Different types of budgets

Operating budget

This budget is prepared for estimating income and expenses for the coming year. All

costs should be forecasted to prepare budget (Pal, 2018 ).

Production budget

Production budget is prepared for maintaining level of production so that adequate units

may be manufactured with much ease having estimation of sales and inventory of finished

goods.

Sales budget

Sales budget is prepared to analyse expected units to be sold in a particular period.

Master budget

It is complete segregation of all the budgets so that overall picture of financial health may

be assessed.

Budgetary control principles

Budgetary control principles are used to record actual performance and then compare the

same with planned performance so that variances can be easily found out. Corrective action can

be taken to remove variances.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

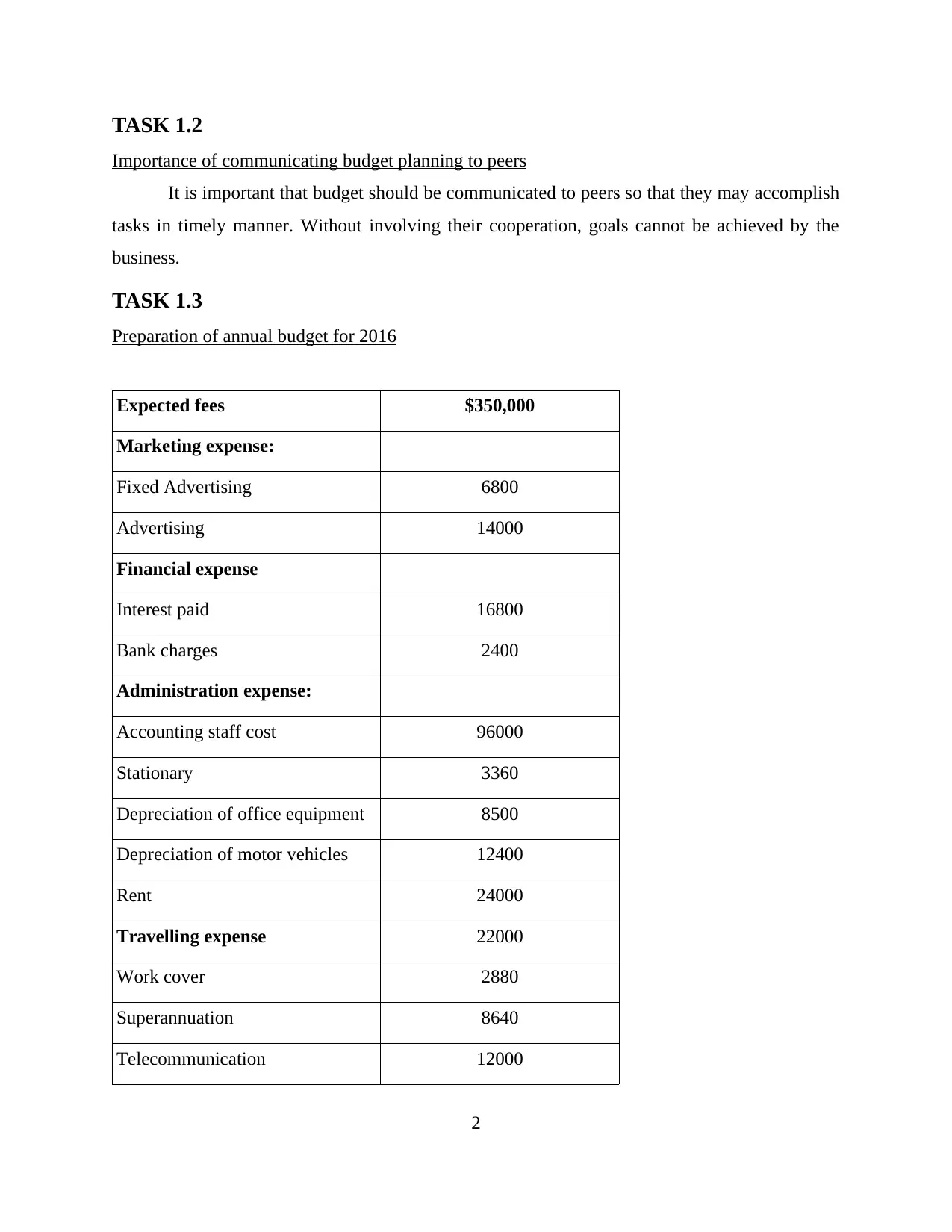

TASK 1.2

Importance of communicating budget planning to peers

It is important that budget should be communicated to peers so that they may accomplish

tasks in timely manner. Without involving their cooperation, goals cannot be achieved by the

business.

TASK 1.3

Preparation of annual budget for 2016

Expected fees $350,000

Marketing expense:

Fixed Advertising 6800

Advertising 14000

Financial expense

Interest paid 16800

Bank charges 2400

Administration expense:

Accounting staff cost 96000

Stationary 3360

Depreciation of office equipment 8500

Depreciation of motor vehicles 12400

Rent 24000

Travelling expense 22000

Work cover 2880

Superannuation 8640

Telecommunication 12000

2

Importance of communicating budget planning to peers

It is important that budget should be communicated to peers so that they may accomplish

tasks in timely manner. Without involving their cooperation, goals cannot be achieved by the

business.

TASK 1.3

Preparation of annual budget for 2016

Expected fees $350,000

Marketing expense:

Fixed Advertising 6800

Advertising 14000

Financial expense

Interest paid 16800

Bank charges 2400

Administration expense:

Accounting staff cost 96000

Stationary 3360

Depreciation of office equipment 8500

Depreciation of motor vehicles 12400

Rent 24000

Travelling expense 22000

Work cover 2880

Superannuation 8640

Telecommunication 12000

2

Total expenses 229780

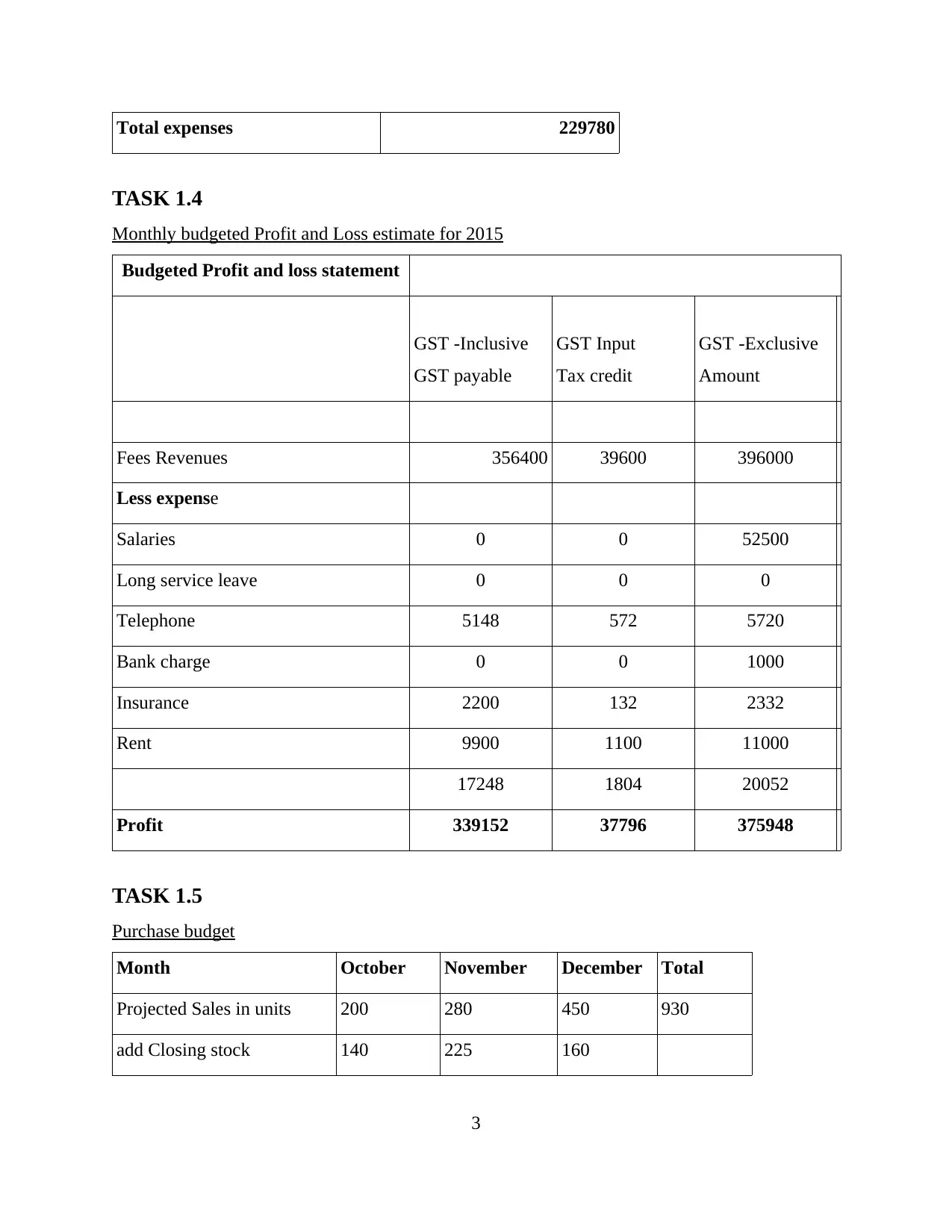

TASK 1.4

Monthly budgeted Profit and Loss estimate for 2015

Budgeted Profit and loss statement

GST -Inclusive

GST payable

GST Input

Tax credit

GST -Exclusive

Amount

Fees Revenues 356400 39600 396000

Less expense

Salaries 0 0 52500

Long service leave 0 0 0

Telephone 5148 572 5720

Bank charge 0 0 1000

Insurance 2200 132 2332

Rent 9900 1100 11000

17248 1804 20052

Profit 339152 37796 375948

TASK 1.5

Purchase budget

Month October November December Total

Projected Sales in units 200 280 450 930

add Closing stock 140 225 160

3

TASK 1.4

Monthly budgeted Profit and Loss estimate for 2015

Budgeted Profit and loss statement

GST -Inclusive

GST payable

GST Input

Tax credit

GST -Exclusive

Amount

Fees Revenues 356400 39600 396000

Less expense

Salaries 0 0 52500

Long service leave 0 0 0

Telephone 5148 572 5720

Bank charge 0 0 1000

Insurance 2200 132 2332

Rent 9900 1100 11000

17248 1804 20052

Profit 339152 37796 375948

TASK 1.5

Purchase budget

Month October November December Total

Projected Sales in units 200 280 450 930

add Closing stock 140 225 160

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

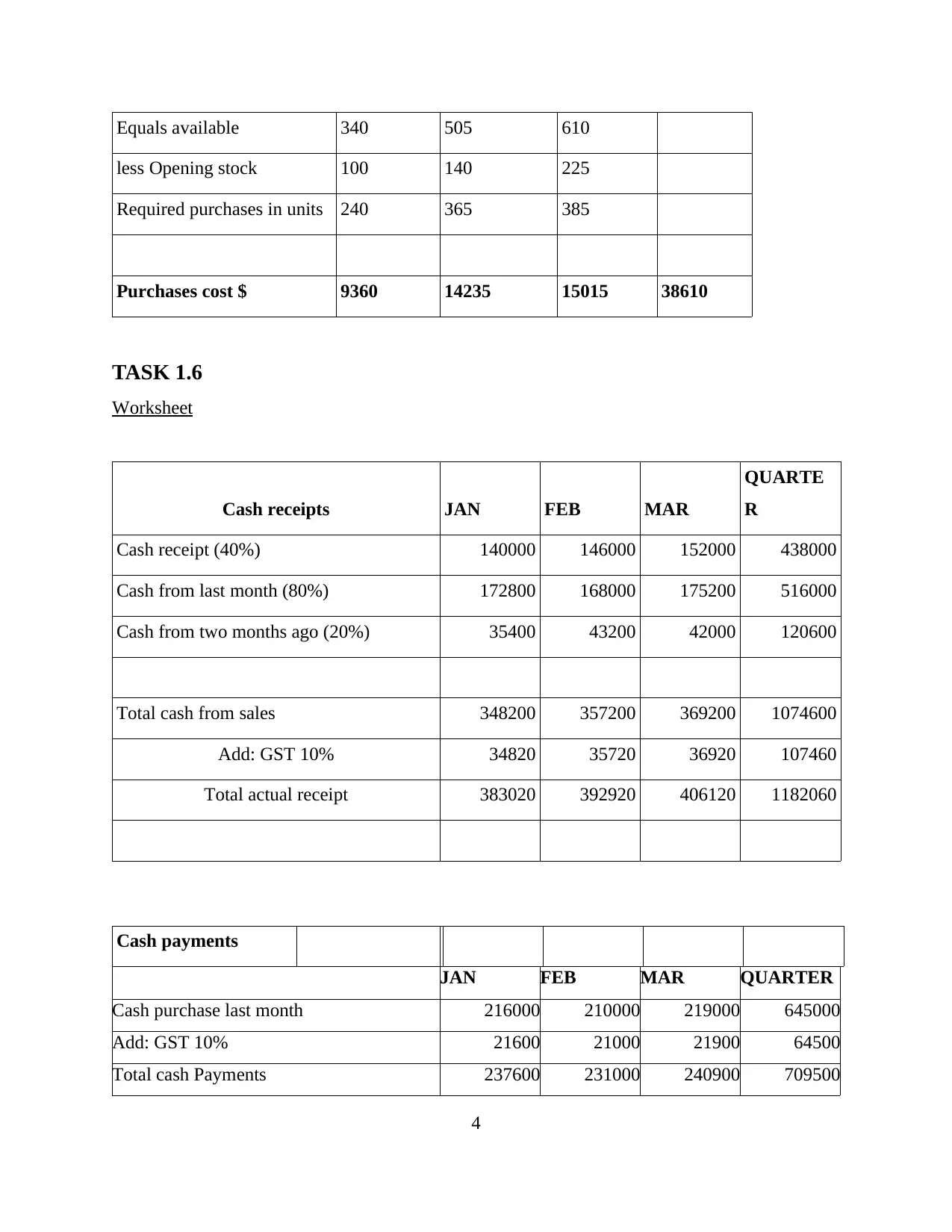

Equals available 340 505 610

less Opening stock 100 140 225

Required purchases in units 240 365 385

Purchases cost $ 9360 14235 15015 38610

TASK 1.6

Worksheet

Cash receipts JAN FEB MAR

QUARTE

R

Cash receipt (40%) 140000 146000 152000 438000

Cash from last month (80%) 172800 168000 175200 516000

Cash from two months ago (20%) 35400 43200 42000 120600

Total cash from sales 348200 357200 369200 1074600

Add: GST 10% 34820 35720 36920 107460

Total actual receipt 383020 392920 406120 1182060

Cash payments

JAN FEB MAR QUARTER

Cash purchase last month 216000 210000 219000 645000

Add: GST 10% 21600 21000 21900 64500

Total cash Payments 237600 231000 240900 709500

4

less Opening stock 100 140 225

Required purchases in units 240 365 385

Purchases cost $ 9360 14235 15015 38610

TASK 1.6

Worksheet

Cash receipts JAN FEB MAR

QUARTE

R

Cash receipt (40%) 140000 146000 152000 438000

Cash from last month (80%) 172800 168000 175200 516000

Cash from two months ago (20%) 35400 43200 42000 120600

Total cash from sales 348200 357200 369200 1074600

Add: GST 10% 34820 35720 36920 107460

Total actual receipt 383020 392920 406120 1182060

Cash payments

JAN FEB MAR QUARTER

Cash purchase last month 216000 210000 219000 645000

Add: GST 10% 21600 21000 21900 64500

Total cash Payments 237600 231000 240900 709500

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

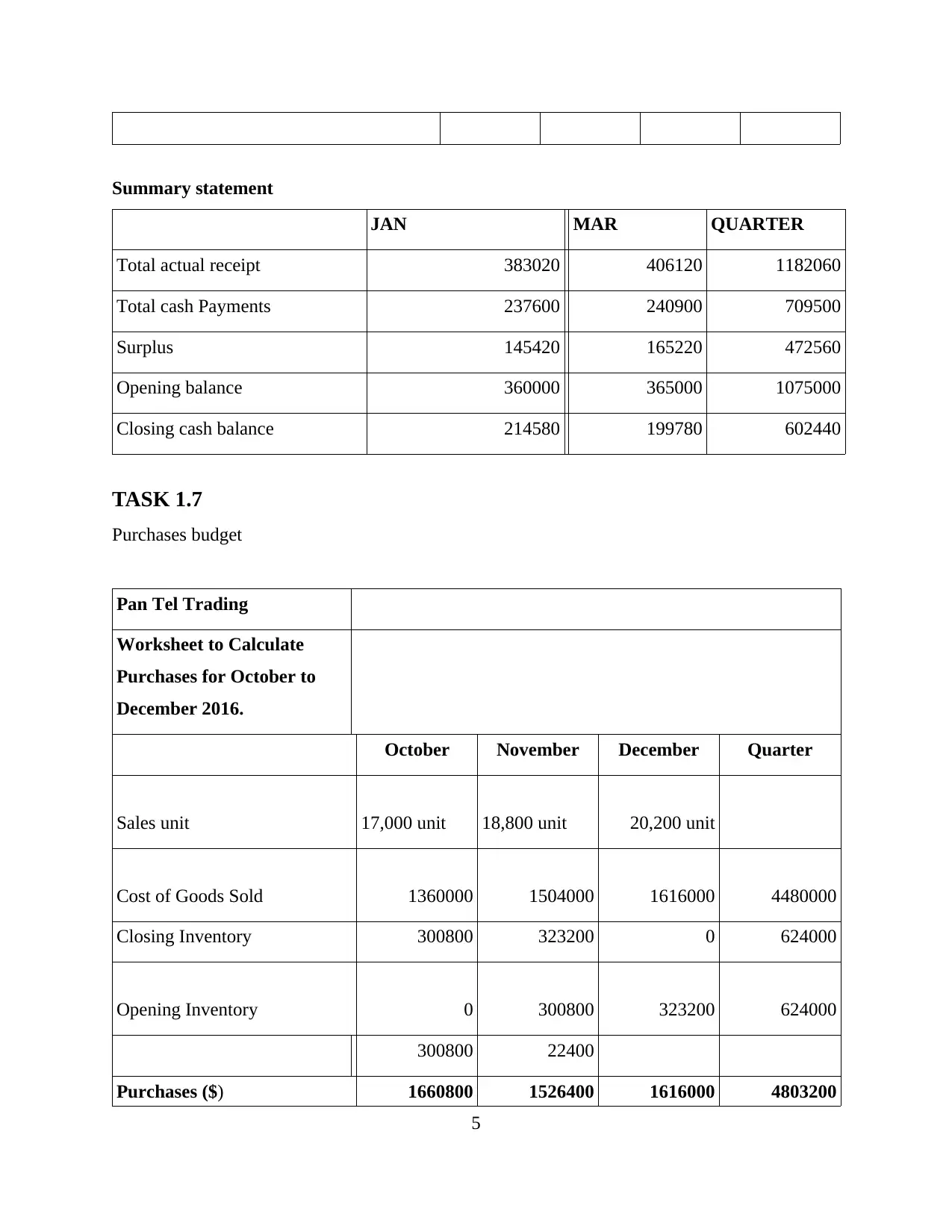

Summary statement

JAN MAR QUARTER

Total actual receipt 383020 406120 1182060

Total cash Payments 237600 240900 709500

Surplus 145420 165220 472560

Opening balance 360000 365000 1075000

Closing cash balance 214580 199780 602440

TASK 1.7

Purchases budget

Pan Tel Trading

Worksheet to Calculate

Purchases for October to

December 2016.

October November December Quarter

Sales unit 17,000 unit 18,800 unit 20,200 unit

Cost of Goods Sold 1360000 1504000 1616000 4480000

Closing Inventory 300800 323200 0 624000

Opening Inventory 0 300800 323200 624000

300800 22400

Purchases ($) 1660800 1526400 1616000 4803200

5

JAN MAR QUARTER

Total actual receipt 383020 406120 1182060

Total cash Payments 237600 240900 709500

Surplus 145420 165220 472560

Opening balance 360000 365000 1075000

Closing cash balance 214580 199780 602440

TASK 1.7

Purchases budget

Pan Tel Trading

Worksheet to Calculate

Purchases for October to

December 2016.

October November December Quarter

Sales unit 17,000 unit 18,800 unit 20,200 unit

Cost of Goods Sold 1360000 1504000 1616000 4480000

Closing Inventory 300800 323200 0 624000

Opening Inventory 0 300800 323200 624000

300800 22400

Purchases ($) 1660800 1526400 1616000 4803200

5

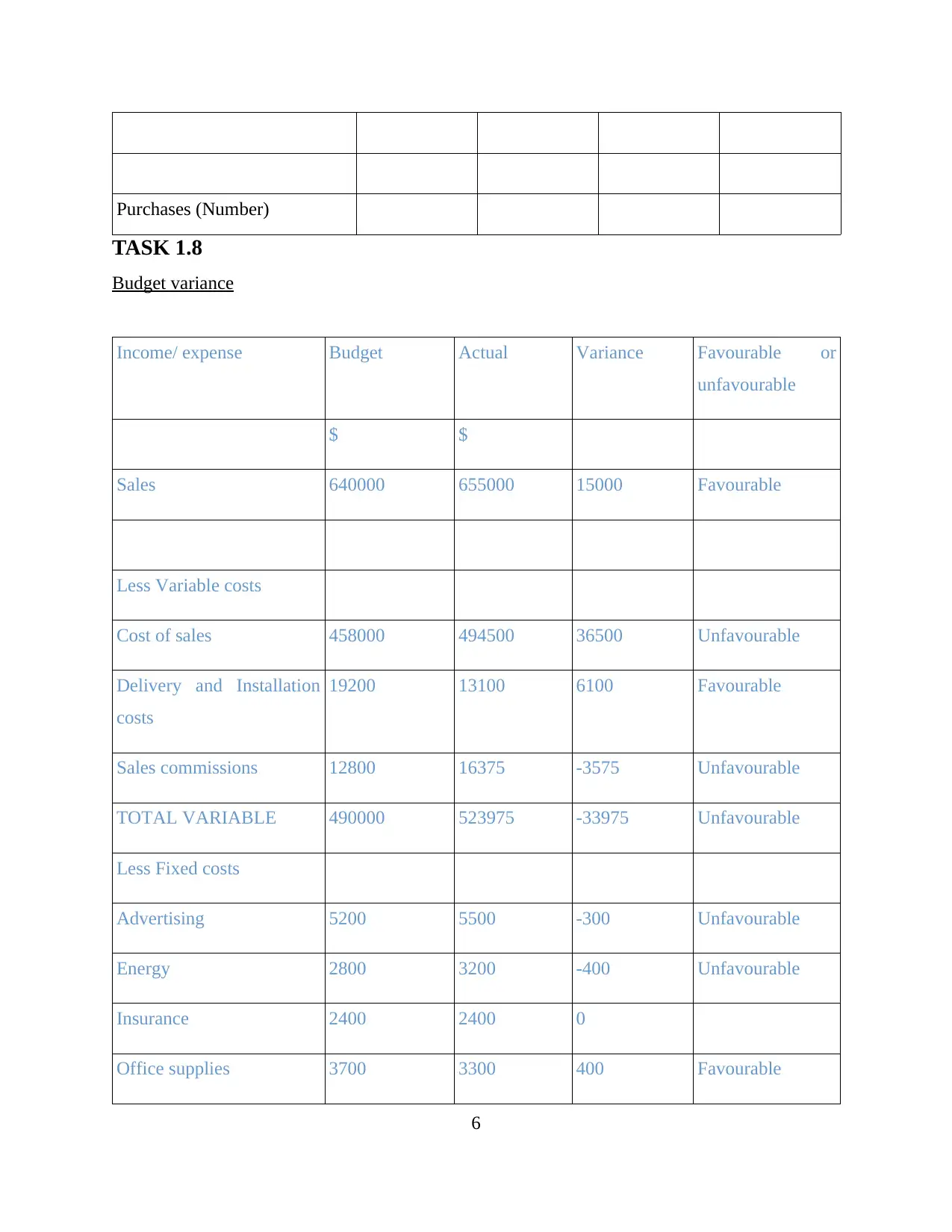

Purchases (Number)

TASK 1.8

Budget variance

Income/ expense Budget Actual Variance Favourable or

unfavourable

$ $

Sales 640000 655000 15000 Favourable

Less Variable costs

Cost of sales 458000 494500 36500 Unfavourable

Delivery and Installation

costs

19200 13100 6100 Favourable

Sales commissions 12800 16375 -3575 Unfavourable

TOTAL VARIABLE 490000 523975 -33975 Unfavourable

Less Fixed costs

Advertising 5200 5500 -300 Unfavourable

Energy 2800 3200 -400 Unfavourable

Insurance 2400 2400 0

Office supplies 3700 3300 400 Favourable

6

TASK 1.8

Budget variance

Income/ expense Budget Actual Variance Favourable or

unfavourable

$ $

Sales 640000 655000 15000 Favourable

Less Variable costs

Cost of sales 458000 494500 36500 Unfavourable

Delivery and Installation

costs

19200 13100 6100 Favourable

Sales commissions 12800 16375 -3575 Unfavourable

TOTAL VARIABLE 490000 523975 -33975 Unfavourable

Less Fixed costs

Advertising 5200 5500 -300 Unfavourable

Energy 2800 3200 -400 Unfavourable

Insurance 2400 2400 0

Office supplies 3700 3300 400 Favourable

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Printing & stationery 6000 5500 500 Favourable

TOTAL FIXED 20100 19900 200 Favourable

TOTAL COSTS 510100 543875 -33775 Unfavourable

NET INCOME 109800 91225 -18575 Unfavourable

TASK 1.9

Discuss forecasting techniques

Delphi method-

It is a forecasting technique which is used to facilitate decisions from panel of experts so

that estimation may be made in effective way.

Time series forecasting-

Time series forecasting is used to gather past trends and forecast the same in future so

that coming trends can be highlighted (Xu, Zhang and Pinedo, 2017.). Yearly, weekly, monthly

data is taken to forecast.

Subjective approach-

Subjective approach is quite effective forecasting technique for which outcomes are

forecasted by experts depending upon their subjective feelings.

Double-entry accounting

The accounting is based on the concept that every transaction has a dual effect and both

debit and credit side should be balanced.

Variance analysis

The difference obtained between planned output and actual one is termed is variance

analysis. For overcoming this, corrective action is taken to improve the situation.

Assessment Activity 2

TASK 2.1

Preparation of budget objectives

Planning

7

TOTAL FIXED 20100 19900 200 Favourable

TOTAL COSTS 510100 543875 -33775 Unfavourable

NET INCOME 109800 91225 -18575 Unfavourable

TASK 1.9

Discuss forecasting techniques

Delphi method-

It is a forecasting technique which is used to facilitate decisions from panel of experts so

that estimation may be made in effective way.

Time series forecasting-

Time series forecasting is used to gather past trends and forecast the same in future so

that coming trends can be highlighted (Xu, Zhang and Pinedo, 2017.). Yearly, weekly, monthly

data is taken to forecast.

Subjective approach-

Subjective approach is quite effective forecasting technique for which outcomes are

forecasted by experts depending upon their subjective feelings.

Double-entry accounting

The accounting is based on the concept that every transaction has a dual effect and both

debit and credit side should be balanced.

Variance analysis

The difference obtained between planned output and actual one is termed is variance

analysis. For overcoming this, corrective action is taken to improve the situation.

Assessment Activity 2

TASK 2.1

Preparation of budget objectives

Planning

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is required that budget should be planned in accordance to the objective of Johnson

Trading so that sales and production forecast may be made (Walczak and Rutkowska, 2017).

Predicting cash flows

Estimating cash flows is required especially in small sized business which is Johnson

Trading in this case so that it may analyse use of working capital.

Resources allocation

Allocation is required so that funds may be properly utilised by the business so that

budgeted results may be obtained.

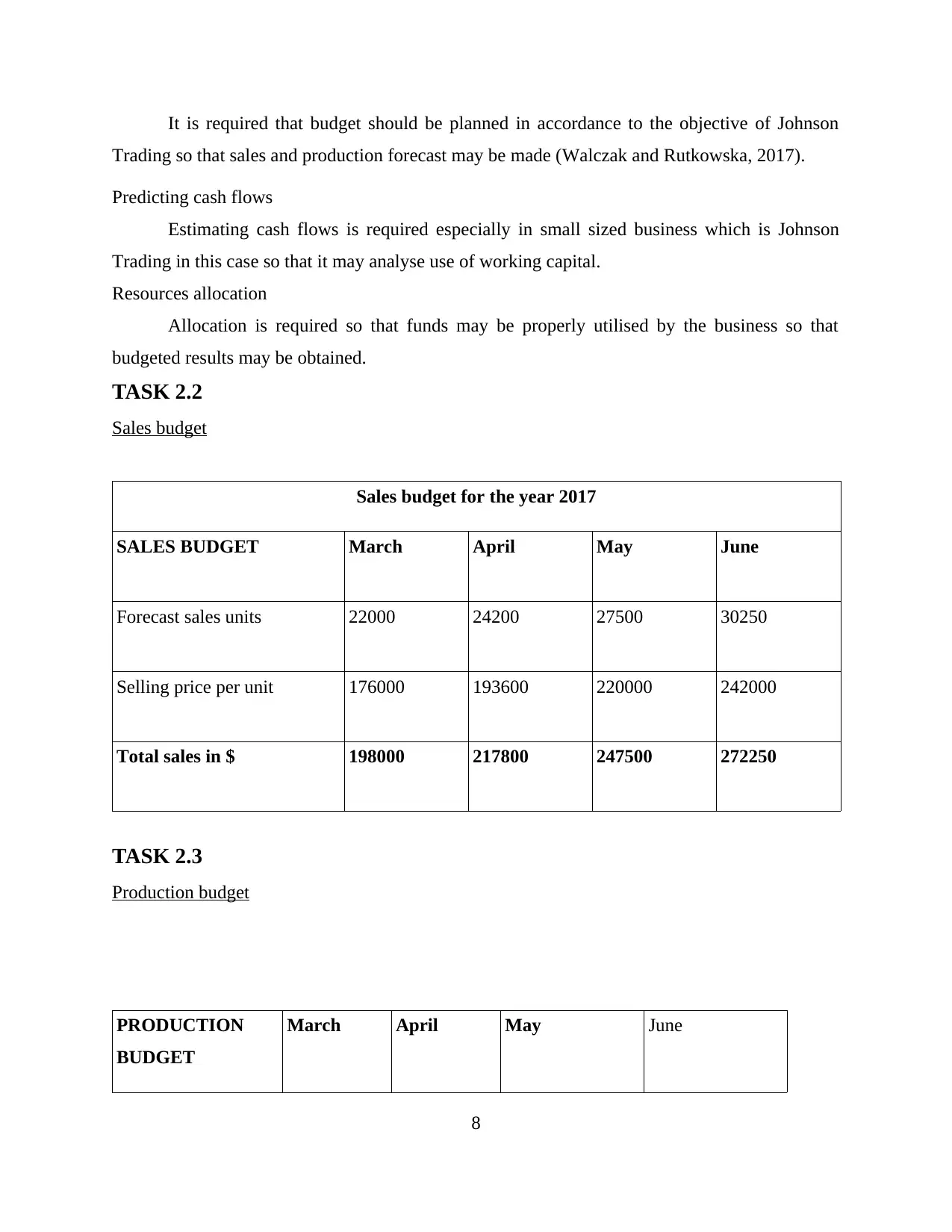

TASK 2.2

Sales budget

Sales budget for the year 2017

SALES BUDGET March April May June

Forecast sales units 22000 24200 27500 30250

Selling price per unit 176000 193600 220000 242000

Total sales in $ 198000 217800 247500 272250

TASK 2.3

Production budget

PRODUCTION

BUDGET

March April May June

8

Trading so that sales and production forecast may be made (Walczak and Rutkowska, 2017).

Predicting cash flows

Estimating cash flows is required especially in small sized business which is Johnson

Trading in this case so that it may analyse use of working capital.

Resources allocation

Allocation is required so that funds may be properly utilised by the business so that

budgeted results may be obtained.

TASK 2.2

Sales budget

Sales budget for the year 2017

SALES BUDGET March April May June

Forecast sales units 22000 24200 27500 30250

Selling price per unit 176000 193600 220000 242000

Total sales in $ 198000 217800 247500 272250

TASK 2.3

Production budget

PRODUCTION

BUDGET

March April May June

8

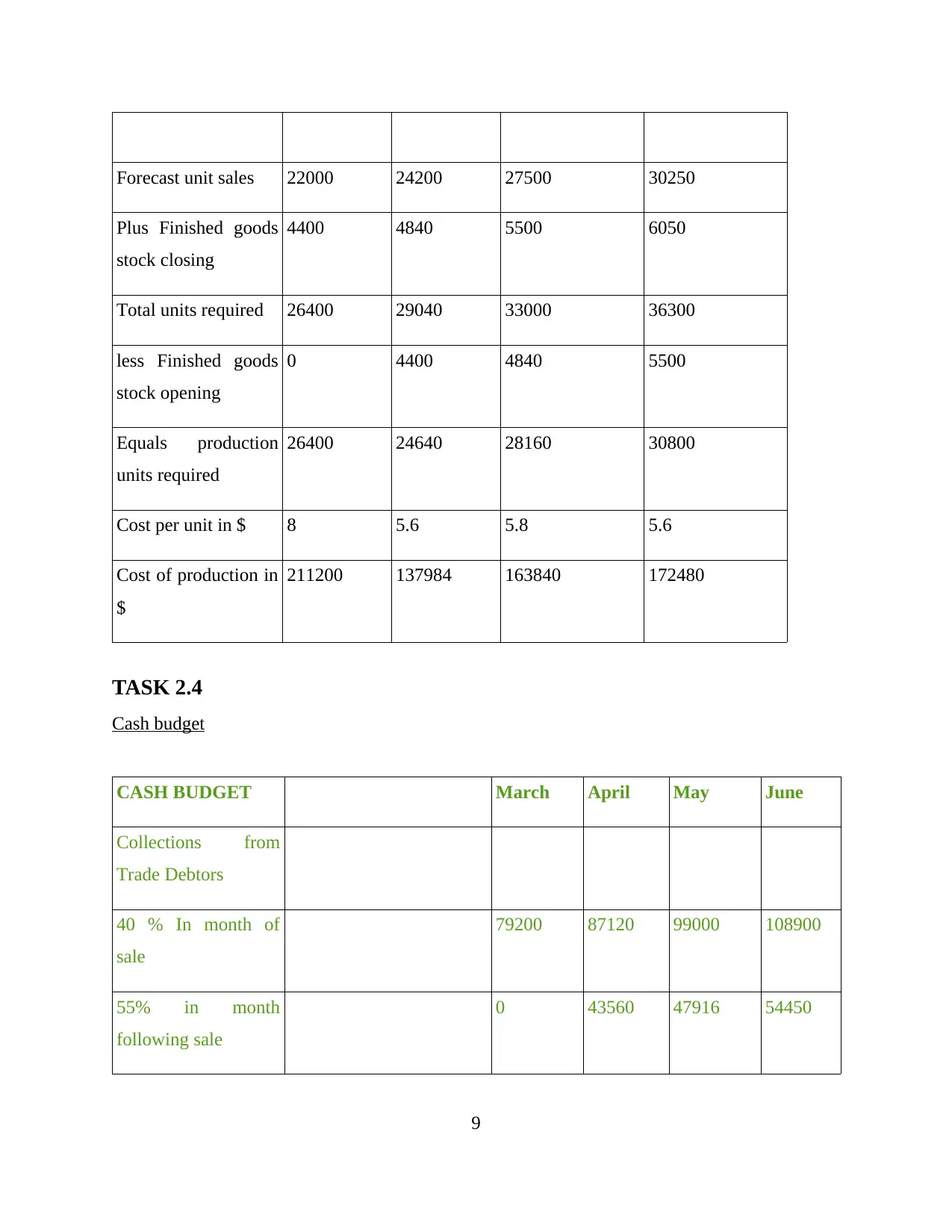

Forecast unit sales 22000 24200 27500 30250

Plus Finished goods

stock closing

4400 4840 5500 6050

Total units required 26400 29040 33000 36300

less Finished goods

stock opening

0 4400 4840 5500

Equals production

units required

26400 24640 28160 30800

Cost per unit in $ 8 5.6 5.8 5.6

Cost of production in

$

211200 137984 163840 172480

TASK 2.4

Cash budget

CASH BUDGET March April May June

Collections from

Trade Debtors

40 % In month of

sale

79200 87120 99000 108900

55% in month

following sale

0 43560 47916 54450

9

Plus Finished goods

stock closing

4400 4840 5500 6050

Total units required 26400 29040 33000 36300

less Finished goods

stock opening

0 4400 4840 5500

Equals production

units required

26400 24640 28160 30800

Cost per unit in $ 8 5.6 5.8 5.6

Cost of production in

$

211200 137984 163840 172480

TASK 2.4

Cash budget

CASH BUDGET March April May June

Collections from

Trade Debtors

40 % In month of

sale

79200 87120 99000 108900

55% in month

following sale

0 43560 47916 54450

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.