Operational Budgets Report: Financial Performance and Budget Analysis

VerifiedAdded on 2020/07/22

|14

|2944

|49

Report

AI Summary

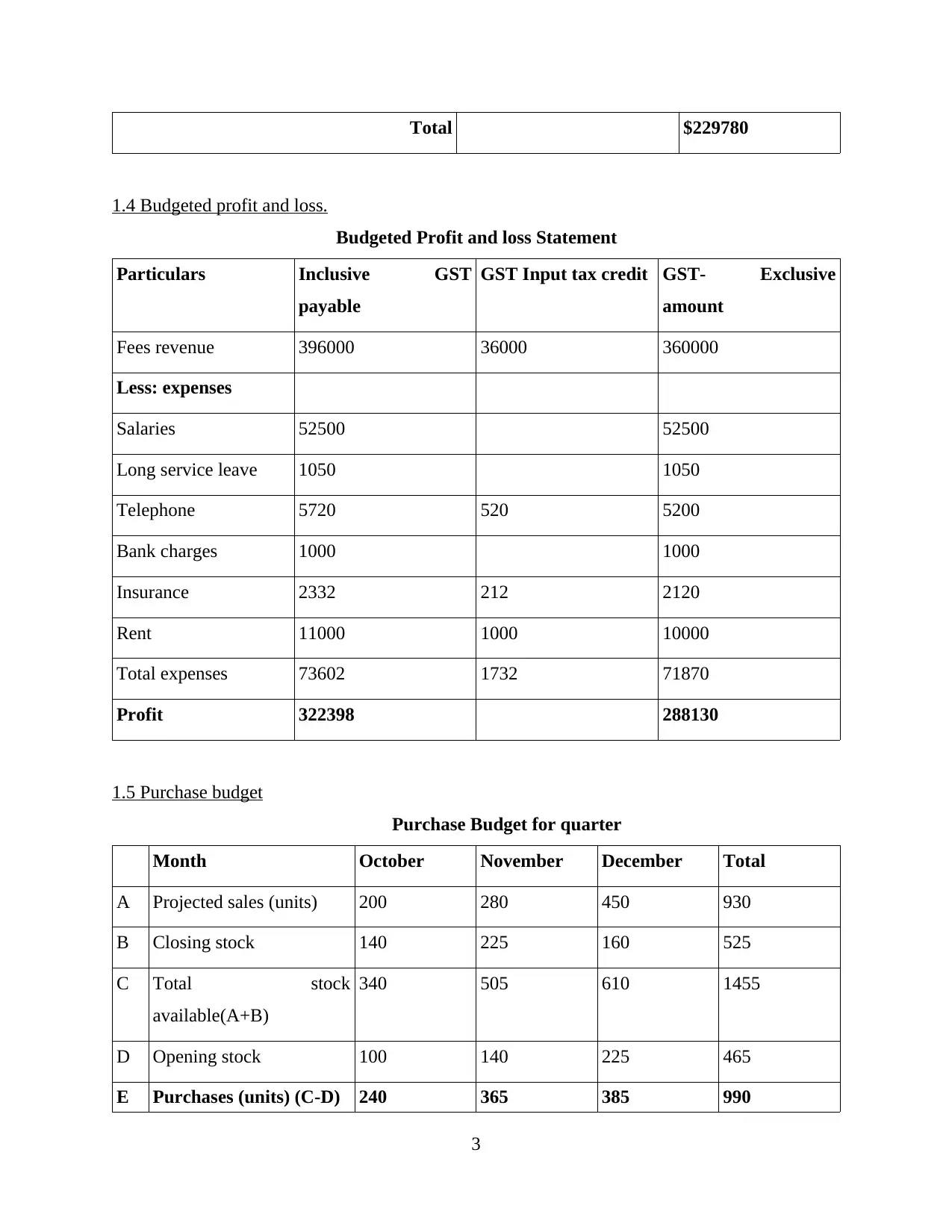

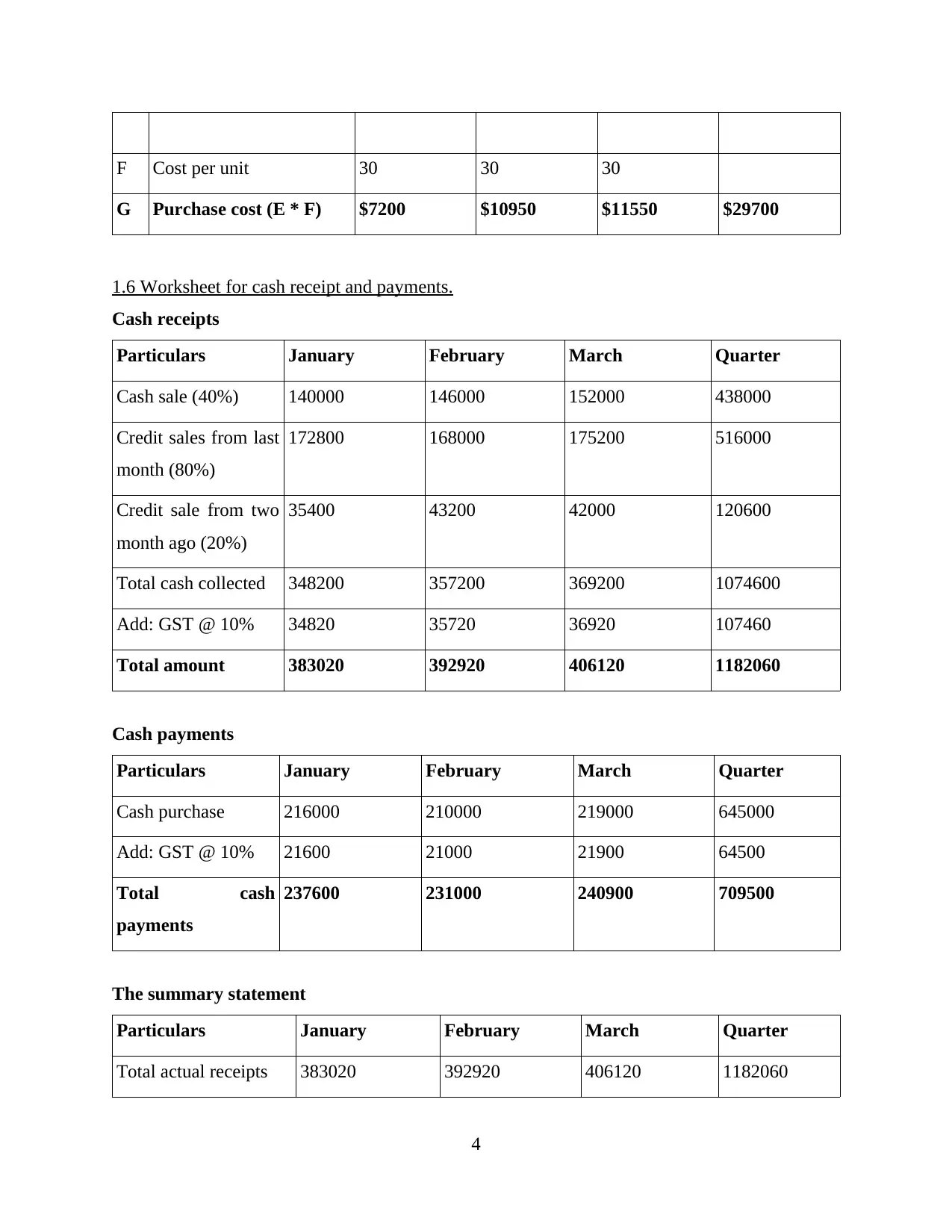

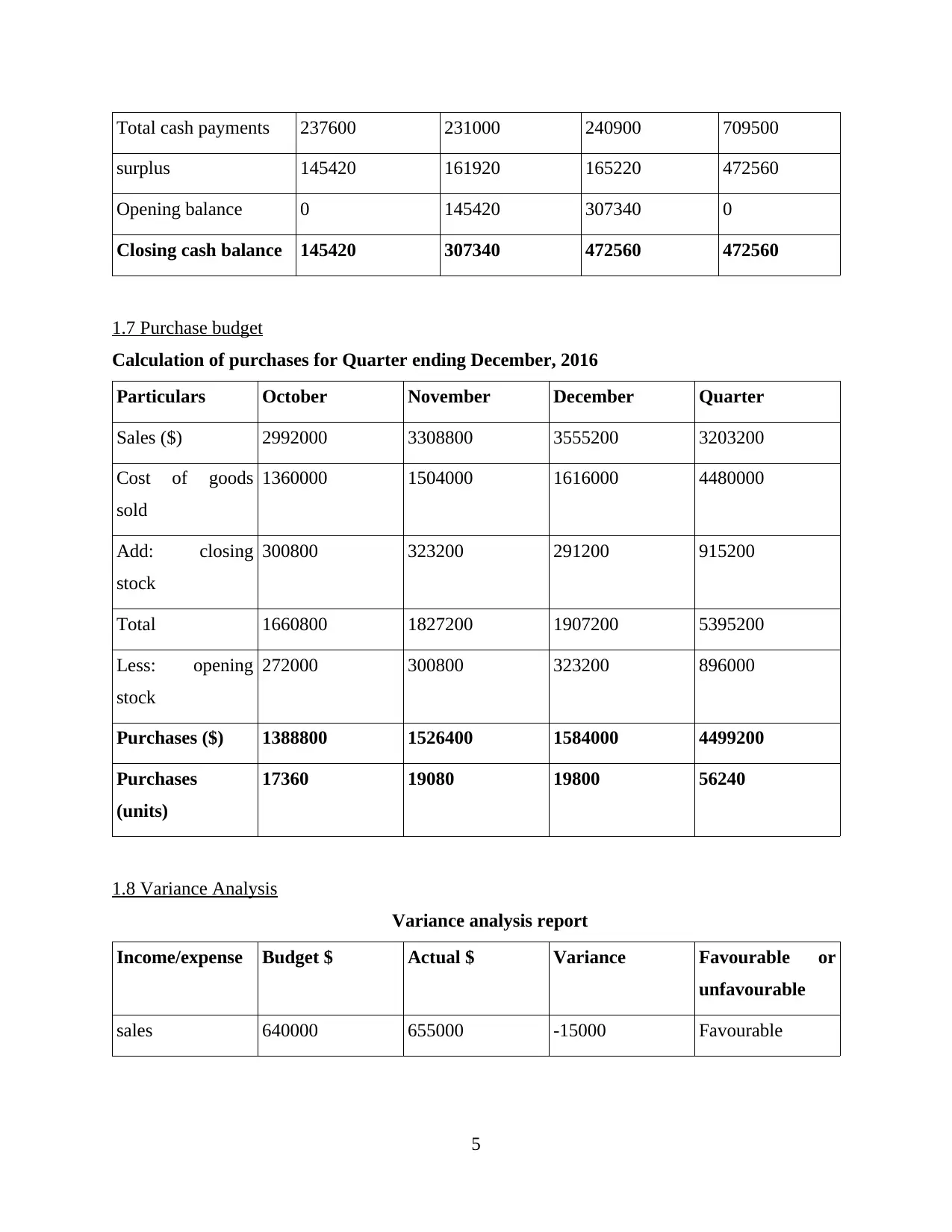

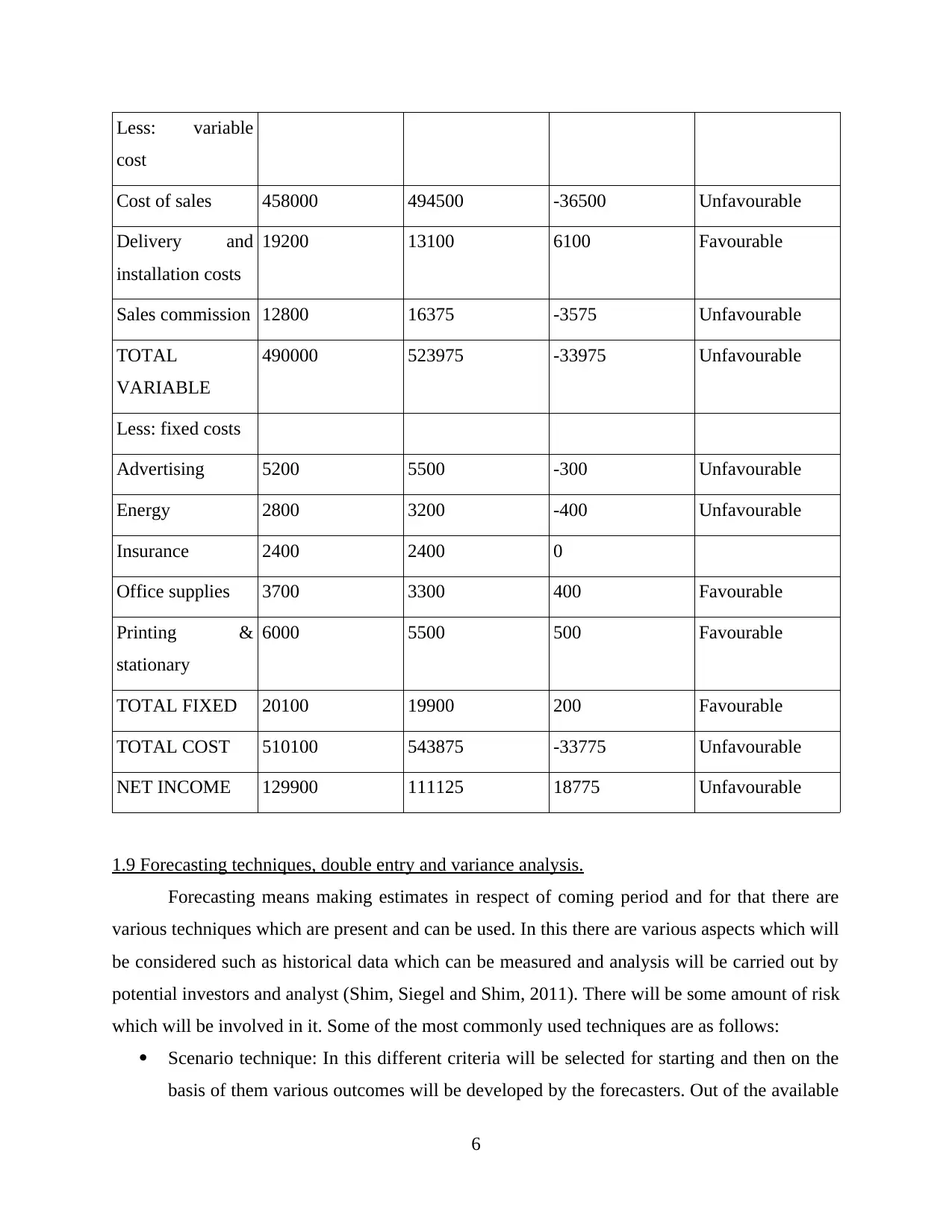

This report delves into the realm of operational budgets within an organization, covering key aspects of financial planning and control. It begins by defining different types of budgets, such as master, operating, cash flow, and static budgets, along with the principles governing budgetary control. The report then explores the scope of budgetary planning, emphasizing the importance of stakeholder consultation and communication. It provides detailed examples, including an annual expenditure budget, a budgeted profit and loss statement, purchase budgets, and worksheets for cash receipts and payments. Variance analysis is discussed, highlighting its role in identifying discrepancies between budgeted and actual figures. The report also covers forecasting techniques, the application of double-entry accounting, and the preparation of various budget components, including sales, production, and cash budgets. Furthermore, it addresses the creation of budgeted income statements and balance sheets, the use of key performance indicators (KPIs), and the recording of reports to facilitate effective financial management and decision-making. The analysis is supported by numerical examples and calculations, providing a practical understanding of the concepts discussed.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.