Asset Allocation Report: Risk, Return and Portfolio Construction

VerifiedAdded on 2022/08/24

|14

|3072

|17

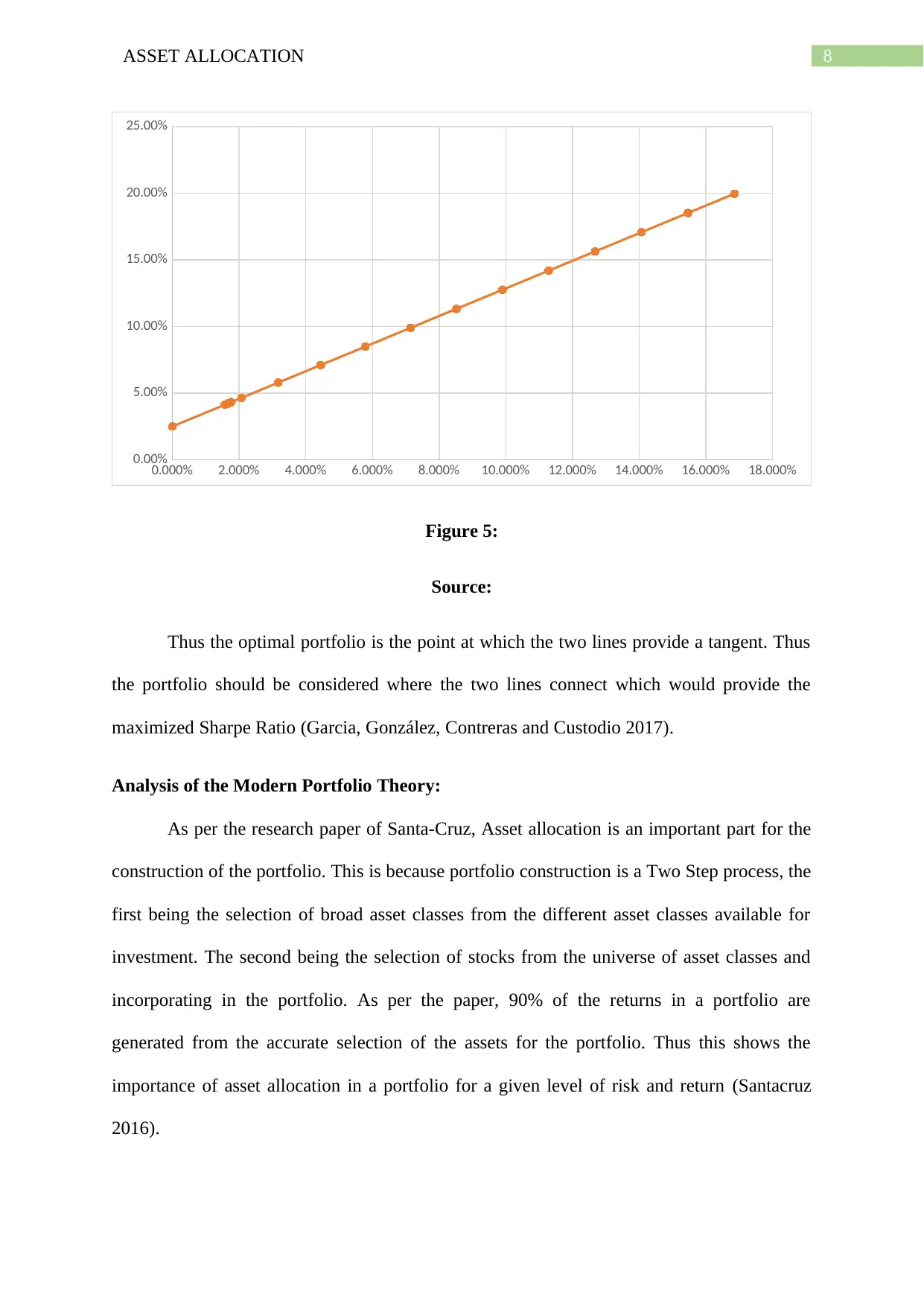

Report

AI Summary

This report delves into the intricacies of asset allocation and portfolio construction, analyzing five broad asset classes over a 20-year period to construct an optimal portfolio. The analysis includes a statistical examination of asset class performance, considering minimum and maximum returns, arithmetic means, and standard deviations to assess risk and volatility. The report also explores the relationships between asset classes using correlation and covariance metrics, highlighting diversification benefits. Furthermore, it constructs an efficient frontier and capital allocation line to determine the optimal portfolio, emphasizing the maximization of the Sharpe Ratio. The report provides an overview of the modern portfolio theory, discussing its application and limitations, including diversification failures during market crashes and the importance of considering higher-order moments. The report references academic papers, and uses these insights to enhance the understanding of asset allocation and its significance in achieving investment objectives.

Running head: ASSET ALLOCATION

Asset Allocation

Name of the Student:

Name of the University:

Author Note:

Asset Allocation

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ASSET ALLOCATION

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Analysis of the asset classes:..................................................................................................2

Performance analysis of the asset class:.................................................................................4

Relationship of the asset class:...............................................................................................5

Portfolio Construction:...........................................................................................................6

Analysis of the Modern Portfolio Theory:.............................................................................8

Conclusion:..............................................................................................................................10

References:...............................................................................................................................11

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Analysis of the asset classes:..................................................................................................2

Performance analysis of the asset class:.................................................................................4

Relationship of the asset class:...............................................................................................5

Portfolio Construction:...........................................................................................................6

Analysis of the Modern Portfolio Theory:.............................................................................8

Conclusion:..............................................................................................................................10

References:...............................................................................................................................11

2ASSET ALLOCATION

Introduction:

The management of a portfolio involves several steps which needs to be undertaken

before the construction of a portfolio. The portfolio management process starts with the

selection of classes of assets which is to be incorporated in the portfolio. Thus the assets

which is to be incorporated is an important aspect, followed by security selection as per the

requirements of the investment policy statement. The investment policy statement states the

risk and return profile of the investor, for whom the portfolio is being constructed. The

portfolio thus constructed needs to be the optimal portfolio for the client at the desired level

of risk and generating return (Výrost, Lyócsa and Baumöhl 2019).

Thus in this report a portfolio consisting of five broad asset classes is analysed over a

20 year time horizon and an optimal portfolio is constructed with the return and risk

generated from the asset class. The Markowitz efficient frontier is constructed and analysed

in regards to the optimal portfolio selected using the risk return profile of the investor.

Thus the modern portfolio theory is discussed providing insights to significant terms

which are used in the management of portfolio or the construction of the portfolio (Roberts

2018).

Discussion:

Analysis of the asset classes:

Thus the asset classes which are being considered with which an optimal portfolio

consisting of these asset classes are highlighted in the following points with a brief

description of each asset class.

Introduction:

The management of a portfolio involves several steps which needs to be undertaken

before the construction of a portfolio. The portfolio management process starts with the

selection of classes of assets which is to be incorporated in the portfolio. Thus the assets

which is to be incorporated is an important aspect, followed by security selection as per the

requirements of the investment policy statement. The investment policy statement states the

risk and return profile of the investor, for whom the portfolio is being constructed. The

portfolio thus constructed needs to be the optimal portfolio for the client at the desired level

of risk and generating return (Výrost, Lyócsa and Baumöhl 2019).

Thus in this report a portfolio consisting of five broad asset classes is analysed over a

20 year time horizon and an optimal portfolio is constructed with the return and risk

generated from the asset class. The Markowitz efficient frontier is constructed and analysed

in regards to the optimal portfolio selected using the risk return profile of the investor.

Thus the modern portfolio theory is discussed providing insights to significant terms

which are used in the management of portfolio or the construction of the portfolio (Roberts

2018).

Discussion:

Analysis of the asset classes:

Thus the asset classes which are being considered with which an optimal portfolio

consisting of these asset classes are highlighted in the following points with a brief

description of each asset class.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ASSET ALLOCATION

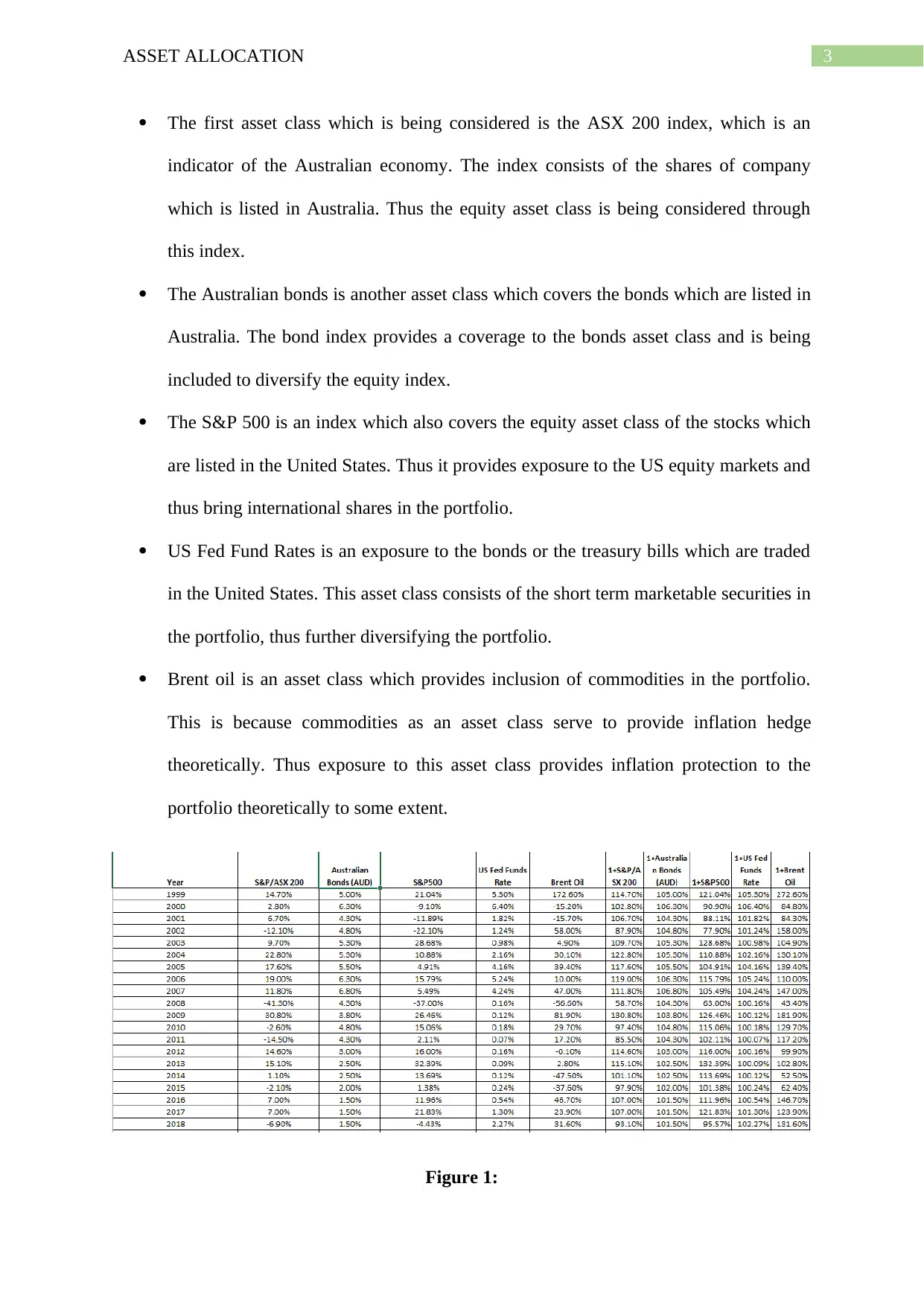

The first asset class which is being considered is the ASX 200 index, which is an

indicator of the Australian economy. The index consists of the shares of company

which is listed in Australia. Thus the equity asset class is being considered through

this index.

The Australian bonds is another asset class which covers the bonds which are listed in

Australia. The bond index provides a coverage to the bonds asset class and is being

included to diversify the equity index.

The S&P 500 is an index which also covers the equity asset class of the stocks which

are listed in the United States. Thus it provides exposure to the US equity markets and

thus bring international shares in the portfolio.

US Fed Fund Rates is an exposure to the bonds or the treasury bills which are traded

in the United States. This asset class consists of the short term marketable securities in

the portfolio, thus further diversifying the portfolio.

Brent oil is an asset class which provides inclusion of commodities in the portfolio.

This is because commodities as an asset class serve to provide inflation hedge

theoretically. Thus exposure to this asset class provides inflation protection to the

portfolio theoretically to some extent.

Figure 1:

The first asset class which is being considered is the ASX 200 index, which is an

indicator of the Australian economy. The index consists of the shares of company

which is listed in Australia. Thus the equity asset class is being considered through

this index.

The Australian bonds is another asset class which covers the bonds which are listed in

Australia. The bond index provides a coverage to the bonds asset class and is being

included to diversify the equity index.

The S&P 500 is an index which also covers the equity asset class of the stocks which

are listed in the United States. Thus it provides exposure to the US equity markets and

thus bring international shares in the portfolio.

US Fed Fund Rates is an exposure to the bonds or the treasury bills which are traded

in the United States. This asset class consists of the short term marketable securities in

the portfolio, thus further diversifying the portfolio.

Brent oil is an asset class which provides inclusion of commodities in the portfolio.

This is because commodities as an asset class serve to provide inflation hedge

theoretically. Thus exposure to this asset class provides inflation protection to the

portfolio theoretically to some extent.

Figure 1:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ASSET ALLOCATION

Source:

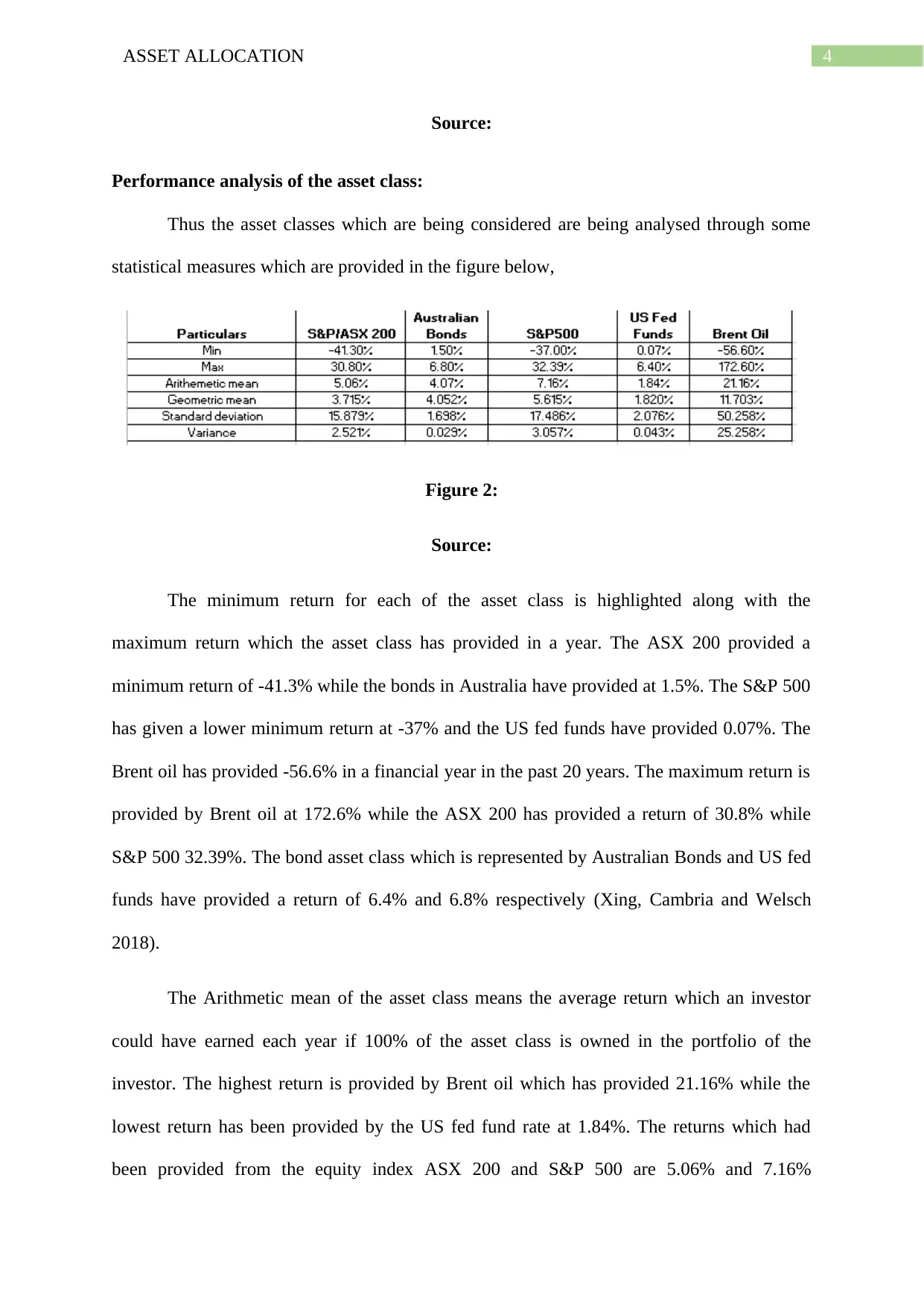

Performance analysis of the asset class:

Thus the asset classes which are being considered are being analysed through some

statistical measures which are provided in the figure below,

Figure 2:

Source:

The minimum return for each of the asset class is highlighted along with the

maximum return which the asset class has provided in a year. The ASX 200 provided a

minimum return of -41.3% while the bonds in Australia have provided at 1.5%. The S&P 500

has given a lower minimum return at -37% and the US fed funds have provided 0.07%. The

Brent oil has provided -56.6% in a financial year in the past 20 years. The maximum return is

provided by Brent oil at 172.6% while the ASX 200 has provided a return of 30.8% while

S&P 500 32.39%. The bond asset class which is represented by Australian Bonds and US fed

funds have provided a return of 6.4% and 6.8% respectively (Xing, Cambria and Welsch

2018).

The Arithmetic mean of the asset class means the average return which an investor

could have earned each year if 100% of the asset class is owned in the portfolio of the

investor. The highest return is provided by Brent oil which has provided 21.16% while the

lowest return has been provided by the US fed fund rate at 1.84%. The returns which had

been provided from the equity index ASX 200 and S&P 500 are 5.06% and 7.16%

Source:

Performance analysis of the asset class:

Thus the asset classes which are being considered are being analysed through some

statistical measures which are provided in the figure below,

Figure 2:

Source:

The minimum return for each of the asset class is highlighted along with the

maximum return which the asset class has provided in a year. The ASX 200 provided a

minimum return of -41.3% while the bonds in Australia have provided at 1.5%. The S&P 500

has given a lower minimum return at -37% and the US fed funds have provided 0.07%. The

Brent oil has provided -56.6% in a financial year in the past 20 years. The maximum return is

provided by Brent oil at 172.6% while the ASX 200 has provided a return of 30.8% while

S&P 500 32.39%. The bond asset class which is represented by Australian Bonds and US fed

funds have provided a return of 6.4% and 6.8% respectively (Xing, Cambria and Welsch

2018).

The Arithmetic mean of the asset class means the average return which an investor

could have earned each year if 100% of the asset class is owned in the portfolio of the

investor. The highest return is provided by Brent oil which has provided 21.16% while the

lowest return has been provided by the US fed fund rate at 1.84%. The returns which had

been provided from the equity index ASX 200 and S&P 500 are 5.06% and 7.16%

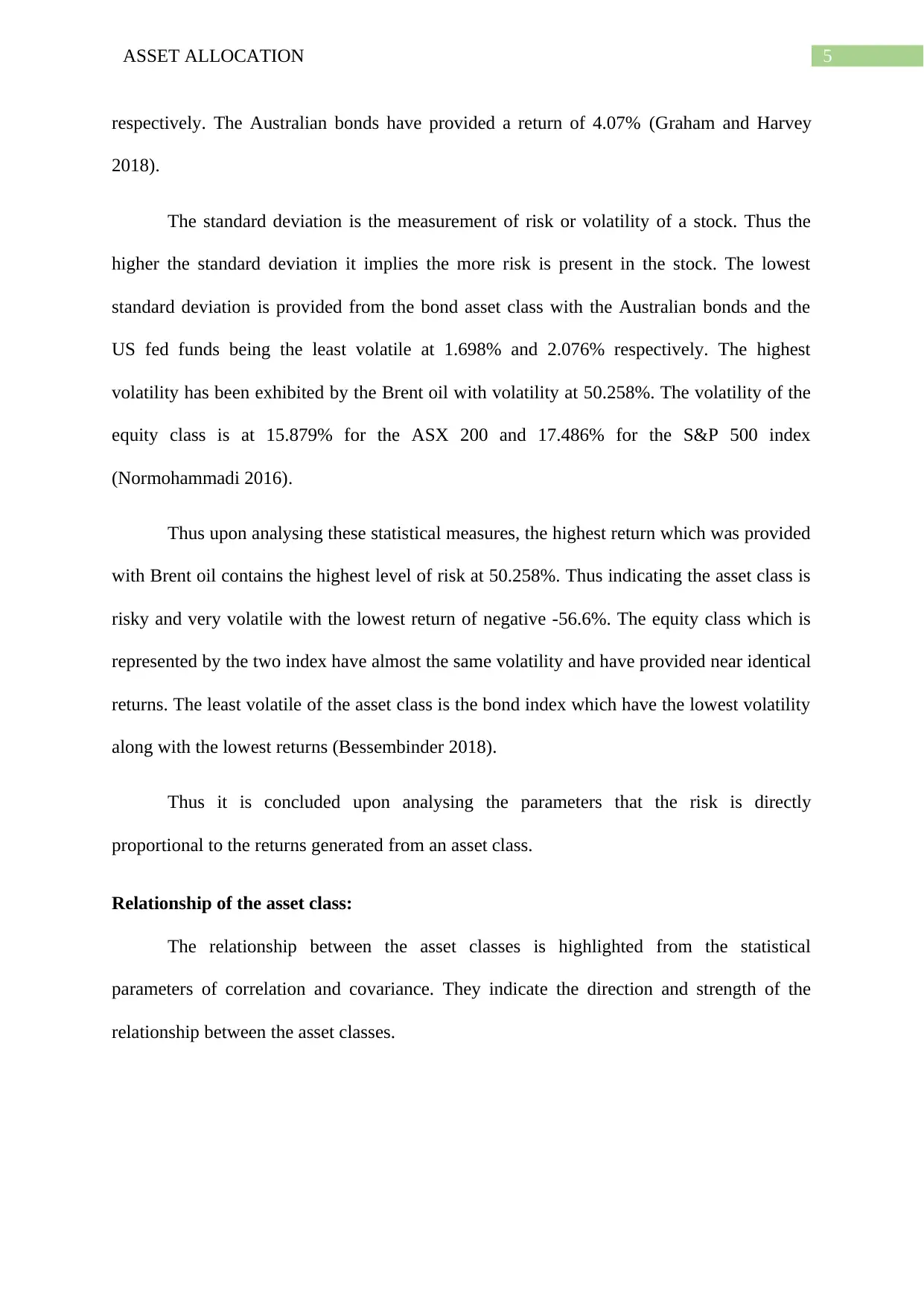

5ASSET ALLOCATION

respectively. The Australian bonds have provided a return of 4.07% (Graham and Harvey

2018).

The standard deviation is the measurement of risk or volatility of a stock. Thus the

higher the standard deviation it implies the more risk is present in the stock. The lowest

standard deviation is provided from the bond asset class with the Australian bonds and the

US fed funds being the least volatile at 1.698% and 2.076% respectively. The highest

volatility has been exhibited by the Brent oil with volatility at 50.258%. The volatility of the

equity class is at 15.879% for the ASX 200 and 17.486% for the S&P 500 index

(Normohammadi 2016).

Thus upon analysing these statistical measures, the highest return which was provided

with Brent oil contains the highest level of risk at 50.258%. Thus indicating the asset class is

risky and very volatile with the lowest return of negative -56.6%. The equity class which is

represented by the two index have almost the same volatility and have provided near identical

returns. The least volatile of the asset class is the bond index which have the lowest volatility

along with the lowest returns (Bessembinder 2018).

Thus it is concluded upon analysing the parameters that the risk is directly

proportional to the returns generated from an asset class.

Relationship of the asset class:

The relationship between the asset classes is highlighted from the statistical

parameters of correlation and covariance. They indicate the direction and strength of the

relationship between the asset classes.

respectively. The Australian bonds have provided a return of 4.07% (Graham and Harvey

2018).

The standard deviation is the measurement of risk or volatility of a stock. Thus the

higher the standard deviation it implies the more risk is present in the stock. The lowest

standard deviation is provided from the bond asset class with the Australian bonds and the

US fed funds being the least volatile at 1.698% and 2.076% respectively. The highest

volatility has been exhibited by the Brent oil with volatility at 50.258%. The volatility of the

equity class is at 15.879% for the ASX 200 and 17.486% for the S&P 500 index

(Normohammadi 2016).

Thus upon analysing these statistical measures, the highest return which was provided

with Brent oil contains the highest level of risk at 50.258%. Thus indicating the asset class is

risky and very volatile with the lowest return of negative -56.6%. The equity class which is

represented by the two index have almost the same volatility and have provided near identical

returns. The least volatile of the asset class is the bond index which have the lowest volatility

along with the lowest returns (Bessembinder 2018).

Thus it is concluded upon analysing the parameters that the risk is directly

proportional to the returns generated from an asset class.

Relationship of the asset class:

The relationship between the asset classes is highlighted from the statistical

parameters of correlation and covariance. They indicate the direction and strength of the

relationship between the asset classes.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ASSET ALLOCATION

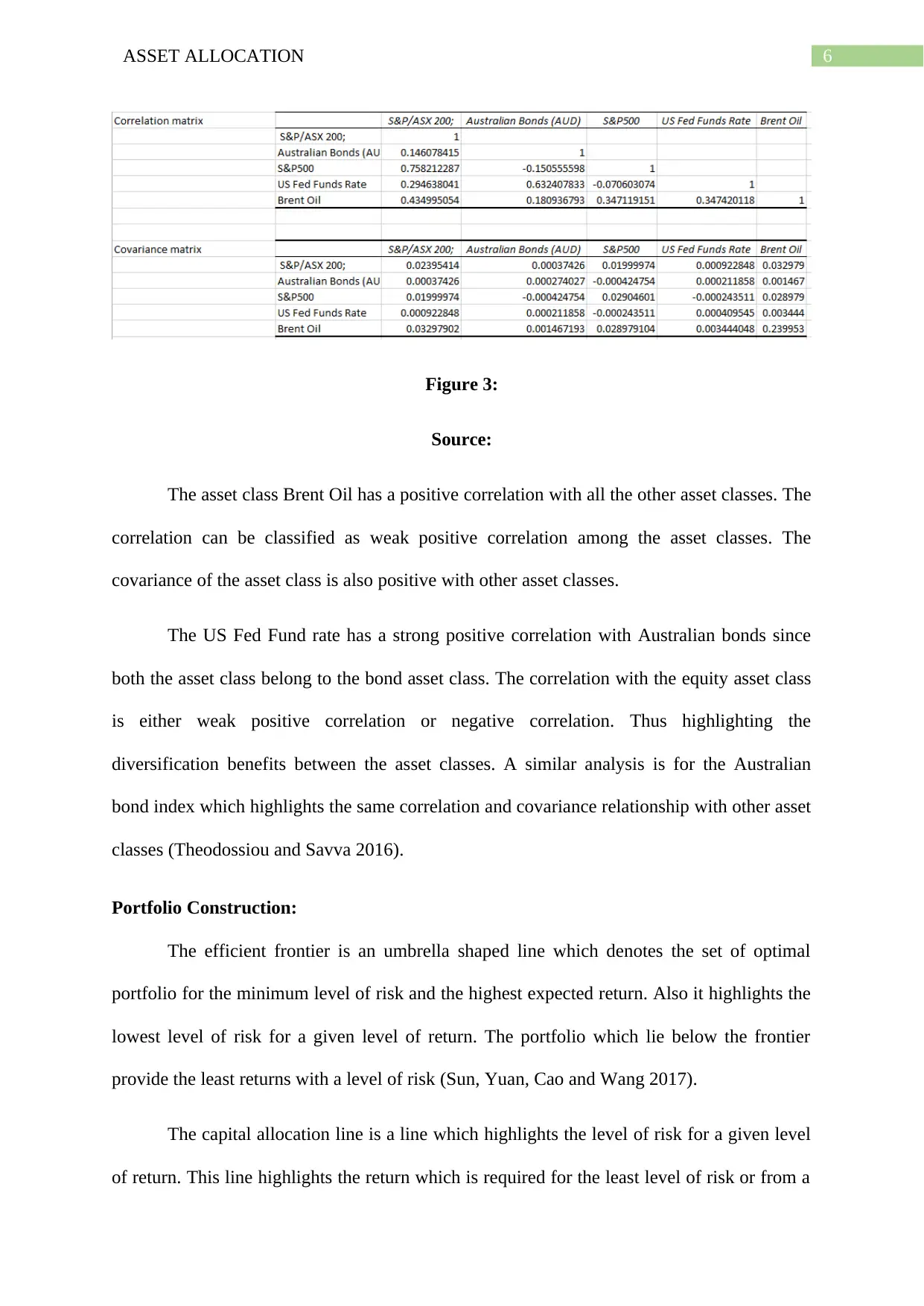

Figure 3:

Source:

The asset class Brent Oil has a positive correlation with all the other asset classes. The

correlation can be classified as weak positive correlation among the asset classes. The

covariance of the asset class is also positive with other asset classes.

The US Fed Fund rate has a strong positive correlation with Australian bonds since

both the asset class belong to the bond asset class. The correlation with the equity asset class

is either weak positive correlation or negative correlation. Thus highlighting the

diversification benefits between the asset classes. A similar analysis is for the Australian

bond index which highlights the same correlation and covariance relationship with other asset

classes (Theodossiou and Savva 2016).

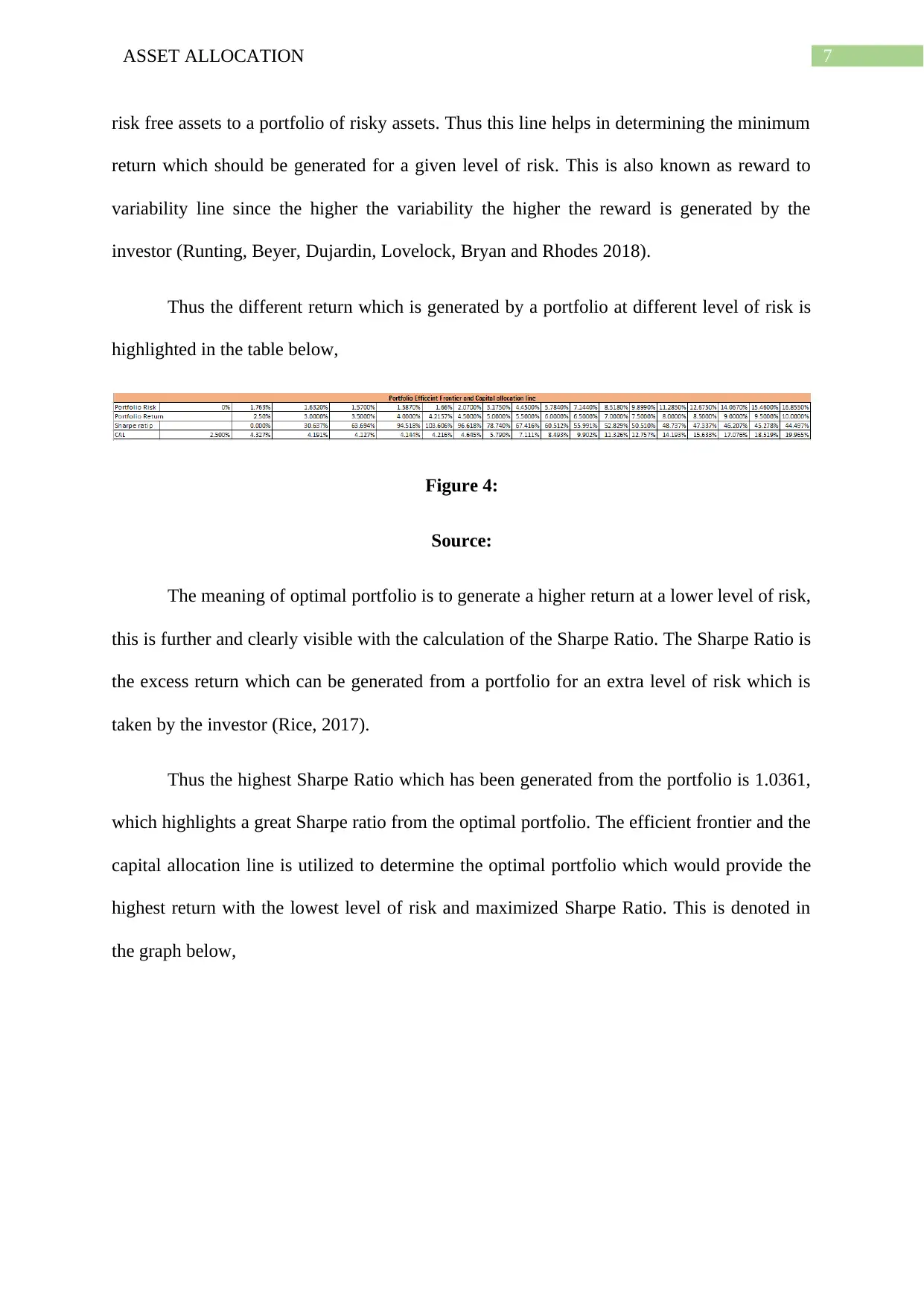

Portfolio Construction:

The efficient frontier is an umbrella shaped line which denotes the set of optimal

portfolio for the minimum level of risk and the highest expected return. Also it highlights the

lowest level of risk for a given level of return. The portfolio which lie below the frontier

provide the least returns with a level of risk (Sun, Yuan, Cao and Wang 2017).

The capital allocation line is a line which highlights the level of risk for a given level

of return. This line highlights the return which is required for the least level of risk or from a

Figure 3:

Source:

The asset class Brent Oil has a positive correlation with all the other asset classes. The

correlation can be classified as weak positive correlation among the asset classes. The

covariance of the asset class is also positive with other asset classes.

The US Fed Fund rate has a strong positive correlation with Australian bonds since

both the asset class belong to the bond asset class. The correlation with the equity asset class

is either weak positive correlation or negative correlation. Thus highlighting the

diversification benefits between the asset classes. A similar analysis is for the Australian

bond index which highlights the same correlation and covariance relationship with other asset

classes (Theodossiou and Savva 2016).

Portfolio Construction:

The efficient frontier is an umbrella shaped line which denotes the set of optimal

portfolio for the minimum level of risk and the highest expected return. Also it highlights the

lowest level of risk for a given level of return. The portfolio which lie below the frontier

provide the least returns with a level of risk (Sun, Yuan, Cao and Wang 2017).

The capital allocation line is a line which highlights the level of risk for a given level

of return. This line highlights the return which is required for the least level of risk or from a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ASSET ALLOCATION

risk free assets to a portfolio of risky assets. Thus this line helps in determining the minimum

return which should be generated for a given level of risk. This is also known as reward to

variability line since the higher the variability the higher the reward is generated by the

investor (Runting, Beyer, Dujardin, Lovelock, Bryan and Rhodes 2018).

Thus the different return which is generated by a portfolio at different level of risk is

highlighted in the table below,

Figure 4:

Source:

The meaning of optimal portfolio is to generate a higher return at a lower level of risk,

this is further and clearly visible with the calculation of the Sharpe Ratio. The Sharpe Ratio is

the excess return which can be generated from a portfolio for an extra level of risk which is

taken by the investor (Rice, 2017).

Thus the highest Sharpe Ratio which has been generated from the portfolio is 1.0361,

which highlights a great Sharpe ratio from the optimal portfolio. The efficient frontier and the

capital allocation line is utilized to determine the optimal portfolio which would provide the

highest return with the lowest level of risk and maximized Sharpe Ratio. This is denoted in

the graph below,

risk free assets to a portfolio of risky assets. Thus this line helps in determining the minimum

return which should be generated for a given level of risk. This is also known as reward to

variability line since the higher the variability the higher the reward is generated by the

investor (Runting, Beyer, Dujardin, Lovelock, Bryan and Rhodes 2018).

Thus the different return which is generated by a portfolio at different level of risk is

highlighted in the table below,

Figure 4:

Source:

The meaning of optimal portfolio is to generate a higher return at a lower level of risk,

this is further and clearly visible with the calculation of the Sharpe Ratio. The Sharpe Ratio is

the excess return which can be generated from a portfolio for an extra level of risk which is

taken by the investor (Rice, 2017).

Thus the highest Sharpe Ratio which has been generated from the portfolio is 1.0361,

which highlights a great Sharpe ratio from the optimal portfolio. The efficient frontier and the

capital allocation line is utilized to determine the optimal portfolio which would provide the

highest return with the lowest level of risk and maximized Sharpe Ratio. This is denoted in

the graph below,

8ASSET ALLOCATION

0.000% 2.000% 4.000% 6.000% 8.000% 10.000% 12.000% 14.000% 16.000% 18.000%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Figure 5:

Source:

Thus the optimal portfolio is the point at which the two lines provide a tangent. Thus

the portfolio should be considered where the two lines connect which would provide the

maximized Sharpe Ratio (Garcia, González, Contreras and Custodio 2017).

Analysis of the Modern Portfolio Theory:

As per the research paper of Santa-Cruz, Asset allocation is an important part for the

construction of the portfolio. This is because portfolio construction is a Two Step process, the

first being the selection of broad asset classes from the different asset classes available for

investment. The second being the selection of stocks from the universe of asset classes and

incorporating in the portfolio. As per the paper, 90% of the returns in a portfolio are

generated from the accurate selection of the assets for the portfolio. Thus this shows the

importance of asset allocation in a portfolio for a given level of risk and return (Santacruz

2016).

0.000% 2.000% 4.000% 6.000% 8.000% 10.000% 12.000% 14.000% 16.000% 18.000%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Figure 5:

Source:

Thus the optimal portfolio is the point at which the two lines provide a tangent. Thus

the portfolio should be considered where the two lines connect which would provide the

maximized Sharpe Ratio (Garcia, González, Contreras and Custodio 2017).

Analysis of the Modern Portfolio Theory:

As per the research paper of Santa-Cruz, Asset allocation is an important part for the

construction of the portfolio. This is because portfolio construction is a Two Step process, the

first being the selection of broad asset classes from the different asset classes available for

investment. The second being the selection of stocks from the universe of asset classes and

incorporating in the portfolio. As per the paper, 90% of the returns in a portfolio are

generated from the accurate selection of the assets for the portfolio. Thus this shows the

importance of asset allocation in a portfolio for a given level of risk and return (Santacruz

2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ASSET ALLOCATION

Also as per the paper of Page and Panariello, the asset allocation is an important part

since it brings diversification benefits to the portfolio. This is due to the correlation which is

between the different asset classes which helps in minimizing the risk and maximising the

return of the portfolio. This is the essence of the modern portfolio theory and asset classes are

selected and taken for the purpose of portfolio construction using this principle to bring the

diversification benefits in the portfolio. This has been highlighted in the portfolio constructed

above as the correlation of the commodities is weak and positive with all other asset classes.

The asset classes which are represented by different index but in the same asset class have

positive correlation, like the equity asset class is represented by the ASX 200 and S&P 500

which have a positive correlation. Also the Bond index which are in the bond asset class have

a positive correlation among themselves. However, the correlation is reduced between the

bond and equity asset class (Page & Panariello 2018).

As per McKay and Thomas, in their paper, they also highlight the benefits of

diversification in a portfolio. However, both the research papers highlight the points when

diversification of a portfolio fails when it is needed the most by the investors. The funds

which are over-diversified and have a large number of active managers fail to provide excess

return since the return which is generated is reduced to pay the active managers fee. This has

been highlighted that the funds which are less actively managed have provided better returns

than the funds which are over diversified. This is because the returns which are generated in

excess are reduced due to the payment of more fees to the fund managers (McKay, Shaoiro &

Thomas 2018).

Also diversification of the portfolio gets reduced when the market crashes due to the

spike in the correlation and thus all asset classes generate negative returns. Thus the portfolio

suffers due to rise in the correlation which leads to the losses in the portfolio. Also the

Also as per the paper of Page and Panariello, the asset allocation is an important part

since it brings diversification benefits to the portfolio. This is due to the correlation which is

between the different asset classes which helps in minimizing the risk and maximising the

return of the portfolio. This is the essence of the modern portfolio theory and asset classes are

selected and taken for the purpose of portfolio construction using this principle to bring the

diversification benefits in the portfolio. This has been highlighted in the portfolio constructed

above as the correlation of the commodities is weak and positive with all other asset classes.

The asset classes which are represented by different index but in the same asset class have

positive correlation, like the equity asset class is represented by the ASX 200 and S&P 500

which have a positive correlation. Also the Bond index which are in the bond asset class have

a positive correlation among themselves. However, the correlation is reduced between the

bond and equity asset class (Page & Panariello 2018).

As per McKay and Thomas, in their paper, they also highlight the benefits of

diversification in a portfolio. However, both the research papers highlight the points when

diversification of a portfolio fails when it is needed the most by the investors. The funds

which are over-diversified and have a large number of active managers fail to provide excess

return since the return which is generated is reduced to pay the active managers fee. This has

been highlighted that the funds which are less actively managed have provided better returns

than the funds which are over diversified. This is because the returns which are generated in

excess are reduced due to the payment of more fees to the fund managers (McKay, Shaoiro &

Thomas 2018).

Also diversification of the portfolio gets reduced when the market crashes due to the

spike in the correlation and thus all asset classes generate negative returns. Thus the portfolio

suffers due to rise in the correlation which leads to the losses in the portfolio. Also the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ASSET ALLOCATION

correlation should be positive when the markets are rising which would lead to the generation

of returns, but the exact opposite is observed with correlation being positive in a crash.

Thus, modern portfolio theory should be used in the construction of an optimal

portfolio but should be supplemented with rigorous analysis with third order moments. Since

the assumption in modern portfolio theory is that the optimal portfolio is constructed using

the Normal distribution. The other moments such as skewness and kurtosis should be

incorporated in the selection of the portfolio. Also the portfolio should be subject to rigorous

stress testing and scenario testing to assess the impact on the portfolio during times of

economic downturn.

Conclusion:

Thus in this report it is concluded about the analysis of the different asset classes and

their importance in portfolio management. The statistical measures which highlight the

performance of the asset classes is analysed with the use of other statistical measures. The

optimal portfolio is constructed and analysed as per the modern portfolio theory. Also the use

of efficient frontier with capital allocation line is used in the selection of the portfolio. The

limitations and the drawbacks of the modern portfolio theory in construction of the portfolio

is analysed. Thus the portfolio construction should include other measures which should

supplement the modern portfolio theory.

correlation should be positive when the markets are rising which would lead to the generation

of returns, but the exact opposite is observed with correlation being positive in a crash.

Thus, modern portfolio theory should be used in the construction of an optimal

portfolio but should be supplemented with rigorous analysis with third order moments. Since

the assumption in modern portfolio theory is that the optimal portfolio is constructed using

the Normal distribution. The other moments such as skewness and kurtosis should be

incorporated in the selection of the portfolio. Also the portfolio should be subject to rigorous

stress testing and scenario testing to assess the impact on the portfolio during times of

economic downturn.

Conclusion:

Thus in this report it is concluded about the analysis of the different asset classes and

their importance in portfolio management. The statistical measures which highlight the

performance of the asset classes is analysed with the use of other statistical measures. The

optimal portfolio is constructed and analysed as per the modern portfolio theory. Also the use

of efficient frontier with capital allocation line is used in the selection of the portfolio. The

limitations and the drawbacks of the modern portfolio theory in construction of the portfolio

is analysed. Thus the portfolio construction should include other measures which should

supplement the modern portfolio theory.

11ASSET ALLOCATION

References:

Akansu, A.N., Kulkarni, S.R. and Malioutov, D.M., 2016. Sparse Markowitz Portfolios.

Bessembinder, H., 2018. Do stocks outperform treasury bills?. Journal of financial

economics, 129(3), pp.440-457.

Bodie, Z, Kane A & Marcus, AJ 2018, Investments, 11th edn, McGraw-Hill Education

(ISBN: 9781259277177).

deLlano-Paz, F., Calvo-Silvosa, A., Antelo, S.I. and Soares, I., 2017. Energy planning and

modern portfolio theory: A review. Renewable and Sustainable Energy Reviews, 77, pp.636-

651.

Dhrymes, P.J., 2017. Portfolio theory: origins, Markowitz and CAPM based selection.

In Portfolio Construction, Measurement, and Efficiency (pp. 39-48). Springer, Cham.

Fischer, J., 2019, October. Modern Portfolio Theory and the Efficient Markets Hypothesis:

How well did they serve Canada? s baby-boom generation?. In Proceedings of Economics

and Finance Conferences (No. 9511941). International Institute of Social and Economic

Sciences.

Garcia, R.C., González, V., Contreras, J. and Custodio, J.E., 2017. Applying modern

portfolio theory for a dynamic energy portfolio allocation in electricity markets. Electric

Power Systems Research, 150, pp.11-23.

Graham, J.R. and Harvey, C.R., 2018. The equity risk premium in 2018. Available at SSRN

3151162.

McKay, S, Shaoiro, R & Thomas, R 2018, ‘What free lunch? The costs of

overdiversification’, Financial Analysts Journal, vol. 74, no. 1, pp. 44-57.

References:

Akansu, A.N., Kulkarni, S.R. and Malioutov, D.M., 2016. Sparse Markowitz Portfolios.

Bessembinder, H., 2018. Do stocks outperform treasury bills?. Journal of financial

economics, 129(3), pp.440-457.

Bodie, Z, Kane A & Marcus, AJ 2018, Investments, 11th edn, McGraw-Hill Education

(ISBN: 9781259277177).

deLlano-Paz, F., Calvo-Silvosa, A., Antelo, S.I. and Soares, I., 2017. Energy planning and

modern portfolio theory: A review. Renewable and Sustainable Energy Reviews, 77, pp.636-

651.

Dhrymes, P.J., 2017. Portfolio theory: origins, Markowitz and CAPM based selection.

In Portfolio Construction, Measurement, and Efficiency (pp. 39-48). Springer, Cham.

Fischer, J., 2019, October. Modern Portfolio Theory and the Efficient Markets Hypothesis:

How well did they serve Canada? s baby-boom generation?. In Proceedings of Economics

and Finance Conferences (No. 9511941). International Institute of Social and Economic

Sciences.

Garcia, R.C., González, V., Contreras, J. and Custodio, J.E., 2017. Applying modern

portfolio theory for a dynamic energy portfolio allocation in electricity markets. Electric

Power Systems Research, 150, pp.11-23.

Graham, J.R. and Harvey, C.R., 2018. The equity risk premium in 2018. Available at SSRN

3151162.

McKay, S, Shaoiro, R & Thomas, R 2018, ‘What free lunch? The costs of

overdiversification’, Financial Analysts Journal, vol. 74, no. 1, pp. 44-57.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.