Finance Capstone: Optimal Portfolio Performance and Diversification

VerifiedAdded on 2023/01/05

|10

|486

|87

Project

AI Summary

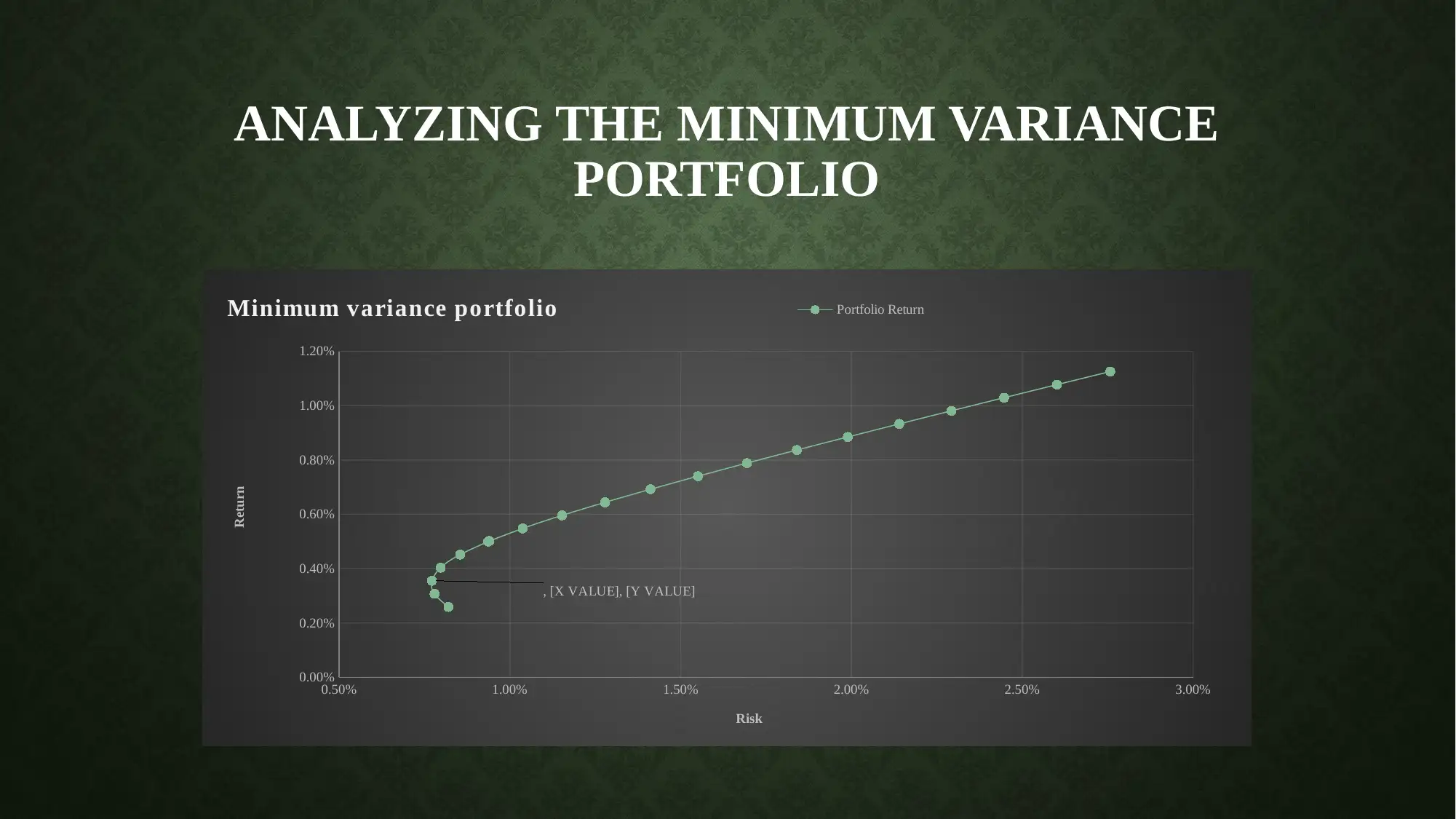

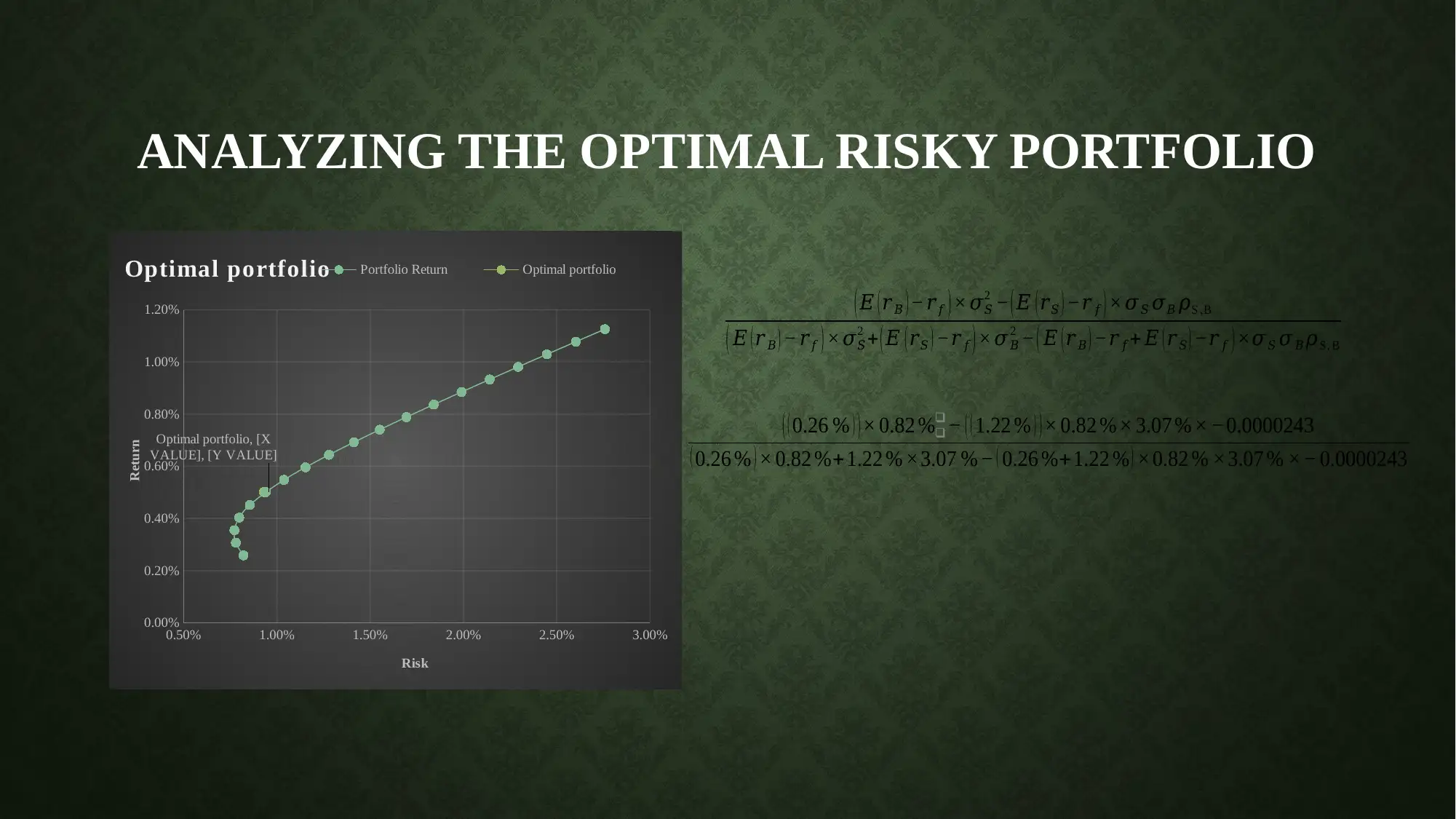

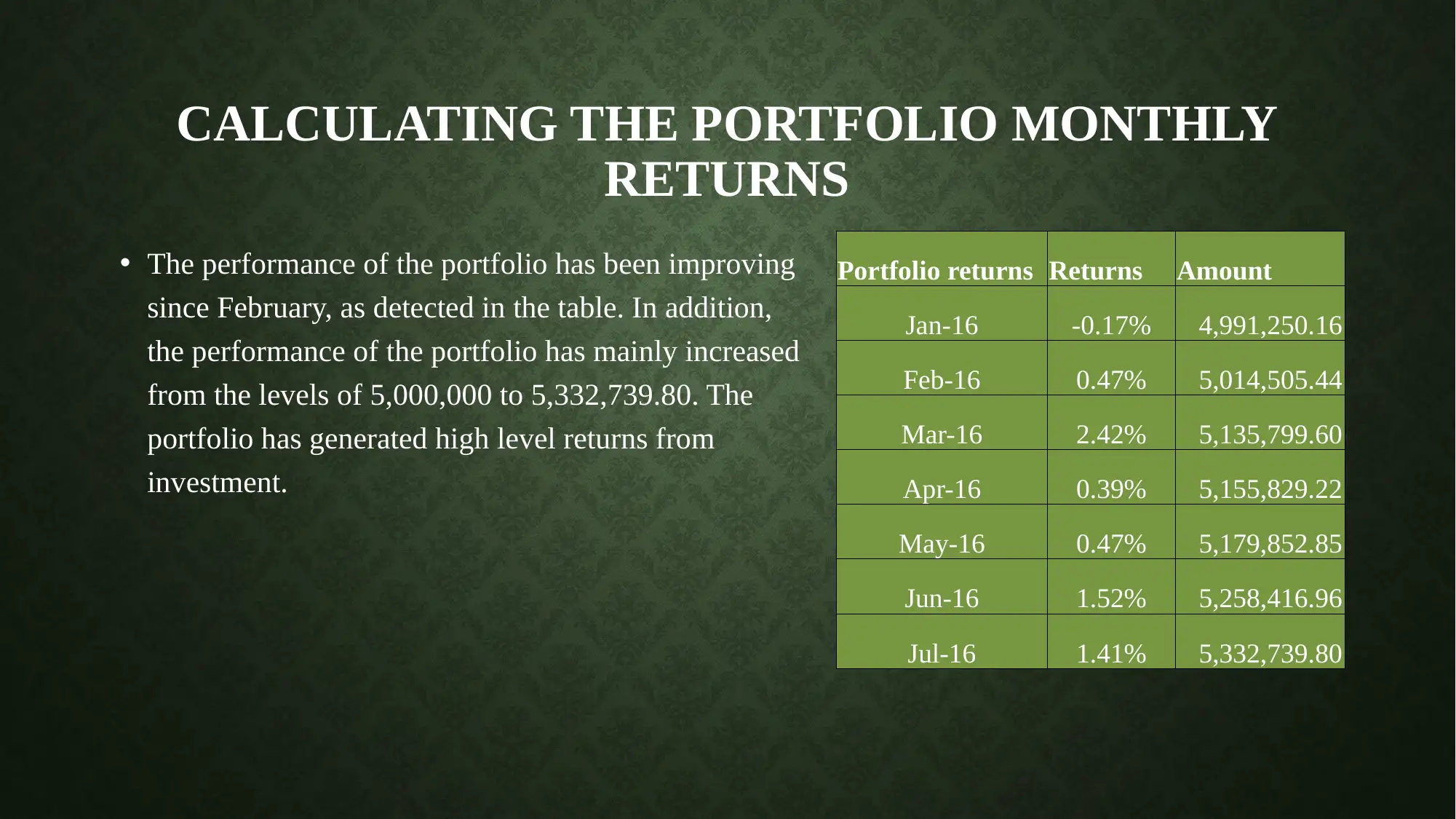

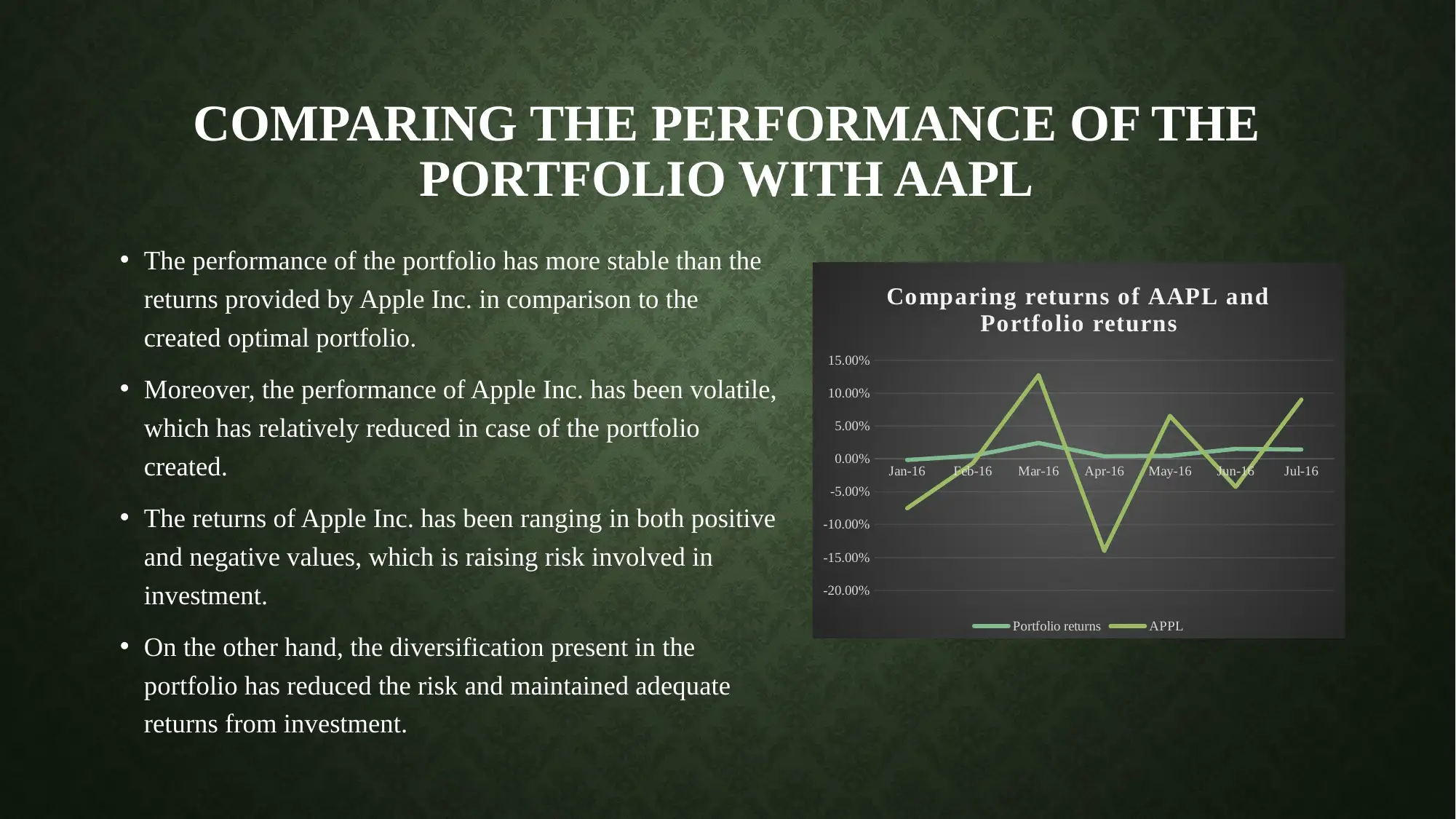

This finance project evaluates the performance of an optimal portfolio, comparing it to Apple Inc. (AAPL) to demonstrate the benefits of diversification. The analysis includes the creation of both minimum variance and optimal portfolios using assets like Vanguard Total Bond Market Index Fund and Vanguard 500 Index. The project calculates monthly returns, compares portfolio stability with AAPL's volatility, and highlights how diversification reduces risk and enhances returns. The conclusion emphasizes the importance of strategic asset allocation in generating income and mitigating risk. The project also involves creating a presentation for potential clients, illustrating portfolio diversification through graphs and comparisons, based on the capstone project steps. This assignment is designed to showcase the ability to analyze portfolio characteristics and communicate its performance effectively.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.