Financial Portfolio Analysis: Sharpe Ratio Calculations and Rankings

VerifiedAdded on 2020/01/28

|9

|1063

|69

Project

AI Summary

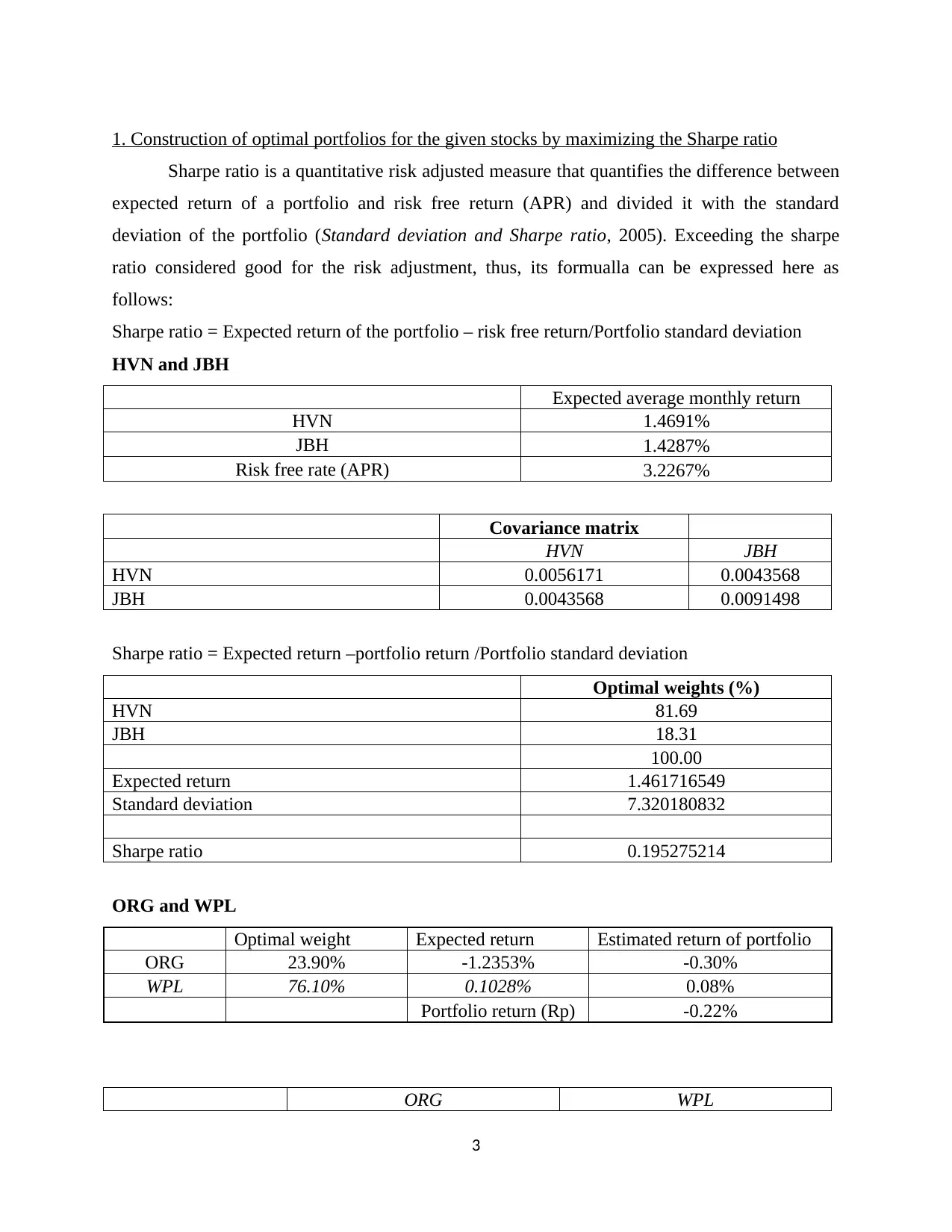

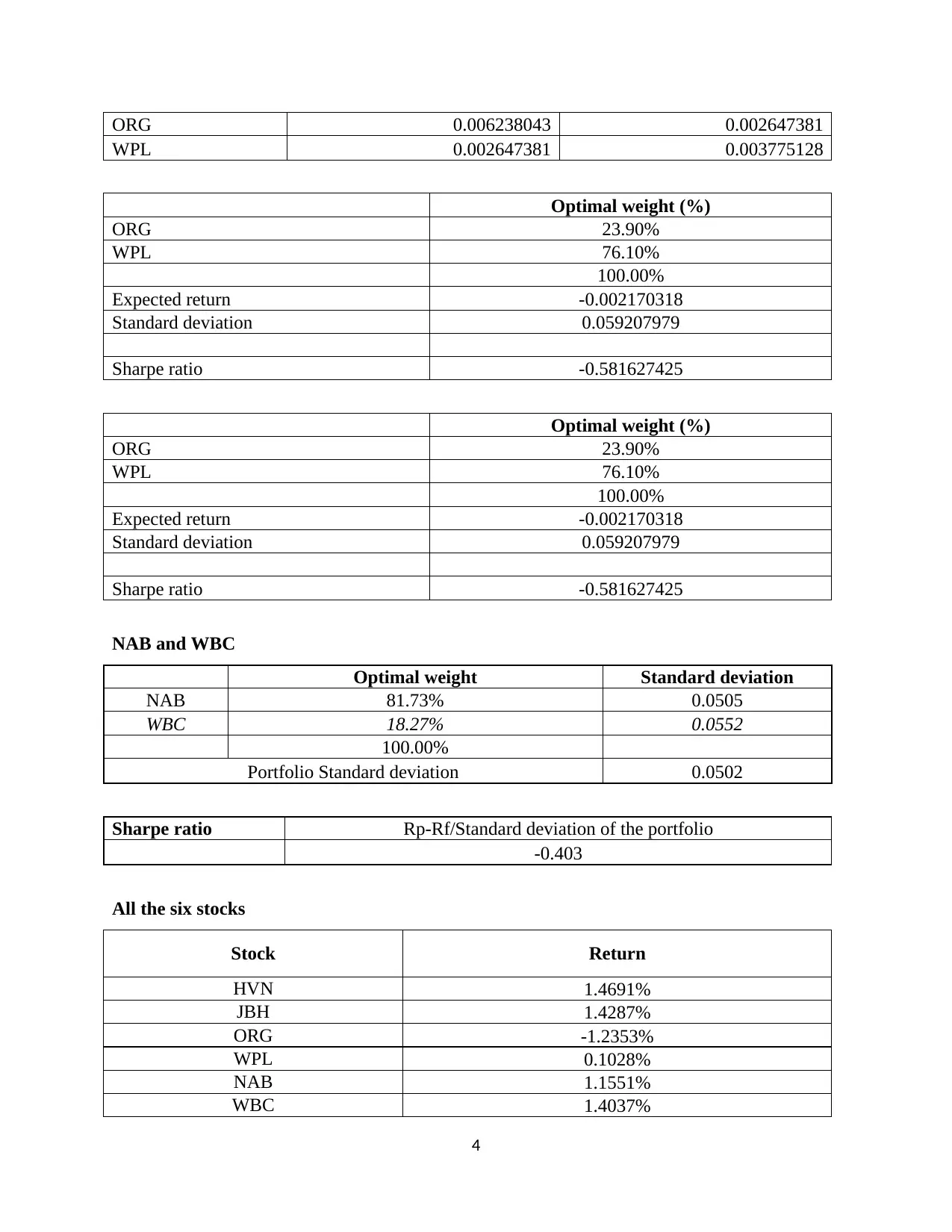

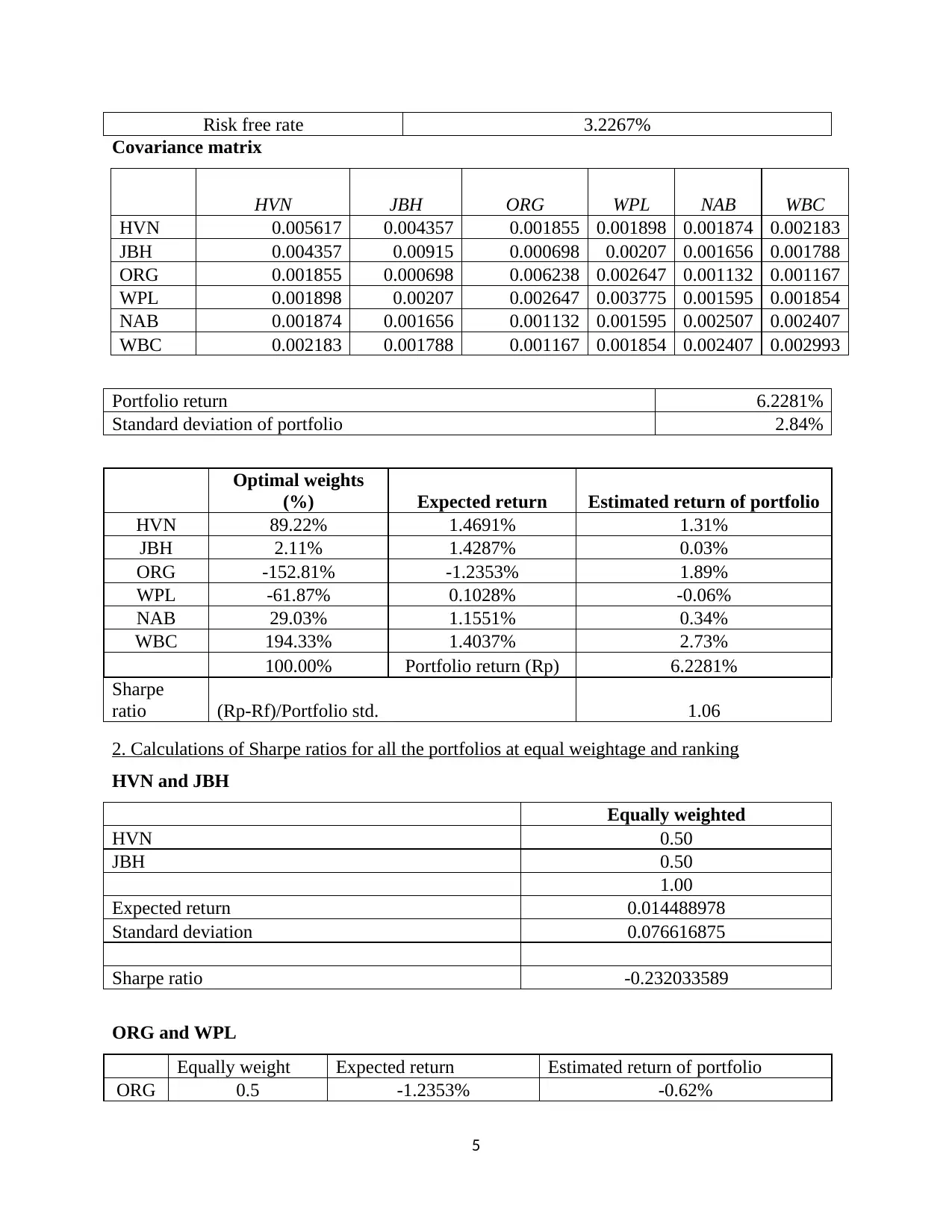

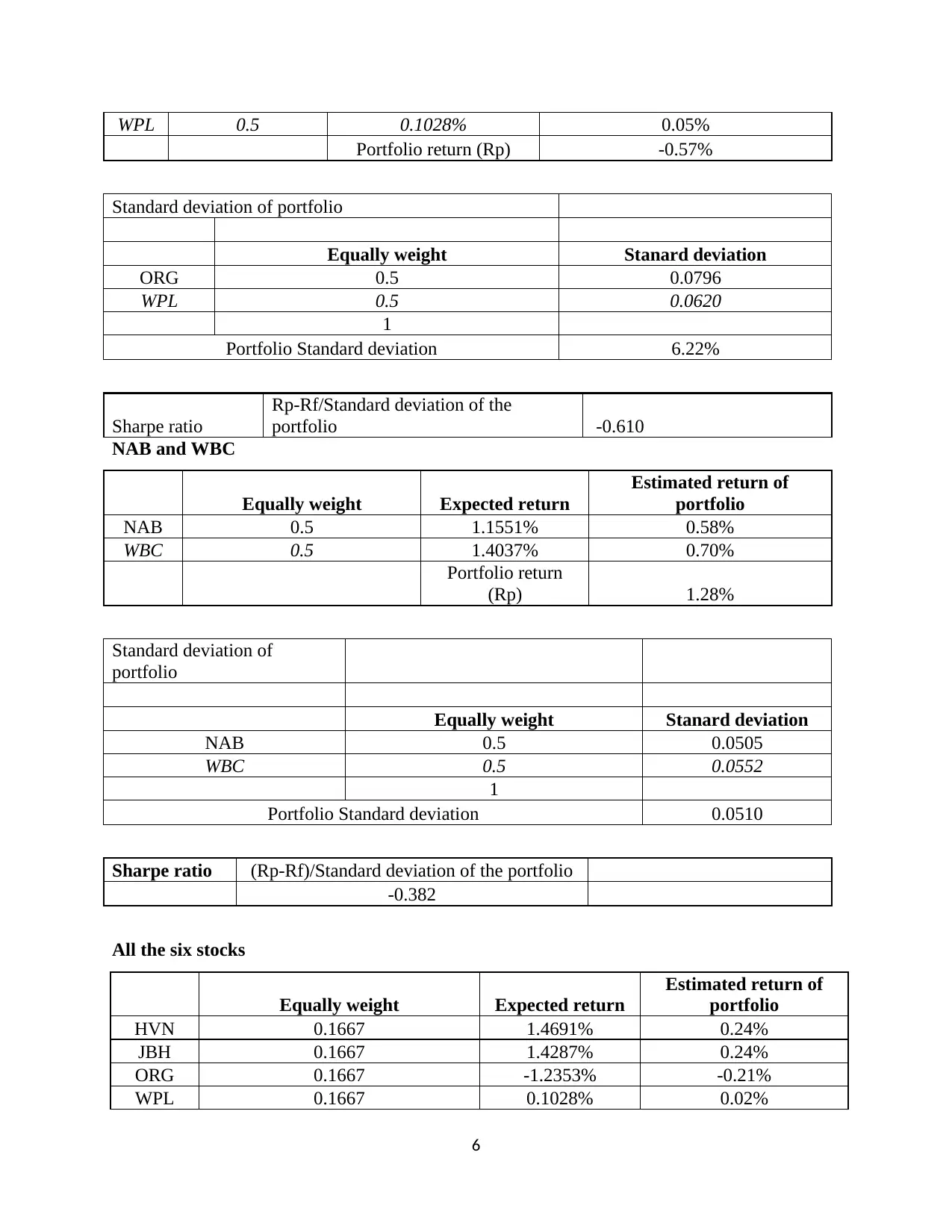

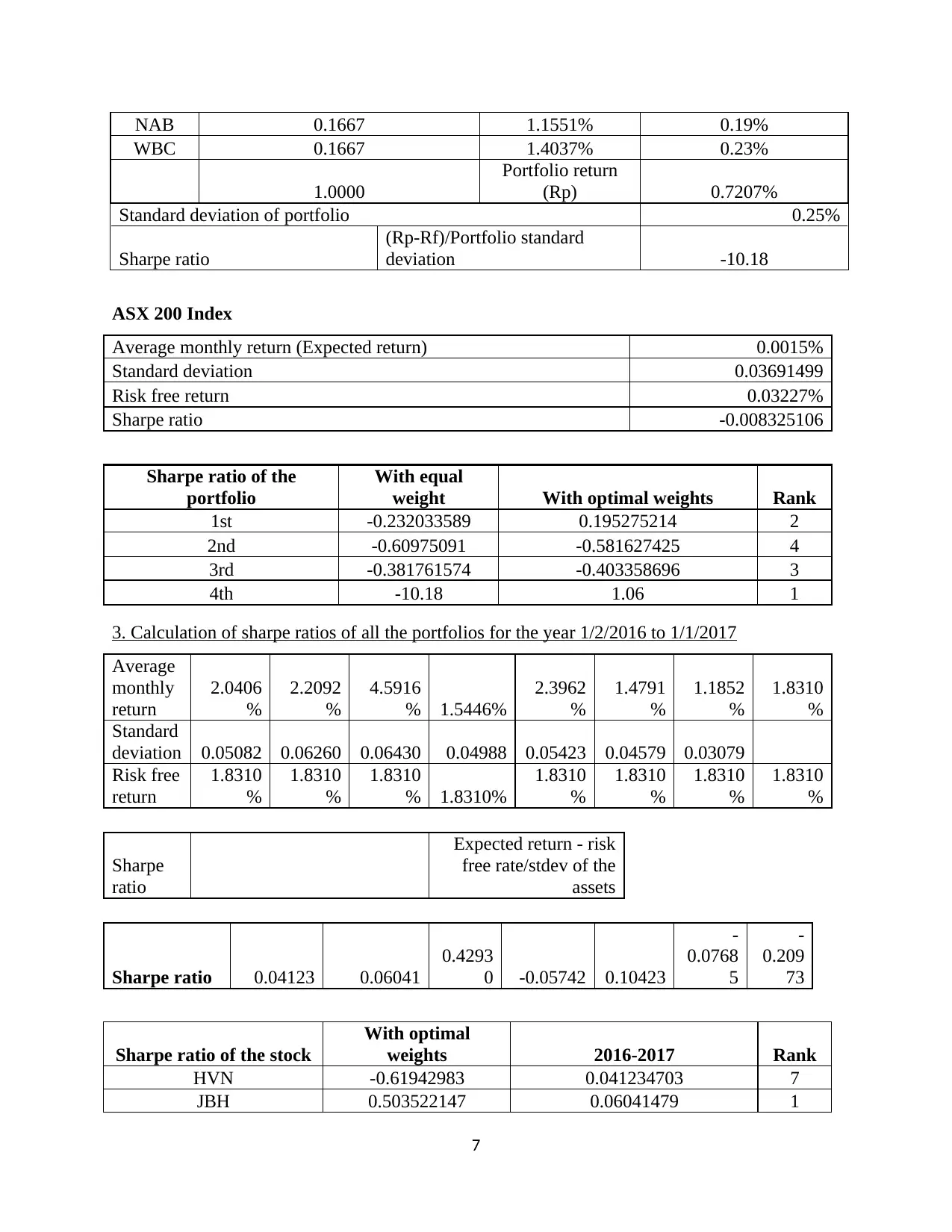

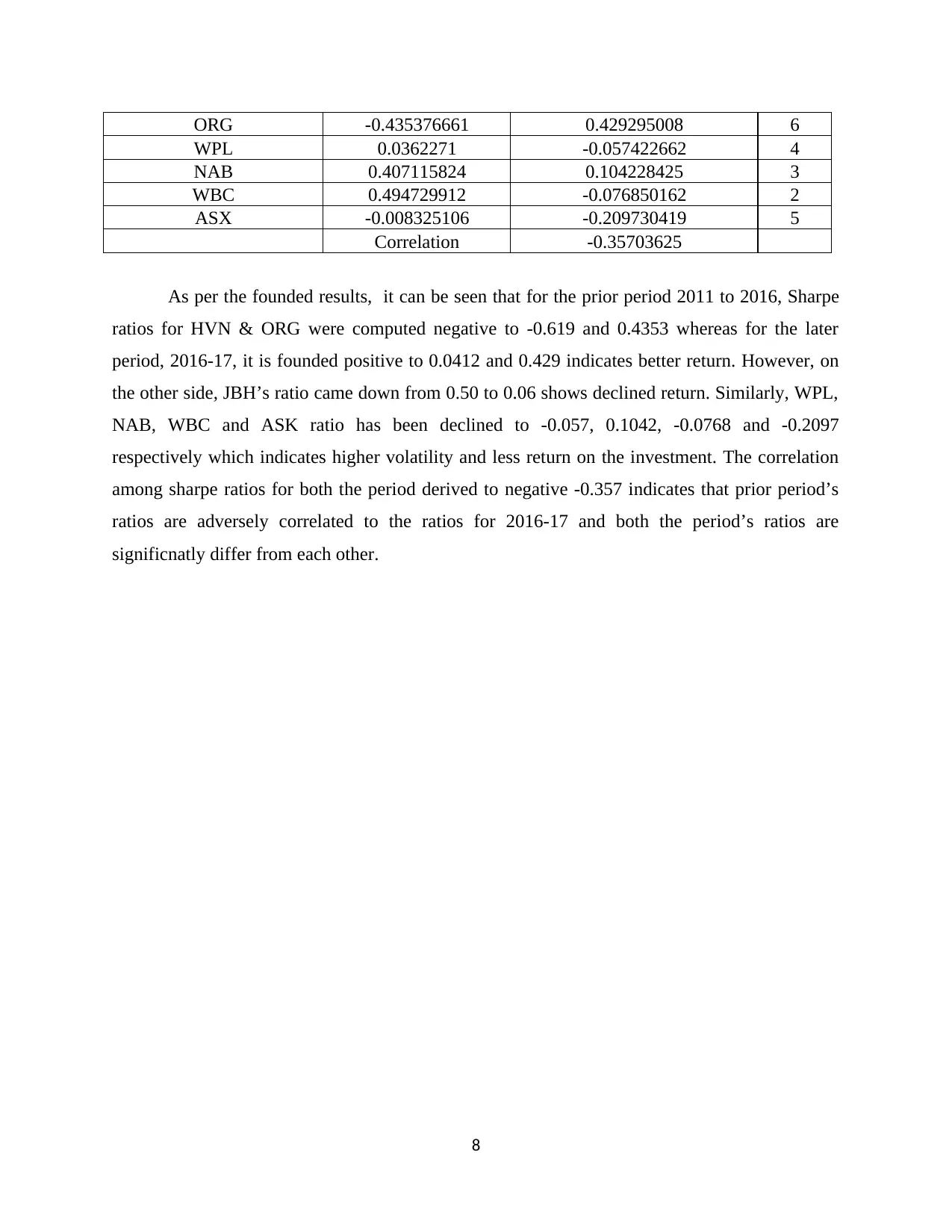

This project undertakes a comprehensive financial portfolio analysis, focusing on the application of the Sharpe ratio as a key metric for assessing risk-adjusted returns. The analysis involves constructing optimal portfolios for given stocks by maximizing the Sharpe ratio, calculating Sharpe ratios for various portfolios under different weighting schemes (equal and optimal), and ranking the portfolios based on their performance. The project also includes calculations of Sharpe ratios for the period from 1/2/2016 to 1/1/2017, providing insights into the performance of the portfolios over time. The methodology encompasses the use of expected average monthly returns, risk-free rates, and covariance matrices to determine optimal weights and evaluate portfolio efficiency. The results highlight the importance of the Sharpe ratio in investment decision-making, demonstrating how it can be used to compare and rank portfolios based on their risk-adjusted returns. The project also includes an analysis of the ASX 200 index and a comparison of Sharpe ratios across different time periods, revealing correlations and changes in portfolio performance.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.