Optimizing Investment Portfolios: Risk, Return, and Asset Allocation

VerifiedAdded on 2023/06/11

|3

|783

|325

Homework Assignment

AI Summary

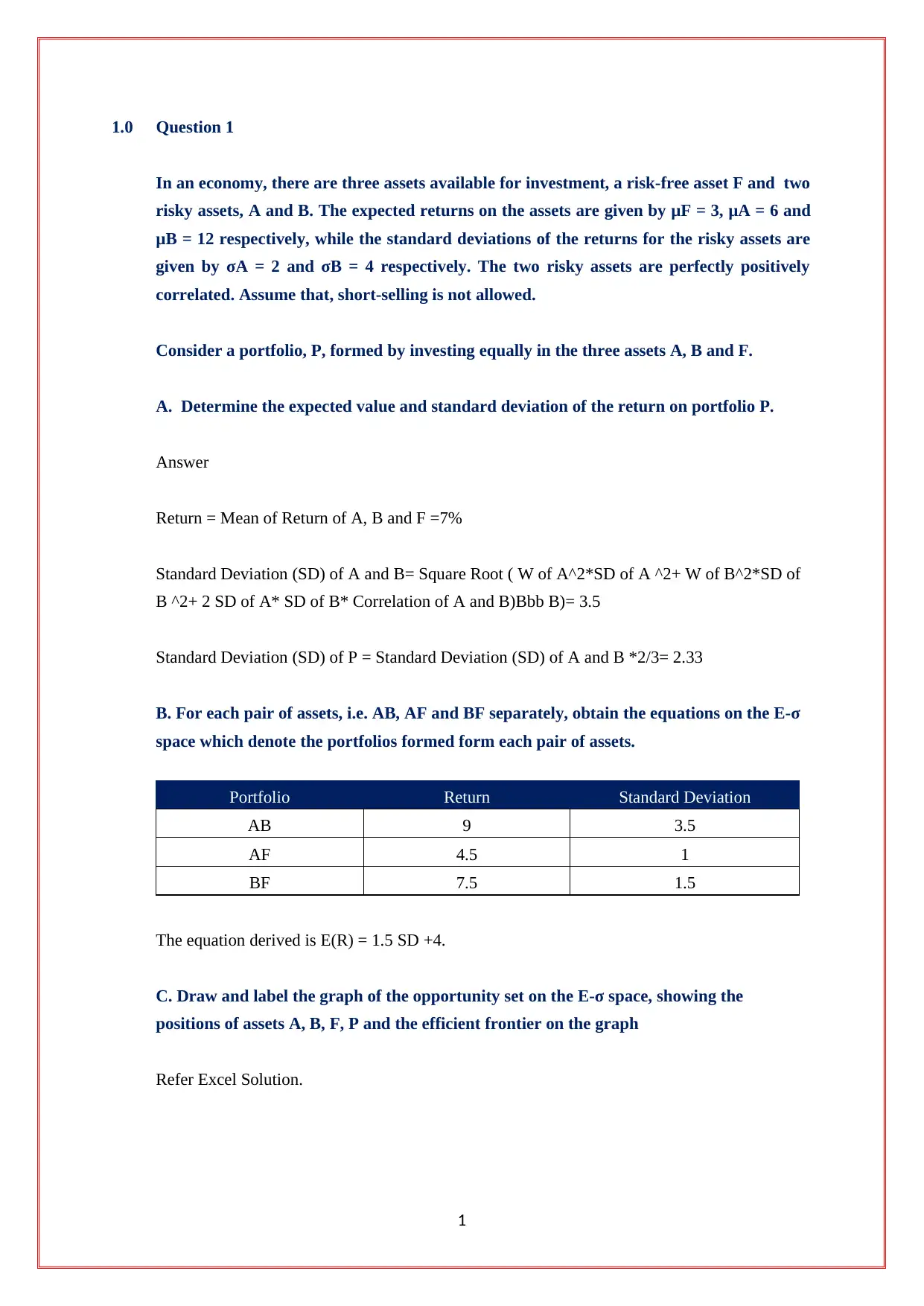

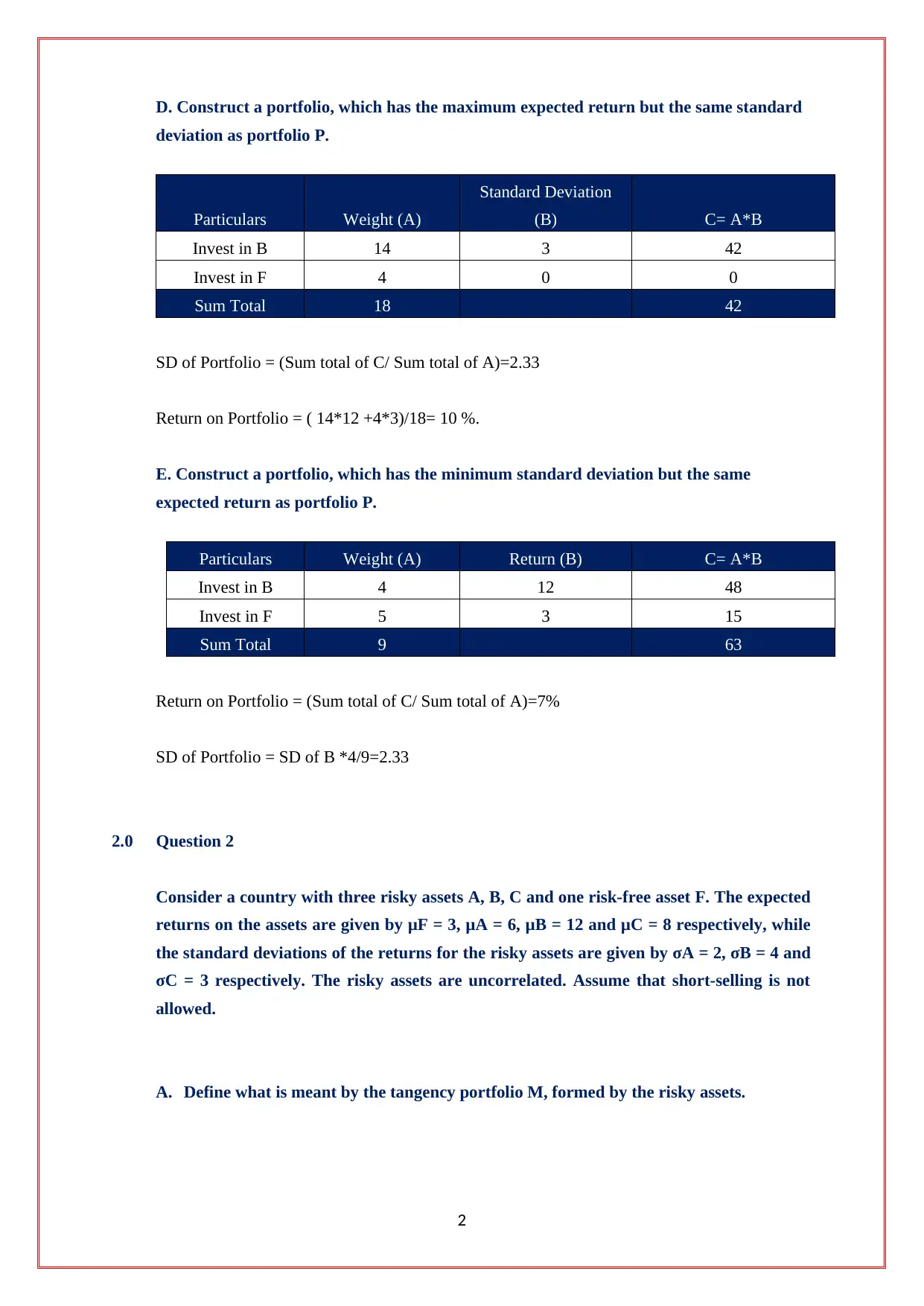

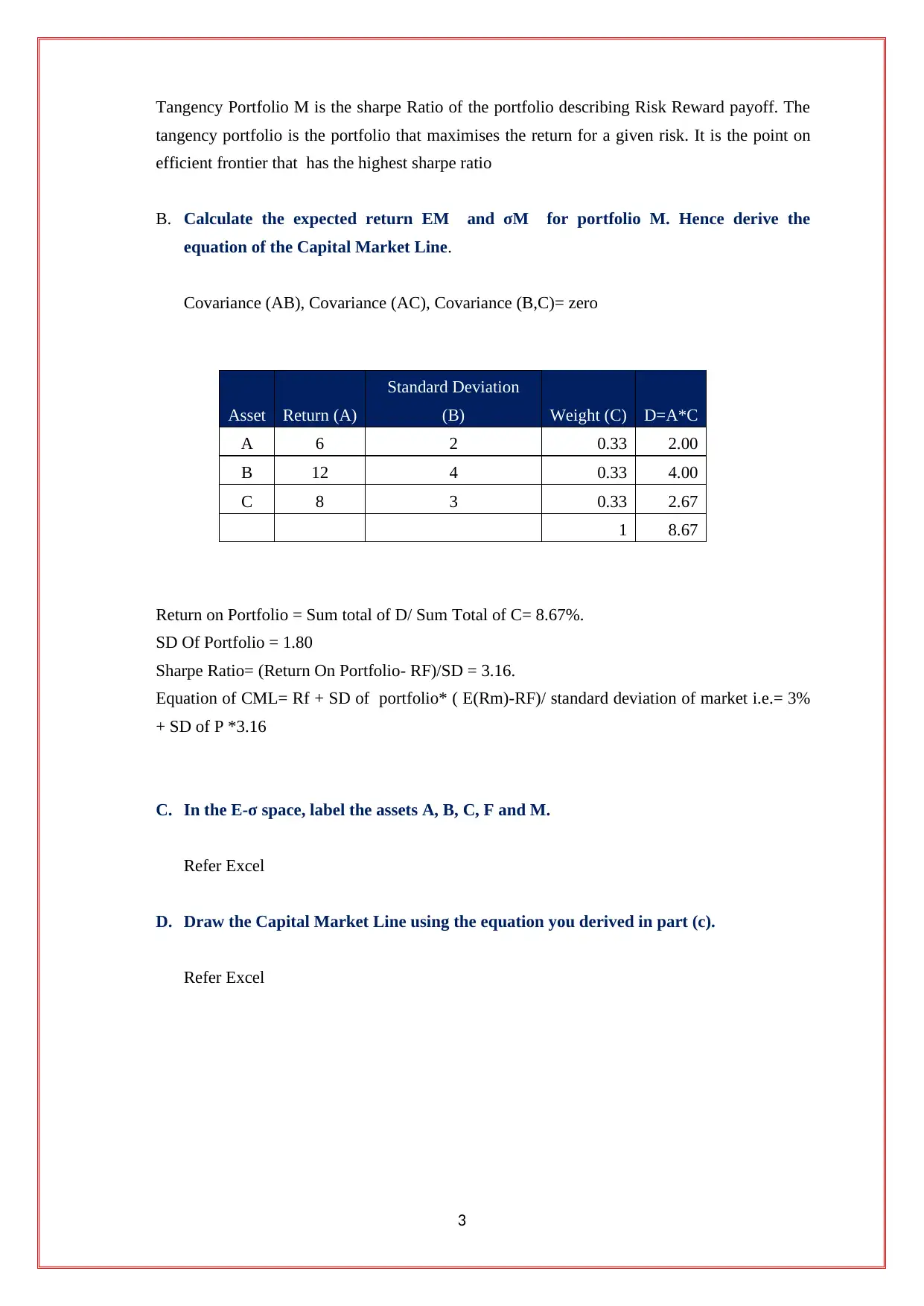

This assignment delves into the principles of portfolio construction and optimization within a financial context. It examines the interplay between risk-free and risky assets, focusing on calculating expected returns and standard deviations for various portfolio compositions. The assignment addresses key concepts such as the Capital Market Line and efficient frontier, illustrating how to construct portfolios that maximize return for a given level of risk or minimize risk for a target return. Through calculations and graphical representations, it explores different asset combinations and their impact on portfolio performance, providing a comprehensive understanding of investment strategies and risk management techniques. The solution includes calculations for portfolio returns, standard deviations, and Sharpe ratios, demonstrating how to determine the optimal portfolio allocation based on risk-reward trade-offs. It also defines the tangency portfolio and its role in maximizing the Sharpe Ratio.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.