Optus Company: Analysis of Inventory Accounting and Cost Management

VerifiedAdded on 2020/04/07

|7

|1518

|40

Report

AI Summary

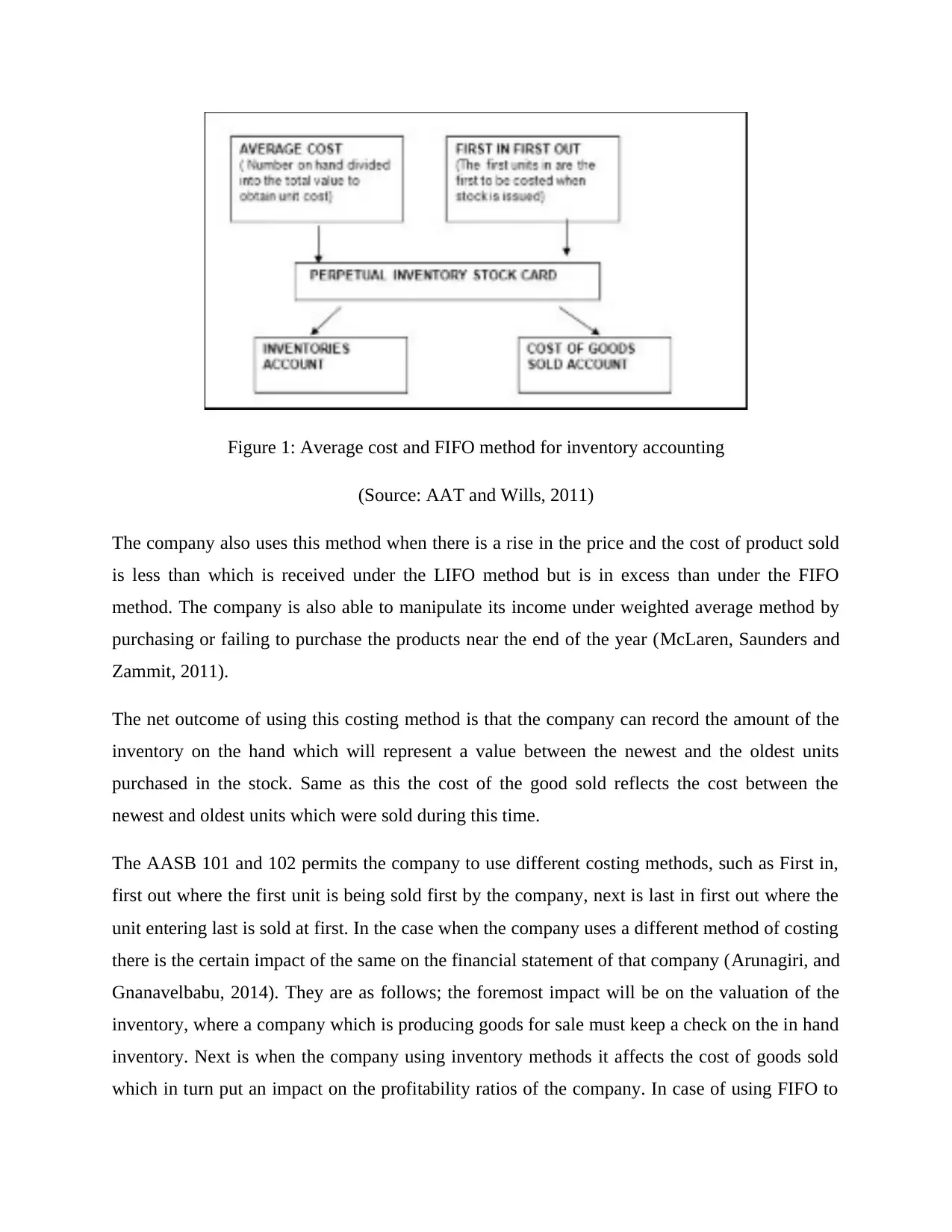

This report provides an in-depth analysis of Optus Pty Ltd's inventory accounting and cost management practices, focusing on the principles outlined in AASB 101 and 102. The study evaluates Optus's use of the weighted average method for inventory valuation, the perpetual inventory system, and the impact of these methods on the company's financial statements. It examines how Optus complies with regulatory norms, including disclosures in its annual reports. The report also discusses the implications of different costing methods, such as FIFO and LIFO, on inventory valuation, cost of goods sold, and profitability ratios. The analysis covers key aspects like work in progress, trade receivables and payables, and the recognition of potential contract losses. The report concludes that Optus adheres to all regulatory standards concerning inventory accounting and cost management, providing appropriate disclosures within its financial statements.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.