Analysis of Optus's Cash Flow, Income, and Tax Accounting Practices

VerifiedAdded on 2021/05/31

|13

|3093

|21

Report

AI Summary

This report provides a comprehensive analysis of Optus's financial statements, focusing on cash flow, other comprehensive income, and corporate income tax. The analysis begins with an examination of the cash flow statement, highlighting changes in operating, investing, and financing activities over a three-year period. It then delves into the components of other comprehensive income, including cash flow hedges and the impact of exchange rate changes. Finally, the report explores Optus's accounting for corporate income, including current and deferred income tax expenses, deferred tax assets and liabilities, and the differences between tax payable and tax expense. The report emphasizes the importance of these financial elements in understanding Optus's overall financial performance and strategic decisions. The report highlights the impact of changes in financial activities such as income tax paid, dividends, investments, and loans, and the effect of deferred tax assets and liabilities.

Running head: CORPORATE ACCOUNTING

Name of the Student

Name of the University

Author note

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Table of Contents

Part A:........................................................................................................................................2

Cash flow Statement:.............................................................................................................2

Part B:.........................................................................................................................................4

Other Comprehensive Income Statements:............................................................................4

Part C:.........................................................................................................................................6

Accounting for Corporate Income:........................................................................................6

References:...............................................................................................................................10

Table of Contents

Part A:........................................................................................................................................2

Cash flow Statement:.............................................................................................................2

Part B:.........................................................................................................................................4

Other Comprehensive Income Statements:............................................................................4

Part C:.........................................................................................................................................6

Accounting for Corporate Income:........................................................................................6

References:...............................................................................................................................10

2CORPORATE ACCOUNTING

Part A:

Cash flow Statement:

i) Cash flow statement forms the integral part of any company’s financial

statement analysis. It is the statement which provides all the information about

the different cash related activities of the company. In a way it is regarded as

the financial heart-beat of any company, as cash is regarded as one of the most

important aspects of any company’s success (Bhandari and Iyer, 2013). In the

case of Optus, many significant ingredients have become a part of any

company. In the cash flow from operating activities, there are dividends

received from joint ventures, income tax paid, dividends which have been

received from the associates. In the case of the operating activities, investment

in joint ventures and associates, payment for the purchase of plant and

machinery have been present, purchase of intangible assets, investments in

AFS investments, payment for acquisition of non-controlling interest,

proceeds from the sale of investments, proceeds from capital reduction,

proceeds from the sale of property and from capital reduction are some of the

most prominent parts of the operating activities of the telephone company.

In the case of the financing activities, there are plenty items which require a

special mention, as there are a whole lot of items present in the financial activities

of the company. Proceeds from the term loans, bond issue, finance lease liabilities,

net proceeds from borrowings, settlement of swap bonds, purchase of performance

shares, dividend paid to non-controlling interest are some of the most important

part of the financing activities of Optus.

Part A:

Cash flow Statement:

i) Cash flow statement forms the integral part of any company’s financial

statement analysis. It is the statement which provides all the information about

the different cash related activities of the company. In a way it is regarded as

the financial heart-beat of any company, as cash is regarded as one of the most

important aspects of any company’s success (Bhandari and Iyer, 2013). In the

case of Optus, many significant ingredients have become a part of any

company. In the cash flow from operating activities, there are dividends

received from joint ventures, income tax paid, dividends which have been

received from the associates. In the case of the operating activities, investment

in joint ventures and associates, payment for the purchase of plant and

machinery have been present, purchase of intangible assets, investments in

AFS investments, payment for acquisition of non-controlling interest,

proceeds from the sale of investments, proceeds from capital reduction,

proceeds from the sale of property and from capital reduction are some of the

most prominent parts of the operating activities of the telephone company.

In the case of the financing activities, there are plenty items which require a

special mention, as there are a whole lot of items present in the financial activities

of the company. Proceeds from the term loans, bond issue, finance lease liabilities,

net proceeds from borrowings, settlement of swap bonds, purchase of performance

shares, dividend paid to non-controlling interest are some of the most important

part of the financing activities of Optus.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

Changes:

When the period of three years are considered, then some real changes have

been seen in all the three activities which constitute the part of the cash flow

statements. In the case of operating activities, notable changes have been seen in

case of the income tax paid, from $598 million to $834 million. Dividend received

from joint ventures has increased from $ 1215 to $1656 million. In the same way,

there have been few changes in the arena of finance activities too. Payment for

acquisition of subsidiaries have decreased considerably specially in the year 2017,

from $450 million to $ 1059 million to absolutely nil in the year 2017, which

suggests that the company has put all its expansion activities presently on hold.

Similarly, the company has also decreased the purchase of intangible assets. It was

$966 million in 2015 and it decreased to $173 million (Optus, 2018). In the case

of the financing activities, a significant amount of changes could be seen,

particularly, in the case of term loans and bond issue, some notable changes have

been seen across the span of the last three years. Proceeds from term loans have

increased considerably across the span of three years from $4915 in 2015, to

$5850 in 2016 to $6175 million in the year 2017. This continuous trend reveals an

important fact for the telecom giant, that the company has become overly

dependent on the presence of these kinds of term loans.

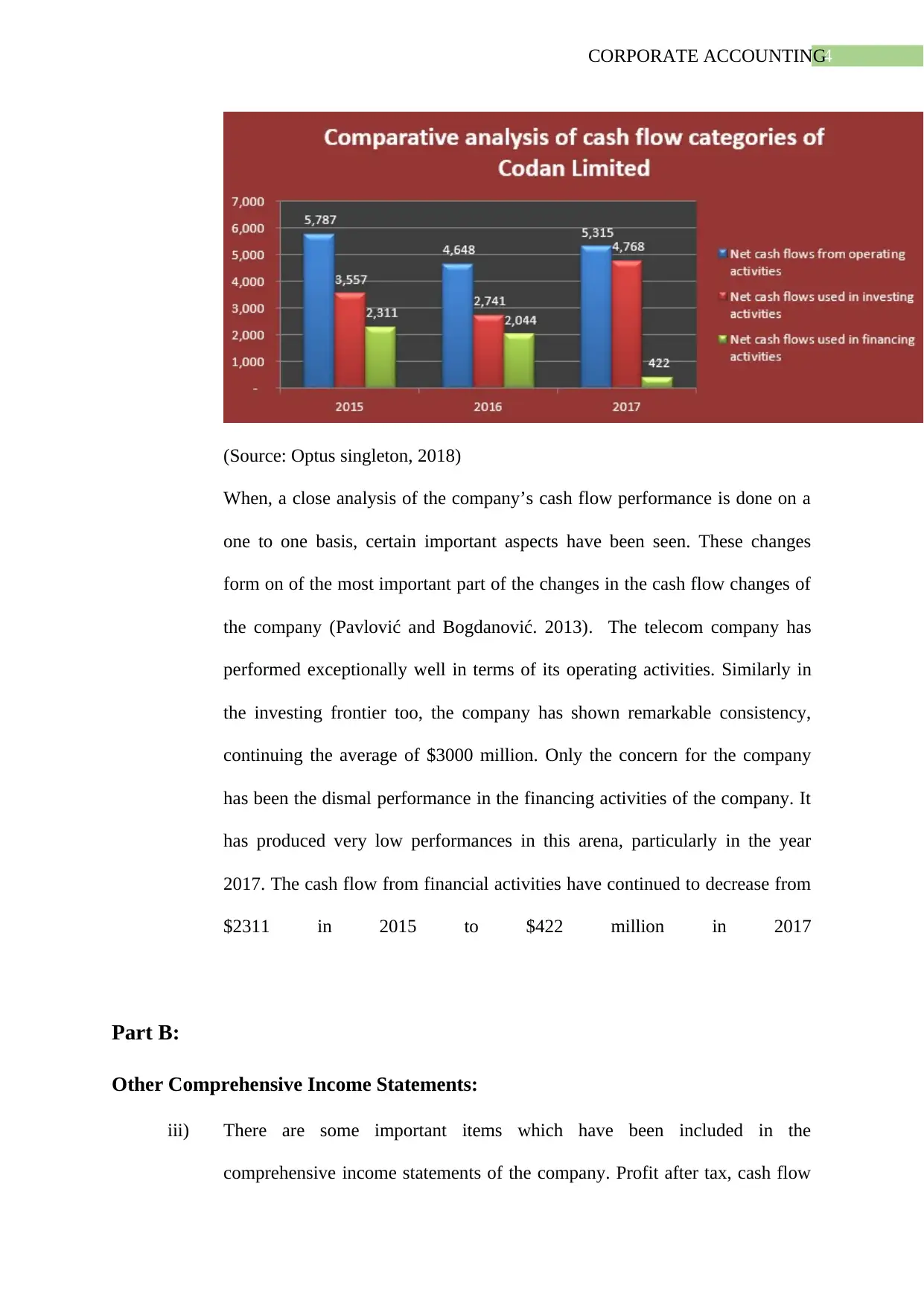

ii) A comparative analysis of the company’s cash flow activity, with a

diagrammatic presentation of the cash flow activities have been presented

below:

Changes:

When the period of three years are considered, then some real changes have

been seen in all the three activities which constitute the part of the cash flow

statements. In the case of operating activities, notable changes have been seen in

case of the income tax paid, from $598 million to $834 million. Dividend received

from joint ventures has increased from $ 1215 to $1656 million. In the same way,

there have been few changes in the arena of finance activities too. Payment for

acquisition of subsidiaries have decreased considerably specially in the year 2017,

from $450 million to $ 1059 million to absolutely nil in the year 2017, which

suggests that the company has put all its expansion activities presently on hold.

Similarly, the company has also decreased the purchase of intangible assets. It was

$966 million in 2015 and it decreased to $173 million (Optus, 2018). In the case

of the financing activities, a significant amount of changes could be seen,

particularly, in the case of term loans and bond issue, some notable changes have

been seen across the span of the last three years. Proceeds from term loans have

increased considerably across the span of three years from $4915 in 2015, to

$5850 in 2016 to $6175 million in the year 2017. This continuous trend reveals an

important fact for the telecom giant, that the company has become overly

dependent on the presence of these kinds of term loans.

ii) A comparative analysis of the company’s cash flow activity, with a

diagrammatic presentation of the cash flow activities have been presented

below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

(Source: Optus singleton, 2018)

When, a close analysis of the company’s cash flow performance is done on a

one to one basis, certain important aspects have been seen. These changes

form on of the most important part of the changes in the cash flow changes of

the company (Pavlović and Bogdanović. 2013). The telecom company has

performed exceptionally well in terms of its operating activities. Similarly in

the investing frontier too, the company has shown remarkable consistency,

continuing the average of $3000 million. Only the concern for the company

has been the dismal performance in the financing activities of the company. It

has produced very low performances in this arena, particularly in the year

2017. The cash flow from financial activities have continued to decrease from

$2311 in 2015 to $422 million in 2017

Part B:

Other Comprehensive Income Statements:

iii) There are some important items which have been included in the

comprehensive income statements of the company. Profit after tax, cash flow

(Source: Optus singleton, 2018)

When, a close analysis of the company’s cash flow performance is done on a

one to one basis, certain important aspects have been seen. These changes

form on of the most important part of the changes in the cash flow changes of

the company (Pavlović and Bogdanović. 2013). The telecom company has

performed exceptionally well in terms of its operating activities. Similarly in

the investing frontier too, the company has shown remarkable consistency,

continuing the average of $3000 million. Only the concern for the company

has been the dismal performance in the financing activities of the company. It

has produced very low performances in this arena, particularly in the year

2017. The cash flow from financial activities have continued to decrease from

$2311 in 2015 to $422 million in 2017

Part B:

Other Comprehensive Income Statements:

iii) There are some important items which have been included in the

comprehensive income statements of the company. Profit after tax, cash flow

5CORPORATE ACCOUNTING

hedges, exchange differences which are arising from the translation of foreign

operations and the various other translation differences. Mainly in the part of

the cash flow hedges, the fair value changes during the years have been

extensively mentioned (accaglobal.com, 2018). The total comprehensive

income has also been obviously mentioned in the comprehensive income

statement, as this is one of the most important aspects of the entire

comprehensive income statement of the company.

iv) A vivid understanding of all these items have been presented below:

Cash Flow hedge: It is used when a business entity is aiming to reduce or limit the exposure

which arises from the frequent changes and fluctuations in the cash flow of any financial

asset or liability. This happens due to changes in a particular kind of risk such as interest rate

risk or any kind of floating rate debt instruments. The hedging instrument is measured at fair

value in order to properly gauge and mitigate the different kinds of risks associated with them

(Hoyle, Schaefer, and Doupnik, 2015). Only the risk associated with the particular assets or

liabilities or any kind of future or forecasted transaction, are hedged upon. In the entire

procedure of hedging, most important the hedging item is to be chosen and after that the

hedging procedures are taken care of.

Changes due to exchange rates: When any company has trading partners or branches

abroad, then in such cases the transaction conducted with these foreign based branches are

impacted due to the changes in the foreign exchange rates. The effects of changes in the

foreign exchange rates helps in outlining the foreign currency transaction and operations in

the financial statements. In this regard, each economic entity, like any business entity, has to

determine a functional currency, which is completely based on the initial economic

environment on which it actually operates and as a result of which the measurement of the

foreign currency transactions could be made possible.

hedges, exchange differences which are arising from the translation of foreign

operations and the various other translation differences. Mainly in the part of

the cash flow hedges, the fair value changes during the years have been

extensively mentioned (accaglobal.com, 2018). The total comprehensive

income has also been obviously mentioned in the comprehensive income

statement, as this is one of the most important aspects of the entire

comprehensive income statement of the company.

iv) A vivid understanding of all these items have been presented below:

Cash Flow hedge: It is used when a business entity is aiming to reduce or limit the exposure

which arises from the frequent changes and fluctuations in the cash flow of any financial

asset or liability. This happens due to changes in a particular kind of risk such as interest rate

risk or any kind of floating rate debt instruments. The hedging instrument is measured at fair

value in order to properly gauge and mitigate the different kinds of risks associated with them

(Hoyle, Schaefer, and Doupnik, 2015). Only the risk associated with the particular assets or

liabilities or any kind of future or forecasted transaction, are hedged upon. In the entire

procedure of hedging, most important the hedging item is to be chosen and after that the

hedging procedures are taken care of.

Changes due to exchange rates: When any company has trading partners or branches

abroad, then in such cases the transaction conducted with these foreign based branches are

impacted due to the changes in the foreign exchange rates. The effects of changes in the

foreign exchange rates helps in outlining the foreign currency transaction and operations in

the financial statements. In this regard, each economic entity, like any business entity, has to

determine a functional currency, which is completely based on the initial economic

environment on which it actually operates and as a result of which the measurement of the

foreign currency transactions could be made possible.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

v) There are certain items which are not regularly shown in the income statement

of the company, these items although form an integral part of any company’s

overall operations. As mentioned above, items such as cash flow hedge funds

and translation reserves for foreign items transactions are not included in the

income statement of the company, on the contrary, they are included in the

other comprehensive income statement. One of the major reasons for this is

the fact that, only those items are included in the other comprehensive income

statement which have not yet been realized. A transaction has been realised,

when the related transaction has been completed, then such an investment is

regarded as sold. Thus, if the company has invested in any bond, then the

value of these bonds changes, which would either be recognised as either loss

or gain for the company. Once the selling of these bonds is complete, then this

gain or loss can be taken out of the other comprehensive income statement,

and can be put into the income statement of the company. This signifies the

realisation of the various different transactions.

Part C:

Accounting for Corporate Income:

vi) In the case of income tax, Optus has some significant amount of contribution

in terms of tax towards the government of its operating countries. The current

income tax expense of the company is basically divided into two portions, one

is the current income tax and the deferred income tax. The current tax for the

year 2017, was $235.7 million, which was $239.6 million in 2016 and the

deferred income tax for the same duration was $299.4 million and $365.8

million respectively (Optus.com.au, 2018). Thus the total income tax expense

for the year was $535.1 million in 2017 and $596.4 million in the year 2016.

v) There are certain items which are not regularly shown in the income statement

of the company, these items although form an integral part of any company’s

overall operations. As mentioned above, items such as cash flow hedge funds

and translation reserves for foreign items transactions are not included in the

income statement of the company, on the contrary, they are included in the

other comprehensive income statement. One of the major reasons for this is

the fact that, only those items are included in the other comprehensive income

statement which have not yet been realized. A transaction has been realised,

when the related transaction has been completed, then such an investment is

regarded as sold. Thus, if the company has invested in any bond, then the

value of these bonds changes, which would either be recognised as either loss

or gain for the company. Once the selling of these bonds is complete, then this

gain or loss can be taken out of the other comprehensive income statement,

and can be put into the income statement of the company. This signifies the

realisation of the various different transactions.

Part C:

Accounting for Corporate Income:

vi) In the case of income tax, Optus has some significant amount of contribution

in terms of tax towards the government of its operating countries. The current

income tax expense of the company is basically divided into two portions, one

is the current income tax and the deferred income tax. The current tax for the

year 2017, was $235.7 million, which was $239.6 million in 2016 and the

deferred income tax for the same duration was $299.4 million and $365.8

million respectively (Optus.com.au, 2018). Thus the total income tax expense

for the year was $535.1 million in 2017 and $596.4 million in the year 2016.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

vii) If the analysis of the income tax expense is done, then some significant

differences could be found. As per the Australian tax rate of 30%, the tax

payable for the year is $1354 million (4515*30%) for the year 2017, which is

actually different from the total income tax actually charged for the year 2017,

which was $535.1 million. This difference exists because of the presence of

presence of the deferred tax assets and liabilities which are present in the

income statement of the company. Another significant item which is the cause

of this difference is the presence of different kinds of depreciation methods

which have been adopted by the companies.

viii) The deferred tax asset of the group for the year 2017 is $657. 8, which was

$692.3 million in the year 2016. The deferred tax liability of the company is

$574 for the year 2017, which was $585.3 million in 2016.

The deferred tax assets of any company is an important strategic invention. When the

business entity has overpaid taxes or has paid the taxes in advance, then as a result of which

the taxes are returned to the company in one way or the other in the form of various kinds of

tax relief. In the same way, the significance of the deferred tax liability cannot be ignored

altogether (Henderson et al., 2015). The significance of the deferred tax liability of any

company is more than that of the deferred tax assets for any company. The amount of income

tax which remain underpaid on the part of the company, which would be ultimately be paid in

the future is known as the deferred tax liability. By doing this, the company doesn’t necessary

fail to fulfil its tax obligations, on the contrary, the company has only transferred or rather

postponed its payment of the tax liabilities for a later date in the future. This is actually done

in order to prevent the payment of the income tax which otherwise would have to be paid for

the income which is earned for the given time period (Watson, 2018). A vivid example of the

deferred tax liability has been provided below:

vii) If the analysis of the income tax expense is done, then some significant

differences could be found. As per the Australian tax rate of 30%, the tax

payable for the year is $1354 million (4515*30%) for the year 2017, which is

actually different from the total income tax actually charged for the year 2017,

which was $535.1 million. This difference exists because of the presence of

presence of the deferred tax assets and liabilities which are present in the

income statement of the company. Another significant item which is the cause

of this difference is the presence of different kinds of depreciation methods

which have been adopted by the companies.

viii) The deferred tax asset of the group for the year 2017 is $657. 8, which was

$692.3 million in the year 2016. The deferred tax liability of the company is

$574 for the year 2017, which was $585.3 million in 2016.

The deferred tax assets of any company is an important strategic invention. When the

business entity has overpaid taxes or has paid the taxes in advance, then as a result of which

the taxes are returned to the company in one way or the other in the form of various kinds of

tax relief. In the same way, the significance of the deferred tax liability cannot be ignored

altogether (Henderson et al., 2015). The significance of the deferred tax liability of any

company is more than that of the deferred tax assets for any company. The amount of income

tax which remain underpaid on the part of the company, which would be ultimately be paid in

the future is known as the deferred tax liability. By doing this, the company doesn’t necessary

fail to fulfil its tax obligations, on the contrary, the company has only transferred or rather

postponed its payment of the tax liabilities for a later date in the future. This is actually done

in order to prevent the payment of the income tax which otherwise would have to be paid for

the income which is earned for the given time period (Watson, 2018). A vivid example of the

deferred tax liability has been provided below:

8CORPORATE ACCOUNTING

A very common source of deferred tax liability is the variance in the depreciation expense

treatment by the different set of tax laws and accounting rules and regulations. The

depreciation expenses for the longer duration of assets for the financial statements purposes is

usually calculated by using a straight-line method, while various different tax rules allow

companies to use an depreciation method. Since the straight-line method produces lower

amount of depreciation when compared to that of the under accelerated method, a company's

accounting income is temporarily higher than its taxable income. The company recognizes

the deferred tax liability on the amount of difference between its accounting earnings before

taxes and taxable income. Later on, as the business entity continues the operation of

depreciating its assets, the difference between straight-line depreciation method and the

accelerated depreciation declines a bit, and the total amount of deferred tax liability is

progressively removed through a series of equipoising various kinds of accounting entries.

Thus deferred tax asset and liabilities form such an important part of any company’s overall

success.

ix) Optus recorded a current tax assets of $395 US$M for the financial year of

2017. The company also reported income tax payable of $535 million for the

financial year of 2017 (Optus, 2018). The income tax which is payable is

different from the income tax expense because the income tax expenses is

what Optus owns in the context of the tax to be paid, based on the standard

accounting rules whereas the income tax payable signifies the actual amount

of the taxes that is owned by the Optus which based upon the different kinds

of tax coding rules (Gao et al., 2015). The current amount of tax represents the

estimated amount of tax on the measureable income during the year, which is

based on the tax rates and the laws adopted during the reporting data whereas

A very common source of deferred tax liability is the variance in the depreciation expense

treatment by the different set of tax laws and accounting rules and regulations. The

depreciation expenses for the longer duration of assets for the financial statements purposes is

usually calculated by using a straight-line method, while various different tax rules allow

companies to use an depreciation method. Since the straight-line method produces lower

amount of depreciation when compared to that of the under accelerated method, a company's

accounting income is temporarily higher than its taxable income. The company recognizes

the deferred tax liability on the amount of difference between its accounting earnings before

taxes and taxable income. Later on, as the business entity continues the operation of

depreciating its assets, the difference between straight-line depreciation method and the

accelerated depreciation declines a bit, and the total amount of deferred tax liability is

progressively removed through a series of equipoising various kinds of accounting entries.

Thus deferred tax asset and liabilities form such an important part of any company’s overall

success.

ix) Optus recorded a current tax assets of $395 US$M for the financial year of

2017. The company also reported income tax payable of $535 million for the

financial year of 2017 (Optus, 2018). The income tax which is payable is

different from the income tax expense because the income tax expenses is

what Optus owns in the context of the tax to be paid, based on the standard

accounting rules whereas the income tax payable signifies the actual amount

of the taxes that is owned by the Optus which based upon the different kinds

of tax coding rules (Gao et al., 2015). The current amount of tax represents the

estimated amount of tax on the measureable income during the year, which is

based on the tax rates and the laws adopted during the reporting data whereas

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

any form of adjustment to the tax payable for Optus is in respect of the

previous accounting years.

x) The income tax expense is not the same, when compared with that of the

income tax which is reflected on the cash flow statement of the company. In

case of the cash flow statement of Optus, the income tax for the year was $

658. 2 million and for the year 2016, was $ 598.2 million. Whereas the

company’s tax expense for the year 2017 was $ 535.1 million and $596

million in the year 2016.

The differences between the two figures primarily exists because of the effects of

income tax on the certain gains and losses which is related to the investing and

financing activities. One more important reason for this huge gap in the two sets of

income taxes is the amount of income tax paid and income tax which is payable

because there are certain accounting transactions that has initiated in the normal day

to day business affairs, as a results of which the final amount of tax determination

remains completely uncertain (Roethke, 2016).

xi) When the overall financial statement analysis of the company is done, certain

important amount of income taxes are analysed in detail. No such abnormality

is seen in the context of the calculation of the income taxes or any kind of

material error calculation, in this regard. Optus, being one of the most

pioneering company which has actually existed in the field of Australian

telecom industry, has always led the market by example. In this regard, the

company has always been very much industrious in terms of the payment of

various kinds of taxes or other expenses, in order to provide an exemplary

behaviour for the other companies to follow. As a result of this, no such kind

of troubles or fraud has been seen from the analysis of the financial statements

any form of adjustment to the tax payable for Optus is in respect of the

previous accounting years.

x) The income tax expense is not the same, when compared with that of the

income tax which is reflected on the cash flow statement of the company. In

case of the cash flow statement of Optus, the income tax for the year was $

658. 2 million and for the year 2016, was $ 598.2 million. Whereas the

company’s tax expense for the year 2017 was $ 535.1 million and $596

million in the year 2016.

The differences between the two figures primarily exists because of the effects of

income tax on the certain gains and losses which is related to the investing and

financing activities. One more important reason for this huge gap in the two sets of

income taxes is the amount of income tax paid and income tax which is payable

because there are certain accounting transactions that has initiated in the normal day

to day business affairs, as a results of which the final amount of tax determination

remains completely uncertain (Roethke, 2016).

xi) When the overall financial statement analysis of the company is done, certain

important amount of income taxes are analysed in detail. No such abnormality

is seen in the context of the calculation of the income taxes or any kind of

material error calculation, in this regard. Optus, being one of the most

pioneering company which has actually existed in the field of Australian

telecom industry, has always led the market by example. In this regard, the

company has always been very much industrious in terms of the payment of

various kinds of taxes or other expenses, in order to provide an exemplary

behaviour for the other companies to follow. As a result of this, no such kind

of troubles or fraud has been seen from the analysis of the financial statements

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

of the company. It has been noted that the company strictly adheres to all the

different accounting policies and norms of the accounting standards of

Australia.

References:

Bhandari, S.B. and Iyer, R., 2013. Predicting business failure using cash flow statement based

measures. Managerial Finance, 39(7), pp.667-676.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial

accounting. Pearson Higher Education AU.

Hoyle, J. B., Schaefer, T., & Doupnik, T. (2015). Advanced accounting. McGraw Hill.

http://www.accaglobal.com, A. (2018). Concepts of profit or loss and other comprehensive

income | P2 Corporate Reporting | ACCA Qualification | Students | ACCA Global. [online]

Accaglobal.com. Available at: http://www.accaglobal.com/in/en/student/exam-support-

resources/professional-exams-study-resources/p2/technical-articles/pl-oci.html [Accessed 20

May 2018].

Johnston, D., & Kutcher, L. (2015). Do stock-based compensation deferred tax assets provide

incremental information about future tax payments?. The Journal of the American Taxation

Association, 38(1), 79-102.

Lombrano, A. and Zanin, L., 2013. IPSAS and local government consolidated financial

statements—proposal for a territorial consolidation method. Public Money & Management,

33(6), pp.429-436.

Mall, C.P. and Singh, A., TAX AND ACCOUNTING ASPECTS OF MERGER &

ACQUISITION. HermeneuticS, p.78.

of the company. It has been noted that the company strictly adheres to all the

different accounting policies and norms of the accounting standards of

Australia.

References:

Bhandari, S.B. and Iyer, R., 2013. Predicting business failure using cash flow statement based

measures. Managerial Finance, 39(7), pp.667-676.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial

accounting. Pearson Higher Education AU.

Hoyle, J. B., Schaefer, T., & Doupnik, T. (2015). Advanced accounting. McGraw Hill.

http://www.accaglobal.com, A. (2018). Concepts of profit or loss and other comprehensive

income | P2 Corporate Reporting | ACCA Qualification | Students | ACCA Global. [online]

Accaglobal.com. Available at: http://www.accaglobal.com/in/en/student/exam-support-

resources/professional-exams-study-resources/p2/technical-articles/pl-oci.html [Accessed 20

May 2018].

Johnston, D., & Kutcher, L. (2015). Do stock-based compensation deferred tax assets provide

incremental information about future tax payments?. The Journal of the American Taxation

Association, 38(1), 79-102.

Lombrano, A. and Zanin, L., 2013. IPSAS and local government consolidated financial

statements—proposal for a territorial consolidation method. Public Money & Management,

33(6), pp.429-436.

Mall, C.P. and Singh, A., TAX AND ACCOUNTING ASPECTS OF MERGER &

ACQUISITION. HermeneuticS, p.78.

11CORPORATE ACCOUNTING

Optus.com.au. (2018). [online] Available at:

https://www.optus.com.au/content/dam/optus/documents/about-us/media-centre/annual-

reports/2016/06/Singtel-Annual-Report-2016.pdf [Accessed 20 May 2018].

Owen, J.R. and Kemp, D., 2013. Social licence and mining: A critical perspective. Resources

policy, 38(1), pp.29-35.

Park, K. and Jang, S.S., 2013. Capital structure, free cash flow, diversification and firm

performance: A holistic analysis. International Journal of Hospitality Management, 33,

pp.51-63.

Pavlović, M. and Bogdanović, J., 2013. Cash flow statement. Škola biznisa, (3-4), pp.129-

147.

References:

Sen, S., 2013. IFRS Convergence and Applicability in India: Some Issues. A journal of

Humanities & Social Science, 1.

Warren, C. S., & Jones, J. (2018). Corporate financial accounting. Cengage Learning.

Watson, L. (2018). The Deferred Tax Asset Valuation Allowance and Firm

Creditworthiness. The Journal of the American Taxation Association, 40(1), 81-85.

Williams, J. (2014). Financial accounting. McGraw-Hill Higher Education.

Optus.com.au. (2018). [online] Available at:

https://www.optus.com.au/content/dam/optus/documents/about-us/media-centre/annual-

reports/2016/06/Singtel-Annual-Report-2016.pdf [Accessed 20 May 2018].

Owen, J.R. and Kemp, D., 2013. Social licence and mining: A critical perspective. Resources

policy, 38(1), pp.29-35.

Park, K. and Jang, S.S., 2013. Capital structure, free cash flow, diversification and firm

performance: A holistic analysis. International Journal of Hospitality Management, 33,

pp.51-63.

Pavlović, M. and Bogdanović, J., 2013. Cash flow statement. Škola biznisa, (3-4), pp.129-

147.

References:

Sen, S., 2013. IFRS Convergence and Applicability in India: Some Issues. A journal of

Humanities & Social Science, 1.

Warren, C. S., & Jones, J. (2018). Corporate financial accounting. Cengage Learning.

Watson, L. (2018). The Deferred Tax Asset Valuation Allowance and Firm

Creditworthiness. The Journal of the American Taxation Association, 40(1), 81-85.

Williams, J. (2014). Financial accounting. McGraw-Hill Higher Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.