Oracle and Sun Microsystems: Financial Analysis and Acquisition

VerifiedAdded on 2023/06/09

|11

|2264

|207

Report

AI Summary

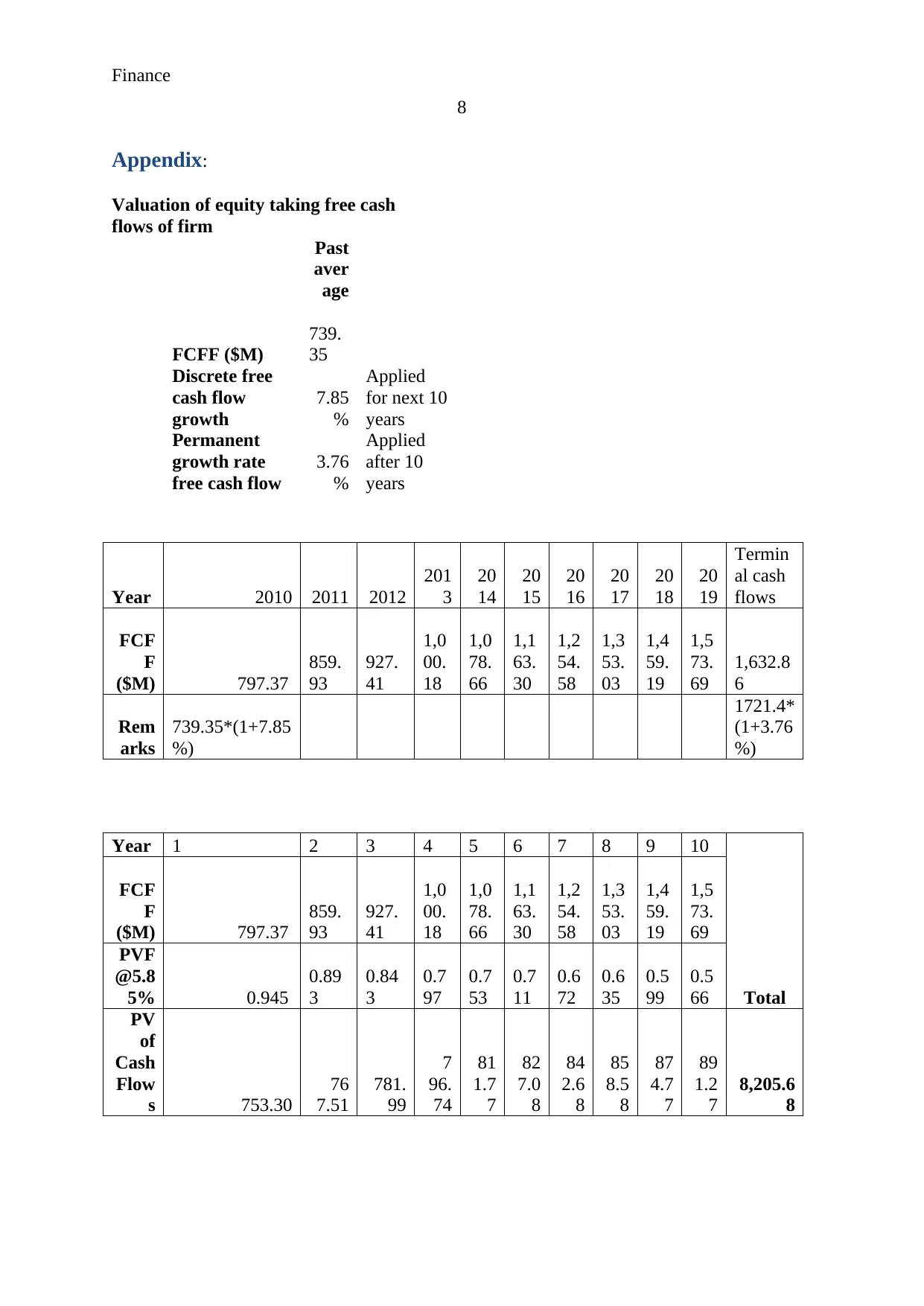

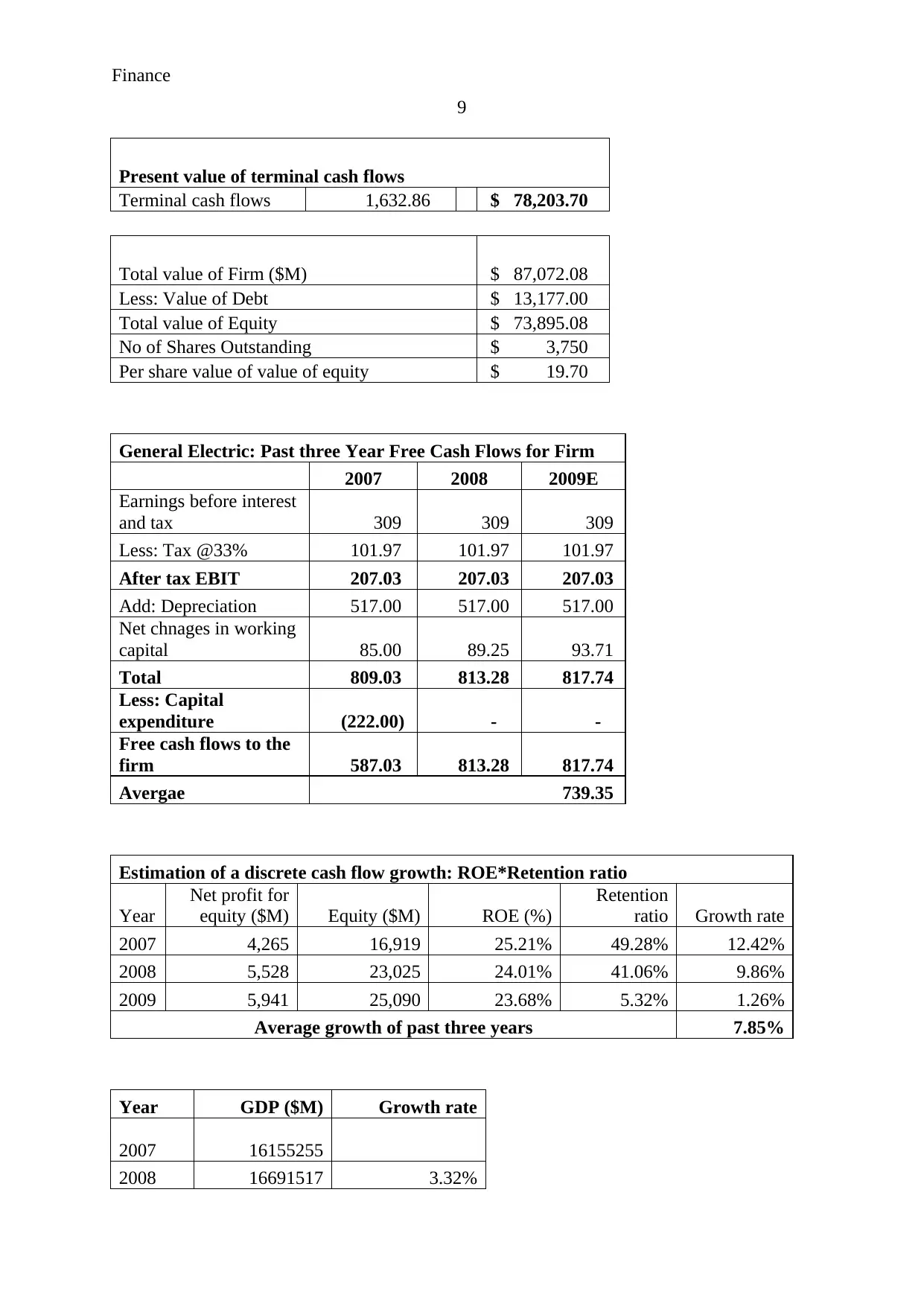

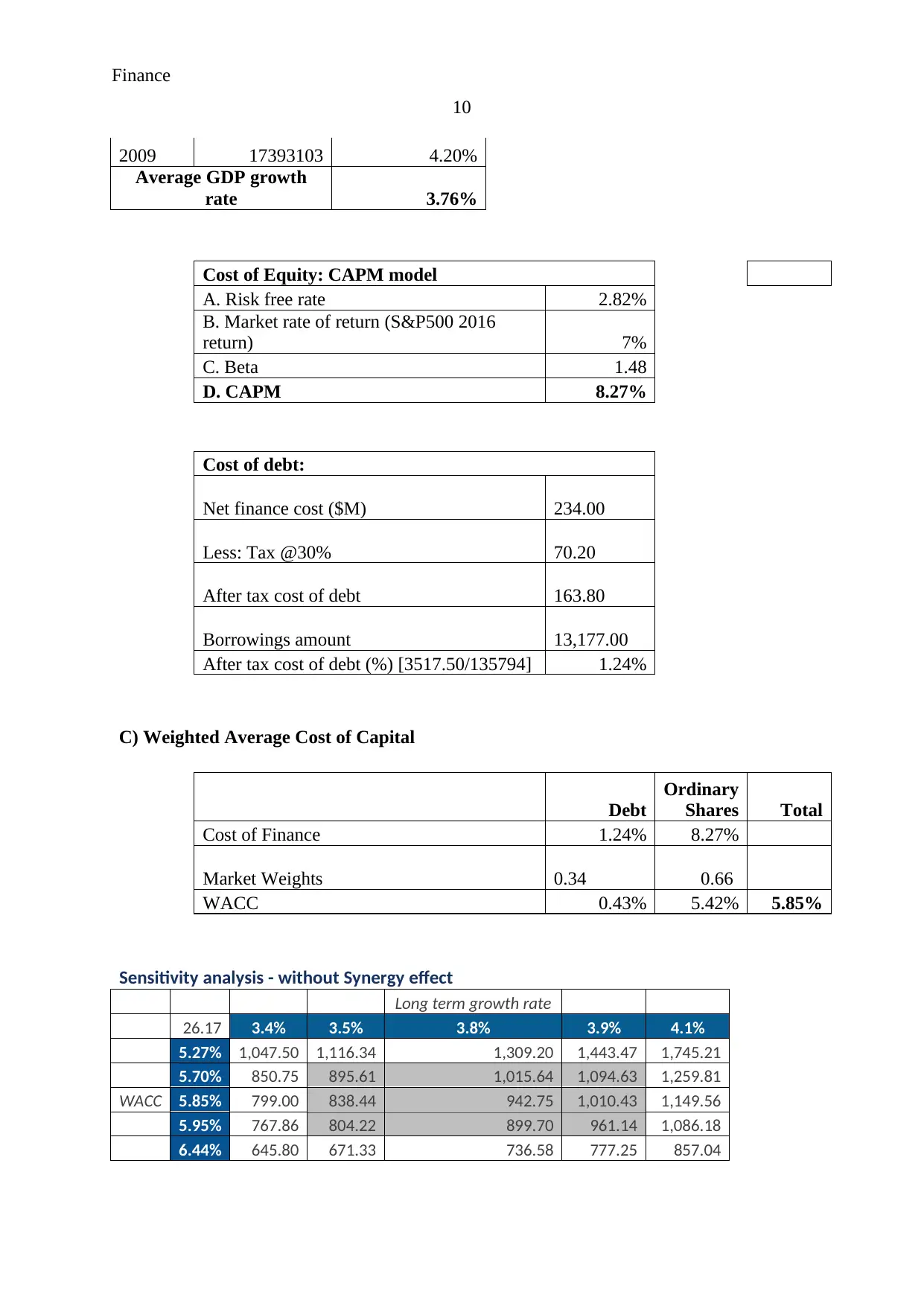

This report provides a financial analysis of Oracle's potential acquisition of Sun Microsystems, evaluating whether the merger is a sound strategic decision and determining an optimal price for Oracle to offer. It uses a Discounted Cash Flow (DCF) valuation model, terminal value calculations, and future cash flow projections to assess Sun Microsystems' worth. The analysis reveals that acquiring Sun Microsystems could benefit Oracle, offering substantial returns and facilitating the achievement of common objectives. The report also includes a synergy analysis, demonstrating improved financial performance and market value post-acquisition. The DCF valuation suggests that Sun Microsystems' stock is undervalued, with a calculated per-share value significantly higher than the current market price and Oracle's initial offer. The report concludes that Oracle should consider offering up to $19.70 per share, the estimated actual worth, to secure the acquisition and maximize potential gains.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.