Enhanced Auditor Reporting: An Analysis of Orica Limited's Audit

VerifiedAdded on 2023/06/07

|13

|2903

|222

Report

AI Summary

This report provides an analysis of the audit report of Orica Limited, a multinational corporation listed on the Australian Stock Exchange (ASX), focusing on its compliance with the Enhanced Auditor Reporting requirements introduced in 2016. The report examines key aspects such as the auditor's independence declaration, the independent auditor's report, non-audit services performed, auditors' remuneration, the role and functions of the audit committee, the independent auditor's report to shareholders, and a review of key audit matters. The analysis evaluates whether the auditors have adhered to the required standards, including those related to independence, ethical responsibilities, and the reporting of key audit matters like goodwill, uncertain tax positions, and environmental provisions. The report highlights the audit opinion given, the nature of non-audit services, the composition and responsibilities of the audit committee, and the reporting of remuneration, providing a comprehensive overview of the audit process and compliance of Orica Limited.

Audit Assurance and Compliance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The purpose of preparing this report is to review as well as analyse the ways that are being

followed by the companies listed on Australian Stock Exchange (ASX), in order to comply with

the new auditor reporting requirements called Enhanced Auditor Requirement. These

requirements were introduced in the year 2016. For the purpose of analysis and review of audited

financial statements, Orica Limited is selected, which is a company listed on ASX. It is

multinational corporation based in Australia and is engaged in providing commercial explosives.

The report analysis whether the auditors have followed audit requirements or not, such as

independence declaration, information about non-audit services, remuneration, key audit matters,

audit committee and report to shareholders.

2

The purpose of preparing this report is to review as well as analyse the ways that are being

followed by the companies listed on Australian Stock Exchange (ASX), in order to comply with

the new auditor reporting requirements called Enhanced Auditor Requirement. These

requirements were introduced in the year 2016. For the purpose of analysis and review of audited

financial statements, Orica Limited is selected, which is a company listed on ASX. It is

multinational corporation based in Australia and is engaged in providing commercial explosives.

The report analysis whether the auditors have followed audit requirements or not, such as

independence declaration, information about non-audit services, remuneration, key audit matters,

audit committee and report to shareholders.

2

Table of Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Background of the Report............................................................................................................4

Scope of the Project.....................................................................................................................4

Discussion........................................................................................................................................4

1) Auditor’s Independence Declaration................................................................................5

2) Independent auditor’s report.............................................................................................6

3) Non-Audit services performed by the Auditor.................................................................6

4) Auditors’ remuneration.....................................................................................................7

5) Role, functions and composition of the Audit Committee................................................8

6) Independent Auditors report to the members (shareholders)............................................9

7) Review all Key Audit Matters noted and the associated audit procedures.......................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

3

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Background of the Report............................................................................................................4

Scope of the Project.....................................................................................................................4

Discussion........................................................................................................................................4

1) Auditor’s Independence Declaration................................................................................5

2) Independent auditor’s report.............................................................................................6

3) Non-Audit services performed by the Auditor.................................................................6

4) Auditors’ remuneration.....................................................................................................7

5) Role, functions and composition of the Audit Committee................................................8

6) Independent Auditors report to the members (shareholders)............................................9

7) Review all Key Audit Matters noted and the associated audit procedures.......................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Background of the Report

The purpose of the project is to review and analyse the impact of the new provisions of

Enhanced Auditor Reporting that has been commenced in the year 2016. The auditors are now

required to fulfill additional requirements to bring about greater transparency in the reporting

system. This will be achieved by evaluating the annual report of a company, which also contains

auditor’s report. The purpose of imposing these standards is to increase transparency in the

reporting and bring clarity in the responsibilities of auditors. Embracing these standards by the

management and auditors will help investors to get insights with respect to key audit matters.

Scope of the Project

The report is divided into seven major headings namely, Auditor’s Independence Declaration;

Independent Auditor’s Report; Non-audit services performed by the auditor; Auditor’s

Remuneration; Audit Committee; Independent Auditor’s Report to the shareholders and; Review

of Key Audit Matters. The compliance of new regulations on above mentioned points by the

company and the auditor has been discussed in detail in the below section.

Discussion

Orica Limited is a multinational corporation based in Australia and, it deals in providing blasting

systems for the purpose of mining and also commercial explosives. The company is chosen for

this analysis because it is a company listed on ASX and operates in many countries. This means

the company has to comply with the new guidelines pertaining to auditor’s reporting. Evaluating

the annual report of Orica Limited will help in gaining an insight on various matters and, also

help in finding out whether the company has complied with regulations or not.

4

Background of the Report

The purpose of the project is to review and analyse the impact of the new provisions of

Enhanced Auditor Reporting that has been commenced in the year 2016. The auditors are now

required to fulfill additional requirements to bring about greater transparency in the reporting

system. This will be achieved by evaluating the annual report of a company, which also contains

auditor’s report. The purpose of imposing these standards is to increase transparency in the

reporting and bring clarity in the responsibilities of auditors. Embracing these standards by the

management and auditors will help investors to get insights with respect to key audit matters.

Scope of the Project

The report is divided into seven major headings namely, Auditor’s Independence Declaration;

Independent Auditor’s Report; Non-audit services performed by the auditor; Auditor’s

Remuneration; Audit Committee; Independent Auditor’s Report to the shareholders and; Review

of Key Audit Matters. The compliance of new regulations on above mentioned points by the

company and the auditor has been discussed in detail in the below section.

Discussion

Orica Limited is a multinational corporation based in Australia and, it deals in providing blasting

systems for the purpose of mining and also commercial explosives. The company is chosen for

this analysis because it is a company listed on ASX and operates in many countries. This means

the company has to comply with the new guidelines pertaining to auditor’s reporting. Evaluating

the annual report of Orica Limited will help in gaining an insight on various matters and, also

help in finding out whether the company has complied with regulations or not.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1) Auditor’s Independence Declaration

Corporations Act, 2001, lays down major compliance requirements regarding reporting of

auditors in Australia. One of the most important matters is related to the independence of the

auditor. According to the act and other regulations by different authorities, an auditor must be

cautious enough to act and work independently from the organization he is associated with

(CAANZ (Chartered Accountants Australia & New Zealand), 2016). In Australia, there are many

laws that govern the work of auditors. Regulations set out in various laws are as under:

Section 307C of the Corporations Act, 2001, deals with the requirement of auditor to

produce a declaration of independence. As per the provisions of this section, an auditor

must declare his independence from the company in the Auditor’s Independence

Declaration. This declaration forms a part of company’s annual report. In addition to this

section, other provisions of this act include Divisions 3, 4 and 5 of Part 2M.4 (Wolters

Kluwer, 2018).

Apart from the Corporations Act 2001, there are certain ethical codes that have been

formulated for the auditors and these are given in APES 110. The regulating authorities

of Australia formulated a regulation requiring the auditors to give a declaration that, they

are complying with the said provisions and are fulfilling their ethical responsibilities.

This is in addition to provisions of Corporations Act, 2001(Chartered Accountants,

2018).

The annual report of Orica Limited contains Independence Declaration by the lead auditors. The

declaration is as per the Corporation Act, 2001 requirements. The annual report also states the

compliance of other provisions related to independence of auditor (APES 110). The auditors

have declared that they have taken care of the provisions of APES 110 while undertaking non-

5

Corporations Act, 2001, lays down major compliance requirements regarding reporting of

auditors in Australia. One of the most important matters is related to the independence of the

auditor. According to the act and other regulations by different authorities, an auditor must be

cautious enough to act and work independently from the organization he is associated with

(CAANZ (Chartered Accountants Australia & New Zealand), 2016). In Australia, there are many

laws that govern the work of auditors. Regulations set out in various laws are as under:

Section 307C of the Corporations Act, 2001, deals with the requirement of auditor to

produce a declaration of independence. As per the provisions of this section, an auditor

must declare his independence from the company in the Auditor’s Independence

Declaration. This declaration forms a part of company’s annual report. In addition to this

section, other provisions of this act include Divisions 3, 4 and 5 of Part 2M.4 (Wolters

Kluwer, 2018).

Apart from the Corporations Act 2001, there are certain ethical codes that have been

formulated for the auditors and these are given in APES 110. The regulating authorities

of Australia formulated a regulation requiring the auditors to give a declaration that, they

are complying with the said provisions and are fulfilling their ethical responsibilities.

This is in addition to provisions of Corporations Act, 2001(Chartered Accountants,

2018).

The annual report of Orica Limited contains Independence Declaration by the lead auditors. The

declaration is as per the Corporation Act, 2001 requirements. The annual report also states the

compliance of other provisions related to independence of auditor (APES 110). The auditors

have declared that they have taken care of the provisions of APES 110 while undertaking non-

5

audit services and fulfilled ethical responsibilities. The information regarding APES 110 formed

the part of Independent auditors report (Orica Limited, 2017).

2) Independent auditor’s report

KPMG is the lead auditor of the company. Auditor of a company can issue four types of audit

opinions namely, unqualified, qualified, adverse opinion and disclaimer of opinion (Leung,

2009). The auditors of Orica Limited have given an unqualified audit opinion for 2017. This is

because they have stated that the provisions of Corporation Act and other Australian Accounting

Standards have been followed by the company. There is no adverse opinion or disclaimer given

by the auditor.

3) Non-Audit services performed by the Auditor

Non- audit services that are provided by an auditor might interfere with the independence of the

auditor. These are the services that are provided by the auditor to the client company in addition

to the audit services. Non-audit services are one of the most important aspects that have a huge

impact on independence of an auditor. Therefore, it is essential for them to exercise careful

judgment before agreeing to provide non-audit services (Frankel, 2018). As per Sarbanes Oxley

Act, which is applicable in the United States of America and some other countries, an auditor

performing audit of a company cannot agree upon providing other non- audit services such as

assisting in preparation of accounts to the same client. However, in Australia, providing such

non- audit services is allowed even auditor is providing audit services to the same client

(Mitchell, 2018). In Australia, the auditors are permitted to perform non- audit services provided

they give a written declaration regarding the same in the annual report. In situations where there

arises a conflict of interest, they must not agree to provide such services and inform it to the

concerned authorities (ASIC, 2018).

6

the part of Independent auditors report (Orica Limited, 2017).

2) Independent auditor’s report

KPMG is the lead auditor of the company. Auditor of a company can issue four types of audit

opinions namely, unqualified, qualified, adverse opinion and disclaimer of opinion (Leung,

2009). The auditors of Orica Limited have given an unqualified audit opinion for 2017. This is

because they have stated that the provisions of Corporation Act and other Australian Accounting

Standards have been followed by the company. There is no adverse opinion or disclaimer given

by the auditor.

3) Non-Audit services performed by the Auditor

Non- audit services that are provided by an auditor might interfere with the independence of the

auditor. These are the services that are provided by the auditor to the client company in addition

to the audit services. Non-audit services are one of the most important aspects that have a huge

impact on independence of an auditor. Therefore, it is essential for them to exercise careful

judgment before agreeing to provide non-audit services (Frankel, 2018). As per Sarbanes Oxley

Act, which is applicable in the United States of America and some other countries, an auditor

performing audit of a company cannot agree upon providing other non- audit services such as

assisting in preparation of accounts to the same client. However, in Australia, providing such

non- audit services is allowed even auditor is providing audit services to the same client

(Mitchell, 2018). In Australia, the auditors are permitted to perform non- audit services provided

they give a written declaration regarding the same in the annual report. In situations where there

arises a conflict of interest, they must not agree to provide such services and inform it to the

concerned authorities (ASIC, 2018).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The auditor of the company performed certain non-audit services as per the independent

auditor’s report in the year 2017. Declaration regarding that has been provided by the auditors

and all such services underwent procedures of corporate governance and were reviewed

thoroughly for independence. However, while evaluating the amount paid for such services, it

was found that despite declaring that non- audit services have been provided in the year 2017, no

payment was made to them and also, the non- audit services are not mentioned in the audit

report(Orica Limited, 2017).

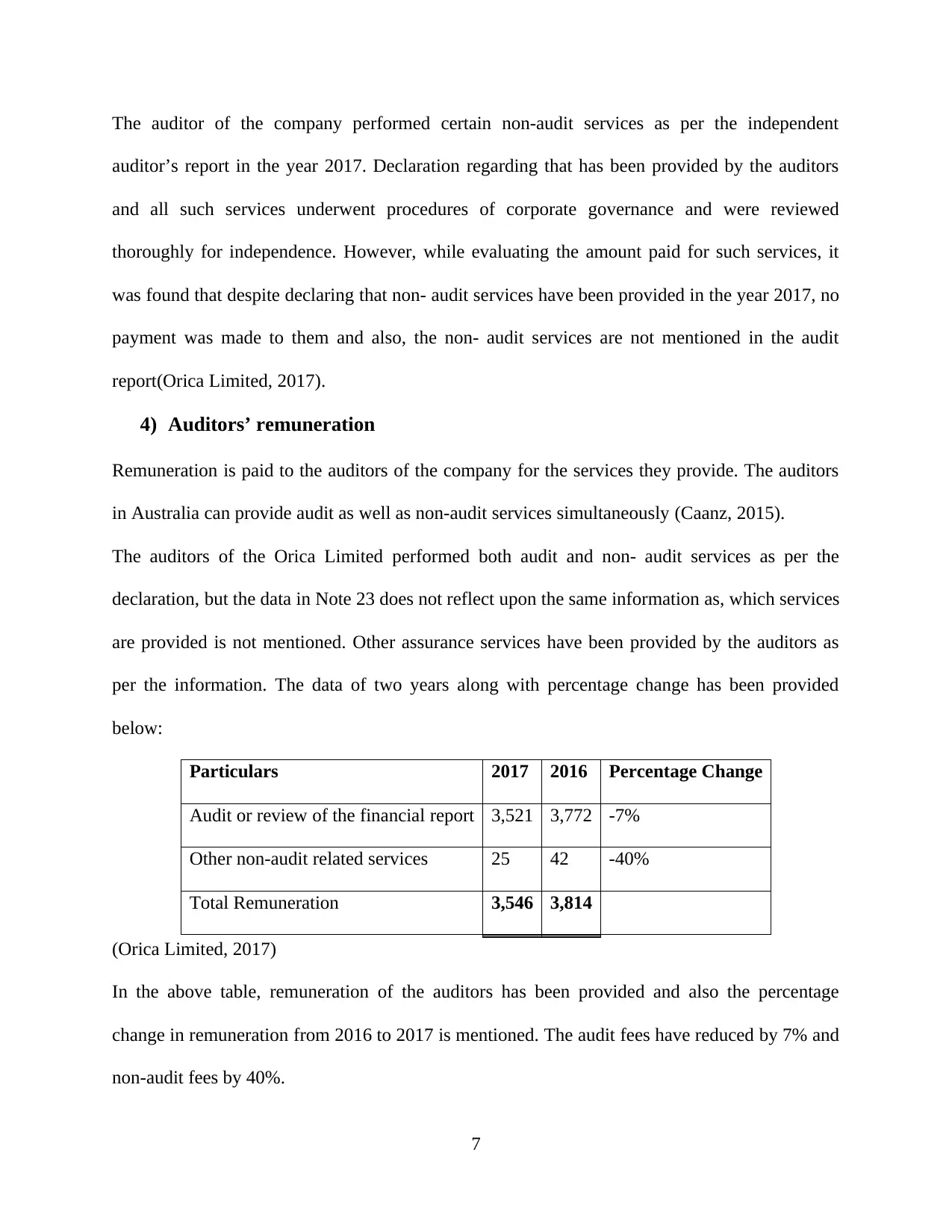

4) Auditors’ remuneration

Remuneration is paid to the auditors of the company for the services they provide. The auditors

in Australia can provide audit as well as non-audit services simultaneously (Caanz, 2015).

The auditors of the Orica Limited performed both audit and non- audit services as per the

declaration, but the data in Note 23 does not reflect upon the same information as, which services

are provided is not mentioned. Other assurance services have been provided by the auditors as

per the information. The data of two years along with percentage change has been provided

below:

Particulars 2017 2016 Percentage Change

Audit or review of the financial report 3,521 3,772 -7%

Other non-audit related services 25 42 -40%

Total Remuneration 3,546 3,814

(Orica Limited, 2017)

In the above table, remuneration of the auditors has been provided and also the percentage

change in remuneration from 2016 to 2017 is mentioned. The audit fees have reduced by 7% and

non-audit fees by 40%.

7

auditor’s report in the year 2017. Declaration regarding that has been provided by the auditors

and all such services underwent procedures of corporate governance and were reviewed

thoroughly for independence. However, while evaluating the amount paid for such services, it

was found that despite declaring that non- audit services have been provided in the year 2017, no

payment was made to them and also, the non- audit services are not mentioned in the audit

report(Orica Limited, 2017).

4) Auditors’ remuneration

Remuneration is paid to the auditors of the company for the services they provide. The auditors

in Australia can provide audit as well as non-audit services simultaneously (Caanz, 2015).

The auditors of the Orica Limited performed both audit and non- audit services as per the

declaration, but the data in Note 23 does not reflect upon the same information as, which services

are provided is not mentioned. Other assurance services have been provided by the auditors as

per the information. The data of two years along with percentage change has been provided

below:

Particulars 2017 2016 Percentage Change

Audit or review of the financial report 3,521 3,772 -7%

Other non-audit related services 25 42 -40%

Total Remuneration 3,546 3,814

(Orica Limited, 2017)

In the above table, remuneration of the auditors has been provided and also the percentage

change in remuneration from 2016 to 2017 is mentioned. The audit fees have reduced by 7% and

non-audit fees by 40%.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

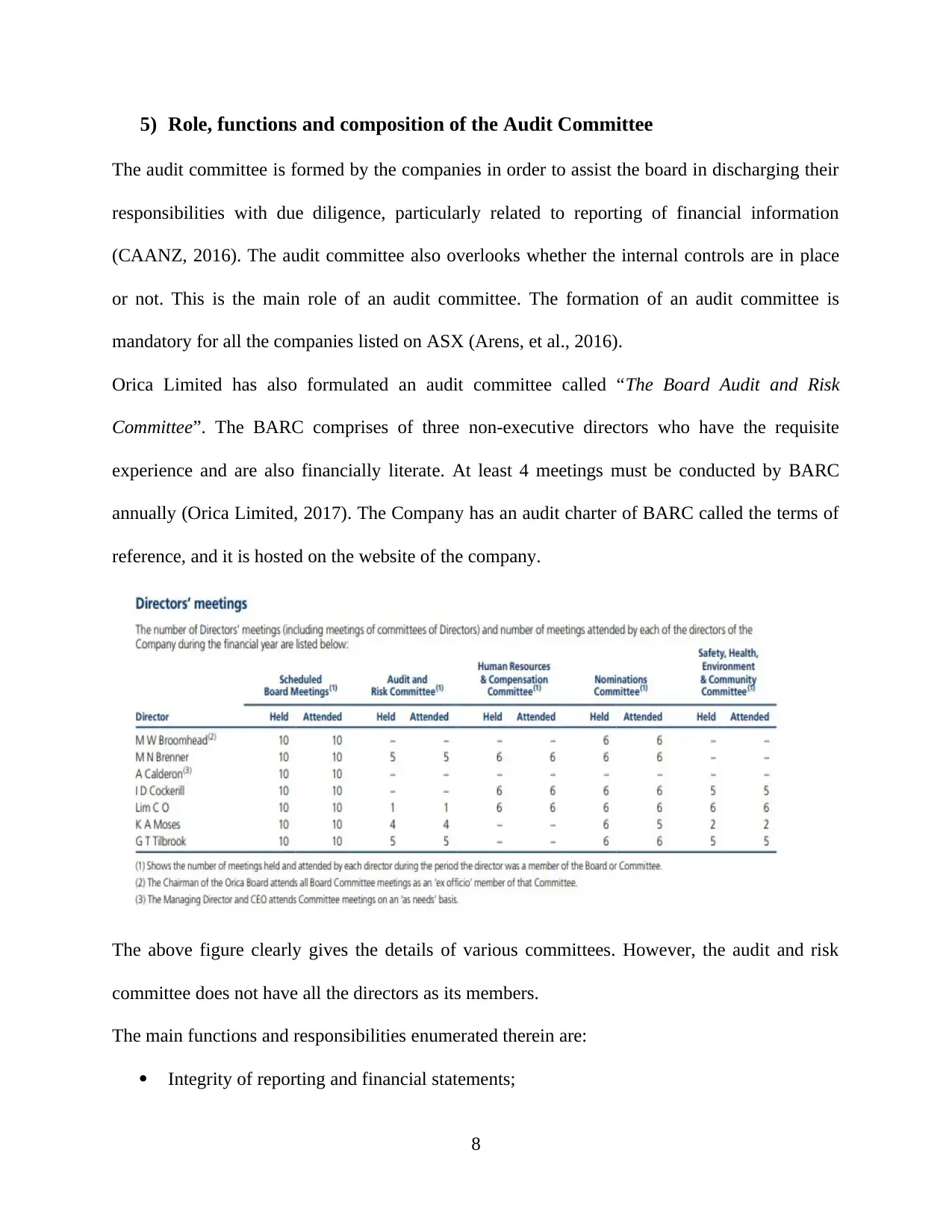

5) Role, functions and composition of the Audit Committee

The audit committee is formed by the companies in order to assist the board in discharging their

responsibilities with due diligence, particularly related to reporting of financial information

(CAANZ, 2016). The audit committee also overlooks whether the internal controls are in place

or not. This is the main role of an audit committee. The formation of an audit committee is

mandatory for all the companies listed on ASX (Arens, et al., 2016).

Orica Limited has also formulated an audit committee called “The Board Audit and Risk

Committee”. The BARC comprises of three non-executive directors who have the requisite

experience and are also financially literate. At least 4 meetings must be conducted by BARC

annually (Orica Limited, 2017). The Company has an audit charter of BARC called the terms of

reference, and it is hosted on the website of the company.

The above figure clearly gives the details of various committees. However, the audit and risk

committee does not have all the directors as its members.

The main functions and responsibilities enumerated therein are:

Integrity of reporting and financial statements;

8

The audit committee is formed by the companies in order to assist the board in discharging their

responsibilities with due diligence, particularly related to reporting of financial information

(CAANZ, 2016). The audit committee also overlooks whether the internal controls are in place

or not. This is the main role of an audit committee. The formation of an audit committee is

mandatory for all the companies listed on ASX (Arens, et al., 2016).

Orica Limited has also formulated an audit committee called “The Board Audit and Risk

Committee”. The BARC comprises of three non-executive directors who have the requisite

experience and are also financially literate. At least 4 meetings must be conducted by BARC

annually (Orica Limited, 2017). The Company has an audit charter of BARC called the terms of

reference, and it is hosted on the website of the company.

The above figure clearly gives the details of various committees. However, the audit and risk

committee does not have all the directors as its members.

The main functions and responsibilities enumerated therein are:

Integrity of reporting and financial statements;

8

External and Internal audit;

Performance of risk and audit functions of the group;

Risk management and internal controls;

Compliances (Orica Limited, 2017).

6) Independent Auditors report to the members (shareholders)

The auditors of a company are required to report their findings in the form of a report to the

shareholders and members of the company. It is the responsibility of the auditor of the company

to express his opinion over the financial statements (Gay & Simnett, 2015). On the other hand,

the preparation of financial statements is a responsibility of management. Appropriate choice of

sound accounting policies and internal controls is a management’s responsibility (Media, 2015).

There was one subsequent event where the company declared dividend of 28 cents per share. Its

effect was not included in current annual report, but will be reflected in the annual report of

2018.

7) Review all Key Audit Matters noted and the associated audit procedures

Enhanced Auditing Reporting requires the auditors to report on the key audit matters that were

identified during the audit of financial statements (Gay & Simnett, 2018). KAM’s are those

areas, which were most significant matters identified during audit and are therefore, essential to

report. The auditor of Orica Limited identified three KAM’s which include: Carrying Value of Goodwill Accounting for uncertain tax positions Accounting for environmental and decommissioning provisions (Orica Limited, 2017)

Carrying value of Goodwill- As per the auditors, testing of goodwill was attributable to one of

the segments called the Minova Segment. Significant judgment was applied in evaluating the

9

Performance of risk and audit functions of the group;

Risk management and internal controls;

Compliances (Orica Limited, 2017).

6) Independent Auditors report to the members (shareholders)

The auditors of a company are required to report their findings in the form of a report to the

shareholders and members of the company. It is the responsibility of the auditor of the company

to express his opinion over the financial statements (Gay & Simnett, 2015). On the other hand,

the preparation of financial statements is a responsibility of management. Appropriate choice of

sound accounting policies and internal controls is a management’s responsibility (Media, 2015).

There was one subsequent event where the company declared dividend of 28 cents per share. Its

effect was not included in current annual report, but will be reflected in the annual report of

2018.

7) Review all Key Audit Matters noted and the associated audit procedures

Enhanced Auditing Reporting requires the auditors to report on the key audit matters that were

identified during the audit of financial statements (Gay & Simnett, 2018). KAM’s are those

areas, which were most significant matters identified during audit and are therefore, essential to

report. The auditor of Orica Limited identified three KAM’s which include: Carrying Value of Goodwill Accounting for uncertain tax positions Accounting for environmental and decommissioning provisions (Orica Limited, 2017)

Carrying value of Goodwill- As per the auditors, testing of goodwill was attributable to one of

the segments called the Minova Segment. Significant judgment was applied in evaluating the

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

available audit evidence. Reason behind this was the huge amount of balance and the recent

performance of this segment. There were a number of external factors that were responsible for

the weak performance of the segment, such as decline in demand of coal in global market as

compared to previous trends, low prices and mandates for reduction in costs. The auditors

checked for the assumptions applied by the management and their value in use models such as

forecast operating costs, forecast terminal growth rates and discount rate model. The auditors

applied tests of control for this matter.

Accounting for environmental and decommissioning provisions- Other KAM from the

perspective auditors was estimating the decommissioning provisions as well as environmental

remediation. Reason to include this as KAM was the inherent complexity associated in

ascertaining such costs, which include costs of legal matters and ground disturbance costs. The

auditors applied tests of control for this matter.

Accounting for uncertain tax positions - Company being a multinational company operates in an

international tax environment and its structure is driven by mergers and acquisitions. The

Company makes sales in many countries of the world. This matter is a KAM, because the

Company operates in varied tax jurisdictions and the interpretation of tax laws requires making

significant judgment by the management. Also, the tax provisions keep on changing in order to

improve the transparency. The auditors applied tests of control and analytical procedures for

this matter.

Conclusion

From the above analysis, it can be said that the auditors have taken care of mostly all the

reporting requirements. However, matter related to non -audit services could have been clearer.

10

performance of this segment. There were a number of external factors that were responsible for

the weak performance of the segment, such as decline in demand of coal in global market as

compared to previous trends, low prices and mandates for reduction in costs. The auditors

checked for the assumptions applied by the management and their value in use models such as

forecast operating costs, forecast terminal growth rates and discount rate model. The auditors

applied tests of control for this matter.

Accounting for environmental and decommissioning provisions- Other KAM from the

perspective auditors was estimating the decommissioning provisions as well as environmental

remediation. Reason to include this as KAM was the inherent complexity associated in

ascertaining such costs, which include costs of legal matters and ground disturbance costs. The

auditors applied tests of control for this matter.

Accounting for uncertain tax positions - Company being a multinational company operates in an

international tax environment and its structure is driven by mergers and acquisitions. The

Company makes sales in many countries of the world. This matter is a KAM, because the

Company operates in varied tax jurisdictions and the interpretation of tax laws requires making

significant judgment by the management. Also, the tax provisions keep on changing in order to

improve the transparency. The auditors applied tests of control and analytical procedures for

this matter.

Conclusion

From the above analysis, it can be said that the auditors have taken care of mostly all the

reporting requirements. However, matter related to non -audit services could have been clearer.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In order to improve the quality of information in the report, it is suggested to remove all the

unnecessary information as important information gets lost amidst irrelevant information. One

such information was about the non- audit services. While at one place it was given that the

auditors have performed certain non -audit services, in the remuneration section it was identified

that there was no mention about the specific assurance services that have been performed. This

information is misleading and hence, must be avoided in future. Other point to be noted is

regarding the roles and responsibilities and other details regarding audit committee are given on

the official website of the company and are therefore not included in reports. I would like to ask

following questions to auditors: What type of non-audit services have you performed in the

company? and how do you justify that it has not affected you independence?

References

Arens, A., Arens, A. A., Best, P., Shailer, G., Fiedler, B., Elder, R., & Beasley, M. (2016).

Auditing, Assurance Services and Ethics in Australia with ACL Access Code Card.

Pearson Education Australia.

ASIC. (2018). Auditor independence and audit quality. Retrieved from Australian Securities &

Investments Commision: https://asic.gov.au/regulatory-resources/financial-reporting-and-

audit/auditors/auditor-independence-and-audit-quality/

CAANZ (Chartered Accountants Australia & New Zealand). (2016). Auditing, Assurance and

Ethics Handbook 2016 Australia: Incorporating All the Standards as at 1 December

2015. John Wiley & Sons.

Caanz. (2015). Auditing and Assurance Handbook 2015 New Zealand+auditing and Assurance

Handbook 2015 New Zealand Wiley E-Text Card. John Wiley & Sons Australia, Limited.

11

unnecessary information as important information gets lost amidst irrelevant information. One

such information was about the non- audit services. While at one place it was given that the

auditors have performed certain non -audit services, in the remuneration section it was identified

that there was no mention about the specific assurance services that have been performed. This

information is misleading and hence, must be avoided in future. Other point to be noted is

regarding the roles and responsibilities and other details regarding audit committee are given on

the official website of the company and are therefore not included in reports. I would like to ask

following questions to auditors: What type of non-audit services have you performed in the

company? and how do you justify that it has not affected you independence?

References

Arens, A., Arens, A. A., Best, P., Shailer, G., Fiedler, B., Elder, R., & Beasley, M. (2016).

Auditing, Assurance Services and Ethics in Australia with ACL Access Code Card.

Pearson Education Australia.

ASIC. (2018). Auditor independence and audit quality. Retrieved from Australian Securities &

Investments Commision: https://asic.gov.au/regulatory-resources/financial-reporting-and-

audit/auditors/auditor-independence-and-audit-quality/

CAANZ (Chartered Accountants Australia & New Zealand). (2016). Auditing, Assurance and

Ethics Handbook 2016 Australia: Incorporating All the Standards as at 1 December

2015. John Wiley & Sons.

Caanz. (2015). Auditing and Assurance Handbook 2015 New Zealand+auditing and Assurance

Handbook 2015 New Zealand Wiley E-Text Card. John Wiley & Sons Australia, Limited.

11

Chartered Accountants. (2018). Perspective. Retrieved from Charteredaccountantsanz.com:

https://www.charteredaccountantsanz.com/-/media/6960ce5ce8cf470ab94d857539f85f71

.ashx

Frankel, R. M. (2018). The Relation Between Auditors' Fees for Non-Audit Services and

Earnings Quality (Classic Reprint). Fb&c Limited.

Gay, G. E., & Simnett, R. (2015). Auditing and Assurance Services in Australia. McGraw-Hill

Education (Australia).

Gay, G., & Simnett, R. (2018). Auditing and Assurance Services in Australia, Seventh Edition.

McGraw-Hill Education Australia.

Leung, P. (2009). Modern Auditing & Assurance Services. John Wiley & Sons Australia.

Media, B. L. (2015). CPA Australia Advanced Audit and Assurance: Passcards. BPP Learning

Media.

Mitchell, K. (2018). Independence – Navigating the murky waters between Audit & Non-Audit

services. Retrieved September 11, 2018, from rochford-group.com: https://rochford-

group.com/independence-navigating-murky-waters-audit-non-audit-services/

Orica Limited. (2017). 2017 Corporate Governance Statement. Retrieved from Orica.com:

http://www.orica.com/ArticleDocuments/329/2017-Corporate-Governance-

Statement.pdf.aspx

Orica Limited. (2017). Annual Report. Retrieved from Orica.com:

https://www.orica.com/ArticleDocuments/1762/AR17_Orica_Annual_Report_WEB.PDF

.aspx

Orica Limited. (2017). Terms of Reference, BARC. Retrieved from Orica.com:

http://www.orica.com/ArticleDocuments/323/201705_BARC-Terms-of-

12

https://www.charteredaccountantsanz.com/-/media/6960ce5ce8cf470ab94d857539f85f71

.ashx

Frankel, R. M. (2018). The Relation Between Auditors' Fees for Non-Audit Services and

Earnings Quality (Classic Reprint). Fb&c Limited.

Gay, G. E., & Simnett, R. (2015). Auditing and Assurance Services in Australia. McGraw-Hill

Education (Australia).

Gay, G., & Simnett, R. (2018). Auditing and Assurance Services in Australia, Seventh Edition.

McGraw-Hill Education Australia.

Leung, P. (2009). Modern Auditing & Assurance Services. John Wiley & Sons Australia.

Media, B. L. (2015). CPA Australia Advanced Audit and Assurance: Passcards. BPP Learning

Media.

Mitchell, K. (2018). Independence – Navigating the murky waters between Audit & Non-Audit

services. Retrieved September 11, 2018, from rochford-group.com: https://rochford-

group.com/independence-navigating-murky-waters-audit-non-audit-services/

Orica Limited. (2017). 2017 Corporate Governance Statement. Retrieved from Orica.com:

http://www.orica.com/ArticleDocuments/329/2017-Corporate-Governance-

Statement.pdf.aspx

Orica Limited. (2017). Annual Report. Retrieved from Orica.com:

https://www.orica.com/ArticleDocuments/1762/AR17_Orica_Annual_Report_WEB.PDF

.aspx

Orica Limited. (2017). Terms of Reference, BARC. Retrieved from Orica.com:

http://www.orica.com/ArticleDocuments/323/201705_BARC-Terms-of-

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.