Origin Energy and the Conceptual Framework: A Detailed Report

VerifiedAdded on 2023/06/13

|19

|2745

|494

Report

AI Summary

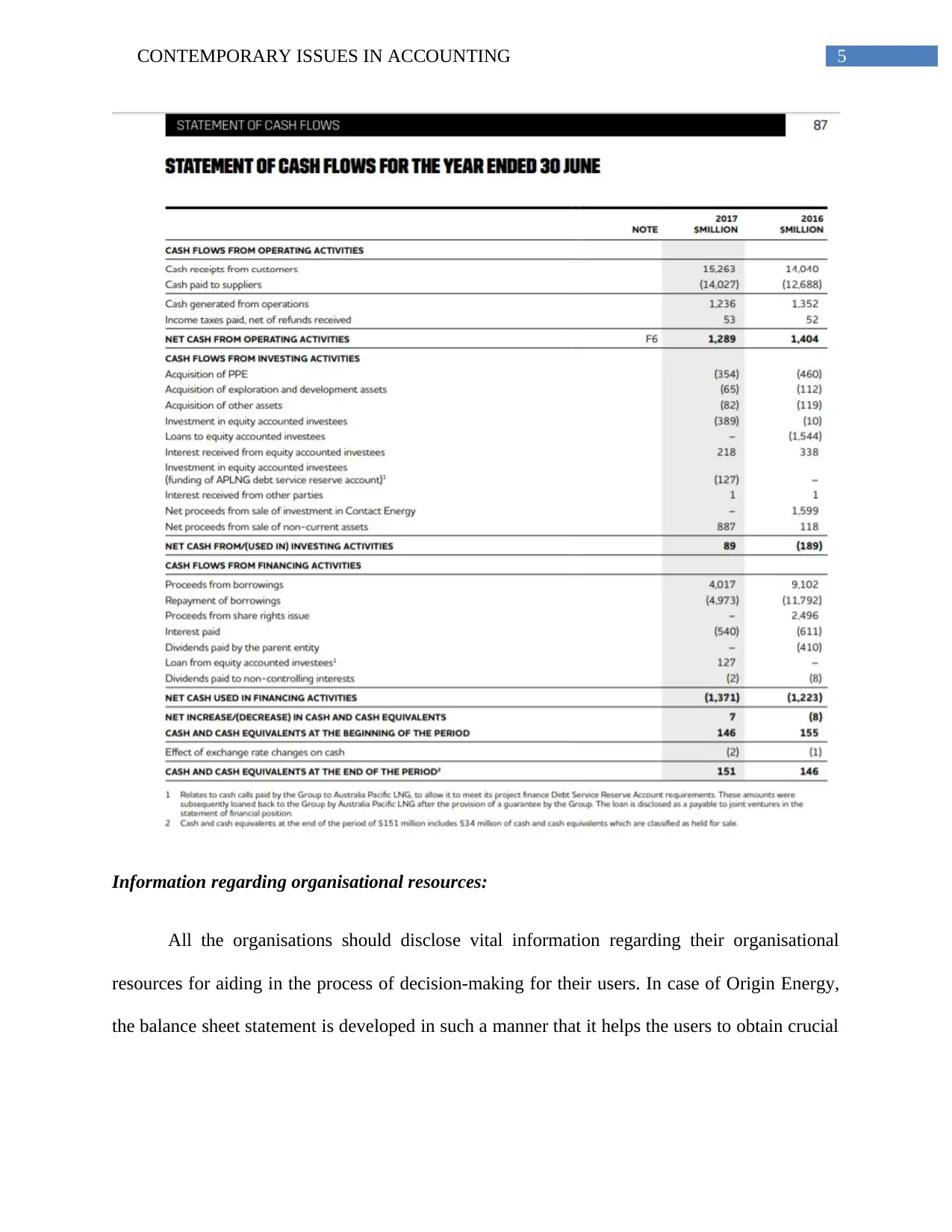

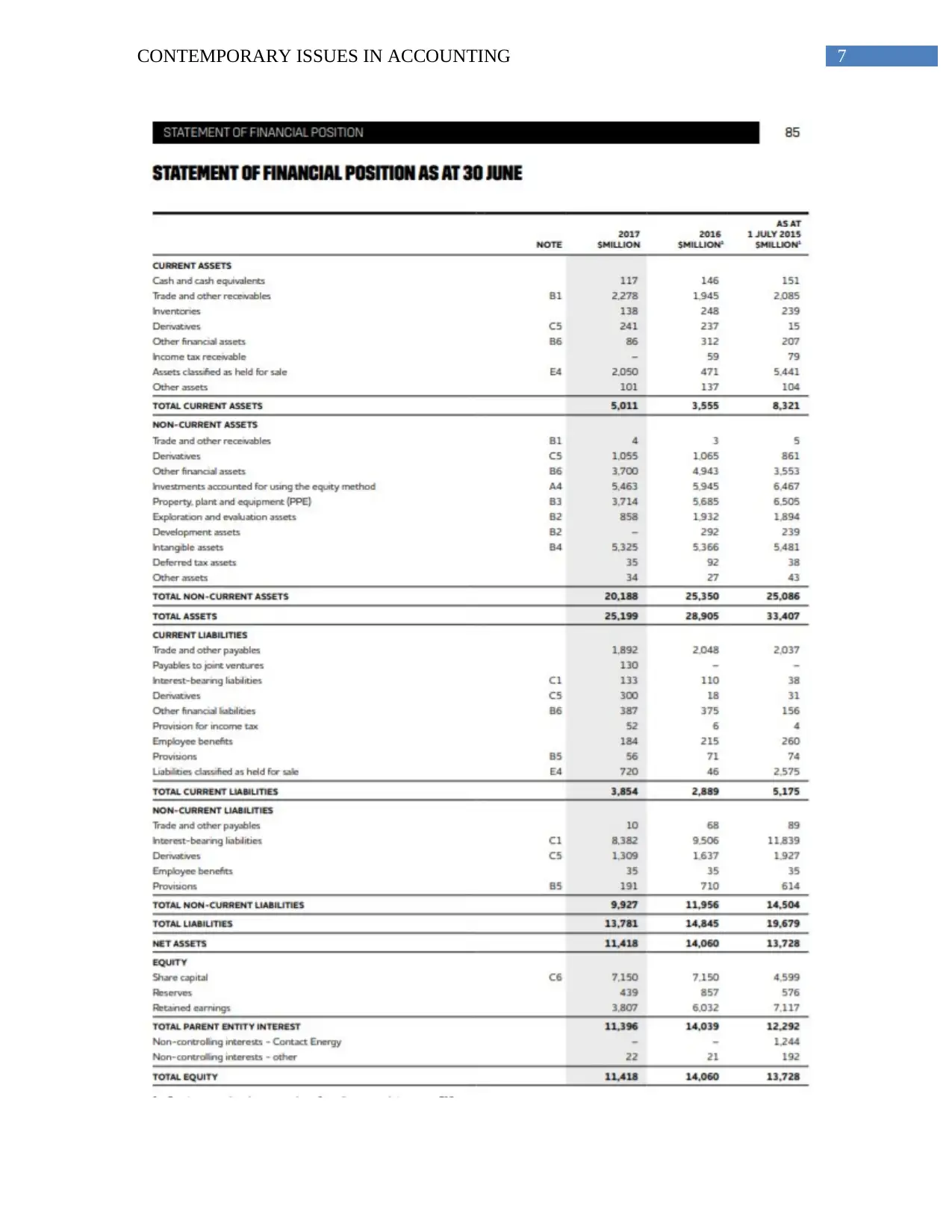

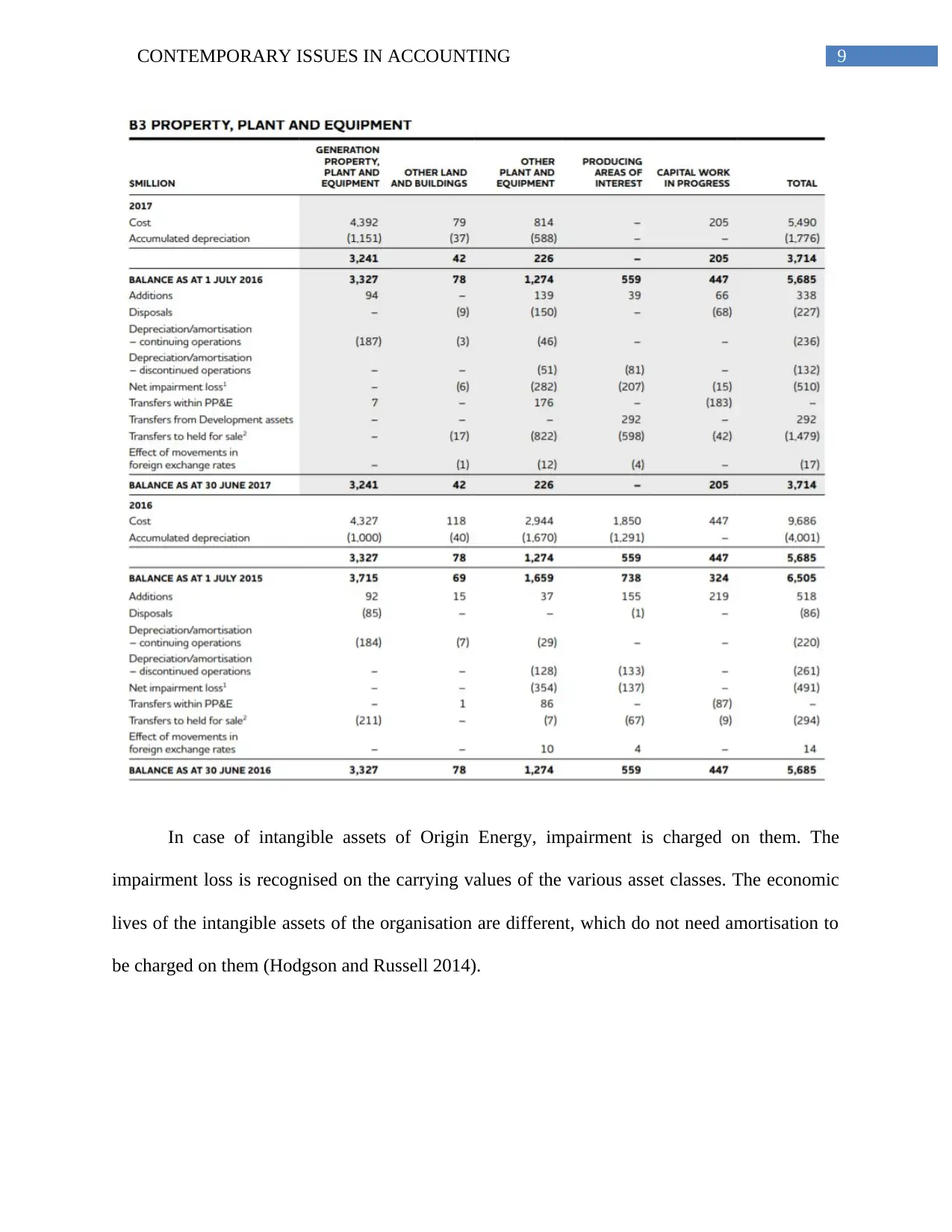

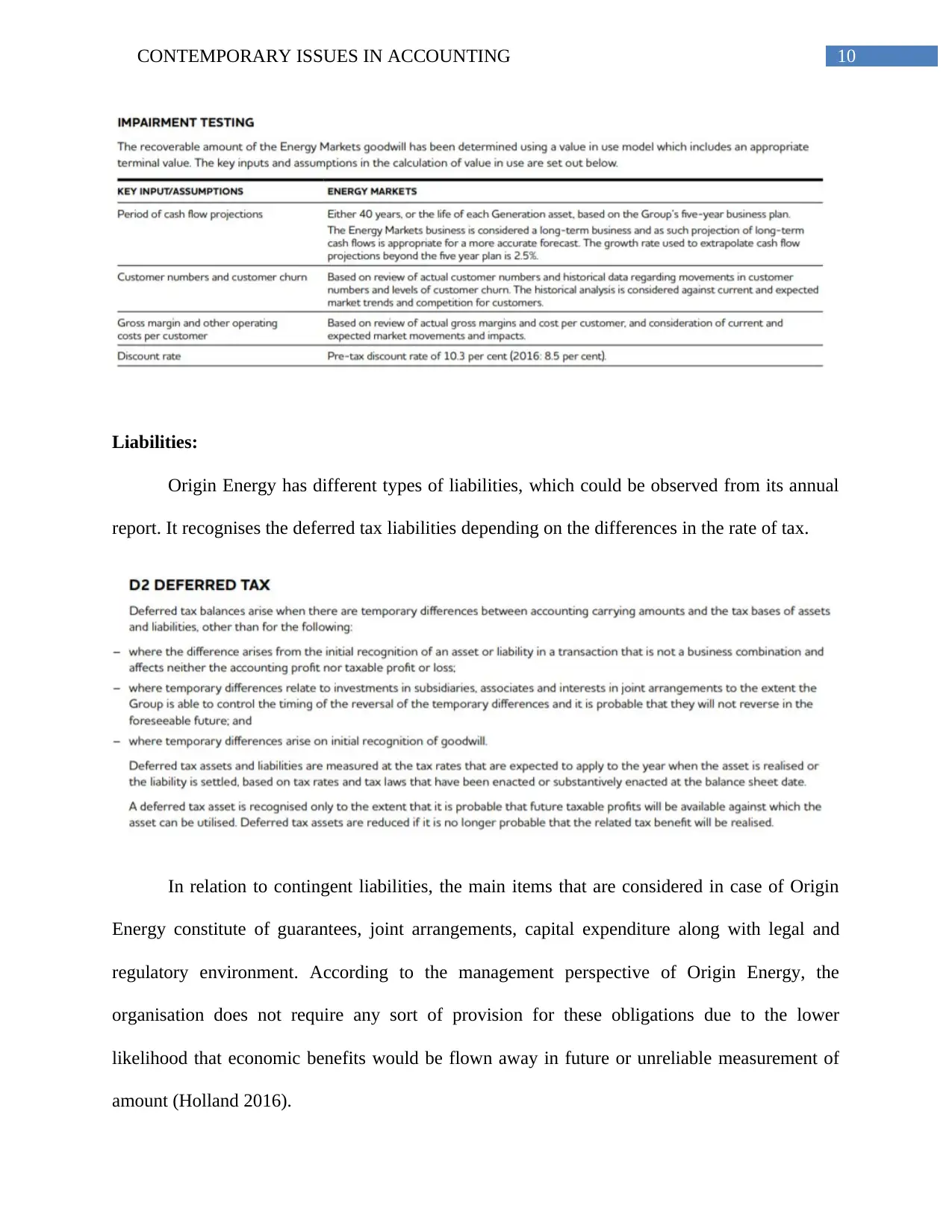

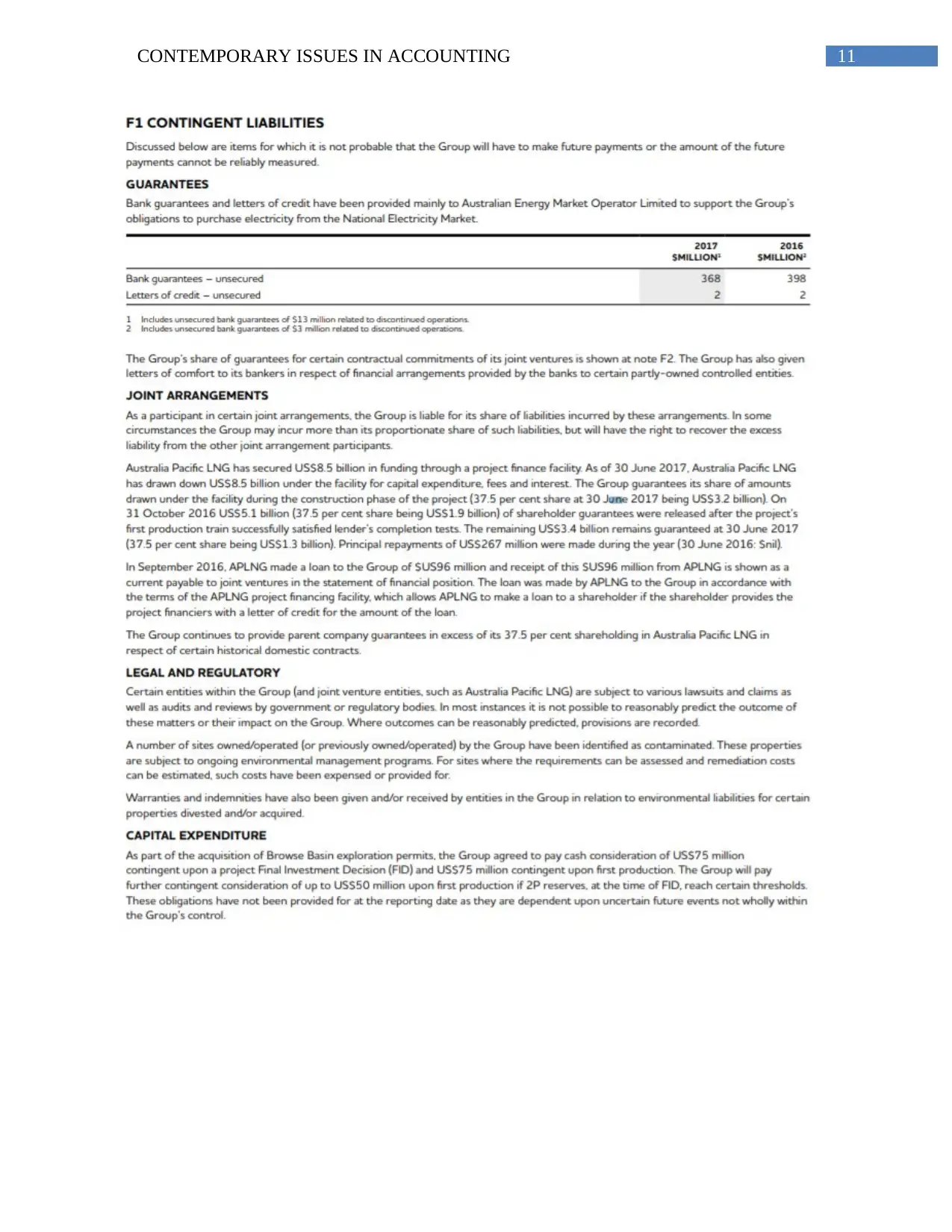

This report assesses Origin Energy Private Limited's conformance with the conceptual framework for financial reporting, focusing on the objectives, recognition criteria, and qualitative characteristics outlined by the AASB. The analysis reveals that Origin Energy adheres to the Corporations Act 2001, AASB, and IFRS, ensuring valuable financial information is delivered to users. The company appropriately recognizes assets, liabilities, equity, revenue, and expenses, providing transparent and faithful representation in its financial statements, which are audited by KPMG. Origin Energy's practices support comparability, verifiability, timeliness, and understandability, ensuring stakeholders receive a clear overview of the organization's financial performance and market position. The report concludes that Origin Energy effectively follows the guidelines and regulations set forth in the conceptual framework, reinforcing trust among users and stakeholders.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.