Origin Energy & Accounting Standards: A Conceptual Framework Review

VerifiedAdded on 2023/06/12

|15

|2323

|272

Report

AI Summary

This report analyzes Origin Energy, an ASX-listed Australian energy company, in relation to its compliance with the Australian Accounting Standards Board (AASB) conceptual framework. It evaluates the company's adherence to the objectives of the framework, including delivering financial information about resources, performance, and changes in performance. The report also examines Origin Energy's application of recognition criteria for assets, liabilities, equity, revenue, and expenses, as well as its demonstration of fundamental (relevance and faithful representation) and enhancing (comparability, verifiability, timeliness, and understandability) qualitative characteristics. The analysis confirms that Origin Energy adheres to AASB standards, the Corporations Act 2001, and International Financial Reporting Standards (IFRS), ensuring transparency and accuracy in its financial reporting.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary Issues in Accounting

Name of the Student

Name of the University

Author’s Note

Contemporary Issues in Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CONTEMPORARY ISSUES IN ACCOUNTING

Abstract

The main aim of this report is to analyse and evaluate different standards and principles of

accounting conceptual framework by relating with an Australian Securities Exchange (ASX)

listed companies that is Origin Energy. The results of the report shows the full compliance of

the company with all the required standards of conceptual framework.

Abstract

The main aim of this report is to analyse and evaluate different standards and principles of

accounting conceptual framework by relating with an Australian Securities Exchange (ASX)

listed companies that is Origin Energy. The results of the report shows the full compliance of

the company with all the required standards of conceptual framework.

2CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................2

Conceptual Framework Objectives..................................................................................................2

Target Audience of Conceptual Framework....................................................................................7

Recognition Criteria.........................................................................................................................7

Fundamental Qualitative Characteristics.........................................................................................9

Enhancing Qualitative Characteristics...........................................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Table of Contents

Introduction......................................................................................................................................2

Conceptual Framework Objectives..................................................................................................2

Target Audience of Conceptual Framework....................................................................................7

Recognition Criteria.........................................................................................................................7

Fundamental Qualitative Characteristics.........................................................................................9

Enhancing Qualitative Characteristics...........................................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

The main aim of this report is to analyse and evaluate different standards and principles

of accounting conceptual framework by relating with an Australian Securities Exchange (ASX)

listed companies. It needs to be mentioned that the business entities of Australia are needed to

comply with the standards and principles of conceptual framework for the purpose of their

financial reporting. In Australia, the presence of accounting conceptual framework can be seen

developed by Australian Accounting Standard Board (AAS) with the cooperation of

International Accounting Standard Board (IASB) (aasb.gov.au 2018). The compliance with all

the standard and principles of this accounting conceptual framework helps in bringing

transparency and accuracy in the financial reporting. For this report, Origin Energy is taken into

consideration. Origin Energy is an Australian energy company with headquarter in Sydney and

the company is listed in ASX in the code of ‘ORG’ (originenergy.com.au 2018).

Conceptual Framework Objectives

The overall aim of the conceptual frameworkof AASB is to make the ASX listed

companies comply with the required standards and principles of financial reporting. For the

achievement of this aim, the AASB conceptual framework has three objectives and they are as

follows:

The first objective is to deliver all the required financial information related to the

financial resources of the business entities to the users so that they can determine the financial

position of the business entities (aasb.gov.au 2018).

Introduction

The main aim of this report is to analyse and evaluate different standards and principles

of accounting conceptual framework by relating with an Australian Securities Exchange (ASX)

listed companies. It needs to be mentioned that the business entities of Australia are needed to

comply with the standards and principles of conceptual framework for the purpose of their

financial reporting. In Australia, the presence of accounting conceptual framework can be seen

developed by Australian Accounting Standard Board (AAS) with the cooperation of

International Accounting Standard Board (IASB) (aasb.gov.au 2018). The compliance with all

the standard and principles of this accounting conceptual framework helps in bringing

transparency and accuracy in the financial reporting. For this report, Origin Energy is taken into

consideration. Origin Energy is an Australian energy company with headquarter in Sydney and

the company is listed in ASX in the code of ‘ORG’ (originenergy.com.au 2018).

Conceptual Framework Objectives

The overall aim of the conceptual frameworkof AASB is to make the ASX listed

companies comply with the required standards and principles of financial reporting. For the

achievement of this aim, the AASB conceptual framework has three objectives and they are as

follows:

The first objective is to deliver all the required financial information related to the

financial resources of the business entities to the users so that they can determine the financial

position of the business entities (aasb.gov.au 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CONTEMPORARY ISSUES IN ACCOUNTING

The second objective of AASB conceptual framework is to deliver all the required

information about major financial aspects of the businesses like sales, cost of goods sold, profit

and others to the users so that they become able to determine the financial performance of the

entities (aasb.gov.au 2018).

The third objective of AASB conceptual framework is to deliver all the necessary

information about the elements like change in profit and others to the users so that it becomes

possible for them to determine the change in financial performance of the business entities

(aasb.gov.au 2018).

The following discussion shows the compliance of Origin Energy with these above-

discussed objectives of conceptual framework through financial reporting:

The second objective of AASB conceptual framework is to deliver all the required

information about major financial aspects of the businesses like sales, cost of goods sold, profit

and others to the users so that they become able to determine the financial performance of the

entities (aasb.gov.au 2018).

The third objective of AASB conceptual framework is to deliver all the necessary

information about the elements like change in profit and others to the users so that it becomes

possible for them to determine the change in financial performance of the business entities

(aasb.gov.au 2018).

The following discussion shows the compliance of Origin Energy with these above-

discussed objectives of conceptual framework through financial reporting:

5CONTEMPORARY ISSUES IN ACCOUNTING

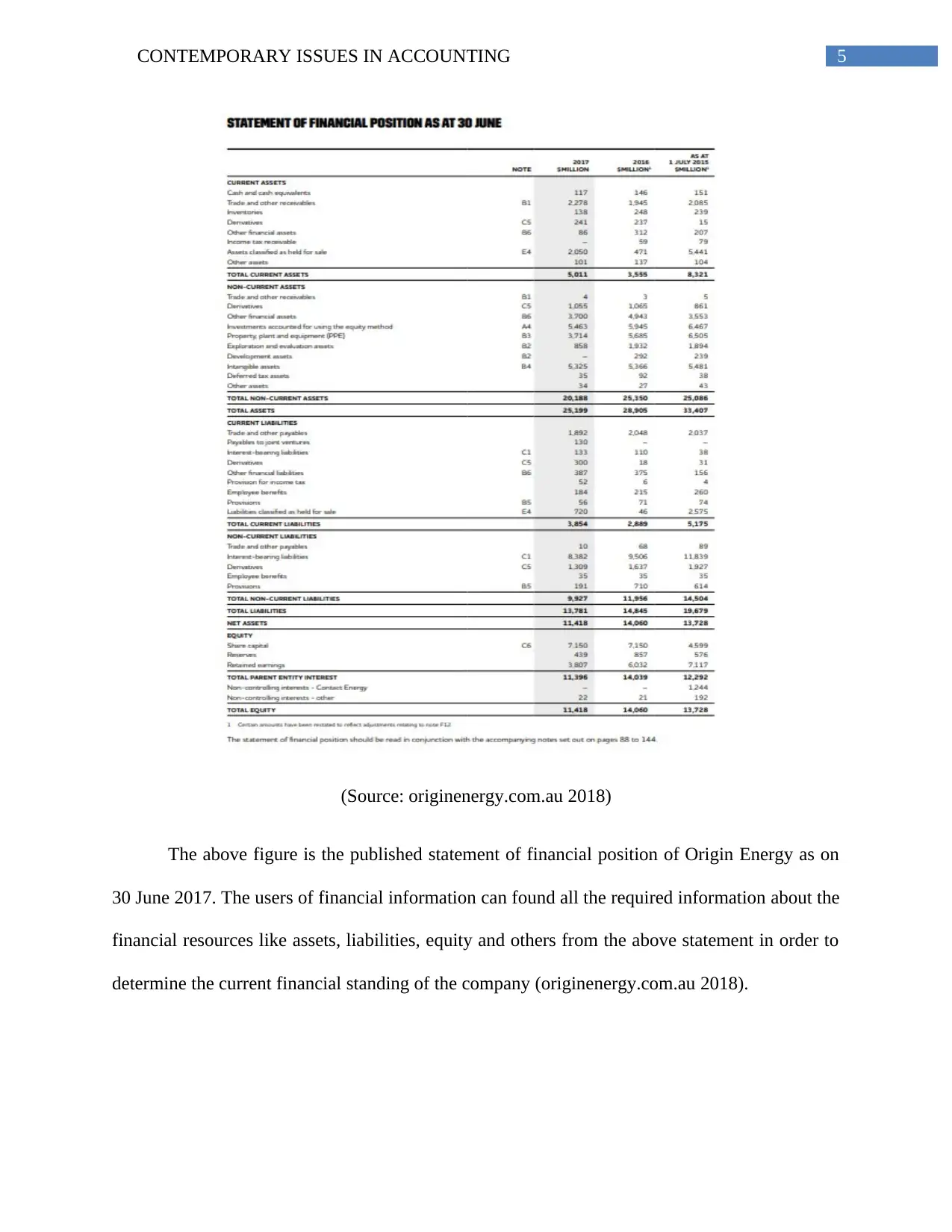

(Source: originenergy.com.au 2018)

The above figure is the published statement of financial position of Origin Energy as on

30 June 2017. The users of financial information can found all the required information about the

financial resources like assets, liabilities, equity and others from the above statement in order to

determine the current financial standing of the company (originenergy.com.au 2018).

(Source: originenergy.com.au 2018)

The above figure is the published statement of financial position of Origin Energy as on

30 June 2017. The users of financial information can found all the required information about the

financial resources like assets, liabilities, equity and others from the above statement in order to

determine the current financial standing of the company (originenergy.com.au 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CONTEMPORARY ISSUES IN ACCOUNTING

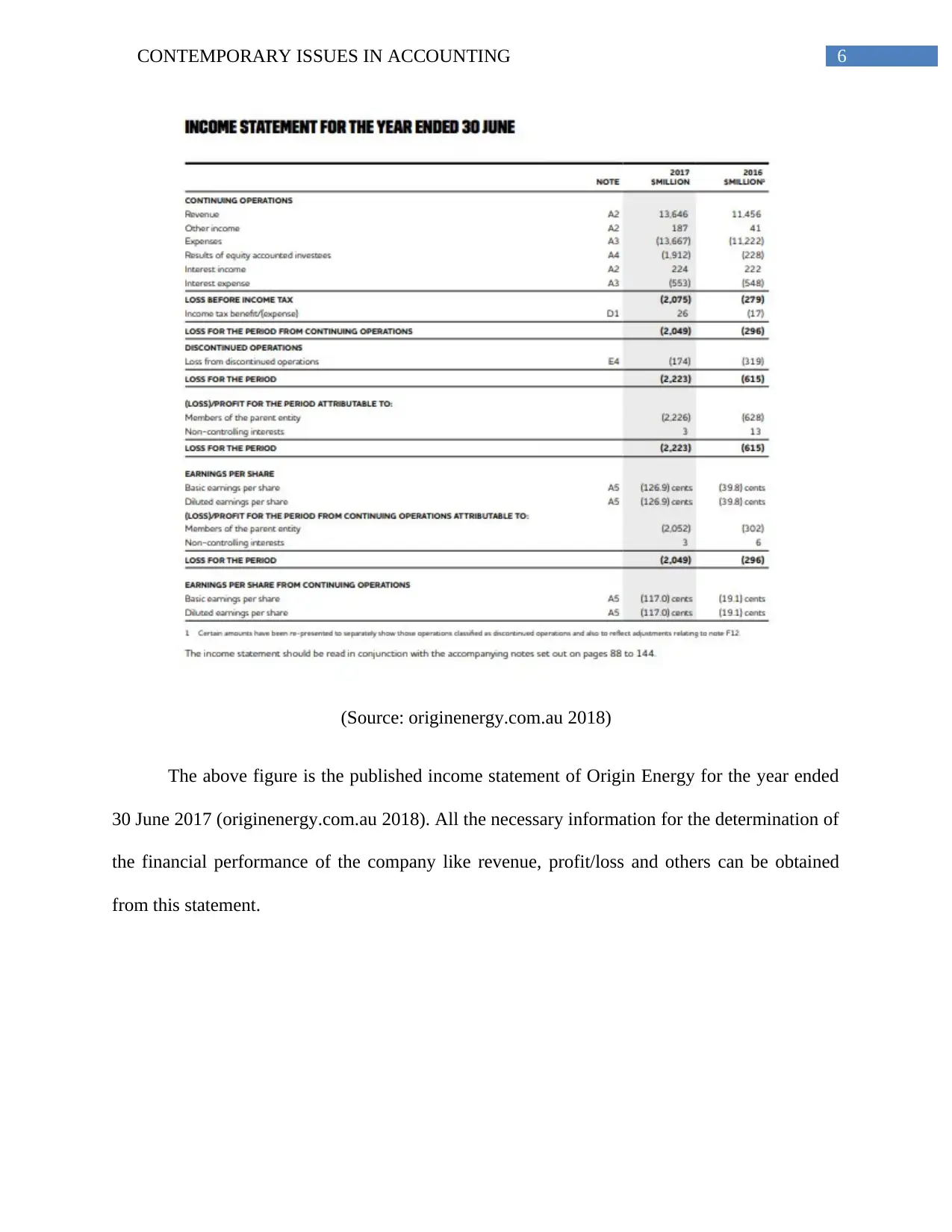

(Source: originenergy.com.au 2018)

The above figure is the published income statement of Origin Energy for the year ended

30 June 2017 (originenergy.com.au 2018). All the necessary information for the determination of

the financial performance of the company like revenue, profit/loss and others can be obtained

from this statement.

(Source: originenergy.com.au 2018)

The above figure is the published income statement of Origin Energy for the year ended

30 June 2017 (originenergy.com.au 2018). All the necessary information for the determination of

the financial performance of the company like revenue, profit/loss and others can be obtained

from this statement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CONTEMPORARY ISSUES IN ACCOUNTING

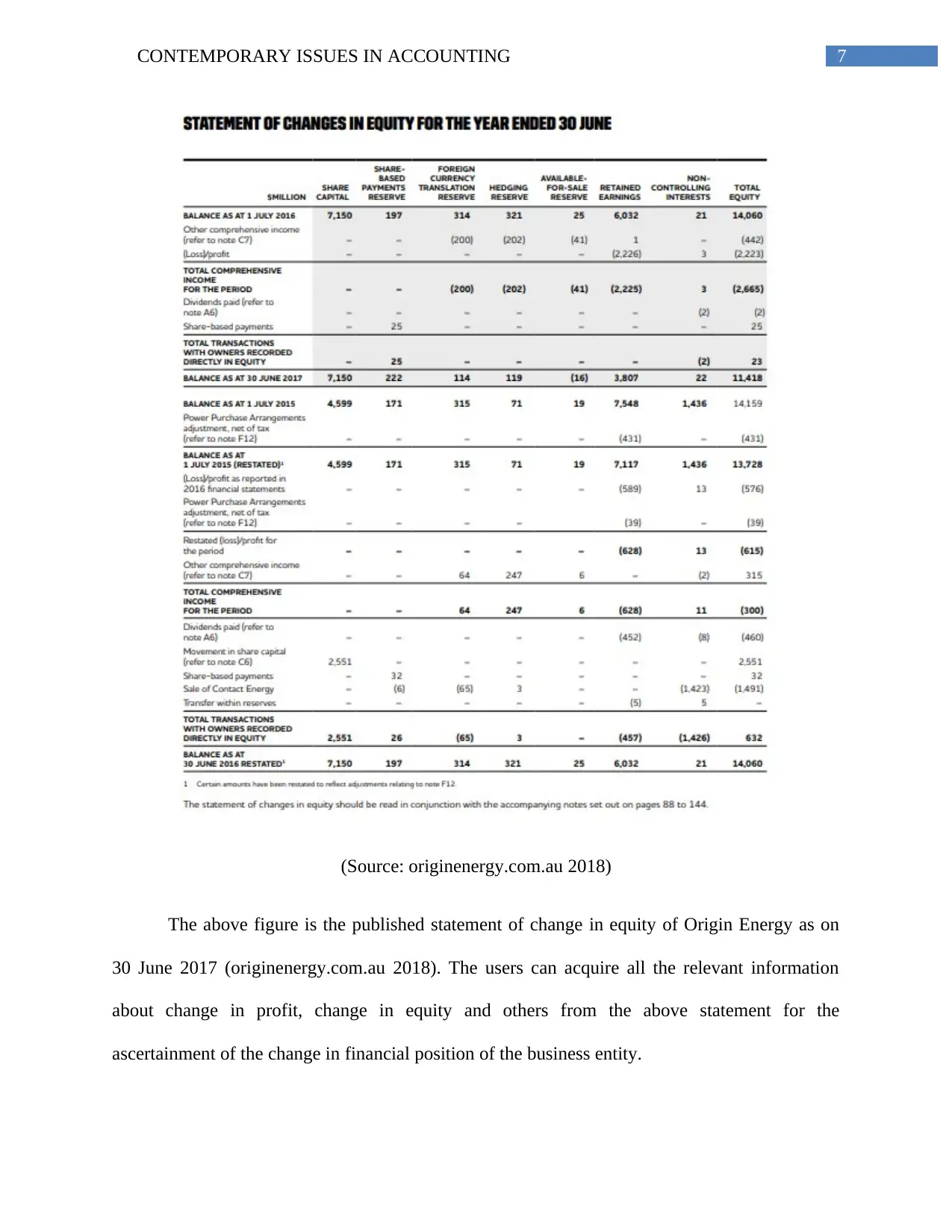

(Source: originenergy.com.au 2018)

The above figure is the published statement of change in equity of Origin Energy as on

30 June 2017 (originenergy.com.au 2018). The users can acquire all the relevant information

about change in profit, change in equity and others from the above statement for the

ascertainment of the change in financial position of the business entity.

(Source: originenergy.com.au 2018)

The above figure is the published statement of change in equity of Origin Energy as on

30 June 2017 (originenergy.com.au 2018). The users can acquire all the relevant information

about change in profit, change in equity and others from the above statement for the

ascertainment of the change in financial position of the business entity.

8CONTEMPORARY ISSUES IN ACCOUNTING

Moreover, as per the 2017 Annual Report of Origin Energy, the entity follows the

standards and principles of Australian Accounting Standard, Corporations Act 2001 and the

pronouncements of AASB to prepare and present the financial statements (originenergy.com.au

2018). Origin Energy also complies with the standards of International Financial Reporting

Standard (IFRS) as issued by IASB. Thus, the presence of all three objectives of AASB

conceptual framework can be seen in the financial reporting of Origin Energy

(originenergy.com.au 2018).

Target Audience of Conceptual Framework

Target audience of AASB conceptual framework is the uses of the financial statements;

they are shareholders, investors, creditors, banks, lenders, customers, taxation authority,

suppliers and the government. All these users require financial information for decision-making

process of different purposes (aasb.gov.au 2018). As per the earlier part of the report, it can be

observed that Origin Energy releases all the required financial information through some major

financial statements; like information about financial resources in the statement of financial

position, performance related information through income statement and change in financial

performance related information through the statement of change in equity. Thus, based on the

above discussion, it can be concluded that the target audience able to adequately use the financial

reports of Origin Energy for their needs (originenergy.com.au 2018).

Recognition Criteria

In the conceptual framework, AASB has provided some specific criteria for the ASX

listed companies in order to recognize assets, liabilities, equity, revenue and expenses and the

Moreover, as per the 2017 Annual Report of Origin Energy, the entity follows the

standards and principles of Australian Accounting Standard, Corporations Act 2001 and the

pronouncements of AASB to prepare and present the financial statements (originenergy.com.au

2018). Origin Energy also complies with the standards of International Financial Reporting

Standard (IFRS) as issued by IASB. Thus, the presence of all three objectives of AASB

conceptual framework can be seen in the financial reporting of Origin Energy

(originenergy.com.au 2018).

Target Audience of Conceptual Framework

Target audience of AASB conceptual framework is the uses of the financial statements;

they are shareholders, investors, creditors, banks, lenders, customers, taxation authority,

suppliers and the government. All these users require financial information for decision-making

process of different purposes (aasb.gov.au 2018). As per the earlier part of the report, it can be

observed that Origin Energy releases all the required financial information through some major

financial statements; like information about financial resources in the statement of financial

position, performance related information through income statement and change in financial

performance related information through the statement of change in equity. Thus, based on the

above discussion, it can be concluded that the target audience able to adequately use the financial

reports of Origin Energy for their needs (originenergy.com.au 2018).

Recognition Criteria

In the conceptual framework, AASB has provided some specific criteria for the ASX

listed companies in order to recognize assets, liabilities, equity, revenue and expenses and the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CONTEMPORARY ISSUES IN ACCOUNTING

business entities must follow these recognition criteria. The following discussion shows the

compliance of Origin Energy with these recognition criteria of AASB.

ASSET: The asset recognition criteria of AASB is shown below:

It is probable that the future economic benefits of the assets will be flown to the business

entities, and

Reliable measurement of these assets can be done (aasb.gov.au 2018).

For the recognition of property, plant and machinery (PPE), Origin Energy uses cost method

after deducting depreciation, depletion, amortization and impairment charges as per AASB 116

(aasb.gov.au 2018). The same technique is followed for the recognition of intangible assets

including goodwill as per AASB 138. The recognition of trade receivable is done based on the

amount billed to the customers. Hence, it can be observed that Origin Energy will be beneficial

with these assets and they can be reliably measured.

LIABILITY: The AASB liability recognition criteria is shown below:

It is probable that the future economic benefits of the liabilities will be flown from the

business entities, and

Reliable measurement of these liabilities can be done (aasb.gov.au 2018).

Interest-bearing liabilities are the long-term borrowings in Origin Energy and their

recognition is done based on fair value after the deduction of transaction cost and the company

has to repay these borrowings. Origin Energy recognizes their other liabilities on their net value.

Thus, it can be seen that the company has to pay all the liabilities and they can be measured

(originenergy.com.au 2018).

business entities must follow these recognition criteria. The following discussion shows the

compliance of Origin Energy with these recognition criteria of AASB.

ASSET: The asset recognition criteria of AASB is shown below:

It is probable that the future economic benefits of the assets will be flown to the business

entities, and

Reliable measurement of these assets can be done (aasb.gov.au 2018).

For the recognition of property, plant and machinery (PPE), Origin Energy uses cost method

after deducting depreciation, depletion, amortization and impairment charges as per AASB 116

(aasb.gov.au 2018). The same technique is followed for the recognition of intangible assets

including goodwill as per AASB 138. The recognition of trade receivable is done based on the

amount billed to the customers. Hence, it can be observed that Origin Energy will be beneficial

with these assets and they can be reliably measured.

LIABILITY: The AASB liability recognition criteria is shown below:

It is probable that the future economic benefits of the liabilities will be flown from the

business entities, and

Reliable measurement of these liabilities can be done (aasb.gov.au 2018).

Interest-bearing liabilities are the long-term borrowings in Origin Energy and their

recognition is done based on fair value after the deduction of transaction cost and the company

has to repay these borrowings. Origin Energy recognizes their other liabilities on their net value.

Thus, it can be seen that the company has to pay all the liabilities and they can be measured

(originenergy.com.au 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CONTEMPORARY ISSUES IN ACCOUNTING

EQUITY: As per the regulation of AASB, business entities are required to follow the same

criteria as assets and liabilities for the recognition of equity. Thus, there is not any exception of

this fact in case of Origin Energy. The company does not have any authorised capital on par

value (aasb.gov.au 2018).

REVENUE: The AASB criteria for revenue recognition of provided below:

It is probable that the future economic benefits will be flown to the business entities, and

It is possible to measure the inflow of future benefits (aasb.gov.au 2018).

Origin Energy recognizes their business revenue at the time of the transfer of the community

to the customer (originenergy.com.au 2018).

EXPENSES: The AASB recognition criteria for expenses is shown below:

It is probable that the future economic benefits will be flown from the business entities,

and

It is possible to measure the outflow of future benefits (aasb.gov.au 2018).

Origin Energy recognizes all of their business expenses at the time of their occurrences and

there is flow of future benefits from the company as Origin Energy has to pay all of their

expenses (originenergy.com.au 2018).

Fundamental Qualitative Characteristics

As per AASB conceptual framework, the fundamental characteristics of financial

information are Relevant and Faithful Representation.

EQUITY: As per the regulation of AASB, business entities are required to follow the same

criteria as assets and liabilities for the recognition of equity. Thus, there is not any exception of

this fact in case of Origin Energy. The company does not have any authorised capital on par

value (aasb.gov.au 2018).

REVENUE: The AASB criteria for revenue recognition of provided below:

It is probable that the future economic benefits will be flown to the business entities, and

It is possible to measure the inflow of future benefits (aasb.gov.au 2018).

Origin Energy recognizes their business revenue at the time of the transfer of the community

to the customer (originenergy.com.au 2018).

EXPENSES: The AASB recognition criteria for expenses is shown below:

It is probable that the future economic benefits will be flown from the business entities,

and

It is possible to measure the outflow of future benefits (aasb.gov.au 2018).

Origin Energy recognizes all of their business expenses at the time of their occurrences and

there is flow of future benefits from the company as Origin Energy has to pay all of their

expenses (originenergy.com.au 2018).

Fundamental Qualitative Characteristics

As per AASB conceptual framework, the fundamental characteristics of financial

information are Relevant and Faithful Representation.

11CONTEMPORARY ISSUES IN ACCOUNTING

As per relevance characteristic, financial information should be able to create positive

difference in the decision-making process of the users (Zhang and Andrew 2014). Earlier

discussion shows that Origin Energy releases all the relevant financial information trough the

publication of their necessary financial statements (originenergy.com.au 2018).

As per faithful representation characteristic, financial statements should reflect all the

financial information about the economic phenomena of the business entities (Cascino et al.

2014). The auditors of Origin Energy have provided the opinion that the company has prepared

their financial statements as per the required financial standards (originenergy.com.au 2018).

Enhancing Qualitative Characteristics

According to AASB conceptual framework, the enhancing qualitative characteristics of

financial reporting are Comparability, Verifiability, Timeliness and Understandability.

Comparability helps in comparing the financial information of companies with the other

companies with the application of required knowledge (Henderson et al. 2015). The provided

financial information of Origin Energy can be easily compared with the other companies in the

presence of required financial knowledge (originenergy.com.au 2018).

Verifiability helps the users in making out the underlying accounting treatments and

assumptions behind the financial reporting of the entities (Christensen and Nikolaev 2013).

Faithful representation of the financial statements ensures the verifiability of the financial

information of Origin Energy (originenergy.com.au 2018).

Timeliness helps in reaching financial information to the users when required (Zeff

2013). Origin Energy releases their financial statements at a particular time of the year that

As per relevance characteristic, financial information should be able to create positive

difference in the decision-making process of the users (Zhang and Andrew 2014). Earlier

discussion shows that Origin Energy releases all the relevant financial information trough the

publication of their necessary financial statements (originenergy.com.au 2018).

As per faithful representation characteristic, financial statements should reflect all the

financial information about the economic phenomena of the business entities (Cascino et al.

2014). The auditors of Origin Energy have provided the opinion that the company has prepared

their financial statements as per the required financial standards (originenergy.com.au 2018).

Enhancing Qualitative Characteristics

According to AASB conceptual framework, the enhancing qualitative characteristics of

financial reporting are Comparability, Verifiability, Timeliness and Understandability.

Comparability helps in comparing the financial information of companies with the other

companies with the application of required knowledge (Henderson et al. 2015). The provided

financial information of Origin Energy can be easily compared with the other companies in the

presence of required financial knowledge (originenergy.com.au 2018).

Verifiability helps the users in making out the underlying accounting treatments and

assumptions behind the financial reporting of the entities (Christensen and Nikolaev 2013).

Faithful representation of the financial statements ensures the verifiability of the financial

information of Origin Energy (originenergy.com.au 2018).

Timeliness helps in reaching financial information to the users when required (Zeff

2013). Origin Energy releases their financial statements at a particular time of the year that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.