Financial Accounting Report: Oroton Group

VerifiedAdded on 2019/10/30

|12

|1898

|87

Report

AI Summary

This report provides a detailed financial analysis of the Oroton Group Limited for the fiscal year ending July 30, 2016. It begins with an overview of the company's history and principal activities, which include retailing and wholesaling leather goods, fashion apparel, and accessories. The report then examines key aspects of the annual report, including the statement of financial position, the independent auditor's report (by PricewaterhouseCoopers), and details about the directors. A significant portion of the report is dedicated to a ratio analysis, covering profitability ratios (net profit margin, return on assets, return on equity), liquidity ratios (current ratio, asset turnover), and leverage ratios (debt-to-equity ratio, interest coverage ratio). The analysis shows improvements in several key metrics compared to the previous year (2015), indicating a positive trend in the company's financial performance. The report concludes that Oroton Group's overall financial position is sound and satisfactory, with better performance than in 2015.

RUNNING HEAD: FINANCIAL ACCOUNTING

FINANCIAL ACCOUNTING

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING 1

Contents

OROTON..............................................................................................................................................2

1.........................................................................................................................................................2

2.........................................................................................................................................................3

3.........................................................................................................................................................3

4.........................................................................................................................................................5

5.........................................................................................................................................................6

6.........................................................................................................................................................7

7.........................................................................................................................................................7

8.........................................................................................................................................................7

Conclusion.......................................................................................................................................11

References.......................................................................................................................................12

Contents

OROTON..............................................................................................................................................2

1.........................................................................................................................................................2

2.........................................................................................................................................................3

3.........................................................................................................................................................3

4.........................................................................................................................................................5

5.........................................................................................................................................................6

6.........................................................................................................................................................7

7.........................................................................................................................................................7

8.........................................................................................................................................................7

Conclusion.......................................................................................................................................11

References.......................................................................................................................................12

FINANCIAL ACCOUNTING 2

OROTON

1.

Oroton is founded in 1938 by Boyd Lane. The Oroton has originated from the latin word

which is ‘oro’ meaning is ‘gold’ and ‘ton’ meaning is ‘a tonne of gold and fortune’.

History and Background:

Oroton is an Australian Company dealing in the finest quality of iconic sixties and

seventies gold and silver women accessories. The company is based in Sydney, Australia.

In 1938, Body Lane has started a textile design company imports finest quality of textiles

from Europe. Further in 1951, Oroton became the most luxurious and elegant brand for

women in fashion world (Oroton, 2017). In 1987, the Oroton Group became listed in

ASX. Later in 2000, it has expanded its collection of sunglasses and optical eyewear. In

2006, it has launched its online channel named oroton.com. In today’s world, Oroton has

evolved to be the most loved brands. Thus, it became the leading luxury lifestyle brand in

Australia. It has broadened its horizon in New Zealand, Hong Kong, Malaysia and

Singapore (Oroton, 2017).

Principal Activities:

Retailing and wholesaling of leather goods.

Fashion Apparel and fashion Accessories.

The products Oroton Group deal in are as follows:

a. Bags (includes Backpacks, Totes, Pouches, Satchels, Briefcases etc.).

b. Accessories (includes Belts, mirrors, keyrings, Scarves, Sunglasses etc.).

c. Watches

d. Wallets

OROTON

1.

Oroton is founded in 1938 by Boyd Lane. The Oroton has originated from the latin word

which is ‘oro’ meaning is ‘gold’ and ‘ton’ meaning is ‘a tonne of gold and fortune’.

History and Background:

Oroton is an Australian Company dealing in the finest quality of iconic sixties and

seventies gold and silver women accessories. The company is based in Sydney, Australia.

In 1938, Body Lane has started a textile design company imports finest quality of textiles

from Europe. Further in 1951, Oroton became the most luxurious and elegant brand for

women in fashion world (Oroton, 2017). In 1987, the Oroton Group became listed in

ASX. Later in 2000, it has expanded its collection of sunglasses and optical eyewear. In

2006, it has launched its online channel named oroton.com. In today’s world, Oroton has

evolved to be the most loved brands. Thus, it became the leading luxury lifestyle brand in

Australia. It has broadened its horizon in New Zealand, Hong Kong, Malaysia and

Singapore (Oroton, 2017).

Principal Activities:

Retailing and wholesaling of leather goods.

Fashion Apparel and fashion Accessories.

The products Oroton Group deal in are as follows:

a. Bags (includes Backpacks, Totes, Pouches, Satchels, Briefcases etc.).

b. Accessories (includes Belts, mirrors, keyrings, Scarves, Sunglasses etc.).

c. Watches

d. Wallets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING 3

e. Fragrances

f. Jewellery

Retailing of fashion label under GAP Label

Licensing of Oroton Brand Name (Annual report, 2016).

The fiscal year under review is 30 July 2016.

2.

Looking at the contents page, section of ‘Statement of financial position’ and

‘Independent auditors report’ dominates the report (Annual report, 2016).

3.

Directors:

S. No. Name Comment

1. John P Schmoll Title: Chairman

Expertise and Experience:

He was retired as a CFO in Coles

Myer Ltd.

Prior to this, he was a senior

professional in Arthur Young and

Edgars Stores Ltd which is the

largest apparel and homeware

retailer in Australia and South

Africa.

He is currently non-executive

director in Patties Foods Ltd.

In Oroton Group, he is a member

of Audit Committee and people

e. Fragrances

f. Jewellery

Retailing of fashion label under GAP Label

Licensing of Oroton Brand Name (Annual report, 2016).

The fiscal year under review is 30 July 2016.

2.

Looking at the contents page, section of ‘Statement of financial position’ and

‘Independent auditors report’ dominates the report (Annual report, 2016).

3.

Directors:

S. No. Name Comment

1. John P Schmoll Title: Chairman

Expertise and Experience:

He was retired as a CFO in Coles

Myer Ltd.

Prior to this, he was a senior

professional in Arthur Young and

Edgars Stores Ltd which is the

largest apparel and homeware

retailer in Australia and South

Africa.

He is currently non-executive

director in Patties Foods Ltd.

In Oroton Group, he is a member

of Audit Committee and people

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING 4

and organisation Committee.

He has an interest in 60,000

ordinary shares.

His total remuneration in 2016

was A$ 162,151.

2. Mark Newman Title: Managing Director and CEO

Expertise and Experience:

He has an experience of over 30

years in apparel and accessories

brands of UK and Asia.

He was VP of Ralph Lauren

Australia and New Zealand in the

year 2010.

Prior to this, He has handled a

senior management and

marketing roles in Richemont

Group in Europe, Hong Kong

and Japan.

He was also a senior professional

in Hackett brand of UK.

Mark has an interest in 48,092

ordinary shares.

His total remuneration in 2016

was A$ 570,412.

and organisation Committee.

He has an interest in 60,000

ordinary shares.

His total remuneration in 2016

was A$ 162,151.

2. Mark Newman Title: Managing Director and CEO

Expertise and Experience:

He has an experience of over 30

years in apparel and accessories

brands of UK and Asia.

He was VP of Ralph Lauren

Australia and New Zealand in the

year 2010.

Prior to this, He has handled a

senior management and

marketing roles in Richemont

Group in Europe, Hong Kong

and Japan.

He was also a senior professional

in Hackett brand of UK.

Mark has an interest in 48,092

ordinary shares.

His total remuneration in 2016

was A$ 570,412.

FINANCIAL ACCOUNTING 5

3. J Will Vicars Title: Non-Executive Director

Expertise and Experience:

He has a vast experience in

financial markets i.e. he was

senior portfolio manager at

NRMA investments and in BT

Australia.

Currently he is chief Investment

officer in Caledonia Private

Investments Pty Limited.

He is a Vice Chairman at St.

Luke’s Hospital foundation.

In Oroton Group, he is a member

of Audit Committee.

He has an interest in 7,229,920

ordinary shares.

His total remuneration in 2016

was A$ 85,129.

4.

Auditors:

PricewaterhouseCoopers are the Auditors of the Oroton Group Limited.

Auditors Opinion:

PWC has conducted the audit of financial statements of Oroton Group Limited

in accordance with Australian Auditing standards (PWC, 2017).

In auditor’s report following line of items are opined:

3. J Will Vicars Title: Non-Executive Director

Expertise and Experience:

He has a vast experience in

financial markets i.e. he was

senior portfolio manager at

NRMA investments and in BT

Australia.

Currently he is chief Investment

officer in Caledonia Private

Investments Pty Limited.

He is a Vice Chairman at St.

Luke’s Hospital foundation.

In Oroton Group, he is a member

of Audit Committee.

He has an interest in 7,229,920

ordinary shares.

His total remuneration in 2016

was A$ 85,129.

4.

Auditors:

PricewaterhouseCoopers are the Auditors of the Oroton Group Limited.

Auditors Opinion:

PWC has conducted the audit of financial statements of Oroton Group Limited

in accordance with Australian Auditing standards (PWC, 2017).

In auditor’s report following line of items are opined:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING 6

o Report on the financial report:

PWC has declared that the Oroton Group Limited has not made any

contravention in preparing financial statements of the year ended 30

July 2016. They have prepared the financial report in accordance with

Australian Accounting Standards (AASB 101) which is in comply with

IFRS as well as Corporation Act 2001.

o Report on the remuneration report:

In remuneration report, the auditors declare that section 300A of the

Corporation Act 2001 are fully complied with (PWC, 2017).

Further there were no contraventions in auditor independence requirements in

Corporation Act 2001 as well as no contraventions of any code of professional

conduct in relation to conducting audit.

The financial statements were signed by Kristin Stubbins (Partner).

5.

Sales:

Particulars 2016 ($’000) 2015 ($’000)

Revenue 136,439 132,017

(Source: Annual Report, 2016; 2015).

Comment: It has been seen from the above table that Revenue has increased in 2016 over

2015.

The reason being that the group has increased its outlets globally and also more people are

buying from the online channel which grows considerably year on year and also the

collections are prompt. Recently the company has awarded with the best Australian fashion

o Report on the financial report:

PWC has declared that the Oroton Group Limited has not made any

contravention in preparing financial statements of the year ended 30

July 2016. They have prepared the financial report in accordance with

Australian Accounting Standards (AASB 101) which is in comply with

IFRS as well as Corporation Act 2001.

o Report on the remuneration report:

In remuneration report, the auditors declare that section 300A of the

Corporation Act 2001 are fully complied with (PWC, 2017).

Further there were no contraventions in auditor independence requirements in

Corporation Act 2001 as well as no contraventions of any code of professional

conduct in relation to conducting audit.

The financial statements were signed by Kristin Stubbins (Partner).

5.

Sales:

Particulars 2016 ($’000) 2015 ($’000)

Revenue 136,439 132,017

(Source: Annual Report, 2016; 2015).

Comment: It has been seen from the above table that Revenue has increased in 2016 over

2015.

The reason being that the group has increased its outlets globally and also more people are

buying from the online channel which grows considerably year on year and also the

collections are prompt. Recently the company has awarded with the best Australian fashion

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING 7

brand. Moreover, in 2015 the group has come up with the 2 new designs which signifies that

the sales must have increased due to these factors.

6.

Cash flows from operating activities:

Particulars 2016 ($’000) 2015 ($’000)

Net Cash flow from

operating activities

13,825 -2,443

(Source: Annual Report, 2016; 2015).

Comment: It has been seen from the above table that Net Cash flow from operating activities

has increased in 2016 over 2015 by 665.90%.

7.

Retained Profits:

Particulars 2016 ($’000)

Retained Profits 16,106

(Source: Annual Report, 2016; 2015).

No, the company does not have borrowings at the year-end 30 July 2016.

8.

Ratios:

i. Profitability ratios:

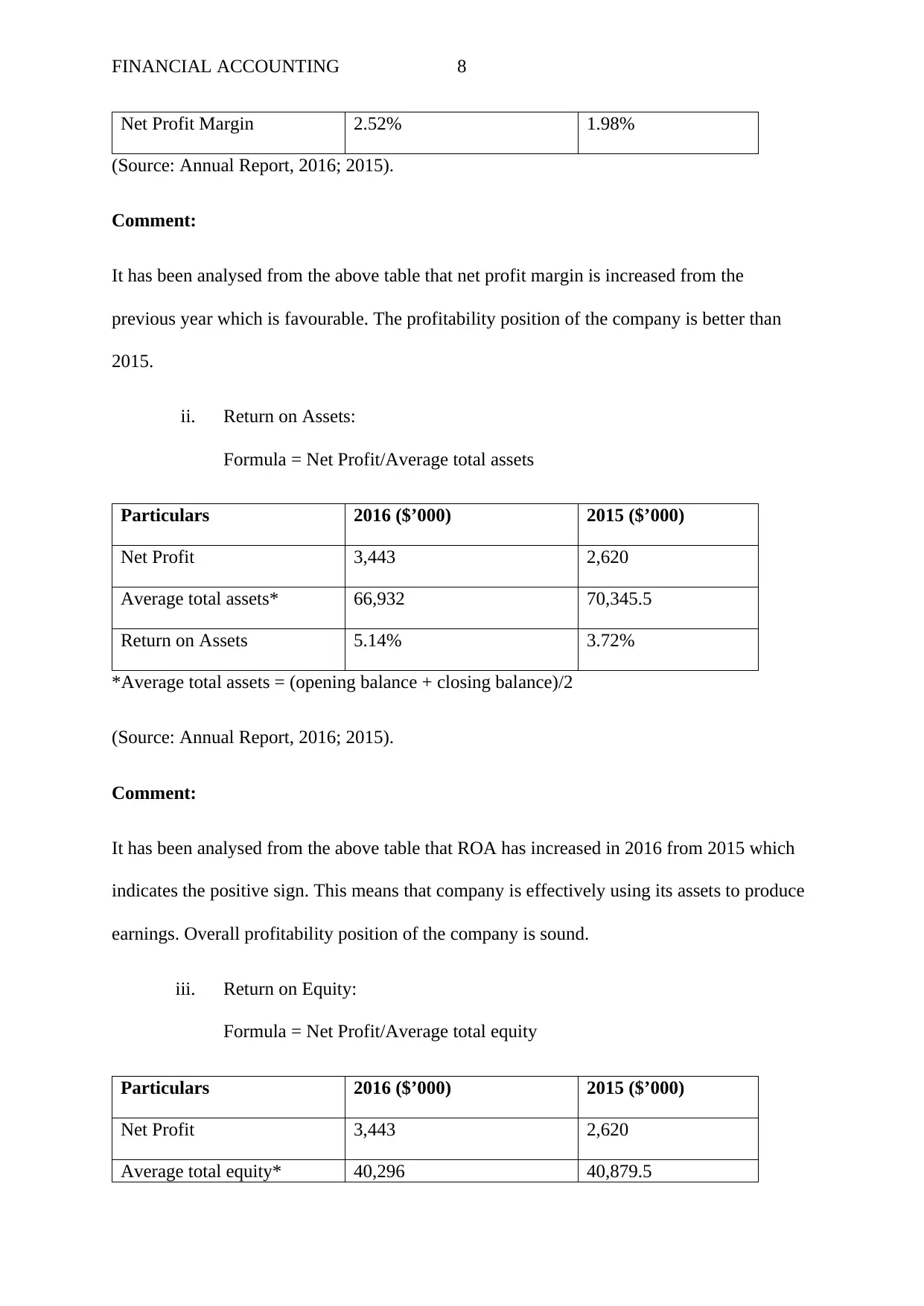

i. Net Profit Margin:

Formula = Net Profit/Revenue

Particulars 2016 ($’000) 2015 ($’000)

Net Profit 3,443 2,620

Revenue 136,439 132,017

brand. Moreover, in 2015 the group has come up with the 2 new designs which signifies that

the sales must have increased due to these factors.

6.

Cash flows from operating activities:

Particulars 2016 ($’000) 2015 ($’000)

Net Cash flow from

operating activities

13,825 -2,443

(Source: Annual Report, 2016; 2015).

Comment: It has been seen from the above table that Net Cash flow from operating activities

has increased in 2016 over 2015 by 665.90%.

7.

Retained Profits:

Particulars 2016 ($’000)

Retained Profits 16,106

(Source: Annual Report, 2016; 2015).

No, the company does not have borrowings at the year-end 30 July 2016.

8.

Ratios:

i. Profitability ratios:

i. Net Profit Margin:

Formula = Net Profit/Revenue

Particulars 2016 ($’000) 2015 ($’000)

Net Profit 3,443 2,620

Revenue 136,439 132,017

FINANCIAL ACCOUNTING 8

Net Profit Margin 2.52% 1.98%

(Source: Annual Report, 2016; 2015).

Comment:

It has been analysed from the above table that net profit margin is increased from the

previous year which is favourable. The profitability position of the company is better than

2015.

ii. Return on Assets:

Formula = Net Profit/Average total assets

Particulars 2016 ($’000) 2015 ($’000)

Net Profit 3,443 2,620

Average total assets* 66,932 70,345.5

Return on Assets 5.14% 3.72%

*Average total assets = (opening balance + closing balance)/2

(Source: Annual Report, 2016; 2015).

Comment:

It has been analysed from the above table that ROA has increased in 2016 from 2015 which

indicates the positive sign. This means that company is effectively using its assets to produce

earnings. Overall profitability position of the company is sound.

iii. Return on Equity:

Formula = Net Profit/Average total equity

Particulars 2016 ($’000) 2015 ($’000)

Net Profit 3,443 2,620

Average total equity* 40,296 40,879.5

Net Profit Margin 2.52% 1.98%

(Source: Annual Report, 2016; 2015).

Comment:

It has been analysed from the above table that net profit margin is increased from the

previous year which is favourable. The profitability position of the company is better than

2015.

ii. Return on Assets:

Formula = Net Profit/Average total assets

Particulars 2016 ($’000) 2015 ($’000)

Net Profit 3,443 2,620

Average total assets* 66,932 70,345.5

Return on Assets 5.14% 3.72%

*Average total assets = (opening balance + closing balance)/2

(Source: Annual Report, 2016; 2015).

Comment:

It has been analysed from the above table that ROA has increased in 2016 from 2015 which

indicates the positive sign. This means that company is effectively using its assets to produce

earnings. Overall profitability position of the company is sound.

iii. Return on Equity:

Formula = Net Profit/Average total equity

Particulars 2016 ($’000) 2015 ($’000)

Net Profit 3,443 2,620

Average total equity* 40,296 40,879.5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING 9

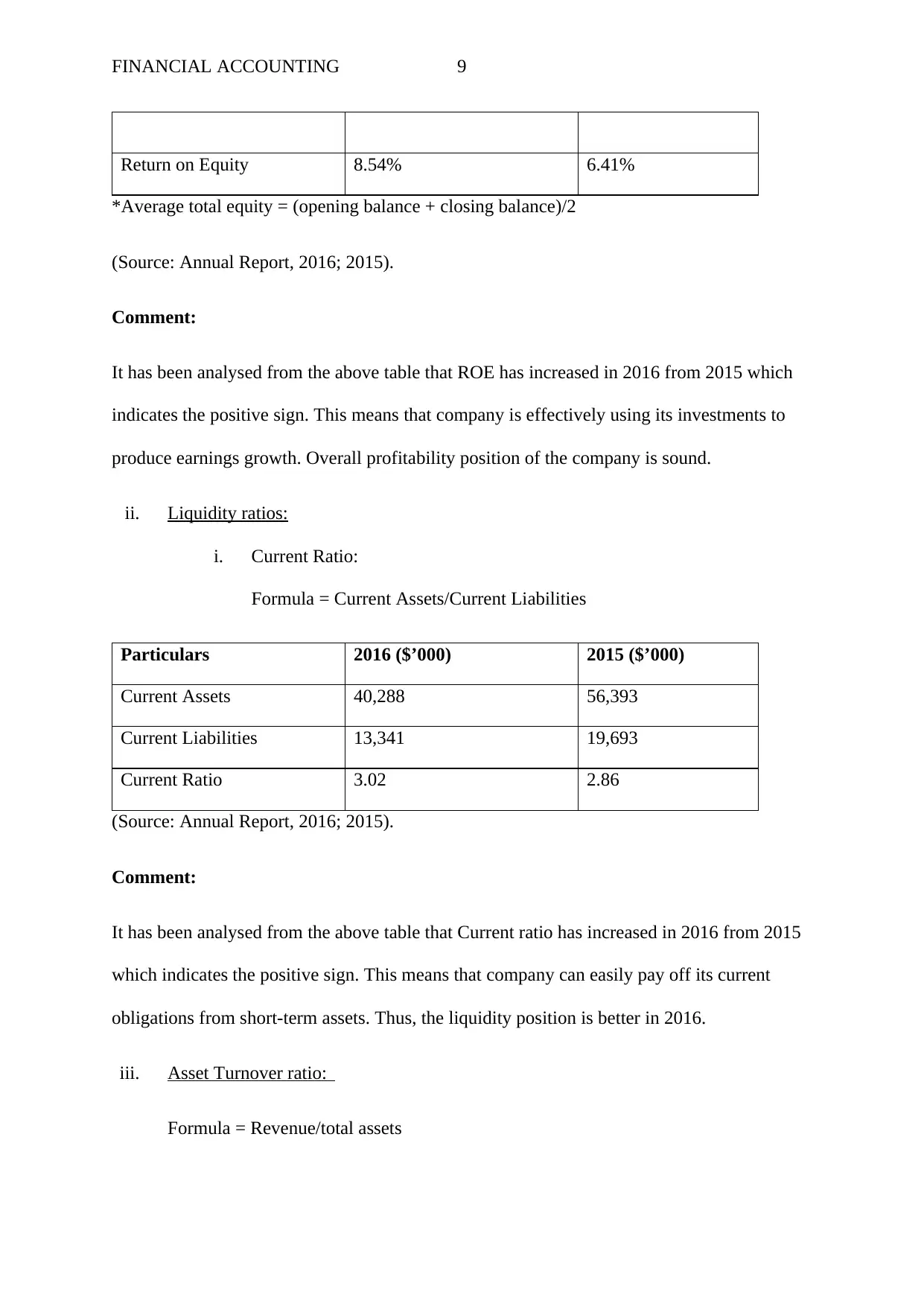

Return on Equity 8.54% 6.41%

*Average total equity = (opening balance + closing balance)/2

(Source: Annual Report, 2016; 2015).

Comment:

It has been analysed from the above table that ROE has increased in 2016 from 2015 which

indicates the positive sign. This means that company is effectively using its investments to

produce earnings growth. Overall profitability position of the company is sound.

ii. Liquidity ratios:

i. Current Ratio:

Formula = Current Assets/Current Liabilities

Particulars 2016 ($’000) 2015 ($’000)

Current Assets 40,288 56,393

Current Liabilities 13,341 19,693

Current Ratio 3.02 2.86

(Source: Annual Report, 2016; 2015).

Comment:

It has been analysed from the above table that Current ratio has increased in 2016 from 2015

which indicates the positive sign. This means that company can easily pay off its current

obligations from short-term assets. Thus, the liquidity position is better in 2016.

iii. Asset Turnover ratio:

Formula = Revenue/total assets

Return on Equity 8.54% 6.41%

*Average total equity = (opening balance + closing balance)/2

(Source: Annual Report, 2016; 2015).

Comment:

It has been analysed from the above table that ROE has increased in 2016 from 2015 which

indicates the positive sign. This means that company is effectively using its investments to

produce earnings growth. Overall profitability position of the company is sound.

ii. Liquidity ratios:

i. Current Ratio:

Formula = Current Assets/Current Liabilities

Particulars 2016 ($’000) 2015 ($’000)

Current Assets 40,288 56,393

Current Liabilities 13,341 19,693

Current Ratio 3.02 2.86

(Source: Annual Report, 2016; 2015).

Comment:

It has been analysed from the above table that Current ratio has increased in 2016 from 2015

which indicates the positive sign. This means that company can easily pay off its current

obligations from short-term assets. Thus, the liquidity position is better in 2016.

iii. Asset Turnover ratio:

Formula = Revenue/total assets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING 10

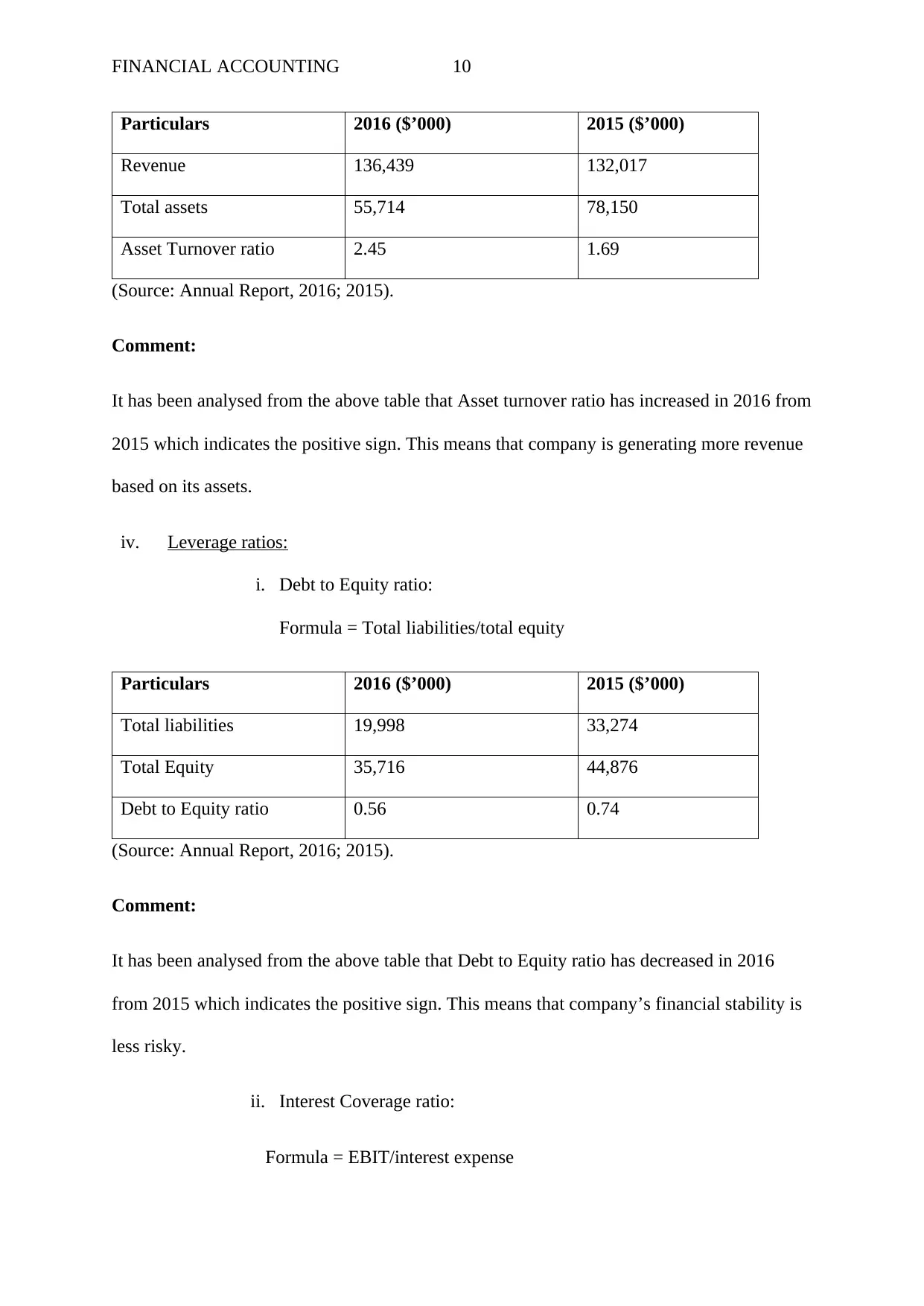

Particulars 2016 ($’000) 2015 ($’000)

Revenue 136,439 132,017

Total assets 55,714 78,150

Asset Turnover ratio 2.45 1.69

(Source: Annual Report, 2016; 2015).

Comment:

It has been analysed from the above table that Asset turnover ratio has increased in 2016 from

2015 which indicates the positive sign. This means that company is generating more revenue

based on its assets.

iv. Leverage ratios:

i. Debt to Equity ratio:

Formula = Total liabilities/total equity

Particulars 2016 ($’000) 2015 ($’000)

Total liabilities 19,998 33,274

Total Equity 35,716 44,876

Debt to Equity ratio 0.56 0.74

(Source: Annual Report, 2016; 2015).

Comment:

It has been analysed from the above table that Debt to Equity ratio has decreased in 2016

from 2015 which indicates the positive sign. This means that company’s financial stability is

less risky.

ii. Interest Coverage ratio:

Formula = EBIT/interest expense

Particulars 2016 ($’000) 2015 ($’000)

Revenue 136,439 132,017

Total assets 55,714 78,150

Asset Turnover ratio 2.45 1.69

(Source: Annual Report, 2016; 2015).

Comment:

It has been analysed from the above table that Asset turnover ratio has increased in 2016 from

2015 which indicates the positive sign. This means that company is generating more revenue

based on its assets.

iv. Leverage ratios:

i. Debt to Equity ratio:

Formula = Total liabilities/total equity

Particulars 2016 ($’000) 2015 ($’000)

Total liabilities 19,998 33,274

Total Equity 35,716 44,876

Debt to Equity ratio 0.56 0.74

(Source: Annual Report, 2016; 2015).

Comment:

It has been analysed from the above table that Debt to Equity ratio has decreased in 2016

from 2015 which indicates the positive sign. This means that company’s financial stability is

less risky.

ii. Interest Coverage ratio:

Formula = EBIT/interest expense

FINANCIAL ACCOUNTING 11

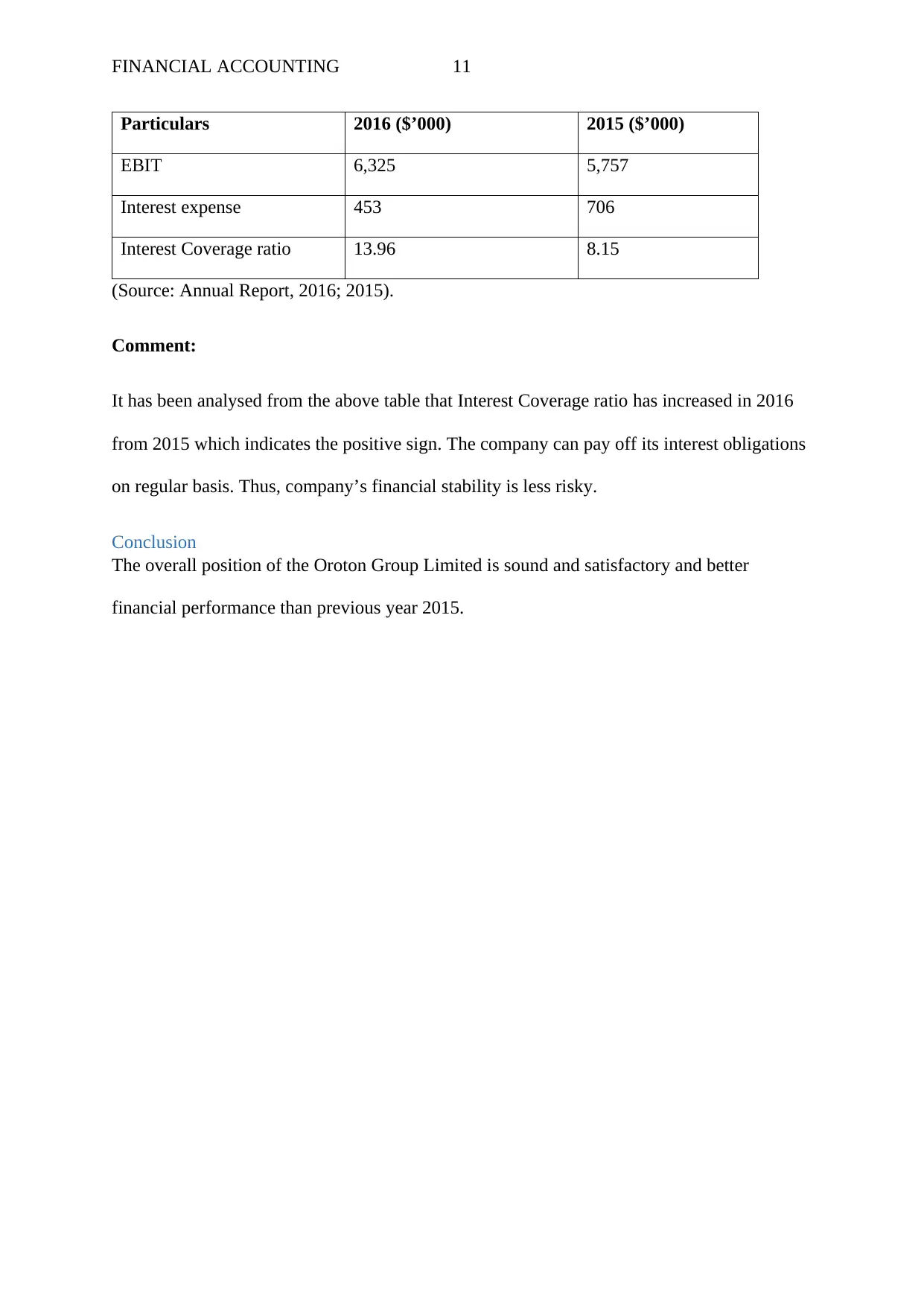

Particulars 2016 ($’000) 2015 ($’000)

EBIT 6,325 5,757

Interest expense 453 706

Interest Coverage ratio 13.96 8.15

(Source: Annual Report, 2016; 2015).

Comment:

It has been analysed from the above table that Interest Coverage ratio has increased in 2016

from 2015 which indicates the positive sign. The company can pay off its interest obligations

on regular basis. Thus, company’s financial stability is less risky.

Conclusion

The overall position of the Oroton Group Limited is sound and satisfactory and better

financial performance than previous year 2015.

Particulars 2016 ($’000) 2015 ($’000)

EBIT 6,325 5,757

Interest expense 453 706

Interest Coverage ratio 13.96 8.15

(Source: Annual Report, 2016; 2015).

Comment:

It has been analysed from the above table that Interest Coverage ratio has increased in 2016

from 2015 which indicates the positive sign. The company can pay off its interest obligations

on regular basis. Thus, company’s financial stability is less risky.

Conclusion

The overall position of the Oroton Group Limited is sound and satisfactory and better

financial performance than previous year 2015.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.