OrotonGroup Limited and Kathmandu Limited: Ratio Analysis Report

VerifiedAdded on 2020/02/24

|7

|1488

|62

Report

AI Summary

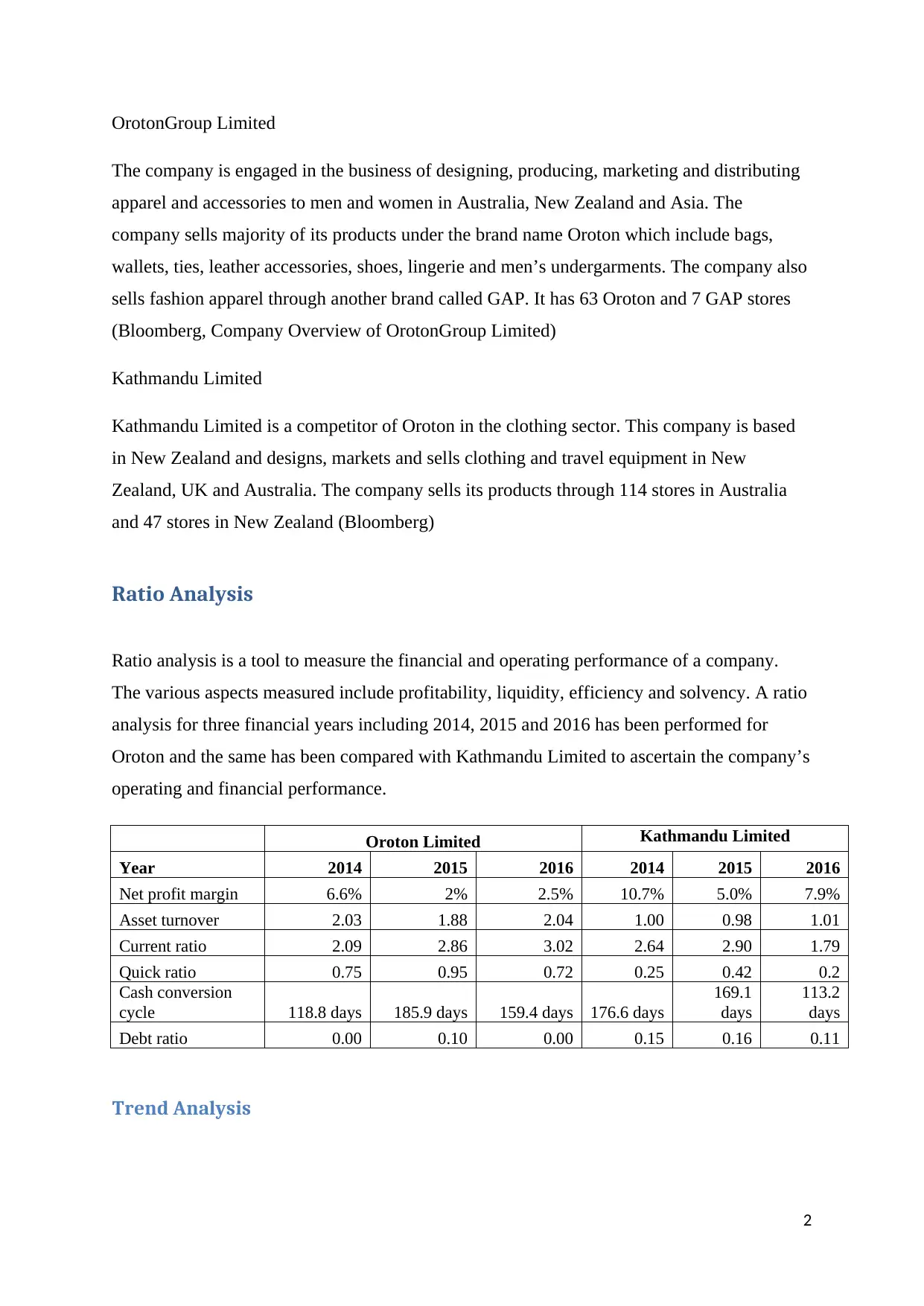

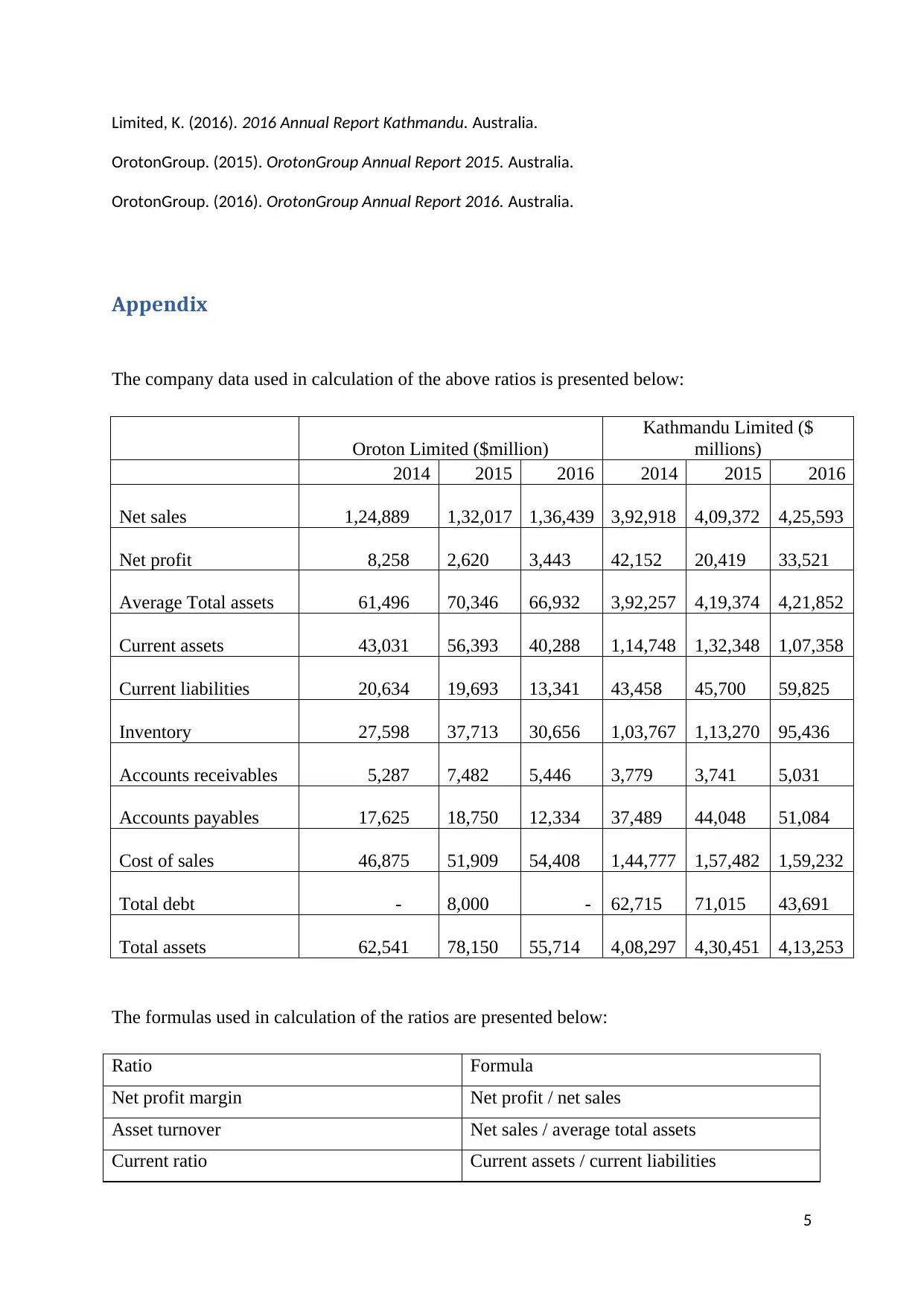

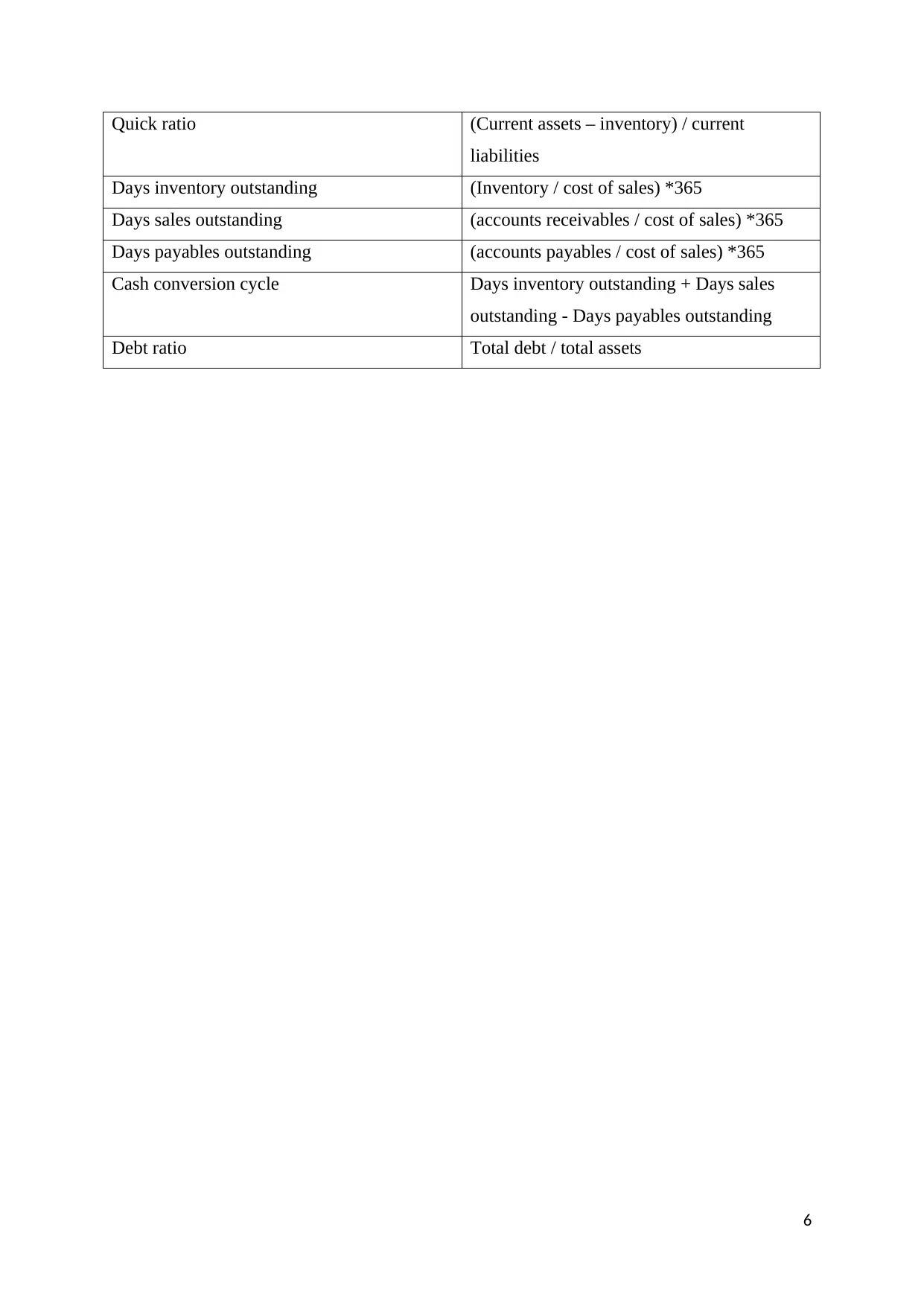

This report presents a detailed ratio analysis comparing the financial performance of OrotonGroup Limited and Kathmandu Limited over three years (2014-2016). The analysis covers key financial ratios, including net profit margin, asset turnover, current ratio, quick ratio, cash conversion cycle, and debt ratio. The report examines trends in these ratios for both companies, highlighting OrotonGroup's lower profit margins but higher asset turnover compared to Kathmandu. A competitor analysis is performed to benchmark Oroton's performance against Kathmandu. The report concludes with recommendations for OrotonGroup to improve its financial performance, focusing on strategies to enhance profit margins, reduce the cash conversion cycle, and improve receivables collection. Data from the companies' annual reports is used to support the calculations and findings.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.