Management Accounting System, Reporting, and Budgeting for Oshodi plc

VerifiedAdded on 2021/02/20

|16

|5405

|60

Report

AI Summary

This report provides a detailed analysis of management accounting principles and their application within Oshodi plc, a fruit juice manufacturing firm. It covers various aspects of management accounting, including management accounting systems (inventory, cost, job costing, and price optimization), reporting methods (account receivable, budget, performance, and cost management reports), and the integration of these systems with organizational processes. The report examines the benefits of different accounting systems and explores the preparation of income statements using both absorption and marginal costing. Furthermore, it discusses the advantages and disadvantages of planning tools, their application in budgeting and forecasting, and compares organizational approaches to solving financial issues with the help of accounting systems. The report aims to provide insights into how management accounting can support strategic decision-making and contribute to the sustainable success of the organization.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................2

MAIN BODY ..................................................................................................................................2

TASK 1............................................................................................................................................2

P1. Management accounting systems and its requirements:........................................................2

P2. Methods in management accounting reporting......................................................................4

D1. Management accounting system and reporting integrated with organisational process.......6

TASK 2............................................................................................................................................6

P3. Preparation of income statements by using absorption and marginal costing......................6

M2. Management accounting techniques for preparation of financial reporting documents......8

D2. Interpretation of income statements......................................................................................9

TASK 3............................................................................................................................................9

P4. Advantages and disadvantages of planning tools..................................................................9

M3. Various kind of planning tools and their application for preparing and forecasting of

budget.........................................................................................................................................10

TASK 4..........................................................................................................................................10

P5. Comparison of organisations to solve the financial issues with the help of accounting

systems.......................................................................................................................................10

M4. Management accounting to solve the financial issues........................................................13

D3. Planning tools to resolve financial problems so to lead the organisation towards

sustainable success.....................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

1

INTRODUCTION...........................................................................................................................2

MAIN BODY ..................................................................................................................................2

TASK 1............................................................................................................................................2

P1. Management accounting systems and its requirements:........................................................2

P2. Methods in management accounting reporting......................................................................4

D1. Management accounting system and reporting integrated with organisational process.......6

TASK 2............................................................................................................................................6

P3. Preparation of income statements by using absorption and marginal costing......................6

M2. Management accounting techniques for preparation of financial reporting documents......8

D2. Interpretation of income statements......................................................................................9

TASK 3............................................................................................................................................9

P4. Advantages and disadvantages of planning tools..................................................................9

M3. Various kind of planning tools and their application for preparing and forecasting of

budget.........................................................................................................................................10

TASK 4..........................................................................................................................................10

P5. Comparison of organisations to solve the financial issues with the help of accounting

systems.......................................................................................................................................10

M4. Management accounting to solve the financial issues........................................................13

D3. Planning tools to resolve financial problems so to lead the organisation towards

sustainable success.....................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

1

INTRODUCTION

Management accounting is a field of accounting that is related to identifying, analysing,

measuring, interpreting and arranging business information and data in a appropriate manner so

that management of the business can make decision in future (Baird. Jia Hu and Reeve, 2011). It

is defined as a process in which analysing the business cost and operation to prepare the financial

reports, records, statement in order to assist to management in decision making process. To

achieve the firm's goal, It is require to assess the financial reports, business operation, cost

structure and other relevant issue that may help in future in betterment of the organisation. The

tools of MA is really helpful in the formation of the business strategies and achievement of the

financial objectives. To better understanding of the management accounting and its system,

Oshodi plc business is chosen in order to set up this report. Oshodi plc is fruit juice

manufacturing firm that produce various kind of fruit juices but specialist in JOJO fruit juice.

This report is consider the various factors of management accounting such as management

accounting systems, reports, budgeting tools and techniques, financial issues, planning

techniques to sustain in the future.

MAIN BODY

TASK 1

P1. Management accounting systems and its requirements:

Management accounting system (MAS) control the business operation by measuring the

business activities regarding cost structure and price for the product. It is a financial process that

refer to detail research of the financial and non monetary activities that may affect to company's

performance. Management accounting is a fundamental process that measure the business

efficiency by operating the fundamental tools and techniques of the firm. It evaluates the

business performance and apply the strategies planning to control the operational activities of the

enterprises. Oshodi plc is using this accounting tools in the firm to better control on the

business operations (Baird, Schoch and Chen, 2012).

Management accounting system: It is system that is defined as appropriate uses of

business detail and information to achieve the business goal by following the rule and processor

of the company. This system help in devising the plan, providing expertise in the reporting

system and assist the management in formulation of financial activities related to business. It is a

2

Management accounting is a field of accounting that is related to identifying, analysing,

measuring, interpreting and arranging business information and data in a appropriate manner so

that management of the business can make decision in future (Baird. Jia Hu and Reeve, 2011). It

is defined as a process in which analysing the business cost and operation to prepare the financial

reports, records, statement in order to assist to management in decision making process. To

achieve the firm's goal, It is require to assess the financial reports, business operation, cost

structure and other relevant issue that may help in future in betterment of the organisation. The

tools of MA is really helpful in the formation of the business strategies and achievement of the

financial objectives. To better understanding of the management accounting and its system,

Oshodi plc business is chosen in order to set up this report. Oshodi plc is fruit juice

manufacturing firm that produce various kind of fruit juices but specialist in JOJO fruit juice.

This report is consider the various factors of management accounting such as management

accounting systems, reports, budgeting tools and techniques, financial issues, planning

techniques to sustain in the future.

MAIN BODY

TASK 1

P1. Management accounting systems and its requirements:

Management accounting system (MAS) control the business operation by measuring the

business activities regarding cost structure and price for the product. It is a financial process that

refer to detail research of the financial and non monetary activities that may affect to company's

performance. Management accounting is a fundamental process that measure the business

efficiency by operating the fundamental tools and techniques of the firm. It evaluates the

business performance and apply the strategies planning to control the operational activities of the

enterprises. Oshodi plc is using this accounting tools in the firm to better control on the

business operations (Baird, Schoch and Chen, 2012).

Management accounting system: It is system that is defined as appropriate uses of

business detail and information to achieve the business goal by following the rule and processor

of the company. This system help in devising the plan, providing expertise in the reporting

system and assist the management in formulation of financial activities related to business. It is a

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

basic business practice that support to business management in adverse situation of the business.

There are antithetic kind of management accounting systems which works to handle the overall

managerial processes and provide a framework to management that help in futuristic issues.

Some of the management accounting systems are defined as follows:

Inventory management system (IMS) - As per this method of IMS, It ascertain the

availability of the material at the right time of requirement. It assure the inflow and

outflow of the stock from the warehouses and stores. It is accumulated system of stock

that provides the information related to stock quantity and its availability at the stores or

warehouses. This system further ensure the availability of goods at right time of

manufacture and supplies. This method is generally uses by the business unit that are

involved in the manufacturing, stores, bulk selling. They uses this system to access the

tags, scan and bar code to handle the stock level of inflow and outflow (Basu, 2012).

Oshodi plc uses this method to control the cost of material of JOJO fruit juice to better

flow of the inward goods so they can provide the better services to it customers.

Cost accounting system (CAS) – This method of MAS is connected with keeps a detail

records of cost subject to fabrication the goods and products. It is detailed structure of

cost that is used by the firm to ascertaining the total cost occur during production of the

goods. This system is generally used by the business to controlling the cost activities and

evaluation the profitability of the business. The framework of cost accounting system are

used by Oshodi plc to determine the correct price of the JOJO fruit juice products. This

cost model verify the cost of particular product and services with cost of sales. With the

help of this system of rules, institution can apportion the accurate cost of input such as

direct material, labour and overhead at various level of manufacture. So they can find out

the profitability of product of their offerings.

Job costing system (JCS) - It is a system that put together the cost data that is related to

with peculiar goods and product. This system of MA is related with allocation of the total

production outlay to total unit of manufactured. As per this system, production

expenditure is generally calculated on the completed projects or tasks. Job costing system

helps in reckoning the total output costs in a arranged manner by dividing cost in sub part

of direct material, labour and other expenses to approximation its actual cost. Oshodi plc

3

There are antithetic kind of management accounting systems which works to handle the overall

managerial processes and provide a framework to management that help in futuristic issues.

Some of the management accounting systems are defined as follows:

Inventory management system (IMS) - As per this method of IMS, It ascertain the

availability of the material at the right time of requirement. It assure the inflow and

outflow of the stock from the warehouses and stores. It is accumulated system of stock

that provides the information related to stock quantity and its availability at the stores or

warehouses. This system further ensure the availability of goods at right time of

manufacture and supplies. This method is generally uses by the business unit that are

involved in the manufacturing, stores, bulk selling. They uses this system to access the

tags, scan and bar code to handle the stock level of inflow and outflow (Basu, 2012).

Oshodi plc uses this method to control the cost of material of JOJO fruit juice to better

flow of the inward goods so they can provide the better services to it customers.

Cost accounting system (CAS) – This method of MAS is connected with keeps a detail

records of cost subject to fabrication the goods and products. It is detailed structure of

cost that is used by the firm to ascertaining the total cost occur during production of the

goods. This system is generally used by the business to controlling the cost activities and

evaluation the profitability of the business. The framework of cost accounting system are

used by Oshodi plc to determine the correct price of the JOJO fruit juice products. This

cost model verify the cost of particular product and services with cost of sales. With the

help of this system of rules, institution can apportion the accurate cost of input such as

direct material, labour and overhead at various level of manufacture. So they can find out

the profitability of product of their offerings.

Job costing system (JCS) - It is a system that put together the cost data that is related to

with peculiar goods and product. This system of MA is related with allocation of the total

production outlay to total unit of manufactured. As per this system, production

expenditure is generally calculated on the completed projects or tasks. Job costing system

helps in reckoning the total output costs in a arranged manner by dividing cost in sub part

of direct material, labour and other expenses to approximation its actual cost. Oshodi plc

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

uses this method to handle the cost related to JOJO fruit juice and it also enables to track

the business disbursement at different locations of production.

Price optimisation system (POS) - This is the functional concepts of the management

accounting system which divine the customer response or feedback on the different level

of pricing structure of relevant goods and services through certain channels. It support in

setting the prices of the product and goods by assessing the customer or market based

response. It is the most important system for the marketing department as with the help of

this system, they can sell the product with effective or market price rate. Oshodi plc is

using this techniques to find out the exact cost of material to sell its at special price.

Company is selling the JOJO fruit juice at effective price so more customer can attract

towards it.

P2. Methods in management accounting reporting.

Management accounting reporting: In any organisations, managers prepares reports that

are confidential addition to serves internal uses only are characterised to management accounting

reports. Accounting reports provides detailed information that is required to trim costs, cutting

inappropriate product lines, rewarding employees whose performance are above the set level and

making investments in certain aspects which delivers best financial returns. Management

associations of Oshodi Plc generates accounting reports on distinct basis such as daily, weekly,

monthly, quarterly and even yearly. Following are accounting reports that are generated by

Osholdi Plc managers:

Account receivable report (ARR): In order to manage cash flow it is very decisive to

create account receivable report as it will help in preparing separate columns having detailed

information about amount, quantity, date and name of creditor. The report helps Oshodi Plc to

list out unused credit memos along with customer invoices that are not paid. It helps managers to

finding issues related with collection processes.

Budget report: To determine expenditure levels, budget reports plays critical; function at

any workplace. Budget reports involves estimated values together with actual results associated

with profit or losses (Bierstaker, Janvrin and Lowe, 2014). At Oshodi Plc, management uses

such report to differentiate estimates, budgeted projections addition to actual performances

attained during financial period.

4

the business disbursement at different locations of production.

Price optimisation system (POS) - This is the functional concepts of the management

accounting system which divine the customer response or feedback on the different level

of pricing structure of relevant goods and services through certain channels. It support in

setting the prices of the product and goods by assessing the customer or market based

response. It is the most important system for the marketing department as with the help of

this system, they can sell the product with effective or market price rate. Oshodi plc is

using this techniques to find out the exact cost of material to sell its at special price.

Company is selling the JOJO fruit juice at effective price so more customer can attract

towards it.

P2. Methods in management accounting reporting.

Management accounting reporting: In any organisations, managers prepares reports that

are confidential addition to serves internal uses only are characterised to management accounting

reports. Accounting reports provides detailed information that is required to trim costs, cutting

inappropriate product lines, rewarding employees whose performance are above the set level and

making investments in certain aspects which delivers best financial returns. Management

associations of Oshodi Plc generates accounting reports on distinct basis such as daily, weekly,

monthly, quarterly and even yearly. Following are accounting reports that are generated by

Osholdi Plc managers:

Account receivable report (ARR): In order to manage cash flow it is very decisive to

create account receivable report as it will help in preparing separate columns having detailed

information about amount, quantity, date and name of creditor. The report helps Oshodi Plc to

list out unused credit memos along with customer invoices that are not paid. It helps managers to

finding issues related with collection processes.

Budget report: To determine expenditure levels, budget reports plays critical; function at

any workplace. Budget reports involves estimated values together with actual results associated

with profit or losses (Bierstaker, Janvrin and Lowe, 2014). At Oshodi Plc, management uses

such report to differentiate estimates, budgeted projections addition to actual performances

attained during financial period.

4

Performance report (PR): To analyse and record individual performances during course

of time performance reports are prepared to control costs as well as evaluating departmental

performances. This reports evaluates the performance of the overall business unit and employees.

These are created with the aim to review business performances at end of financial period.

Administrations of Oshodi Plc uses such kind of accounting report in order to frame key strategic

decisions associated with future of company. It offers detailed statements that are required to

measure outcomes of particular operation in context to success over particular time frame.

Cost managerial report: To calculate costs of different products which are

manufactured at workplace, cost managerial reports are produce that helps in summarising

information about associated costs on certain operations. It comprises overhead costs, inventory

wastage together with labour costs (Bloomfield, 2015). The report provides accurate information

to production managers of Oshodi Plc about expenses so to manage costs for optimising

resources between all departments. Using the report, businesses carefully check information

related to costs addition to this they can also evaluate operations that are consuming more costs

which help them to become aware about all activities while producing JOJO fruit juice.

M1. Benefits of management accounting systems and their application in organisational context.

Management accounting systems comprises distinct systems that benefits the company in

several aspects. In relevance to Oshodi Plc, benefits of all accounting systems are as follows:

Systems Benefits

Inventory management system The system benefits in appropriately tracking movement of

materials along with goods from manufacturing procedures

to supply chain management so to reduce wastages of

inventory addition to improving certain areas.

Price optimisation system Price optimising system helps Oshodi Plc to reduce errors,

providing consistency in operations as well as optimising

data insights so that appropriate prices are determined to

particular product after considering customers perceptions.

Cost accounting system The system benefits Oshodi Plc managers by helping them

5

of time performance reports are prepared to control costs as well as evaluating departmental

performances. This reports evaluates the performance of the overall business unit and employees.

These are created with the aim to review business performances at end of financial period.

Administrations of Oshodi Plc uses such kind of accounting report in order to frame key strategic

decisions associated with future of company. It offers detailed statements that are required to

measure outcomes of particular operation in context to success over particular time frame.

Cost managerial report: To calculate costs of different products which are

manufactured at workplace, cost managerial reports are produce that helps in summarising

information about associated costs on certain operations. It comprises overhead costs, inventory

wastage together with labour costs (Bloomfield, 2015). The report provides accurate information

to production managers of Oshodi Plc about expenses so to manage costs for optimising

resources between all departments. Using the report, businesses carefully check information

related to costs addition to this they can also evaluate operations that are consuming more costs

which help them to become aware about all activities while producing JOJO fruit juice.

M1. Benefits of management accounting systems and their application in organisational context.

Management accounting systems comprises distinct systems that benefits the company in

several aspects. In relevance to Oshodi Plc, benefits of all accounting systems are as follows:

Systems Benefits

Inventory management system The system benefits in appropriately tracking movement of

materials along with goods from manufacturing procedures

to supply chain management so to reduce wastages of

inventory addition to improving certain areas.

Price optimisation system Price optimising system helps Oshodi Plc to reduce errors,

providing consistency in operations as well as optimising

data insights so that appropriate prices are determined to

particular product after considering customers perceptions.

Cost accounting system The system benefits Oshodi Plc managers by helping them

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to control, reducing and setting prices. It also helps in

proper planning, eliminating wastages as well as analysing

reasons for losses so that effective decisions are

implemented to increase profit margins (Boučková, 2015).

Job costing system The system helps in allocating costs to particular jobs or

projects so to determine efficiency through making

effective estimations of product costs.

D1. Management accounting system and reporting integrated with organisational process.

Organisations performs distinct operations by using accounting systems with reporting

mechanisms to meet targets. Accounting systems like job costing, price optimisation, inventory

management and cost management system enhance internal functionality by providing paths

involving procedures to increasing profitability and efficiency of Oshodi plc. Accounting reports

also provides procedures to evaluate performances so that rewards and training programs are

provided to employees so that improvements are made in organisational performances (Chiu,

Teoh and Tian, 2012). Hence, systems and reports of accounting are closely linked with

procedures of organisation to achieve greater revenues.

TASK 2.

P3. Preparation of income statements by using absorption and marginal costing.

Cost is a monetary term which is identified as disbursement of business items such as

material expenses, direct labour, overhead and other expenditures.

Absorption costing- It is a costing method that determines the value from total cost of

manufactured output for every unit. It reckon the overall cost such as direct material, labour and

other expenses cost. This method used both the cost in accounting variable cost and fix cost

considered as cost of unit.

Marginal costing- It shows the extra cost to alteration in the total manufactured item due to

produce one additional unit of a production. Marginal cost take over only variable cost as a

production cost. In this costing technique, fixed cost is taken as periodical cost and variable cost

is taken as unit or product cost (Collis and Hussey, 2017).

6

proper planning, eliminating wastages as well as analysing

reasons for losses so that effective decisions are

implemented to increase profit margins (Boučková, 2015).

Job costing system The system helps in allocating costs to particular jobs or

projects so to determine efficiency through making

effective estimations of product costs.

D1. Management accounting system and reporting integrated with organisational process.

Organisations performs distinct operations by using accounting systems with reporting

mechanisms to meet targets. Accounting systems like job costing, price optimisation, inventory

management and cost management system enhance internal functionality by providing paths

involving procedures to increasing profitability and efficiency of Oshodi plc. Accounting reports

also provides procedures to evaluate performances so that rewards and training programs are

provided to employees so that improvements are made in organisational performances (Chiu,

Teoh and Tian, 2012). Hence, systems and reports of accounting are closely linked with

procedures of organisation to achieve greater revenues.

TASK 2.

P3. Preparation of income statements by using absorption and marginal costing.

Cost is a monetary term which is identified as disbursement of business items such as

material expenses, direct labour, overhead and other expenditures.

Absorption costing- It is a costing method that determines the value from total cost of

manufactured output for every unit. It reckon the overall cost such as direct material, labour and

other expenses cost. This method used both the cost in accounting variable cost and fix cost

considered as cost of unit.

Marginal costing- It shows the extra cost to alteration in the total manufactured item due to

produce one additional unit of a production. Marginal cost take over only variable cost as a

production cost. In this costing technique, fixed cost is taken as periodical cost and variable cost

is taken as unit or product cost (Collis and Hussey, 2017).

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

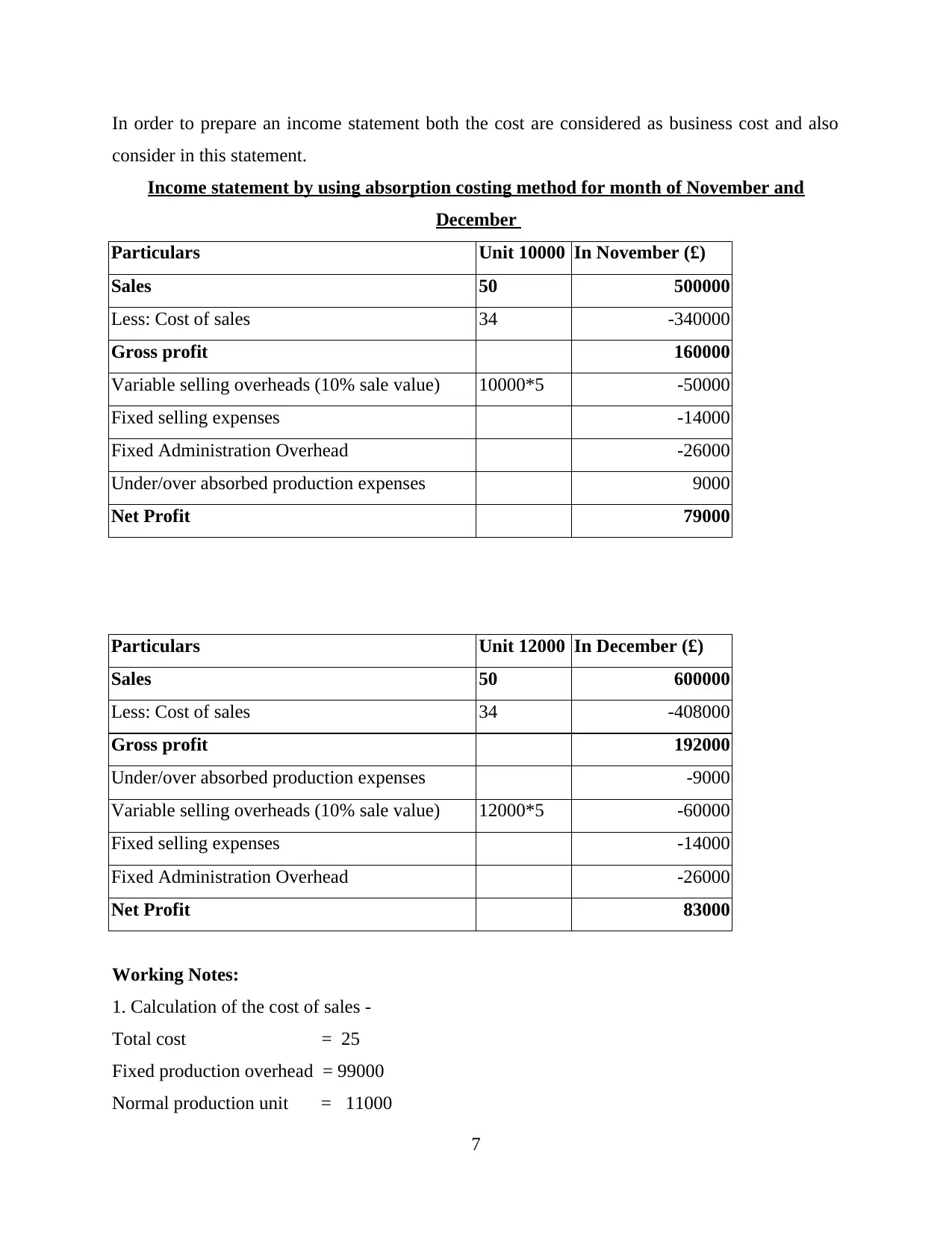

In order to prepare an income statement both the cost are considered as business cost and also

consider in this statement.

Income statement by using absorption costing method for month of November and

December

Particulars Unit 10000 In November (£)

Sales 50 500000

Less: Cost of sales 34 -340000

Gross profit 160000

Variable selling overheads (10% sale value) 10000*5 -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Under/over absorbed production expenses 9000

Net Profit 79000

Particulars Unit 12000 In December (£)

Sales 50 600000

Less: Cost of sales 34 -408000

Gross profit 192000

Under/over absorbed production expenses -9000

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Net Profit 83000

Working Notes:

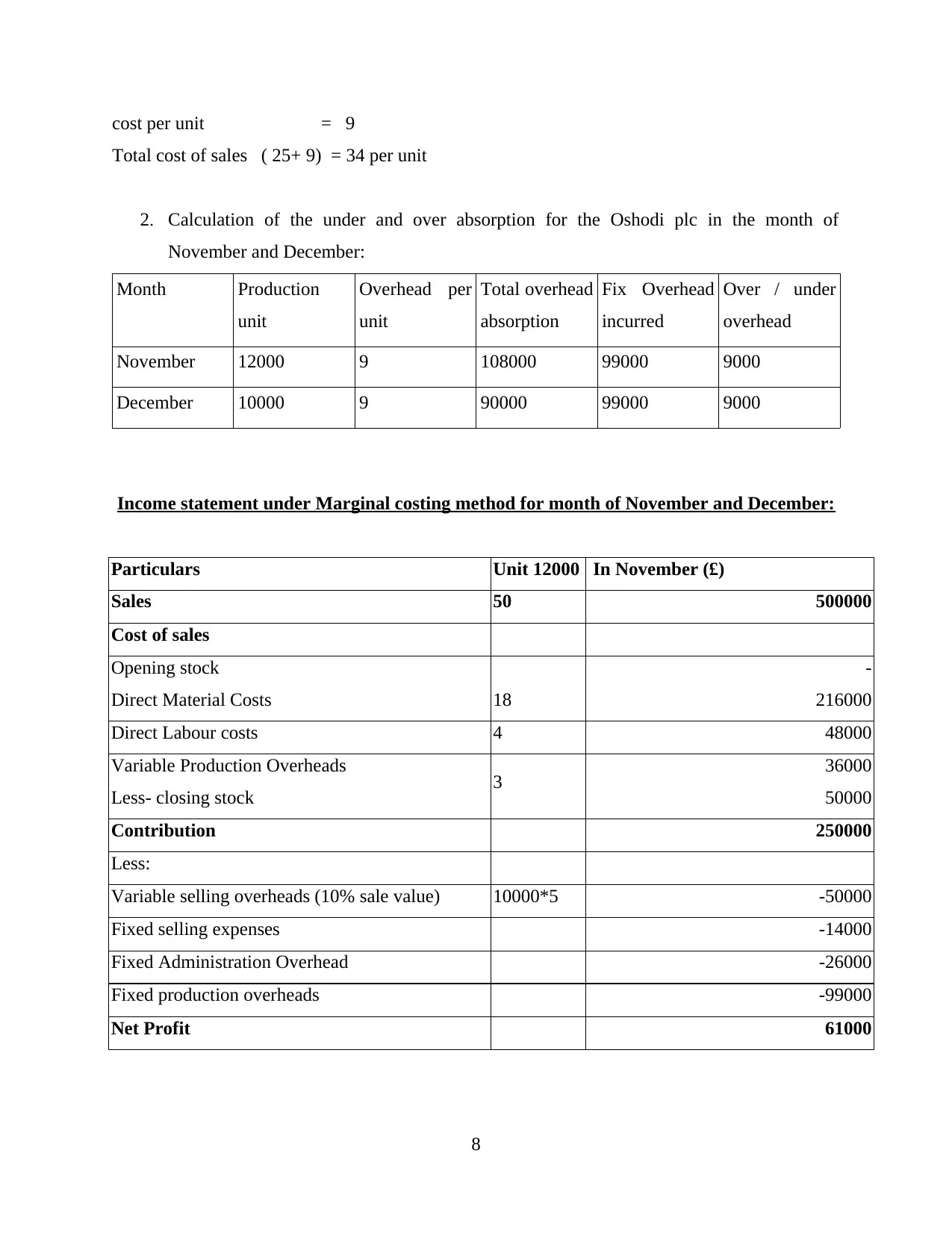

1. Calculation of the cost of sales -

Total cost = 25

Fixed production overhead = 99000

Normal production unit = 11000

7

consider in this statement.

Income statement by using absorption costing method for month of November and

December

Particulars Unit 10000 In November (£)

Sales 50 500000

Less: Cost of sales 34 -340000

Gross profit 160000

Variable selling overheads (10% sale value) 10000*5 -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Under/over absorbed production expenses 9000

Net Profit 79000

Particulars Unit 12000 In December (£)

Sales 50 600000

Less: Cost of sales 34 -408000

Gross profit 192000

Under/over absorbed production expenses -9000

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Net Profit 83000

Working Notes:

1. Calculation of the cost of sales -

Total cost = 25

Fixed production overhead = 99000

Normal production unit = 11000

7

cost per unit = 9

Total cost of sales ( 25+ 9) = 34 per unit

2. Calculation of the under and over absorption for the Oshodi plc in the month of

November and December:

Month Production

unit

Overhead per

unit

Total overhead

absorption

Fix Overhead

incurred

Over / under

overhead

November 12000 9 108000 99000 9000

December 10000 9 90000 99000 9000

Income statement under Marginal costing method for month of November and December:

Particulars Unit 12000 In November (£)

Sales 50 500000

Cost of sales

Opening stock

Direct Material Costs 18

-

216000

Direct Labour costs 4 48000

Variable Production Overheads

Less- closing stock 3 36000

50000

Contribution 250000

Less:

Variable selling overheads (10% sale value) 10000*5 -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Fixed production overheads -99000

Net Profit 61000

8

Total cost of sales ( 25+ 9) = 34 per unit

2. Calculation of the under and over absorption for the Oshodi plc in the month of

November and December:

Month Production

unit

Overhead per

unit

Total overhead

absorption

Fix Overhead

incurred

Over / under

overhead

November 12000 9 108000 99000 9000

December 10000 9 90000 99000 9000

Income statement under Marginal costing method for month of November and December:

Particulars Unit 12000 In November (£)

Sales 50 500000

Cost of sales

Opening stock

Direct Material Costs 18

-

216000

Direct Labour costs 4 48000

Variable Production Overheads

Less- closing stock 3 36000

50000

Contribution 250000

Less:

Variable selling overheads (10% sale value) 10000*5 -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Fixed production overheads -99000

Net Profit 61000

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

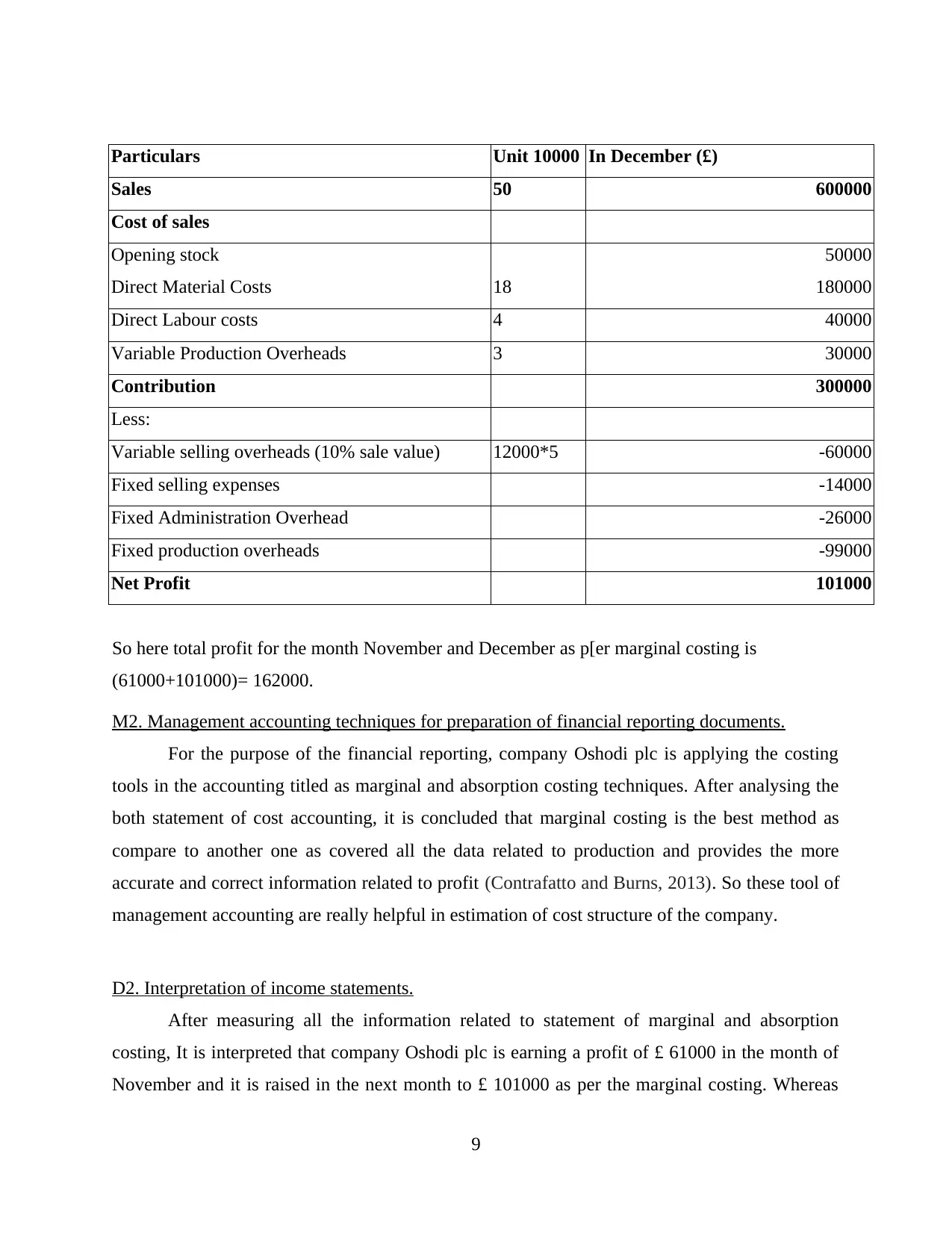

Particulars Unit 10000 In December (£)

Sales 50 600000

Cost of sales

Opening stock

Direct Material Costs 18

50000

180000

Direct Labour costs 4 40000

Variable Production Overheads 3 30000

Contribution 300000

Less:

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Fixed production overheads -99000

Net Profit 101000

So here total profit for the month November and December as p[er marginal costing is

(61000+101000)= 162000.

M2. Management accounting techniques for preparation of financial reporting documents.

For the purpose of the financial reporting, company Oshodi plc is applying the costing

tools in the accounting titled as marginal and absorption costing techniques. After analysing the

both statement of cost accounting, it is concluded that marginal costing is the best method as

compare to another one as covered all the data related to production and provides the more

accurate and correct information related to profit (Contrafatto and Burns, 2013). So these tool of

management accounting are really helpful in estimation of cost structure of the company.

D2. Interpretation of income statements.

After measuring all the information related to statement of marginal and absorption

costing, It is interpreted that company Oshodi plc is earning a profit of £ 61000 in the month of

November and it is raised in the next month to £ 101000 as per the marginal costing. Whereas

9

Sales 50 600000

Cost of sales

Opening stock

Direct Material Costs 18

50000

180000

Direct Labour costs 4 40000

Variable Production Overheads 3 30000

Contribution 300000

Less:

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Fixed production overheads -99000

Net Profit 101000

So here total profit for the month November and December as p[er marginal costing is

(61000+101000)= 162000.

M2. Management accounting techniques for preparation of financial reporting documents.

For the purpose of the financial reporting, company Oshodi plc is applying the costing

tools in the accounting titled as marginal and absorption costing techniques. After analysing the

both statement of cost accounting, it is concluded that marginal costing is the best method as

compare to another one as covered all the data related to production and provides the more

accurate and correct information related to profit (Contrafatto and Burns, 2013). So these tool of

management accounting are really helpful in estimation of cost structure of the company.

D2. Interpretation of income statements.

After measuring all the information related to statement of marginal and absorption

costing, It is interpreted that company Oshodi plc is earning a profit of £ 61000 in the month of

November and it is raised in the next month to £ 101000 as per the marginal costing. Whereas

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profit as per absorption costing is £ 79000 in the month of November. It is uplift by 4000 and

become £ 83000. so the profit under the marginal costing is higher as it eliminate the extra or

irrelevant cost in he calculation of total profit.

TASK 3

P4. Advantages and disadvantages of planning tools.

Budget are the projections which are prepared to predict future position of the company.

With the help of budgets, managers of Oshodi Plc creates spending plan and ensures that the

have enough money to facilitate daily operations without facing any sort of hurdle. By carefully

following spending plan, it helps the company to keep out of any debt as well as overcoming

debt situations in effective manner.

Budgetary control: It is accompanying with definite procedures that helps in

establishing business goals by using budgets (Fullerton, Kennedy and Widener, 2014). It

measures the actual performance by considering the standard data and information and make

favourable comparison to identifying the deviation. These are used to ensure adequate limits of

spendings at workplace. Importance of budgetary control at Oshodi plc is to evaluate the impact

of excessive spendings on corporate profits. For this, following planning tools are opted by

finance team of Oshodi Plc:

Cash budget: It is prepared to plan the flows of cash during accounting period. It

includes the cash inflow and outflow for the particular period of time. It includes payments and

receipts in context to revenue collected, loans paid and expenses disbursed. It is used at Oshodi

plc in order to ascertain cash position during particular time period so to arrange cash for

estimates shortages or controlling excess usage of cash.

Advantages: Cash budget helps Oshodi Plc to prioritizing payments as well as analysing

variances in movement of cash in budget period.

Disadvantages: Cash budget only provides estimates which can be wrong or fails to

deliver appropriate factual knowledge that can results in more outflow of cash for the company.

Operating budget: It includes estimates related with totality of resources that are

required to effectively perform operations. It is used by accountants of Oshodi Plc to estimate

workloads, tracking incomes and controlling expenses so to achieve ambitious targets.

10

become £ 83000. so the profit under the marginal costing is higher as it eliminate the extra or

irrelevant cost in he calculation of total profit.

TASK 3

P4. Advantages and disadvantages of planning tools.

Budget are the projections which are prepared to predict future position of the company.

With the help of budgets, managers of Oshodi Plc creates spending plan and ensures that the

have enough money to facilitate daily operations without facing any sort of hurdle. By carefully

following spending plan, it helps the company to keep out of any debt as well as overcoming

debt situations in effective manner.

Budgetary control: It is accompanying with definite procedures that helps in

establishing business goals by using budgets (Fullerton, Kennedy and Widener, 2014). It

measures the actual performance by considering the standard data and information and make

favourable comparison to identifying the deviation. These are used to ensure adequate limits of

spendings at workplace. Importance of budgetary control at Oshodi plc is to evaluate the impact

of excessive spendings on corporate profits. For this, following planning tools are opted by

finance team of Oshodi Plc:

Cash budget: It is prepared to plan the flows of cash during accounting period. It

includes the cash inflow and outflow for the particular period of time. It includes payments and

receipts in context to revenue collected, loans paid and expenses disbursed. It is used at Oshodi

plc in order to ascertain cash position during particular time period so to arrange cash for

estimates shortages or controlling excess usage of cash.

Advantages: Cash budget helps Oshodi Plc to prioritizing payments as well as analysing

variances in movement of cash in budget period.

Disadvantages: Cash budget only provides estimates which can be wrong or fails to

deliver appropriate factual knowledge that can results in more outflow of cash for the company.

Operating budget: It includes estimates related with totality of resources that are

required to effectively perform operations. It is used by accountants of Oshodi Plc to estimate

workloads, tracking incomes and controlling expenses so to achieve ambitious targets.

10

Advantages: It benefits selected business in managing current expenses, increasing

accountability, building financial reserves and projecting expenses so to overcome from weak

operations (Håkansson, Kraus and Lind, 2010).

Disadvantage: one of the limitation of such budget is that it requires long range planning

that requires more time and efforts of managers which results in additional costing and decreased

profit margins.

Master budget: It provides detailed summary of other budgets such as sales budget,

capital budget, general expenses budget and many more. Master budget is concluded the all the

budgeting a summarised form for all the department. It delivers information related with

different departments of Oshodi Plc in one go.

Advantages: It assists management of company in financial planning as well as allocating

funds among departments so that confident communication is shared with stakeholders.

Disadvantages: Master budget fails to provide exact information concerned with

subsidiary budgets that results in lack of specificity to management of Oshodi Plc.

M3. Various kind of planning tools and their application for preparing and forecasting of budget.

Certain planning tools are used to prepare as well as forecasting budget in effective

manner. Master budget, cash budget as well as operating budget are some of the kinds of

planning tools that are For example, master budget is applied by Oshodi Plc in order to extract

detailed summary of other budgets where as cash budget is applied to generate estimates about

cash flows during particular budgeting period (Jacobs, 2012).

TASK 4.

P5. Comparison of organisations to solve the financial issues with the help of accounting

systems.

In the modern era of business, most of business enterprises are facing difficulties

regarding the financial issue or lack of funds. It is arises due to mismanagement in the business

operations of the company. It totally depends on the management of the business that how they

handle these issue and earn more profit in the future. It is mandatory to resolve the business issue

to better flow of the functional activities in the business. Some of the financial issue are

described as under:

11

accountability, building financial reserves and projecting expenses so to overcome from weak

operations (Håkansson, Kraus and Lind, 2010).

Disadvantage: one of the limitation of such budget is that it requires long range planning

that requires more time and efforts of managers which results in additional costing and decreased

profit margins.

Master budget: It provides detailed summary of other budgets such as sales budget,

capital budget, general expenses budget and many more. Master budget is concluded the all the

budgeting a summarised form for all the department. It delivers information related with

different departments of Oshodi Plc in one go.

Advantages: It assists management of company in financial planning as well as allocating

funds among departments so that confident communication is shared with stakeholders.

Disadvantages: Master budget fails to provide exact information concerned with

subsidiary budgets that results in lack of specificity to management of Oshodi Plc.

M3. Various kind of planning tools and their application for preparing and forecasting of budget.

Certain planning tools are used to prepare as well as forecasting budget in effective

manner. Master budget, cash budget as well as operating budget are some of the kinds of

planning tools that are For example, master budget is applied by Oshodi Plc in order to extract

detailed summary of other budgets where as cash budget is applied to generate estimates about

cash flows during particular budgeting period (Jacobs, 2012).

TASK 4.

P5. Comparison of organisations to solve the financial issues with the help of accounting

systems.

In the modern era of business, most of business enterprises are facing difficulties

regarding the financial issue or lack of funds. It is arises due to mismanagement in the business

operations of the company. It totally depends on the management of the business that how they

handle these issue and earn more profit in the future. It is mandatory to resolve the business issue

to better flow of the functional activities in the business. Some of the financial issue are

described as under:

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.