Management Accounting Report: OVATION SYSTEMS Financial Strategies

VerifiedAdded on 2020/10/22

|18

|5303

|72

Report

AI Summary

This report delves into the core concepts of management accounting, providing a comprehensive overview of its principles and applications within the context of OVATION SYSTEMS. It begins by defining management accounting, outlining its essential requirements, and differentiating it from financial accounting. The report then explores various management accounting systems, including cost accounting, inventory management, job costing, and price optimization, assessing their benefits and integration within an organization. Task 2 focuses on costing methods, comparing and contrasting absorption and marginal costing, and applying break-even analysis. The report also covers financial reporting, the application of management accounting techniques, and the accurate interpretation of financial data. Finally, Task 3 examines planning tools, evaluating their advantages and disadvantages in preparing, forecasting, and analyzing budgets. The report concludes by analyzing how management accounting techniques can address financial problems, promoting sustainable success, and identifying the role of planning tools in achieving organizational goals.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

Task 1...............................................................................................................................................4

A. Explain the management accounting and give the essential requirements of the different

types of management accounting system ...................................................................................4

B. Providing the different types of management accounting report used by the OVATION

SYSTEMS...................................................................................................................................5

C. Assessing the benefits of the different types of management accounting systems ...............6

D. How management accounting system and management accounting reporting is integrated

in an organization. ......................................................................................................................8

Task 2...............................................................................................................................................9

A. Explain the absorption costing and marginal costing methods .............................................9

B.1 Solve the following problem with marginal and absorption costing methods.....................9

B.2 . With the use of break even analysis solve the following question...................................10

C . Apply the range of management accounting techniques and produce appropriate financial

reporting documents accurately................................................................................................11

D. Produce financial reports that accurately apply and interpret the data for the business

activities shown in the scenarios in Task 2 above.....................................................................12

Task 3.............................................................................................................................................12

A. Explain the advantage and disadvantages for different types of planning tools..................12

B. Show the application of the planning tools for preparing, forecasting and analysing

budgets. ....................................................................................................................................14

C. Compare how the organization is different in adopting management accounting system

with responds with the financial problems...............................................................................14

D. Analyse how your management accounting techniques could respond to financial problems

and lead the organization to sustainable success.......................................................................16

E. Evaluate how planning tools could be used to solve financial problems and lead the

organization to sustainable success...........................................................................................16

Planning tools helps in identifying the social and environment trends which can provides

companies' ability to create value over time. ...........................................................................16

INTRODUCTION...........................................................................................................................4

Task 1...............................................................................................................................................4

A. Explain the management accounting and give the essential requirements of the different

types of management accounting system ...................................................................................4

B. Providing the different types of management accounting report used by the OVATION

SYSTEMS...................................................................................................................................5

C. Assessing the benefits of the different types of management accounting systems ...............6

D. How management accounting system and management accounting reporting is integrated

in an organization. ......................................................................................................................8

Task 2...............................................................................................................................................9

A. Explain the absorption costing and marginal costing methods .............................................9

B.1 Solve the following problem with marginal and absorption costing methods.....................9

B.2 . With the use of break even analysis solve the following question...................................10

C . Apply the range of management accounting techniques and produce appropriate financial

reporting documents accurately................................................................................................11

D. Produce financial reports that accurately apply and interpret the data for the business

activities shown in the scenarios in Task 2 above.....................................................................12

Task 3.............................................................................................................................................12

A. Explain the advantage and disadvantages for different types of planning tools..................12

B. Show the application of the planning tools for preparing, forecasting and analysing

budgets. ....................................................................................................................................14

C. Compare how the organization is different in adopting management accounting system

with responds with the financial problems...............................................................................14

D. Analyse how your management accounting techniques could respond to financial problems

and lead the organization to sustainable success.......................................................................16

E. Evaluate how planning tools could be used to solve financial problems and lead the

organization to sustainable success...........................................................................................16

Planning tools helps in identifying the social and environment trends which can provides

companies' ability to create value over time. ...........................................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

REFERENCES..............................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

To solve the financial and managerial issues in the organization there are lots of tools and

techniques management accounting have. Management accounting plays an important role in the

to achieve the organizational goals. The present report will provide the meaning of management

accounting and the essential requirements of the management accounting system and their

implement in business accounting. The report will also depict the uses of marginal and

absorption costing and importance of break-even analysis in an organization to find out the

financial health of the organization apart from that this assignment will provide benefit and uses

of different planning tools with their benefits and drawbacks.

Task 1

A. Explain the management accounting and give the essential requirements of the different types

of management accounting system

Management accounting is process of identifying, interpreting, analyzing and

communicating all the financial information in the shadow of the OVATIONS SYSTEMS goals.

In between financial and management accounting there lies only one basic difference I.e the

information provided by management accounting aims at assisting the managers in decision

making, while in the financial accounting targets at providing information to the outsiders which

are related with organization (Ax and Greve, 2017). Managers of the organization requires the

financial information and accurate statistical data day by day to interpret day to day short run

decision. Management needs report which is contained by the management accounting.

Accounting is the process of finding, measuring, and communication profitable data to

permit the decision and judgments by the users accordingly American accounting association.

Management accounting system help in varying their application (Cooper, Ezzamel and Qu,

2017). Inside the organization various departments are there and each are fashioned to provide

the information which the management needs for assessing the decision. Management

accounting is consisted of the various system which are discussed under -

Cost accounting system

To do the valuation of inventory, profitability analysis and cost control for the

approximate cost of product OVATION SYSTEM applied the framework named costing system

or cost accounting system. In this system of accounting the allocation of cost is done by the

managers with the help of activity based costing or traditional costing system. Approaching the

To solve the financial and managerial issues in the organization there are lots of tools and

techniques management accounting have. Management accounting plays an important role in the

to achieve the organizational goals. The present report will provide the meaning of management

accounting and the essential requirements of the management accounting system and their

implement in business accounting. The report will also depict the uses of marginal and

absorption costing and importance of break-even analysis in an organization to find out the

financial health of the organization apart from that this assignment will provide benefit and uses

of different planning tools with their benefits and drawbacks.

Task 1

A. Explain the management accounting and give the essential requirements of the different types

of management accounting system

Management accounting is process of identifying, interpreting, analyzing and

communicating all the financial information in the shadow of the OVATIONS SYSTEMS goals.

In between financial and management accounting there lies only one basic difference I.e the

information provided by management accounting aims at assisting the managers in decision

making, while in the financial accounting targets at providing information to the outsiders which

are related with organization (Ax and Greve, 2017). Managers of the organization requires the

financial information and accurate statistical data day by day to interpret day to day short run

decision. Management needs report which is contained by the management accounting.

Accounting is the process of finding, measuring, and communication profitable data to

permit the decision and judgments by the users accordingly American accounting association.

Management accounting system help in varying their application (Cooper, Ezzamel and Qu,

2017). Inside the organization various departments are there and each are fashioned to provide

the information which the management needs for assessing the decision. Management

accounting is consisted of the various system which are discussed under -

Cost accounting system

To do the valuation of inventory, profitability analysis and cost control for the

approximate cost of product OVATION SYSTEM applied the framework named costing system

or cost accounting system. In this system of accounting the allocation of cost is done by the

managers with the help of activity based costing or traditional costing system. Approaching the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

actual product, cost is an important function of management accounting (Eldenburg and et.al.,

2016). Cost accounting is the system which focus on the reducing the cost of production with

the help of weighing the inputs' production cost plus fixed cost. It is a key concept of the

management accounting as it provides with the analytical tool like variance analysis, budgeting

tool, marginal costing etc to take the decision.

Inventory management

It is the method to inspecting, controlling, oversee the ordering, storage and the uses of

the ingredients which OVATION SYSTEM apply in the production of goods it sells. This

system of inventory management uses the various application like bar code scanners, desktop

software, etc in consumable, stocks and goods (Fullerton, Kennedy and Widener, 2014). It

includes all the information regarding the inventory from the raw material to the selling. It helps

in improving the bottom line of the company, enhances the inventory accuracy and the work

flow of an organization.

Job costing system

Job costing system is the system of allocation of the cost of manufacturing to the

independent batches or items of the product. When goods processed are different from one

another the job costing system is applied (Kihn, and Ihantola, 2015). Information obtained from

this is important for determining the correctness of estimating system of company to quote the

price. The three kinds of information job costing requires that are labor, direct material and lab

our.

Price optimizing system

Price optimization is the technique give to the organization to determine how the

consumer will react at different pricing of product and services through different channels. It

also helps in deciding the cost which the OVATION SYSTEM determines will be best to fulfill

its goals and objectives (Management Accounting: Meaning, Functions and Characteristics,

2017).

B. Providing the different types of management accounting report used by the OVATION

SYSTEMS

The internal information received by the financial accounting is focused by the

managerial accounting. It is applied for the planning, analysis, controlling and decision making

in the organization (Malmi, 2016). It is depended upon the financial statements such as, balance

2016). Cost accounting is the system which focus on the reducing the cost of production with

the help of weighing the inputs' production cost plus fixed cost. It is a key concept of the

management accounting as it provides with the analytical tool like variance analysis, budgeting

tool, marginal costing etc to take the decision.

Inventory management

It is the method to inspecting, controlling, oversee the ordering, storage and the uses of

the ingredients which OVATION SYSTEM apply in the production of goods it sells. This

system of inventory management uses the various application like bar code scanners, desktop

software, etc in consumable, stocks and goods (Fullerton, Kennedy and Widener, 2014). It

includes all the information regarding the inventory from the raw material to the selling. It helps

in improving the bottom line of the company, enhances the inventory accuracy and the work

flow of an organization.

Job costing system

Job costing system is the system of allocation of the cost of manufacturing to the

independent batches or items of the product. When goods processed are different from one

another the job costing system is applied (Kihn, and Ihantola, 2015). Information obtained from

this is important for determining the correctness of estimating system of company to quote the

price. The three kinds of information job costing requires that are labor, direct material and lab

our.

Price optimizing system

Price optimization is the technique give to the organization to determine how the

consumer will react at different pricing of product and services through different channels. It

also helps in deciding the cost which the OVATION SYSTEM determines will be best to fulfill

its goals and objectives (Management Accounting: Meaning, Functions and Characteristics,

2017).

B. Providing the different types of management accounting report used by the OVATION

SYSTEMS

The internal information received by the financial accounting is focused by the

managerial accounting. It is applied for the planning, analysis, controlling and decision making

in the organization (Malmi, 2016). It is depended upon the financial statements such as, balance

sheet, income statements etc. The organization needs various reports like budget, cost report,

performance report etc.

Cost reports

Management accounting helps in calculating the cost of the products and services. By

taking into consideration all raw product expenses, labour, cost plus any other cost. After taking

all the expenses and cost the sums are then divided into amounts of good manufactured. This all

data is presented in the cost report. This report helps the managers to identify the capability of

cost to its cost value of the products and services with the selling price. It assesses the managers

to control the loop hole of cost and develop the plan for profit margin.

Budgets

Budget estimates all the expenses of the organization. Budget is the very important

element of management accounting. Budget is the systematic procedure which is consisted of all

the past expenses upcoming expenses so that the goals and objectives can be received. For an

OVATION SYSTEM it is necessary while attempt to attaining its goals whereas staying In

budgeted amount. If the amount exceed the variance in actual and standard cost takes place.

Performance report

The accountant managers takes the help of budget to compare the actual outcomes of

revenues and expenses to budgeted amount (Nitzl, 2018). The variances occur and evaluated

when the new budgets is prepared including all the essential information is listed on the

performance report. Performance report is actually the evaluation of the performance presented

in the systematic format. Mostly these reports are made every year, but some organization make

them monthly or quarterly. Performance reports assist mangers in future planning of demands for

the production and cost enhancement

C. Assessing the benefits of the different types of management accounting systems

Following are the benefits of the different types of management accounting system.

Management

accounting systems

Benefits

Cost accounting

system

It validates the concern to measure its efficiency, to continue and

to improve it.

It ascertains both the activity I.e profitable and non profitable.

performance report etc.

Cost reports

Management accounting helps in calculating the cost of the products and services. By

taking into consideration all raw product expenses, labour, cost plus any other cost. After taking

all the expenses and cost the sums are then divided into amounts of good manufactured. This all

data is presented in the cost report. This report helps the managers to identify the capability of

cost to its cost value of the products and services with the selling price. It assesses the managers

to control the loop hole of cost and develop the plan for profit margin.

Budgets

Budget estimates all the expenses of the organization. Budget is the very important

element of management accounting. Budget is the systematic procedure which is consisted of all

the past expenses upcoming expenses so that the goals and objectives can be received. For an

OVATION SYSTEM it is necessary while attempt to attaining its goals whereas staying In

budgeted amount. If the amount exceed the variance in actual and standard cost takes place.

Performance report

The accountant managers takes the help of budget to compare the actual outcomes of

revenues and expenses to budgeted amount (Nitzl, 2018). The variances occur and evaluated

when the new budgets is prepared including all the essential information is listed on the

performance report. Performance report is actually the evaluation of the performance presented

in the systematic format. Mostly these reports are made every year, but some organization make

them monthly or quarterly. Performance reports assist mangers in future planning of demands for

the production and cost enhancement

C. Assessing the benefits of the different types of management accounting systems

Following are the benefits of the different types of management accounting system.

Management

accounting systems

Benefits

Cost accounting

system

It validates the concern to measure its efficiency, to continue and

to improve it.

It ascertains both the activity I.e profitable and non profitable.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It helps the managers to guide in the reduction of prices.

Cost accounting helps in the information of proper planning.

It provides the ability to the managers to take the decision.

Inventory

management system

It helps in balancing the overall inventory management of an

organization in systematic way.

Inventory balance I.e if the organization have good inventory

management it will help the OVATION SYSTEM to find out

how many inventories firm requires for the production.

Inventory management system helps in accurate planning of the

demand curve, keeps right amount of the products.

It increases the employee efficiencies. It consists of various tools

like inventory management software, bar code scanners to utilize

all the resources and time.

It helps in the retention of the customer in an organization.

Job costing system It provides the extent for control of the costs by applying suitable

steps. The cost may be discover at any stage of the job

It jobs costing method profit earned from each job is entitled

separately.

On the basis of past records in job costing the cost can be

estimated by the management

The comparison of actual cost of previous job with present job

executed.

Through compilation of historical cost in job costing trend

analysis can be explained.

Prize optimization

system

The prize optimizing system provides the opportunities to

concentrates on various goals. It helps in reap of financial

benefits the financial benefits.

It helps the management to work parallel with all the categories

It helps to take the decision quickly

Cost accounting helps in the information of proper planning.

It provides the ability to the managers to take the decision.

Inventory

management system

It helps in balancing the overall inventory management of an

organization in systematic way.

Inventory balance I.e if the organization have good inventory

management it will help the OVATION SYSTEM to find out

how many inventories firm requires for the production.

Inventory management system helps in accurate planning of the

demand curve, keeps right amount of the products.

It increases the employee efficiencies. It consists of various tools

like inventory management software, bar code scanners to utilize

all the resources and time.

It helps in the retention of the customer in an organization.

Job costing system It provides the extent for control of the costs by applying suitable

steps. The cost may be discover at any stage of the job

It jobs costing method profit earned from each job is entitled

separately.

On the basis of past records in job costing the cost can be

estimated by the management

The comparison of actual cost of previous job with present job

executed.

Through compilation of historical cost in job costing trend

analysis can be explained.

Prize optimization

system

The prize optimizing system provides the opportunities to

concentrates on various goals. It helps in reap of financial

benefits the financial benefits.

It helps the management to work parallel with all the categories

It helps to take the decision quickly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It monitors results and upgrade the input data to maintain the

accuracy

Managerial accounting helps the OVATION SYSTEM to do effective planning and

working with the help of various types of management accounting system. These system plays

an important role in the organization to assessing the good decision making so that firm can

accomplish its goals and objectives.

D. How management accounting system and management accounting reporting is integrated in

an organization.

The management accounting systems and the reporting are in organization for the

supporting of the competitive advantages by the processing communicating and collecting the

information which are required by the management for the efficient planning, controlling and

evaluating the processes of the business and company strategies (Otley, 2016). The top

accountant of the organization is the controller of these two techniques which helps the

management to reach the goals and objectives. Following are some important facts which helps

organization in the integration of management techniques-

Helping forecasts the future

The word forecasting delivers the meaning that is related to the future. Before starting the

venture many questions arises in the mind of the owner like should company invest more

equipment, should the company should diversify in different market or not. The answer of all

question are provided with the help of management techniques and reporting system.

Helping in make or buy decision

To control the cost and exceed the profit of the organization it is very important to do

right decision-making regarding whether to buy or to do the production to reduce the cost.

Through these techniques, insights will be developed which will be enable decision-making

making at strategic and operational levels.

Helps to understand the performance variances

In every organization there is a set standard for each and every activity. The

discrepancies in the business performance is the variance between what is set and what is

actually achieved. This reporting and system techniques helps to identify the cause behind the

variances and appropriate solution.

accuracy

Managerial accounting helps the OVATION SYSTEM to do effective planning and

working with the help of various types of management accounting system. These system plays

an important role in the organization to assessing the good decision making so that firm can

accomplish its goals and objectives.

D. How management accounting system and management accounting reporting is integrated in

an organization.

The management accounting systems and the reporting are in organization for the

supporting of the competitive advantages by the processing communicating and collecting the

information which are required by the management for the efficient planning, controlling and

evaluating the processes of the business and company strategies (Otley, 2016). The top

accountant of the organization is the controller of these two techniques which helps the

management to reach the goals and objectives. Following are some important facts which helps

organization in the integration of management techniques-

Helping forecasts the future

The word forecasting delivers the meaning that is related to the future. Before starting the

venture many questions arises in the mind of the owner like should company invest more

equipment, should the company should diversify in different market or not. The answer of all

question are provided with the help of management techniques and reporting system.

Helping in make or buy decision

To control the cost and exceed the profit of the organization it is very important to do

right decision-making regarding whether to buy or to do the production to reduce the cost.

Through these techniques, insights will be developed which will be enable decision-making

making at strategic and operational levels.

Helps to understand the performance variances

In every organization there is a set standard for each and every activity. The

discrepancies in the business performance is the variance between what is set and what is

actually achieved. This reporting and system techniques helps to identify the cause behind the

variances and appropriate solution.

Task 2

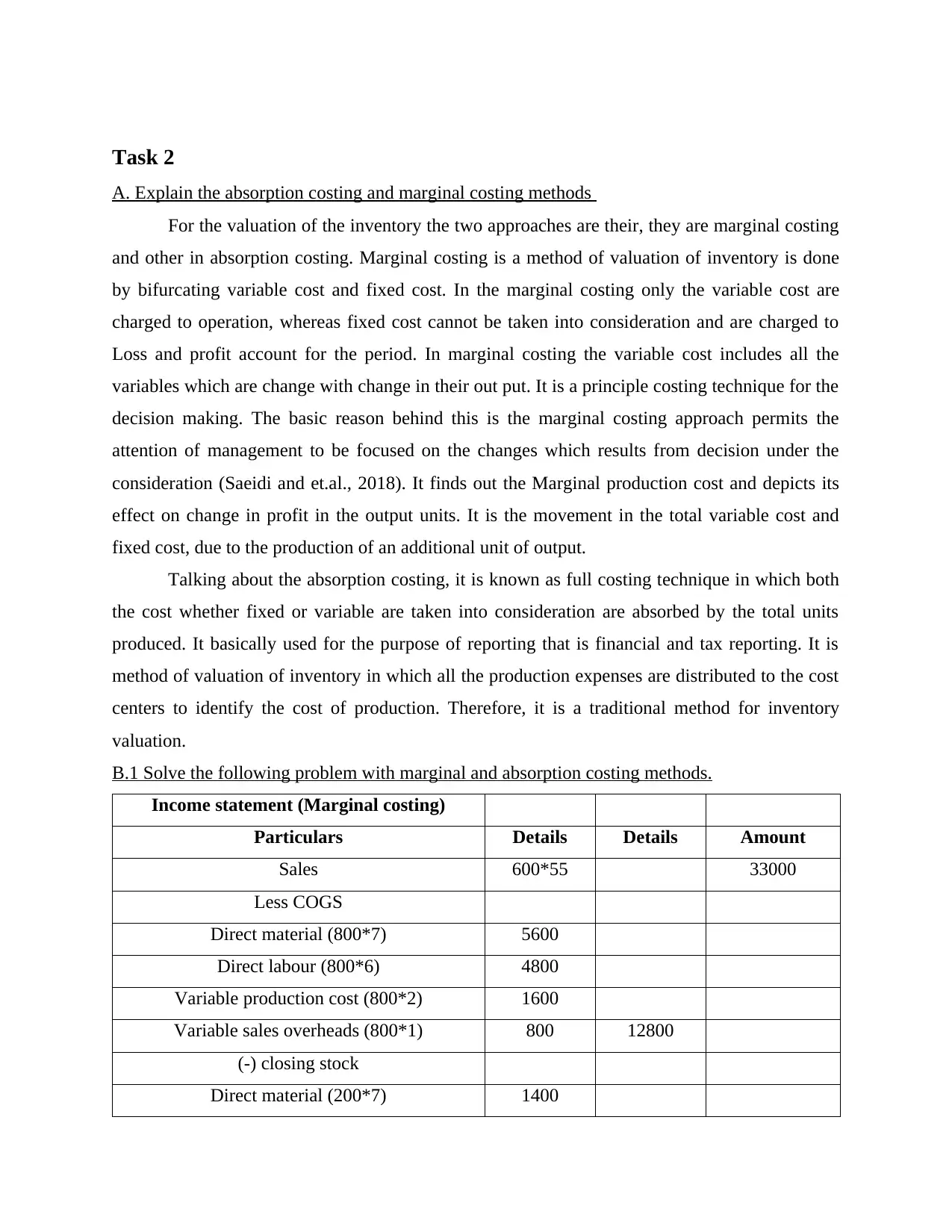

A. Explain the absorption costing and marginal costing methods

For the valuation of the inventory the two approaches are their, they are marginal costing

and other in absorption costing. Marginal costing is a method of valuation of inventory is done

by bifurcating variable cost and fixed cost. In the marginal costing only the variable cost are

charged to operation, whereas fixed cost cannot be taken into consideration and are charged to

Loss and profit account for the period. In marginal costing the variable cost includes all the

variables which are change with change in their out put. It is a principle costing technique for the

decision making. The basic reason behind this is the marginal costing approach permits the

attention of management to be focused on the changes which results from decision under the

consideration (Saeidi and et.al., 2018). It finds out the Marginal production cost and depicts its

effect on change in profit in the output units. It is the movement in the total variable cost and

fixed cost, due to the production of an additional unit of output.

Talking about the absorption costing, it is known as full costing technique in which both

the cost whether fixed or variable are taken into consideration are absorbed by the total units

produced. It basically used for the purpose of reporting that is financial and tax reporting. It is

method of valuation of inventory in which all the production expenses are distributed to the cost

centers to identify the cost of production. Therefore, it is a traditional method for inventory

valuation.

B.1 Solve the following problem with marginal and absorption costing methods.

Income statement (Marginal costing)

Particulars Details Details Amount

Sales 600*55 33000

Less COGS

Direct material (800*7) 5600

Direct labour (800*6) 4800

Variable production cost (800*2) 1600

Variable sales overheads (800*1) 800 12800

(-) closing stock

Direct material (200*7) 1400

A. Explain the absorption costing and marginal costing methods

For the valuation of the inventory the two approaches are their, they are marginal costing

and other in absorption costing. Marginal costing is a method of valuation of inventory is done

by bifurcating variable cost and fixed cost. In the marginal costing only the variable cost are

charged to operation, whereas fixed cost cannot be taken into consideration and are charged to

Loss and profit account for the period. In marginal costing the variable cost includes all the

variables which are change with change in their out put. It is a principle costing technique for the

decision making. The basic reason behind this is the marginal costing approach permits the

attention of management to be focused on the changes which results from decision under the

consideration (Saeidi and et.al., 2018). It finds out the Marginal production cost and depicts its

effect on change in profit in the output units. It is the movement in the total variable cost and

fixed cost, due to the production of an additional unit of output.

Talking about the absorption costing, it is known as full costing technique in which both

the cost whether fixed or variable are taken into consideration are absorbed by the total units

produced. It basically used for the purpose of reporting that is financial and tax reporting. It is

method of valuation of inventory in which all the production expenses are distributed to the cost

centers to identify the cost of production. Therefore, it is a traditional method for inventory

valuation.

B.1 Solve the following problem with marginal and absorption costing methods.

Income statement (Marginal costing)

Particulars Details Details Amount

Sales 600*55 33000

Less COGS

Direct material (800*7) 5600

Direct labour (800*6) 4800

Variable production cost (800*2) 1600

Variable sales overheads (800*1) 800 12800

(-) closing stock

Direct material (200*7) 1400

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

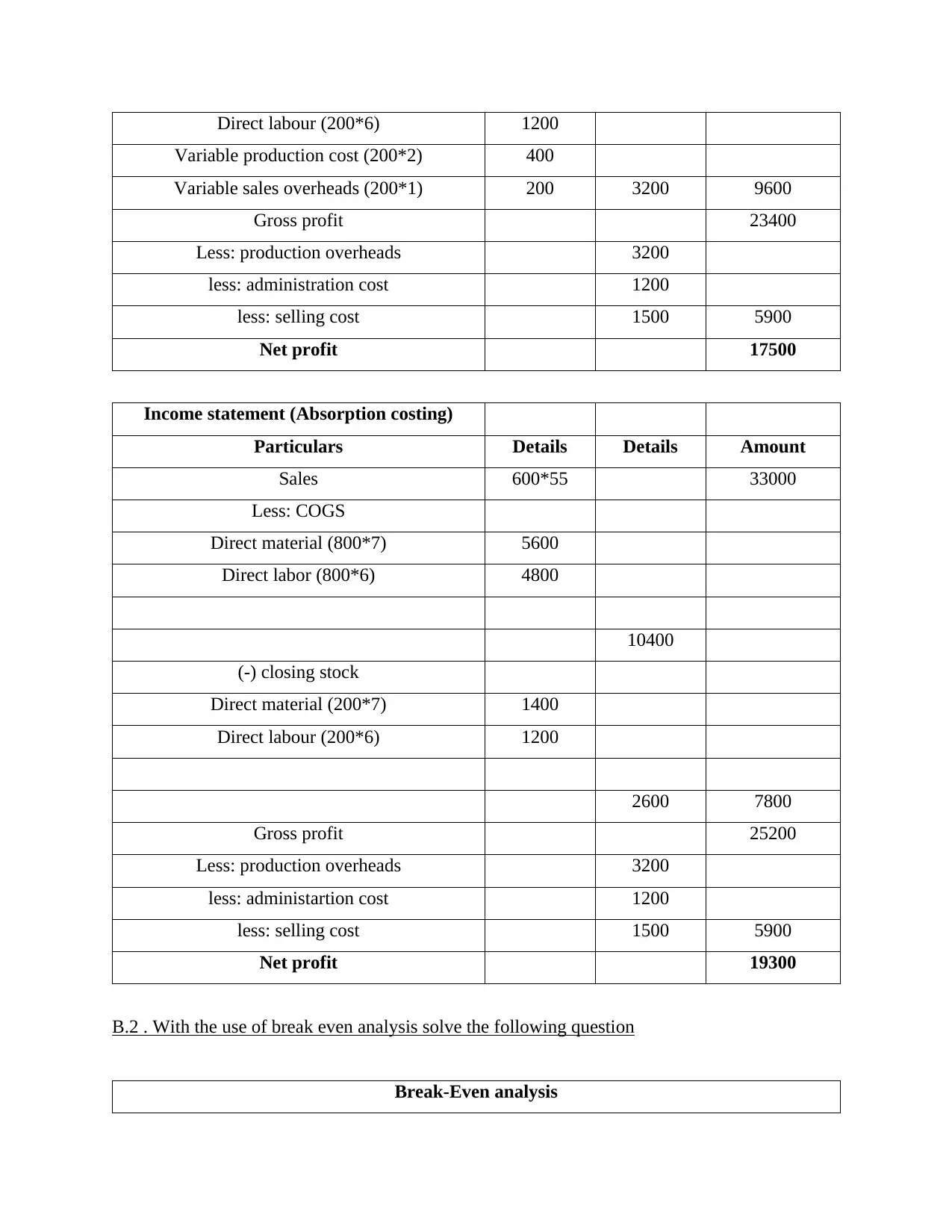

Direct labour (200*6) 1200

Variable production cost (200*2) 400

Variable sales overheads (200*1) 200 3200 9600

Gross profit 23400

Less: production overheads 3200

less: administration cost 1200

less: selling cost 1500 5900

Net profit 17500

Income statement (Absorption costing)

Particulars Details Details Amount

Sales 600*55 33000

Less: COGS

Direct material (800*7) 5600

Direct labor (800*6) 4800

10400

(-) closing stock

Direct material (200*7) 1400

Direct labour (200*6) 1200

2600 7800

Gross profit 25200

Less: production overheads 3200

less: administartion cost 1200

less: selling cost 1500 5900

Net profit 19300

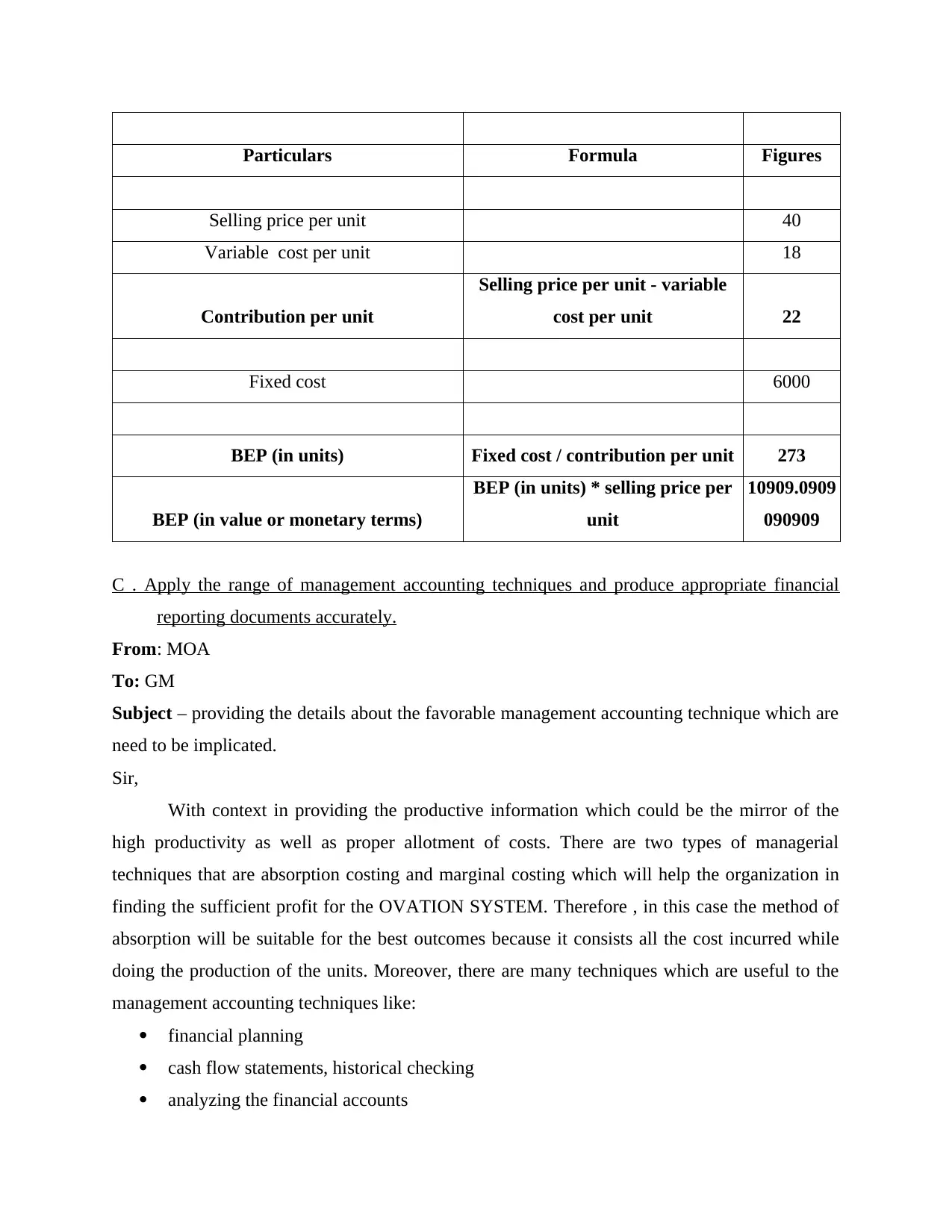

B.2 . With the use of break even analysis solve the following question

Break-Even analysis

Variable production cost (200*2) 400

Variable sales overheads (200*1) 200 3200 9600

Gross profit 23400

Less: production overheads 3200

less: administration cost 1200

less: selling cost 1500 5900

Net profit 17500

Income statement (Absorption costing)

Particulars Details Details Amount

Sales 600*55 33000

Less: COGS

Direct material (800*7) 5600

Direct labor (800*6) 4800

10400

(-) closing stock

Direct material (200*7) 1400

Direct labour (200*6) 1200

2600 7800

Gross profit 25200

Less: production overheads 3200

less: administartion cost 1200

less: selling cost 1500 5900

Net profit 19300

B.2 . With the use of break even analysis solve the following question

Break-Even analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars Formula Figures

Selling price per unit 40

Variable cost per unit 18

Contribution per unit

Selling price per unit - variable

cost per unit 22

Fixed cost 6000

BEP (in units) Fixed cost / contribution per unit 273

BEP (in value or monetary terms)

BEP (in units) * selling price per

unit

10909.0909

090909

C . Apply the range of management accounting techniques and produce appropriate financial

reporting documents accurately.

From: MOA

To: GM

Subject – providing the details about the favorable management accounting technique which are

need to be implicated.

Sir,

With context in providing the productive information which could be the mirror of the

high productivity as well as proper allotment of costs. There are two types of managerial

techniques that are absorption costing and marginal costing which will help the organization in

finding the sufficient profit for the OVATION SYSTEM. Therefore , in this case the method of

absorption will be suitable for the best outcomes because it consists all the cost incurred while

doing the production of the units. Moreover, there are many techniques which are useful to the

management accounting techniques like:

financial planning

cash flow statements, historical checking

analyzing the financial accounts

Selling price per unit 40

Variable cost per unit 18

Contribution per unit

Selling price per unit - variable

cost per unit 22

Fixed cost 6000

BEP (in units) Fixed cost / contribution per unit 273

BEP (in value or monetary terms)

BEP (in units) * selling price per

unit

10909.0909

090909

C . Apply the range of management accounting techniques and produce appropriate financial

reporting documents accurately.

From: MOA

To: GM

Subject – providing the details about the favorable management accounting technique which are

need to be implicated.

Sir,

With context in providing the productive information which could be the mirror of the

high productivity as well as proper allotment of costs. There are two types of managerial

techniques that are absorption costing and marginal costing which will help the organization in

finding the sufficient profit for the OVATION SYSTEM. Therefore , in this case the method of

absorption will be suitable for the best outcomes because it consists all the cost incurred while

doing the production of the units. Moreover, there are many techniques which are useful to the

management accounting techniques like:

financial planning

cash flow statements, historical checking

analyzing the financial accounts

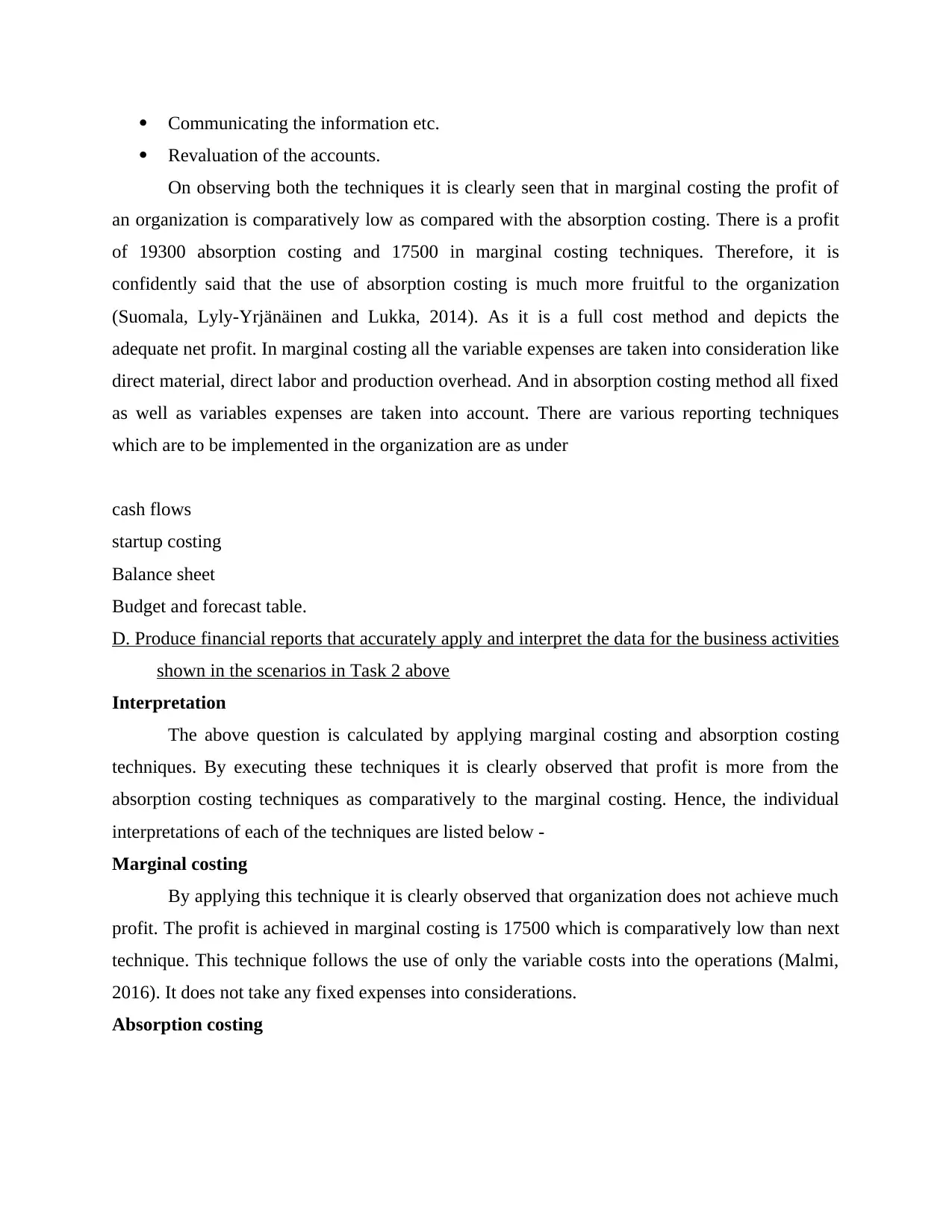

Communicating the information etc.

Revaluation of the accounts.

On observing both the techniques it is clearly seen that in marginal costing the profit of

an organization is comparatively low as compared with the absorption costing. There is a profit

of 19300 absorption costing and 17500 in marginal costing techniques. Therefore, it is

confidently said that the use of absorption costing is much more fruitful to the organization

(Suomala, Lyly-Yrjänäinen and Lukka, 2014). As it is a full cost method and depicts the

adequate net profit. In marginal costing all the variable expenses are taken into consideration like

direct material, direct labor and production overhead. And in absorption costing method all fixed

as well as variables expenses are taken into account. There are various reporting techniques

which are to be implemented in the organization are as under

cash flows

startup costing

Balance sheet

Budget and forecast table.

D. Produce financial reports that accurately apply and interpret the data for the business activities

shown in the scenarios in Task 2 above

Interpretation

The above question is calculated by applying marginal costing and absorption costing

techniques. By executing these techniques it is clearly observed that profit is more from the

absorption costing techniques as comparatively to the marginal costing. Hence, the individual

interpretations of each of the techniques are listed below -

Marginal costing

By applying this technique it is clearly observed that organization does not achieve much

profit. The profit is achieved in marginal costing is 17500 which is comparatively low than next

technique. This technique follows the use of only the variable costs into the operations (Malmi,

2016). It does not take any fixed expenses into considerations.

Absorption costing

Revaluation of the accounts.

On observing both the techniques it is clearly seen that in marginal costing the profit of

an organization is comparatively low as compared with the absorption costing. There is a profit

of 19300 absorption costing and 17500 in marginal costing techniques. Therefore, it is

confidently said that the use of absorption costing is much more fruitful to the organization

(Suomala, Lyly-Yrjänäinen and Lukka, 2014). As it is a full cost method and depicts the

adequate net profit. In marginal costing all the variable expenses are taken into consideration like

direct material, direct labor and production overhead. And in absorption costing method all fixed

as well as variables expenses are taken into account. There are various reporting techniques

which are to be implemented in the organization are as under

cash flows

startup costing

Balance sheet

Budget and forecast table.

D. Produce financial reports that accurately apply and interpret the data for the business activities

shown in the scenarios in Task 2 above

Interpretation

The above question is calculated by applying marginal costing and absorption costing

techniques. By executing these techniques it is clearly observed that profit is more from the

absorption costing techniques as comparatively to the marginal costing. Hence, the individual

interpretations of each of the techniques are listed below -

Marginal costing

By applying this technique it is clearly observed that organization does not achieve much

profit. The profit is achieved in marginal costing is 17500 which is comparatively low than next

technique. This technique follows the use of only the variable costs into the operations (Malmi,

2016). It does not take any fixed expenses into considerations.

Absorption costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.