An Overview and Assessment of MA Research in China (1997-2005)

VerifiedAdded on 2022/08/27

|37

|23322

|19

Report

AI Summary

This report provides an in-depth overview and assessment of management accounting research in China, analyzing 283 articles published in 18 major Chinese academic journals between 1997 and 2005. The study highlights significant shifts in topic mixes across different periods and identifies normative/conceptual papers as the dominant research method, followed by case studies, surveys, and other methodologies. It notes a lack of explicit theory application in a substantial portion of the articles and considerable overlap between topical coverage and managerial concerns. The research further examines the journals' selection criteria and factors influencing Chinese scholars' research capabilities, incentives, and focus. The report concludes by identifying shortcomings that limit the reliability and generalizability of the findings, and suggests possible avenues for future development in the field, providing valuable insights for both Chinese and international scholars interested in collaboration and advancing management accounting research in China. The research also provides a critical evaluation of the empirical studies using criteria such as construct validity, internal validity, external validity, and reliability.

129

JOURNAL OF MANAGEMENT ACCOUNTING RESEARCH

Volume Twenty, Special Issue

2008

pp. 129–164

An Overview and Assessment of

Contemporary Management

Accounting Research in China

Rong-Ruey Duh

National Taiwan University

Jason Zezhong Xiao

Cardiff University

Chee W. Chow

San Diego State University

ABSTRACT: This paper provides an overview of 283 management accounting articles

published in 18 major Chinese academic journals from 1997 to 2005. We find signifi-

cantly different topic mixes between the periods 1997 to 2001 and 2002 to 2005.In

terms of research method, normative / conceptual papers dominate in both subperiods,

followed in descending order by case studies, surveys, field-archivalstudies, and an-

alyticalmodeling research. About 80 percent of the papers do not have any explicit or

detectable application of theory. Finally, considerable overlap exists between the arti-

cles’ topicalcoverage and issues considered important by managers. Overall, due to

lack of theory application and other methodologicallimitations, this literature has not

yet built a strong basis for understanding and leading management accounting devel-

opment in China. Thus, we further examine the journals’ selection standards and pro-

cesses, as wellas factors that may have influenced Chinese scholars’ research ability,

incentives, and focus. We conclude by offering suggestions for future development.

Keywords: management accounting research; China.

INTRODUCTION

Since China embraced privatization and market reform in 1978, Chinese firms have

gained global importance as suppliers, competitors, customers, partners, and targets

of foreign investment (OECD 2005; Roberts and Engardis 2006). This development,

in turn, has spurred interest in understanding Chinese firms’ management practices. Over

the years, a number of studies have appeared in the international (English) literature de-

scribing or analyzing Chinese firms’ management accounting (MA) practices (e.g., Skousen

and Yang 1988; Bromwich and Wang 1991; Scapens and Meng 1993; Firth 1996; Chalos and

O’Connor 2004; O’Connor et al. 2004, 2006; Chow et al. 2007). While these studies have

contributed useful findings, they have only looked at limited aspects of the phenomenon.

The authors are indebted to two anonymous reviewers and the editor for many helpful suggestions for improving

this paper.

JOURNAL OF MANAGEMENT ACCOUNTING RESEARCH

Volume Twenty, Special Issue

2008

pp. 129–164

An Overview and Assessment of

Contemporary Management

Accounting Research in China

Rong-Ruey Duh

National Taiwan University

Jason Zezhong Xiao

Cardiff University

Chee W. Chow

San Diego State University

ABSTRACT: This paper provides an overview of 283 management accounting articles

published in 18 major Chinese academic journals from 1997 to 2005. We find signifi-

cantly different topic mixes between the periods 1997 to 2001 and 2002 to 2005.In

terms of research method, normative / conceptual papers dominate in both subperiods,

followed in descending order by case studies, surveys, field-archivalstudies, and an-

alyticalmodeling research. About 80 percent of the papers do not have any explicit or

detectable application of theory. Finally, considerable overlap exists between the arti-

cles’ topicalcoverage and issues considered important by managers. Overall, due to

lack of theory application and other methodologicallimitations, this literature has not

yet built a strong basis for understanding and leading management accounting devel-

opment in China. Thus, we further examine the journals’ selection standards and pro-

cesses, as wellas factors that may have influenced Chinese scholars’ research ability,

incentives, and focus. We conclude by offering suggestions for future development.

Keywords: management accounting research; China.

INTRODUCTION

Since China embraced privatization and market reform in 1978, Chinese firms have

gained global importance as suppliers, competitors, customers, partners, and targets

of foreign investment (OECD 2005; Roberts and Engardis 2006). This development,

in turn, has spurred interest in understanding Chinese firms’ management practices. Over

the years, a number of studies have appeared in the international (English) literature de-

scribing or analyzing Chinese firms’ management accounting (MA) practices (e.g., Skousen

and Yang 1988; Bromwich and Wang 1991; Scapens and Meng 1993; Firth 1996; Chalos and

O’Connor 2004; O’Connor et al. 2004, 2006; Chow et al. 2007). While these studies have

contributed useful findings, they have only looked at limited aspects of the phenomenon.

The authors are indebted to two anonymous reviewers and the editor for many helpful suggestions for improving

this paper.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

130 Duh, Xiao, and Chow

Journal of Management Accounting Research, Special Issue 2008

Furthermore, they have almost exclusively been survey based and as such, lack the ability

to explore in depth the nature of processes or issues of ‘‘how’’ and ‘‘why’’ (Yin 1994).

Among the reasons underlying the limited scope and size of this (English language)

literature, perhaps one of the most important is the language barrier. While there is a

countrywide push for English learning, the number of Chinese company employees with

a good command of English is still low. A related obstacle is that internal documents of

Chinese business enterprises (except for joint ventures) tend to be in Chinese. Perhaps no

less important, Chinese companies are as yet not accustomed to opening themselves to

outside researchers. Rather, gaining such access requires good interpersonal relationships

built over an extended period (‘‘guanxi’’) (O’Connor et al. 2004).

Taken together, these factors suggest that at least for some time, the primary source of

knowledge about Chinese firms’ MA practices will remain the scholars / writers residing and

working in China. The objective of this article is to give individuals who do not read

Chinese an overview of the MA research published in China. Beyond describing charac-

teristics of this literature like topic coverage, methods, and theories, we identify many

shortcomings that limit the reliability and generalizability of its findings. 1 We further ex-

plore factors that may have affected the supply and screening of Chinese MA research, and

suggest possible directions for future development. Beyond assisting the advancement of

Chinese MA research, this report also can help Chinese and foreign scholars to identify

opportunities for collaboration.

We limited this review to the major Chinese academic journals that publish MA re-

search. We assumed that these outlets would tend to uphold higher quality standards, and

thus their content would be more accurate and reliable. To develop the list of journals for

inclusion, we asked senior accounting faculty of ten major Chinese universities to identify

the core journals that their institutions used for personnel decisions.2 The following 18

journals came from aggregating their responses. While some of these (e.g., Accounting

Research, Auditing Research) have an obvious accounting focus, others (e.g., China Man-

agement Science, Economic Science) cover a range of business-related topics.

(1) Accounting Research

(2) Auditing Research

(3) Banking Research

(4) China Accounting and Finance Review

(5) China Management Science

(6) China Soft Sciences

(7) Economic Research

(8) Economic Science

(9) Economic Theory and Economic Management

(10) Finance and Accounting 3

1 Chow et al. (2007) also review studies of MA in China published in both English and Chinese journals. However,

beyond being much smaller in scale, their review emphasizes summary and description, whereas the present

review stresses critically assessing the literature’s coverage, depth, relevance to practice, and theoretical and

methodological adequacy.

2 Five of these are comprehensive universities that have the largest numbers of key academic disciplines in

economics and management conferred by the Ministry of Education. These are Nankai, Fudan, Wuhan, Tsinghua,

and Peking. The other five are the first ones authorized by the government to offer an accounting Ph.D. program:

Xiamen, Renmin, Northeast University of Finance and Economics, Shanghai University of Finance and Eco-

nomics, and Central South University of Finance and Economics.

3 Finance and Accounting has been treated as a practitioner journal by some major Chinese universities in recent

years, but before 2005 (the last year covered by our survey), it was a major outlet of MA papers written by

Chinese academics. This still is the case and the trend may well continue for some time into the future.

Journal of Management Accounting Research, Special Issue 2008

Furthermore, they have almost exclusively been survey based and as such, lack the ability

to explore in depth the nature of processes or issues of ‘‘how’’ and ‘‘why’’ (Yin 1994).

Among the reasons underlying the limited scope and size of this (English language)

literature, perhaps one of the most important is the language barrier. While there is a

countrywide push for English learning, the number of Chinese company employees with

a good command of English is still low. A related obstacle is that internal documents of

Chinese business enterprises (except for joint ventures) tend to be in Chinese. Perhaps no

less important, Chinese companies are as yet not accustomed to opening themselves to

outside researchers. Rather, gaining such access requires good interpersonal relationships

built over an extended period (‘‘guanxi’’) (O’Connor et al. 2004).

Taken together, these factors suggest that at least for some time, the primary source of

knowledge about Chinese firms’ MA practices will remain the scholars / writers residing and

working in China. The objective of this article is to give individuals who do not read

Chinese an overview of the MA research published in China. Beyond describing charac-

teristics of this literature like topic coverage, methods, and theories, we identify many

shortcomings that limit the reliability and generalizability of its findings. 1 We further ex-

plore factors that may have affected the supply and screening of Chinese MA research, and

suggest possible directions for future development. Beyond assisting the advancement of

Chinese MA research, this report also can help Chinese and foreign scholars to identify

opportunities for collaboration.

We limited this review to the major Chinese academic journals that publish MA re-

search. We assumed that these outlets would tend to uphold higher quality standards, and

thus their content would be more accurate and reliable. To develop the list of journals for

inclusion, we asked senior accounting faculty of ten major Chinese universities to identify

the core journals that their institutions used for personnel decisions.2 The following 18

journals came from aggregating their responses. While some of these (e.g., Accounting

Research, Auditing Research) have an obvious accounting focus, others (e.g., China Man-

agement Science, Economic Science) cover a range of business-related topics.

(1) Accounting Research

(2) Auditing Research

(3) Banking Research

(4) China Accounting and Finance Review

(5) China Management Science

(6) China Soft Sciences

(7) Economic Research

(8) Economic Science

(9) Economic Theory and Economic Management

(10) Finance and Accounting 3

1 Chow et al. (2007) also review studies of MA in China published in both English and Chinese journals. However,

beyond being much smaller in scale, their review emphasizes summary and description, whereas the present

review stresses critically assessing the literature’s coverage, depth, relevance to practice, and theoretical and

methodological adequacy.

2 Five of these are comprehensive universities that have the largest numbers of key academic disciplines in

economics and management conferred by the Ministry of Education. These are Nankai, Fudan, Wuhan, Tsinghua,

and Peking. The other five are the first ones authorized by the government to offer an accounting Ph.D. program:

Xiamen, Renmin, Northeast University of Finance and Economics, Shanghai University of Finance and Eco-

nomics, and Central South University of Finance and Economics.

3 Finance and Accounting has been treated as a practitioner journal by some major Chinese universities in recent

years, but before 2005 (the last year covered by our survey), it was a major outlet of MA papers written by

Chinese academics. This still is the case and the trend may well continue for some time into the future.

An Overview and Assessment of Contemporary Management Accounting Research in China 131

Journal of Management Accounting Research, Special Issue 2008

(11) Finance and Economic Research

(12) Management Science

(13) Management World

(14) Nankai Economic Research

(15) Nankai Business Review

(16) Peking University Journal (social science edition)

(17) Public Finance Research

(18) Tsinghua University Journal (social science edition)

To balance comprehensiveness and currency of coverage, we collected all MA-related

articles published in these journals for the period 1997–2005. The year 1997 was selected

as the starting point because it marked a major change in thinking in China’s central

government, which wields absolute power over how economic activities in the country are

conducted.4 We concluded with 2005 because this was the last year for which complete

volumes for all 18 journals were available at the time of data collection (late 2006). 5 We

also sought to identify trends in various attributes of the published studies (e.g., topics,

method, use of theory), but because there existed considerable year-to-year variations, we

divided the 1997–2005 time span into 1997–2001 and 2002–2005 subperiods to smooth

out transient effects. China became a member of the World Trade Organization in 2001.

This has brought requirements for substantially increased market openness, reduced gov-

ernment interference, and increased management autonomy. Open-end mutual funds also

became available in China in 2001, and have since become important participants in the

Chinese stock market. Meanwhile, government actions to strengthen the role of external

participants in corporate governance, investor protection, and shareholder activism have

accelerated.6 Developments like these are likely to have increased Chinese firms’ incentives

and ability to improve their MA practices, in turn possibly affecting Chinese researchers’

topic choices and access to data.

We followed Luft and Shields (2003, 172) in defining MA as accounting in the man-

agement of organizations. Thus, we excluded measurement and recognition criteria / stan-

dards for financial reporting, auditing, or taxation. We then followed Shields (1997) to

classify the articles by topic, method, theory, and setting. To categorize the articles by

research method, we defined normative / conceptual papers as ones that develop ideas or

4 During the 15th National Congress of the Communist Party of China (CPC) held in that year, the then Secretary-

General of the CPC, Jiang Zeming, ushered in an ideological breakthrough by calling for experimenting with

all forms of ownership that can be used to advance socialist productive forces (Jiang 1997). In particular, Jiang’s

report paved the way for politically and ideologically accepting joint-stock companies as a means of transforming

the thousands of state-owned enterprises and organizing societal resources. An indication of this ideological

change’s importance is the increase of listed companies from 745 in 1997 to 1,377 by the end of 2004. In the

management accounting arena, the Accounting Society of China, which hitherto had focused its activities on

financial accounting and reporting, organized in 1997 for the first time a national contest in management ac-

counting research. The Society again organized a national best papers contest in 1999 and established a Man-

agement Accounting Special Interest Section in that year.

5 Given the direction of developments that we observe, we have to acknowledge the possibility that articles

published after 2005 may exhibit a different pattern from those of the earlier years. However, given the relatively

small number of MA articles published in each year, our overall conclusions are unlikely to be materially

affected.

6 For example, the China Securities Regulatory Commission issued ‘‘Guidelines for Establishing an Independent

Directors System for Listed Companies’’ in August 2001 and the ‘‘Code of Corporate Governance for Listed

Companies in China’’ in January 2002. These regulations imposed explicit requirements for the appointment of

qualified independent directors on corporate boards, prohibited the appointment of controlling shareholders and

associated parties to be directors, and conferred greater powers on the independent directors for monitoring

related parties transactions and for the appointment and dismissal of auditors, directors, and senior executives.

Journal of Management Accounting Research, Special Issue 2008

(11) Finance and Economic Research

(12) Management Science

(13) Management World

(14) Nankai Economic Research

(15) Nankai Business Review

(16) Peking University Journal (social science edition)

(17) Public Finance Research

(18) Tsinghua University Journal (social science edition)

To balance comprehensiveness and currency of coverage, we collected all MA-related

articles published in these journals for the period 1997–2005. The year 1997 was selected

as the starting point because it marked a major change in thinking in China’s central

government, which wields absolute power over how economic activities in the country are

conducted.4 We concluded with 2005 because this was the last year for which complete

volumes for all 18 journals were available at the time of data collection (late 2006). 5 We

also sought to identify trends in various attributes of the published studies (e.g., topics,

method, use of theory), but because there existed considerable year-to-year variations, we

divided the 1997–2005 time span into 1997–2001 and 2002–2005 subperiods to smooth

out transient effects. China became a member of the World Trade Organization in 2001.

This has brought requirements for substantially increased market openness, reduced gov-

ernment interference, and increased management autonomy. Open-end mutual funds also

became available in China in 2001, and have since become important participants in the

Chinese stock market. Meanwhile, government actions to strengthen the role of external

participants in corporate governance, investor protection, and shareholder activism have

accelerated.6 Developments like these are likely to have increased Chinese firms’ incentives

and ability to improve their MA practices, in turn possibly affecting Chinese researchers’

topic choices and access to data.

We followed Luft and Shields (2003, 172) in defining MA as accounting in the man-

agement of organizations. Thus, we excluded measurement and recognition criteria / stan-

dards for financial reporting, auditing, or taxation. We then followed Shields (1997) to

classify the articles by topic, method, theory, and setting. To categorize the articles by

research method, we defined normative / conceptual papers as ones that develop ideas or

4 During the 15th National Congress of the Communist Party of China (CPC) held in that year, the then Secretary-

General of the CPC, Jiang Zeming, ushered in an ideological breakthrough by calling for experimenting with

all forms of ownership that can be used to advance socialist productive forces (Jiang 1997). In particular, Jiang’s

report paved the way for politically and ideologically accepting joint-stock companies as a means of transforming

the thousands of state-owned enterprises and organizing societal resources. An indication of this ideological

change’s importance is the increase of listed companies from 745 in 1997 to 1,377 by the end of 2004. In the

management accounting arena, the Accounting Society of China, which hitherto had focused its activities on

financial accounting and reporting, organized in 1997 for the first time a national contest in management ac-

counting research. The Society again organized a national best papers contest in 1999 and established a Man-

agement Accounting Special Interest Section in that year.

5 Given the direction of developments that we observe, we have to acknowledge the possibility that articles

published after 2005 may exhibit a different pattern from those of the earlier years. However, given the relatively

small number of MA articles published in each year, our overall conclusions are unlikely to be materially

affected.

6 For example, the China Securities Regulatory Commission issued ‘‘Guidelines for Establishing an Independent

Directors System for Listed Companies’’ in August 2001 and the ‘‘Code of Corporate Governance for Listed

Companies in China’’ in January 2002. These regulations imposed explicit requirements for the appointment of

qualified independent directors on corporate boards, prohibited the appointment of controlling shareholders and

associated parties to be directors, and conferred greater powers on the independent directors for monitoring

related parties transactions and for the appointment and dismissal of auditors, directors, and senior executives.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

132 Duh, Xiao, and Chow

Journal of Management Accounting Research, Special Issue 2008

arguments without using data or modeling (Maher 2001). Case studies are research under-

takings that involve the observation in natural settings of policies, practices, people, struc-

ture, and context within a single organization (Birnberg et al. 1990; Yin 1994). A field-

archival study is similar to a case study except that the data of interest are publicly available

through, for example, databases. A survey study typically involves using questionnaires to

collect data from respondents in a sample of organizations (Kerlinger and Lee 2000;

Birnberg et al. 1990). An analytical modeling study is defined as one that involves math-

ematical proof of propositions or searching for solutions through, for example, optimization

techniques.

Beyond showing the distribution of articles across several attributes (e.g., topic cover-

age, setting), we critically evaluated the empirical studies using the criteria of construct

validity, internal validity, external validity, and reliability (Abdel-khalik and Ajinkya 1979;

Birnberg et al. 1990; Van der Stede et al. 2005; Yin 1994). 7 For analytical modeling re-

search, we followed Demski (2007) in examining the research question, preparation of the

model, and ability to satisfy the Ralph test. As Demski explains, a well-prepared model is

one that can answer the question that it poses. Thus, for example, it would be meaningless

to ask a model that assumes certainty what information is needed. As for the Ralph test, a

study is seen as passing this test to the extent that its central question is of classroom

importance and the answer that it provides is useful.

In total we found 283 MA articles, most of which had appeared in two journals:

Accounting Research (116) and Finance and Accounting (124). These 283 articles cover a

broad range of topics, including management control systems, cost accounting and man-

agement, externally oriented MA, decision-making techniques, and information technology

applications. We also found some significant differences in topic coverage between the two

subperiods 1997–2001 and 2002–2005.

7 Construct validity refers to whether a particular operational definition is indeed a valid measure of the construct

in question (Birnberg et al. 1990; Kerlinger and Lee 2000). For case study research, construct validity is con-

cerned with whether the issues or variables involved are specified, and whether the measures for the issues or

variables do indeed reflect the specific issues or variables under investigation. Triangulating with multiple sources

of evidence and creating a formal and presentable database are procedures for increasing construct validity (Yin

1994). For survey research, construct validity is concerned with the extent to which different measures of the

same construct converge and the extent to which measures of distinct constructs diverge (Cook and Campbell

1979; Kerlinger and Lee 2000). For field-archival research, researchers often rely on proxies if the variables of

interest cannot be directly measured; construct validity is expected to increase with the use of commonly

employed and / or widely validated measures. Internal validity is concerned with whether observed changes in

the dependent variables are indeed caused by changes in the independent variable(s) (Cook and Campbell 1979).

Internal validity does not apply to descriptive or exploratory studies (Yin 1994), and thus is assessed only for

the research that involves hypothesis testing and causal inferences. Pattern-matching is frequently used

for assessing internal validity of causal case study research (Yin 1994), and we examine whether such studies

in our sample have compared their observed patterns with ones predicted by theory. For survey research, we

focus on whether the authors have performed pre-testing, follow-up procedures, and nonresponse bias analysis

(Van der Stede et al. 2005). For field-archival research, we focus on whether the articles have used control

variables and whether there are omitted variables. External validity refers to the extent to which the obtained

result(s) can be generalized to other samples or settings (Campbell and Stanley 1966). Yin (1994) distinguishes

between statistical generalization and analytical generalization. The former concerns the ability to generalize the

findings obtained from one sample to other samples while in analytical generalization, researchers attempt to

generalize a set of results to some broader theory (Yin 1994). Yin (1994) suggests that while statistical gener-

alization applies to survey research, it does not apply to case study research. As such, for case study research,

we focus on whether the article under review explains why a case site is selected. For survey research and field-

archival research, we focus on sample description and response rate (in the case of survey research). Reliability

refers to the degree to which findings obtained by a researcher can be replicated by another researcher using

the same procedures. For case study research, we focus on whether the authors have used a case study protocol

or similar procedures. For survey research, we focus on reliability of measures for the variables of interest. For

field-archival research, we focus on the description of samples and databases.

Journal of Management Accounting Research, Special Issue 2008

arguments without using data or modeling (Maher 2001). Case studies are research under-

takings that involve the observation in natural settings of policies, practices, people, struc-

ture, and context within a single organization (Birnberg et al. 1990; Yin 1994). A field-

archival study is similar to a case study except that the data of interest are publicly available

through, for example, databases. A survey study typically involves using questionnaires to

collect data from respondents in a sample of organizations (Kerlinger and Lee 2000;

Birnberg et al. 1990). An analytical modeling study is defined as one that involves math-

ematical proof of propositions or searching for solutions through, for example, optimization

techniques.

Beyond showing the distribution of articles across several attributes (e.g., topic cover-

age, setting), we critically evaluated the empirical studies using the criteria of construct

validity, internal validity, external validity, and reliability (Abdel-khalik and Ajinkya 1979;

Birnberg et al. 1990; Van der Stede et al. 2005; Yin 1994). 7 For analytical modeling re-

search, we followed Demski (2007) in examining the research question, preparation of the

model, and ability to satisfy the Ralph test. As Demski explains, a well-prepared model is

one that can answer the question that it poses. Thus, for example, it would be meaningless

to ask a model that assumes certainty what information is needed. As for the Ralph test, a

study is seen as passing this test to the extent that its central question is of classroom

importance and the answer that it provides is useful.

In total we found 283 MA articles, most of which had appeared in two journals:

Accounting Research (116) and Finance and Accounting (124). These 283 articles cover a

broad range of topics, including management control systems, cost accounting and man-

agement, externally oriented MA, decision-making techniques, and information technology

applications. We also found some significant differences in topic coverage between the two

subperiods 1997–2001 and 2002–2005.

7 Construct validity refers to whether a particular operational definition is indeed a valid measure of the construct

in question (Birnberg et al. 1990; Kerlinger and Lee 2000). For case study research, construct validity is con-

cerned with whether the issues or variables involved are specified, and whether the measures for the issues or

variables do indeed reflect the specific issues or variables under investigation. Triangulating with multiple sources

of evidence and creating a formal and presentable database are procedures for increasing construct validity (Yin

1994). For survey research, construct validity is concerned with the extent to which different measures of the

same construct converge and the extent to which measures of distinct constructs diverge (Cook and Campbell

1979; Kerlinger and Lee 2000). For field-archival research, researchers often rely on proxies if the variables of

interest cannot be directly measured; construct validity is expected to increase with the use of commonly

employed and / or widely validated measures. Internal validity is concerned with whether observed changes in

the dependent variables are indeed caused by changes in the independent variable(s) (Cook and Campbell 1979).

Internal validity does not apply to descriptive or exploratory studies (Yin 1994), and thus is assessed only for

the research that involves hypothesis testing and causal inferences. Pattern-matching is frequently used

for assessing internal validity of causal case study research (Yin 1994), and we examine whether such studies

in our sample have compared their observed patterns with ones predicted by theory. For survey research, we

focus on whether the authors have performed pre-testing, follow-up procedures, and nonresponse bias analysis

(Van der Stede et al. 2005). For field-archival research, we focus on whether the articles have used control

variables and whether there are omitted variables. External validity refers to the extent to which the obtained

result(s) can be generalized to other samples or settings (Campbell and Stanley 1966). Yin (1994) distinguishes

between statistical generalization and analytical generalization. The former concerns the ability to generalize the

findings obtained from one sample to other samples while in analytical generalization, researchers attempt to

generalize a set of results to some broader theory (Yin 1994). Yin (1994) suggests that while statistical gener-

alization applies to survey research, it does not apply to case study research. As such, for case study research,

we focus on whether the article under review explains why a case site is selected. For survey research and field-

archival research, we focus on sample description and response rate (in the case of survey research). Reliability

refers to the degree to which findings obtained by a researcher can be replicated by another researcher using

the same procedures. For case study research, we focus on whether the authors have used a case study protocol

or similar procedures. For survey research, we focus on reliability of measures for the variables of interest. For

field-archival research, we focus on the description of samples and databases.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

An Overview and Assessment of Contemporary Management Accounting Research in China 133

Journal of Management Accounting Research, Special Issue 2008

We found that normative / conceptualpapers dominated the sample, followed in de-

scending order by case studies, surveys, field-archival studies, and analytical modeling

research. There was a significant association between the papers’ age and their research

methods. There also was a greater focus on specific industrial, as compared to generic,

settings in the 2002–2005 period. In terms of theoretical underpinnings, 226 (79.9 percent)

of the articles were totally based on the authors’ own reasoning, with no explicit or de-

tectable application of extant theories or reference to empirical evidence. Among the much

smaller number of articles that explicitly or implicitly invoked theories, finance and eco-

nomic theories are applied most frequently. Because theory is important for guiding research

design and interpreting the findings, it is encouraging that both the absolute number and

proportion of papers applying theories are substantially higher in the more recent (2002–

2005) period.

In the following four sections of this report, we summarize the contents of the papers

by research topics, research methods, research settings, and the application of theory. Crit-

ical comments on the research are integrated into the sections on research methods and

theory application. The sixth section of the paper compares the topics covered by this set

of articles and ones identified by Chinese business managers as being important, while

the seventh section examines some factors that may have shaped Chinese MA research. The

final section provides a summary and discusses potential directions for advancing MA

research in China.

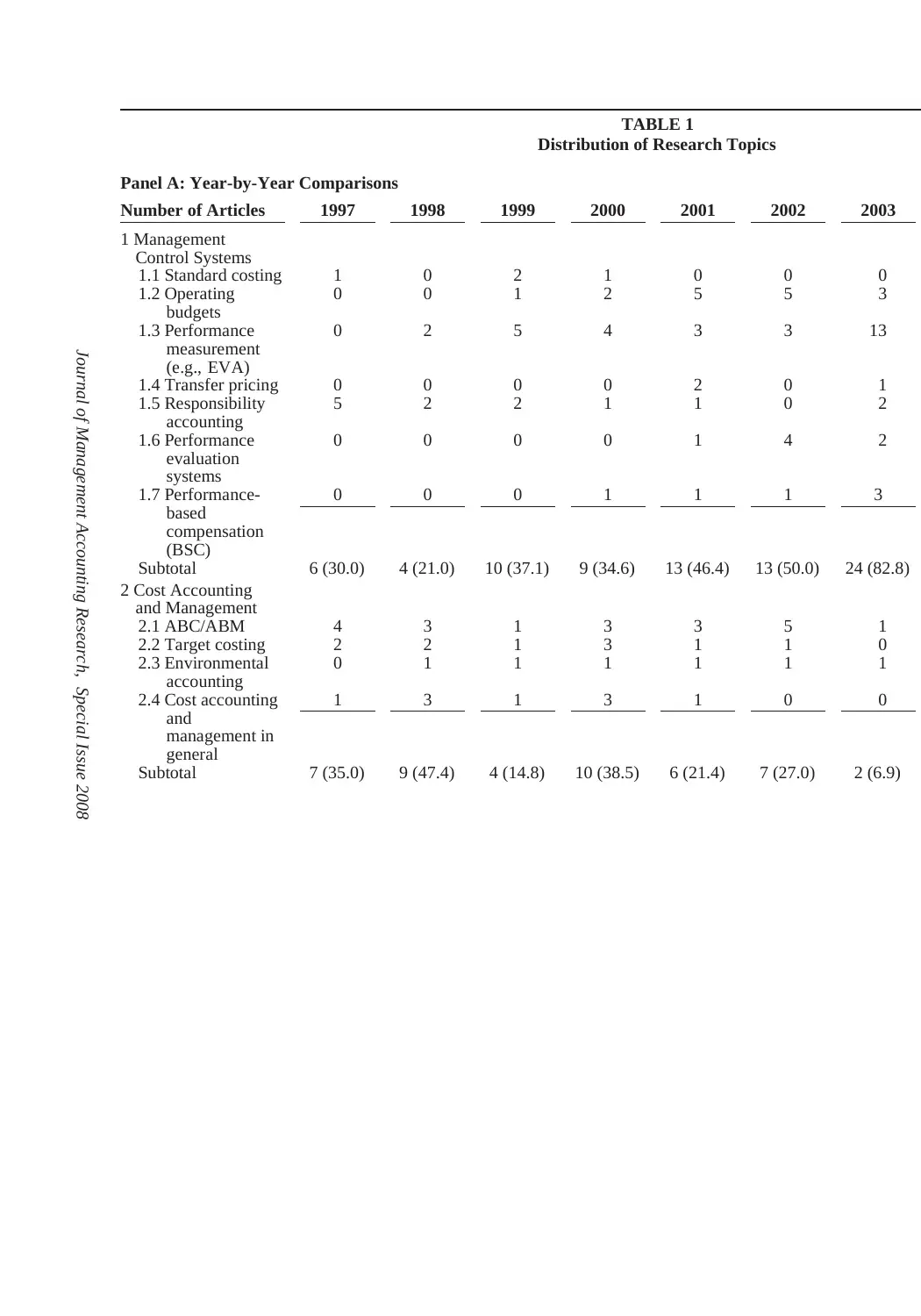

DISTRIBUTION OF RESEARCH TOPICS

To avoid an overly fragmented discussion, we followed the general approach of Shields

(1997) and assigned the 283 articles among the following categories: management control

systems, cost accounting and management, decision-making methods, externally oriented

MA, MA in general, information technology applications, and a catchall ‘‘other’’ category.

Table 1 shows the specific topics placed in each category. For example, the topics subsumed

under the ‘‘management control systems’’ heading include standard costing, operating budg-

ets, performance measurement (e.g., economic value added [EVA]), transfer pricing, re-

sponsibility accounting, performance evaluation systems (e.g., balanced scorecard), and

performance-based compensation.8 Panel A of Table 1 shows that 133 (47.0 percent) of the

articles examine issues related to management control systems, 69 (24.4 percent) deal with

cost accounting and management, 19 (6.7 percent) pertain to externally oriented MA, seven

(2.5 percent) focus on decision-making methods, and two (0.7 percent) address information

technology (IT) applications. The remaining articles either discuss general issues in MA

(34 articles, 12.0 percent) or other MA-related topics (19 articles, 6.7 percent).

Management Control Systems

Among the topics under the management control systems rubric, performance mea-

surement (47 articles) and operating budgeting (44 articles) have received the most atten-

tion. More than 20 percent of the performance measurement articles focus on EVA. Some

of these elaborate on the development and components of EVA, and provide guidelines to

enhance the benefits from using this measurement approach. Others are spread across the

8 We acknowledge that some of the topics could reasonably be placed in different categories from those we have

selected. For example, CVP and standard costing could also be considered cost accounting and management

techniques. However, the general thrust of our findings is not sensitive to these reclassifications, in part due to

the small numbers of studies on these topics. Also, we provide enough detail in Table 1 for readers to apply

their own topic classifications.

Journal of Management Accounting Research, Special Issue 2008

We found that normative / conceptualpapers dominated the sample, followed in de-

scending order by case studies, surveys, field-archival studies, and analytical modeling

research. There was a significant association between the papers’ age and their research

methods. There also was a greater focus on specific industrial, as compared to generic,

settings in the 2002–2005 period. In terms of theoretical underpinnings, 226 (79.9 percent)

of the articles were totally based on the authors’ own reasoning, with no explicit or de-

tectable application of extant theories or reference to empirical evidence. Among the much

smaller number of articles that explicitly or implicitly invoked theories, finance and eco-

nomic theories are applied most frequently. Because theory is important for guiding research

design and interpreting the findings, it is encouraging that both the absolute number and

proportion of papers applying theories are substantially higher in the more recent (2002–

2005) period.

In the following four sections of this report, we summarize the contents of the papers

by research topics, research methods, research settings, and the application of theory. Crit-

ical comments on the research are integrated into the sections on research methods and

theory application. The sixth section of the paper compares the topics covered by this set

of articles and ones identified by Chinese business managers as being important, while

the seventh section examines some factors that may have shaped Chinese MA research. The

final section provides a summary and discusses potential directions for advancing MA

research in China.

DISTRIBUTION OF RESEARCH TOPICS

To avoid an overly fragmented discussion, we followed the general approach of Shields

(1997) and assigned the 283 articles among the following categories: management control

systems, cost accounting and management, decision-making methods, externally oriented

MA, MA in general, information technology applications, and a catchall ‘‘other’’ category.

Table 1 shows the specific topics placed in each category. For example, the topics subsumed

under the ‘‘management control systems’’ heading include standard costing, operating budg-

ets, performance measurement (e.g., economic value added [EVA]), transfer pricing, re-

sponsibility accounting, performance evaluation systems (e.g., balanced scorecard), and

performance-based compensation.8 Panel A of Table 1 shows that 133 (47.0 percent) of the

articles examine issues related to management control systems, 69 (24.4 percent) deal with

cost accounting and management, 19 (6.7 percent) pertain to externally oriented MA, seven

(2.5 percent) focus on decision-making methods, and two (0.7 percent) address information

technology (IT) applications. The remaining articles either discuss general issues in MA

(34 articles, 12.0 percent) or other MA-related topics (19 articles, 6.7 percent).

Management Control Systems

Among the topics under the management control systems rubric, performance mea-

surement (47 articles) and operating budgeting (44 articles) have received the most atten-

tion. More than 20 percent of the performance measurement articles focus on EVA. Some

of these elaborate on the development and components of EVA, and provide guidelines to

enhance the benefits from using this measurement approach. Others are spread across the

8 We acknowledge that some of the topics could reasonably be placed in different categories from those we have

selected. For example, CVP and standard costing could also be considered cost accounting and management

techniques. However, the general thrust of our findings is not sensitive to these reclassifications, in part due to

the small numbers of studies on these topics. Also, we provide enough detail in Table 1 for readers to apply

their own topic classifications.

134 Duh, Xiao, and Chow

Journal of Management Accounting Research, Special Issue 2008

following three categories: (1) surveys on the potential benefits of EVA to firms, the pro-

cedures in calculating EVA including cost of equity capital, adjustments of generally ac-

cepted accounting principles (GAAP) numbers, and the difficulties of making such calcu-

lations; (2) calculations of EVA for listed companies and comparing the rankings with one

provided by Stern Stewart; and (3) comparing EVA and other financial measures on their

association with stock prices. There also are papers that review the development of per-

formance measurement and / or introduce and compare various performance measures (e.g.,

shareholder value added, cash value added, cash flow return on investment), and case studies

on how firms evaluate the performance of departments or subsidiaries. The State-Owned

Capital Performance Measurement System promoted by the central government is also

reviewed, and evaluated by the associations of measures in the system (e.g., return on

equity) with stock prices or returns. 9 Some papers provide suggestions for firms in selecting

performance measures. Pan (2002), for example, argues that different performance measures

should be used by firms with different characteristics, e.g., high-tech firms (share price

based) and traditional firms (net income based); growth firms (share price based) and mature

firms (net income based).

Most of the operating budgeting articles point out the pitfalls of, misunderstandings

about, or difficulties in budgeting practices, and offer guidelines for improvement. For

example, Zhao (2003) indicates that mistakes often observed in practice include preparing

budgets for their own sake without thinking of the purposes of budgeting; erroneously

thinking that budgeting is purely a financial exercise that involves only finance staff and

financial control; vulnerability to budgetary slack creation; and preparing budgets on an

incremental basis without analyzing the costs and revenues of activities along the value

chain. Wang (1999) argues that firms at different stages of development should have dif-

ferent foci in their budget management systems, e.g., capital budgeting for new firms, sales

budgeting for growth firms, cost control for mature firms, and cash flows for declining

firms. Yu et al. (2004) propose a budgeting system framework consisting of three modes:

production capacity oriented, sales oriented, and profit oriented. In turn, each mode contains

five elements: modules and their relations, relations with financial accounting, relations

with non-financial measures, relations with strategy, and relations with incentive systems.

Beyond these normative articles, there are reports on successful budgeting system imple-

mentations which include details on the contents and processes of budgeting, and how

budgeting systems relate to other systems such as responsibility accounting.

Even though responsibility accounting has long been used in China, it still attracted

the attention of 13 articles. Writings on this topic encompass (1) explaining the origin

and development of the internal economic responsibility system (IERS); (2) comparing

IERS to responsibility accounting systems in the West; (3) highlighting the problems

with implementing a responsibility accounting system; (4) describing the operation of in-

ternal banks in various firms such as oil and gas companies; and (5) case studies of the

internal contract system’s application in railroad construction projects and the iron and steel

9 Zhang (2001) makes the case that Chinese companies’ performance measurement practices are heavily influenced

by government mandates. First, the ‘‘Basic Financial Standards for Business Enterprises’’ of 1992 stipulated

ratios meant to support central government control (e.g., debt to assets, current ratio, quick ratio, stock turnover,

profit and tax over sales, and return on equity). In 1995 the Ministry of Finance issued the (trial) ‘‘Measurement

System for Enterprise Performance Evaluation,’’ which also specified measures to be computed (e.g., return on

sales, return on equity, capital maintenance and growth rate, debt to assets ratio). Finally, a new ‘‘State Owned

Capital Performance Measurement System’’ was introduced by four government ministries (Ministry of Finance,

State Economic and Trade Commission, Ministry of Personnel, and State Development and Planning Commis-

sion) in the 1995–1999 period. This system included 32 items such as return on equity, solvency, and growth

potential. More details about these developments are available in Chow et al. (2007).

Journal of Management Accounting Research, Special Issue 2008

following three categories: (1) surveys on the potential benefits of EVA to firms, the pro-

cedures in calculating EVA including cost of equity capital, adjustments of generally ac-

cepted accounting principles (GAAP) numbers, and the difficulties of making such calcu-

lations; (2) calculations of EVA for listed companies and comparing the rankings with one

provided by Stern Stewart; and (3) comparing EVA and other financial measures on their

association with stock prices. There also are papers that review the development of per-

formance measurement and / or introduce and compare various performance measures (e.g.,

shareholder value added, cash value added, cash flow return on investment), and case studies

on how firms evaluate the performance of departments or subsidiaries. The State-Owned

Capital Performance Measurement System promoted by the central government is also

reviewed, and evaluated by the associations of measures in the system (e.g., return on

equity) with stock prices or returns. 9 Some papers provide suggestions for firms in selecting

performance measures. Pan (2002), for example, argues that different performance measures

should be used by firms with different characteristics, e.g., high-tech firms (share price

based) and traditional firms (net income based); growth firms (share price based) and mature

firms (net income based).

Most of the operating budgeting articles point out the pitfalls of, misunderstandings

about, or difficulties in budgeting practices, and offer guidelines for improvement. For

example, Zhao (2003) indicates that mistakes often observed in practice include preparing

budgets for their own sake without thinking of the purposes of budgeting; erroneously

thinking that budgeting is purely a financial exercise that involves only finance staff and

financial control; vulnerability to budgetary slack creation; and preparing budgets on an

incremental basis without analyzing the costs and revenues of activities along the value

chain. Wang (1999) argues that firms at different stages of development should have dif-

ferent foci in their budget management systems, e.g., capital budgeting for new firms, sales

budgeting for growth firms, cost control for mature firms, and cash flows for declining

firms. Yu et al. (2004) propose a budgeting system framework consisting of three modes:

production capacity oriented, sales oriented, and profit oriented. In turn, each mode contains

five elements: modules and their relations, relations with financial accounting, relations

with non-financial measures, relations with strategy, and relations with incentive systems.

Beyond these normative articles, there are reports on successful budgeting system imple-

mentations which include details on the contents and processes of budgeting, and how

budgeting systems relate to other systems such as responsibility accounting.

Even though responsibility accounting has long been used in China, it still attracted

the attention of 13 articles. Writings on this topic encompass (1) explaining the origin

and development of the internal economic responsibility system (IERS); (2) comparing

IERS to responsibility accounting systems in the West; (3) highlighting the problems

with implementing a responsibility accounting system; (4) describing the operation of in-

ternal banks in various firms such as oil and gas companies; and (5) case studies of the

internal contract system’s application in railroad construction projects and the iron and steel

9 Zhang (2001) makes the case that Chinese companies’ performance measurement practices are heavily influenced

by government mandates. First, the ‘‘Basic Financial Standards for Business Enterprises’’ of 1992 stipulated

ratios meant to support central government control (e.g., debt to assets, current ratio, quick ratio, stock turnover,

profit and tax over sales, and return on equity). In 1995 the Ministry of Finance issued the (trial) ‘‘Measurement

System for Enterprise Performance Evaluation,’’ which also specified measures to be computed (e.g., return on

sales, return on equity, capital maintenance and growth rate, debt to assets ratio). Finally, a new ‘‘State Owned

Capital Performance Measurement System’’ was introduced by four government ministries (Ministry of Finance,

State Economic and Trade Commission, Ministry of Personnel, and State Development and Planning Commis-

sion) in the 1995–1999 period. This system included 32 items such as return on equity, solvency, and growth

potential. More details about these developments are available in Chow et al. (2007).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

An Overview and Assessment of Contemporary Management Accounting Research in China 135

Journal of Management Accounting Research, Special Issue 2008

manufacturing industries. Focusing on responsibility accounting practices in general, Liu

et al. (1998) argue that Western responsibility accounting is richer than that practiced in

China. In particular, they assert that the former starts from market or sales forecasts, while

the latter starts from targets passed down from superiors; the former is authoritative and

relates to compensation while the latter does not; the former involves the whole firm, its

components and their heads while the latter does not involve subunits and heads; and the

former emphasizes such value indicators as capital, cost, and profit whereas the latter

stresses production and physical indicators. Yang (1997) argues that China’s Internal Eco-

nomic Responsibility System (IERS) differs from the responsibility accounting systems of

the West. He traces the origins of IERS to the ‘‘Shift and Group Business Accounting

System’’ used in the 1950s and 1960s to make individual workers fulfill their own respon-

sibility. The system evolved in the subsequent decades into the IERS. While many forms

of IERS exist in practice, they share several features. First, all involve a contract-based

relationship between the enterprise, usually represented by its top managers, and its super-

visory state agency. Second, the managers face substantial risks and rewards because their

performance is linked to their enterprises’ performance. Third, there is an open selection

of enterprise managers. Finally, most systems have multiyear targets and incentives in order

to curb management myopia.

Articles on the internal bank hold that it is another unique feature of responsibility

accounting systems in China (e.g., Zhang 1997). This mechanism can be traced back to

1970 as a means for settling internal transactions, credit and funds-use control, and re-

sponsibility management. It was widely promoted by the State Economic Commission

(which later became the State Economic and Trade Commission) in 1979, and became

widespread in the late 1980s and early 1990s (Zhang 1993). Zhang (1997) maintains that

the internal bank must be integrated with other components of responsibility accounting

such as responsibility unit assignment, responsibility budgeting, control, and evaluation of

responsibility units. In contrast to these analyses at general levels, Miao (2000) focuses on

specific company practices and compares standard costing in Baogang (an iron and steel

company) with responsibility cost management in Angang (another iron and steel company).

All of the 11 articles on performance evaluation systems deal with the balanced score-

card (BSC). Most are concerned with explaining the concepts and contents of BSC and

why it is superior to the traditional performance evaluation system. These papers elaborate

on the four dimensions of performance measures as suggested by Kaplan and Norton (1992,

1996, 2001) and their linkages with firm strategy. The limitations of BSC also are indicated,

including the development and implementation costs, and the difficulty of setting targets

and weights for the performance measures. Several papers report on how BSC adoptions

in the banking and high-tech industries enhance competitive advantages. Integrating BSC

with other systems such as EVA, executive stock options, and enterprise resource planning

(ERP) also is discussed. It is pointed out, for example, that applying BSC in an ERP

environment can facilitate access to performance measurement data and help to assess

supply chain performance. Finally, the ten articles on performance-based compensation

either address the association between managerial incentive contracts and accounting choice

by reviewing and summarizing the Western agency theory literature, or replicate prior West-

ern studies by empirically examining the determinants of executive compensation including

firm performance, managerial control, managerial ownership, diversification, and firm risk.

Taken as a whole, this category of research introduces new management control systems

such as EVA and BSC, on the one hand. On the other hand, it explicitly points out the

unique features of management control systems in China by, for example, comparing re-

sponsibility accounting in China with that in the West. Although a majority of these articles

Journal of Management Accounting Research, Special Issue 2008

manufacturing industries. Focusing on responsibility accounting practices in general, Liu

et al. (1998) argue that Western responsibility accounting is richer than that practiced in

China. In particular, they assert that the former starts from market or sales forecasts, while

the latter starts from targets passed down from superiors; the former is authoritative and

relates to compensation while the latter does not; the former involves the whole firm, its

components and their heads while the latter does not involve subunits and heads; and the

former emphasizes such value indicators as capital, cost, and profit whereas the latter

stresses production and physical indicators. Yang (1997) argues that China’s Internal Eco-

nomic Responsibility System (IERS) differs from the responsibility accounting systems of

the West. He traces the origins of IERS to the ‘‘Shift and Group Business Accounting

System’’ used in the 1950s and 1960s to make individual workers fulfill their own respon-

sibility. The system evolved in the subsequent decades into the IERS. While many forms

of IERS exist in practice, they share several features. First, all involve a contract-based

relationship between the enterprise, usually represented by its top managers, and its super-

visory state agency. Second, the managers face substantial risks and rewards because their

performance is linked to their enterprises’ performance. Third, there is an open selection

of enterprise managers. Finally, most systems have multiyear targets and incentives in order

to curb management myopia.

Articles on the internal bank hold that it is another unique feature of responsibility

accounting systems in China (e.g., Zhang 1997). This mechanism can be traced back to

1970 as a means for settling internal transactions, credit and funds-use control, and re-

sponsibility management. It was widely promoted by the State Economic Commission

(which later became the State Economic and Trade Commission) in 1979, and became

widespread in the late 1980s and early 1990s (Zhang 1993). Zhang (1997) maintains that

the internal bank must be integrated with other components of responsibility accounting

such as responsibility unit assignment, responsibility budgeting, control, and evaluation of

responsibility units. In contrast to these analyses at general levels, Miao (2000) focuses on

specific company practices and compares standard costing in Baogang (an iron and steel

company) with responsibility cost management in Angang (another iron and steel company).

All of the 11 articles on performance evaluation systems deal with the balanced score-

card (BSC). Most are concerned with explaining the concepts and contents of BSC and

why it is superior to the traditional performance evaluation system. These papers elaborate

on the four dimensions of performance measures as suggested by Kaplan and Norton (1992,

1996, 2001) and their linkages with firm strategy. The limitations of BSC also are indicated,

including the development and implementation costs, and the difficulty of setting targets

and weights for the performance measures. Several papers report on how BSC adoptions

in the banking and high-tech industries enhance competitive advantages. Integrating BSC

with other systems such as EVA, executive stock options, and enterprise resource planning

(ERP) also is discussed. It is pointed out, for example, that applying BSC in an ERP

environment can facilitate access to performance measurement data and help to assess

supply chain performance. Finally, the ten articles on performance-based compensation

either address the association between managerial incentive contracts and accounting choice

by reviewing and summarizing the Western agency theory literature, or replicate prior West-

ern studies by empirically examining the determinants of executive compensation including

firm performance, managerial control, managerial ownership, diversification, and firm risk.

Taken as a whole, this category of research introduces new management control systems

such as EVA and BSC, on the one hand. On the other hand, it explicitly points out the

unique features of management control systems in China by, for example, comparing re-

sponsibility accounting in China with that in the West. Although a majority of these articles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

136 Duh, Xiao, and Chow

Journal of Management Accounting Research, Special Issue 2008

do not involve, in theory, development or testing, a few use the archival field data to

investigate the relevance of various performance measures to stock price, and the deter-

minants of executive compensation.

Cost Accounting and Management

Almost half (31) of the 69 articles in this category pursue issues related to activity-

based costing / activity-based management (ABC / ABM). There also are 10 articles on target

costing and nine on environmental accounting; the remaining 19 articles address a range

of general issues in this area.

The ABC / ABM papers introduce and explain concepts such as value-added activities,

cost drivers, resource drivers, activity drivers, and the procedures for calculating ABC

product costs. Symptoms of obsolete cost systems also are mentioned. Differences between

‘‘traditional’’ cost systems and ABC are discussed via numerical examples, some of which

are based on field data. There also are case studies of ABC adoption by firms in the

petroleum, electrical devices, iron and steel, and railroad industries. Some papers suggest

conditions conducive to ABC/ABM adoption, including adequacy of information systems

and quality of the accounting personnel. Other papers propose integrating ABC/ ABM with

other MA practices like the budgeting system (activity-based budgeting), variance analysis,

standard costing, responsibility accounting, Pareto analysis, cause and effect analysis, and

value chain analysis. Capacity management via ABC also is suggested by differentiating

among idle, non-productive, and productive capacity. It is even proposed that cost of capital

be included in ABC product costs for conducting product profitability analysis. In contrast,

one paper argues that process flows, activity consumption, activity driver rates, and market

situations are changing over time and thus, static models of product costing are not appro-

priate (Zhang and Wei 2000). This paper, however, does not back up its assertions with

any explicit analytical model. Another paper proposes a workshop activity optimization

model using ABC, and uses data from an actual company to solve the optimization problem

(Zhang et al. 2002).

The relatively high level of attention to target costing (10 articles) may be due to its

perceived similarity to the highly touted Hangang experience. Hangang is the abbreviated

English name of Handan Iron and Steel Co. Its cost management practice is often compared

to target costing and considered a major factor for the company’s economic success. Re-

search on the Hangang experience highlights the implementation and distinctive features

of this practice. In particular, the company introduced a system of ‘‘market simulation-

based accounting and cost negation’’ in 1991. Under this system, Hangang set internal

transfer prices among branch factories by taking the average market prices of half-finished

goods and adjusting these for market changes semi-annually or annually. The transfer prices

were included in calculating each factory’s manufacturing costs and gross profit, and ad-

ministrative expenses and financial expenses were deducted from the latter to arrive at the

profit figure. If a factory’s manufacturing cost was lower than the target set by the company,

then there would be a reward. Otherwise, no reward would be forthcoming (this approach

to determining rewards is what constitutes the ‘‘cost negation’’ method).

A number of papers are concerned with whether the Hangang system is or is not target

costing. Wang (1998) argues that it is, while Sun and Cao (2000) argue that it is not because

target costing has an ex ante focus, whereas the Hangang system is ex post because of cost

negation. Sun and Cao (2000) further emphasize that target costing focuses on new product

planning, and extends cost management beyond the firm to include supply chain partners.

Thus, even in the case of an exemplary Chinese business enterprise, MA practices still

Journal of Management Accounting Research, Special Issue 2008

do not involve, in theory, development or testing, a few use the archival field data to

investigate the relevance of various performance measures to stock price, and the deter-

minants of executive compensation.

Cost Accounting and Management

Almost half (31) of the 69 articles in this category pursue issues related to activity-

based costing / activity-based management (ABC / ABM). There also are 10 articles on target

costing and nine on environmental accounting; the remaining 19 articles address a range

of general issues in this area.

The ABC / ABM papers introduce and explain concepts such as value-added activities,

cost drivers, resource drivers, activity drivers, and the procedures for calculating ABC

product costs. Symptoms of obsolete cost systems also are mentioned. Differences between

‘‘traditional’’ cost systems and ABC are discussed via numerical examples, some of which

are based on field data. There also are case studies of ABC adoption by firms in the

petroleum, electrical devices, iron and steel, and railroad industries. Some papers suggest

conditions conducive to ABC/ABM adoption, including adequacy of information systems

and quality of the accounting personnel. Other papers propose integrating ABC/ ABM with

other MA practices like the budgeting system (activity-based budgeting), variance analysis,

standard costing, responsibility accounting, Pareto analysis, cause and effect analysis, and

value chain analysis. Capacity management via ABC also is suggested by differentiating

among idle, non-productive, and productive capacity. It is even proposed that cost of capital

be included in ABC product costs for conducting product profitability analysis. In contrast,

one paper argues that process flows, activity consumption, activity driver rates, and market

situations are changing over time and thus, static models of product costing are not appro-

priate (Zhang and Wei 2000). This paper, however, does not back up its assertions with

any explicit analytical model. Another paper proposes a workshop activity optimization

model using ABC, and uses data from an actual company to solve the optimization problem

(Zhang et al. 2002).

The relatively high level of attention to target costing (10 articles) may be due to its

perceived similarity to the highly touted Hangang experience. Hangang is the abbreviated

English name of Handan Iron and Steel Co. Its cost management practice is often compared

to target costing and considered a major factor for the company’s economic success. Re-

search on the Hangang experience highlights the implementation and distinctive features

of this practice. In particular, the company introduced a system of ‘‘market simulation-

based accounting and cost negation’’ in 1991. Under this system, Hangang set internal

transfer prices among branch factories by taking the average market prices of half-finished

goods and adjusting these for market changes semi-annually or annually. The transfer prices

were included in calculating each factory’s manufacturing costs and gross profit, and ad-

ministrative expenses and financial expenses were deducted from the latter to arrive at the

profit figure. If a factory’s manufacturing cost was lower than the target set by the company,

then there would be a reward. Otherwise, no reward would be forthcoming (this approach

to determining rewards is what constitutes the ‘‘cost negation’’ method).

A number of papers are concerned with whether the Hangang system is or is not target

costing. Wang (1998) argues that it is, while Sun and Cao (2000) argue that it is not because

target costing has an ex ante focus, whereas the Hangang system is ex post because of cost

negation. Sun and Cao (2000) further emphasize that target costing focuses on new product

planning, and extends cost management beyond the firm to include supply chain partners.

Thus, even in the case of an exemplary Chinese business enterprise, MA practices still

An Overview and Assessment of Contemporary Management Accounting Research in China 137

Journal of Management Accounting Research, Special Issue 2008

seem to lag cutting-edge developments, though Xu (2002) reports that Hangang’s cost

management system has evolved to place an increasing emphasis on ex ante cost design.

Of the articles that do not mention the Hangang experience, several explain the concepts

and implementation of target costing in the product planning and design stage. Others

suggest using ABC to assist in cost estimation, and several suggest the possibility of em-

ploying value engineering. The articles related to environmental accounting call for its

inclusion within the scope of MA. Methods of calculating internal and external environ-

mental costs are proposed, and their allocation to products is suggested to reflect the ‘‘true’’

costs and to calculate ‘‘green bottom lines.’’ The remaining cost accounting and manage-

ment articles discuss issues in this area, but either do not specify a particular MA technique,

or mention several techniques at once. Some call for changes in cost management (e.g.,

adoption of daily cost reporting and the total cost management notion) in response to

changes in the manufacturing and market environments and management theories. Others

offer cost management suggestions to firms in the distribution and real estate industries.

There also are case studies from the petroleum and iron and steel industries. One paper

reports the results of a survey on cost management methods in use. Proposals also are

offered for defining the scope of ‘‘modern’’ cost management and the concept of cost.

Zhang (2004), for example, suggests establishing standards to define costs, and stipulating

the procedures for cost calculation and allocation.

Decision-Making Methods

Articles under this heading encompass capital budgeting (four articles) and CVP anal-

ysis (three articles). Relating to the former, a paper argues that risk analysis should be

explicitly incorporated into capital budgeting, and demonstrates Monte Carlo simulation

with a case study. Another paper suggests using EVA as a criterion for assessing the per-

formance of information technology investments. The other papers either emphasize the

distinction between making capital budget decisions and their administration, or call for

attention to strategic and organizational aspects of capital budgeting. The articles on CVP

include a case study in the petroleum industry and an explanation of a break-even period

measure (the length of time required to achieve a pre-specified level of profit).

Externally Oriented Management Accounting

Two lines of research fall into this category: value chain analysis (ten articles) and

strategic MA (nine articles). Some papers on value chain analysis elaborate on the ‘‘value

chain accounting management’’ system proposed by a Chinese scholar named Dawu Yan.

In 1983, Yan had suggested that ‘‘it is feasible to abstract the content of accounting man-

agement into value activities,’’ and that ‘‘accounting management should be part of the

value management system’’ (Yan and Yin 2003a, 200b). Yu and Zhang (2005) assert that

the approach suggested by Yan changes the scope and content of MA by integrating value

chain analysis and MA and as such, is a contribution to accounting theory in the world.

Chi and Yang (2005) position value chain accounting management as a tool as well as an

essential part of value chain management. Yang (2005) proposes changes to information

systems to facilitate management and control over the allied enterprises in the value chain.

Other papers offer guidelines for value chain analysis, integrate value chain analysis with

ABC to manage costs along the value chain, or review the evolution of thoughts about

‘‘value,’’ including the concept of a value chain. Finally, a paper extends value chain man-

agement to the virtual value chain and proposes the concept of a cyber value flow.

Journal of Management Accounting Research, Special Issue 2008

seem to lag cutting-edge developments, though Xu (2002) reports that Hangang’s cost

management system has evolved to place an increasing emphasis on ex ante cost design.

Of the articles that do not mention the Hangang experience, several explain the concepts

and implementation of target costing in the product planning and design stage. Others

suggest using ABC to assist in cost estimation, and several suggest the possibility of em-

ploying value engineering. The articles related to environmental accounting call for its

inclusion within the scope of MA. Methods of calculating internal and external environ-

mental costs are proposed, and their allocation to products is suggested to reflect the ‘‘true’’

costs and to calculate ‘‘green bottom lines.’’ The remaining cost accounting and manage-

ment articles discuss issues in this area, but either do not specify a particular MA technique,

or mention several techniques at once. Some call for changes in cost management (e.g.,

adoption of daily cost reporting and the total cost management notion) in response to

changes in the manufacturing and market environments and management theories. Others

offer cost management suggestions to firms in the distribution and real estate industries.

There also are case studies from the petroleum and iron and steel industries. One paper

reports the results of a survey on cost management methods in use. Proposals also are

offered for defining the scope of ‘‘modern’’ cost management and the concept of cost.

Zhang (2004), for example, suggests establishing standards to define costs, and stipulating

the procedures for cost calculation and allocation.

Decision-Making Methods

Articles under this heading encompass capital budgeting (four articles) and CVP anal-

ysis (three articles). Relating to the former, a paper argues that risk analysis should be

explicitly incorporated into capital budgeting, and demonstrates Monte Carlo simulation

with a case study. Another paper suggests using EVA as a criterion for assessing the per-

formance of information technology investments. The other papers either emphasize the

distinction between making capital budget decisions and their administration, or call for

attention to strategic and organizational aspects of capital budgeting. The articles on CVP

include a case study in the petroleum industry and an explanation of a break-even period

measure (the length of time required to achieve a pre-specified level of profit).

Externally Oriented Management Accounting

Two lines of research fall into this category: value chain analysis (ten articles) and