MGT520: Financial Analysis of Warren Buffett's PacifiCorp Investment

VerifiedAdded on 2023/01/23

|6

|1229

|27

Case Study

AI Summary

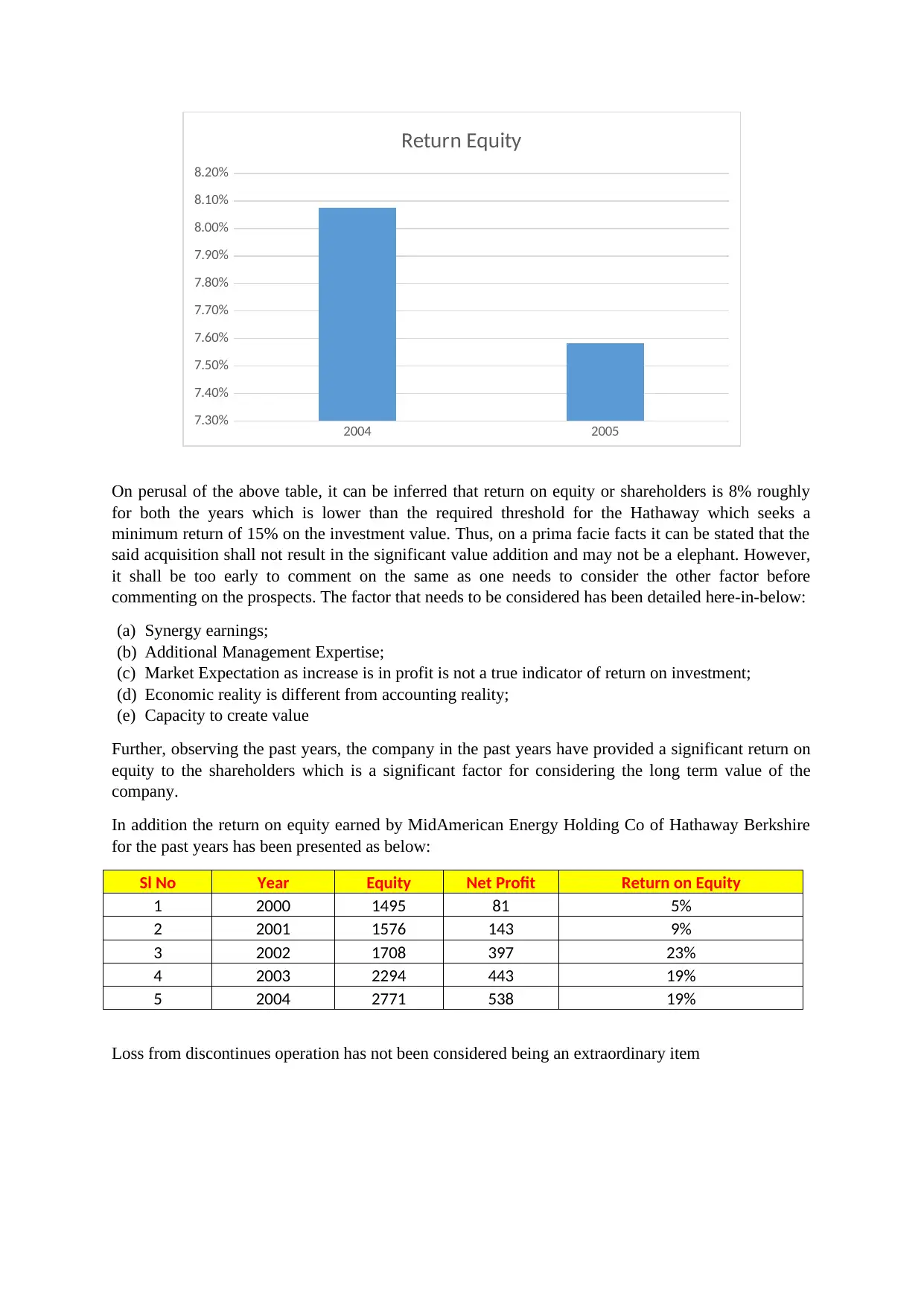

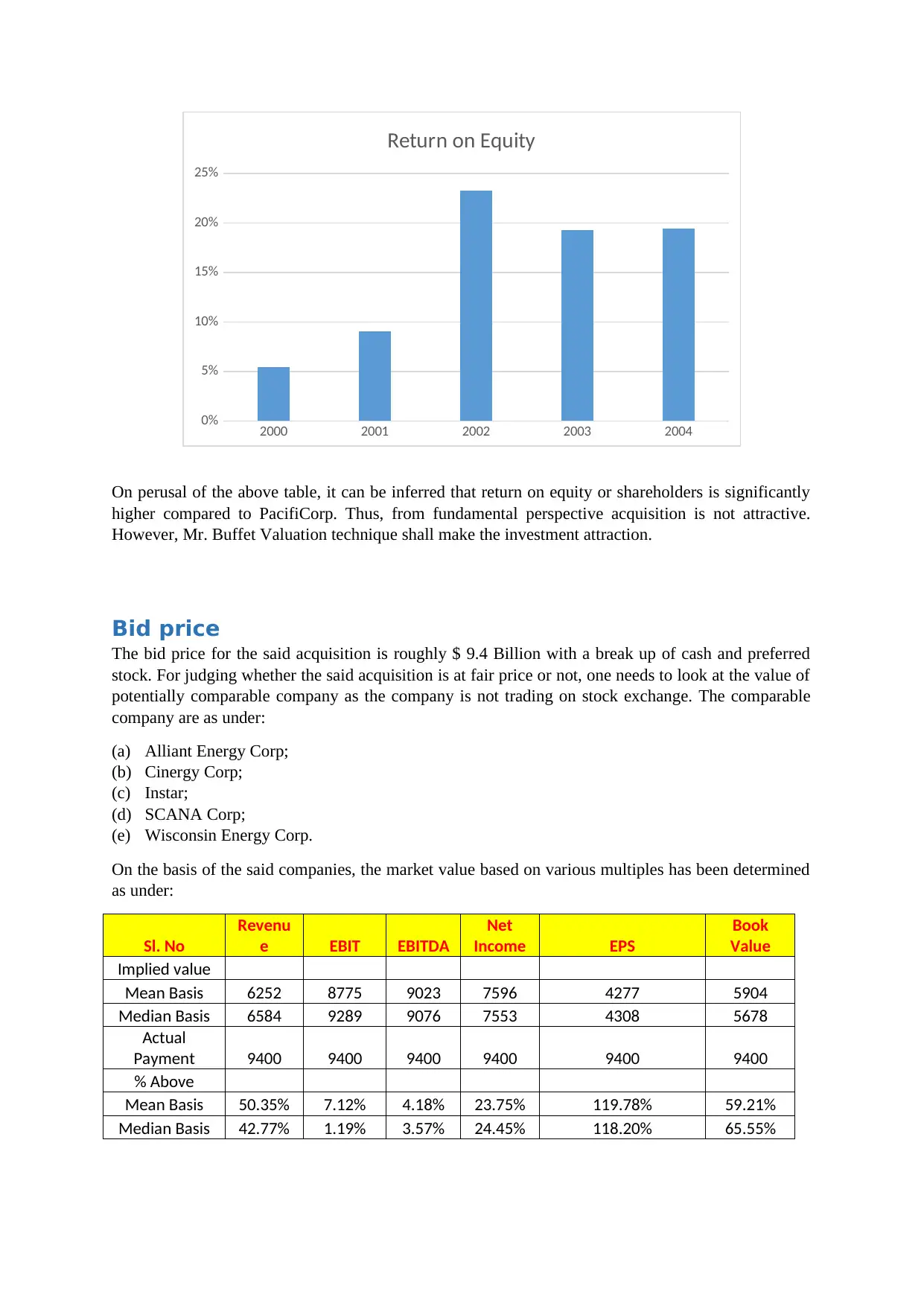

This report provides an in-depth analysis of Warren Buffett's proposed investment in PacifiCorp, examining whether the acquisition constitutes a sound financial decision. The case study delves into the financial performance of PacifiCorp, calculating the return on equity and comparing it to Hathaway Berkshire's required return. It explores the bid price, comparing it to comparable companies using various valuation multiples, with a focus on EBITDA as the most relevant metric. The report also discusses the factors influencing the increase in share price and concludes that the current acquisition valuation is appropriate, while acknowledging that the ultimate success of the acquisition requires consideration of broader economic factors. The report uses the principles of value-based investment strategy and the doctrines of Warren Buffet and Charlie Munger.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.