Determinants of Cost of Equity: Evidence from Pakistan Stock Exchange

VerifiedAdded on 2022/10/15

|16

|7786

|18

Report

AI Summary

This research paper examines the determinants of the cost of equity in Pakistan, utilizing a dataset of 263 firms listed on the Pakistan Stock Exchange. The study employs the Capital Asset Pricing Model (CAPM) to calculate the cost of equity, considering the signaling effect of information on market performance. Correlation and regression analyses are conducted to assess the impact of various factors, including net earnings, retention of funds, times interest earned, gearing, fixed asset backing, long-term debt, tax, and market capitalization. The results highlight a significant impact of market capitalization on the cost of equity, while other factors show no significant effect. The study also identifies a sector-specific range for the cost of equity, indicating the volatility of Pakistani financial markets in line with signaling theory. The paper contributes to the existing literature by applying Western-identified determinants in an emerging market context and aligns with the Pecking Order Proposition. It explores the relationship between wealth maximization and the cost of capital, providing valuable insights for corporate finance managers in Pakistan's industrial sectors.

Abasyn Journal of Social Sciences – Volume 9 – Issue 2

527

The Determinants of the Cost of Equity: Evidence from Pakistan

Muhammad Akhtar

Assistant Professor, Riphah International University, Islamabad.

Dr. Ahmad Raza Bilal

Assistant Professor, Superior University Lahore, Pakistan

Dr. Muhammad Naveed

Assistant Professor, Riphah International University, Islamabad.

Abstract

This research investigates the determinants of cost of equity using a data set of

263 firms listed on Pakistan stock exchange. Keeping in view the signaling effect

of information on the performance of capital markets in Pakistan, we used

Capital Asset Pricing Model (CAPM) to calculate the cost of equity. Correlation

and regression analysis were run to test the main effect of net earnings,

retention of fund, time interest earned, gearing, fixed asset backing, long term

debt, tax, market capitalization on cost of equity. The results’ robustness is

evidenced that market capitalization has significant impact on cost of equity. We

also show that net earnings growth, retention of funds, times interest earned,

gearing, fixed asset backing, long term debt and tax have no impact on cost of

equity. Finally, we find a sector-specific range of cost of equity that falls

between 11.54 to 16.78 percent. This indicates that financial markets in

Pakistan are more volatile with respect to any information in line with the

signaling theory.

Keywords: Determinants of Cost of Equity, Capital Asset Pricing Model,

Pakistan

The purpose of this study is to bridge the gap between theory and

practice by analyzing the determinants of cost of equity. Although many

studies have been undertaken on the determinants of capital structure,

however insufficient attention has been paid to the determinants of cost

of equity in emerging market. The cost of capital is an important issue in

corporate finance, still very less is known about it in emerging markets

(Barry, Peavy & Rodriguez, 1998). Majority of the studies on cost of

equity suggest different determinants for cost of equity: Informational

quality (Lambert, Leuz & Verrecchia, 2007), earning restatement (Hribar

& Jenkins, 2004), disclosure level (Espinosa & Trombetta, 2007),

Information Asymmetry (Lambert, Leuz & Verrecchia, 2012),

Ownership (Core, Hail & Verdi, 2015), Voluntary disclosure (Clinch &

Verrecchia, 2015), informed trading (Brennan, Huh & Subrahmanyam,

2015) and corporate social responsibility (Xu, Liu & Huang, 2015). All

of these studies deal with developing economies and emerging

economies but none of these studies has shaded lights in Pakistan

perspective. A vast number of literatures suggest that due macro

economic factors the determinants of cost of equity may vary from

527

The Determinants of the Cost of Equity: Evidence from Pakistan

Muhammad Akhtar

Assistant Professor, Riphah International University, Islamabad.

Dr. Ahmad Raza Bilal

Assistant Professor, Superior University Lahore, Pakistan

Dr. Muhammad Naveed

Assistant Professor, Riphah International University, Islamabad.

Abstract

This research investigates the determinants of cost of equity using a data set of

263 firms listed on Pakistan stock exchange. Keeping in view the signaling effect

of information on the performance of capital markets in Pakistan, we used

Capital Asset Pricing Model (CAPM) to calculate the cost of equity. Correlation

and regression analysis were run to test the main effect of net earnings,

retention of fund, time interest earned, gearing, fixed asset backing, long term

debt, tax, market capitalization on cost of equity. The results’ robustness is

evidenced that market capitalization has significant impact on cost of equity. We

also show that net earnings growth, retention of funds, times interest earned,

gearing, fixed asset backing, long term debt and tax have no impact on cost of

equity. Finally, we find a sector-specific range of cost of equity that falls

between 11.54 to 16.78 percent. This indicates that financial markets in

Pakistan are more volatile with respect to any information in line with the

signaling theory.

Keywords: Determinants of Cost of Equity, Capital Asset Pricing Model,

Pakistan

The purpose of this study is to bridge the gap between theory and

practice by analyzing the determinants of cost of equity. Although many

studies have been undertaken on the determinants of capital structure,

however insufficient attention has been paid to the determinants of cost

of equity in emerging market. The cost of capital is an important issue in

corporate finance, still very less is known about it in emerging markets

(Barry, Peavy & Rodriguez, 1998). Majority of the studies on cost of

equity suggest different determinants for cost of equity: Informational

quality (Lambert, Leuz & Verrecchia, 2007), earning restatement (Hribar

& Jenkins, 2004), disclosure level (Espinosa & Trombetta, 2007),

Information Asymmetry (Lambert, Leuz & Verrecchia, 2012),

Ownership (Core, Hail & Verdi, 2015), Voluntary disclosure (Clinch &

Verrecchia, 2015), informed trading (Brennan, Huh & Subrahmanyam,

2015) and corporate social responsibility (Xu, Liu & Huang, 2015). All

of these studies deal with developing economies and emerging

economies but none of these studies has shaded lights in Pakistan

perspective. A vast number of literatures suggest that due macro

economic factors the determinants of cost of equity may vary from

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abasyn Journal of Social Sciences – Volume 9 – Issue 2

528

country to country and culture to culture. Therefore the current study is

an attempt to fill this gap aligned with the Pecking order Proposition.

Out of many objectives of corporate finance managers one is the

maximization of the shareholders’ wealth. The conventional measure of

maximize of the shareholders wealth by increasing net income of the

business is not a viable approach. The study of suggests that there is

linear association between wealth maximization and cost of capital

(Bhatnagar, Kumari & Sharma, 2015). However, the said objective could

be achieved by lowering the cost of capital. We conducted this study in

different industrial sectors of Pakistan, Thus Pakistani industry provided

a natural laboratory for verifying the impact of different variables

identified as determinants of firms’ cost of equity. Several studies

suggest several determinants of cost equity. In particular we examine

how net earnings growth, retention of funds, times interest earned,

gearing, fixed asset backing, long term debt, tax, and market

capitalization may be helpful in determining the cost of equity.

Earning is a determinant of cost of equity (Fama & French,

1998). Growth in earnings stimulates the expectations of the shareholders

which increase cost of equity

(Bilal, Khan and Akoorie, 2016). Times interest earned is another

determinant of equity. Greater interest coverage ratio reduces financial

risk and cost of equity as well (Horne & Wachowicz, 1998). Debt

financing will increase the financial risk and ultimately increases the

expected return of the equity holder (Change & Rhee, 1990). Short term

financing is on higher side as compared to long term financing in

emerging markets (Booth, Aivazian, Demirguc-Kunt & Maksmivoc,

2001). The investor requires compensation for risk and if risk

diversification is not possible the cost of equity will increase (Clarkson,

Guedes & Thompson, 1996). The study contributes to literature by

examining the determinants identified in the west and applying them in

the developing market like Pakistan.

Related Literature and Hypothesis

The cost of capital is a blend of equity, preferred stock and debt

which constitutes capital structure. Cost of capital has been productive

and significant area of investigation in the field of finance (Da, Guo &

Jagannathan, 2009). Two basic components which constitute cost of

equity are dividend yield and capital gains; dividend yield may be

regarded more determinable than capital gains (Pointon & Omran, 2004).

Pecking order theory reveals that initially firm uses internally generated

funds if not possible then, debt is used which leads to high leverage

(Drobetz & Fix, 2003). Capital structure cause major impact on cost of

equity cost (Modigliani & Miller, 1958). Static Trade off Theory

emphasis that, firm sets specific targets for debt to value the firm

(Mayers & Majluf, 1984). Signaling Theory by Ross (1977) shows that

debt gives signals in the market about positive inflows.

528

country to country and culture to culture. Therefore the current study is

an attempt to fill this gap aligned with the Pecking order Proposition.

Out of many objectives of corporate finance managers one is the

maximization of the shareholders’ wealth. The conventional measure of

maximize of the shareholders wealth by increasing net income of the

business is not a viable approach. The study of suggests that there is

linear association between wealth maximization and cost of capital

(Bhatnagar, Kumari & Sharma, 2015). However, the said objective could

be achieved by lowering the cost of capital. We conducted this study in

different industrial sectors of Pakistan, Thus Pakistani industry provided

a natural laboratory for verifying the impact of different variables

identified as determinants of firms’ cost of equity. Several studies

suggest several determinants of cost equity. In particular we examine

how net earnings growth, retention of funds, times interest earned,

gearing, fixed asset backing, long term debt, tax, and market

capitalization may be helpful in determining the cost of equity.

Earning is a determinant of cost of equity (Fama & French,

1998). Growth in earnings stimulates the expectations of the shareholders

which increase cost of equity

(Bilal, Khan and Akoorie, 2016). Times interest earned is another

determinant of equity. Greater interest coverage ratio reduces financial

risk and cost of equity as well (Horne & Wachowicz, 1998). Debt

financing will increase the financial risk and ultimately increases the

expected return of the equity holder (Change & Rhee, 1990). Short term

financing is on higher side as compared to long term financing in

emerging markets (Booth, Aivazian, Demirguc-Kunt & Maksmivoc,

2001). The investor requires compensation for risk and if risk

diversification is not possible the cost of equity will increase (Clarkson,

Guedes & Thompson, 1996). The study contributes to literature by

examining the determinants identified in the west and applying them in

the developing market like Pakistan.

Related Literature and Hypothesis

The cost of capital is a blend of equity, preferred stock and debt

which constitutes capital structure. Cost of capital has been productive

and significant area of investigation in the field of finance (Da, Guo &

Jagannathan, 2009). Two basic components which constitute cost of

equity are dividend yield and capital gains; dividend yield may be

regarded more determinable than capital gains (Pointon & Omran, 2004).

Pecking order theory reveals that initially firm uses internally generated

funds if not possible then, debt is used which leads to high leverage

(Drobetz & Fix, 2003). Capital structure cause major impact on cost of

equity cost (Modigliani & Miller, 1958). Static Trade off Theory

emphasis that, firm sets specific targets for debt to value the firm

(Mayers & Majluf, 1984). Signaling Theory by Ross (1977) shows that

debt gives signals in the market about positive inflows.

Abasyn Journal of Social Sciences – Volume 9 – Issue 2

529

Net Earnings’ Growth and Cost of Equity

Net earnings’ growth and cost of equity have strong correlation.

According to Bazley and Hancock (2004), Equity investor’s assume all

risks and is ultimately entitled for the rewards. In the same vein, growth

in earnings will lead to high cost of equity (Fama & French, 1998).

Earnings’ has vital importance for the shareholders (Gibson, 1998).

Public disclosure regarding earnings has association with the cost of the

capital (botosan, plumlee & Xie, 2004). Country level disclosure has an

impact on realized returns and cost of capital (Core, Hail & Verdi, 2015).

It is further argued that increase in profits will increase the market price

of the shares which will result in capital gain and hence will increase the

cost of equity (Gibson, 1998). Companies with high growth opportunities

have generally high price earnings ratio and companies with low growth

opportunities have low price earnings ratio (Gibson, 1998). Based on the

argument our first hypothesis can be stated as follows:

H 1: Net earnings’ growth and cost of equity are positively correlated.

Retention of Funds and Cost of Equity

The debate about the preferred mode of financing needs a special

consideration with respect to Pakistan. The overall trend in the selection

of modes of financing moves in the following way that retained earnings

is preferred source of financing over the equity. If debt financing and

equity financing are compared debt finance is also preferred over the

equity. The better disclosure information to the users of financial

statements has association with stock prices which effects cost of capital

(Gelb & Zarowin, 2002). The specific reason is being aligned with the

pecking order proposition that the equity cost will be reduced as internal

funds should avoid issue costs (Krishnan & Mayer, 1996; Mayers, 1984).

Therefore the study hypothesizes that:

H 2: Retention of funds has negative impact on cost of equity.

Times Interest Earned and Cost of Equity

The ability of the firm to carry debt can be viewed by

considering the interest earned and fixed charges coverage (Gibson,

1998). Gibson further argues that if the time interest earned is

inadequate, firms will not be able to meet their interest obligations.

Failure to meet interest obligation can results in legal action and

bankruptcy (Brigham & Ehrhardt, 2002). Greater interest coverage

reduces financial risk. Investors demand high return for the high risk.

Therefore growth in earnings leads to greater interest coverage ratio

which lowers the risk and ultimately negatively impact cost of equity.

The higher ratio shows, that company can cover its interest payments and

the capacity to take new debts (Horne & Wachowicz, 1998). Based on

this view, the study hypothesizes that:

H 3: Times interest earned has negatively impact on cost of equity.

529

Net Earnings’ Growth and Cost of Equity

Net earnings’ growth and cost of equity have strong correlation.

According to Bazley and Hancock (2004), Equity investor’s assume all

risks and is ultimately entitled for the rewards. In the same vein, growth

in earnings will lead to high cost of equity (Fama & French, 1998).

Earnings’ has vital importance for the shareholders (Gibson, 1998).

Public disclosure regarding earnings has association with the cost of the

capital (botosan, plumlee & Xie, 2004). Country level disclosure has an

impact on realized returns and cost of capital (Core, Hail & Verdi, 2015).

It is further argued that increase in profits will increase the market price

of the shares which will result in capital gain and hence will increase the

cost of equity (Gibson, 1998). Companies with high growth opportunities

have generally high price earnings ratio and companies with low growth

opportunities have low price earnings ratio (Gibson, 1998). Based on the

argument our first hypothesis can be stated as follows:

H 1: Net earnings’ growth and cost of equity are positively correlated.

Retention of Funds and Cost of Equity

The debate about the preferred mode of financing needs a special

consideration with respect to Pakistan. The overall trend in the selection

of modes of financing moves in the following way that retained earnings

is preferred source of financing over the equity. If debt financing and

equity financing are compared debt finance is also preferred over the

equity. The better disclosure information to the users of financial

statements has association with stock prices which effects cost of capital

(Gelb & Zarowin, 2002). The specific reason is being aligned with the

pecking order proposition that the equity cost will be reduced as internal

funds should avoid issue costs (Krishnan & Mayer, 1996; Mayers, 1984).

Therefore the study hypothesizes that:

H 2: Retention of funds has negative impact on cost of equity.

Times Interest Earned and Cost of Equity

The ability of the firm to carry debt can be viewed by

considering the interest earned and fixed charges coverage (Gibson,

1998). Gibson further argues that if the time interest earned is

inadequate, firms will not be able to meet their interest obligations.

Failure to meet interest obligation can results in legal action and

bankruptcy (Brigham & Ehrhardt, 2002). Greater interest coverage

reduces financial risk. Investors demand high return for the high risk.

Therefore growth in earnings leads to greater interest coverage ratio

which lowers the risk and ultimately negatively impact cost of equity.

The higher ratio shows, that company can cover its interest payments and

the capacity to take new debts (Horne & Wachowicz, 1998). Based on

this view, the study hypothesizes that:

H 3: Times interest earned has negatively impact on cost of equity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Abasyn Journal of Social Sciences – Volume 9 – Issue 2

530

Gearing and Cost of Equity

The use of fixed operating costs by the firm is called financial

leverage or gearing (Horne & Wachowicz, 1998). Gearing presents the

ratio of total liabilities to equity also known as capital structure ratio. The

capital structure depicts the long term solvency of the firms (Khan &

Jain, 1993). There is a strong link between gearing and cost of equity

(Change & Rhee, 1990). High dividend payout ratio leads towards

higher debt financing (Change & Rhee, 1990). Debt financing will

increase the financial risk and will increase the expected return of the

equity holder. They will demand higher return for assuming high risk and

therefore cost of equity will increase. In developing countries use of

short term financing is on higher side than the long term financing

(Booth, Aivazian, Demirguc-Kunt & Maksmivoc, 2001). This leads us to

formulate the hypothesis that:

H 4: Gearing has positive impact on cost of equity.

Fixed Assets Backing and Cost of Equity

Fixed Assets backing allows the firms to raise debts at cheaper

rates (Rafiq, Iqbal, & Atiq, 2008). They further argued that companies

can pledge their assets which are fully depreciated but still have market

value. Total assets have a negative relation to the cost of equity. The

cost of equity will reduce due to increase in fixed assets. As asset

backing may make the business more secure and hence reduce the cost of

capital. In the same vein, investor requires compensation for the higher

risk if the risk cannot be diversified away due to which cost of equity

will increase (Clarkson, Guedes & Thompson, 1996). Fixed asset

backing makes the business less risky and hence the expected rate of

return of shareholder decreases. The higher ratio of tangible assets allows

the companies to borrow more at relatively cheaper rates (Rafiq, Iqbal, &

Atiq, 2008). Firm with large amount of fixed assets can borrow at lower

rates as compare to others because of fixed assets backing (Shah &

Hijazi, 2004). They further documents that fixed asset backing make

business secure and hence reduce the cost of equity. Therefore the

hypothesize that:

H 5: Fixed asset backing has negative impact on cost of equity.

Long Term Debt and Cost of Equity

The use of long term debt significantly impact earnings (Gibson,

1998). Gibson further argues that financial leverage is successful if firms

earn more than it pays on borrowed funds. When the capital structure of

any firm is low geared the preference shareholders and debenture holders

enjoy greater degree of security (Nizam, 1999). He further documents

that burden of interest payable impacts on equity earnings. Even there is

positive effect of disclosure policy on cost of debt (Nikolaev & Vanlent,

530

Gearing and Cost of Equity

The use of fixed operating costs by the firm is called financial

leverage or gearing (Horne & Wachowicz, 1998). Gearing presents the

ratio of total liabilities to equity also known as capital structure ratio. The

capital structure depicts the long term solvency of the firms (Khan &

Jain, 1993). There is a strong link between gearing and cost of equity

(Change & Rhee, 1990). High dividend payout ratio leads towards

higher debt financing (Change & Rhee, 1990). Debt financing will

increase the financial risk and will increase the expected return of the

equity holder. They will demand higher return for assuming high risk and

therefore cost of equity will increase. In developing countries use of

short term financing is on higher side than the long term financing

(Booth, Aivazian, Demirguc-Kunt & Maksmivoc, 2001). This leads us to

formulate the hypothesis that:

H 4: Gearing has positive impact on cost of equity.

Fixed Assets Backing and Cost of Equity

Fixed Assets backing allows the firms to raise debts at cheaper

rates (Rafiq, Iqbal, & Atiq, 2008). They further argued that companies

can pledge their assets which are fully depreciated but still have market

value. Total assets have a negative relation to the cost of equity. The

cost of equity will reduce due to increase in fixed assets. As asset

backing may make the business more secure and hence reduce the cost of

capital. In the same vein, investor requires compensation for the higher

risk if the risk cannot be diversified away due to which cost of equity

will increase (Clarkson, Guedes & Thompson, 1996). Fixed asset

backing makes the business less risky and hence the expected rate of

return of shareholder decreases. The higher ratio of tangible assets allows

the companies to borrow more at relatively cheaper rates (Rafiq, Iqbal, &

Atiq, 2008). Firm with large amount of fixed assets can borrow at lower

rates as compare to others because of fixed assets backing (Shah &

Hijazi, 2004). They further documents that fixed asset backing make

business secure and hence reduce the cost of equity. Therefore the

hypothesize that:

H 5: Fixed asset backing has negative impact on cost of equity.

Long Term Debt and Cost of Equity

The use of long term debt significantly impact earnings (Gibson,

1998). Gibson further argues that financial leverage is successful if firms

earn more than it pays on borrowed funds. When the capital structure of

any firm is low geared the preference shareholders and debenture holders

enjoy greater degree of security (Nizam, 1999). He further documents

that burden of interest payable impacts on equity earnings. Even there is

positive effect of disclosure policy on cost of debt (Nikolaev & Vanlent,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abasyn Journal of Social Sciences – Volume 9 – Issue 2

531

2005). Increase in long term debt, increases financial risk and all the

risks have to be borne by the equity holder. Their expected return

increases with the increase in risk. The volatility of profits will increase

the debt (Lawrence, 1990). Therefore the expected return of the equity

holders increases. On the bases of above arguments it is hypothesize that:

H 6: Increase in the long term debt positively impact cost of equity.

Tax and Cost of Equity

Tax is a form of cash outflow which ultimately reduces the

profitability. The reduction in cash flow reduces the return on the equity.

Therefore tax may have negative impact on cost of equity. In the same

vein voluntary disclosure of firms in the financial statements leads to

lower cost of capital as compare to the firms that do not disclose

(Cheynel, 2013). Firm characteristics and disclosure practices decrease

cost of capital (Chen, Dhaliwal & Xie, 2010). Interest on debt also

creates cash inflow impact due to tax shield on interest. This

phenomenon also confirms with the concept of (Modigliani & Miller,

1963) that tax reduces return to shareholders and also the cost of debt

may be reduced as tax is treated as expense and deducted from the

income. Uncertainty regarding future cash flows distribution creates

uncertainty among investors, who require higher return for higher

information risk (Paugam & Ramond, 2015). Therefore, the study

hypothesizes that:

H 7: Tax may have negative impact on cost of equity.

Market Capitalization and Cost of Equity

Market capitalization increases the value of the firm due to

which cost of equity decreases. Stock market capitalization can be

calculated as number of shares multiplied by market price per share. A

lot of capital comes in but it is suggested that when funds depart, it

departs more rapidly than it came in (Bekaert, Harvey & Lumsdaine,

2002). In the same vein market capitalization and corporate social

responsibility move in the same direction. Hence corporate social

responsibility reduces earnings forecasts, volatility of returns and cost of

capital (Maretno, Harjoto & Jo, 2015). Bekaert, Harvey and Lumsdaine,

(2002) further argued that initially inflows in equity increase the return

on equity, later this effect decreases over time, which reduces the cost of

equity. To investigate relationship between market capitalization and the

cost of equity, the following hypothesis has been formulated:

H 8: Market capitalization has a negative impact on cost of equity.

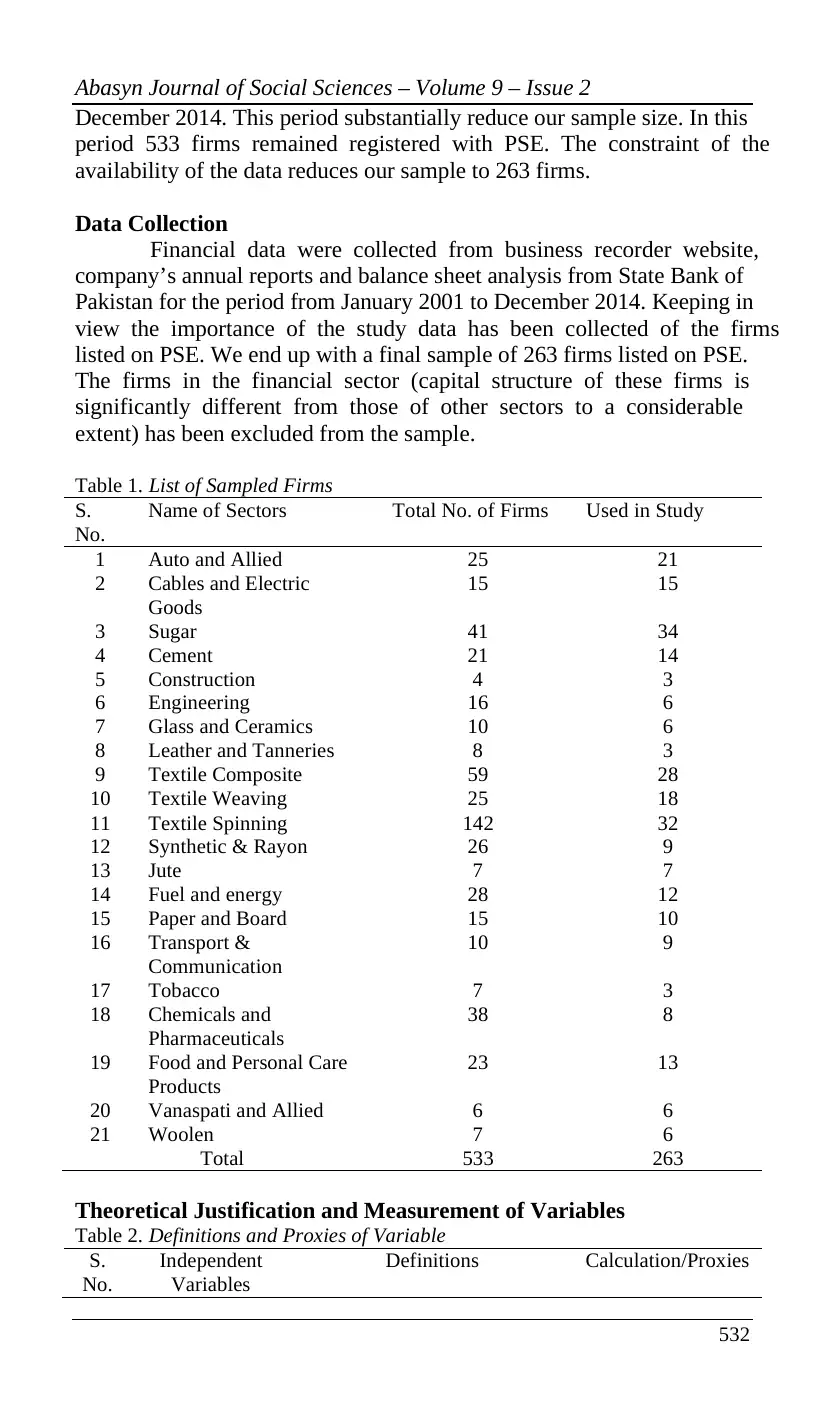

Research Methodology

Sample

Our sample consists of firms that are listed on Pakistan Stock

Exchange (PSE). We begin our sample period from January 2009 to

531

2005). Increase in long term debt, increases financial risk and all the

risks have to be borne by the equity holder. Their expected return

increases with the increase in risk. The volatility of profits will increase

the debt (Lawrence, 1990). Therefore the expected return of the equity

holders increases. On the bases of above arguments it is hypothesize that:

H 6: Increase in the long term debt positively impact cost of equity.

Tax and Cost of Equity

Tax is a form of cash outflow which ultimately reduces the

profitability. The reduction in cash flow reduces the return on the equity.

Therefore tax may have negative impact on cost of equity. In the same

vein voluntary disclosure of firms in the financial statements leads to

lower cost of capital as compare to the firms that do not disclose

(Cheynel, 2013). Firm characteristics and disclosure practices decrease

cost of capital (Chen, Dhaliwal & Xie, 2010). Interest on debt also

creates cash inflow impact due to tax shield on interest. This

phenomenon also confirms with the concept of (Modigliani & Miller,

1963) that tax reduces return to shareholders and also the cost of debt

may be reduced as tax is treated as expense and deducted from the

income. Uncertainty regarding future cash flows distribution creates

uncertainty among investors, who require higher return for higher

information risk (Paugam & Ramond, 2015). Therefore, the study

hypothesizes that:

H 7: Tax may have negative impact on cost of equity.

Market Capitalization and Cost of Equity

Market capitalization increases the value of the firm due to

which cost of equity decreases. Stock market capitalization can be

calculated as number of shares multiplied by market price per share. A

lot of capital comes in but it is suggested that when funds depart, it

departs more rapidly than it came in (Bekaert, Harvey & Lumsdaine,

2002). In the same vein market capitalization and corporate social

responsibility move in the same direction. Hence corporate social

responsibility reduces earnings forecasts, volatility of returns and cost of

capital (Maretno, Harjoto & Jo, 2015). Bekaert, Harvey and Lumsdaine,

(2002) further argued that initially inflows in equity increase the return

on equity, later this effect decreases over time, which reduces the cost of

equity. To investigate relationship between market capitalization and the

cost of equity, the following hypothesis has been formulated:

H 8: Market capitalization has a negative impact on cost of equity.

Research Methodology

Sample

Our sample consists of firms that are listed on Pakistan Stock

Exchange (PSE). We begin our sample period from January 2009 to

Abasyn Journal of Social Sciences – Volume 9 – Issue 2

532

December 2014. This period substantially reduce our sample size. In this

period 533 firms remained registered with PSE. The constraint of the

availability of the data reduces our sample to 263 firms.

Data Collection

Financial data were collected from business recorder website,

company’s annual reports and balance sheet analysis from State Bank of

Pakistan for the period from January 2001 to December 2014. Keeping in

view the importance of the study data has been collected of the firms

listed on PSE. We end up with a final sample of 263 firms listed on PSE.

The firms in the financial sector (capital structure of these firms is

significantly different from those of other sectors to a considerable

extent) has been excluded from the sample.

Table 1. List of Sampled Firms

S.

No.

Name of Sectors Total No. of Firms Used in Study

1 Auto and Allied 25 21

2 Cables and Electric

Goods

15 15

3 Sugar 41 34

4 Cement 21 14

5 Construction 4 3

6 Engineering 16 6

7 Glass and Ceramics 10 6

8 Leather and Tanneries 8 3

9 Textile Composite 59 28

10 Textile Weaving 25 18

11 Textile Spinning 142 32

12 Synthetic & Rayon 26 9

13 Jute 7 7

14 Fuel and energy 28 12

15 Paper and Board 15 10

16 Transport &

Communication

10 9

17 Tobacco 7 3

18 Chemicals and

Pharmaceuticals

38 8

19 Food and Personal Care

Products

23 13

20 Vanaspati and Allied 6 6

21 Woolen 7 6

Total 533 263

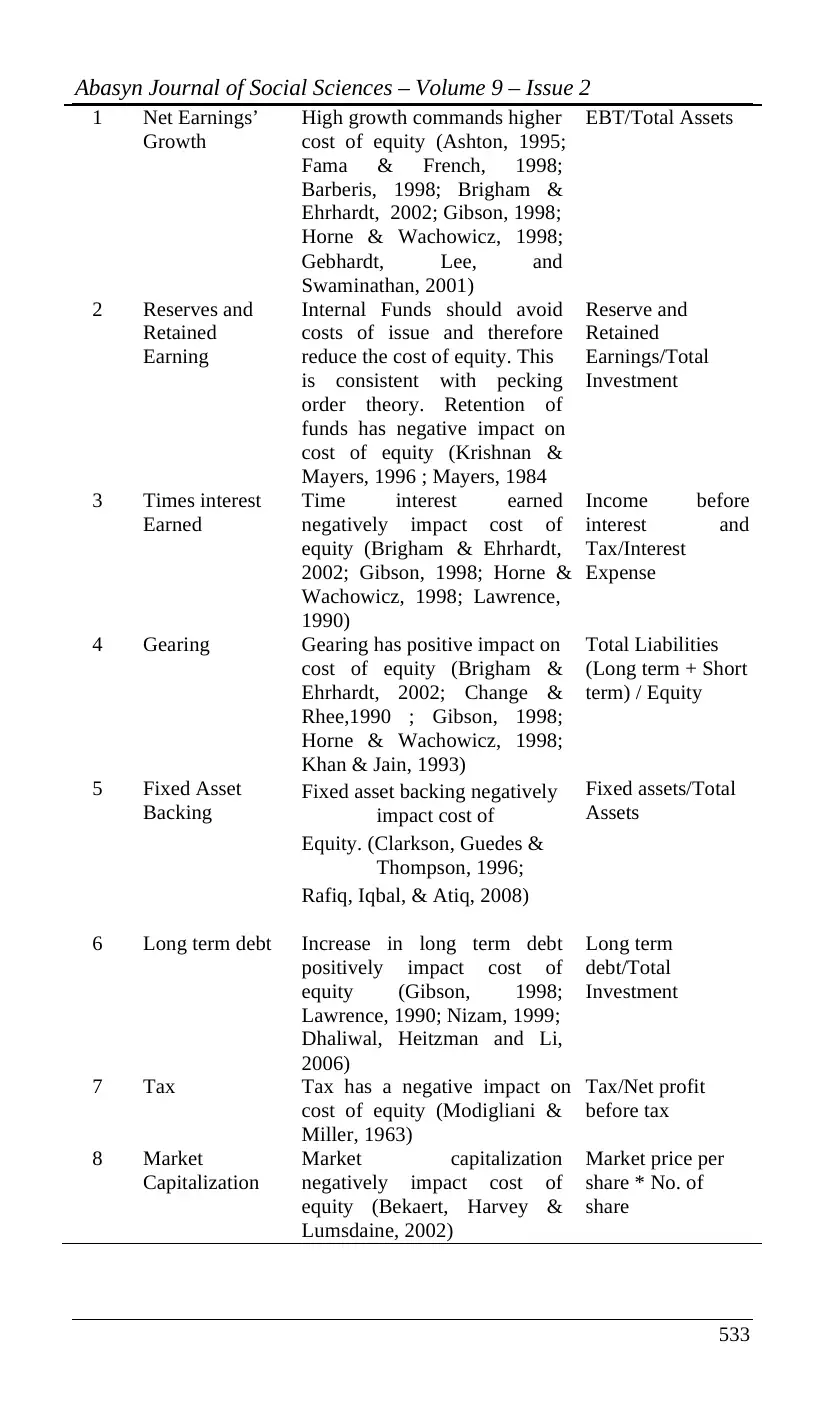

Theoretical Justification and Measurement of Variables

Table 2. Definitions and Proxies of Variable

S.

No.

Independent

Variables

Definitions Calculation/Proxies

532

December 2014. This period substantially reduce our sample size. In this

period 533 firms remained registered with PSE. The constraint of the

availability of the data reduces our sample to 263 firms.

Data Collection

Financial data were collected from business recorder website,

company’s annual reports and balance sheet analysis from State Bank of

Pakistan for the period from January 2001 to December 2014. Keeping in

view the importance of the study data has been collected of the firms

listed on PSE. We end up with a final sample of 263 firms listed on PSE.

The firms in the financial sector (capital structure of these firms is

significantly different from those of other sectors to a considerable

extent) has been excluded from the sample.

Table 1. List of Sampled Firms

S.

No.

Name of Sectors Total No. of Firms Used in Study

1 Auto and Allied 25 21

2 Cables and Electric

Goods

15 15

3 Sugar 41 34

4 Cement 21 14

5 Construction 4 3

6 Engineering 16 6

7 Glass and Ceramics 10 6

8 Leather and Tanneries 8 3

9 Textile Composite 59 28

10 Textile Weaving 25 18

11 Textile Spinning 142 32

12 Synthetic & Rayon 26 9

13 Jute 7 7

14 Fuel and energy 28 12

15 Paper and Board 15 10

16 Transport &

Communication

10 9

17 Tobacco 7 3

18 Chemicals and

Pharmaceuticals

38 8

19 Food and Personal Care

Products

23 13

20 Vanaspati and Allied 6 6

21 Woolen 7 6

Total 533 263

Theoretical Justification and Measurement of Variables

Table 2. Definitions and Proxies of Variable

S.

No.

Independent

Variables

Definitions Calculation/Proxies

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Abasyn Journal of Social Sciences – Volume 9 – Issue 2

533

1 Net Earnings’

Growth

High growth commands higher

cost of equity (Ashton, 1995;

Fama & French, 1998;

Barberis, 1998; Brigham &

Ehrhardt, 2002; Gibson, 1998;

Horne & Wachowicz, 1998;

Gebhardt, Lee, and

Swaminathan, 2001)

EBT/Total Assets

2 Reserves and

Retained

Earning

Internal Funds should avoid

costs of issue and therefore

reduce the cost of equity. This

is consistent with pecking

order theory. Retention of

funds has negative impact on

cost of equity (Krishnan &

Mayers, 1996 ; Mayers, 1984

Reserve and

Retained

Earnings/Total

Investment

3 Times interest

Earned

Time interest earned

negatively impact cost of

equity (Brigham & Ehrhardt,

2002; Gibson, 1998; Horne &

Wachowicz, 1998; Lawrence,

1990)

Income before

interest and

Tax/Interest

Expense

4 Gearing Gearing has positive impact on

cost of equity (Brigham &

Ehrhardt, 2002; Change &

Rhee,1990 ; Gibson, 1998;

Horne & Wachowicz, 1998;

Khan & Jain, 1993)

Total Liabilities

(Long term + Short

term) / Equity

5 Fixed Asset

Backing Fixed asset backing negatively

impact cost of

Equity. (Clarkson, Guedes &

Thompson, 1996;

Rafiq, Iqbal, & Atiq, 2008)

Fixed assets/Total

Assets

6 Long term debt Increase in long term debt

positively impact cost of

equity (Gibson, 1998;

Lawrence, 1990; Nizam, 1999;

Dhaliwal, Heitzman and Li,

2006)

Long term

debt/Total

Investment

7 Tax Tax has a negative impact on

cost of equity (Modigliani &

Miller, 1963)

Tax/Net profit

before tax

8 Market

Capitalization

Market capitalization

negatively impact cost of

equity (Bekaert, Harvey &

Lumsdaine, 2002)

Market price per

share * No. of

share

533

1 Net Earnings’

Growth

High growth commands higher

cost of equity (Ashton, 1995;

Fama & French, 1998;

Barberis, 1998; Brigham &

Ehrhardt, 2002; Gibson, 1998;

Horne & Wachowicz, 1998;

Gebhardt, Lee, and

Swaminathan, 2001)

EBT/Total Assets

2 Reserves and

Retained

Earning

Internal Funds should avoid

costs of issue and therefore

reduce the cost of equity. This

is consistent with pecking

order theory. Retention of

funds has negative impact on

cost of equity (Krishnan &

Mayers, 1996 ; Mayers, 1984

Reserve and

Retained

Earnings/Total

Investment

3 Times interest

Earned

Time interest earned

negatively impact cost of

equity (Brigham & Ehrhardt,

2002; Gibson, 1998; Horne &

Wachowicz, 1998; Lawrence,

1990)

Income before

interest and

Tax/Interest

Expense

4 Gearing Gearing has positive impact on

cost of equity (Brigham &

Ehrhardt, 2002; Change &

Rhee,1990 ; Gibson, 1998;

Horne & Wachowicz, 1998;

Khan & Jain, 1993)

Total Liabilities

(Long term + Short

term) / Equity

5 Fixed Asset

Backing Fixed asset backing negatively

impact cost of

Equity. (Clarkson, Guedes &

Thompson, 1996;

Rafiq, Iqbal, & Atiq, 2008)

Fixed assets/Total

Assets

6 Long term debt Increase in long term debt

positively impact cost of

equity (Gibson, 1998;

Lawrence, 1990; Nizam, 1999;

Dhaliwal, Heitzman and Li,

2006)

Long term

debt/Total

Investment

7 Tax Tax has a negative impact on

cost of equity (Modigliani &

Miller, 1963)

Tax/Net profit

before tax

8 Market

Capitalization

Market capitalization

negatively impact cost of

equity (Bekaert, Harvey &

Lumsdaine, 2002)

Market price per

share * No. of

share

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abasyn Journal of Social Sciences – Volume 9 – Issue 2

534

Measures, Data Analysis & Results

Cost of Equity Estimates

Our measure for cost of equity was Capital Asset Pricing Model

(CAPM). However there is strong debate about the appropriateness of

the method to calculate cost of equity. In the same vein Nasr, Boubakri

and Cosset (2012), states that there is no strong consensus on the method

to calculate cost of equity. CAPM was developed by Nobel Laureate

William Sharpe’s in 1960s. Other methods are also available to capture

market behavior, but the advantage with the CAPM is that it is simple

has real world applicability (Horne & Wachowicz, 1998). CAPM

provides reality and allows illustrating certain implications about risk. It

is significant for practical applications and plays major role in the field of

cost of equity. CAPM was the first model developed by the financial

theorists (Graham & Harvey, 2001). To calculate the cost of equity about

75% of finance professors support using the CAPM (Welch, 2008). A

survey of CFOs was conducted and it indicates that 73.5% of responding

financial executives uses CAPM (Graham & Harvey, 2001). CAPM, has

also been tested by Shah and Butt in 2009 to calculate cost of equity. The

CAPM is extremely appealing model at an intellectual level, it is logical

and rational. Once someone understands and works with CAPM his

reaction is usually to accept it without question (Brigham & Ehrhardt,

2002). A survey conducted by Bruner, Eades, Harris and Higgins, (1998)

found that the CAPM is commonly preferred by the practitioners.

Therefore the current study used CAPM to estimate cost of equity in line

with (Shah & Butt, 2009).

The Regression Model

Panel regression analysis has been used which is in line with

(Hall, Hutchinson & Michaelas, 2004, Rafiq, Iqbal & Atiq, 2004; Shah &

Hijazi, 2004).

Keit = β 0 + β 1 (NEGit) + β 2 (RFit) + β 3 (TIEit) + β 4 (GRit) +β5 (FAit) +β6

(LDit) +β7 (TXit) + β8 (MCit) +e

Where:

Ke = Cost of equity,

NEG = Net Earnings Growth

RF = Retention of Funds

TIE = Times Interest Earned

GR = Gearing

FA = Fixed Asset Backing

LD = Long term debt

T = Tax

MC= Market Capitalization

534

Measures, Data Analysis & Results

Cost of Equity Estimates

Our measure for cost of equity was Capital Asset Pricing Model

(CAPM). However there is strong debate about the appropriateness of

the method to calculate cost of equity. In the same vein Nasr, Boubakri

and Cosset (2012), states that there is no strong consensus on the method

to calculate cost of equity. CAPM was developed by Nobel Laureate

William Sharpe’s in 1960s. Other methods are also available to capture

market behavior, but the advantage with the CAPM is that it is simple

has real world applicability (Horne & Wachowicz, 1998). CAPM

provides reality and allows illustrating certain implications about risk. It

is significant for practical applications and plays major role in the field of

cost of equity. CAPM was the first model developed by the financial

theorists (Graham & Harvey, 2001). To calculate the cost of equity about

75% of finance professors support using the CAPM (Welch, 2008). A

survey of CFOs was conducted and it indicates that 73.5% of responding

financial executives uses CAPM (Graham & Harvey, 2001). CAPM, has

also been tested by Shah and Butt in 2009 to calculate cost of equity. The

CAPM is extremely appealing model at an intellectual level, it is logical

and rational. Once someone understands and works with CAPM his

reaction is usually to accept it without question (Brigham & Ehrhardt,

2002). A survey conducted by Bruner, Eades, Harris and Higgins, (1998)

found that the CAPM is commonly preferred by the practitioners.

Therefore the current study used CAPM to estimate cost of equity in line

with (Shah & Butt, 2009).

The Regression Model

Panel regression analysis has been used which is in line with

(Hall, Hutchinson & Michaelas, 2004, Rafiq, Iqbal & Atiq, 2004; Shah &

Hijazi, 2004).

Keit = β 0 + β 1 (NEGit) + β 2 (RFit) + β 3 (TIEit) + β 4 (GRit) +β5 (FAit) +β6

(LDit) +β7 (TXit) + β8 (MCit) +e

Where:

Ke = Cost of equity,

NEG = Net Earnings Growth

RF = Retention of Funds

TIE = Times Interest Earned

GR = Gearing

FA = Fixed Asset Backing

LD = Long term debt

T = Tax

MC= Market Capitalization

Abasyn Journal of Social Sciences – Volume 9 – Issue 2

535

e = Error term

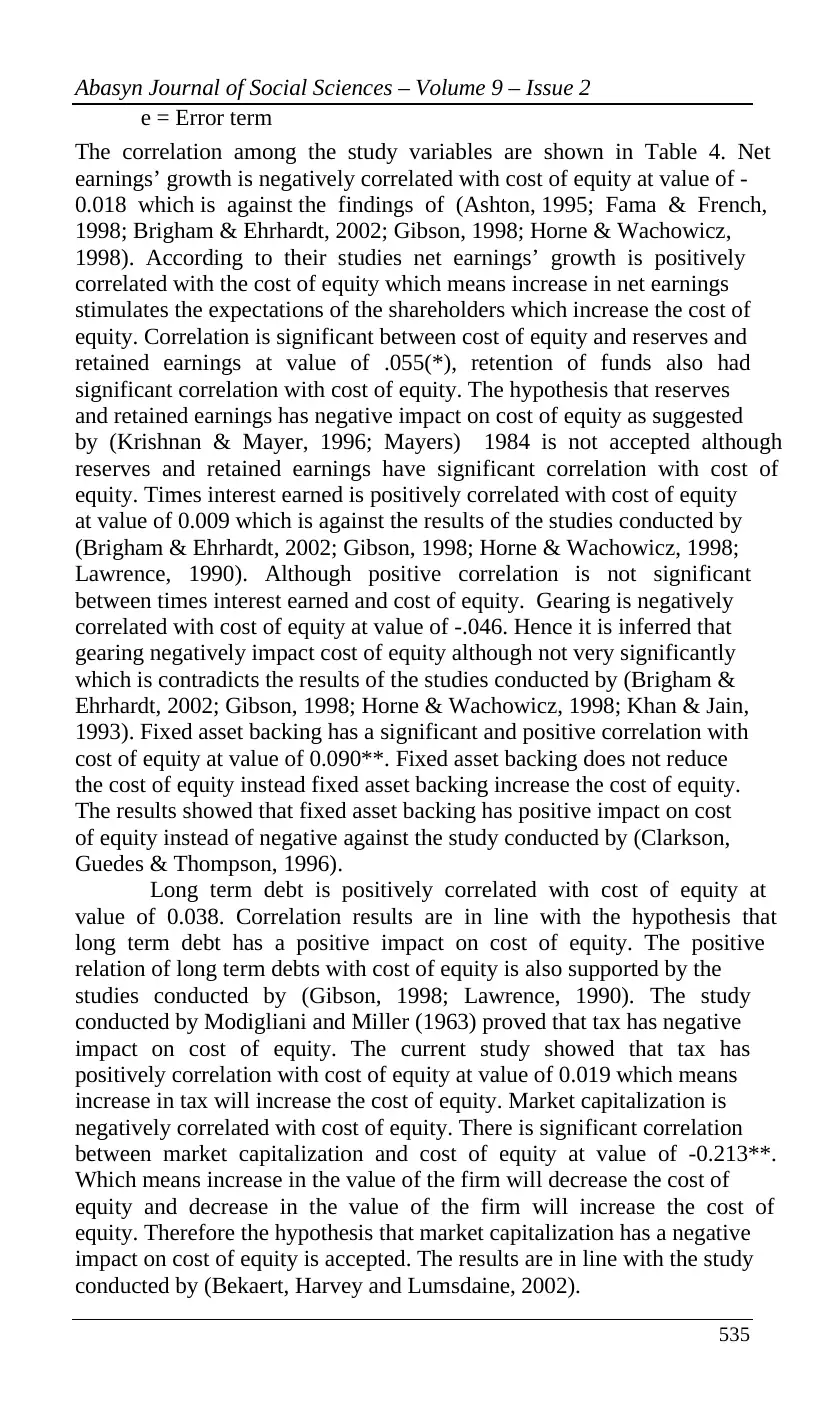

The correlation among the study variables are shown in Table 4. Net

earnings’ growth is negatively correlated with cost of equity at value of -

0.018 which is against the findings of (Ashton, 1995; Fama & French,

1998; Brigham & Ehrhardt, 2002; Gibson, 1998; Horne & Wachowicz,

1998). According to their studies net earnings’ growth is positively

correlated with the cost of equity which means increase in net earnings

stimulates the expectations of the shareholders which increase the cost of

equity. Correlation is significant between cost of equity and reserves and

retained earnings at value of .055(*), retention of funds also had

significant correlation with cost of equity. The hypothesis that reserves

and retained earnings has negative impact on cost of equity as suggested

by (Krishnan & Mayer, 1996; Mayers) 1984 is not accepted although

reserves and retained earnings have significant correlation with cost of

equity. Times interest earned is positively correlated with cost of equity

at value of 0.009 which is against the results of the studies conducted by

(Brigham & Ehrhardt, 2002; Gibson, 1998; Horne & Wachowicz, 1998;

Lawrence, 1990). Although positive correlation is not significant

between times interest earned and cost of equity. Gearing is negatively

correlated with cost of equity at value of -.046. Hence it is inferred that

gearing negatively impact cost of equity although not very significantly

which is contradicts the results of the studies conducted by (Brigham &

Ehrhardt, 2002; Gibson, 1998; Horne & Wachowicz, 1998; Khan & Jain,

1993). Fixed asset backing has a significant and positive correlation with

cost of equity at value of 0.090**. Fixed asset backing does not reduce

the cost of equity instead fixed asset backing increase the cost of equity.

The results showed that fixed asset backing has positive impact on cost

of equity instead of negative against the study conducted by (Clarkson,

Guedes & Thompson, 1996).

Long term debt is positively correlated with cost of equity at

value of 0.038. Correlation results are in line with the hypothesis that

long term debt has a positive impact on cost of equity. The positive

relation of long term debts with cost of equity is also supported by the

studies conducted by (Gibson, 1998; Lawrence, 1990). The study

conducted by Modigliani and Miller (1963) proved that tax has negative

impact on cost of equity. The current study showed that tax has

positively correlation with cost of equity at value of 0.019 which means

increase in tax will increase the cost of equity. Market capitalization is

negatively correlated with cost of equity. There is significant correlation

between market capitalization and cost of equity at value of -0.213**.

Which means increase in the value of the firm will decrease the cost of

equity and decrease in the value of the firm will increase the cost of

equity. Therefore the hypothesis that market capitalization has a negative

impact on cost of equity is accepted. The results are in line with the study

conducted by (Bekaert, Harvey and Lumsdaine, 2002).

535

e = Error term

The correlation among the study variables are shown in Table 4. Net

earnings’ growth is negatively correlated with cost of equity at value of -

0.018 which is against the findings of (Ashton, 1995; Fama & French,

1998; Brigham & Ehrhardt, 2002; Gibson, 1998; Horne & Wachowicz,

1998). According to their studies net earnings’ growth is positively

correlated with the cost of equity which means increase in net earnings

stimulates the expectations of the shareholders which increase the cost of

equity. Correlation is significant between cost of equity and reserves and

retained earnings at value of .055(*), retention of funds also had

significant correlation with cost of equity. The hypothesis that reserves

and retained earnings has negative impact on cost of equity as suggested

by (Krishnan & Mayer, 1996; Mayers) 1984 is not accepted although

reserves and retained earnings have significant correlation with cost of

equity. Times interest earned is positively correlated with cost of equity

at value of 0.009 which is against the results of the studies conducted by

(Brigham & Ehrhardt, 2002; Gibson, 1998; Horne & Wachowicz, 1998;

Lawrence, 1990). Although positive correlation is not significant

between times interest earned and cost of equity. Gearing is negatively

correlated with cost of equity at value of -.046. Hence it is inferred that

gearing negatively impact cost of equity although not very significantly

which is contradicts the results of the studies conducted by (Brigham &

Ehrhardt, 2002; Gibson, 1998; Horne & Wachowicz, 1998; Khan & Jain,

1993). Fixed asset backing has a significant and positive correlation with

cost of equity at value of 0.090**. Fixed asset backing does not reduce

the cost of equity instead fixed asset backing increase the cost of equity.

The results showed that fixed asset backing has positive impact on cost

of equity instead of negative against the study conducted by (Clarkson,

Guedes & Thompson, 1996).

Long term debt is positively correlated with cost of equity at

value of 0.038. Correlation results are in line with the hypothesis that

long term debt has a positive impact on cost of equity. The positive

relation of long term debts with cost of equity is also supported by the

studies conducted by (Gibson, 1998; Lawrence, 1990). The study

conducted by Modigliani and Miller (1963) proved that tax has negative

impact on cost of equity. The current study showed that tax has

positively correlation with cost of equity at value of 0.019 which means

increase in tax will increase the cost of equity. Market capitalization is

negatively correlated with cost of equity. There is significant correlation

between market capitalization and cost of equity at value of -0.213**.

Which means increase in the value of the firm will decrease the cost of

equity and decrease in the value of the firm will increase the cost of

equity. Therefore the hypothesis that market capitalization has a negative

impact on cost of equity is accepted. The results are in line with the study

conducted by (Bekaert, Harvey and Lumsdaine, 2002).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Abasyn Journal of Social Sciences – Volume 9 – Issue 2

536

Table 4. Correlation between Cost of Equity with Independent Variables

Ke NEG RRE NFA TIE G FAB L T MC

Ke 1

NEG -.018 1

RRE .055(*) .006 1

TIE .009 .123(**) .004 -.005 1

G -.046 -.003 -

.001 .006 -.001 1

FAB .090(**) -

.146(**)

-

.024 .005 -

.089(**)

-

.007 1

L .038 -.024 -

.026 -.001 -.039 -

.037 .191(**) 1

T .019 -.005 .004 .005 .002 -

.008 .018 -.006 1

MC -

.213(**) -.060(*) -

.039

-

.047(*) .158(**) -

.009

-

.254(**)

-

.167(**) .020 1

* Correlation is significant at the 0.05 level (1-tailed).

** Correlation is significant at the 0.01 level (1-tailed).

Table 3. Regression Model Summary

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .234(a) .055 .048 6.30603

a Predictors: (Constant), MC, G, T, RRE, NFA, NEG, L, TIE, FAB

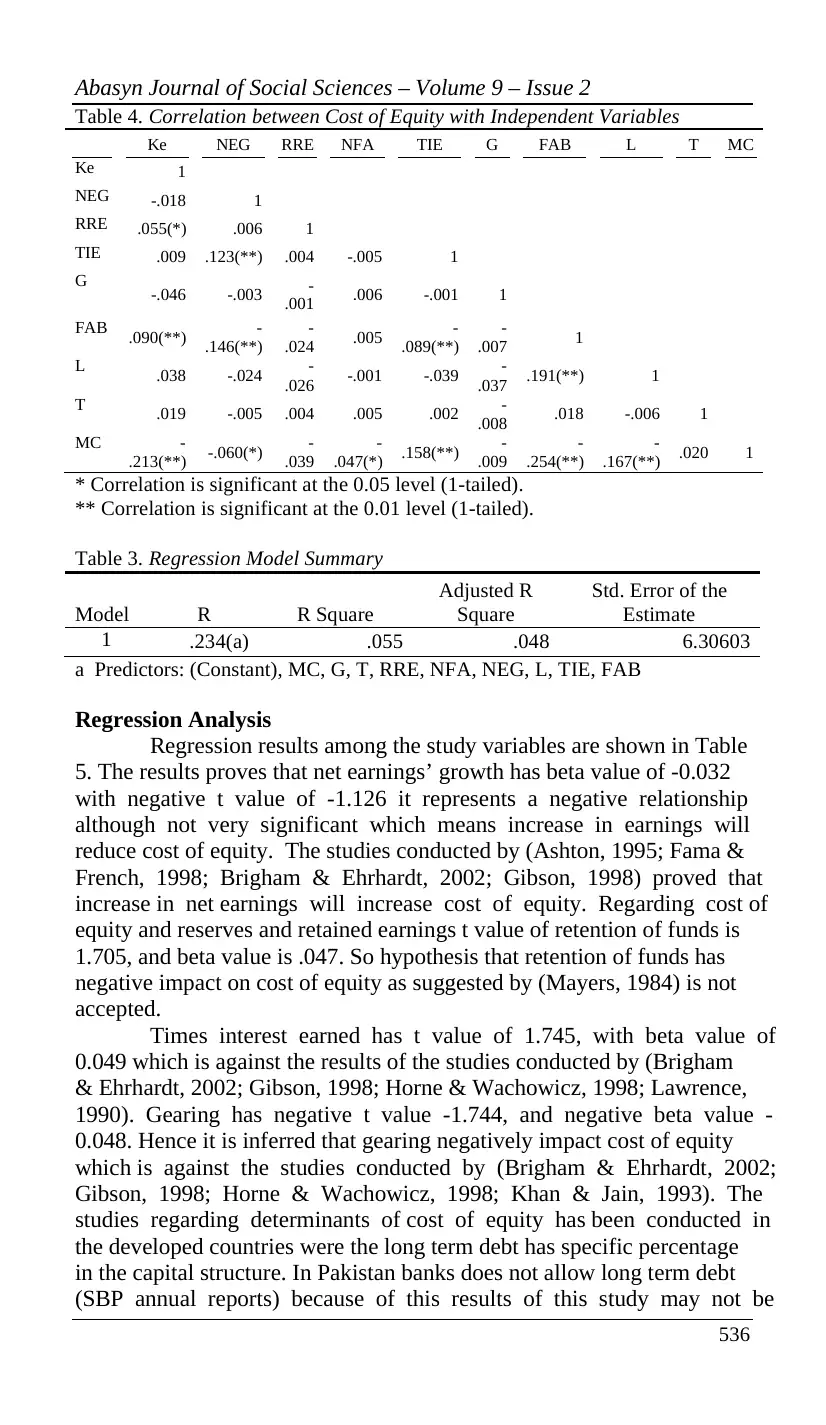

Regression Analysis

Regression results among the study variables are shown in Table

5. The results proves that net earnings’ growth has beta value of -0.032

with negative t value of -1.126 it represents a negative relationship

although not very significant which means increase in earnings will

reduce cost of equity. The studies conducted by (Ashton, 1995; Fama &

French, 1998; Brigham & Ehrhardt, 2002; Gibson, 1998) proved that

increase in net earnings will increase cost of equity. Regarding cost of

equity and reserves and retained earnings t value of retention of funds is

1.705, and beta value is .047. So hypothesis that retention of funds has

negative impact on cost of equity as suggested by (Mayers, 1984) is not

accepted.

Times interest earned has t value of 1.745, with beta value of

0.049 which is against the results of the studies conducted by (Brigham

& Ehrhardt, 2002; Gibson, 1998; Horne & Wachowicz, 1998; Lawrence,

1990). Gearing has negative t value -1.744, and negative beta value -

0.048. Hence it is inferred that gearing negatively impact cost of equity

which is against the studies conducted by (Brigham & Ehrhardt, 2002;

Gibson, 1998; Horne & Wachowicz, 1998; Khan & Jain, 1993). The

studies regarding determinants of cost of equity has been conducted in

the developed countries were the long term debt has specific percentage

in the capital structure. In Pakistan banks does not allow long term debt

(SBP annual reports) because of this results of this study may not be

536

Table 4. Correlation between Cost of Equity with Independent Variables

Ke NEG RRE NFA TIE G FAB L T MC

Ke 1

NEG -.018 1

RRE .055(*) .006 1

TIE .009 .123(**) .004 -.005 1

G -.046 -.003 -

.001 .006 -.001 1

FAB .090(**) -

.146(**)

-

.024 .005 -

.089(**)

-

.007 1

L .038 -.024 -

.026 -.001 -.039 -

.037 .191(**) 1

T .019 -.005 .004 .005 .002 -

.008 .018 -.006 1

MC -

.213(**) -.060(*) -

.039

-

.047(*) .158(**) -

.009

-

.254(**)

-

.167(**) .020 1

* Correlation is significant at the 0.05 level (1-tailed).

** Correlation is significant at the 0.01 level (1-tailed).

Table 3. Regression Model Summary

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .234(a) .055 .048 6.30603

a Predictors: (Constant), MC, G, T, RRE, NFA, NEG, L, TIE, FAB

Regression Analysis

Regression results among the study variables are shown in Table

5. The results proves that net earnings’ growth has beta value of -0.032

with negative t value of -1.126 it represents a negative relationship

although not very significant which means increase in earnings will

reduce cost of equity. The studies conducted by (Ashton, 1995; Fama &

French, 1998; Brigham & Ehrhardt, 2002; Gibson, 1998) proved that

increase in net earnings will increase cost of equity. Regarding cost of

equity and reserves and retained earnings t value of retention of funds is

1.705, and beta value is .047. So hypothesis that retention of funds has

negative impact on cost of equity as suggested by (Mayers, 1984) is not

accepted.

Times interest earned has t value of 1.745, with beta value of

0.049 which is against the results of the studies conducted by (Brigham

& Ehrhardt, 2002; Gibson, 1998; Horne & Wachowicz, 1998; Lawrence,

1990). Gearing has negative t value -1.744, and negative beta value -

0.048. Hence it is inferred that gearing negatively impact cost of equity

which is against the studies conducted by (Brigham & Ehrhardt, 2002;

Gibson, 1998; Horne & Wachowicz, 1998; Khan & Jain, 1993). The

studies regarding determinants of cost of equity has been conducted in

the developed countries were the long term debt has specific percentage

in the capital structure. In Pakistan banks does not allow long term debt

(SBP annual reports) because of this results of this study may not be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abasyn Journal of Social Sciences – Volume 9 – Issue 2

537

according to the results of the studies conducted in the developed

countries.

Fixed asset backing has t value of 1.274 and beta value of .037

therefore fixed asset backing has positive impact on cost of equity

instead of negative against the literature. Fixed assets are totally financed

by equity in Pakistan and in the developed countries they are also finance

by long term debts as well; this might be the reason for the results which

are against the results of the studies conducted by (Clarkson et al., 1996).

Long term debt has -.139 t values along with beta of -0.004. Tax has t

value of 0.786, and beta value is 0.022. Pakistan economy is

undocumented and therefore taxation system is mainly depend on proper

documentation (Faruqi, 2011), which might be the reason for the

differences in results with respect to the studies conducted in the

developed countries. Market capitalization has t value of -7.259, with

beta value of -0.212. Therefore, it is established that with the increase in

the value of the firm the cost of equity will be decreased and vice versa.

The results are in line with (Bekaert et al., 2002). Hypothesis that market

capitalization has a negative impact on cost of equity is accepted.

Table 5. Main Effect of IV’s on Cost of Equity

Dependent Variable

Cost of Equity

Independent Variables Coefficients t-statistics

Intercept 20.12995 12.446

Net Earnings’ Growth (NEG) -.032 -1.126

Reserves and Retained Earnings

(RRE) .047 1.705

Times Interest Earned (TIE) .049 1.745

Gearing (G) -.048 -1.744

Fixed Asset Backing (FAB) .037 1.274

Long Term Debt (LTD) -.004 -.139

Tax (T) .022 .786

Market Capitalization (MC) -.212 -7.259

R Square .055

Adjusted R Square .048

Industry Wise Cost of Equity

Cost of equity in different industries has been shown in Table 7.

Minimum cost of equity is in Auto and allied industry which is 11.54%

and highest in construction industry which is 16.78% in line with the

findings of (Pointon and Omran, 2004). Their study in Egypt also

reported high cost of equity in construction industry, same stands true

with respect to Pakistan. Cost of equity in cables & electric goods, sugar,

cement, glass& ceramics, textile composite, synthetic & Rayon, jute,

fuel & energy, paper & board, transport & communication, chemical &

pharmaceuticals, food & personal care products, vanaspati & allied and

woolen is ranging between 13.02% to 13.94. In tobacco industry cost of

537

according to the results of the studies conducted in the developed

countries.

Fixed asset backing has t value of 1.274 and beta value of .037

therefore fixed asset backing has positive impact on cost of equity

instead of negative against the literature. Fixed assets are totally financed

by equity in Pakistan and in the developed countries they are also finance

by long term debts as well; this might be the reason for the results which

are against the results of the studies conducted by (Clarkson et al., 1996).

Long term debt has -.139 t values along with beta of -0.004. Tax has t

value of 0.786, and beta value is 0.022. Pakistan economy is

undocumented and therefore taxation system is mainly depend on proper

documentation (Faruqi, 2011), which might be the reason for the

differences in results with respect to the studies conducted in the

developed countries. Market capitalization has t value of -7.259, with

beta value of -0.212. Therefore, it is established that with the increase in

the value of the firm the cost of equity will be decreased and vice versa.

The results are in line with (Bekaert et al., 2002). Hypothesis that market

capitalization has a negative impact on cost of equity is accepted.

Table 5. Main Effect of IV’s on Cost of Equity

Dependent Variable

Cost of Equity

Independent Variables Coefficients t-statistics

Intercept 20.12995 12.446

Net Earnings’ Growth (NEG) -.032 -1.126

Reserves and Retained Earnings

(RRE) .047 1.705

Times Interest Earned (TIE) .049 1.745

Gearing (G) -.048 -1.744

Fixed Asset Backing (FAB) .037 1.274

Long Term Debt (LTD) -.004 -.139

Tax (T) .022 .786

Market Capitalization (MC) -.212 -7.259

R Square .055

Adjusted R Square .048

Industry Wise Cost of Equity

Cost of equity in different industries has been shown in Table 7.

Minimum cost of equity is in Auto and allied industry which is 11.54%

and highest in construction industry which is 16.78% in line with the

findings of (Pointon and Omran, 2004). Their study in Egypt also

reported high cost of equity in construction industry, same stands true

with respect to Pakistan. Cost of equity in cables & electric goods, sugar,

cement, glass& ceramics, textile composite, synthetic & Rayon, jute,

fuel & energy, paper & board, transport & communication, chemical &

pharmaceuticals, food & personal care products, vanaspati & allied and

woolen is ranging between 13.02% to 13.94. In tobacco industry cost of

Abasyn Journal of Social Sciences – Volume 9 – Issue 2

538

equity is 12.06527 percent. Cost of equity is 15.28% in Leather, 14% in

tanneries, 14.21% in textile spinning and textile weaving. The average

cost of equity for all the industries in Pakistan is around 13.65 percent

which is in line with the finding of (Estrada, 2000) in emerging markets.

Conclusion

We find strong evidence that market capitalization has

significant impact on cost of equity. The results of the study were

counter to expectation and proves that net earnings growth, retention of

funds, times interest earned, gearing, fixed asset backing, long term debt

and tax have no impact on cost of equity. This may be because of the

corporate sector in Pakistan has been dominated by the family owned

businesses with non professional board of directors selected on the bases

of links (Shah & Butt, 2009). Secondly at present our empirical and

theoretical understanding of the cost of equity is still early with respect to

Pakistan. We caveat our results to some extent but current study still

provides solution for the deficiency in the existing literature by studying

the determinants of cost of equity in Pakistan.

Contribution of the Study

Our study contributes to economic growth measurement by

providing real results of cost of equity in different sectors of Pakistan.

No-doubt net income takes into account the cost of debt, which is

presented in income statement as interest expense, but does not

represents the cost of equity, therefore firms making a net profit can be

still unprofitable in an economic sense if the profit is less than their cost

of equity (Brigham & Houston, 2004). Current study provides first-hand

information to domestic and foreign investors regarding cost of doing

business in different industrial sectors of Pakistan. Global observation

reveals the fact that expected return by the equity holders is different

from industry due to the availability of investing opportunities. Finally

social and cultural aspects may be viewed as the determinants of cost of

equity.

Future Directions

Factors affecting cost of equity is very important area of research

as after determining the factors that effects cost of equity these factors

may be controlled to minimize the cost of equity that may contribute

towards maximization of shareholder wealth. So in the future research

may be conducted on how determinants of capital structure may differ

from sector to sector or industry to industry in Pakistan. This is because

literature suggests that determinants of cost of equity may vary from

industry to industry.

538

equity is 12.06527 percent. Cost of equity is 15.28% in Leather, 14% in

tanneries, 14.21% in textile spinning and textile weaving. The average

cost of equity for all the industries in Pakistan is around 13.65 percent

which is in line with the finding of (Estrada, 2000) in emerging markets.

Conclusion

We find strong evidence that market capitalization has

significant impact on cost of equity. The results of the study were

counter to expectation and proves that net earnings growth, retention of

funds, times interest earned, gearing, fixed asset backing, long term debt

and tax have no impact on cost of equity. This may be because of the

corporate sector in Pakistan has been dominated by the family owned

businesses with non professional board of directors selected on the bases

of links (Shah & Butt, 2009). Secondly at present our empirical and

theoretical understanding of the cost of equity is still early with respect to

Pakistan. We caveat our results to some extent but current study still

provides solution for the deficiency in the existing literature by studying

the determinants of cost of equity in Pakistan.

Contribution of the Study

Our study contributes to economic growth measurement by

providing real results of cost of equity in different sectors of Pakistan.

No-doubt net income takes into account the cost of debt, which is

presented in income statement as interest expense, but does not

represents the cost of equity, therefore firms making a net profit can be

still unprofitable in an economic sense if the profit is less than their cost

of equity (Brigham & Houston, 2004). Current study provides first-hand

information to domestic and foreign investors regarding cost of doing

business in different industrial sectors of Pakistan. Global observation

reveals the fact that expected return by the equity holders is different

from industry due to the availability of investing opportunities. Finally

social and cultural aspects may be viewed as the determinants of cost of

equity.

Future Directions

Factors affecting cost of equity is very important area of research

as after determining the factors that effects cost of equity these factors

may be controlled to minimize the cost of equity that may contribute

towards maximization of shareholder wealth. So in the future research

may be conducted on how determinants of capital structure may differ

from sector to sector or industry to industry in Pakistan. This is because

literature suggests that determinants of cost of equity may vary from

industry to industry.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.