Financial Analysis and Corporate Management Report: Paltel Company

VerifiedAdded on 2022/09/05

|17

|3614

|15

Report

AI Summary

This report provides a detailed analysis of the Palestine Telecommunication Company's (Paltel) corporate finance strategies. It begins with an introduction to corporate finance, outlining the process of finding financial needs and sourcing finance to maximize shareholder wealth. The report analyzes Paltel's financial and operating performance, including its financial position based on the 2018 annual report. It examines the company's capital structure, debt-to-equity ratio, and dividend policies over the past few years, highlighting the impact on its financial performance. The report also assesses Paltel's investment opportunities, financing needs, and the application of various investment appraisal techniques such as Net Present Value (NPV), Internal Rate of Return (IRR), Discounted Payback, Accounting Rate of Return (ARR), and Profitability Index (PI) to aid in investment decision-making. Finally, it concludes with an overview of the company's strengths and weaknesses, recommending an investment strategy for future growth. The report also includes a discussion on the cost of equity and debt, as well as suggestions for financing decisions, such as raising capital through debt or equity, and their respective impacts on the company's financial position and shareholder wealth.

Running head: CORPORATE FINANCE

Corporate Finance

Name of the Student:

Name of the University:

Author’s Note:

Corporate Finance

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE FINANCE

Executive Summary:

Corporate finance is the process of finding financial needs of corporations and sourcing such

finance needs with efficient capital structure with the objective of achieving overall objectives of

the business and to maximize shareholders wealth. In this report the financial and operating

performance and financial position of the Palestine Telecommunications Company has been

analyzed along with their corporate management strategies. The capital structure and dividend

policies of the company have also been analyzed to understand their financial management or

corporate finance strategies aiming towards achieving the objective of the shareholders wealth

maximization. With an assessment of investment needs for the company various strategies have

been suggested for sourcing such investment. Further, various investment appraisal techniques

and method have been applied and analyzed to help in decision making for the investment.

Lastly, the report concludes with outlining overall strengths and weaknesses of the company and

recommending an investment strategy.

Executive Summary:

Corporate finance is the process of finding financial needs of corporations and sourcing such

finance needs with efficient capital structure with the objective of achieving overall objectives of

the business and to maximize shareholders wealth. In this report the financial and operating

performance and financial position of the Palestine Telecommunications Company has been

analyzed along with their corporate management strategies. The capital structure and dividend

policies of the company have also been analyzed to understand their financial management or

corporate finance strategies aiming towards achieving the objective of the shareholders wealth

maximization. With an assessment of investment needs for the company various strategies have

been suggested for sourcing such investment. Further, various investment appraisal techniques

and method have been applied and analyzed to help in decision making for the investment.

Lastly, the report concludes with outlining overall strengths and weaknesses of the company and

recommending an investment strategy.

2CORPORATE FINANCE

Table of Contents

1. Introduction:................................................................................................................................3

2. Background to the company:.......................................................................................................3

3. Challenges and investment opportunities for PALTEL:.............................................................4

4. Capital structure and dividend policy of the Palestine Telecommunication Company:..............5

5. Financing needs and financing decisions:...................................................................................7

6. Investment appraisal techniques:.................................................................................................9

Net Present Value:.....................................................................................................................11

Internal Rate of Return:.............................................................................................................12

Discounted payback:..................................................................................................................12

Accounting rate of return:..........................................................................................................13

Profitability Index:.....................................................................................................................13

7. Conclusion and recommendation:.............................................................................................14

8. References and bibliography:....................................................................................................15

Table of Contents

1. Introduction:................................................................................................................................3

2. Background to the company:.......................................................................................................3

3. Challenges and investment opportunities for PALTEL:.............................................................4

4. Capital structure and dividend policy of the Palestine Telecommunication Company:..............5

5. Financing needs and financing decisions:...................................................................................7

6. Investment appraisal techniques:.................................................................................................9

Net Present Value:.....................................................................................................................11

Internal Rate of Return:.............................................................................................................12

Discounted payback:..................................................................................................................12

Accounting rate of return:..........................................................................................................13

Profitability Index:.....................................................................................................................13

7. Conclusion and recommendation:.............................................................................................14

8. References and bibliography:....................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE FINANCE

1. Introduction:

In this report, financial performance and financial position of the Palestine

Telecommunication Company have been analyzed to understand and interpret the corporate

strategies of the company. Information from the 2018 annual report and financial statement of

the company have been considered for such analysis. For further analysis previous few years

financial statements and annual report information have also been considered (Paltelgroup.ps

2020). In this report the present capital structure of the company has been analyzed to understand

the leverage benefit the company is having currently. Dividend policies have also been analyzed

and interpreted based on the dividend payout for the last few years. Based on their present capital

structure and leverage in the capital based, financing decision have been suggested and

investment appraisal techniques have been applied to help in making investment decisions.

2. Background to the company:

Palestine Telecommunication Company is a group of companies in the

telecommunication industry in Palestine. It is the largest telecommunication in Palestine. The

Palestine Telecommunication Company is also considered as the largest employer in the country

(Paltelgroup.ps 2020). In recent few years a downtrend in the financial performance of the

company can be observed. It can be observed from the 2018 annual report of the company that,

the total assets of the company or the net worth of the company has been decreased from JD925

million to JD858 million, which implies shrunk in the capital base and financial position of the

company (Paltelgroup.ps 2020).

From the income statement of the company is can be observed that there is a marginal

increase in the net income of the company, which implies improvement in the financial

1. Introduction:

In this report, financial performance and financial position of the Palestine

Telecommunication Company have been analyzed to understand and interpret the corporate

strategies of the company. Information from the 2018 annual report and financial statement of

the company have been considered for such analysis. For further analysis previous few years

financial statements and annual report information have also been considered (Paltelgroup.ps

2020). In this report the present capital structure of the company has been analyzed to understand

the leverage benefit the company is having currently. Dividend policies have also been analyzed

and interpreted based on the dividend payout for the last few years. Based on their present capital

structure and leverage in the capital based, financing decision have been suggested and

investment appraisal techniques have been applied to help in making investment decisions.

2. Background to the company:

Palestine Telecommunication Company is a group of companies in the

telecommunication industry in Palestine. It is the largest telecommunication in Palestine. The

Palestine Telecommunication Company is also considered as the largest employer in the country

(Paltelgroup.ps 2020). In recent few years a downtrend in the financial performance of the

company can be observed. It can be observed from the 2018 annual report of the company that,

the total assets of the company or the net worth of the company has been decreased from JD925

million to JD858 million, which implies shrunk in the capital base and financial position of the

company (Paltelgroup.ps 2020).

From the income statement of the company is can be observed that there is a marginal

increase in the net income of the company, which implies improvement in the financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE FINANCE

performance of the company. In the year 2010 and onwards various international

telecommunication companies entered into the market telecommunication market of the

Palestine and exploited some share of the customer base of the industry, but still the Palestine

Telecommunication Company has certain advantages over their competitors which helped them

to become a sustainable company over the last decade. It can be observed from the 2018 annual

report of the company that, there is an increase in the cash generation form the operating

activities of the company (Paltelgroup.ps 2020).

Shares of the Palestine Telecommunication Company is listed in the Palestine Stock

Exchange and currently it is trading at JD4.12 with the total trade volume of 7,566 shares. The

shares of the company was listed in the Palestine Stock Exchange in the year 2006 and it was

traded at JD8.31 in the initial day at a trading volume of 27,751,871. Thereafter a gradual fall in

the share price of the company can be observed till 2007. In the mid of the year 2008 an increase

in the share price of the company can be observed with the improvement in the financial

performance of the company. From 2008 to 2014 a marginal fluctuation in the share price of the

company can be observed, which implies a sustainable financial performance of the company.

Thereafter, from 2014 onward the share price of the company started falling and the trend

continues till now. Behind, such a continuous decrease in the share price of the company can be

identified with the increase in competition in the market and international investment in the

telecommunication industry of the country (Paltelgroup.ps 2020).

3. Challenges and investment opportunities for PALTEL:

Though a marginal improvement in the financial performance can be observed in the year

2018 as compared to the last few years, the company still needs to invest in technology

development to improve the quality of their services and to reach out to more and more

performance of the company. In the year 2010 and onwards various international

telecommunication companies entered into the market telecommunication market of the

Palestine and exploited some share of the customer base of the industry, but still the Palestine

Telecommunication Company has certain advantages over their competitors which helped them

to become a sustainable company over the last decade. It can be observed from the 2018 annual

report of the company that, there is an increase in the cash generation form the operating

activities of the company (Paltelgroup.ps 2020).

Shares of the Palestine Telecommunication Company is listed in the Palestine Stock

Exchange and currently it is trading at JD4.12 with the total trade volume of 7,566 shares. The

shares of the company was listed in the Palestine Stock Exchange in the year 2006 and it was

traded at JD8.31 in the initial day at a trading volume of 27,751,871. Thereafter a gradual fall in

the share price of the company can be observed till 2007. In the mid of the year 2008 an increase

in the share price of the company can be observed with the improvement in the financial

performance of the company. From 2008 to 2014 a marginal fluctuation in the share price of the

company can be observed, which implies a sustainable financial performance of the company.

Thereafter, from 2014 onward the share price of the company started falling and the trend

continues till now. Behind, such a continuous decrease in the share price of the company can be

identified with the increase in competition in the market and international investment in the

telecommunication industry of the country (Paltelgroup.ps 2020).

3. Challenges and investment opportunities for PALTEL:

Though a marginal improvement in the financial performance can be observed in the year

2018 as compared to the last few years, the company still needs to invest in technology

development to improve the quality of their services and to reach out to more and more

5CORPORATE FINANCE

customers. The company had been working towards meeting that needs for the last few years and

with that objective they have acquired full stake in the other companies in the same industry. By

the end of 2018 financial year the company had been holding hundred percent interest in four

companies and also various other tie ups and agreements with some other regional operators and

companies (Paltelgroup.ps 2020).

Therefore, the need for investment in technologies and improvement in service of the

company can be well observed from the above analysis. Now, comes the question, how such

financing needs can be fulfilled. It can be observed that the company is having equity share

capital and long term loans in their total capital structure. Hence, the company can raise their

financing needs through the issue of equity shares or theory the long term loans. In the following

parts of this report, some of such financing strategies of the company have been analyzed and the

investment appraisal techniques have been applied to suggest the company in meeting their

financing needs and building an efficient corporate strategy (Paltelgroup.ps 2020).

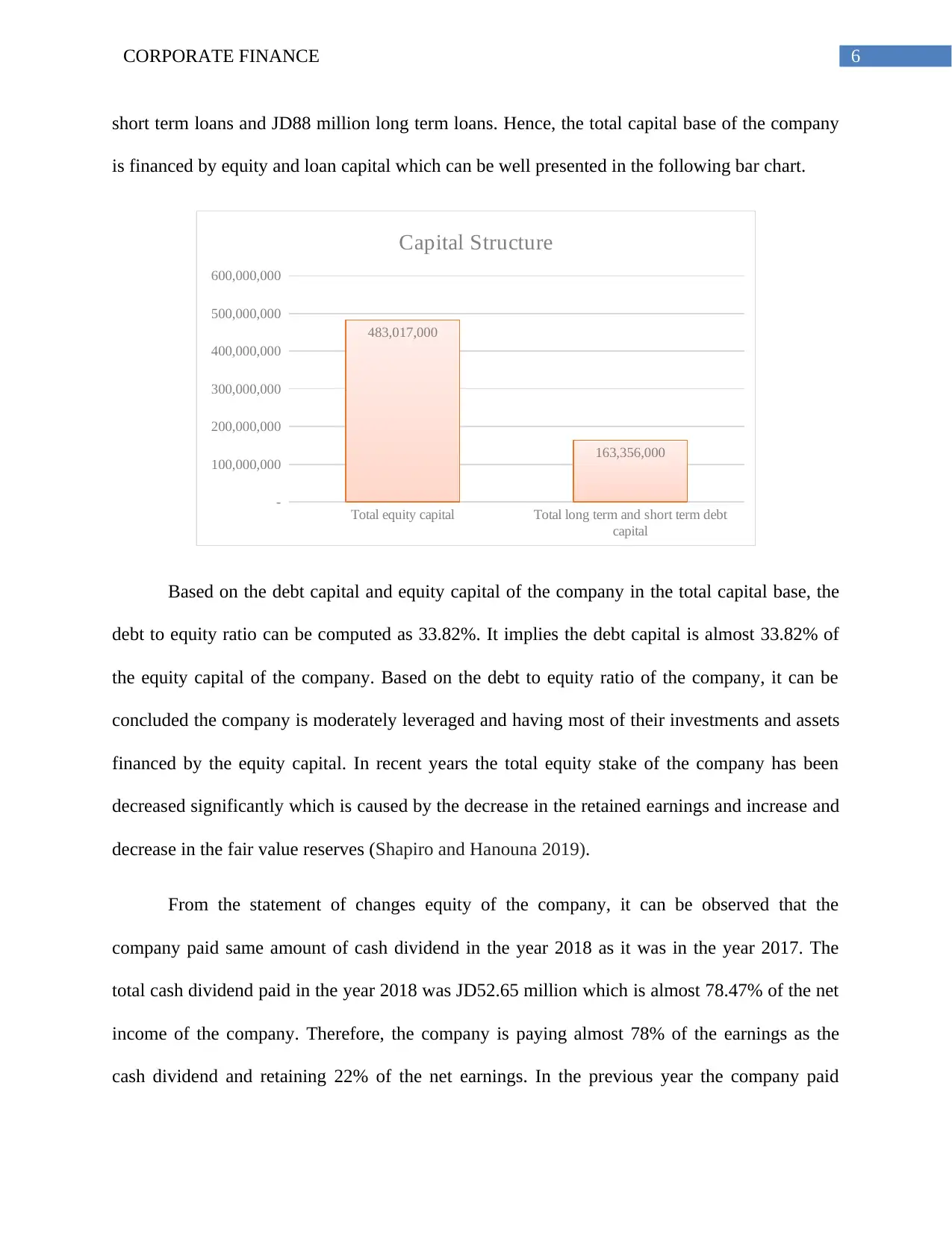

4. Capital structure and dividend policy of the Palestine Telecommunication Company:

Capital structure of the company is the combination of different means of capital sources

in the total capital base of the company. In other words, the capital structure theory talks about

the optimal combination of different sources of capital in financing the total capital need of the

company. As the Palestine Telecommunication Company is a listed company limited by shares,

the main source of capital of the company is the common stocks or equity share capital. In

addition, the company financed their various investments and projects with the long term and

short term loans and borrowings. It can be observed from the 2018 consolidated balance sheet of

the company that the company is having JD483 million total equity which has been decreased

from JD565 million in the previous year (Paltelgroup.ps 2020). They are having JD74 million

customers. The company had been working towards meeting that needs for the last few years and

with that objective they have acquired full stake in the other companies in the same industry. By

the end of 2018 financial year the company had been holding hundred percent interest in four

companies and also various other tie ups and agreements with some other regional operators and

companies (Paltelgroup.ps 2020).

Therefore, the need for investment in technologies and improvement in service of the

company can be well observed from the above analysis. Now, comes the question, how such

financing needs can be fulfilled. It can be observed that the company is having equity share

capital and long term loans in their total capital structure. Hence, the company can raise their

financing needs through the issue of equity shares or theory the long term loans. In the following

parts of this report, some of such financing strategies of the company have been analyzed and the

investment appraisal techniques have been applied to suggest the company in meeting their

financing needs and building an efficient corporate strategy (Paltelgroup.ps 2020).

4. Capital structure and dividend policy of the Palestine Telecommunication Company:

Capital structure of the company is the combination of different means of capital sources

in the total capital base of the company. In other words, the capital structure theory talks about

the optimal combination of different sources of capital in financing the total capital need of the

company. As the Palestine Telecommunication Company is a listed company limited by shares,

the main source of capital of the company is the common stocks or equity share capital. In

addition, the company financed their various investments and projects with the long term and

short term loans and borrowings. It can be observed from the 2018 consolidated balance sheet of

the company that the company is having JD483 million total equity which has been decreased

from JD565 million in the previous year (Paltelgroup.ps 2020). They are having JD74 million

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE FINANCE

short term loans and JD88 million long term loans. Hence, the total capital base of the company

is financed by equity and loan capital which can be well presented in the following bar chart.

Total equity capital Total long term and short term debt

capital

-

100,000,000

200,000,000

300,000,000

400,000,000

500,000,000

600,000,000

483,017,000

163,356,000

Capital Structure

Based on the debt capital and equity capital of the company in the total capital base, the

debt to equity ratio can be computed as 33.82%. It implies the debt capital is almost 33.82% of

the equity capital of the company. Based on the debt to equity ratio of the company, it can be

concluded the company is moderately leveraged and having most of their investments and assets

financed by the equity capital. In recent years the total equity stake of the company has been

decreased significantly which is caused by the decrease in the retained earnings and increase and

decrease in the fair value reserves (Shapiro and Hanouna 2019).

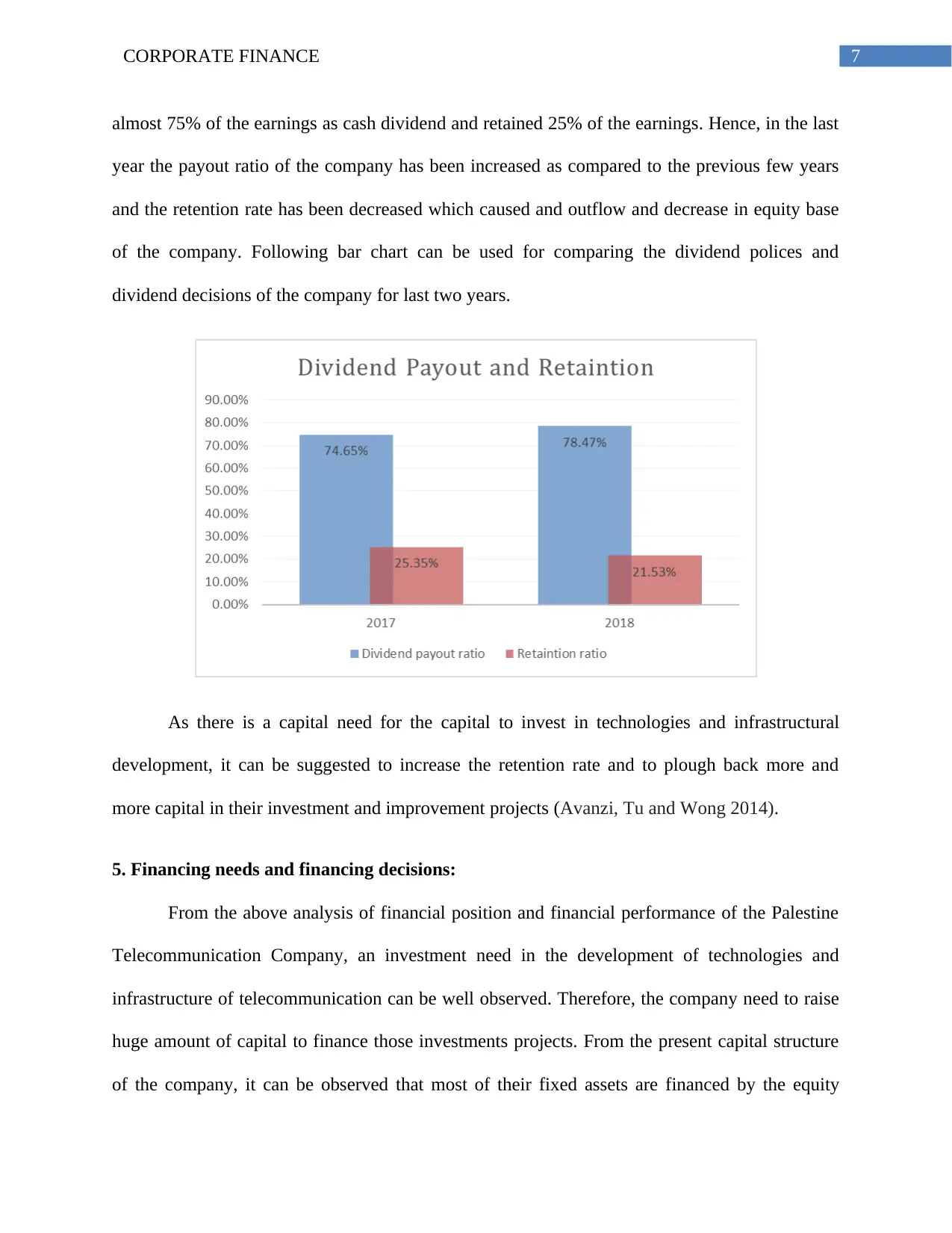

From the statement of changes equity of the company, it can be observed that the

company paid same amount of cash dividend in the year 2018 as it was in the year 2017. The

total cash dividend paid in the year 2018 was JD52.65 million which is almost 78.47% of the net

income of the company. Therefore, the company is paying almost 78% of the earnings as the

cash dividend and retaining 22% of the net earnings. In the previous year the company paid

short term loans and JD88 million long term loans. Hence, the total capital base of the company

is financed by equity and loan capital which can be well presented in the following bar chart.

Total equity capital Total long term and short term debt

capital

-

100,000,000

200,000,000

300,000,000

400,000,000

500,000,000

600,000,000

483,017,000

163,356,000

Capital Structure

Based on the debt capital and equity capital of the company in the total capital base, the

debt to equity ratio can be computed as 33.82%. It implies the debt capital is almost 33.82% of

the equity capital of the company. Based on the debt to equity ratio of the company, it can be

concluded the company is moderately leveraged and having most of their investments and assets

financed by the equity capital. In recent years the total equity stake of the company has been

decreased significantly which is caused by the decrease in the retained earnings and increase and

decrease in the fair value reserves (Shapiro and Hanouna 2019).

From the statement of changes equity of the company, it can be observed that the

company paid same amount of cash dividend in the year 2018 as it was in the year 2017. The

total cash dividend paid in the year 2018 was JD52.65 million which is almost 78.47% of the net

income of the company. Therefore, the company is paying almost 78% of the earnings as the

cash dividend and retaining 22% of the net earnings. In the previous year the company paid

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE FINANCE

almost 75% of the earnings as cash dividend and retained 25% of the earnings. Hence, in the last

year the payout ratio of the company has been increased as compared to the previous few years

and the retention rate has been decreased which caused and outflow and decrease in equity base

of the company. Following bar chart can be used for comparing the dividend polices and

dividend decisions of the company for last two years.

As there is a capital need for the capital to invest in technologies and infrastructural

development, it can be suggested to increase the retention rate and to plough back more and

more capital in their investment and improvement projects (Avanzi, Tu and Wong 2014).

5. Financing needs and financing decisions:

From the above analysis of financial position and financial performance of the Palestine

Telecommunication Company, an investment need in the development of technologies and

infrastructure of telecommunication can be well observed. Therefore, the company need to raise

huge amount of capital to finance those investments projects. From the present capital structure

of the company, it can be observed that most of their fixed assets are financed by the equity

almost 75% of the earnings as cash dividend and retained 25% of the earnings. Hence, in the last

year the payout ratio of the company has been increased as compared to the previous few years

and the retention rate has been decreased which caused and outflow and decrease in equity base

of the company. Following bar chart can be used for comparing the dividend polices and

dividend decisions of the company for last two years.

As there is a capital need for the capital to invest in technologies and infrastructural

development, it can be suggested to increase the retention rate and to plough back more and

more capital in their investment and improvement projects (Avanzi, Tu and Wong 2014).

5. Financing needs and financing decisions:

From the above analysis of financial position and financial performance of the Palestine

Telecommunication Company, an investment need in the development of technologies and

infrastructure of telecommunication can be well observed. Therefore, the company need to raise

huge amount of capital to finance those investments projects. From the present capital structure

of the company, it can be observed that most of their fixed assets are financed by the equity

8CORPORATE FINANCE

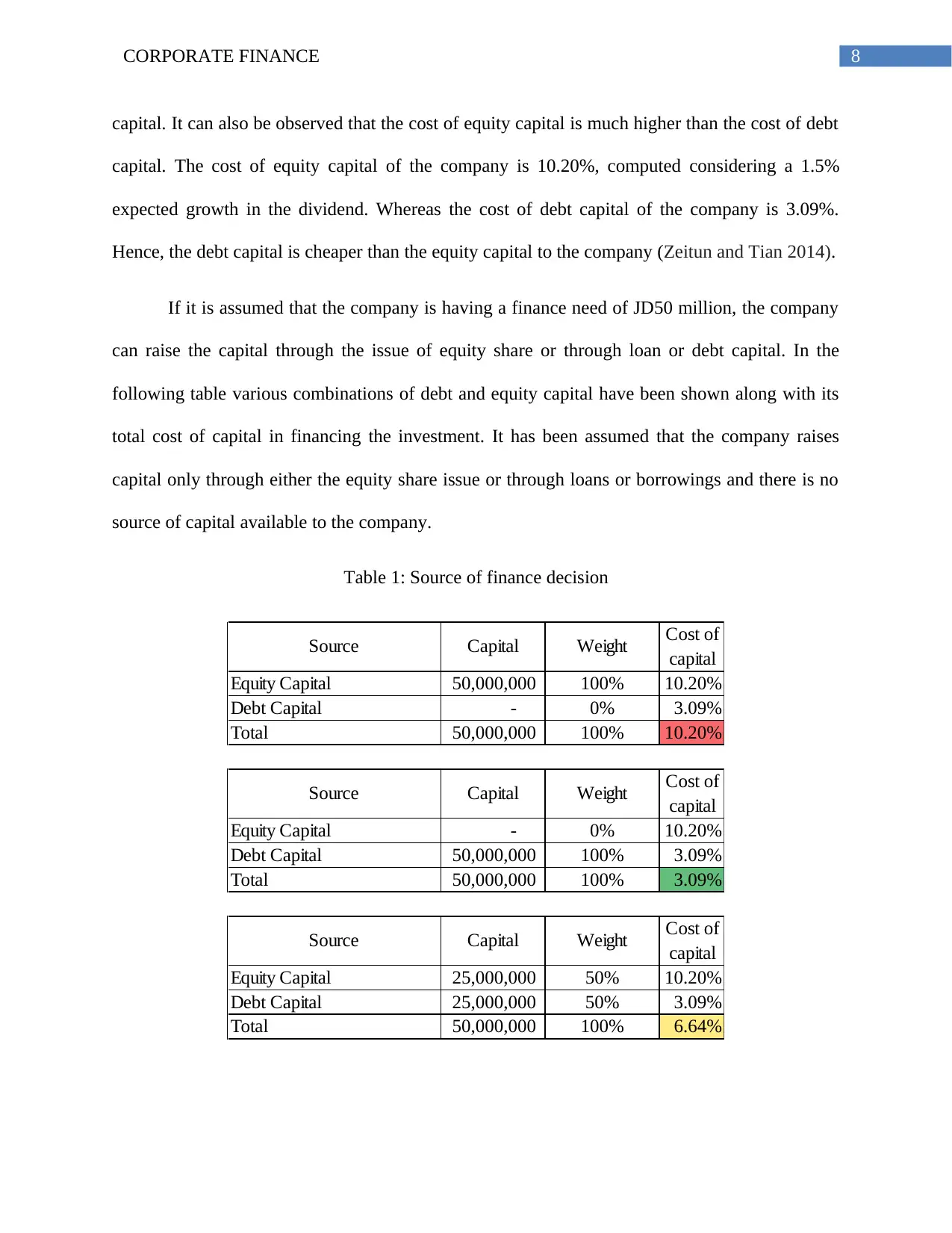

capital. It can also be observed that the cost of equity capital is much higher than the cost of debt

capital. The cost of equity capital of the company is 10.20%, computed considering a 1.5%

expected growth in the dividend. Whereas the cost of debt capital of the company is 3.09%.

Hence, the debt capital is cheaper than the equity capital to the company (Zeitun and Tian 2014).

If it is assumed that the company is having a finance need of JD50 million, the company

can raise the capital through the issue of equity share or through loan or debt capital. In the

following table various combinations of debt and equity capital have been shown along with its

total cost of capital in financing the investment. It has been assumed that the company raises

capital only through either the equity share issue or through loans or borrowings and there is no

source of capital available to the company.

Table 1: Source of finance decision

Source Capital Weight Cost of

capital

Equity Capital 50,000,000 100% 10.20%

Debt Capital - 0% 3.09%

Total 50,000,000 100% 10.20%

Source Capital Weight Cost of

capital

Equity Capital - 0% 10.20%

Debt Capital 50,000,000 100% 3.09%

Total 50,000,000 100% 3.09%

Source Capital Weight Cost of

capital

Equity Capital 25,000,000 50% 10.20%

Debt Capital 25,000,000 50% 3.09%

Total 50,000,000 100% 6.64%

Equity Capital 20,000,000 40% 10.20%

Debt Capital 30,000,000 60% 3.09%

Total 50,000,000 100% 5.93%

capital. It can also be observed that the cost of equity capital is much higher than the cost of debt

capital. The cost of equity capital of the company is 10.20%, computed considering a 1.5%

expected growth in the dividend. Whereas the cost of debt capital of the company is 3.09%.

Hence, the debt capital is cheaper than the equity capital to the company (Zeitun and Tian 2014).

If it is assumed that the company is having a finance need of JD50 million, the company

can raise the capital through the issue of equity share or through loan or debt capital. In the

following table various combinations of debt and equity capital have been shown along with its

total cost of capital in financing the investment. It has been assumed that the company raises

capital only through either the equity share issue or through loans or borrowings and there is no

source of capital available to the company.

Table 1: Source of finance decision

Source Capital Weight Cost of

capital

Equity Capital 50,000,000 100% 10.20%

Debt Capital - 0% 3.09%

Total 50,000,000 100% 10.20%

Source Capital Weight Cost of

capital

Equity Capital - 0% 10.20%

Debt Capital 50,000,000 100% 3.09%

Total 50,000,000 100% 3.09%

Source Capital Weight Cost of

capital

Equity Capital 25,000,000 50% 10.20%

Debt Capital 25,000,000 50% 3.09%

Total 50,000,000 100% 6.64%

Equity Capital 20,000,000 40% 10.20%

Debt Capital 30,000,000 60% 3.09%

Total 50,000,000 100% 5.93%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE FINANCE

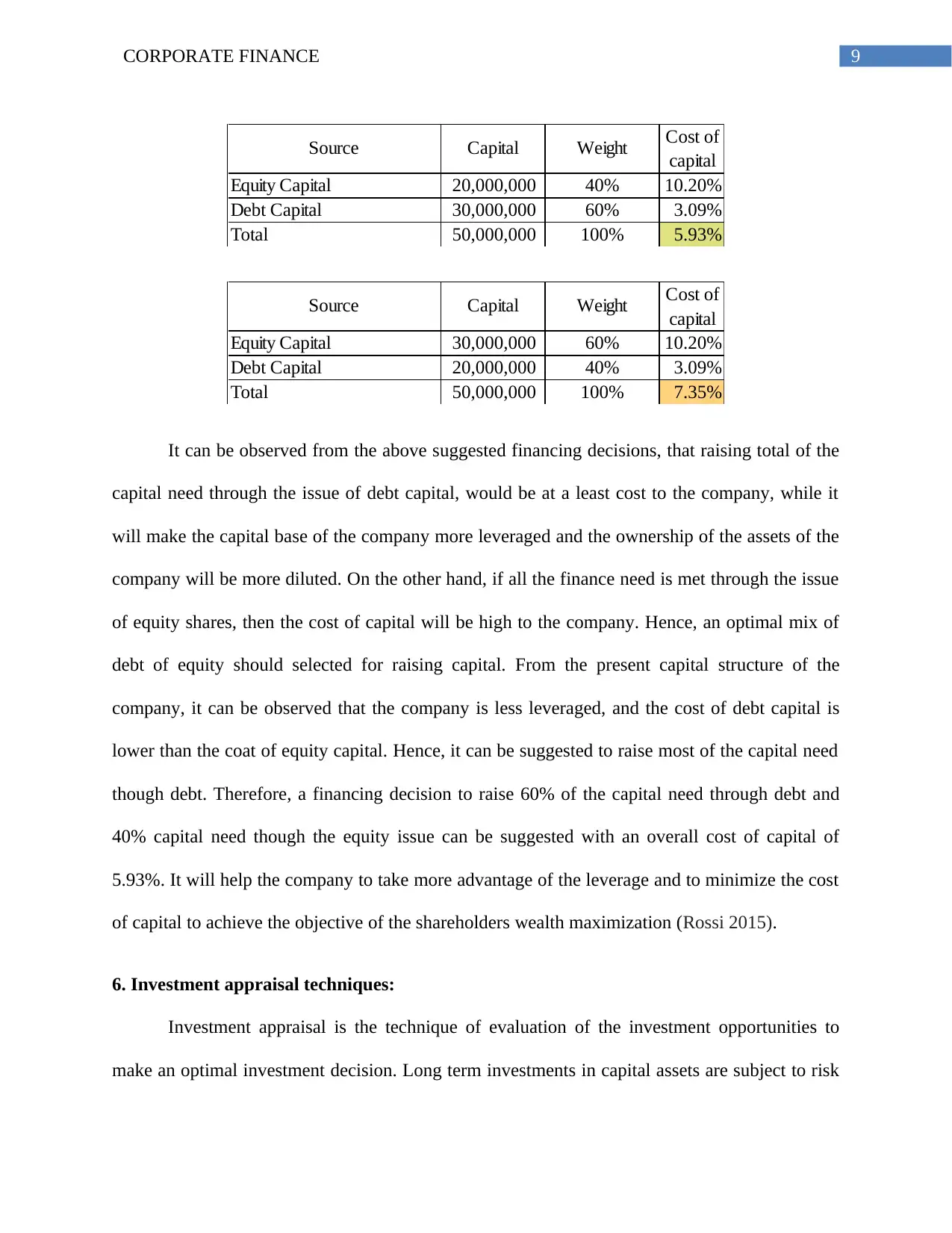

Equity Capital 25,000,000 50% 10.20%

Debt Capital 25,000,000 50% 3.09%

Total 50,000,000 100% 6.64%

Source Capital Weight Cost of

capital

Equity Capital 20,000,000 40% 10.20%

Debt Capital 30,000,000 60% 3.09%

Total 50,000,000 100% 5.93%

Source Capital Weight Cost of

capital

Equity Capital 30,000,000 60% 10.20%

Debt Capital 20,000,000 40% 3.09%

Total 50,000,000 100% 7.35%

It can be observed from the above suggested financing decisions, that raising total of the

capital need through the issue of debt capital, would be at a least cost to the company, while it

will make the capital base of the company more leveraged and the ownership of the assets of the

company will be more diluted. On the other hand, if all the finance need is met through the issue

of equity shares, then the cost of capital will be high to the company. Hence, an optimal mix of

debt of equity should selected for raising capital. From the present capital structure of the

company, it can be observed that the company is less leveraged, and the cost of debt capital is

lower than the coat of equity capital. Hence, it can be suggested to raise most of the capital need

though debt. Therefore, a financing decision to raise 60% of the capital need through debt and

40% capital need though the equity issue can be suggested with an overall cost of capital of

5.93%. It will help the company to take more advantage of the leverage and to minimize the cost

of capital to achieve the objective of the shareholders wealth maximization (Rossi 2015).

6. Investment appraisal techniques:

Investment appraisal is the technique of evaluation of the investment opportunities to

make an optimal investment decision. Long term investments in capital assets are subject to risk

Equity Capital 25,000,000 50% 10.20%

Debt Capital 25,000,000 50% 3.09%

Total 50,000,000 100% 6.64%

Source Capital Weight Cost of

capital

Equity Capital 20,000,000 40% 10.20%

Debt Capital 30,000,000 60% 3.09%

Total 50,000,000 100% 5.93%

Source Capital Weight Cost of

capital

Equity Capital 30,000,000 60% 10.20%

Debt Capital 20,000,000 40% 3.09%

Total 50,000,000 100% 7.35%

It can be observed from the above suggested financing decisions, that raising total of the

capital need through the issue of debt capital, would be at a least cost to the company, while it

will make the capital base of the company more leveraged and the ownership of the assets of the

company will be more diluted. On the other hand, if all the finance need is met through the issue

of equity shares, then the cost of capital will be high to the company. Hence, an optimal mix of

debt of equity should selected for raising capital. From the present capital structure of the

company, it can be observed that the company is less leveraged, and the cost of debt capital is

lower than the coat of equity capital. Hence, it can be suggested to raise most of the capital need

though debt. Therefore, a financing decision to raise 60% of the capital need through debt and

40% capital need though the equity issue can be suggested with an overall cost of capital of

5.93%. It will help the company to take more advantage of the leverage and to minimize the cost

of capital to achieve the objective of the shareholders wealth maximization (Rossi 2015).

6. Investment appraisal techniques:

Investment appraisal is the technique of evaluation of the investment opportunities to

make an optimal investment decision. Long term investments in capital assets are subject to risk

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE FINANCE

and capital cannot be switched over to other investment options easily. Hence, before making an

investment in the capital assets, costs and benefits associated with such investment options must

be analyzed. Time value of money is the consideration for utilization of the capital or the

expected return for sacrificing the use of capital for a period of time. Hence, while making such

investment evaluation and investment analysis, the time value of money must be considered

(Baum and Crosby 2014). Based on the fact that whether the time value of money has been

considered or not, the investment appraisal or investment evaluation techniques and methods can

be classified into discounted techniques and non-discounted techniques.

Net present value method, discounted payback method, internal rate of return are the

example of discounted investment appraisal techniques, on the other hand, accounting rate of

return, payback period are some example of non-discounted techniques of investment appraisal.

Investment Appraisal

Techniques

Discounted

Methods

Net Present Value

Internal Rate of

Return

Dicounted

Payback

Non Discounted

Methods

Accounting Rate

of Return

Profitability Index

and capital cannot be switched over to other investment options easily. Hence, before making an

investment in the capital assets, costs and benefits associated with such investment options must

be analyzed. Time value of money is the consideration for utilization of the capital or the

expected return for sacrificing the use of capital for a period of time. Hence, while making such

investment evaluation and investment analysis, the time value of money must be considered

(Baum and Crosby 2014). Based on the fact that whether the time value of money has been

considered or not, the investment appraisal or investment evaluation techniques and methods can

be classified into discounted techniques and non-discounted techniques.

Net present value method, discounted payback method, internal rate of return are the

example of discounted investment appraisal techniques, on the other hand, accounting rate of

return, payback period are some example of non-discounted techniques of investment appraisal.

Investment Appraisal

Techniques

Discounted

Methods

Net Present Value

Internal Rate of

Return

Dicounted

Payback

Non Discounted

Methods

Accounting Rate

of Return

Profitability Index

11CORPORATE FINANCE

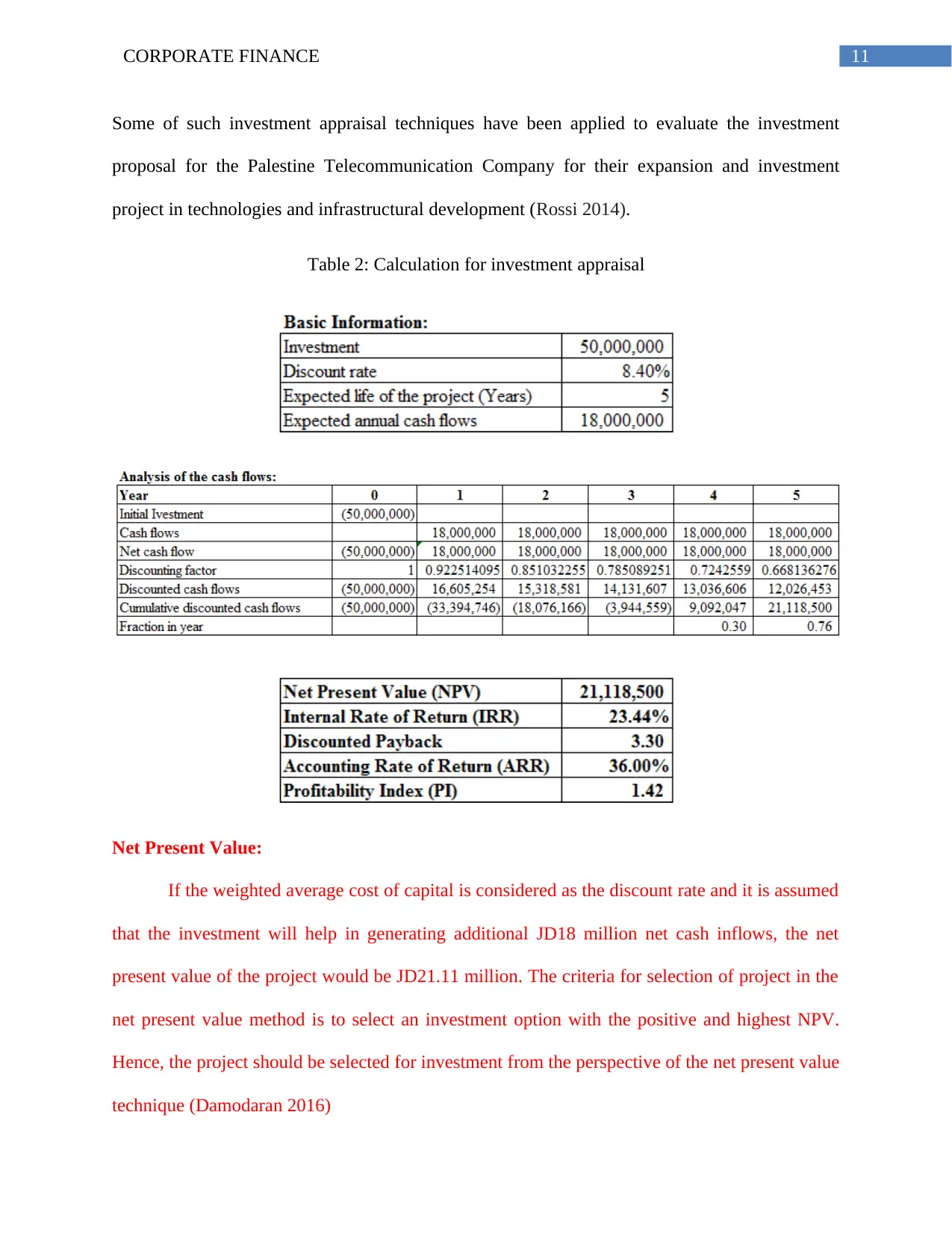

Some of such investment appraisal techniques have been applied to evaluate the investment

proposal for the Palestine Telecommunication Company for their expansion and investment

project in technologies and infrastructural development (Rossi 2014).

Table 2: Calculation for investment appraisal

Net Present Value:

If the weighted average cost of capital is considered as the discount rate and it is assumed

that the investment will help in generating additional JD18 million net cash inflows, the net

present value of the project would be JD21.11 million. The criteria for selection of project in the

net present value method is to select an investment option with the positive and highest NPV.

Hence, the project should be selected for investment from the perspective of the net present value

technique (Damodaran 2016)

Some of such investment appraisal techniques have been applied to evaluate the investment

proposal for the Palestine Telecommunication Company for their expansion and investment

project in technologies and infrastructural development (Rossi 2014).

Table 2: Calculation for investment appraisal

Net Present Value:

If the weighted average cost of capital is considered as the discount rate and it is assumed

that the investment will help in generating additional JD18 million net cash inflows, the net

present value of the project would be JD21.11 million. The criteria for selection of project in the

net present value method is to select an investment option with the positive and highest NPV.

Hence, the project should be selected for investment from the perspective of the net present value

technique (Damodaran 2016)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.