Paradise Industries: Expenditure and Conversion Cycle Analysis

VerifiedAdded on 2023/01/11

|13

|2794

|1

Case Study

AI Summary

This case study examines Paradise Industries' expenditure and cash conversion cycles, providing detailed flowcharts and analyses. The expenditure cycle analysis identifies structural and documentation weaknesses, such as the accountant's overloaded responsibilities and incomplete documentation, and proposes internal control improvements. The cash conversion cycle section explores associated risks, including payment delays, liquidity decline, and inventory issues, and suggests risk management strategies such as streamlining inventory, increasing the buying cycle, and focusing on the end-to-end supply chain. The report emphasizes the importance of strong internal controls and proactive risk management to improve financial processes.

CASE STUDY-

PARADISE

INDUSTRIES

PARADISE

INDUSTRIES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

1. System flow chart of expenditure cycle...................................................................................4

1.1 Analysis of physical internal control weaknesses in the expenditure cycle......................4

2. System flow chart of conversion cycle....................................................................................8

2.2 Analysis of the risks exist in the conversion cycle and the changes needed to reduce the

risks..........................................................................................................................................8

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

1. System flow chart of expenditure cycle...................................................................................4

1.1 Analysis of physical internal control weaknesses in the expenditure cycle......................4

2. System flow chart of conversion cycle....................................................................................8

2.2 Analysis of the risks exist in the conversion cycle and the changes needed to reduce the

risks..........................................................................................................................................8

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

This project report is based on two operating concept; expenditure cycle and cash conversion

cycle. Expenditure cycle flow chart will show how and when purchase order is placed and how

many copies required to be distributed to initiate purchase order and it also discuss about

treatment of work in progress status. Discussion of weakness in current model of procurement

process has been discussed and proper recommendation is also suggested for the same. The other

concept which is cash conversion cycle; discusses about period and risk associated with

conversion of finished goods into cash and also explained the process of whole cycle.

This project report is based on two operating concept; expenditure cycle and cash conversion

cycle. Expenditure cycle flow chart will show how and when purchase order is placed and how

many copies required to be distributed to initiate purchase order and it also discuss about

treatment of work in progress status. Discussion of weakness in current model of procurement

process has been discussed and proper recommendation is also suggested for the same. The other

concept which is cash conversion cycle; discusses about period and risk associated with

conversion of finished goods into cash and also explained the process of whole cycle.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

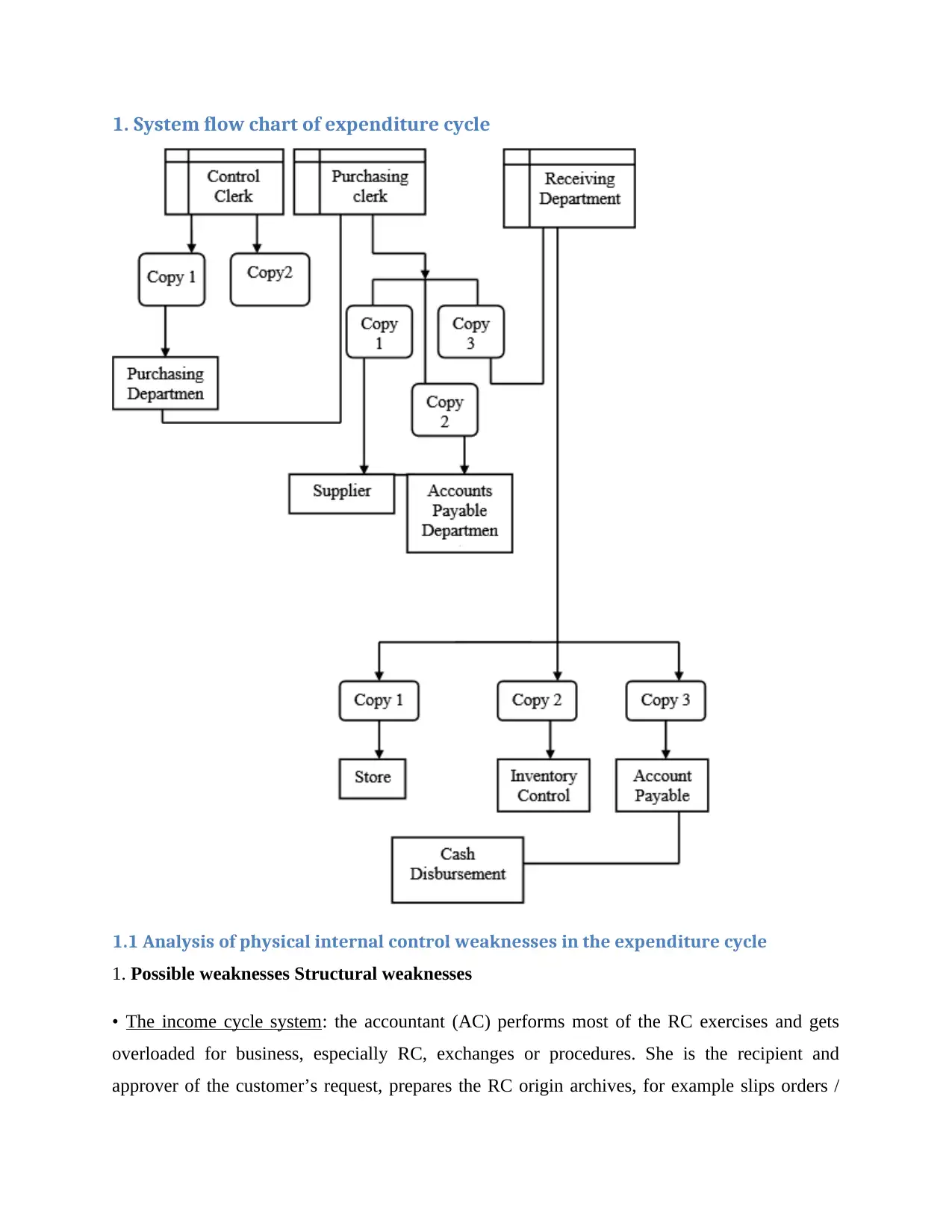

1. System flow chart of expenditure cycle

1.1 Analysis of physical internal control weaknesses in the expenditure cycle

1. Possible weaknesses Structural weaknesses

• The income cycle system: the accountant (AC) performs most of the RC exercises and gets

overloaded for business, especially RC, exchanges or procedures. She is the recipient and

approver of the customer’s request, prepares the RC origin archives, for example slips orders /

1.1 Analysis of physical internal control weaknesses in the expenditure cycle

1. Possible weaknesses Structural weaknesses

• The income cycle system: the accountant (AC) performs most of the RC exercises and gets

overloaded for business, especially RC, exchanges or procedures. She is the recipient and

approver of the customer’s request, prepares the RC origin archives, for example slips orders /

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

tender packing, but also maintains the general inventory and invoices the individual very

purchase. This is where false actions can occur. For models, the CA may have an unstable

position with the customer and deceive the President / Owner; it can also incur more significant

costs for the customer, but it records and reports on the exchange using the standard charge

(Arens and et.al., 2003).

• Expenditure cycle system: the Company combines licensing, registration and care operations in

one office; control of reception, purchasing and inventory (R, P and IC). This is a violation of the

isolation of duties. R, P and IC staff perform most EC exercises and have many business

responsibilities, especially EC, exchanges or procedures. She makes the requests, receives

organized returns, analyzes and records the stock and publishes the accounts payable data

archive. This is where false actions can occur. For models, the R, P and IC staff may have

inconsistent positions with the merchant and deceive the President / Owner; it can also take

unscheduled soup (except hard food) and no one will pay attention (Chan, 2006).

2. Weaknesses of documentation and commercial actions (methods)

The potential pitfalls of documentation and commercial (technical) activities within the spending

cycle of giant eggplants are:

• Good numbers in the CE archives, for example, do not contradict the number of registrations.

There will be problems in the production and splitting of the output / report, especially when the

organization starts implementing a new accounting framework (Gay and Simnett, 2012).

• During the section function of the contract request, the accountant directly supports the request

without checking the customer's credit records (customer control record or source of customer

accounting data). It appears that the client has not yet given much effort to the organization.

Internal control weaknesses (IC)

The possible shortcomings of the general control of the body's RC structure are:

Organizational Controls

Employee accounting; there are many functions of this nature that should be isolated, for

example, from costs, sales records, generalization of inventory and information

purchase. This is where false actions can occur. For models, the CA may have an unstable

position with the customer and deceive the President / Owner; it can also incur more significant

costs for the customer, but it records and reports on the exchange using the standard charge

(Arens and et.al., 2003).

• Expenditure cycle system: the Company combines licensing, registration and care operations in

one office; control of reception, purchasing and inventory (R, P and IC). This is a violation of the

isolation of duties. R, P and IC staff perform most EC exercises and have many business

responsibilities, especially EC, exchanges or procedures. She makes the requests, receives

organized returns, analyzes and records the stock and publishes the accounts payable data

archive. This is where false actions can occur. For models, the R, P and IC staff may have

inconsistent positions with the merchant and deceive the President / Owner; it can also take

unscheduled soup (except hard food) and no one will pay attention (Chan, 2006).

2. Weaknesses of documentation and commercial actions (methods)

The potential pitfalls of documentation and commercial (technical) activities within the spending

cycle of giant eggplants are:

• Good numbers in the CE archives, for example, do not contradict the number of registrations.

There will be problems in the production and splitting of the output / report, especially when the

organization starts implementing a new accounting framework (Gay and Simnett, 2012).

• During the section function of the contract request, the accountant directly supports the request

without checking the customer's credit records (customer control record or source of customer

accounting data). It appears that the client has not yet given much effort to the organization.

Internal control weaknesses (IC)

The possible shortcomings of the general control of the body's RC structure are:

Organizational Controls

Employee accounting; there are many functions of this nature that should be isolated, for

example, from costs, sales records, generalization of inventory and information

management. This could cause an incompatibility between AC and client. In addition, the

President / Owner will not review reports in support of the exchange (Australia, 2007).

Documentation checks

The RC documents are not complete:

Multiple duplicates of sales order (CO) records are needed because one is not enough. In

the unlikely event that the accountant simply instructs CO data on the phone, an

operations manager seems likely to be writing inaccurate data, which could lead to a

misunderstanding.

For telephone request, there is no specific CO reported by the customer and Registered

Identification Order (OA), in this way the exchange does not have a strong authority and

lack of evidence.

Resource responsibility checks

Employees insist on Shipping to organize (create) goods from the creation of warehouse /

place when AC or the President / Owner give a verbal request, at least not verified, to

make sure that (report) is identified by the shipping staff at the time of the transfer . This

is risky as it is likely to produce results but there is no evidence (Ebert and Griffin, 2005).

Executives exercise controls

There were no administrative strategies regarding the RC, for example credit approval, account

privileges, contracts and collection methods; this can cause inconveniences as the group

continues to develop and starts using more people to manage the RC exercises. With the non-

emergence of manufacturing methods, RC methods can be rendered in conditions of uncertainty

and inconsistency. Also, if the accountant leaves, the organization will have difficulty preparing

the new employee to replace him.

President / Owner will not review reports in support of the exchange (Australia, 2007).

Documentation checks

The RC documents are not complete:

Multiple duplicates of sales order (CO) records are needed because one is not enough. In

the unlikely event that the accountant simply instructs CO data on the phone, an

operations manager seems likely to be writing inaccurate data, which could lead to a

misunderstanding.

For telephone request, there is no specific CO reported by the customer and Registered

Identification Order (OA), in this way the exchange does not have a strong authority and

lack of evidence.

Resource responsibility checks

Employees insist on Shipping to organize (create) goods from the creation of warehouse /

place when AC or the President / Owner give a verbal request, at least not verified, to

make sure that (report) is identified by the shipping staff at the time of the transfer . This

is risky as it is likely to produce results but there is no evidence (Ebert and Griffin, 2005).

Executives exercise controls

There were no administrative strategies regarding the RC, for example credit approval, account

privileges, contracts and collection methods; this can cause inconveniences as the group

continues to develop and starts using more people to manage the RC exercises. With the non-

emergence of manufacturing methods, RC methods can be rendered in conditions of uncertainty

and inconsistency. Also, if the accountant leaves, the organization will have difficulty preparing

the new employee to replace him.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The possible shortcomings of the general control of the body's EC framework are:

Organizational Controls

The staff involved in receiving, purchasing and checking the account has many

responsibilities, which should be separated, for example, from inventory control, credit

liabilities and information management. Most of the CE modules are completed by R, P

and IC personnel. This could cause an irresponsible position.

Document checks

CE documents are not complete as there are no adequate documents of:

Purchase application, which indicates that it is not allowed in the application

configuration.

Purchase request, which indicates that there is no official officer for the exchange.

Report received. This is critical for stock trading and further analysis.

Internal controls suggested

For the RC framework:

• There should be complex administrative arrangements regarding RC, such as credit agreement,

account privileges and exchange and collection mechanisms.

• Revisions must be made in accordance with the procedures and procedures relating to

bargaining and receipts (with a probability that they have been established).

• Exchange mails, such as the cash receipt diary and redemption records, must be set periodically

to provide audit trail and audit template. For the

CE Framework:

• Management strategies should be in place in relation to purchase limits, purchasing returns and

the method of purchasing and distributing cash.

• Purchases and cash payment strategies and agreements should be reviewed (just in case they

are negotiated).

Organizational Controls

The staff involved in receiving, purchasing and checking the account has many

responsibilities, which should be separated, for example, from inventory control, credit

liabilities and information management. Most of the CE modules are completed by R, P

and IC personnel. This could cause an irresponsible position.

Document checks

CE documents are not complete as there are no adequate documents of:

Purchase application, which indicates that it is not allowed in the application

configuration.

Purchase request, which indicates that there is no official officer for the exchange.

Report received. This is critical for stock trading and further analysis.

Internal controls suggested

For the RC framework:

• There should be complex administrative arrangements regarding RC, such as credit agreement,

account privileges and exchange and collection mechanisms.

• Revisions must be made in accordance with the procedures and procedures relating to

bargaining and receipts (with a probability that they have been established).

• Exchange mails, such as the cash receipt diary and redemption records, must be set periodically

to provide audit trail and audit template. For the

CE Framework:

• Management strategies should be in place in relation to purchase limits, purchasing returns and

the method of purchasing and distributing cash.

• Purchases and cash payment strategies and agreements should be reviewed (just in case they

are negotiated).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

• Managers periodically monitor audits, check for violations and reports regarding mobile

accounts.

• Monitoring such as stock surprises must be observed in order to prevent stock theft and to

prevent staff. The recommendations of these internal controls are in line with the control and

audit functions of the COSO internal control module.

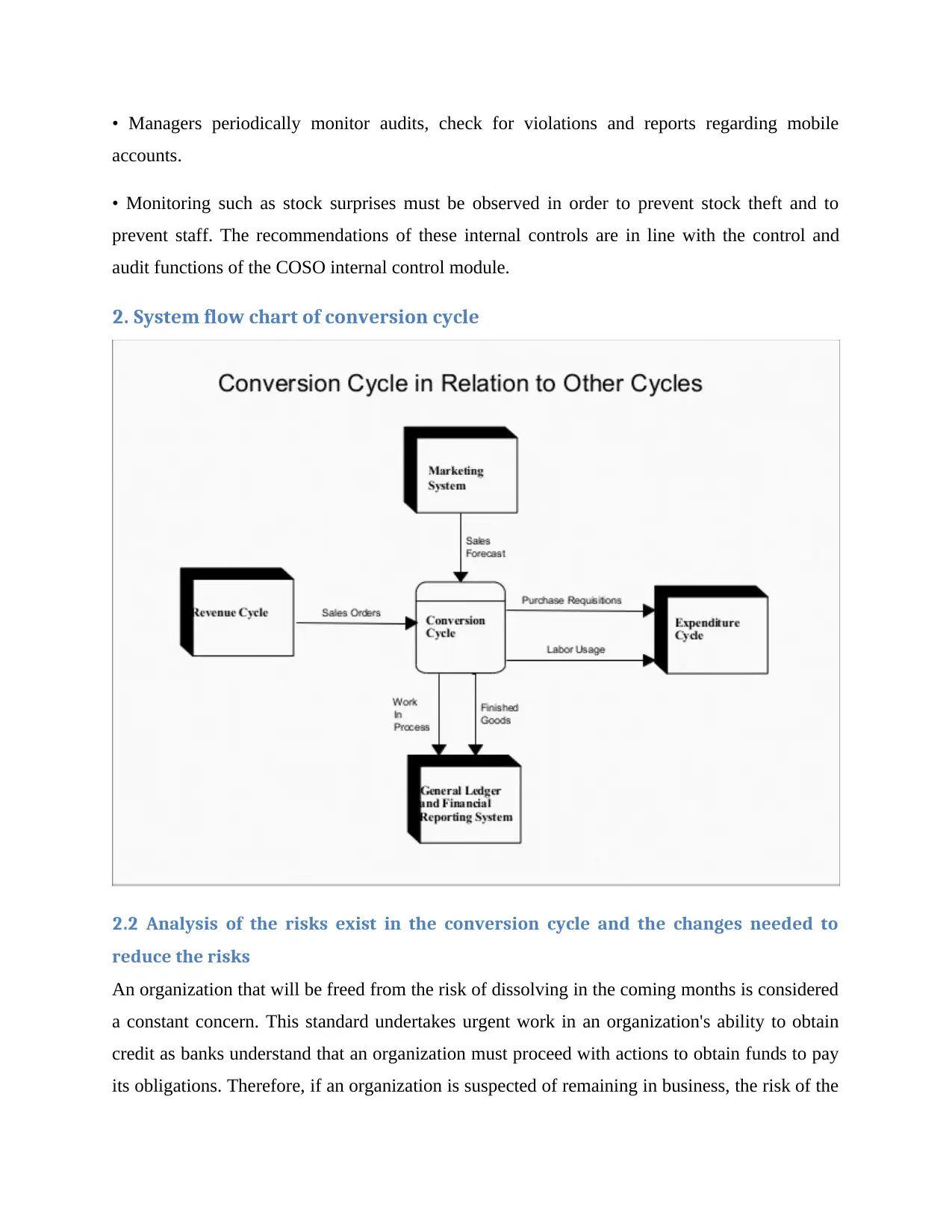

2. System flow chart of conversion cycle

2.2 Analysis of the risks exist in the conversion cycle and the changes needed to

reduce the risks

An organization that will be freed from the risk of dissolving in the coming months is considered

a constant concern. This standard undertakes urgent work in an organization's ability to obtain

credit as banks understand that an organization must proceed with actions to obtain funds to pay

its obligations. Therefore, if an organization is suspected of remaining in business, the risk of the

accounts.

• Monitoring such as stock surprises must be observed in order to prevent stock theft and to

prevent staff. The recommendations of these internal controls are in line with the control and

audit functions of the COSO internal control module.

2. System flow chart of conversion cycle

2.2 Analysis of the risks exist in the conversion cycle and the changes needed to

reduce the risks

An organization that will be freed from the risk of dissolving in the coming months is considered

a constant concern. This standard undertakes urgent work in an organization's ability to obtain

credit as banks understand that an organization must proceed with actions to obtain funds to pay

its obligations. Therefore, if an organization is suspected of remaining in business, the risk of the

organization entering into its credit agreements increases. It also appears that it is difficult for the

organization to obtain major credit or credit. This risk is reflected halfway through a group's cash

conversion cycle (Hoggett and et.al., 2006).

Types of risks involved in cash conversion cycle:

1. Delay in Payment: The real problem starts when longer customers pay and AR DO increases

dramatically. Perhaps the worst recipe for this situation is that the organization is financing the

hole by getting from the banks. This is risky, given that the new role is not part of the activities

or investments, but rather the attention of tenants. Talking to the agency's tenants and

maximizing the AP DO may be a good idea to manage the expansion in the DO DO. Sadly, this

just shifts distress down the line. The result is a series of organizations that are attracted to

money and work solely to pay their tenants (Head and Herman, 2002).

2. Decline in Liquidity: A reasonable assessment of group liquidity is important because

reduced liquidity leads to an increase in liquidity risk. Financial experts and experts are

committed to an organization's ability to make money and have sufficient funds available to meet

normal needs, and vendors are committed to determining whether an organization usually has the

money to pay for the goods that have been shipped. to buy. Liquidity is also a requirement for

external assessors for responsibilities, for example by examining the issues at stake.

3. Void Invoices: A company is contacted by someone who pretends to represent a supplier /

service provider / creditor. Contact can be made by phone, letter, fax or e-mail. The scammer

asks that the bank details for the payment (e.g. details of the bank account recipient) be changed

for the next invoices. The suggested new account is actually controlled by the scammer.

4. Lack of inputs: Absence of data sources e.g. derived materials and components for operating

procedures, e.g. creation line.

5. Deficiency inventory: Depression stocks can occur due to presented problems, poor business

forecasts and disappointing stocks should be regular limited intensity for sale. For example, a

design brand offers a shoe model in 3 shapes. A month after the start of the season, shadow is

almost never sold and should be limited to cancellations for the next series.

organization to obtain major credit or credit. This risk is reflected halfway through a group's cash

conversion cycle (Hoggett and et.al., 2006).

Types of risks involved in cash conversion cycle:

1. Delay in Payment: The real problem starts when longer customers pay and AR DO increases

dramatically. Perhaps the worst recipe for this situation is that the organization is financing the

hole by getting from the banks. This is risky, given that the new role is not part of the activities

or investments, but rather the attention of tenants. Talking to the agency's tenants and

maximizing the AP DO may be a good idea to manage the expansion in the DO DO. Sadly, this

just shifts distress down the line. The result is a series of organizations that are attracted to

money and work solely to pay their tenants (Head and Herman, 2002).

2. Decline in Liquidity: A reasonable assessment of group liquidity is important because

reduced liquidity leads to an increase in liquidity risk. Financial experts and experts are

committed to an organization's ability to make money and have sufficient funds available to meet

normal needs, and vendors are committed to determining whether an organization usually has the

money to pay for the goods that have been shipped. to buy. Liquidity is also a requirement for

external assessors for responsibilities, for example by examining the issues at stake.

3. Void Invoices: A company is contacted by someone who pretends to represent a supplier /

service provider / creditor. Contact can be made by phone, letter, fax or e-mail. The scammer

asks that the bank details for the payment (e.g. details of the bank account recipient) be changed

for the next invoices. The suggested new account is actually controlled by the scammer.

4. Lack of inputs: Absence of data sources e.g. derived materials and components for operating

procedures, e.g. creation line.

5. Deficiency inventory: Depression stocks can occur due to presented problems, poor business

forecasts and disappointing stocks should be regular limited intensity for sale. For example, a

design brand offers a shoe model in 3 shapes. A month after the start of the season, shadow is

almost never sold and should be limited to cancellations for the next series.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6. Acutely sharpened: An article is generating more interest than expected and is sold out

immediately. This can talk about lost income opportunity if the window for offers is limited. For

example, a famous toy at Christmas could create a buzz that will crumble in January.

7. A worthy loss: Every day there is an object, part or material sitting on the rack that can be

found inexpensively. The value may decline rapidly due to other competitive inputs or non-

quantifiable transportation costs.

8. Natural hazards: Check for faults that lead to inaccurate stock analysis. For example, a

company discovers a large number of dollars loses action when playing the year-end review.

9. Channel index: Stocks transported to transport facilities speak of an unusual type of stock

risk. Occasionally have supporters the ability to return unsold shares, increasing profits when

something doesn't sell. Insufficient stocks in a channel can also damage future contracts when

subscribers cease applying.

Changes needed to reduce the risks/ Risk management:

Focus on seeing the end-to-end supply chain:

The slippery thing about flexible chains is that your sphere of influence includes only exercises

for suppliers, your organization and your customers. It is what your suppliers, customers, etc.

that are permanently excluded from the condition (Laudon and Laudon, 2004).

1. Simplify the inventory:

Perhaps one of the most convincing companies for flexible chain starters is adjusting the size of

the stock so that it responds quickly and limits the amount of money tied to resources. To load

from the warehouse and inventory while still being loaded enough to meet the customer's needs,

start by going through these methods from beginning to end:

• Reduce the multilateral nature of the article plan

• Manage supplier delivery times

• Adoption of coordination procedures (eg JIT and VMI)

immediately. This can talk about lost income opportunity if the window for offers is limited. For

example, a famous toy at Christmas could create a buzz that will crumble in January.

7. A worthy loss: Every day there is an object, part or material sitting on the rack that can be

found inexpensively. The value may decline rapidly due to other competitive inputs or non-

quantifiable transportation costs.

8. Natural hazards: Check for faults that lead to inaccurate stock analysis. For example, a

company discovers a large number of dollars loses action when playing the year-end review.

9. Channel index: Stocks transported to transport facilities speak of an unusual type of stock

risk. Occasionally have supporters the ability to return unsold shares, increasing profits when

something doesn't sell. Insufficient stocks in a channel can also damage future contracts when

subscribers cease applying.

Changes needed to reduce the risks/ Risk management:

Focus on seeing the end-to-end supply chain:

The slippery thing about flexible chains is that your sphere of influence includes only exercises

for suppliers, your organization and your customers. It is what your suppliers, customers, etc.

that are permanently excluded from the condition (Laudon and Laudon, 2004).

1. Simplify the inventory:

Perhaps one of the most convincing companies for flexible chain starters is adjusting the size of

the stock so that it responds quickly and limits the amount of money tied to resources. To load

from the warehouse and inventory while still being loaded enough to meet the customer's needs,

start by going through these methods from beginning to end:

• Reduce the multilateral nature of the article plan

• Manage supplier delivery times

• Adoption of coordination procedures (eg JIT and VMI)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

• Eliminate people from unnecessary channel

• Improve tender measurement and application organization.

2. Increase the buying cycle:

Flexible (and inevitably) risk-taking risks can pose some formidable obstacles in the time it takes

for suppliers to pay. When trying to lengthen the time to half the installments (to keep as much

money as accessible as you would expect), the impacts on the income of the installment

providers can be capricious (McLeod and Schell, 2001).

In any case, the downside, an administrative understanding and the possible limits of the first

bets can help you reorder the amount you have in your pocket. Find a position in these regions of

your flexible chain:

• Monitor the stability of the contracts to limit the installments more quickly than the established

conditions

• Identification forms and workflow receipt quotas

• Establish a supplier base for a more competitive impact in contract exchanges

3. Advance Order to Money Circle:

The billing method is variable, depending on the time, dependence and accuracy. Finally, when

the client begins to prepare behavioral therapy for a hobby, many have entered the procedure to

ensure adequate and accurate treatment (Romney and Steinbart, 2006).

Limiting this request to collection times is difficult while maintaining a high production rate,

reliable behavior in time and precision of disposal without failures. Try dividing your approach

into these small areas to see where you might have a chance to start shortening your time from

order to money:

• Automatically submit billing forms (speed and accuracy).

• Actively pursues intuitive discoveries and underlying causes.

• Importance with the extent of the credit conditions offered to the various customers.

• Improve tender measurement and application organization.

2. Increase the buying cycle:

Flexible (and inevitably) risk-taking risks can pose some formidable obstacles in the time it takes

for suppliers to pay. When trying to lengthen the time to half the installments (to keep as much

money as accessible as you would expect), the impacts on the income of the installment

providers can be capricious (McLeod and Schell, 2001).

In any case, the downside, an administrative understanding and the possible limits of the first

bets can help you reorder the amount you have in your pocket. Find a position in these regions of

your flexible chain:

• Monitor the stability of the contracts to limit the installments more quickly than the established

conditions

• Identification forms and workflow receipt quotas

• Establish a supplier base for a more competitive impact in contract exchanges

3. Advance Order to Money Circle:

The billing method is variable, depending on the time, dependence and accuracy. Finally, when

the client begins to prepare behavioral therapy for a hobby, many have entered the procedure to

ensure adequate and accurate treatment (Romney and Steinbart, 2006).

Limiting this request to collection times is difficult while maintaining a high production rate,

reliable behavior in time and precision of disposal without failures. Try dividing your approach

into these small areas to see where you might have a chance to start shortening your time from

order to money:

• Automatically submit billing forms (speed and accuracy).

• Actively pursues intuitive discoveries and underlying causes.

• Importance with the extent of the credit conditions offered to the various customers.

CONCLUSION

Hence, from the above analysis it can be concluded that; t he organization should update its

documentation so that there is better control and consistent quality of business exchange.

Similarly, appropriate isolation of responsibilities should be updated within the organization to

prevent hatred and theft for employees. He is also invited to lead the reviews. In addition, make

specific recommendations, which rely on the COSO integrated internal control framework,

created by the creator.

Hence, from the above analysis it can be concluded that; t he organization should update its

documentation so that there is better control and consistent quality of business exchange.

Similarly, appropriate isolation of responsibilities should be updated within the organization to

prevent hatred and theft for employees. He is also invited to lead the reviews. In addition, make

specific recommendations, which rely on the COSO integrated internal control framework,

created by the creator.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.