Paradise Industries: Internal Control Weaknesses Case Study

VerifiedAdded on 2023/01/11

|12

|3226

|38

Case Study

AI Summary

This case study analyzes Paradise Industries' expenditure and conversion cycles, identifying weaknesses in internal controls and assessing associated risks. The analysis begins with a system flow chart of the expenditure cycle, followed by an examination of its physical internal control weaknesses, such as the infringement of duties within the purchasing and inventory departments, and weaknesses in documentation and commercial actions. The study then transitions to the conversion cycle, assessing the risks involved, including payment delays, liquidity decline, and fraudulent invoices. Recommendations for improving internal controls in both cycles are provided, aligning with COSO internal control modules. The case study emphasizes the importance of separating duties, completing documentation, and implementing management strategies to mitigate risks and enhance operational efficiency. The conclusion summarizes the key findings and recommendations, providing a comprehensive overview of the company's financial and operational challenges and suggesting improvements.

Case Study – Paradise

Industries

Industries

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

SYSTEM FLOW CHART FOR EXPENDITURE CYCLE...........................................................3

Analysis of physical internal control weaknesses in the expenditure cycle................................4

SYSTEM FLOW CHART FOR CONVERSION CYCLE.............................................................8

Analysis of the risks exist in the conversion cycle and the changes needed to reduce the risks. 8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

SYSTEM FLOW CHART FOR EXPENDITURE CYCLE...........................................................3

Analysis of physical internal control weaknesses in the expenditure cycle................................4

SYSTEM FLOW CHART FOR CONVERSION CYCLE.............................................................8

Analysis of the risks exist in the conversion cycle and the changes needed to reduce the risks. 8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

The strategic information system is developed regarding the response to the corporate

business initiatives. It is used for providing advantage of competition to the specific organisation

as it delivers many services at lower prices and differentiated way that are used in order to

concentrate on demanding market session which is an innovation. Moreover it is an important

feature within the corporate and information technology world which is useful for the company

to store a locate move and process their data information in order to develop and receive it

(Rezvani, Dong and Khosravi, 2017). Along with this it is also useful in enabling various tools

and techniques that are helpful for the company to apply specific metrics and analytical tools

regarding the information function and also allows them to analyse the resourceful opportunities

for the growth and operations of supply efficiency.

Despite from this the project is based on two prominent operating concepts that is

expenditure cycle and cash conversion cycle. In this the cash conversion cycle describes

regarding the time period and risk factor which is concerned with the conversion of final goods

into cash and also describe the procedure of whole cycle. Furthermore, the expenditure cycle

flowchart describe when and how the buying order is placed and how many copies are need to be

distributed in order to start the purchasing order as it discuss regarding the treatment of work in

progress status. Along with this it also includes the discussion of weakness of the current model

of procurement procedure which is discussed with proper recommendation.

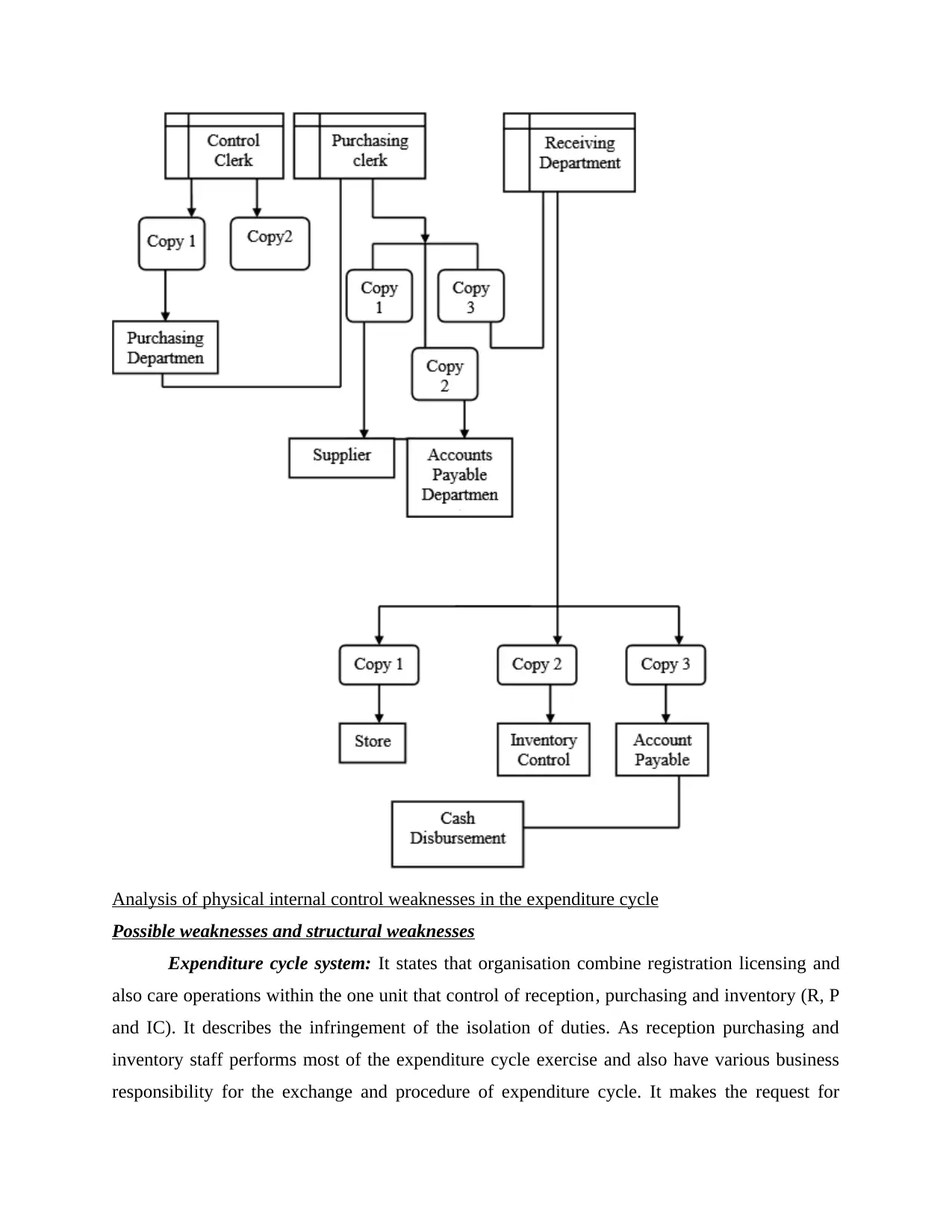

SYSTEM FLOW CHART FOR EXPENDITURE CYCLE

It is the centralised system with various terminals located in different departments. In this

the terminals are networked to various digital accounting records and computer applications that

are hosted on the server of data processing department. Along with this the data processing

Centre scans the inventory records in order to look the prominent items that should be

replenished (Shanks and et. al., 2018). Moreover the computer application is considered as the

data processing department that automatically scans the accounts that are payable to the

subsidiary files that are due for the payment. In this context it required a flow diagram in order to

understand it more briefly.

The strategic information system is developed regarding the response to the corporate

business initiatives. It is used for providing advantage of competition to the specific organisation

as it delivers many services at lower prices and differentiated way that are used in order to

concentrate on demanding market session which is an innovation. Moreover it is an important

feature within the corporate and information technology world which is useful for the company

to store a locate move and process their data information in order to develop and receive it

(Rezvani, Dong and Khosravi, 2017). Along with this it is also useful in enabling various tools

and techniques that are helpful for the company to apply specific metrics and analytical tools

regarding the information function and also allows them to analyse the resourceful opportunities

for the growth and operations of supply efficiency.

Despite from this the project is based on two prominent operating concepts that is

expenditure cycle and cash conversion cycle. In this the cash conversion cycle describes

regarding the time period and risk factor which is concerned with the conversion of final goods

into cash and also describe the procedure of whole cycle. Furthermore, the expenditure cycle

flowchart describe when and how the buying order is placed and how many copies are need to be

distributed in order to start the purchasing order as it discuss regarding the treatment of work in

progress status. Along with this it also includes the discussion of weakness of the current model

of procurement procedure which is discussed with proper recommendation.

SYSTEM FLOW CHART FOR EXPENDITURE CYCLE

It is the centralised system with various terminals located in different departments. In this

the terminals are networked to various digital accounting records and computer applications that

are hosted on the server of data processing department. Along with this the data processing

Centre scans the inventory records in order to look the prominent items that should be

replenished (Shanks and et. al., 2018). Moreover the computer application is considered as the

data processing department that automatically scans the accounts that are payable to the

subsidiary files that are due for the payment. In this context it required a flow diagram in order to

understand it more briefly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Analysis of physical internal control weaknesses in the expenditure cycle

Possible weaknesses and structural weaknesses

Expenditure cycle system: It states that organisation combine registration licensing and

also care operations within the one unit that control of reception, purchasing and inventory (R, P

and IC). It describes the infringement of the isolation of duties. As reception purchasing and

inventory staff performs most of the expenditure cycle exercise and also have various business

responsibility for the exchange and procedure of expenditure cycle. It makes the request for

Possible weaknesses and structural weaknesses

Expenditure cycle system: It states that organisation combine registration licensing and

also care operations within the one unit that control of reception, purchasing and inventory (R, P

and IC). It describes the infringement of the isolation of duties. As reception purchasing and

inventory staff performs most of the expenditure cycle exercise and also have various business

responsibility for the exchange and procedure of expenditure cycle. It makes the request for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

receiving the organised Returns determine and keep the records within the stock by publishing

the account payable data that is achieved (Ogiela, 2016). It is where the wrong activities can

occur. For models the reception purchasing and inventory cost staff has inconsistent position

within the Merchant and also mislead the owner by which they can take and Scheduled soup and

nobody will pay prominent attention.

Income cycle system: In this context the accountant AC takes all the work of RC and also

gets overloaded because of the business activities specifically RC that exchange the whole

procedure. As RC is the recipient and approve the request of the customer and also prepare the

origin archives. For instance tender packaging and slip orders that are useful in maintaining the

general inventory and also include the invoices of individual purchase. Therefore, it describes the

wrong activities which arise (Kummer and Schmiedel, 2016). By considering the model CA have

an unbalanced position with the prominent customers and also mislead the owner and President

which leads to incur more prominent cost for their customers and also keep the records in terms

of reports for the exchange of using the standard charges.

Weaknesses of documentation and commercial actions

It describes the significant pitfalls of the documentation and commercial actions which

describe the technical activities in order to spend the cycle regarding the giant eggplants are:

It includes the good numbers for the CE archives which include the context of the various

numbers of registrations. Moreover, there will be no issues regarding the splitting of

outputs report and production specifically when their company start executing the new

accounting framework.

At the time of functioning of the contract request the accountant directly support the

request without analyzing the credit records of customers which describe that customer

control record and the various sources of accounting data of customer. Therefore, it

describe that the client has not yet given the prominent effort towards the company.

Internal control weaknesses

It includes the possible shortcomings regarding the general control of the body of RC

structure:

Organizational controls

It describes the employee accounting which include various functions of the nature that

must be cut off like the cost sales records generalization of Information and inventory

the account payable data that is achieved (Ogiela, 2016). It is where the wrong activities can

occur. For models the reception purchasing and inventory cost staff has inconsistent position

within the Merchant and also mislead the owner by which they can take and Scheduled soup and

nobody will pay prominent attention.

Income cycle system: In this context the accountant AC takes all the work of RC and also

gets overloaded because of the business activities specifically RC that exchange the whole

procedure. As RC is the recipient and approve the request of the customer and also prepare the

origin archives. For instance tender packaging and slip orders that are useful in maintaining the

general inventory and also include the invoices of individual purchase. Therefore, it describes the

wrong activities which arise (Kummer and Schmiedel, 2016). By considering the model CA have

an unbalanced position with the prominent customers and also mislead the owner and President

which leads to incur more prominent cost for their customers and also keep the records in terms

of reports for the exchange of using the standard charges.

Weaknesses of documentation and commercial actions

It describes the significant pitfalls of the documentation and commercial actions which

describe the technical activities in order to spend the cycle regarding the giant eggplants are:

It includes the good numbers for the CE archives which include the context of the various

numbers of registrations. Moreover, there will be no issues regarding the splitting of

outputs report and production specifically when their company start executing the new

accounting framework.

At the time of functioning of the contract request the accountant directly support the

request without analyzing the credit records of customers which describe that customer

control record and the various sources of accounting data of customer. Therefore, it

describe that the client has not yet given the prominent effort towards the company.

Internal control weaknesses

It includes the possible shortcomings regarding the general control of the body of RC

structure:

Organizational controls

It describes the employee accounting which include various functions of the nature that

must be cut off like the cost sales records generalization of Information and inventory

management. This can arise because of incompatibility among AC and client. Along with this the

owner and President will not oversee the reports regarding the support of exchange (Cassidy,

2016).

Documentation checks

The documents of RC are not complete:

It includes the various duplicates of sales order (CO) records that are required as first one

is not sufficient full stop in that case the event that the accountant simply guide toCO data

on the telephone describe the operations manager seems like to write and have the

inaccurate information which can leads to develop misunderstanding among them.

In this context the phone request describe that there is no particular CO reported by the

client and registered identification order. In this context the manner includes the

exchange which does not have the strong authority and also have shortage of evidence.

Resource responsibility checks

It describe that employees insist on creating and shipping the organised commodities

from the creation of warehouse when AC and the president give the prominent verbal request. In

that case it is not verified to ensure that the report is evaluated by the shipping staff during

transferring the things (Pearlson, Saunders and Galletta, 2019). It is considered as risky which is

likely to develop result as there is no significant evidence.

Executives exercise controls

It depicts that there is no administrator strategies concerning the RC like providing credit

approval account privileges collection methods and contracts which can arise inconvenience for

the group and continuous to develop as it use many people to manage the RC activities.

Moreover it also describe the non emergence of operational methods include the RC methods

that can be provided in various conditions that are uncertain and inconsistent. Along with this if

the accountant leaves the company then they face various complexities in order to prepare the

employees to replace the accountant (Fayoumi and Loucopoulos, 2016).

The probable shortcomings of the general control for the EC framework:

Organizational controls

It describes that the employees are involved in receiving checking and purchasing the

accounts which is responsibility and should be separated like from the inventory control

information system and credit liabilities. It describe that the CE modules are completed by the

owner and President will not oversee the reports regarding the support of exchange (Cassidy,

2016).

Documentation checks

The documents of RC are not complete:

It includes the various duplicates of sales order (CO) records that are required as first one

is not sufficient full stop in that case the event that the accountant simply guide toCO data

on the telephone describe the operations manager seems like to write and have the

inaccurate information which can leads to develop misunderstanding among them.

In this context the phone request describe that there is no particular CO reported by the

client and registered identification order. In this context the manner includes the

exchange which does not have the strong authority and also have shortage of evidence.

Resource responsibility checks

It describe that employees insist on creating and shipping the organised commodities

from the creation of warehouse when AC and the president give the prominent verbal request. In

that case it is not verified to ensure that the report is evaluated by the shipping staff during

transferring the things (Pearlson, Saunders and Galletta, 2019). It is considered as risky which is

likely to develop result as there is no significant evidence.

Executives exercise controls

It depicts that there is no administrator strategies concerning the RC like providing credit

approval account privileges collection methods and contracts which can arise inconvenience for

the group and continuous to develop as it use many people to manage the RC activities.

Moreover it also describe the non emergence of operational methods include the RC methods

that can be provided in various conditions that are uncertain and inconsistent. Along with this if

the accountant leaves the company then they face various complexities in order to prepare the

employees to replace the accountant (Fayoumi and Loucopoulos, 2016).

The probable shortcomings of the general control for the EC framework:

Organizational controls

It describes that the employees are involved in receiving checking and purchasing the

accounts which is responsibility and should be separated like from the inventory control

information system and credit liabilities. It describe that the CE modules are completed by the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reception purchasing and inventory control people as it can arise because of irresponsible

position.

Document checks

CE documents are not complete because there are no prominent and adequate documents

provided:

Purchase application which describe that it is not permitted for the application

configuration.

Purchase request describe that there is no official individual for the exchange.

Report received considered as the critical think for the stock trading and further

determination.

Internal controls suggested

RC framework:

It describes the complexity of the administrative arrangement concerning RC including

the current agreement exchange collection mechanism and account privileges.

Along with this provision must be made according with the proper process that is

concerned with receipts and negotiation.

It also include the exchanging of emails considering the cash received diary and

redemption records that should be set on the periodical basis in order to offer the audit

template and trail.

CE framework:

It includes the management strategies that are concerned with the purchasing limits

returns and the method of distributing and purchasing cash.

Moreover cash payment and purchase strategies describe the agreement that should be

reviewed in terms of negotiation.

In this context managers periodically manner monitor audits and order to check the

violation and also report it regarding the mobile accounts.

It includes monitoring of stock that should be observed in order to prevent the theft of

stock and prevent their employees as well. Recommendation for the internal control

includes the in client with the control and Audit functions of COSO internal control

module.

position.

Document checks

CE documents are not complete because there are no prominent and adequate documents

provided:

Purchase application which describe that it is not permitted for the application

configuration.

Purchase request describe that there is no official individual for the exchange.

Report received considered as the critical think for the stock trading and further

determination.

Internal controls suggested

RC framework:

It describes the complexity of the administrative arrangement concerning RC including

the current agreement exchange collection mechanism and account privileges.

Along with this provision must be made according with the proper process that is

concerned with receipts and negotiation.

It also include the exchanging of emails considering the cash received diary and

redemption records that should be set on the periodical basis in order to offer the audit

template and trail.

CE framework:

It includes the management strategies that are concerned with the purchasing limits

returns and the method of distributing and purchasing cash.

Moreover cash payment and purchase strategies describe the agreement that should be

reviewed in terms of negotiation.

In this context managers periodically manner monitor audits and order to check the

violation and also report it regarding the mobile accounts.

It includes monitoring of stock that should be observed in order to prevent the theft of

stock and prevent their employees as well. Recommendation for the internal control

includes the in client with the control and Audit functions of COSO internal control

module.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

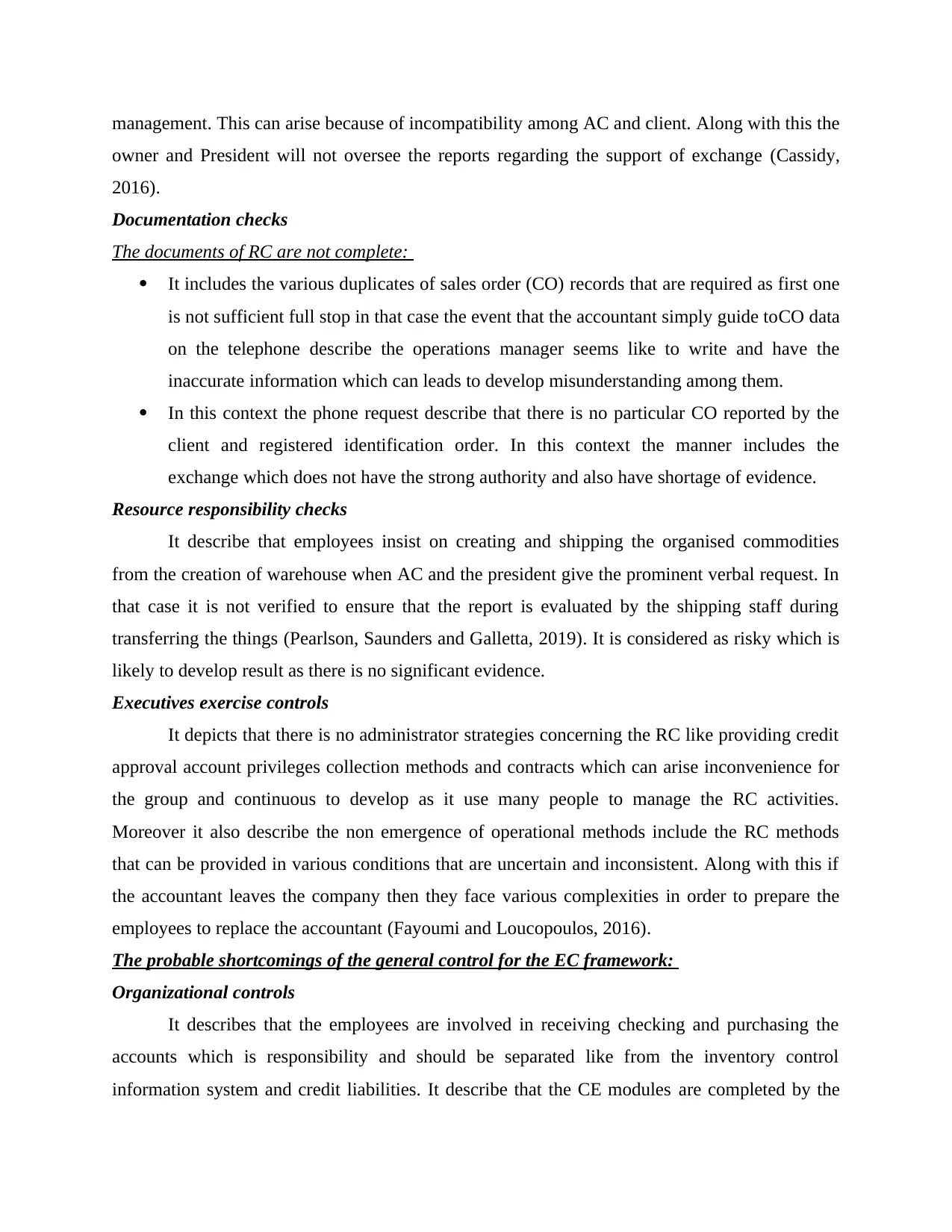

SYSTEM FLOW CHART FOR CONVERSION CYCLE

Analysis of the risks exist in the conversion cycle and the changes needed to reduce the risks

As per this the company is free from the risk factor regarding dissolving in coming months

that is related with constant concern. In this context it describe the standard that undertakes the

urgent work for the ability of Organisation in order to obtain the credits from the Financial

Institutions and also understand that company need to proceed with their activities to achieve

their funds to pay the obligations (Sun, Strang and Firmin, 2017). In this context the organisation

need to suspect it for the remaining business by which the risk of the company enter from the

side of credit agreement that increases. Therefore the risk reflect the half way a of the cash

conversion cycle.

Kinds of risk involved in cash conversion cycle

Analysis of the risks exist in the conversion cycle and the changes needed to reduce the risks

As per this the company is free from the risk factor regarding dissolving in coming months

that is related with constant concern. In this context it describe the standard that undertakes the

urgent work for the ability of Organisation in order to obtain the credits from the Financial

Institutions and also understand that company need to proceed with their activities to achieve

their funds to pay the obligations (Sun, Strang and Firmin, 2017). In this context the organisation

need to suspect it for the remaining business by which the risk of the company enter from the

side of credit agreement that increases. Therefore the risk reflect the half way a of the cash

conversion cycle.

Kinds of risk involved in cash conversion cycle

Delay in payment: It describes the real issues that begin when the customers pay AR DO

that increases radically. Despite from this the worst thing of this situation is that company is

financing as a whole bye getting capital from the banks. It is considered as the risky type as it

provides the new role which is not the part of activities or investment but also pay the attention

of the tenants (Appelbaum and et. al., 2017). By considering the tenants of agency and also

increase the AP DO which is considered as the best idea in order to manage the expansion for the

DO DO. At last it just move the displaced down from the line which results in a series of

organisation that are attracted towards the money and work exclusively in order to pay their

tenants.

Decline in liquidity: It includes the reasonable assessment of group liquidity that is

significant as it leads to reduce the liquidity which describes an increment in liquidity risk. In

this context the financial exports are dedicated to the ability of Organization in order to make

money and also have sufficient funds that are available to match the normal needs and also

determine that the organization usually pay their money for the goods that has been shipped. In

order to purchase the liquidity its need the external accessories for the responsibility like

examining the problems that are at stake (Draijer, 2020).

Void invoices: It described that company is contacted by individual who pretend to

become the represent as a supplier creditor and service provider. In this context the contact

should be made by letter email fax or by telephone. Moreover the scammer asks the bank details

for the payment that has been changed for the next invoice full stop therefore it is suggested that

new account is managed by the scammer.

Lack of inputs: It includes the lack of data sources like derived materials and

components in order to operate the procedure for instance creation line.

Deficiency inventory: It describe the depressing stock which occur because of the

existing issues including poor business forecasting and unsatisfactory stock which is regular and

Limited for the sale. For instance, it describes the design that offer a brand including the shoe

model within few prominent shapes.

Worthy loss: It describes the regular object including the part of material that is sitting on

the frame that is found inexpensively (Archer-Brown and Kietzmann, 2018). Along with this the

value can be decline on the frequent basis because of the other competitive inputs and non

quantifiable transportation cost.

that increases radically. Despite from this the worst thing of this situation is that company is

financing as a whole bye getting capital from the banks. It is considered as the risky type as it

provides the new role which is not the part of activities or investment but also pay the attention

of the tenants (Appelbaum and et. al., 2017). By considering the tenants of agency and also

increase the AP DO which is considered as the best idea in order to manage the expansion for the

DO DO. At last it just move the displaced down from the line which results in a series of

organisation that are attracted towards the money and work exclusively in order to pay their

tenants.

Decline in liquidity: It includes the reasonable assessment of group liquidity that is

significant as it leads to reduce the liquidity which describes an increment in liquidity risk. In

this context the financial exports are dedicated to the ability of Organization in order to make

money and also have sufficient funds that are available to match the normal needs and also

determine that the organization usually pay their money for the goods that has been shipped. In

order to purchase the liquidity its need the external accessories for the responsibility like

examining the problems that are at stake (Draijer, 2020).

Void invoices: It described that company is contacted by individual who pretend to

become the represent as a supplier creditor and service provider. In this context the contact

should be made by letter email fax or by telephone. Moreover the scammer asks the bank details

for the payment that has been changed for the next invoice full stop therefore it is suggested that

new account is managed by the scammer.

Lack of inputs: It includes the lack of data sources like derived materials and

components in order to operate the procedure for instance creation line.

Deficiency inventory: It describe the depressing stock which occur because of the

existing issues including poor business forecasting and unsatisfactory stock which is regular and

Limited for the sale. For instance, it describes the design that offer a brand including the shoe

model within few prominent shapes.

Worthy loss: It describes the regular object including the part of material that is sitting on

the frame that is found inexpensively (Archer-Brown and Kietzmann, 2018). Along with this the

value can be decline on the frequent basis because of the other competitive inputs and non

quantifiable transportation cost.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Natural hazards: In describe the check for the fault that can arise because of inaccurate

stock determination like company discovers the large number of dollar loss activities while

analysing the year end review.

Changing needs to eliminate the risk management

Put emphasis on observing the end to end supply chain:

It describes the crazy things which are concerned with the flexible change which

influence the sphere considering the prominent exercise for the Suppliers Company and

customers. It described that the customers and suppliers are the permanent and excluded from the

conditions of business.

Simplify the inventory: It describe the most convincing company regarding the flexible chain

starter which include managing the size and stock for the quick response and limitations

guarding the amount of money that belongs from the resources (Rajnoha and et. al., 2016).

Moreover it describe the load from the stock room and inventory that is still loaded to match the

requirements of customers by going through the methods from start to end:

It reduces the joint nature of article plan. Manage prominent supplier and delivery of the

stipulated period of time.

Acceptance of coordinated procedure like JIT.

Reduce people from the unnecessary channel. Increase tender measurement and

application Association.

Increase the buying cycle: It includes the inevitable risk taking risk that describes the

frightened barriers at the time of taking the suppliers to pay. By considering the try to extend the

time at the half of the installment that influences the income regarding the installment that leads

to become impulsive for the providers (Shao, Feng and Hu, 2016). Moreover find a position for

the particular regions for the flexible chain:

Evaluation forms and workflow receipt area.

Set up a supplier base to become more competitive and impact the contract exchanges.

Evaluate the stability of the contracts to bind the installments rapidly rather than

established conditions.

Advance order to money circle: it is considered as the billing method that is variable and

depends on the time and accuracy. It describes that the client begins to prepare the behavior

therapy in order to enter the procedure to make sure the adequate and accurate treatment.

stock determination like company discovers the large number of dollar loss activities while

analysing the year end review.

Changing needs to eliminate the risk management

Put emphasis on observing the end to end supply chain:

It describes the crazy things which are concerned with the flexible change which

influence the sphere considering the prominent exercise for the Suppliers Company and

customers. It described that the customers and suppliers are the permanent and excluded from the

conditions of business.

Simplify the inventory: It describe the most convincing company regarding the flexible chain

starter which include managing the size and stock for the quick response and limitations

guarding the amount of money that belongs from the resources (Rajnoha and et. al., 2016).

Moreover it describe the load from the stock room and inventory that is still loaded to match the

requirements of customers by going through the methods from start to end:

It reduces the joint nature of article plan. Manage prominent supplier and delivery of the

stipulated period of time.

Acceptance of coordinated procedure like JIT.

Reduce people from the unnecessary channel. Increase tender measurement and

application Association.

Increase the buying cycle: It includes the inevitable risk taking risk that describes the

frightened barriers at the time of taking the suppliers to pay. By considering the try to extend the

time at the half of the installment that influences the income regarding the installment that leads

to become impulsive for the providers (Shao, Feng and Hu, 2016). Moreover find a position for

the particular regions for the flexible chain:

Evaluation forms and workflow receipt area.

Set up a supplier base to become more competitive and impact the contract exchanges.

Evaluate the stability of the contracts to bind the installments rapidly rather than

established conditions.

Advance order to money circle: it is considered as the billing method that is variable and

depends on the time and accuracy. It describes that the client begins to prepare the behavior

therapy in order to enter the procedure to make sure the adequate and accurate treatment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Moreover, the collection request depicts facing the difficult while managing the high production

rate that is reliable on the behavior and precision of the disposal without facing failure. It leads to

divide the approach into various small areas to analyze the prominent chants to begin the

shortening the time to order money:

Automatically submit the building forms including accuracy and speed.

Actively pursue intuitive discoveries and fundamental causes.

Significant for the extent of credit conditions offering to the various customers.

CONCLUSION

Therefore from the preceding information it is analysed that company need to update

regarding its documentation as because of this it prominently control and consistent the quality

of the exchange of Business Services. Along with this the suitable isolation of duties need to be

updated regarding the company in order to prevent the theft from the side of staff. In addition to

this it also make prominent recommendations that are relied on the COSO integrated internal

control Framework that is developed by the creator.

rate that is reliable on the behavior and precision of the disposal without facing failure. It leads to

divide the approach into various small areas to analyze the prominent chants to begin the

shortening the time to order money:

Automatically submit the building forms including accuracy and speed.

Actively pursue intuitive discoveries and fundamental causes.

Significant for the extent of credit conditions offering to the various customers.

CONCLUSION

Therefore from the preceding information it is analysed that company need to update

regarding its documentation as because of this it prominently control and consistent the quality

of the exchange of Business Services. Along with this the suitable isolation of duties need to be

updated regarding the company in order to prevent the theft from the side of staff. In addition to

this it also make prominent recommendations that are relied on the COSO integrated internal

control Framework that is developed by the creator.

REFERENCES

Books and Journals

Appelbaum, D and et. al., 2017. Impact of business analytics and enterprise systems on

managerial accounting. International Journal of Accounting Information Systems. 25.

pp.29-44.

Archer-Brown, C. and Kietzmann, J., 2018. Strategic knowledge management and enterprise

social media. Journal of Knowledge Management.

Cassidy, A., 2016. A practical guide to information systems strategic planning. CRC press.

Draijer, C., 2020. Best practices of business simulation with SAP R/3. Journal of Information

Systems Education. 15(3). p.5.

Fayoumi, A. and Loucopoulos, P., 2016. Conceptual modeling for the design of intelligent and

emergent information systems. Expert Systems with Applications. 59. pp.174-194.

Kummer, T.F. and Schmiedel, T., 2016. Reviewing the role of culture in strategic information

systems research: A call for prescriptive theorizing on culture

management. Communications of the Association for Information Systems. 38(1). p.5.

Ogiela, L., 2016. Cryptographic techniques of strategic data splitting and secure information

management. Pervasive and Mobile Computing. 29. pp.130-141.

Pearlson, K.E., Saunders, C.S. and Galletta, D.F., 2019. Managing and using information

systems: A strategic approach. John Wiley & Sons.

Rajnoha, R and et. al., 2016. Business intelligence as a key information and knowledge tool for

strategic business performance management. Economics and management.

Rezvani, A., Dong, L. and Khosravi, P., 2017. Promoting the continuing usage of strategic

information systems: The role of supervisory leadership in the successful implementation

of enterprise systems. International Journal of Information Management. 37(5). pp.417-

430.

Shanks, G and et. al., 2018. Achieving benefits with enterprise architecture. The Journal of

Strategic Information Systems. 27(2). pp.139-156.

Shao, Z., Feng, Y. and Hu, Q., 2016. Effectiveness of top management support in enterprise

systems success: a contingency perspective of fit between leadership style and system

life-cycle. European Journal of Information Systems. 25(2). pp.131-153.

Sun, Z., Strang, K. and Firmin, S., 2017. Business analytics-based enterprise information

systems. Journal of Computer Information Systems. 57(2). pp.169-178.

Books and Journals

Appelbaum, D and et. al., 2017. Impact of business analytics and enterprise systems on

managerial accounting. International Journal of Accounting Information Systems. 25.

pp.29-44.

Archer-Brown, C. and Kietzmann, J., 2018. Strategic knowledge management and enterprise

social media. Journal of Knowledge Management.

Cassidy, A., 2016. A practical guide to information systems strategic planning. CRC press.

Draijer, C., 2020. Best practices of business simulation with SAP R/3. Journal of Information

Systems Education. 15(3). p.5.

Fayoumi, A. and Loucopoulos, P., 2016. Conceptual modeling for the design of intelligent and

emergent information systems. Expert Systems with Applications. 59. pp.174-194.

Kummer, T.F. and Schmiedel, T., 2016. Reviewing the role of culture in strategic information

systems research: A call for prescriptive theorizing on culture

management. Communications of the Association for Information Systems. 38(1). p.5.

Ogiela, L., 2016. Cryptographic techniques of strategic data splitting and secure information

management. Pervasive and Mobile Computing. 29. pp.130-141.

Pearlson, K.E., Saunders, C.S. and Galletta, D.F., 2019. Managing and using information

systems: A strategic approach. John Wiley & Sons.

Rajnoha, R and et. al., 2016. Business intelligence as a key information and knowledge tool for

strategic business performance management. Economics and management.

Rezvani, A., Dong, L. and Khosravi, P., 2017. Promoting the continuing usage of strategic

information systems: The role of supervisory leadership in the successful implementation

of enterprise systems. International Journal of Information Management. 37(5). pp.417-

430.

Shanks, G and et. al., 2018. Achieving benefits with enterprise architecture. The Journal of

Strategic Information Systems. 27(2). pp.139-156.

Shao, Z., Feng, Y. and Hu, Q., 2016. Effectiveness of top management support in enterprise

systems success: a contingency perspective of fit between leadership style and system

life-cycle. European Journal of Information Systems. 25(2). pp.131-153.

Sun, Z., Strang, K. and Firmin, S., 2017. Business analytics-based enterprise information

systems. Journal of Computer Information Systems. 57(2). pp.169-178.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.