Analysis of Strategic Information Systems: Paradise Industries Report

VerifiedAdded on 2023/01/11

|11

|3235

|87

Report

AI Summary

This report provides an in-depth analysis of the strategic information systems employed by Paradise Industries, a manufacturing company based in Adelaide. The report examines the expenditure cycle, which encompasses the acquisition of inventory and materials, detailing the system flow from purchase requisitions to payment. It also explores the conversion cycle, focusing on the transformation of inventory into finished goods, including production scheduling and cost accounting. The report identifies internal control weaknesses within the expenditure cycle, such as potential inaccuracies and unauthorized access, and proposes solutions. Furthermore, it analyzes the risks inherent in the conversion cycle, including material theft and quality control issues, suggesting improvements like supervisor oversight and quality management tools. The analysis highlights the need for streamlined processes and centralized information systems to enhance efficiency and mitigate risks within both cycles, ultimately aiming to improve the company's competitive advantage.

Strategic Information

Systems for Business and

Enterprise

Systems for Business and

Enterprise

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...............................................................................................................3

MAIN BODY.......................................................................................................................3

System Flow of Expenditure Cycle................................................................................3

System Flow of Conversion Cycle.................................................................................5

Analysis of physical internal control weaknesses in the expenditure cycle...................6

Analysis of the risks which are exist in the conversion cycle along with changes

needed to reduce risks...................................................................................................7

CONCLUSION.................................................................................................................10

REFERENCES................................................................................................................11

INTRODUCTION...............................................................................................................3

MAIN BODY.......................................................................................................................3

System Flow of Expenditure Cycle................................................................................3

System Flow of Conversion Cycle.................................................................................5

Analysis of physical internal control weaknesses in the expenditure cycle...................6

Analysis of the risks which are exist in the conversion cycle along with changes

needed to reduce risks...................................................................................................7

CONCLUSION.................................................................................................................10

REFERENCES................................................................................................................11

INTRODUCTION

Strategic information system in business is developed to gain competitive

advantage by the business. Strategic information system in organisations also

contributes in effective coordination and communication within organisation. This report

will discuss about strategic information system at Paradise Industries. Business

activities of the company are manufacturing of high precision machine tools and it is

based in Adelaide. This report will discuss about expenditure cycle which is concerned

with acquisition of inventory and information system in expenditure cycle at the

industries. Limitations of expenditure cycle have also been discussed in this report.

Conversion cycle and its information system will also be discussed in the report. In

relation with system of information at Paradise Industries they have centralised

computer system and its terminals are distributed in all departments of the Paradise

Industries.

MAIN BODY

System Flow of Expenditure Cycle

Expenditure Cycle is concerned with acquisition of material and inventory in the

organisation. This cycle mainly involves three stages which are ordering inventory and

material, receiving inventory and payment for the inventory. This is based on material

requirement which is calculated on the basis of production forecast of the Paradise

Industries (Moser and et.al., 2019). This is one of the most important phase and

involves important function of Paradise because Paradise Industries is a manufacturing

industry hence effectiveness of the material requisition can affect the effectiveness of

the complete manufacturing process.

Expenditure cycle in Paradise Industries starts from time when inventory falls

recorder point. This is an automated process and when inventory falls on reorder point

automatically generates purchase requisition and one copy gets printed on the terminal

of purchase department. This is followed by selection of supplier by purchasing clerk

Strategic information system in business is developed to gain competitive

advantage by the business. Strategic information system in organisations also

contributes in effective coordination and communication within organisation. This report

will discuss about strategic information system at Paradise Industries. Business

activities of the company are manufacturing of high precision machine tools and it is

based in Adelaide. This report will discuss about expenditure cycle which is concerned

with acquisition of inventory and information system in expenditure cycle at the

industries. Limitations of expenditure cycle have also been discussed in this report.

Conversion cycle and its information system will also be discussed in the report. In

relation with system of information at Paradise Industries they have centralised

computer system and its terminals are distributed in all departments of the Paradise

Industries.

MAIN BODY

System Flow of Expenditure Cycle

Expenditure Cycle is concerned with acquisition of material and inventory in the

organisation. This cycle mainly involves three stages which are ordering inventory and

material, receiving inventory and payment for the inventory. This is based on material

requirement which is calculated on the basis of production forecast of the Paradise

Industries (Moser and et.al., 2019). This is one of the most important phase and

involves important function of Paradise because Paradise Industries is a manufacturing

industry hence effectiveness of the material requisition can affect the effectiveness of

the complete manufacturing process.

Expenditure cycle in Paradise Industries starts from time when inventory falls

recorder point. This is an automated process and when inventory falls on reorder point

automatically generates purchase requisition and one copy gets printed on the terminal

of purchase department. This is followed by selection of supplier by purchasing clerk

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

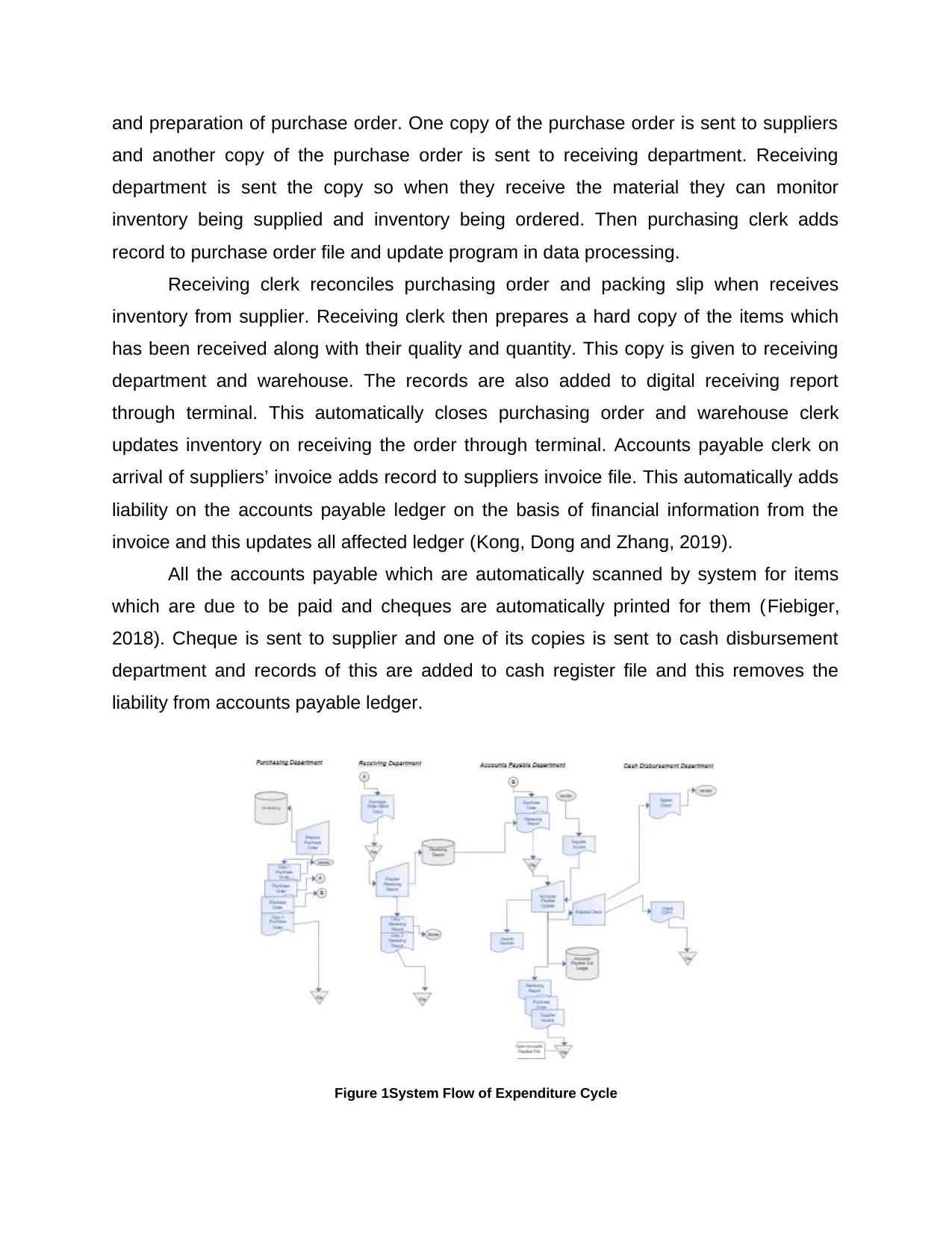

and preparation of purchase order. One copy of the purchase order is sent to suppliers

and another copy of the purchase order is sent to receiving department. Receiving

department is sent the copy so when they receive the material they can monitor

inventory being supplied and inventory being ordered. Then purchasing clerk adds

record to purchase order file and update program in data processing.

Receiving clerk reconciles purchasing order and packing slip when receives

inventory from supplier. Receiving clerk then prepares a hard copy of the items which

has been received along with their quality and quantity. This copy is given to receiving

department and warehouse. The records are also added to digital receiving report

through terminal. This automatically closes purchasing order and warehouse clerk

updates inventory on receiving the order through terminal. Accounts payable clerk on

arrival of suppliers’ invoice adds record to suppliers invoice file. This automatically adds

liability on the accounts payable ledger on the basis of financial information from the

invoice and this updates all affected ledger (Kong, Dong and Zhang, 2019).

All the accounts payable which are automatically scanned by system for items

which are due to be paid and cheques are automatically printed for them (Fiebiger,

2018). Cheque is sent to supplier and one of its copies is sent to cash disbursement

department and records of this are added to cash register file and this removes the

liability from accounts payable ledger.

Figure 1System Flow of Expenditure Cycle

and another copy of the purchase order is sent to receiving department. Receiving

department is sent the copy so when they receive the material they can monitor

inventory being supplied and inventory being ordered. Then purchasing clerk adds

record to purchase order file and update program in data processing.

Receiving clerk reconciles purchasing order and packing slip when receives

inventory from supplier. Receiving clerk then prepares a hard copy of the items which

has been received along with their quality and quantity. This copy is given to receiving

department and warehouse. The records are also added to digital receiving report

through terminal. This automatically closes purchasing order and warehouse clerk

updates inventory on receiving the order through terminal. Accounts payable clerk on

arrival of suppliers’ invoice adds record to suppliers invoice file. This automatically adds

liability on the accounts payable ledger on the basis of financial information from the

invoice and this updates all affected ledger (Kong, Dong and Zhang, 2019).

All the accounts payable which are automatically scanned by system for items

which are due to be paid and cheques are automatically printed for them (Fiebiger,

2018). Cheque is sent to supplier and one of its copies is sent to cash disbursement

department and records of this are added to cash register file and this removes the

liability from accounts payable ledger.

Figure 1System Flow of Expenditure Cycle

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

System Flow of Conversion Cycle

Conversion cycle is a process which converts the inventory into final goods.

Conversion cycle in Paradise Industries is based on quarterly forecast of sales. This

quarterly forecast of sales goes to production planning and control clerk. Digital

production schedule from terminal is updated from the terminal by production planning

clerk and this includes batches of production to be produced in next quarter.

Supervisor of the work centre gets digital documents and prints hard copy of the

work orders, move tickets and material requisition (Sugathadasa, 2018). Move tickets

and material requisition are distributed to work centres by the supervisor. Staff members

submit two copies of material requisition to warehouse for material and in case material

is required beyond the standard quantity as designed by production planning and

control clerk they supervisor issues additional material requisition. Move tickets are

send to cost accounting once production gets completed in each production phase in

each work centre by staff members. This is done so that completion of production phase

can be marked in cost accounting. Labour time spend on each batch is also recorded

and sent to cost accounting, this is done so that cost accounting can calculate correct

cost of the production on the basis of completer information. Work centre supervisor

closes the open work order file after completion of production.

Clerk at the warehouse files one copy of material requisition and updates

material inventory. The clerk at the warehouse sends one copy of the material

requisition to cost accounting. This is done so that cost accounting can involve cost of

material required in production of the batch. Lastly digital general voucher is prepared

by the clerk and is posted to general ledger control accounts.

This digital ledger is accessed by cost accounting clerk and work-in-process

account is prepared for production batch (Lagesh, Srikanth and Acharya, 2018). In this

clerk also receives move tickets, job tickets and material requisition in the process of

production and these are used for posting in work-in-process ledger. After this digital

general voucher is prepared by cost accounting clerk to reflect status of work-in-process

and transfer the record to finished goods inventory.

Conversion cycle is a process which converts the inventory into final goods.

Conversion cycle in Paradise Industries is based on quarterly forecast of sales. This

quarterly forecast of sales goes to production planning and control clerk. Digital

production schedule from terminal is updated from the terminal by production planning

clerk and this includes batches of production to be produced in next quarter.

Supervisor of the work centre gets digital documents and prints hard copy of the

work orders, move tickets and material requisition (Sugathadasa, 2018). Move tickets

and material requisition are distributed to work centres by the supervisor. Staff members

submit two copies of material requisition to warehouse for material and in case material

is required beyond the standard quantity as designed by production planning and

control clerk they supervisor issues additional material requisition. Move tickets are

send to cost accounting once production gets completed in each production phase in

each work centre by staff members. This is done so that completion of production phase

can be marked in cost accounting. Labour time spend on each batch is also recorded

and sent to cost accounting, this is done so that cost accounting can calculate correct

cost of the production on the basis of completer information. Work centre supervisor

closes the open work order file after completion of production.

Clerk at the warehouse files one copy of material requisition and updates

material inventory. The clerk at the warehouse sends one copy of the material

requisition to cost accounting. This is done so that cost accounting can involve cost of

material required in production of the batch. Lastly digital general voucher is prepared

by the clerk and is posted to general ledger control accounts.

This digital ledger is accessed by cost accounting clerk and work-in-process

account is prepared for production batch (Lagesh, Srikanth and Acharya, 2018). In this

clerk also receives move tickets, job tickets and material requisition in the process of

production and these are used for posting in work-in-process ledger. After this digital

general voucher is prepared by cost accounting clerk to reflect status of work-in-process

and transfer the record to finished goods inventory.

This leads to end of conversion cycle when all the production work gets

completed in every phase of production and it becomes finished goods inventory.

Analysis of physical internal control weaknesses in the expenditure cycle

In the context of expenditure cycle it can be said that accountant and all involved

person in this cycle like suppliers, account payable, receiver face several problems in

managing or controlling them. Some primary and basic risks which are associated with

expenditure cycle are: unauthorized inventory purchased, when sometimes receiver

collect wrong quantity of products, wrong items or even damaged items. All these

problems sometimes create problems in accounting as accountant makes transactions

of purchases and cash disbursements in an inaccurate manner which can create

problems in cash disbursements (Karim, Nawawi and Salin, 2018). It is also stated that

in an expenditure cycle, companies like paradise industries involve all those person who

are not required and do not play specific and important role. Their unnecessary

involvement in this process and access to accounting records as well as confidential

reports can become the reason of leakage of that informations and lack of transparency.

They can make this process of expenditure cycle complicated which can create lack of

understanding and clarity. It can be said that Paradise industries can make an effective

use of clear, short and simple expenditure process or cycle which can be understood by

all involved members and making it successful. The big process of this cycle which is

being discussed above is complicated and difficult in understanding. In the context of

information flow which is one of the important flow needs to have by all companies, is

mainly based on distribution of all departments of paradise industries so, it can be said

that by keeping it centralized it can be made simpler.

The whole process of expenditure cycle of paradise industries consists of main 4

departments which are: accounts payable, cash disbursement department, purchasing

as well as receiving department. Each department plays an important role such as

ordering for products which is one of the main step of completing this cycle, receiving of

products, storing all those products at warehouse and paying for all those received

completed in every phase of production and it becomes finished goods inventory.

Analysis of physical internal control weaknesses in the expenditure cycle

In the context of expenditure cycle it can be said that accountant and all involved

person in this cycle like suppliers, account payable, receiver face several problems in

managing or controlling them. Some primary and basic risks which are associated with

expenditure cycle are: unauthorized inventory purchased, when sometimes receiver

collect wrong quantity of products, wrong items or even damaged items. All these

problems sometimes create problems in accounting as accountant makes transactions

of purchases and cash disbursements in an inaccurate manner which can create

problems in cash disbursements (Karim, Nawawi and Salin, 2018). It is also stated that

in an expenditure cycle, companies like paradise industries involve all those person who

are not required and do not play specific and important role. Their unnecessary

involvement in this process and access to accounting records as well as confidential

reports can become the reason of leakage of that informations and lack of transparency.

They can make this process of expenditure cycle complicated which can create lack of

understanding and clarity. It can be said that Paradise industries can make an effective

use of clear, short and simple expenditure process or cycle which can be understood by

all involved members and making it successful. The big process of this cycle which is

being discussed above is complicated and difficult in understanding. In the context of

information flow which is one of the important flow needs to have by all companies, is

mainly based on distribution of all departments of paradise industries so, it can be said

that by keeping it centralized it can be made simpler.

The whole process of expenditure cycle of paradise industries consists of main 4

departments which are: accounts payable, cash disbursement department, purchasing

as well as receiving department. Each department plays an important role such as

ordering for products which is one of the main step of completing this cycle, receiving of

products, storing all those products at warehouse and paying for all those received

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

items. It is quite good but the main problem which is being identified that all

departments carries out their separate accounting records and match them with others

which is time consuming process and can delay in other functions. So, it can be said

that for solving this problem and time saving, Paradise industries can complete

accounting process in single attempt and at single department by making its system

centralized (Zhou, Chen and Cheng, 2016). It can help it out in carrying out other

processes and functions in a timely and an in an effective manner.

Failure in approving vendor lists, not checking vendor lists and only keep it with

themselves and after finding problems in quantity, and quality and other factors can

create several problems. By keeping all processes and accounting at centralized

system all departments of paradise industries will be able to check and match their

products along with informations, supplies, receiving of products and all other things

from the central system. So, overall it can be said that one of the main problems is

repetition of each functions at all departments which consume time, efforts and delay in

completing other functions. Eliminating all those people who are not required in this

process and whose involvement is creating problems can be done by paradise

industries. Making accurate recording, checking it twice, thrice, inform purchasing

department about damaged products, changing products and any other types of errors

in by receiving department at that time can also support this industry in solving all

problems related to expenditure cycle (RACHID and LAHMOUCHI, 2018).

Analysis of the risks which are exist in the conversion cycle along with changes needed

to reduce risks

In the context of conversion cycle it can be said that it is mainly depend and

connected with production and sales department. Many companies start production

process by forecasting sales as per the previous year. On the basis of forecasting of

sales expected, all these informations is communicated to production department and

production department starts manufacturing of process but sometimes or often it leads

changes in sales expectations and the actual sales or purchasing demand. It is one of

the main problems which can sometimes have negative effects on the performance and

departments carries out their separate accounting records and match them with others

which is time consuming process and can delay in other functions. So, it can be said

that for solving this problem and time saving, Paradise industries can complete

accounting process in single attempt and at single department by making its system

centralized (Zhou, Chen and Cheng, 2016). It can help it out in carrying out other

processes and functions in a timely and an in an effective manner.

Failure in approving vendor lists, not checking vendor lists and only keep it with

themselves and after finding problems in quantity, and quality and other factors can

create several problems. By keeping all processes and accounting at centralized

system all departments of paradise industries will be able to check and match their

products along with informations, supplies, receiving of products and all other things

from the central system. So, overall it can be said that one of the main problems is

repetition of each functions at all departments which consume time, efforts and delay in

completing other functions. Eliminating all those people who are not required in this

process and whose involvement is creating problems can be done by paradise

industries. Making accurate recording, checking it twice, thrice, inform purchasing

department about damaged products, changing products and any other types of errors

in by receiving department at that time can also support this industry in solving all

problems related to expenditure cycle (RACHID and LAHMOUCHI, 2018).

Analysis of the risks which are exist in the conversion cycle along with changes needed

to reduce risks

In the context of conversion cycle it can be said that it is mainly depend and

connected with production and sales department. Many companies start production

process by forecasting sales as per the previous year. On the basis of forecasting of

sales expected, all these informations is communicated to production department and

production department starts manufacturing of process but sometimes or often it leads

changes in sales expectations and the actual sales or purchasing demand. It is one of

the main problems which can sometimes have negative effects on the performance and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

sales. Estimation of sales and starting manufacturing or conversion cycles involves

many departments of paradise industries and any type of changes in production and

sales can affect performance of all involved departments. These departments are:

human resource management, cost estimation department, cost accounting, material

requisition and production department. Any changes in estimation and production affect

performance of all departments which can create problems in the future (Ramadhani,

Hartanto and Nugroho, 2018). So, it can be said that involvement of all departments in

just one cycle can make this process complicated, time consuming which can hamper

functions of each separate department. There are several other risks which are

associated with conversion cycle of paradise industries include:

It is stated that there are chances if theft as well as damages of raw materials

which can create problems in conversion cycle to the great extent. It is also analysed

that paradise industries appoint a production clerk in order to having records of work

orders in production schedule and there is requirement of having supervisor who can

supervise and cross check all these records and transactions but if it does not appoint

supervisor to check work records then it can create several problems like changes in

cash disbursements and others. Quality is one of the important factors which is being

considered by customers and on which basis company can increase their customers,

sales and revenues as well but failure in managing quantity and quality in this

conversion cycle can create many problems. Because it is stated that quality and

quantity aspects are not involved in the whole process of conversion. Industries do not

focus on these factors. So, in this context, it can be said that implementing some tools

in manufacturing of products like TQM, Six sigma, company can maintain quality of

products and can solve this main problem associated with conversion cycle

(Tiruvengadam, 2018).

Other main problem is complicated, time consuming of this cycle because of

involving all members of company such as warehouse staff, production staff and other

can make this process complicated and any changes can sometimes become the

reason of conflicts. Miscommunication can also become reason of errors in conversion

cycle of paradise industries. For solving these problems, it is important for paradise

many departments of paradise industries and any type of changes in production and

sales can affect performance of all involved departments. These departments are:

human resource management, cost estimation department, cost accounting, material

requisition and production department. Any changes in estimation and production affect

performance of all departments which can create problems in the future (Ramadhani,

Hartanto and Nugroho, 2018). So, it can be said that involvement of all departments in

just one cycle can make this process complicated, time consuming which can hamper

functions of each separate department. There are several other risks which are

associated with conversion cycle of paradise industries include:

It is stated that there are chances if theft as well as damages of raw materials

which can create problems in conversion cycle to the great extent. It is also analysed

that paradise industries appoint a production clerk in order to having records of work

orders in production schedule and there is requirement of having supervisor who can

supervise and cross check all these records and transactions but if it does not appoint

supervisor to check work records then it can create several problems like changes in

cash disbursements and others. Quality is one of the important factors which is being

considered by customers and on which basis company can increase their customers,

sales and revenues as well but failure in managing quantity and quality in this

conversion cycle can create many problems. Because it is stated that quality and

quantity aspects are not involved in the whole process of conversion. Industries do not

focus on these factors. So, in this context, it can be said that implementing some tools

in manufacturing of products like TQM, Six sigma, company can maintain quality of

products and can solve this main problem associated with conversion cycle

(Tiruvengadam, 2018).

Other main problem is complicated, time consuming of this cycle because of

involving all members of company such as warehouse staff, production staff and other

can make this process complicated and any changes can sometimes become the

reason of conflicts. Miscommunication can also become reason of errors in conversion

cycle of paradise industries. For solving these problems, it is important for paradise

industries to appoint a supervisor who perform main functions of conversion cycle and

making the process easier and effective as well. Supervisor should be allowed to take

help of production clerk if required and improving process. It can help them out to

accomplish goals and making conversion cycle process easier.

In addition, it is analysed that conversion cycle process is connected with

inventory of company and any changes in it can directly affect inventory. One of the

reasons of it is production department start working on the estimation of sales and

demand by people and shortage in raw materials and input can directly affect the

process of conversion cycle and production process as well. In this case, staff members

of production department put pressure on other departments to buy raw materials and

inputs and this pressure can create problems in getting poor quality of products or delay

in the submission of the final product. Just like shortage of inventory which creates

problem of poor quality, excess of inventory as per the wrong estimation can also create

problems. It can increase cost of warehousing, storage of inventory, damages of extra

or excessive inventory which can increase operational cost and lower profit margin of

the company. So, in this type of cases, it can be suggested to company that it should

employ a special employee who can forecast in an effective manner. It can also be

said that company should buy extra those raw materials that can last for log run and

cannot be damaged. This can solve problems of shortage of inventory or raw materials

and can support production department to complete conversion cycle and process in an

effective manner. On the other hand, in the case of excessive of inventory, it can be

said that company should make contract with selling companies or suppliers that if they

find excessive of raw materials then they can resell it to sales department, companies or

suppliers. This contract and improved relation can help them out in reselling excessive

inventory to suppliers and becoming cost effective (Paton and Buergelt, 2019).

Reliability as well as validity of informations in conversion cycle can be other

main problems. Wrong or incorrect recording of informations of estimated sales and

requirement of raw materials and other elements can direct affect cost of the company.

It can also affect requisition of inventory and overall cost of that inventory. SO, overall it

can be said that changes in sales estimation can lead either excessive or shortage of

making the process easier and effective as well. Supervisor should be allowed to take

help of production clerk if required and improving process. It can help them out to

accomplish goals and making conversion cycle process easier.

In addition, it is analysed that conversion cycle process is connected with

inventory of company and any changes in it can directly affect inventory. One of the

reasons of it is production department start working on the estimation of sales and

demand by people and shortage in raw materials and input can directly affect the

process of conversion cycle and production process as well. In this case, staff members

of production department put pressure on other departments to buy raw materials and

inputs and this pressure can create problems in getting poor quality of products or delay

in the submission of the final product. Just like shortage of inventory which creates

problem of poor quality, excess of inventory as per the wrong estimation can also create

problems. It can increase cost of warehousing, storage of inventory, damages of extra

or excessive inventory which can increase operational cost and lower profit margin of

the company. So, in this type of cases, it can be suggested to company that it should

employ a special employee who can forecast in an effective manner. It can also be

said that company should buy extra those raw materials that can last for log run and

cannot be damaged. This can solve problems of shortage of inventory or raw materials

and can support production department to complete conversion cycle and process in an

effective manner. On the other hand, in the case of excessive of inventory, it can be

said that company should make contract with selling companies or suppliers that if they

find excessive of raw materials then they can resell it to sales department, companies or

suppliers. This contract and improved relation can help them out in reselling excessive

inventory to suppliers and becoming cost effective (Paton and Buergelt, 2019).

Reliability as well as validity of informations in conversion cycle can be other

main problems. Wrong or incorrect recording of informations of estimated sales and

requirement of raw materials and other elements can direct affect cost of the company.

It can also affect requisition of inventory and overall cost of that inventory. SO, overall it

can be said that changes in sales estimation can lead either excessive or shortage of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

products which both affects either quality of products or cost of the company. It can also

be suggested to paradise industries that by making changes in conversion approach,

employing supervisor, specialist sales forecasting, making relation with sales

companies, suppliers can help them out in solving all problems of conversion cycle.

CONCLUSION

On the basis of above discussion it can be concluded that expenditure cycle and

conversion cycle may be different but important part of the complete production cycle.

This is because production involves acquisition of inventory and then conversion of

inventory to finished goods. In these cycles at Paradise Industries there are several

issues and first is that this is very expanded and this possess the possibility of affecting

quality of the cycle while acquisition of material. In the cycle of conversion there are

several parties involved and has limitation like conversion based of sales forecast and

not involving quality checks.

be suggested to paradise industries that by making changes in conversion approach,

employing supervisor, specialist sales forecasting, making relation with sales

companies, suppliers can help them out in solving all problems of conversion cycle.

CONCLUSION

On the basis of above discussion it can be concluded that expenditure cycle and

conversion cycle may be different but important part of the complete production cycle.

This is because production involves acquisition of inventory and then conversion of

inventory to finished goods. In these cycles at Paradise Industries there are several

issues and first is that this is very expanded and this possess the possibility of affecting

quality of the cycle while acquisition of material. In the cycle of conversion there are

several parties involved and has limitation like conversion based of sales forecast and

not involving quality checks.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journal

Fiebiger, B., 2018. Semi-autonomous household expenditures as the causa causans of

postwar US business cycles: the stability and instability of Luxemburg-type

external markets. Cambridge Journal of Economics.

Karim, N.A., Nawawi, A. and Salin, A.S.A.P., 2018. Inventory control weaknesses–a

case study of lubricant manufacturing company. Journal of Financial Crime.

Kong, X., Dong, K. and Zhang, L., 2019. Characteristics and determinants of

asymmetric phase shifts in China’s manufacturing industrial production

cycles. Applied Economics. pp.1-11.

Lagesh, M.A., Srikanth, M. and Acharya, D., 2018. Corporate performance during

business cycles: Evidence from Indian manufacturing firms. Global Business

Review. 19(5). pp.1261-1274.

Moser, P and et.al., 2019. Manufacturing Management in Process Industries: The

Impact of Market Conditions and Capital Expenditure on Firm

Performance. IEEE Transactions on Engineering Management.

Paton, D. and Buergelt, P., 2019. Risk, transformation and adaptation: ideas for

reframing approaches to disaster risk reduction. International journal of

environmental research and public health. 16(14). p.2594.

RACHID, Y. and LAHMOUCHI, M., 2018. Internal control practices in a Moroccan public

enterprise: A case study. ASIA LIFE SCIENCES. 16(1). pp.275-290.

Ramadhani, S.T.A., Hartanto, R. and Nugroho, E., 2018. RISK-MANAGEMENT BASED

GOVERNMENT INFORMATION SYSTEM SECURITY USING OCTAVE

ALLEGRO FRAMEWORK. In Proceeding of International Seminar &

Conference on Learning Organization.

Sugathadasa, D.D.K., 2018. The Relationship between Cash Conversion Cycle and

Firm Profitability: Special Reference to Manufacturing Companies in Colombo

Stock Exchange. Journal of Economics and Finance. 6. pp.38-47.

Tiruvengadam, N., 2018. An Analytical Exploration of the Theorized Relationship

Between Total Productivity and Cash Conversion Cycle. In Proceedings of the

International Annual Conference of the American Society for Engineering

Management. (pp. 1-10). American Society for Engineering Management

(ASEM).

Zhou, H., Chen, H. and Cheng, Z., 2016. Internal control, corporate life cycle, and firm

performance. The Political Economy of Chinese Finance. 12(3). pp.189-209.

Books and Journal

Fiebiger, B., 2018. Semi-autonomous household expenditures as the causa causans of

postwar US business cycles: the stability and instability of Luxemburg-type

external markets. Cambridge Journal of Economics.

Karim, N.A., Nawawi, A. and Salin, A.S.A.P., 2018. Inventory control weaknesses–a

case study of lubricant manufacturing company. Journal of Financial Crime.

Kong, X., Dong, K. and Zhang, L., 2019. Characteristics and determinants of

asymmetric phase shifts in China’s manufacturing industrial production

cycles. Applied Economics. pp.1-11.

Lagesh, M.A., Srikanth, M. and Acharya, D., 2018. Corporate performance during

business cycles: Evidence from Indian manufacturing firms. Global Business

Review. 19(5). pp.1261-1274.

Moser, P and et.al., 2019. Manufacturing Management in Process Industries: The

Impact of Market Conditions and Capital Expenditure on Firm

Performance. IEEE Transactions on Engineering Management.

Paton, D. and Buergelt, P., 2019. Risk, transformation and adaptation: ideas for

reframing approaches to disaster risk reduction. International journal of

environmental research and public health. 16(14). p.2594.

RACHID, Y. and LAHMOUCHI, M., 2018. Internal control practices in a Moroccan public

enterprise: A case study. ASIA LIFE SCIENCES. 16(1). pp.275-290.

Ramadhani, S.T.A., Hartanto, R. and Nugroho, E., 2018. RISK-MANAGEMENT BASED

GOVERNMENT INFORMATION SYSTEM SECURITY USING OCTAVE

ALLEGRO FRAMEWORK. In Proceeding of International Seminar &

Conference on Learning Organization.

Sugathadasa, D.D.K., 2018. The Relationship between Cash Conversion Cycle and

Firm Profitability: Special Reference to Manufacturing Companies in Colombo

Stock Exchange. Journal of Economics and Finance. 6. pp.38-47.

Tiruvengadam, N., 2018. An Analytical Exploration of the Theorized Relationship

Between Total Productivity and Cash Conversion Cycle. In Proceedings of the

International Annual Conference of the American Society for Engineering

Management. (pp. 1-10). American Society for Engineering Management

(ASEM).

Zhou, H., Chen, H. and Cheng, Z., 2016. Internal control, corporate life cycle, and firm

performance. The Political Economy of Chinese Finance. 12(3). pp.189-209.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.