Accounting and Finance: BEP, Capital Budgeting, and Income Statement

VerifiedAdded on 2023/01/07

|20

|3983

|67

Homework Assignment

AI Summary

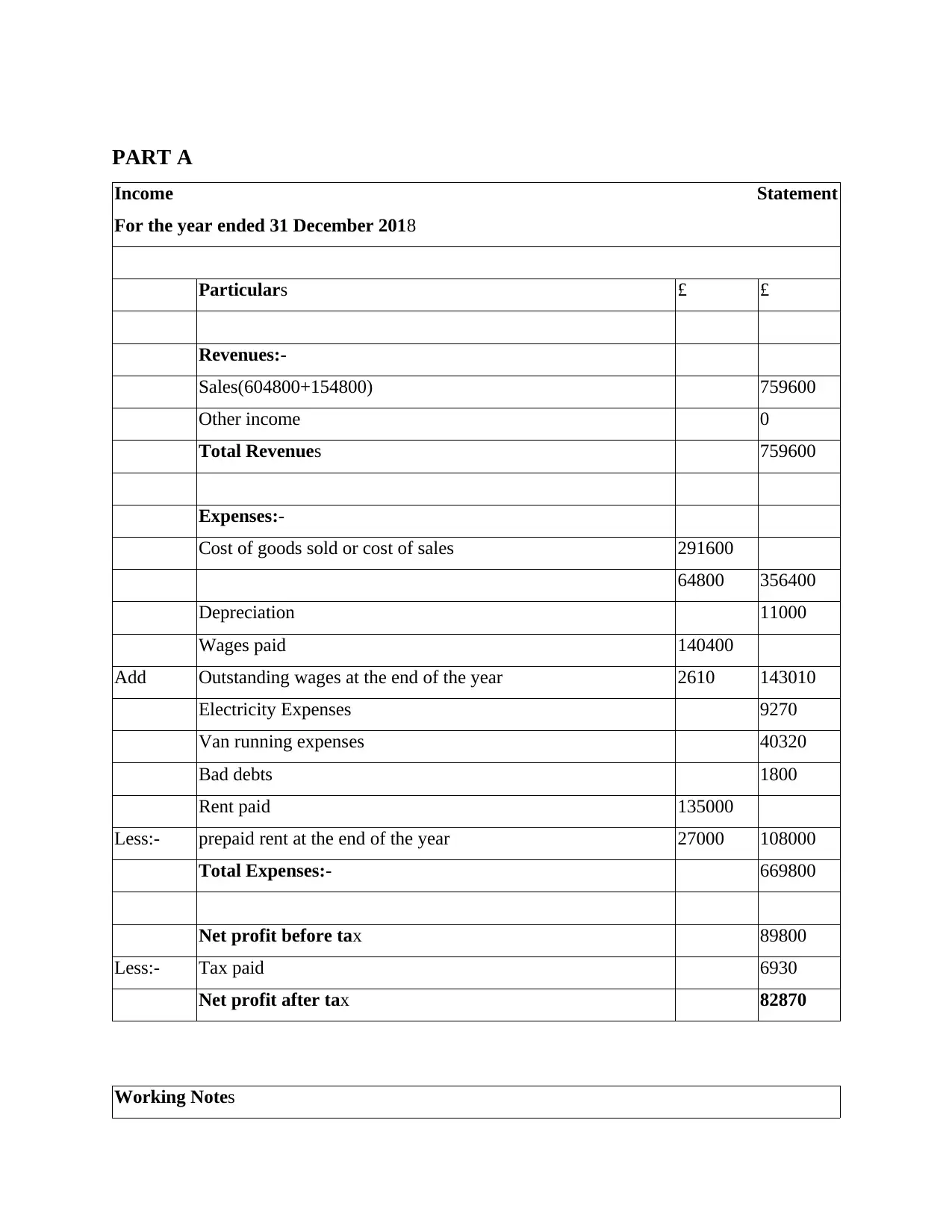

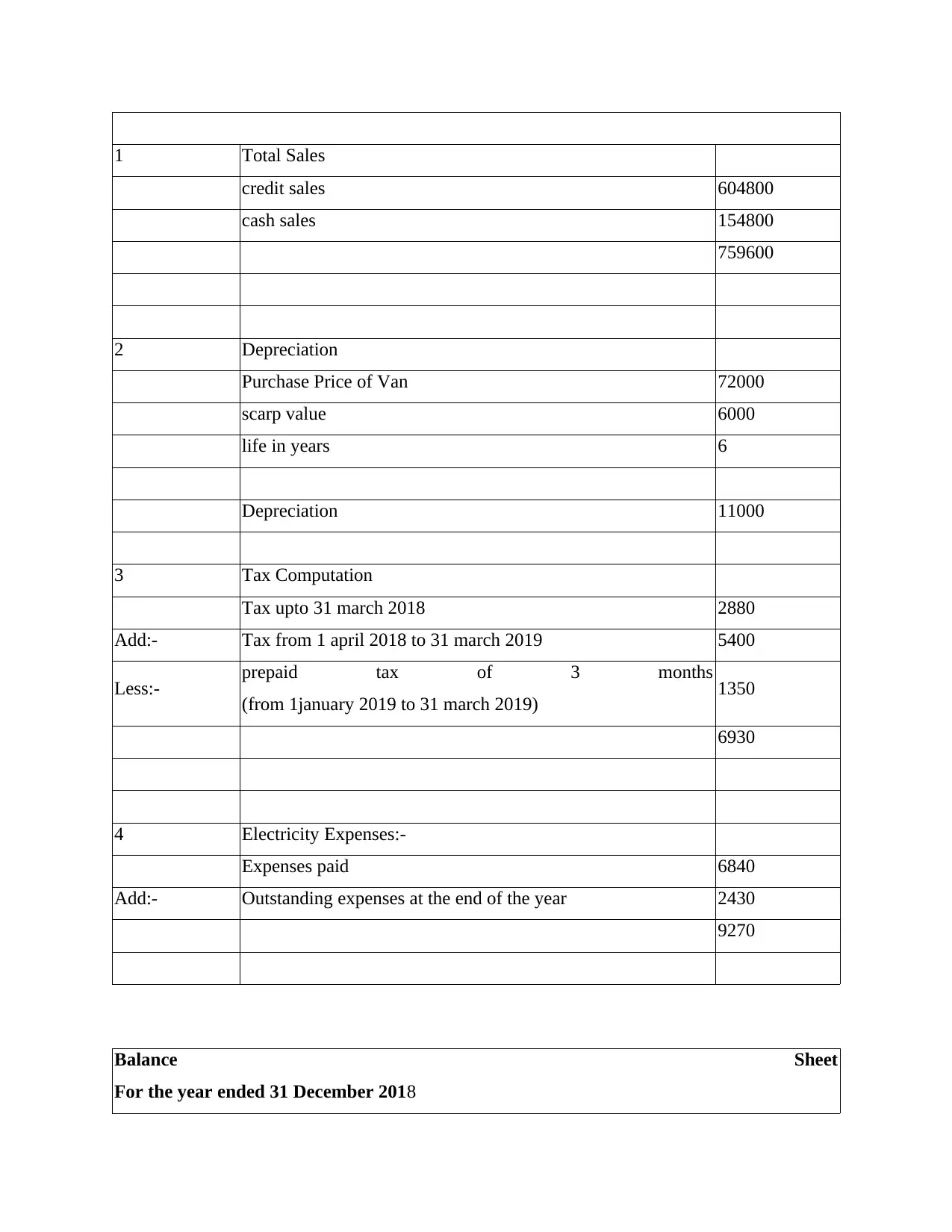

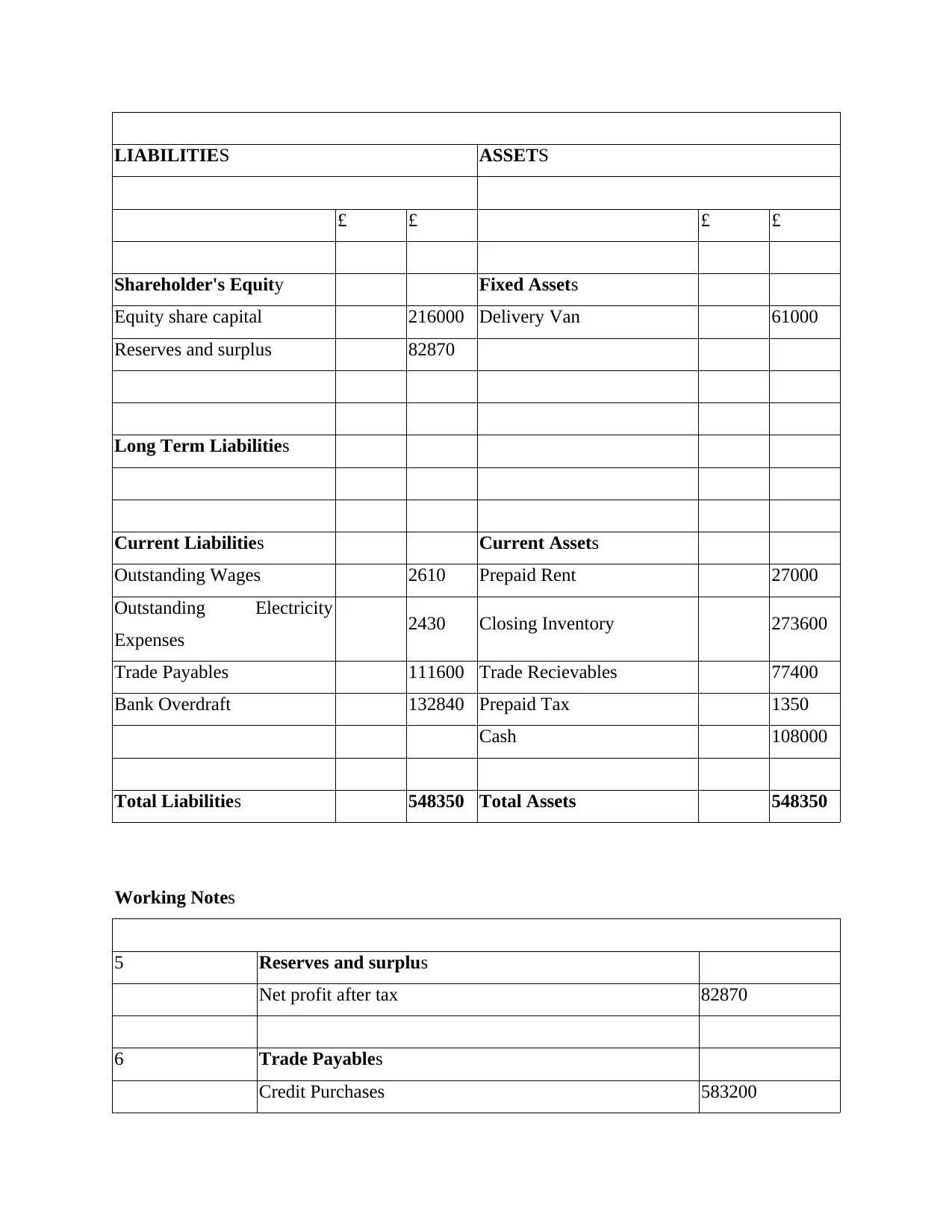

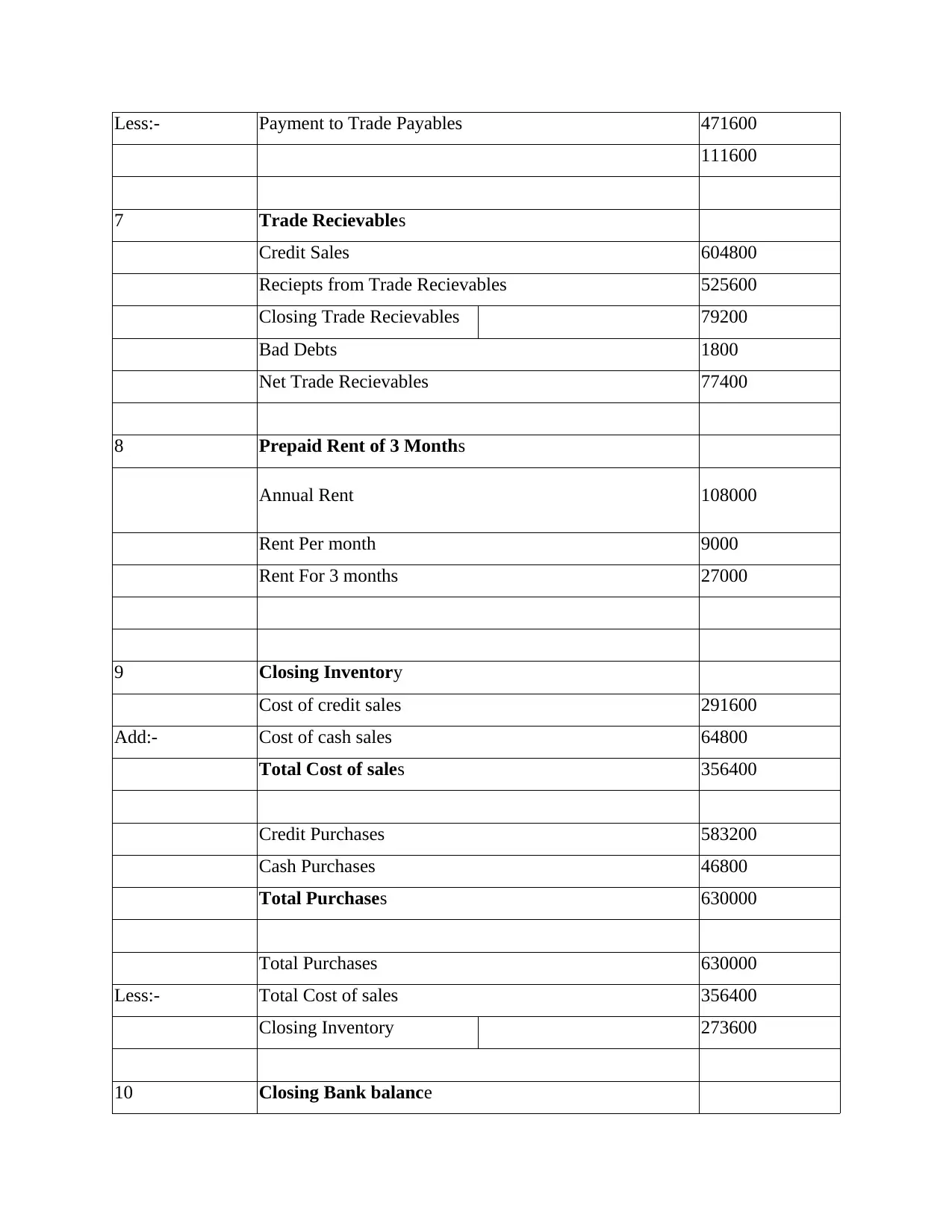

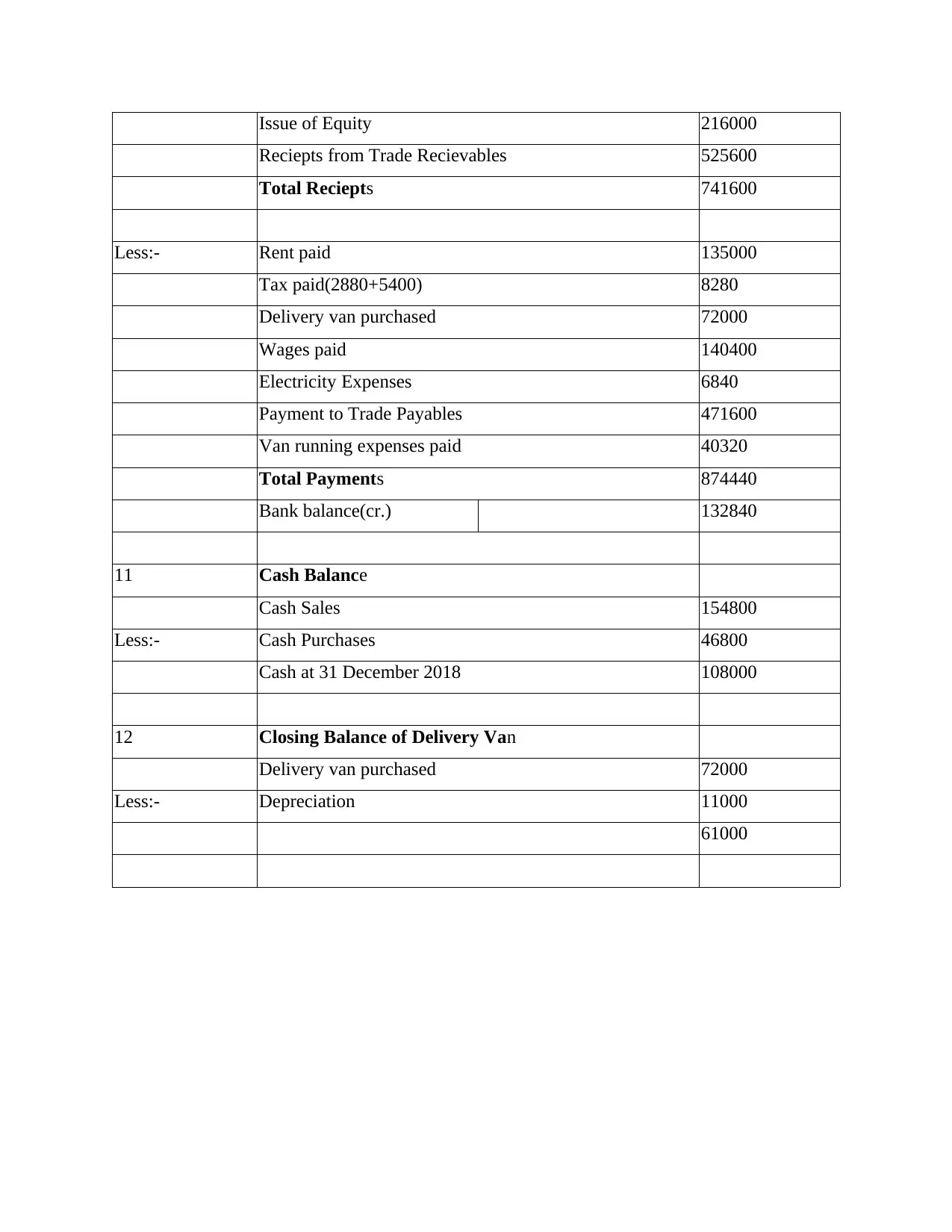

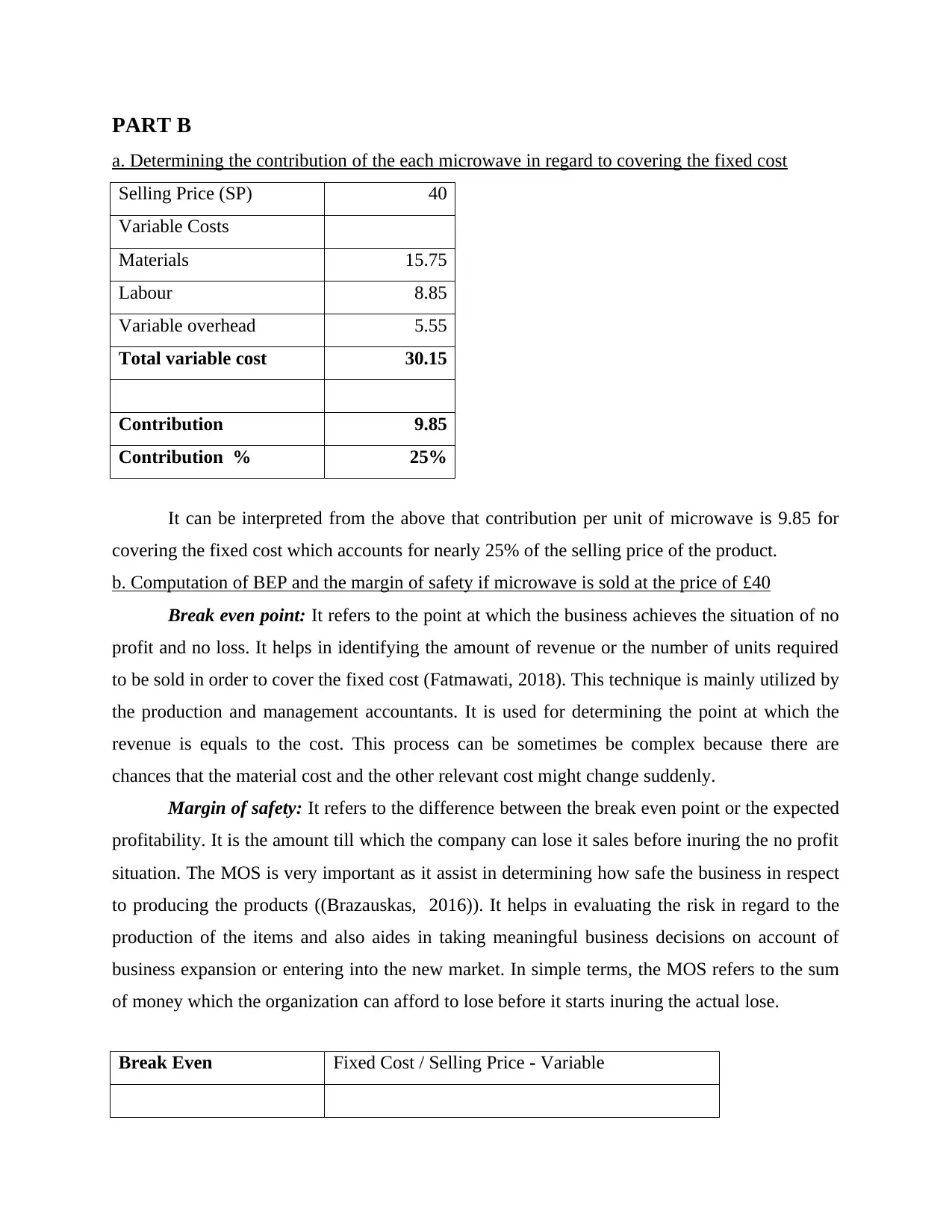

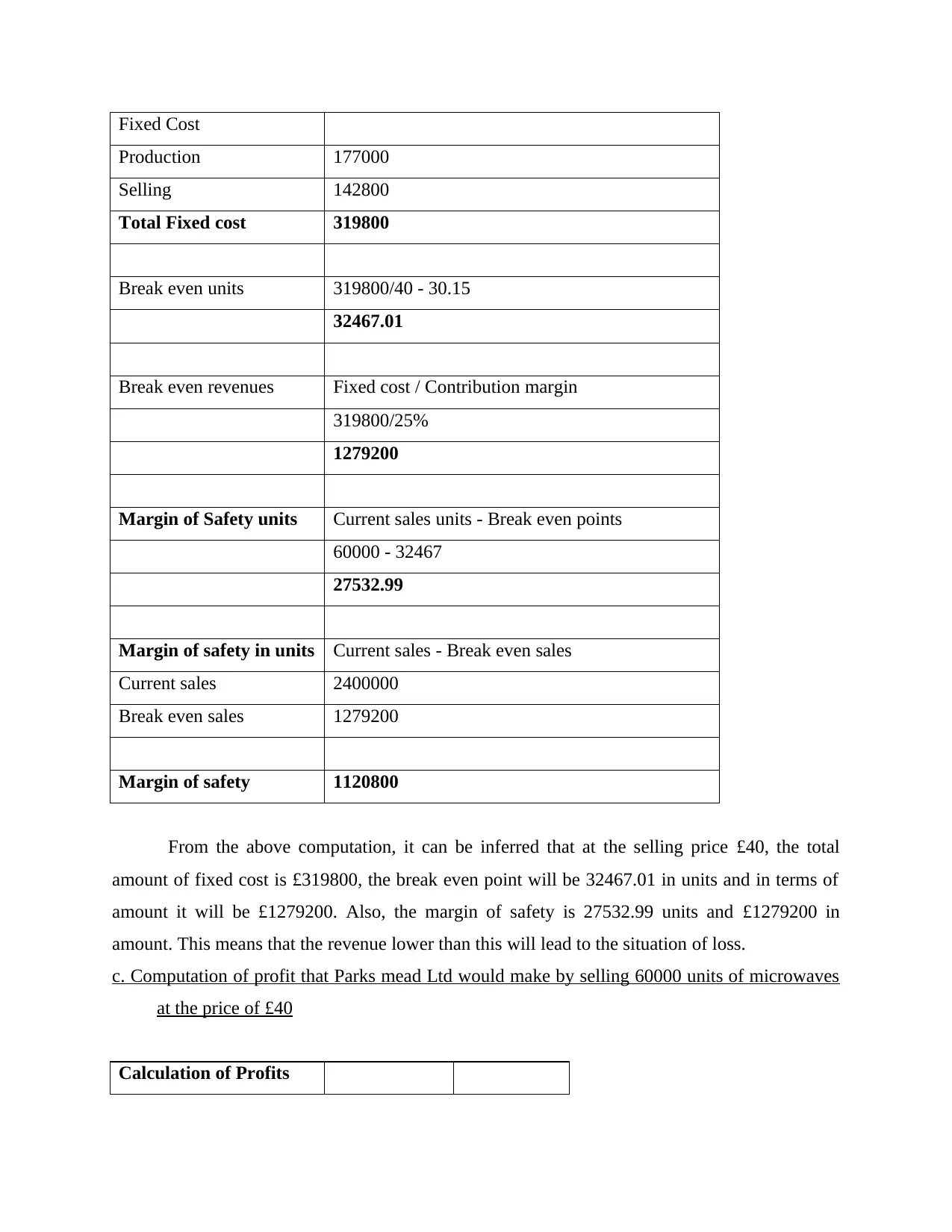

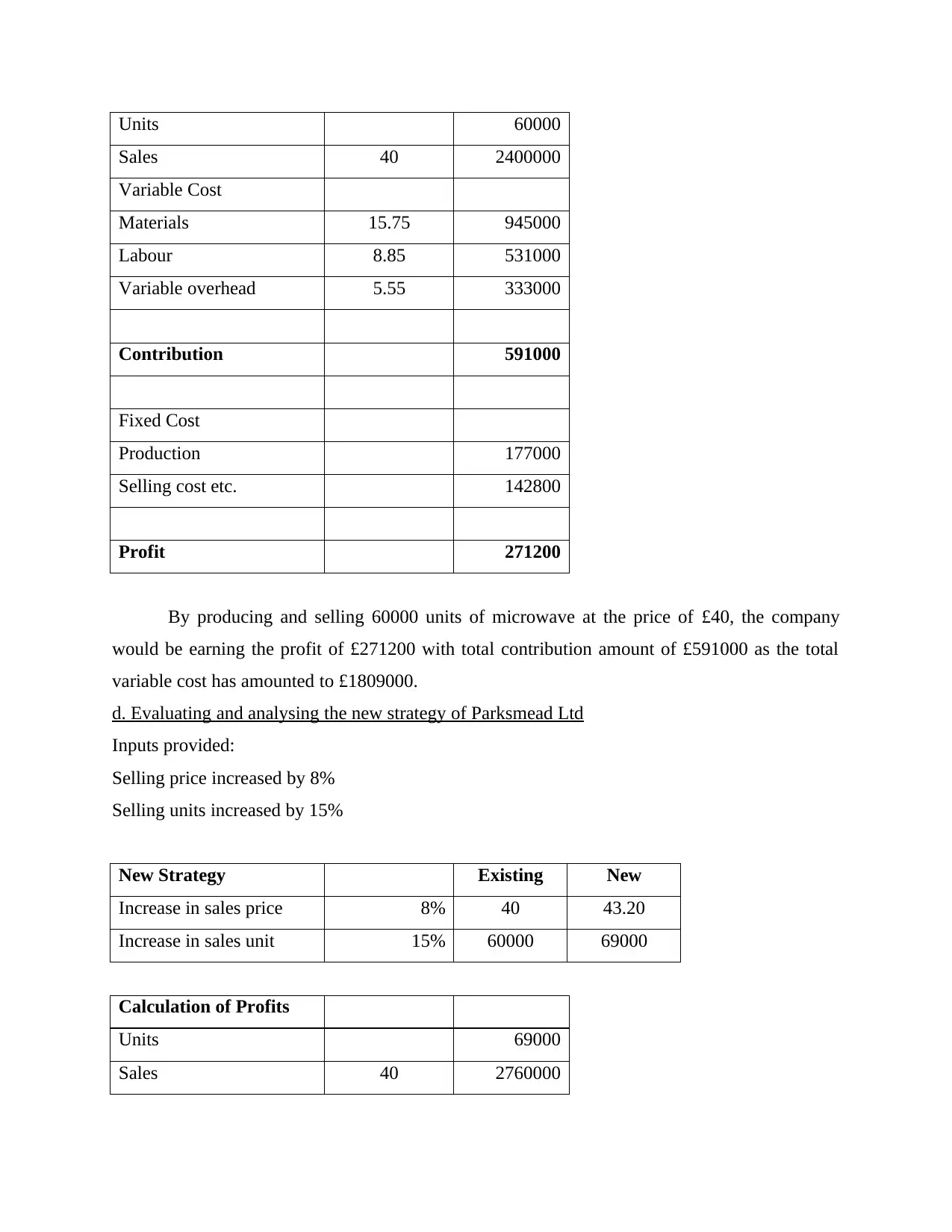

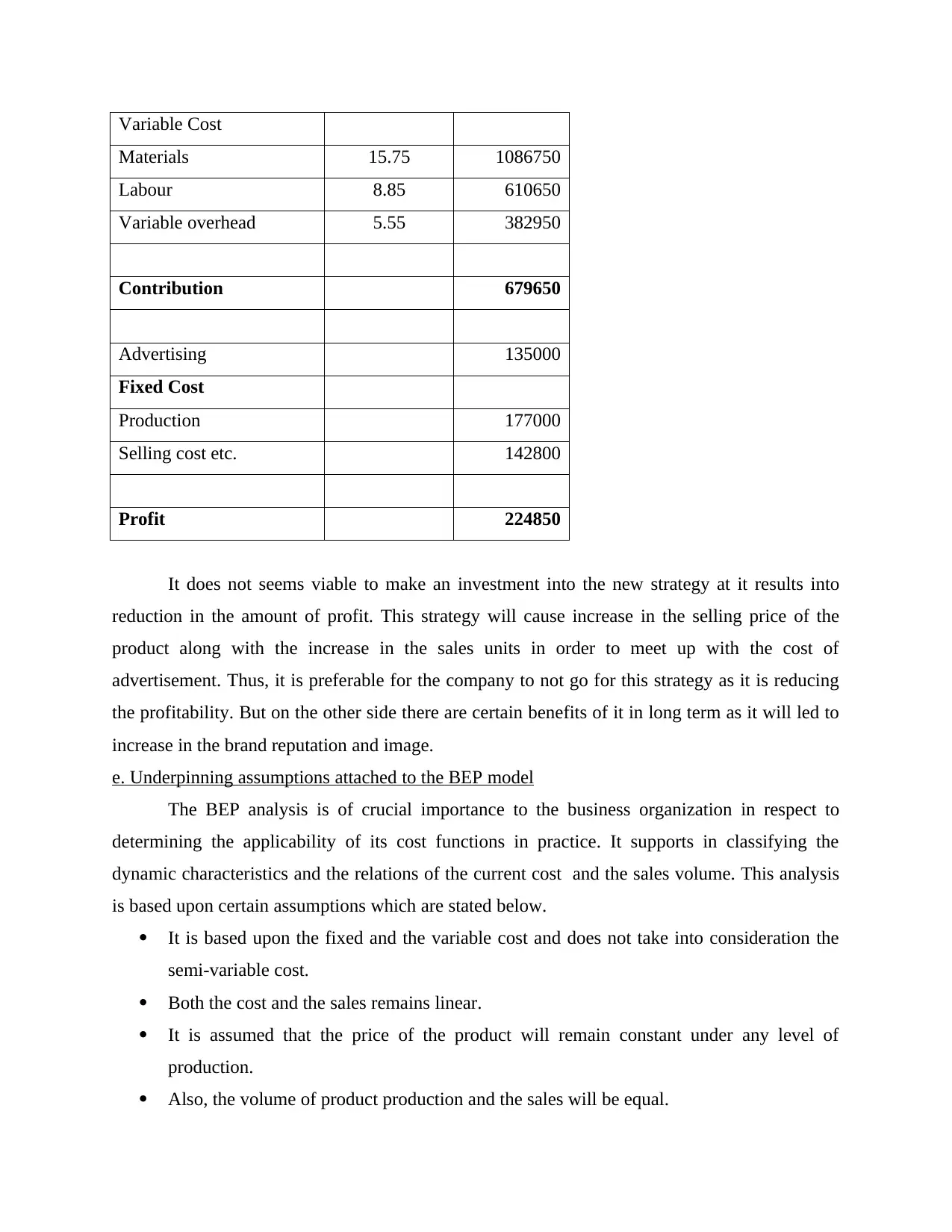

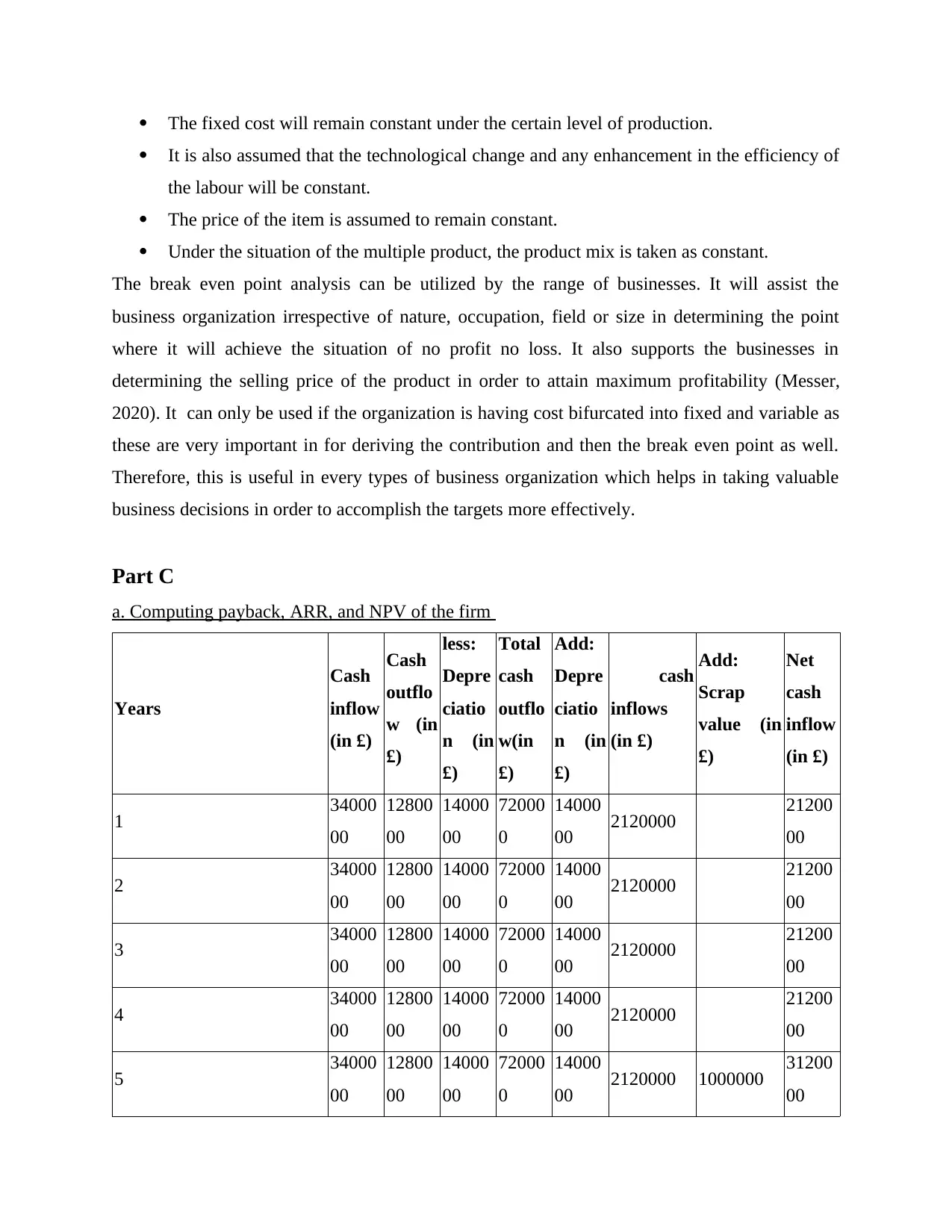

This assignment delves into core accounting and finance principles. Part A presents an income statement for Parksmead Ltd, including detailed working notes for calculations. Part B focuses on break-even analysis (BEP), determining contribution margins, calculating BEP and margin of safety, and evaluating a new sales strategy. Part C explores capital budgeting techniques by computing payback period, Average Rate of Return (ARR), and Net Present Value (NPV). It also explains the benefits and limitations of these tools and discusses the advantages and disadvantages of using budgets as a strategic technique. The assignment provides a comprehensive analysis of financial statements, cost-volume-profit analysis, and investment appraisal methods.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.