HI6028 Taxation Theory, Practice & Law: Partnership & FBT Analysis

VerifiedAdded on 2023/04/25

|11

|1800

|447

Homework Assignment

AI Summary

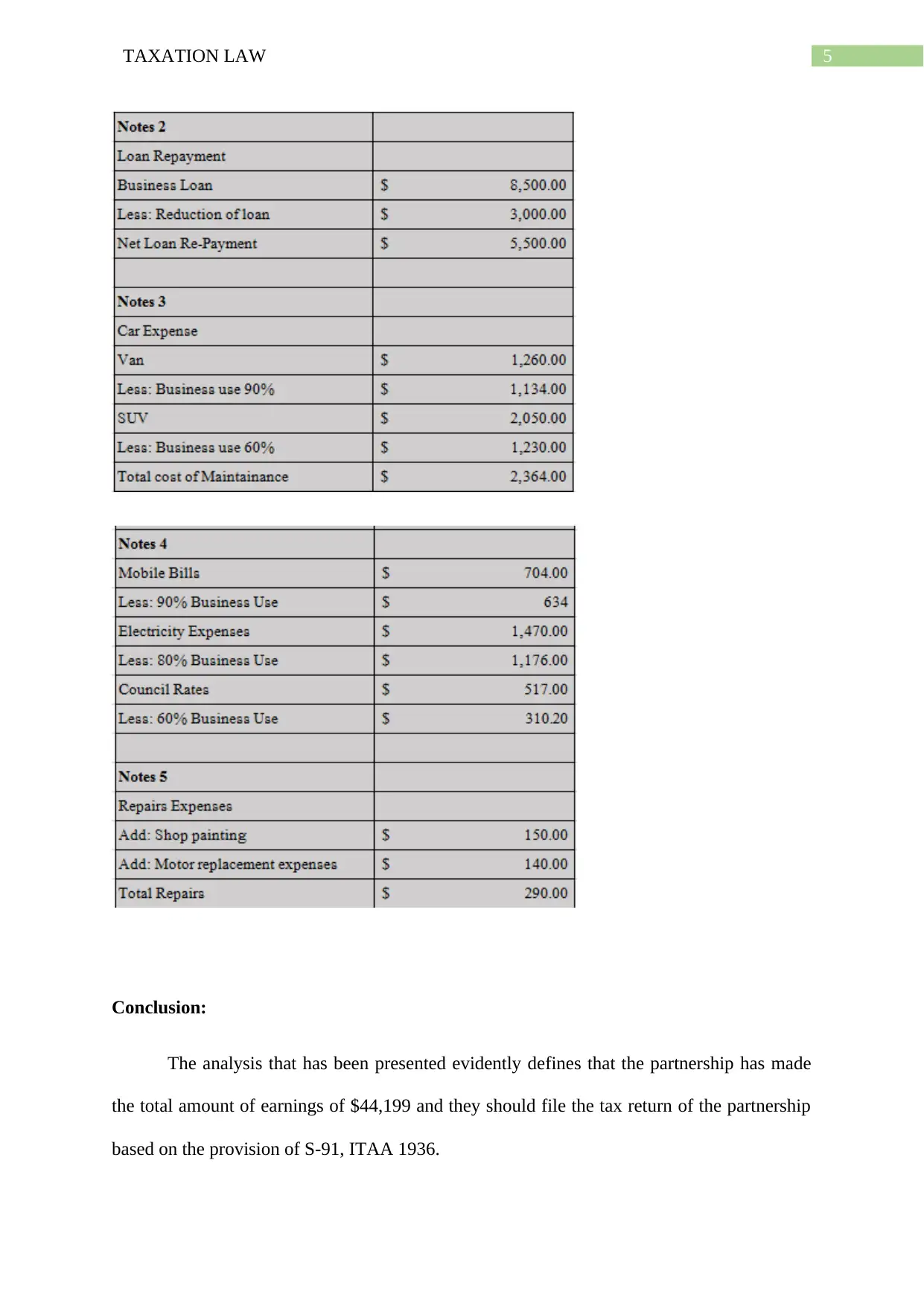

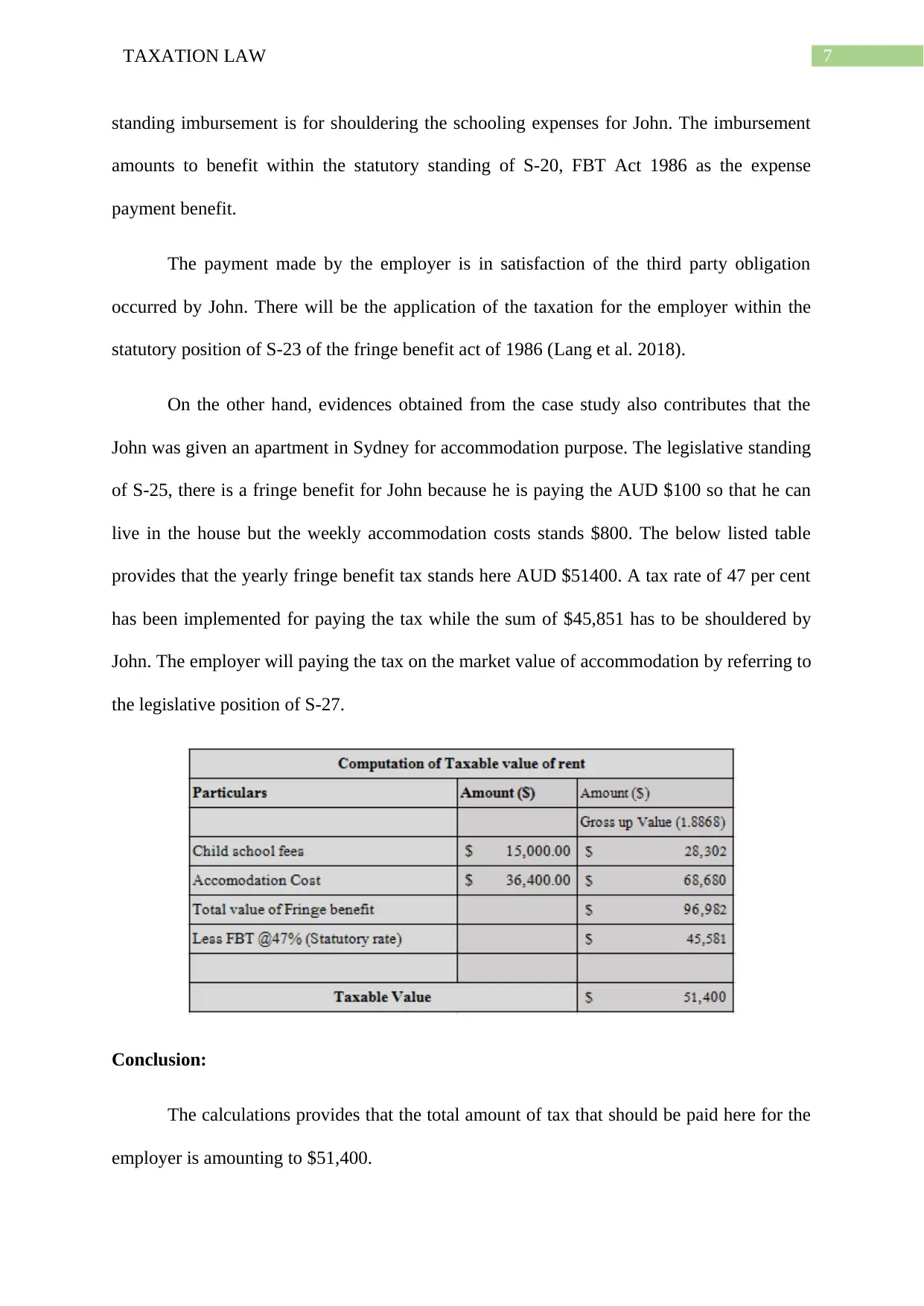

This assignment solution addresses two key taxation issues. The first question involves calculating the net earnings of a partnership (Brekkie and Lunch and OZ Bottle Shop) and determining the appropriate income distribution among partners, referencing Division 5 of the ITAA 1936 and relevant case law like FCT v Amalgamated Zinc Ltd. It identifies deductible expenses and capital outlays. The second question focuses on fringe benefit tax (FBT) consequences for an employer, specifically concerning expense payment fringe benefits and housing fringe benefits provided to an employee, citing sections of the FBTAA 1986. It calculates the FBT liability for the employer based on provided information and relevant tax rates. The document concludes by determining the total tax amount payable by the employer, providing a comprehensive analysis of the taxation implications in both scenarios.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.