HI6028 Taxation Law: Partnership Income and Fringe Benefits Analysis

VerifiedAdded on 2023/04/24

|13

|2786

|127

Homework Assignment

AI Summary

This assignment solution addresses a taxation law problem concerning a partnership, Brekkie and Lunch and OZ Bottle Shop. The solution begins by calculating the net income of the partnership, detailing the treatment of various income and expense items, including sales, car expenses, electricity, council rates, business insurance, mobile bills, union fees, account charges, repair expenses, interest on a loan, and depreciation. The calculation of depreciation uses both prime cost and diminishing value methods. The assignment then explores the implications of fringe benefits tax (FBT), specifically for a senior executive named John, calculating the taxable value of fringe benefits, considering exemptions, and determining the FBT payable. The solution references relevant sections of the Income Tax Assessment Act 1997 and the Fringe Benefits Tax Assessment Act 1986, providing detailed working notes and calculations to support the findings. The assignment is designed to provide a comprehensive understanding of partnership income and fringe benefit tax.

Taxation law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1: Calculation of net income in partnership................................................................3

General provisions related to the deduction.......................................................................3

Deduction of the expenses related to borrowing................................................................4

Provisions related to the depreciation................................................................................4

Deduction of the membership fee......................................................................................4

Question 2: Implications of fringe benefits tax..........................................................................9

References................................................................................................................................12

Question 1: Calculation of net income in partnership................................................................3

General provisions related to the deduction.......................................................................3

Deduction of the expenses related to borrowing................................................................4

Provisions related to the depreciation................................................................................4

Deduction of the membership fee......................................................................................4

Question 2: Implications of fringe benefits tax..........................................................................9

References................................................................................................................................12

QUESTION 1: CALCULATION OF NET INCOME IN PARTNERSHIP

Income tax assessment act 1997, Section 995-1(1), describe the partnership as an association

of the two or more persons running business as a partner in lieu of statutory income. In the

layman language, it can be said that partnership is the relationship between the two or more

than two people carrying out the commercial activity with the view of earning a profit

(Burkhauser, Hahn, and Wilkins, 2015). The partnership is not considered as the separate

legal entity from the persons carrying the business.

The income tax is levied only on the limited partnership, other than this there is no tax charge

on the partnership firm. Along with this, the deduction of the partnership loss is not allowed

from the assessable income of the partnership firm (Chardon, Freudenberg, and Brimble,

2016).

The present study is related to the determination of the net income of the partnership firm.

There are several provisions described under the income tax related to the deduction,

exemption, allowance and many others for the computation of the assessable income of the

firm (Chardon, Freudenberg and Brimble, 2016). The related provisions are described as

below –

General provisions related to the deduction

Generally, all the expenses incurred for producing the taxable income is allowed as

deduction. Income tax assessment act 1997, section 25-10 is related with the deduction in

case of repair and maintenance expenses incurred by the assessee. Generally, all the revenue

expenses are allowed as a deduction, and no deduction can be claimed of the capital

expenditure. Along with this, only that portion of the expenses can be claimed which is

related to the commercial activity. The term repair is not defined under the Act; it is

ascertained by considering the facts and circumstances.

Moreover, the repair on the initial installation is considered as the capital expenditure, and it

is not allowed as a deduction (Daley and Wood, 2016). Further, any expense which improves

the functional quality or substantially enhances the performance is regarded as the capital

expenditure, and the same is not allowed as deduction.

Income tax assessment act 1997, Section 995-1(1), describe the partnership as an association

of the two or more persons running business as a partner in lieu of statutory income. In the

layman language, it can be said that partnership is the relationship between the two or more

than two people carrying out the commercial activity with the view of earning a profit

(Burkhauser, Hahn, and Wilkins, 2015). The partnership is not considered as the separate

legal entity from the persons carrying the business.

The income tax is levied only on the limited partnership, other than this there is no tax charge

on the partnership firm. Along with this, the deduction of the partnership loss is not allowed

from the assessable income of the partnership firm (Chardon, Freudenberg, and Brimble,

2016).

The present study is related to the determination of the net income of the partnership firm.

There are several provisions described under the income tax related to the deduction,

exemption, allowance and many others for the computation of the assessable income of the

firm (Chardon, Freudenberg and Brimble, 2016). The related provisions are described as

below –

General provisions related to the deduction

Generally, all the expenses incurred for producing the taxable income is allowed as

deduction. Income tax assessment act 1997, section 25-10 is related with the deduction in

case of repair and maintenance expenses incurred by the assessee. Generally, all the revenue

expenses are allowed as a deduction, and no deduction can be claimed of the capital

expenditure. Along with this, only that portion of the expenses can be claimed which is

related to the commercial activity. The term repair is not defined under the Act; it is

ascertained by considering the facts and circumstances.

Moreover, the repair on the initial installation is considered as the capital expenditure, and it

is not allowed as a deduction (Daley and Wood, 2016). Further, any expense which improves

the functional quality or substantially enhances the performance is regarded as the capital

expenditure, and the same is not allowed as deduction.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As per the legal case law of Kitto J in W Thomas, expenditure incurred for maintenance of

the income-generating asset is considered as the revenue expenditure, and the same can be

claimed as a deduction.

Deduction of the expenses related to borrowing

All the expenses related to the borrowing are allowed as deduction if the borrowing is used

for the business. Generally, the expenses can be claimed during the term of the loan. The

payment of interest is allowed as a deduction (Doerrenberg, Peichl, and Siegloch, 2017).

Provisions related to the depreciation

Depreciation is allowed as a deduction from the income of the assessee. There is two methods

by which the depreciation can be computed, which are the prime cost method and the

diminishing value method (Feldstein, 2015).

Depreciation by the prime cost method

Cost of the asset*(days held/365)*100%/effective life of the asset

Depreciation by diminishing value method

If the asset is purchased before 10May 2006

Base Value*(days held/365)*150%/effective life of the asset

If the asset is purchased after 9 May 2006

Base Value*(days held/365)*200%/effective life of the asset

The income tax act prescribes the effective life of the asset separately, which is considered

while calculating the depreciation.

Deduction of the membership fee

Any payment related to the membership is allowed as a deduction only if the partner is the

member of that particular union.

the income-generating asset is considered as the revenue expenditure, and the same can be

claimed as a deduction.

Deduction of the expenses related to borrowing

All the expenses related to the borrowing are allowed as deduction if the borrowing is used

for the business. Generally, the expenses can be claimed during the term of the loan. The

payment of interest is allowed as a deduction (Doerrenberg, Peichl, and Siegloch, 2017).

Provisions related to the depreciation

Depreciation is allowed as a deduction from the income of the assessee. There is two methods

by which the depreciation can be computed, which are the prime cost method and the

diminishing value method (Feldstein, 2015).

Depreciation by the prime cost method

Cost of the asset*(days held/365)*100%/effective life of the asset

Depreciation by diminishing value method

If the asset is purchased before 10May 2006

Base Value*(days held/365)*150%/effective life of the asset

If the asset is purchased after 9 May 2006

Base Value*(days held/365)*200%/effective life of the asset

The income tax act prescribes the effective life of the asset separately, which is considered

while calculating the depreciation.

Deduction of the membership fee

Any payment related to the membership is allowed as a deduction only if the partner is the

member of that particular union.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

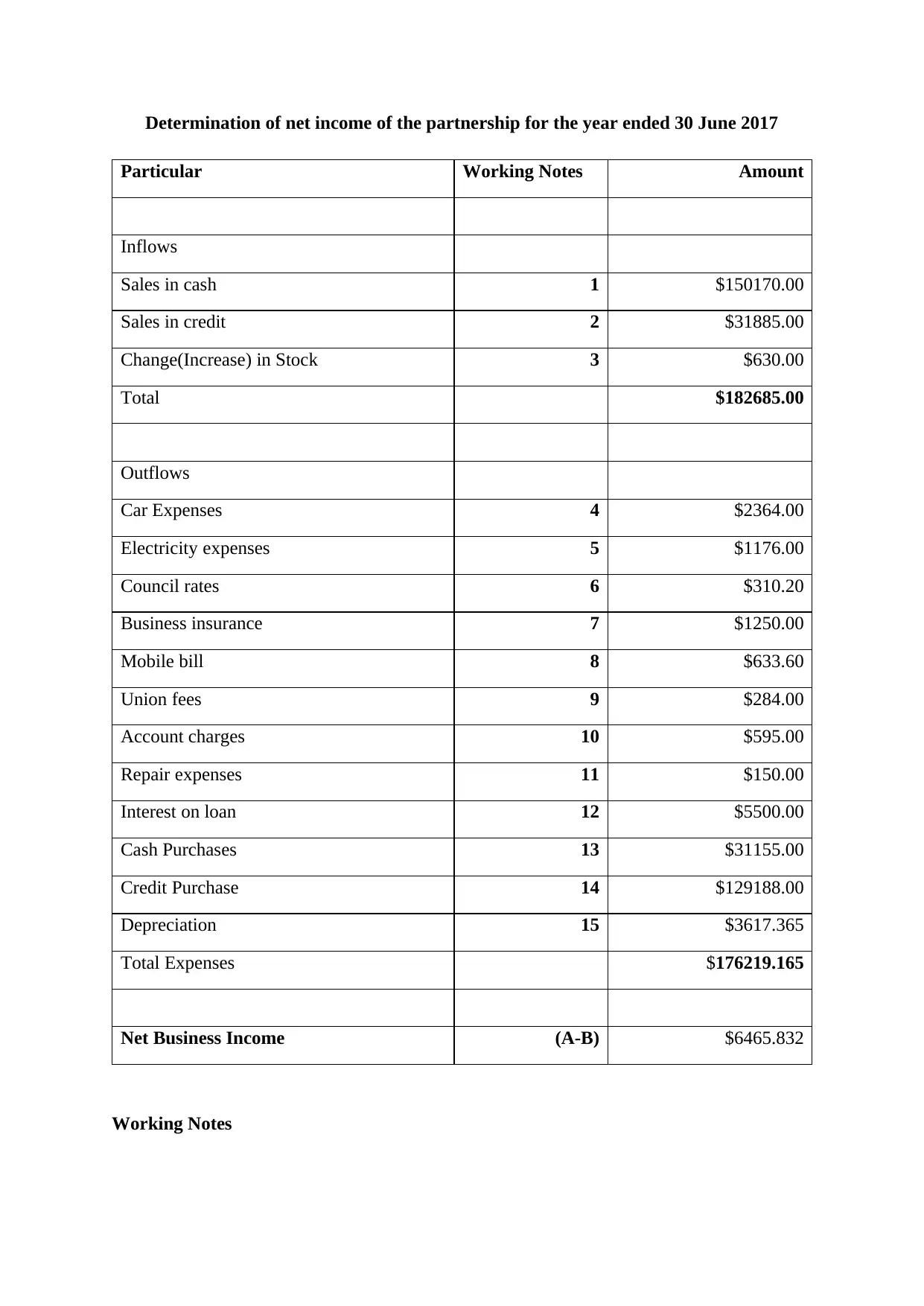

Determination of net income of the partnership for the year ended 30 June 2017

Particular Working Notes Amount

Inflows

Sales in cash 1 $150170.00

Sales in credit 2 $31885.00

Change(Increase) in Stock 3 $630.00

Total $182685.00

Outflows

Car Expenses 4 $2364.00

Electricity expenses 5 $1176.00

Council rates 6 $310.20

Business insurance 7 $1250.00

Mobile bill 8 $633.60

Union fees 9 $284.00

Account charges 10 $595.00

Repair expenses 11 $150.00

Interest on loan 12 $5500.00

Cash Purchases 13 $31155.00

Credit Purchase 14 $129188.00

Depreciation 15 $3617.365

Total Expenses $176219.165

Net Business Income (A-B) $6465.832

Working Notes

Particular Working Notes Amount

Inflows

Sales in cash 1 $150170.00

Sales in credit 2 $31885.00

Change(Increase) in Stock 3 $630.00

Total $182685.00

Outflows

Car Expenses 4 $2364.00

Electricity expenses 5 $1176.00

Council rates 6 $310.20

Business insurance 7 $1250.00

Mobile bill 8 $633.60

Union fees 9 $284.00

Account charges 10 $595.00

Repair expenses 11 $150.00

Interest on loan 12 $5500.00

Cash Purchases 13 $31155.00

Credit Purchase 14 $129188.00

Depreciation 15 $3617.365

Total Expenses $176219.165

Net Business Income (A-B) $6465.832

Working Notes

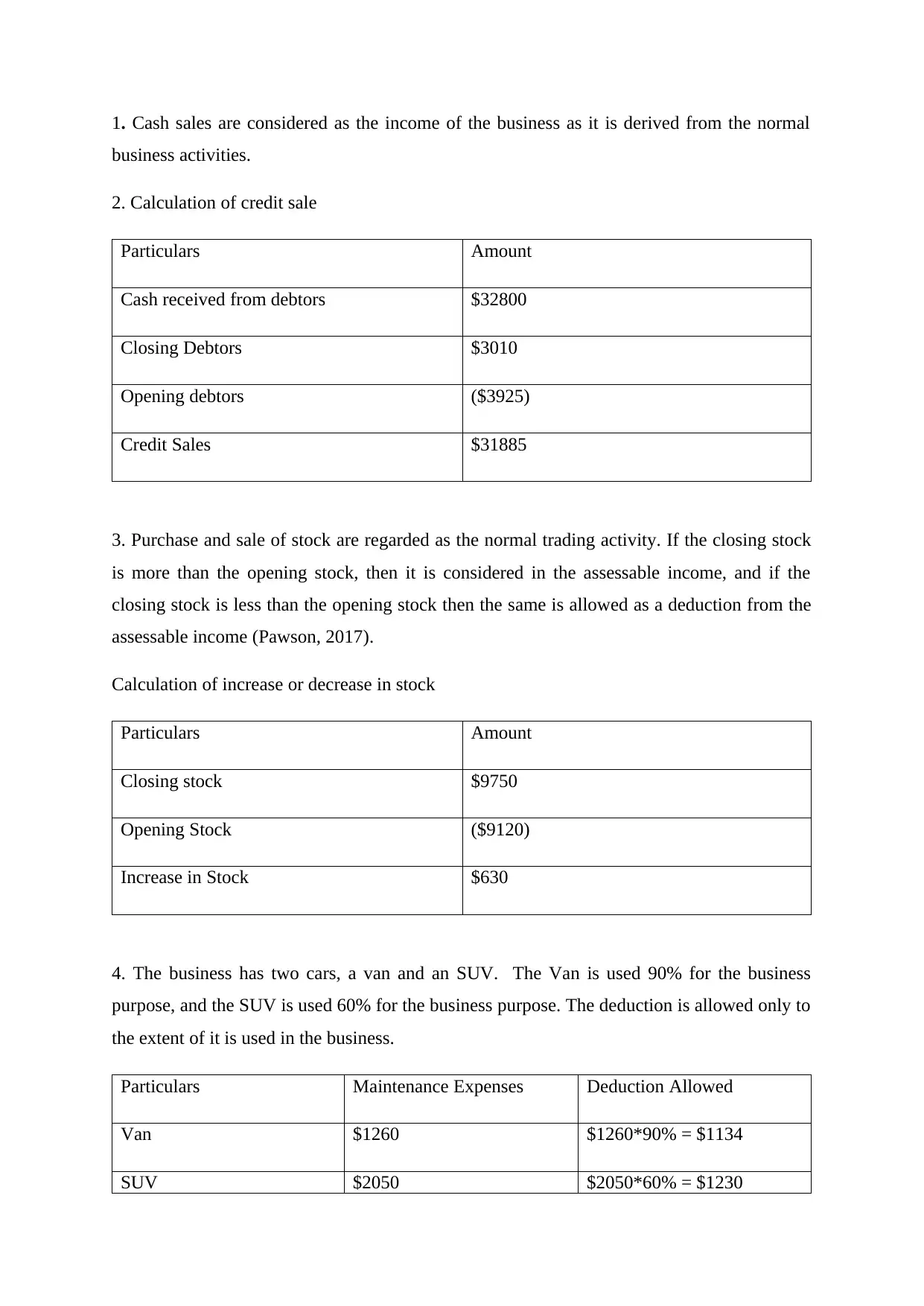

1. Cash sales are considered as the income of the business as it is derived from the normal

business activities.

2. Calculation of credit sale

Particulars Amount

Cash received from debtors $32800

Closing Debtors $3010

Opening debtors ($3925)

Credit Sales $31885

3. Purchase and sale of stock are regarded as the normal trading activity. If the closing stock

is more than the opening stock, then it is considered in the assessable income, and if the

closing stock is less than the opening stock then the same is allowed as a deduction from the

assessable income (Pawson, 2017).

Calculation of increase or decrease in stock

Particulars Amount

Closing stock $9750

Opening Stock ($9120)

Increase in Stock $630

4. The business has two cars, a van and an SUV. The Van is used 90% for the business

purpose, and the SUV is used 60% for the business purpose. The deduction is allowed only to

the extent of it is used in the business.

Particulars Maintenance Expenses Deduction Allowed

Van $1260 $1260*90% = $1134

SUV $2050 $2050*60% = $1230

business activities.

2. Calculation of credit sale

Particulars Amount

Cash received from debtors $32800

Closing Debtors $3010

Opening debtors ($3925)

Credit Sales $31885

3. Purchase and sale of stock are regarded as the normal trading activity. If the closing stock

is more than the opening stock, then it is considered in the assessable income, and if the

closing stock is less than the opening stock then the same is allowed as a deduction from the

assessable income (Pawson, 2017).

Calculation of increase or decrease in stock

Particulars Amount

Closing stock $9750

Opening Stock ($9120)

Increase in Stock $630

4. The business has two cars, a van and an SUV. The Van is used 90% for the business

purpose, and the SUV is used 60% for the business purpose. The deduction is allowed only to

the extent of it is used in the business.

Particulars Maintenance Expenses Deduction Allowed

Van $1260 $1260*90% = $1134

SUV $2050 $2050*60% = $1230

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total Deduction $2364

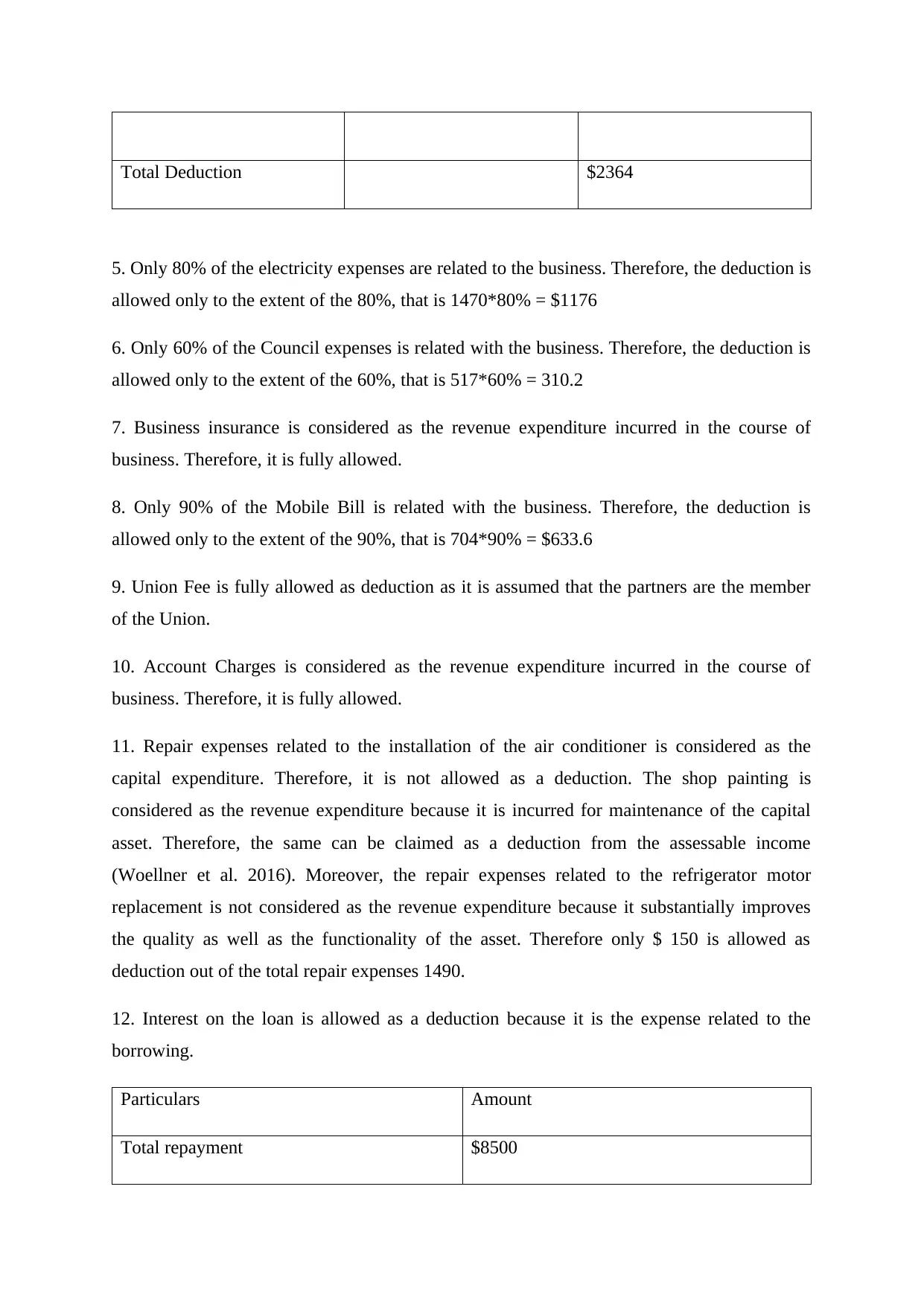

5. Only 80% of the electricity expenses are related to the business. Therefore, the deduction is

allowed only to the extent of the 80%, that is 1470*80% = $1176

6. Only 60% of the Council expenses is related with the business. Therefore, the deduction is

allowed only to the extent of the 60%, that is 517*60% = 310.2

7. Business insurance is considered as the revenue expenditure incurred in the course of

business. Therefore, it is fully allowed.

8. Only 90% of the Mobile Bill is related with the business. Therefore, the deduction is

allowed only to the extent of the 90%, that is 704*90% = $633.6

9. Union Fee is fully allowed as deduction as it is assumed that the partners are the member

of the Union.

10. Account Charges is considered as the revenue expenditure incurred in the course of

business. Therefore, it is fully allowed.

11. Repair expenses related to the installation of the air conditioner is considered as the

capital expenditure. Therefore, it is not allowed as a deduction. The shop painting is

considered as the revenue expenditure because it is incurred for maintenance of the capital

asset. Therefore, the same can be claimed as a deduction from the assessable income

(Woellner et al. 2016). Moreover, the repair expenses related to the refrigerator motor

replacement is not considered as the revenue expenditure because it substantially improves

the quality as well as the functionality of the asset. Therefore only $ 150 is allowed as

deduction out of the total repair expenses 1490.

12. Interest on the loan is allowed as a deduction because it is the expense related to the

borrowing.

Particulars Amount

Total repayment $8500

5. Only 80% of the electricity expenses are related to the business. Therefore, the deduction is

allowed only to the extent of the 80%, that is 1470*80% = $1176

6. Only 60% of the Council expenses is related with the business. Therefore, the deduction is

allowed only to the extent of the 60%, that is 517*60% = 310.2

7. Business insurance is considered as the revenue expenditure incurred in the course of

business. Therefore, it is fully allowed.

8. Only 90% of the Mobile Bill is related with the business. Therefore, the deduction is

allowed only to the extent of the 90%, that is 704*90% = $633.6

9. Union Fee is fully allowed as deduction as it is assumed that the partners are the member

of the Union.

10. Account Charges is considered as the revenue expenditure incurred in the course of

business. Therefore, it is fully allowed.

11. Repair expenses related to the installation of the air conditioner is considered as the

capital expenditure. Therefore, it is not allowed as a deduction. The shop painting is

considered as the revenue expenditure because it is incurred for maintenance of the capital

asset. Therefore, the same can be claimed as a deduction from the assessable income

(Woellner et al. 2016). Moreover, the repair expenses related to the refrigerator motor

replacement is not considered as the revenue expenditure because it substantially improves

the quality as well as the functionality of the asset. Therefore only $ 150 is allowed as

deduction out of the total repair expenses 1490.

12. Interest on the loan is allowed as a deduction because it is the expense related to the

borrowing.

Particulars Amount

Total repayment $8500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Principal Amount $3000

Amount of Interest $5500

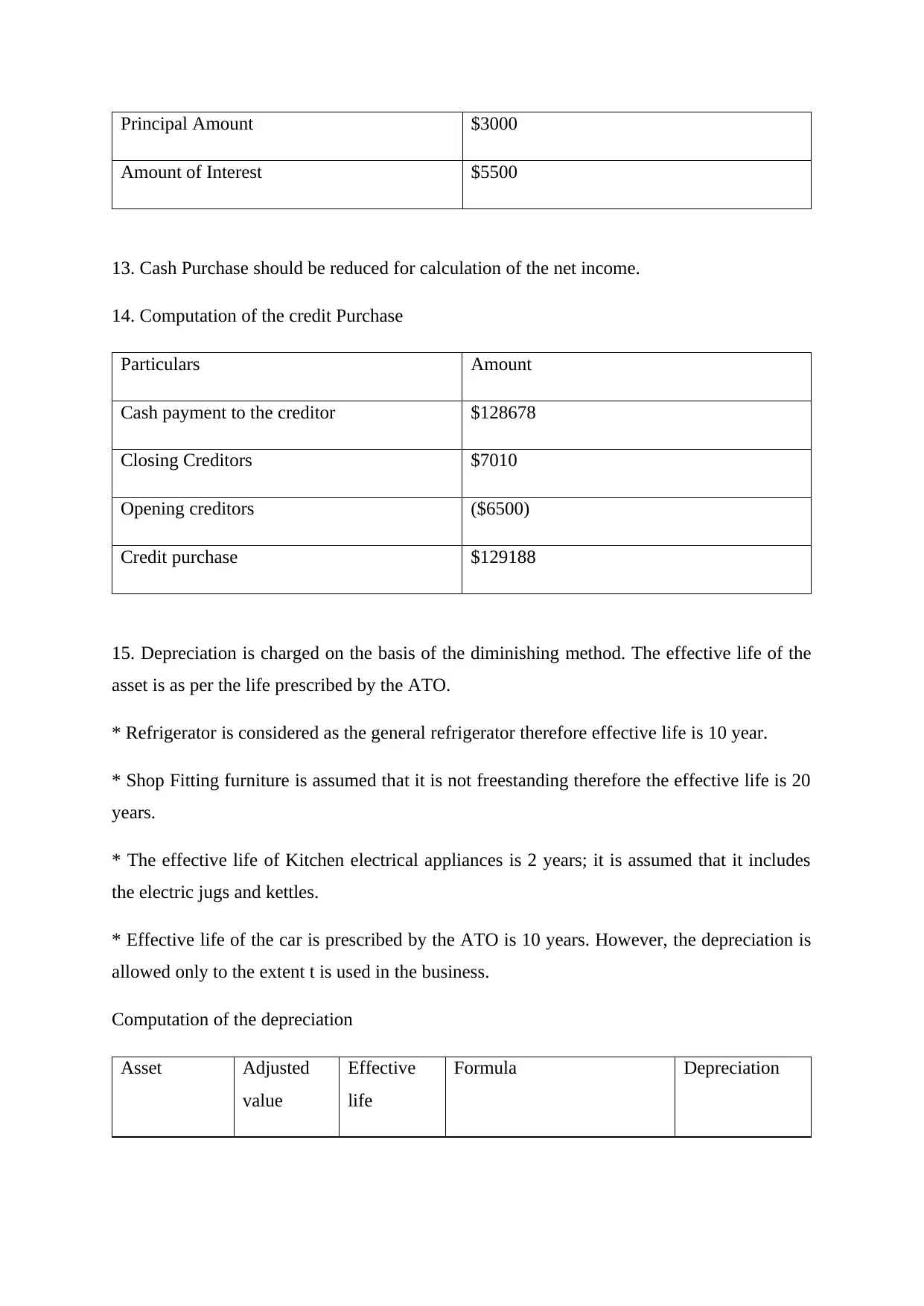

13. Cash Purchase should be reduced for calculation of the net income.

14. Computation of the credit Purchase

Particulars Amount

Cash payment to the creditor $128678

Closing Creditors $7010

Opening creditors ($6500)

Credit purchase $129188

15. Depreciation is charged on the basis of the diminishing method. The effective life of the

asset is as per the life prescribed by the ATO.

* Refrigerator is considered as the general refrigerator therefore effective life is 10 year.

* Shop Fitting furniture is assumed that it is not freestanding therefore the effective life is 20

years.

* The effective life of Kitchen electrical appliances is 2 years; it is assumed that it includes

the electric jugs and kettles.

* Effective life of the car is prescribed by the ATO is 10 years. However, the depreciation is

allowed only to the extent t is used in the business.

Computation of the depreciation

Asset Adjusted

value

Effective

life

Formula Depreciation

Amount of Interest $5500

13. Cash Purchase should be reduced for calculation of the net income.

14. Computation of the credit Purchase

Particulars Amount

Cash payment to the creditor $128678

Closing Creditors $7010

Opening creditors ($6500)

Credit purchase $129188

15. Depreciation is charged on the basis of the diminishing method. The effective life of the

asset is as per the life prescribed by the ATO.

* Refrigerator is considered as the general refrigerator therefore effective life is 10 year.

* Shop Fitting furniture is assumed that it is not freestanding therefore the effective life is 20

years.

* The effective life of Kitchen electrical appliances is 2 years; it is assumed that it includes

the electric jugs and kettles.

* Effective life of the car is prescribed by the ATO is 10 years. However, the depreciation is

allowed only to the extent t is used in the business.

Computation of the depreciation

Asset Adjusted

value

Effective

life

Formula Depreciation

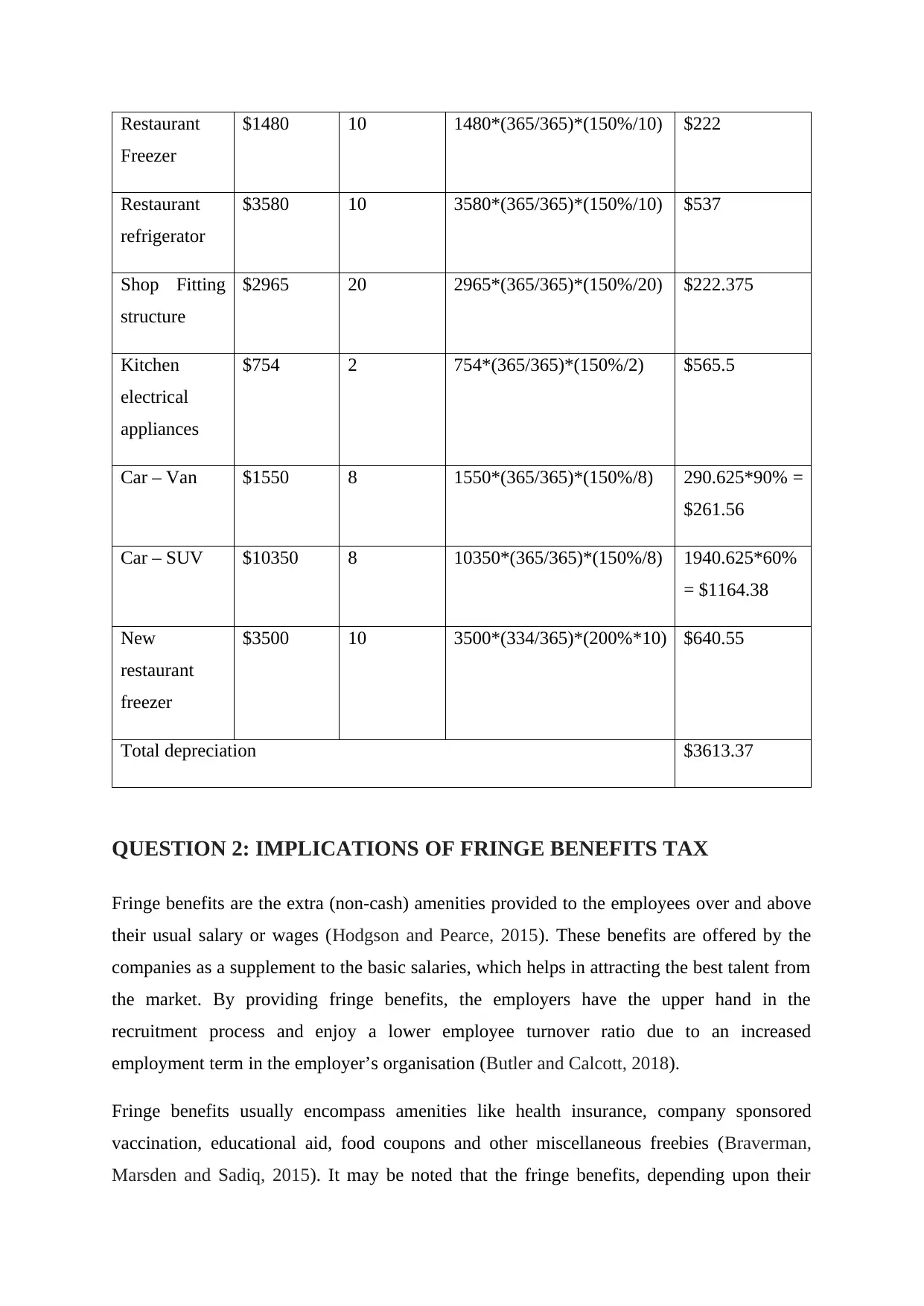

Restaurant

Freezer

$1480 10 1480*(365/365)*(150%/10) $222

Restaurant

refrigerator

$3580 10 3580*(365/365)*(150%/10) $537

Shop Fitting

structure

$2965 20 2965*(365/365)*(150%/20) $222.375

Kitchen

electrical

appliances

$754 2 754*(365/365)*(150%/2) $565.5

Car – Van $1550 8 1550*(365/365)*(150%/8) 290.625*90% =

$261.56

Car – SUV $10350 8 10350*(365/365)*(150%/8) 1940.625*60%

= $1164.38

New

restaurant

freezer

$3500 10 3500*(334/365)*(200%*10) $640.55

Total depreciation $3613.37

QUESTION 2: IMPLICATIONS OF FRINGE BENEFITS TAX

Fringe benefits are the extra (non-cash) amenities provided to the employees over and above

their usual salary or wages (Hodgson and Pearce, 2015). These benefits are offered by the

companies as a supplement to the basic salaries, which helps in attracting the best talent from

the market. By providing fringe benefits, the employers have the upper hand in the

recruitment process and enjoy a lower employee turnover ratio due to an increased

employment term in the employer’s organisation (Butler and Calcott, 2018).

Fringe benefits usually encompass amenities like health insurance, company sponsored

vaccination, educational aid, food coupons and other miscellaneous freebies (Braverman,

Marsden and Sadiq, 2015). It may be noted that the fringe benefits, depending upon their

Freezer

$1480 10 1480*(365/365)*(150%/10) $222

Restaurant

refrigerator

$3580 10 3580*(365/365)*(150%/10) $537

Shop Fitting

structure

$2965 20 2965*(365/365)*(150%/20) $222.375

Kitchen

electrical

appliances

$754 2 754*(365/365)*(150%/2) $565.5

Car – Van $1550 8 1550*(365/365)*(150%/8) 290.625*90% =

$261.56

Car – SUV $10350 8 10350*(365/365)*(150%/8) 1940.625*60%

= $1164.38

New

restaurant

freezer

$3500 10 3500*(334/365)*(200%*10) $640.55

Total depreciation $3613.37

QUESTION 2: IMPLICATIONS OF FRINGE BENEFITS TAX

Fringe benefits are the extra (non-cash) amenities provided to the employees over and above

their usual salary or wages (Hodgson and Pearce, 2015). These benefits are offered by the

companies as a supplement to the basic salaries, which helps in attracting the best talent from

the market. By providing fringe benefits, the employers have the upper hand in the

recruitment process and enjoy a lower employee turnover ratio due to an increased

employment term in the employer’s organisation (Butler and Calcott, 2018).

Fringe benefits usually encompass amenities like health insurance, company sponsored

vaccination, educational aid, food coupons and other miscellaneous freebies (Braverman,

Marsden and Sadiq, 2015). It may be noted that the fringe benefits, depending upon their

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

categorisation done by the Internal Revenue Department, might be brought within the scope

of taxation. However, the liability to discharge the fringe benefits tax lies upon the employer

and not the employee, under the Australian tax system vide the Fringe Benefits Tax

Assessment Act, 1986 (Tang and Wan, 2015).

Applicable Provisions and Laws

The FBT (Fringe Benefits Tax) rate for the FBT year ending March 2019 is fixed at 47%, a

sum total of the highest marginal tax rate which tantamounts to 45% and the Medicare Levy

currently fixed at 2%, to be paid by the employer. The taxable amount of the fringe benefits

will be calculated as follows: -

Gross Value of the Fringe Benefits Paid by the Employer

Less: Any Reimbursement, whether in Part or Full, Made by the Employee

= Taxable Amount of Fringe Benefits

However, it shall be noted that the Fringe Benefits Tax is imposed only if the value exceeds

the threshold limit, and is even exempt in some cases. Following are the fringe benefits that

are exempted under the Australian tax system:-

Employee Relocation Expenditure

Backward Area Accommodation

House Rent Allowance, subject to certain conditions

Other ancillary benefits such as free laptops, briefcases and mobile phones.

FBT Consequences in John’s Case

In the given case, John, a senior executive in a printing company is receiving fringe benefits

to the tune of $56, 600, calculated as follows: -

Child’s Education Allowance = $15, 000

Add: Apartment Accommodation = $41, 600 ($800 per week x 52 weeks)

Total Fringe Benefits Provided = $56, 600

Since the above two benefits do not fall in the exemption list, the liability to pay the FBT

persists upon the employer. However, the amount paid by John in respect of the

of taxation. However, the liability to discharge the fringe benefits tax lies upon the employer

and not the employee, under the Australian tax system vide the Fringe Benefits Tax

Assessment Act, 1986 (Tang and Wan, 2015).

Applicable Provisions and Laws

The FBT (Fringe Benefits Tax) rate for the FBT year ending March 2019 is fixed at 47%, a

sum total of the highest marginal tax rate which tantamounts to 45% and the Medicare Levy

currently fixed at 2%, to be paid by the employer. The taxable amount of the fringe benefits

will be calculated as follows: -

Gross Value of the Fringe Benefits Paid by the Employer

Less: Any Reimbursement, whether in Part or Full, Made by the Employee

= Taxable Amount of Fringe Benefits

However, it shall be noted that the Fringe Benefits Tax is imposed only if the value exceeds

the threshold limit, and is even exempt in some cases. Following are the fringe benefits that

are exempted under the Australian tax system:-

Employee Relocation Expenditure

Backward Area Accommodation

House Rent Allowance, subject to certain conditions

Other ancillary benefits such as free laptops, briefcases and mobile phones.

FBT Consequences in John’s Case

In the given case, John, a senior executive in a printing company is receiving fringe benefits

to the tune of $56, 600, calculated as follows: -

Child’s Education Allowance = $15, 000

Add: Apartment Accommodation = $41, 600 ($800 per week x 52 weeks)

Total Fringe Benefits Provided = $56, 600

Since the above two benefits do not fall in the exemption list, the liability to pay the FBT

persists upon the employer. However, the amount paid by John in respect of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accommodation will be deducted from the gross taxable value, and the final amount

chargeable to tax will be: -

Gross Value of Fringe Benefits Provided (as calculated above) = $56, 600

Less: Reimbursement Value to be Deducted ($100 x 52 weeks) = $5, 200

Net Taxable Value of Fringe Benefits = $51, 400

Since the above fringe benefits fall in type 2 (lower gross up rate) category, no GST credit

claim will be available. Hence, the calculation for FBT for the year ending March 2019 in

John’s case will be: -

Net Taxable Value of Fringe Benefits x FBT Rate x Type 2 Gross-up Rate

= $51, 400 x 47% x 1.8868

Fringe Benefits Tax = $45, 581.3144

chargeable to tax will be: -

Gross Value of Fringe Benefits Provided (as calculated above) = $56, 600

Less: Reimbursement Value to be Deducted ($100 x 52 weeks) = $5, 200

Net Taxable Value of Fringe Benefits = $51, 400

Since the above fringe benefits fall in type 2 (lower gross up rate) category, no GST credit

claim will be available. Hence, the calculation for FBT for the year ending March 2019 in

John’s case will be: -

Net Taxable Value of Fringe Benefits x FBT Rate x Type 2 Gross-up Rate

= $51, 400 x 47% x 1.8868

Fringe Benefits Tax = $45, 581.3144

REFERENCES

Braverman, D., Marsden, S. and Sadiq, K., 2015. Assessing Taxpayer Response to Legislative

Changes: A Case Study of In-House Fringe Benefits Rules. J. Austl. Tax'n, 17, p.1.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Butler, C. and Calcott, P., 2018. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, 25(3), pp.654-672.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Chardon, T., Freudenberg, B., & Brimble, M. 2016. Tax literacy in Australia: not knowing your

deduction from your offset. Austl. Tax F., 31, 321.

Daley, J. and Wood, D., 2016. Fiscal challenges for Australia: The next decade and beyond. Asia

& the Pacific Policy Studies, 3(3), pp.475-494.

Doerrenberg, P., Peichl, A. and Siegloch, S., 2017. The elasticity of taxable income in the

presence of deduction possibilities. Journal of Public Economics, 151, pp.41-55.

Feldstein, M., 2015. Raising revenue by limiting tax expenditures. Tax Policy and

Economy, 29(1), pp.1-11.

Hodgson, H. and Pearce, P., 2015. TravelSmart or travel tax breaks: is the fringe benefits tax a

barrier to active commuting in Australia? 1. eJournal of Tax Research, 13(3), p.819.

Pawson, M. 2017. Reflections on the Australian tax system. Taxation in Australia, 52(3), 106.

Tang, R. and Wan, J., 2015. Fringe benefits tax and fly-in fly-out arrangements: John Holland

Group Pty Ltd v Commissioner of Taxation. Australian Resources and Energy Law

Journal, 34(1), p.17.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. 2016. Australian Taxation Law

2016. OUP Catalogue.

Braverman, D., Marsden, S. and Sadiq, K., 2015. Assessing Taxpayer Response to Legislative

Changes: A Case Study of In-House Fringe Benefits Rules. J. Austl. Tax'n, 17, p.1.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Butler, C. and Calcott, P., 2018. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, 25(3), pp.654-672.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Chardon, T., Freudenberg, B., & Brimble, M. 2016. Tax literacy in Australia: not knowing your

deduction from your offset. Austl. Tax F., 31, 321.

Daley, J. and Wood, D., 2016. Fiscal challenges for Australia: The next decade and beyond. Asia

& the Pacific Policy Studies, 3(3), pp.475-494.

Doerrenberg, P., Peichl, A. and Siegloch, S., 2017. The elasticity of taxable income in the

presence of deduction possibilities. Journal of Public Economics, 151, pp.41-55.

Feldstein, M., 2015. Raising revenue by limiting tax expenditures. Tax Policy and

Economy, 29(1), pp.1-11.

Hodgson, H. and Pearce, P., 2015. TravelSmart or travel tax breaks: is the fringe benefits tax a

barrier to active commuting in Australia? 1. eJournal of Tax Research, 13(3), p.819.

Pawson, M. 2017. Reflections on the Australian tax system. Taxation in Australia, 52(3), 106.

Tang, R. and Wan, J., 2015. Fringe benefits tax and fly-in fly-out arrangements: John Holland

Group Pty Ltd v Commissioner of Taxation. Australian Resources and Energy Law

Journal, 34(1), p.17.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. 2016. Australian Taxation Law

2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.