Taxation Calculation: Analyzing Partnership and Individual Tax Returns

VerifiedAdded on 2020/07/23

|8

|2017

|42

Homework Assignment

AI Summary

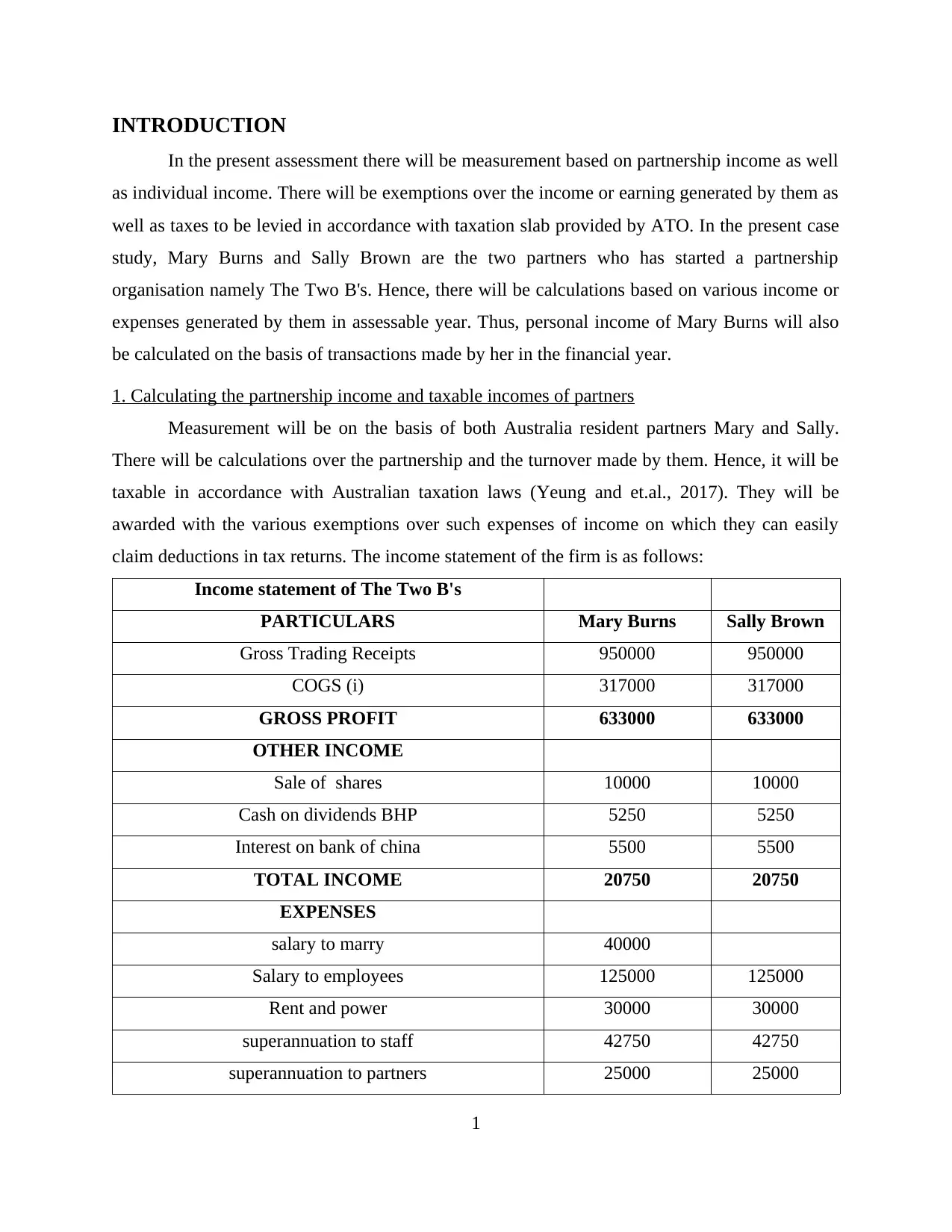

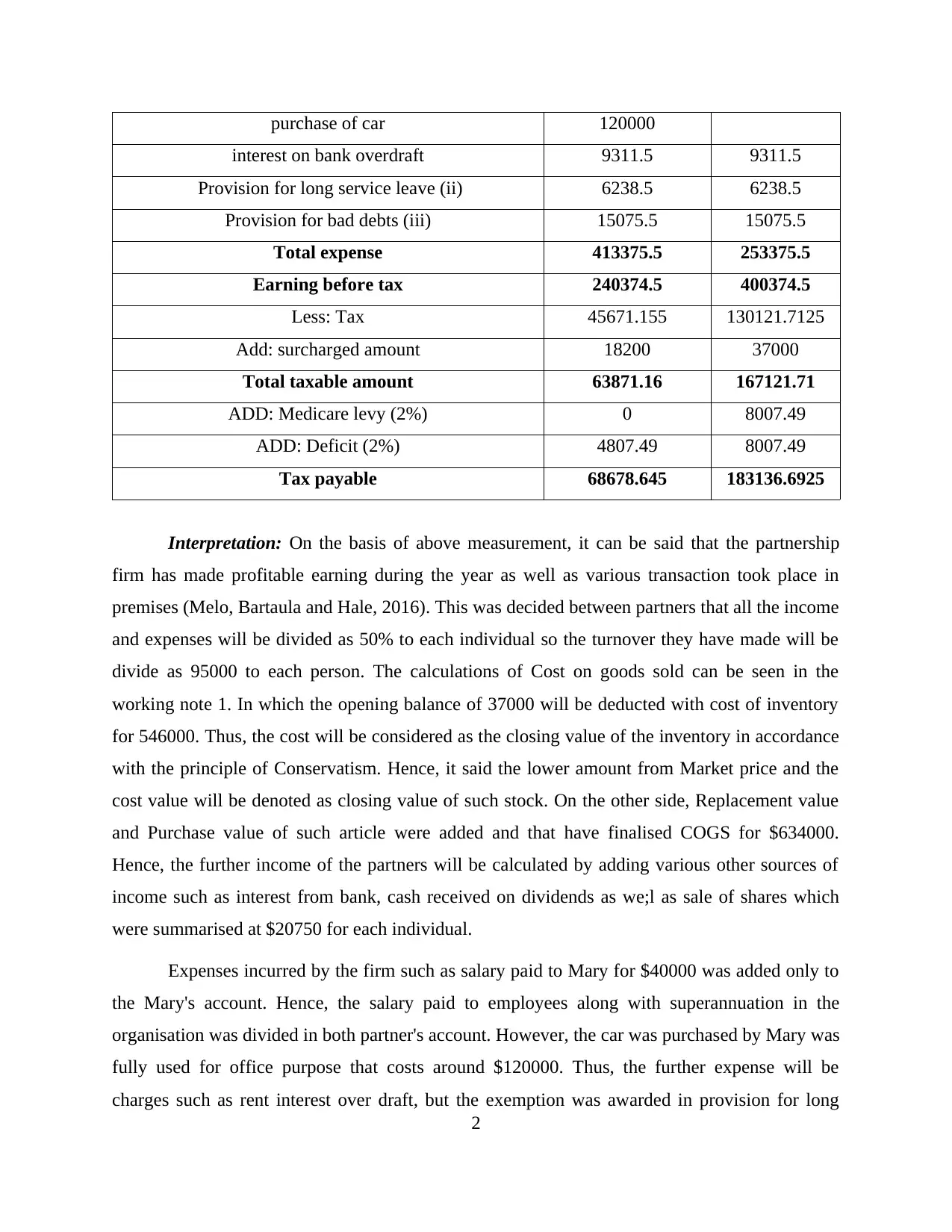

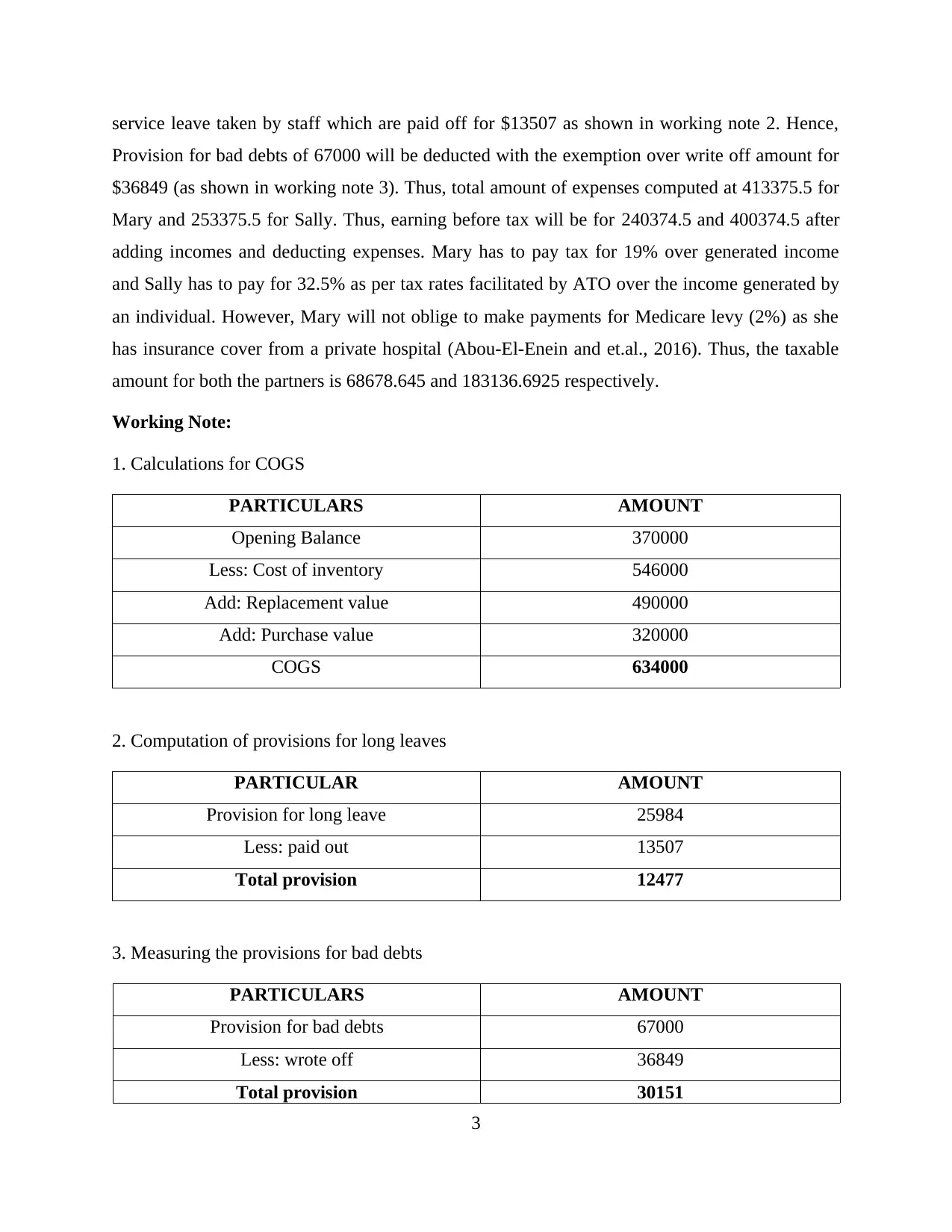

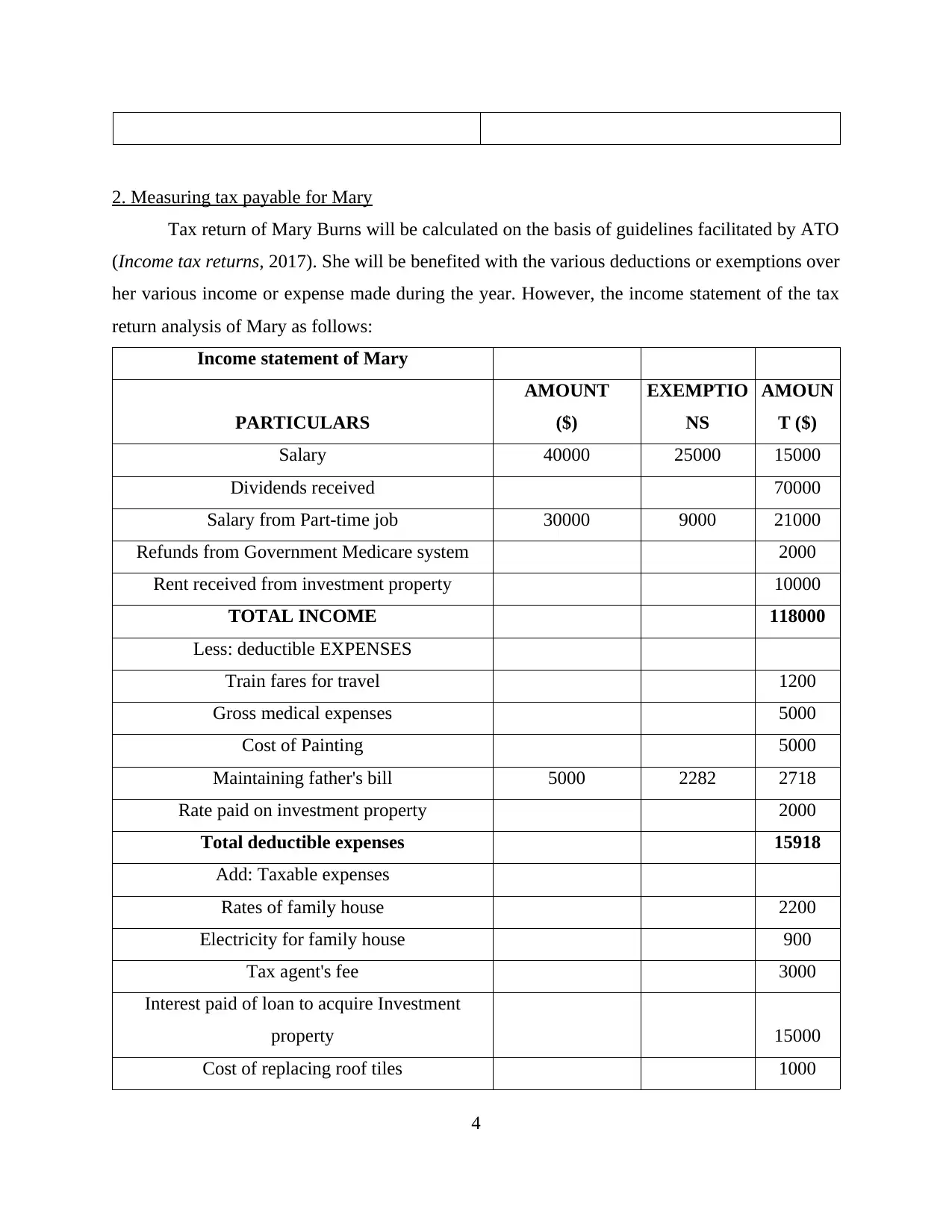

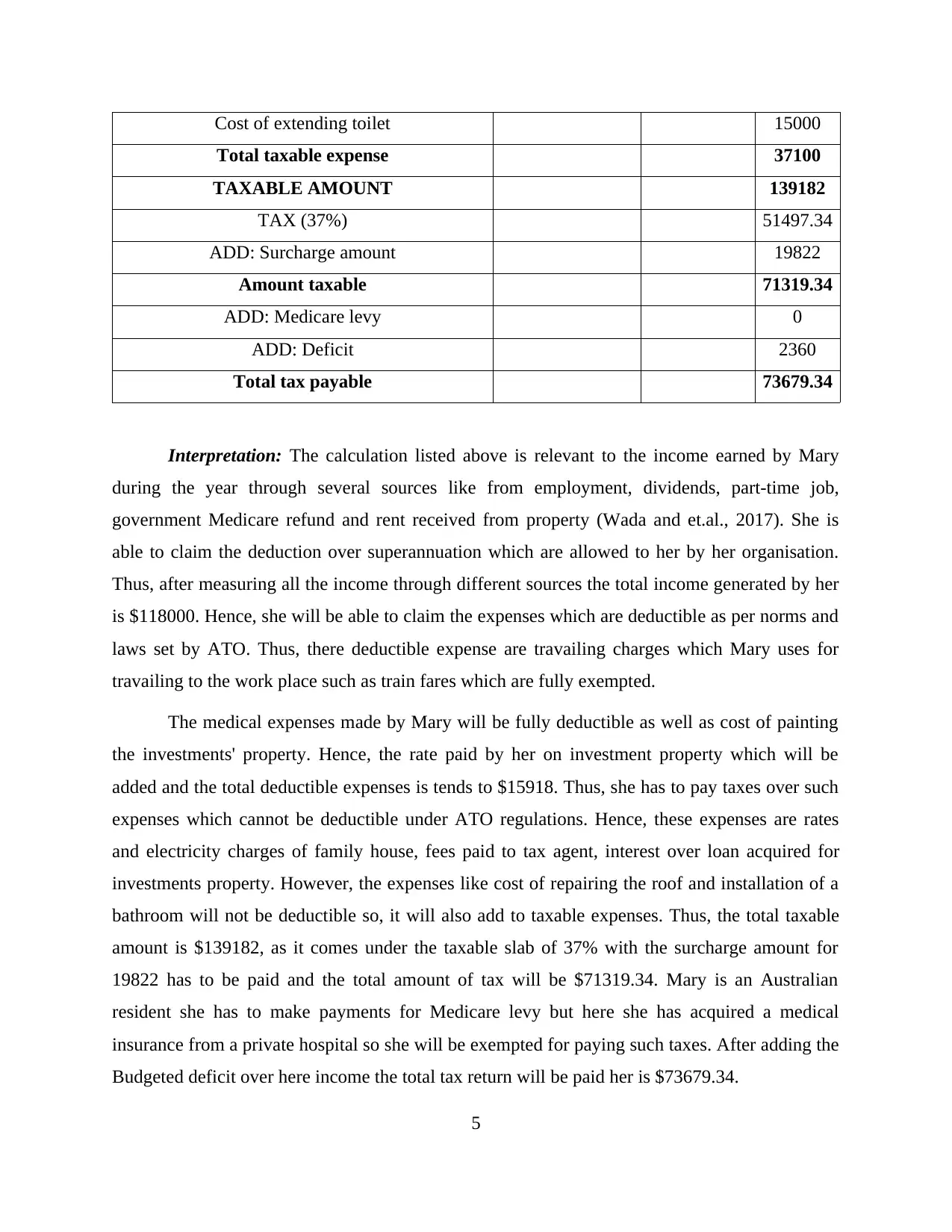

This assignment focuses on calculating the partnership and individual income tax liabilities for 'The Two B's,' a partnership comprising Mary Burns and Sally Brown, based on Australian taxation laws. The analysis includes calculating partnership income, cost of goods sold (COGS), and taxable income for each partner, accounting for various income sources, expenses, and deductions such as salaries, superannuation, and provisions for bad debts. The assignment also details Mary's individual tax return, considering her income from employment, dividends, and investments, along with deductible and taxable expenses. The calculations incorporate relevant tax rates, surcharges, and Medicare levies, culminating in the determination of the total tax payable for both the partnership and Mary, providing a comprehensive overview of the tax implications for both business and personal finances. The assignment references relevant working notes and Australian tax guidelines.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.