Taxation of Partnerships: Income Statements and Tax Calculations

VerifiedAdded on 2020/05/08

|9

|1590

|73

Homework Assignment

AI Summary

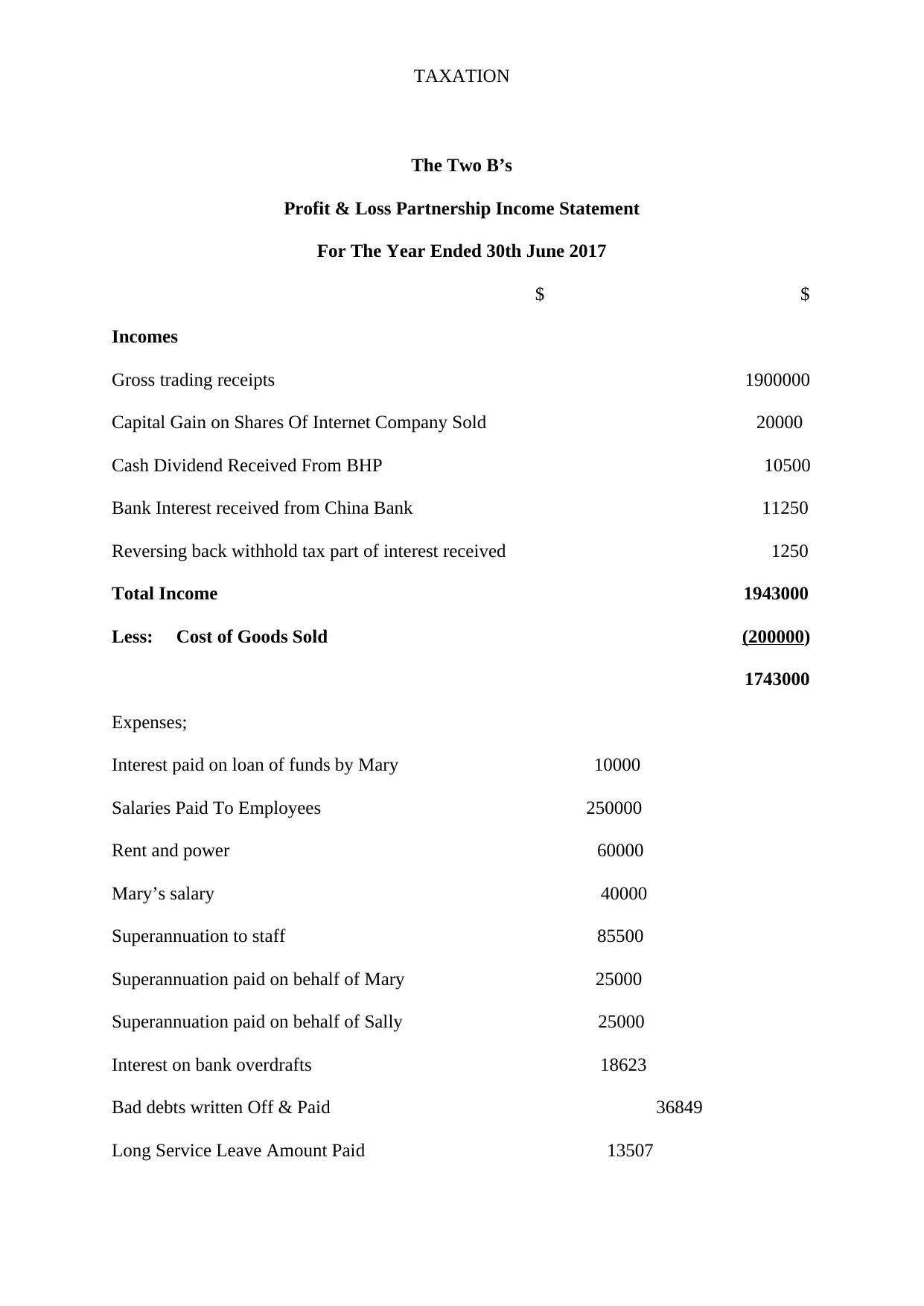

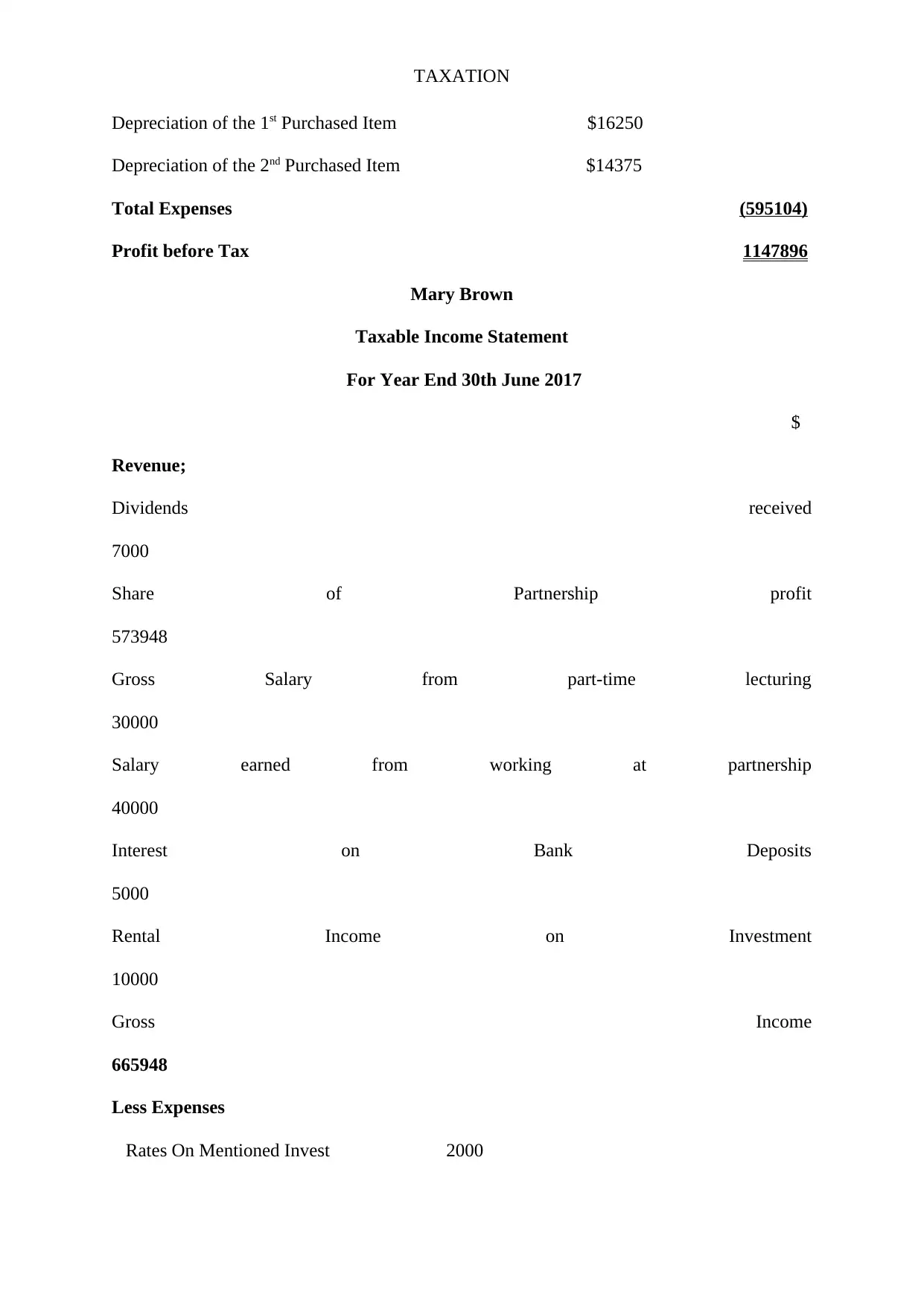

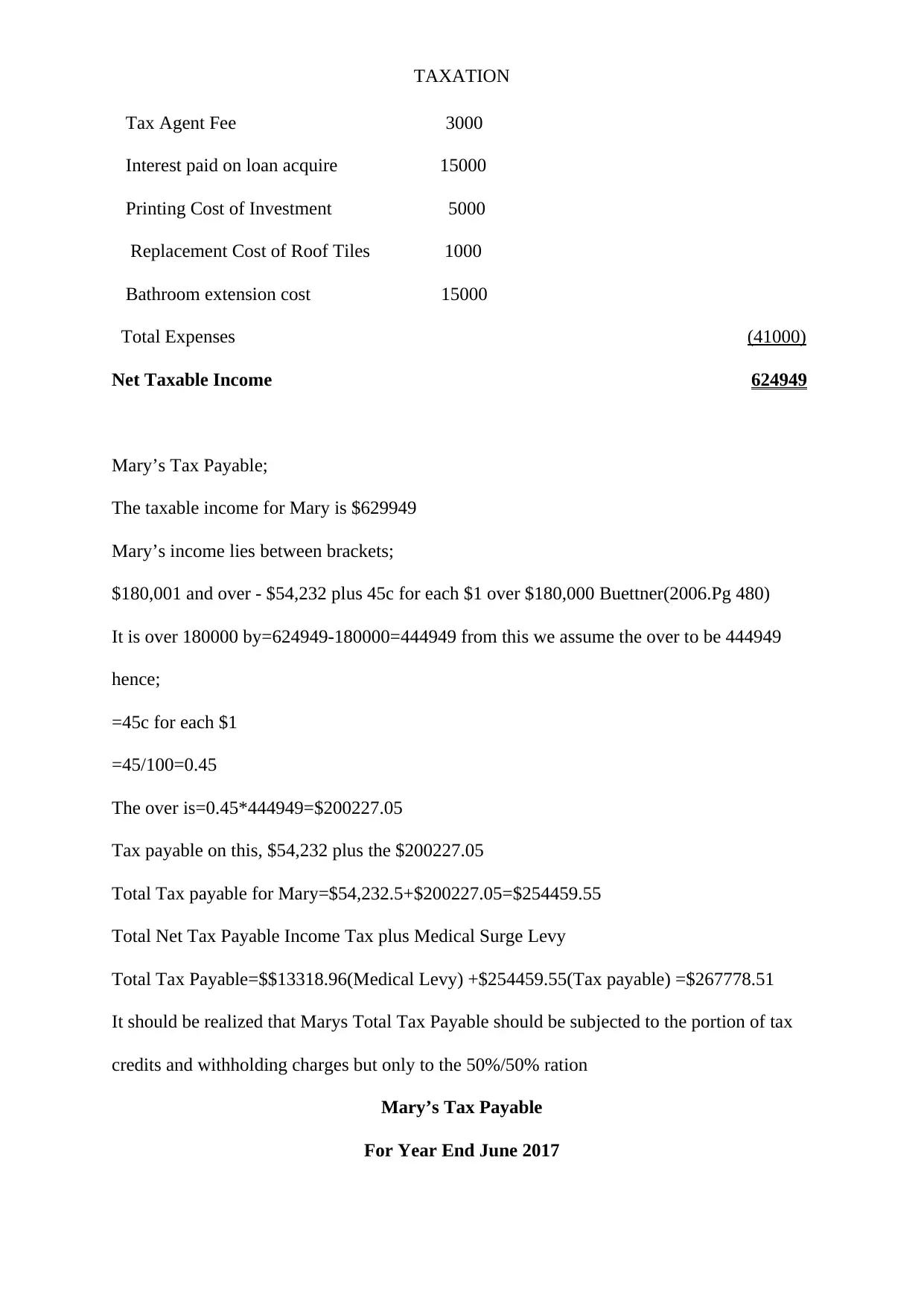

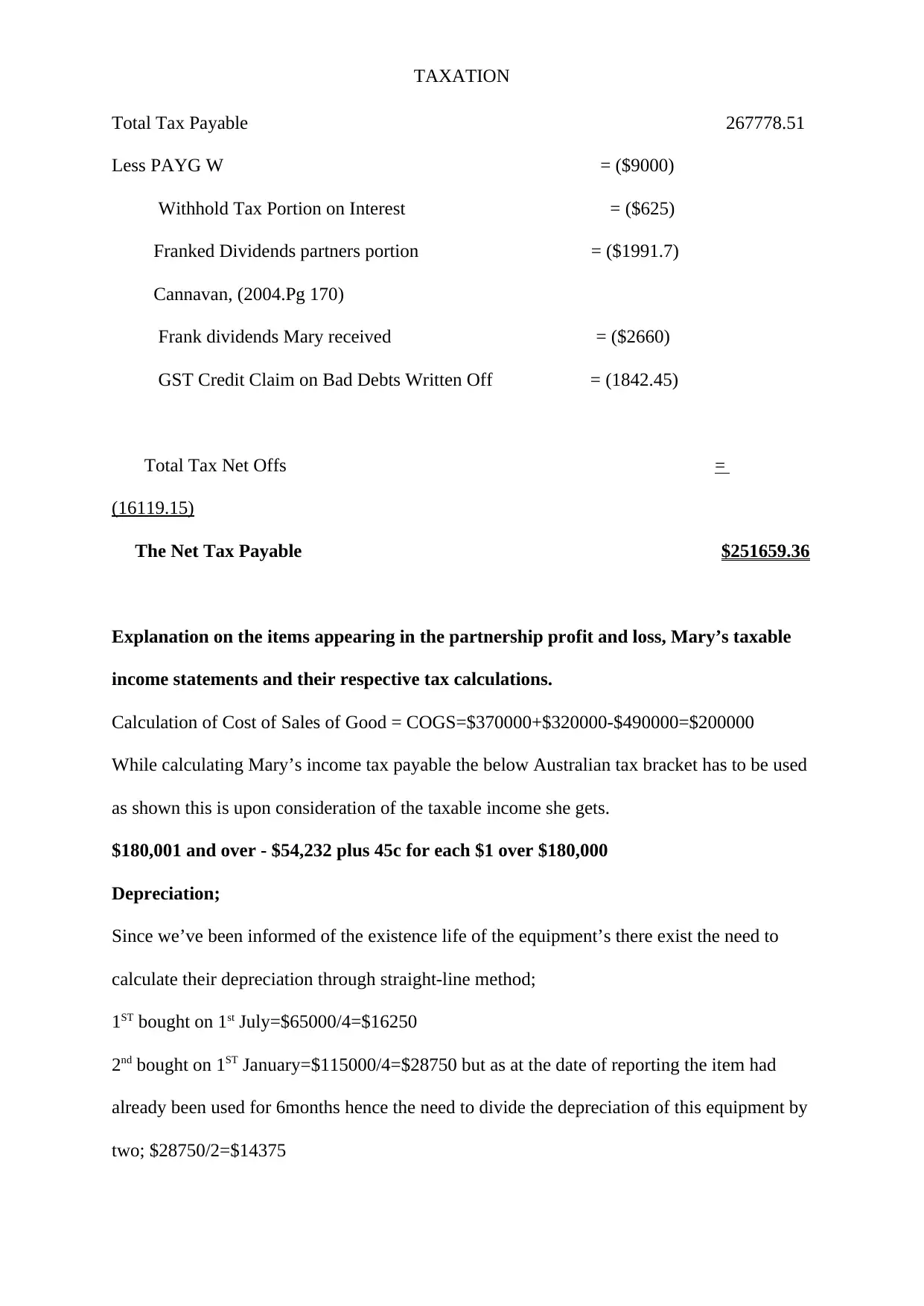

This assignment solution addresses partnership taxation, focusing on the "Two B's" partnership. It begins with the partnership's profit and loss income statement for the year ending June 30, 2017, detailing various income sources like trading receipts, capital gains, dividends, and interest, alongside expenses such as cost of goods sold, salaries, rent, depreciation, and interest. The solution then presents Mary Brown's taxable income statement, outlining her revenue sources (dividends, salary, interest, and rental income) and associated expenses. It meticulously calculates Mary's tax payable, considering Australian tax brackets, depreciation, and the medical levy. Furthermore, the solution includes detailed explanations of items in both statements, such as the calculation of cost of goods sold and depreciation, along with references to relevant tax regulations and case law. The document also covers the GST implications and the sharing of profits and losses between partners, providing a comprehensive analysis of the partnership's and Mary's tax positions. The solution also includes the calculation of Mary's tax payable and net tax payable after considering PAYG withholding, withholding tax, franked dividends, and GST credits.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.