Investment Appraisal: Evaluating Payback Period & IRR in Accounting

VerifiedAdded on 2023/06/12

|6

|907

|309

Homework Assignment

AI Summary

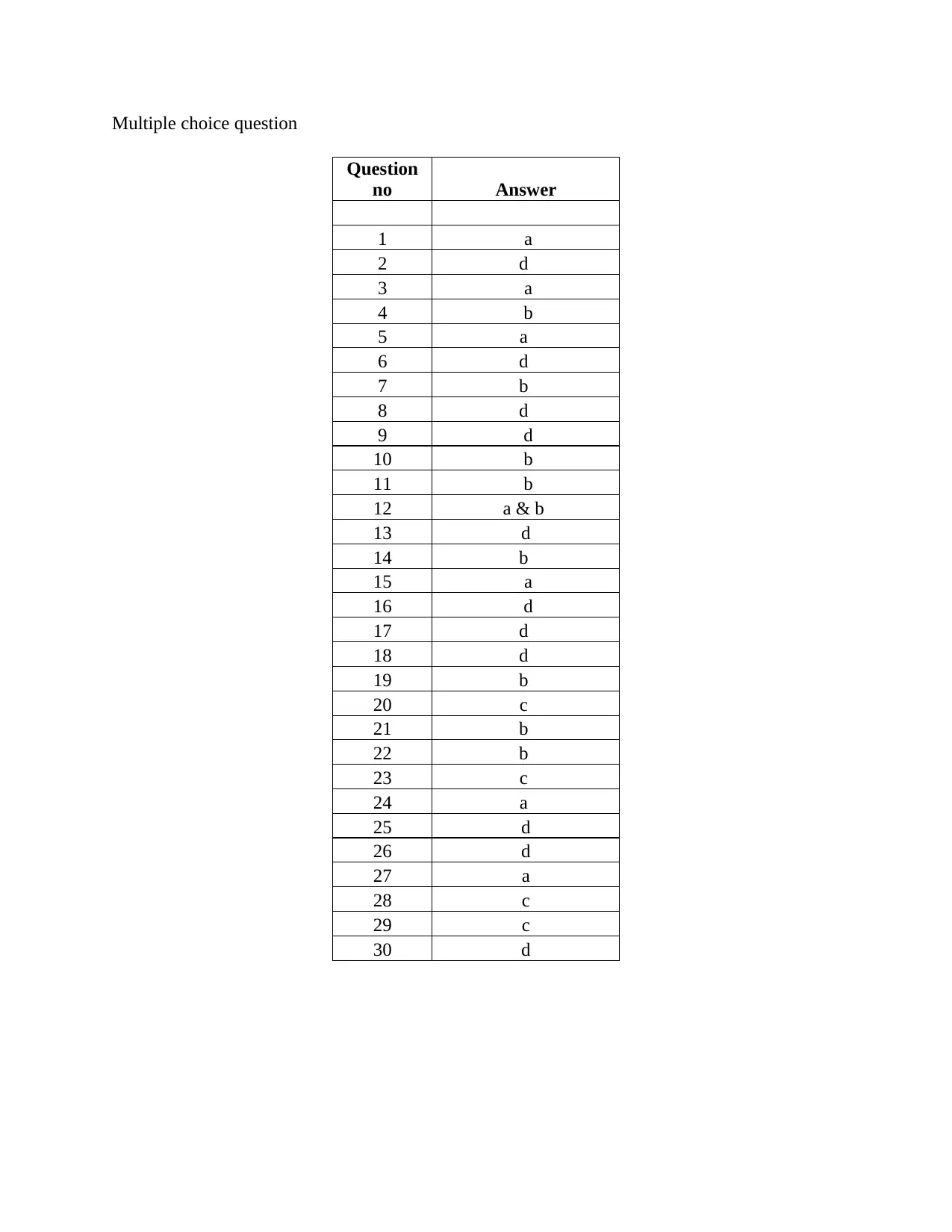

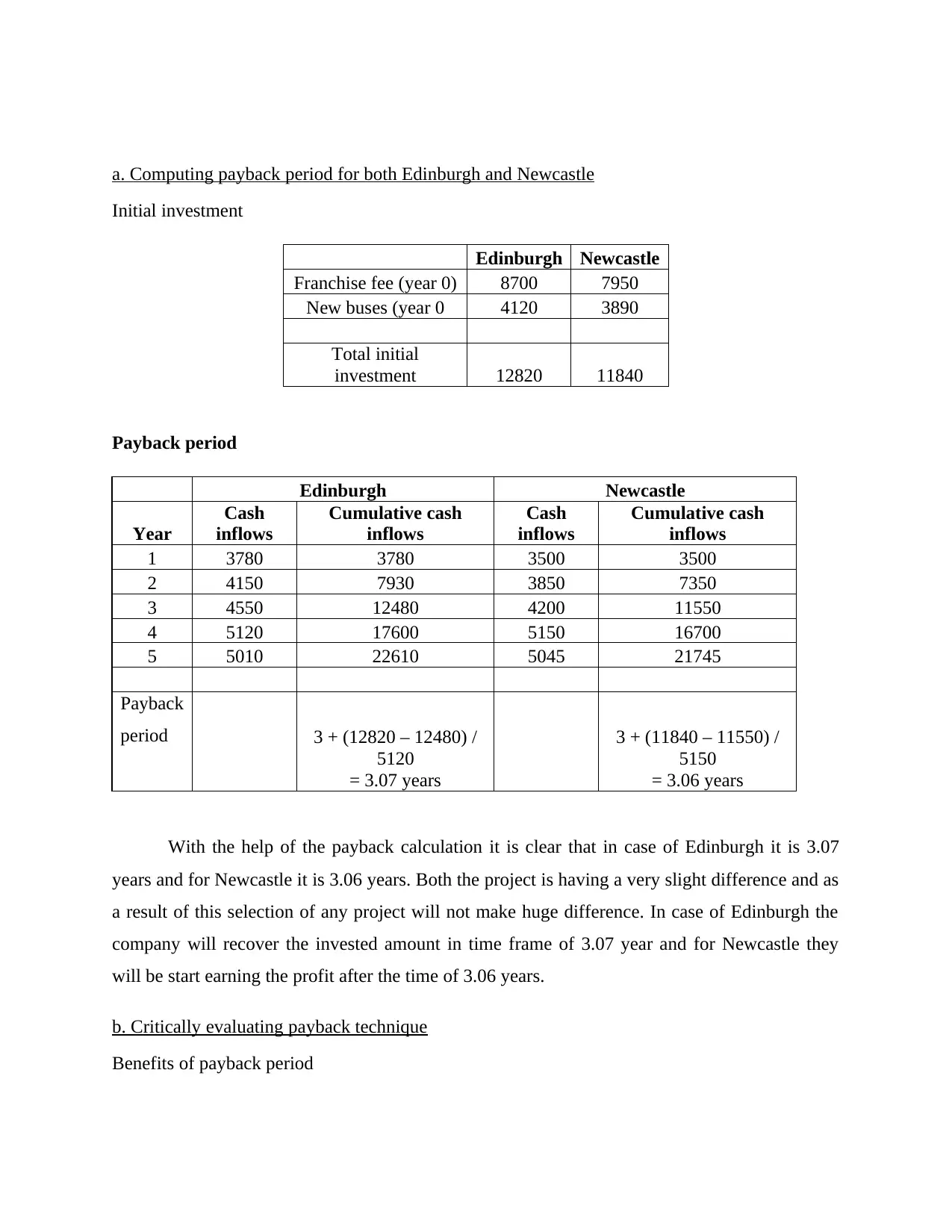

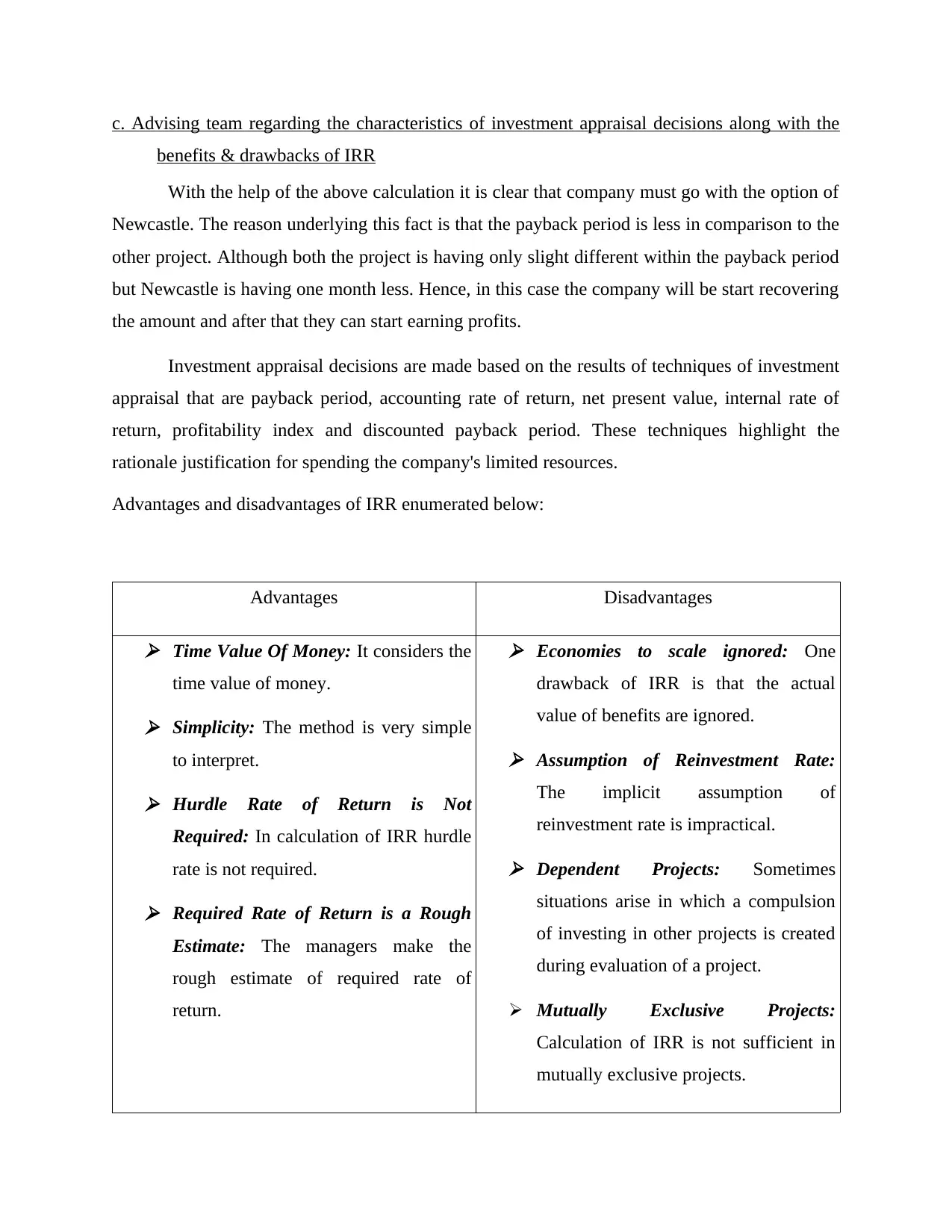

This assignment provides a detailed solution to an accounting exam question focusing on investment appraisal techniques, specifically the payback period method and internal rate of return (IRR). It begins by calculating the payback period for two investment options, Edinburgh and Newcastle, determining that Newcastle has a slightly shorter payback period. The solution then critically evaluates the payback period technique, outlining its benefits such as simplicity and liquidity focus, while also addressing its drawbacks like ignoring the time value of money and profitability. Furthermore, the assignment advises a team on the characteristics of investment appraisal decisions, highlighting the advantages and disadvantages of using IRR, including its consideration of the time value of money but also its potential for unrealistic reinvestment rate assumptions. Ultimately, the assignment recommends choosing the Newcastle project based on its shorter payback period, emphasizing the importance of recovering initial investments quickly. Desklib offers a wealth of similar solved assignments and study resources for students.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.