Payroll Data Preparation and Payment Authorization for Pitstop Pty Ltd

VerifiedAdded on 2020/01/07

|11

|3286

|201

Practical Assignment

AI Summary

This assignment analyzes the preparation of payroll data and authorization of payments for Pitstop Pty Ltd, a retail and fuel service company. It involves calculating pay for each employee based on time sheets and employment status, including ordinary time, overtime, and various allowances. The report details the calculation of gross wages, tax withholdings (PAYG, HELP, and tax offsets), and net pay, considering factors like casual loading, Saturday loading, and superannuation contributions. It also covers the reconciliation of the payroll register, with specific examples for employees like Employee 001, Richard Swift, Paul Singh, and Al Carron, including details on deductions for child support and salary sacrifice. The assignment highlights the importance of accurate record-keeping, adherence to relevant legislation, and organizational procedures in managing payroll effectively. The assignment also includes a discussion on the forwarding of data on worksheets and the use of payroll registers for payment authorization.

Prepare payroll data and authorize payment

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK A : CALCULATING PAY AND PROVIDING PAY DATA.............................................3

Checking and time sheet hours for the fortnight ending 24th June 2012....................................3

Calculating pay for each employee on pay calculation work sheet.............................................3

Schedule forwarding of data on worksheet..................................................................................8

TASK B: RECONCILING PAYROLL REGISTOR AND AUTHORIZE PAYMENT................8

Reconciling the Bendigo pay registor..........................................................................................8

TASK C: HANLDING PAYROLL ENQUIRY..............................................................................9

Preparing payroll data and authorize payment.............................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

2

INTRODUCTION...........................................................................................................................3

TASK A : CALCULATING PAY AND PROVIDING PAY DATA.............................................3

Checking and time sheet hours for the fortnight ending 24th June 2012....................................3

Calculating pay for each employee on pay calculation work sheet.............................................3

Schedule forwarding of data on worksheet..................................................................................8

TASK B: RECONCILING PAYROLL REGISTOR AND AUTHORIZE PAYMENT................8

Reconciling the Bendigo pay registor..........................................................................................8

TASK C: HANLDING PAYROLL ENQUIRY..............................................................................9

Preparing payroll data and authorize payment.............................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

2

INTRODUCTION

The preparation of payroll is the most important aspect for a business through which

appropriate financial data can be maintained for corporation. It consists of information related to

salaries, wages and bonuses as well as withheld taxes. Present report is based upon case scenario

of Pitstop Pty Ltd which is retail and fuel service company. The product and service range of

corporation consists of hot pies, supermarket goods, gas and cold drinks. In this regard, payroll

of workforce working in Pitstop has been calculated in worksheet. In addition to this, pay

register has been completed along with authorization. Apart from this, relevant legislation and

organizational procedures are also referred for preparing the pay roll sheet.

TASK A : CALCULATING PAY AND PROVIDING PAY DATA

Checking and time sheet hours for the fortnight ending 24th June 2012

The information such as time sheet, working hours and emplyement status are checked

for calculating fortnight payroll. It shows that different departments are there in Pitstop and

accordingly respective information has been recorded in excel sheet(Tao, Chuang and Lin,

2016). It has been found thatall fouremployees of Pitstop work in the employment

classification “retail workers level 2” and job title of the same is “store worker”. Furthermore,

two employees work on casual basis whereas remaining work for full time.

Calculating pay for each employee on pay calculation work sheet

The payroll processing procedure has been used for calculating pay for each employee.

Under this, first of all employees' detail is verified so that necessary changes and deduction can

be made from their salary account. It facilitates to prepare the payroll effectively and meeting

expectations of all related parties of Pitstop. However, store manager's approval is also taken for

the overtime thereby employees can effectively work with integration (Rockerbie and Easton,

2014). It aids to enhance their salary as they get opportunity to work for overtime. It is also

helpful for proper coordination and maintaining appropriate environment of business.

Thereafter, working hours of each workforce is verified by observing the time sheet. In

such manner operation manager will come to know that how many leaves are taken by workforce

and what were the total working hours. Furthermore, leave verification is also done by checking

the time sheet. The basic aim behind leave verification is to analyze allotted leave and those

3

The preparation of payroll is the most important aspect for a business through which

appropriate financial data can be maintained for corporation. It consists of information related to

salaries, wages and bonuses as well as withheld taxes. Present report is based upon case scenario

of Pitstop Pty Ltd which is retail and fuel service company. The product and service range of

corporation consists of hot pies, supermarket goods, gas and cold drinks. In this regard, payroll

of workforce working in Pitstop has been calculated in worksheet. In addition to this, pay

register has been completed along with authorization. Apart from this, relevant legislation and

organizational procedures are also referred for preparing the pay roll sheet.

TASK A : CALCULATING PAY AND PROVIDING PAY DATA

Checking and time sheet hours for the fortnight ending 24th June 2012

The information such as time sheet, working hours and emplyement status are checked

for calculating fortnight payroll. It shows that different departments are there in Pitstop and

accordingly respective information has been recorded in excel sheet(Tao, Chuang and Lin,

2016). It has been found thatall fouremployees of Pitstop work in the employment

classification “retail workers level 2” and job title of the same is “store worker”. Furthermore,

two employees work on casual basis whereas remaining work for full time.

Calculating pay for each employee on pay calculation work sheet

The payroll processing procedure has been used for calculating pay for each employee.

Under this, first of all employees' detail is verified so that necessary changes and deduction can

be made from their salary account. It facilitates to prepare the payroll effectively and meeting

expectations of all related parties of Pitstop. However, store manager's approval is also taken for

the overtime thereby employees can effectively work with integration (Rockerbie and Easton,

2014). It aids to enhance their salary as they get opportunity to work for overtime. It is also

helpful for proper coordination and maintaining appropriate environment of business.

Thereafter, working hours of each workforce is verified by observing the time sheet. In

such manner operation manager will come to know that how many leaves are taken by workforce

and what were the total working hours. Furthermore, leave verification is also done by checking

the time sheet. The basic aim behind leave verification is to analyze allotted leave and those

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which are taken by employees. Apart from this, time sheet totals is complied for extracting all

relevant information for tax threshold and other details. Furthermore, due wage is also

calculated in accordance with working hours and basic wage paid for each employee. On the

other hand, tax withholding is calculated on the basis of gross pay for each employee. All these

taxes are subtracted from the gross pay where net income is calculated. This proves to be

effective for gathering information related to superannuation (contribution/salary sacrifices)

(Chung, Steenburgh and Sudhir, 2013). Moreover, payroll register is prepared by finance

manager wherein all detail of selected workforce is filled in the register. By assessing given

payroll register, HR department can assess performance of business as well as pay scale of each

workforce. This is because payroll has direct impact on net income generate by business due to

subtraction of tax. Moreover, individual pay information and pay register is sent to Pitstop head

office for detail inquiries and resolving all related issues of respective personnel.

The following sheet is providing detail information related to pay for each employees. It

shows that casual status of employment is there and accordingly working hours are observed.

Further, it has been found that no any leave has been taken by employee 001 and he is paying tax

worth 210 dollar.

Employee 001

Hourly rate: 18 Salary:

Pay period

Start date: 11 June

2012

End date: 24 June

2012

Forwarded to

head office

Gross wages Hours Rate

Ordinary time 52.5 1 945

Overtime (1.5*hourly rate) 0 1.5 0

Overtime (2*hourly rate) 10 2 360

Holiday pay (A/L) 0 1 0

Casual loading (25%) 0.25 236.25

Saturday loading (10%) 7.5 0.1 13.5

Holiday leave loading (17.5%) 0 0 0

Personal leave paid 0 1 0

Total 1554.75

Allowances

Car

Pre-tax deduction

Superannuation

Salary sacrifice

Taxes

4

relevant information for tax threshold and other details. Furthermore, due wage is also

calculated in accordance with working hours and basic wage paid for each employee. On the

other hand, tax withholding is calculated on the basis of gross pay for each employee. All these

taxes are subtracted from the gross pay where net income is calculated. This proves to be

effective for gathering information related to superannuation (contribution/salary sacrifices)

(Chung, Steenburgh and Sudhir, 2013). Moreover, payroll register is prepared by finance

manager wherein all detail of selected workforce is filled in the register. By assessing given

payroll register, HR department can assess performance of business as well as pay scale of each

workforce. This is because payroll has direct impact on net income generate by business due to

subtraction of tax. Moreover, individual pay information and pay register is sent to Pitstop head

office for detail inquiries and resolving all related issues of respective personnel.

The following sheet is providing detail information related to pay for each employees. It

shows that casual status of employment is there and accordingly working hours are observed.

Further, it has been found that no any leave has been taken by employee 001 and he is paying tax

worth 210 dollar.

Employee 001

Hourly rate: 18 Salary:

Pay period

Start date: 11 June

2012

End date: 24 June

2012

Forwarded to

head office

Gross wages Hours Rate

Ordinary time 52.5 1 945

Overtime (1.5*hourly rate) 0 1.5 0

Overtime (2*hourly rate) 10 2 360

Holiday pay (A/L) 0 1 0

Casual loading (25%) 0.25 236.25

Saturday loading (10%) 7.5 0.1 13.5

Holiday leave loading (17.5%) 0 0 0

Personal leave paid 0 1 0

Total 1554.75

Allowances

Car

Pre-tax deduction

Superannuation

Salary sacrifice

Taxes

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

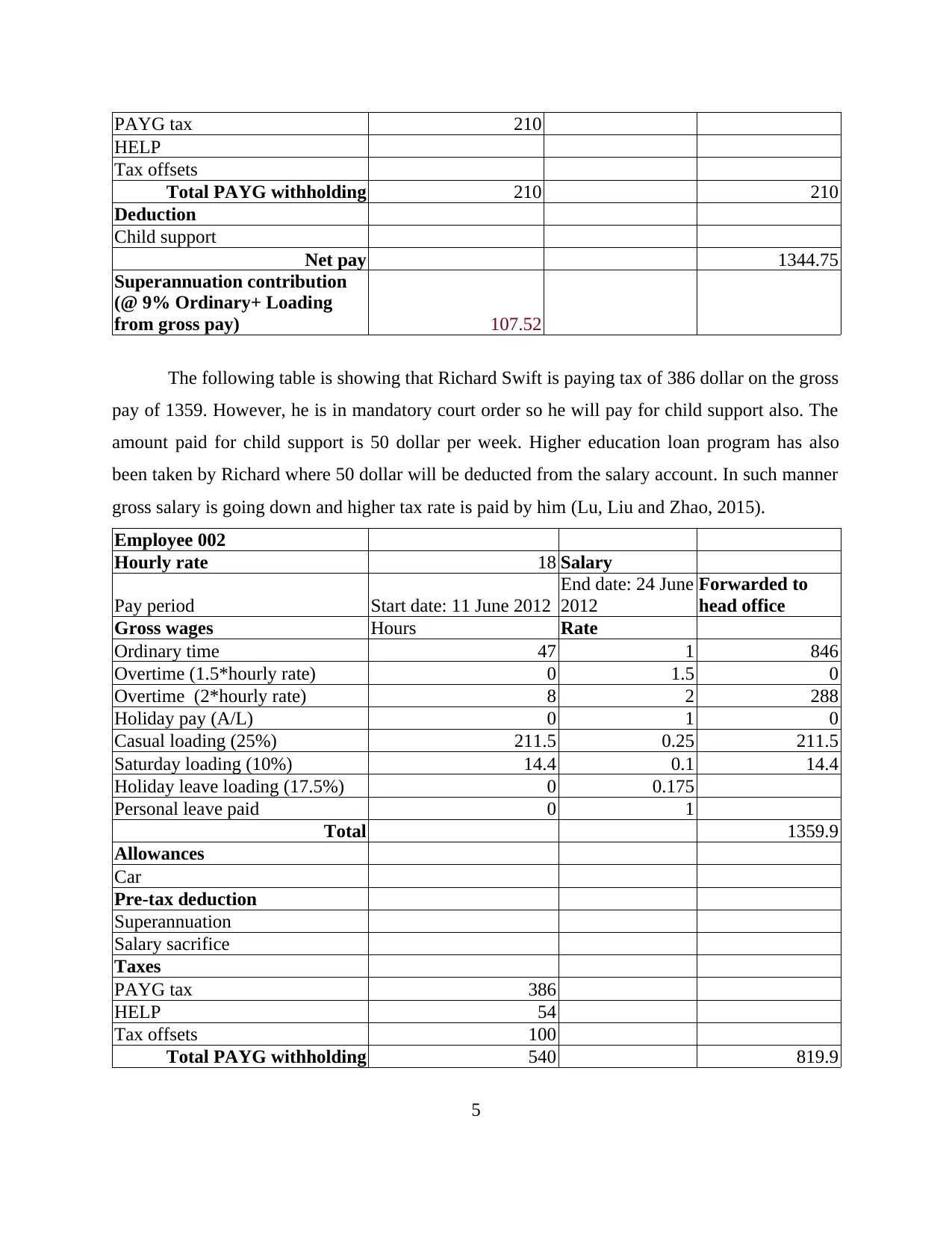

PAYG tax 210

HELP

Tax offsets

Total PAYG withholding 210 210

Deduction

Child support

Net pay 1344.75

Superannuation contribution

(@ 9% Ordinary+ Loading

from gross pay) 107.52

The following table is showing that Richard Swift is paying tax of 386 dollar on the gross

pay of 1359. However, he is in mandatory court order so he will pay for child support also. The

amount paid for child support is 50 dollar per week. Higher education loan program has also

been taken by Richard where 50 dollar will be deducted from the salary account. In such manner

gross salary is going down and higher tax rate is paid by him (Lu, Liu and Zhao, 2015).

Employee 002

Hourly rate 18 Salary

Pay period Start date: 11 June 2012

End date: 24 June

2012

Forwarded to

head office

Gross wages Hours Rate

Ordinary time 47 1 846

Overtime (1.5*hourly rate) 0 1.5 0

Overtime (2*hourly rate) 8 2 288

Holiday pay (A/L) 0 1 0

Casual loading (25%) 211.5 0.25 211.5

Saturday loading (10%) 14.4 0.1 14.4

Holiday leave loading (17.5%) 0 0.175

Personal leave paid 0 1

Total 1359.9

Allowances

Car

Pre-tax deduction

Superannuation

Salary sacrifice

Taxes

PAYG tax 386

HELP 54

Tax offsets 100

Total PAYG withholding 540 819.9

5

HELP

Tax offsets

Total PAYG withholding 210 210

Deduction

Child support

Net pay 1344.75

Superannuation contribution

(@ 9% Ordinary+ Loading

from gross pay) 107.52

The following table is showing that Richard Swift is paying tax of 386 dollar on the gross

pay of 1359. However, he is in mandatory court order so he will pay for child support also. The

amount paid for child support is 50 dollar per week. Higher education loan program has also

been taken by Richard where 50 dollar will be deducted from the salary account. In such manner

gross salary is going down and higher tax rate is paid by him (Lu, Liu and Zhao, 2015).

Employee 002

Hourly rate 18 Salary

Pay period Start date: 11 June 2012

End date: 24 June

2012

Forwarded to

head office

Gross wages Hours Rate

Ordinary time 47 1 846

Overtime (1.5*hourly rate) 0 1.5 0

Overtime (2*hourly rate) 8 2 288

Holiday pay (A/L) 0 1 0

Casual loading (25%) 211.5 0.25 211.5

Saturday loading (10%) 14.4 0.1 14.4

Holiday leave loading (17.5%) 0 0.175

Personal leave paid 0 1

Total 1359.9

Allowances

Car

Pre-tax deduction

Superannuation

Salary sacrifice

Taxes

PAYG tax 386

HELP 54

Tax offsets 100

Total PAYG withholding 540 819.9

5

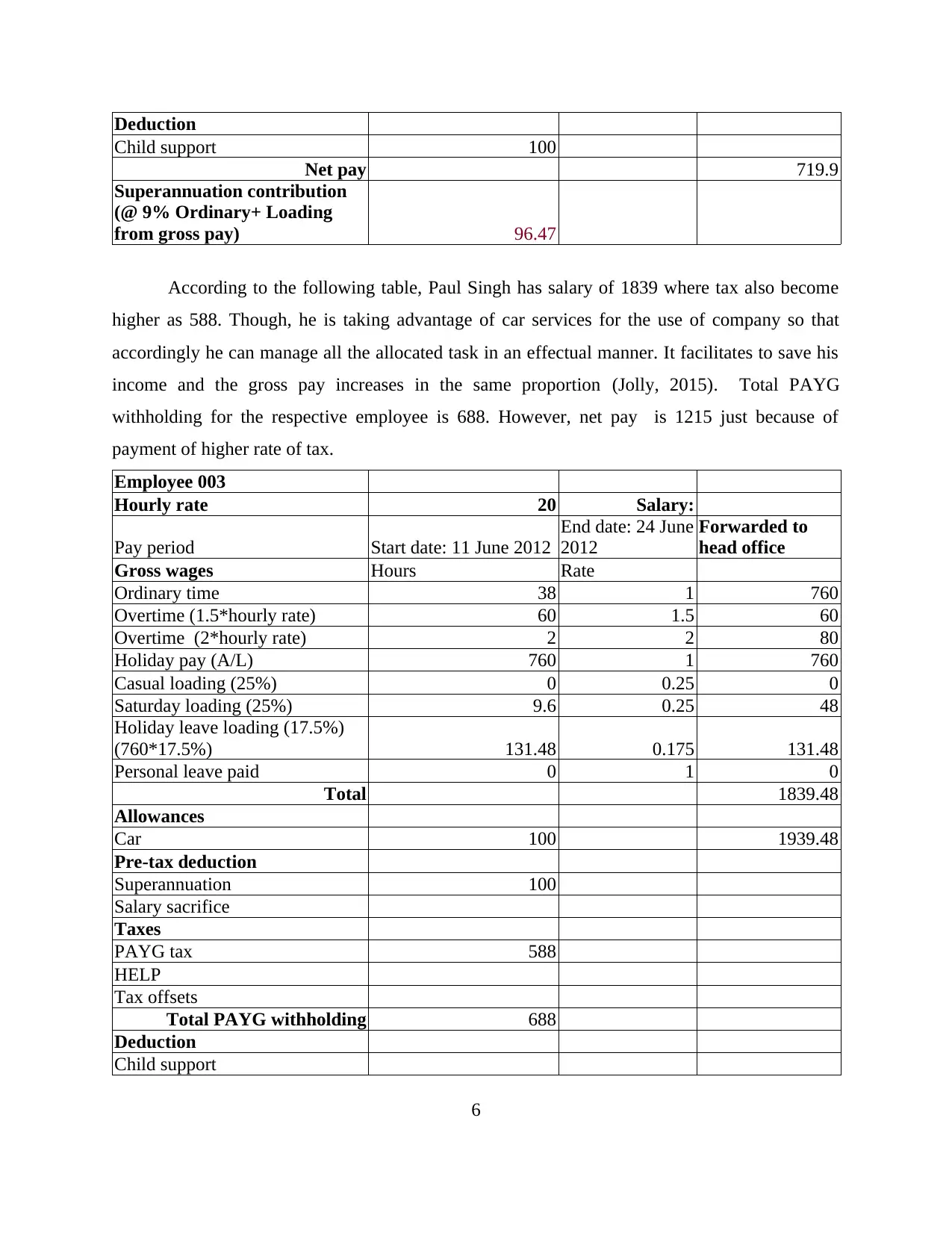

Deduction

Child support 100

Net pay 719.9

Superannuation contribution

(@ 9% Ordinary+ Loading

from gross pay) 96.47

According to the following table, Paul Singh has salary of 1839 where tax also become

higher as 588. Though, he is taking advantage of car services for the use of company so that

accordingly he can manage all the allocated task in an effectual manner. It facilitates to save his

income and the gross pay increases in the same proportion (Jolly, 2015). Total PAYG

withholding for the respective employee is 688. However, net pay is 1215 just because of

payment of higher rate of tax.

Employee 003

Hourly rate 20 Salary:

Pay period Start date: 11 June 2012

End date: 24 June

2012

Forwarded to

head office

Gross wages Hours Rate

Ordinary time 38 1 760

Overtime (1.5*hourly rate) 60 1.5 60

Overtime (2*hourly rate) 2 2 80

Holiday pay (A/L) 760 1 760

Casual loading (25%) 0 0.25 0

Saturday loading (25%) 9.6 0.25 48

Holiday leave loading (17.5%)

(760*17.5%) 131.48 0.175 131.48

Personal leave paid 0 1 0

Total 1839.48

Allowances

Car 100 1939.48

Pre-tax deduction

Superannuation 100

Salary sacrifice

Taxes

PAYG tax 588

HELP

Tax offsets

Total PAYG withholding 688

Deduction

Child support

6

Child support 100

Net pay 719.9

Superannuation contribution

(@ 9% Ordinary+ Loading

from gross pay) 96.47

According to the following table, Paul Singh has salary of 1839 where tax also become

higher as 588. Though, he is taking advantage of car services for the use of company so that

accordingly he can manage all the allocated task in an effectual manner. It facilitates to save his

income and the gross pay increases in the same proportion (Jolly, 2015). Total PAYG

withholding for the respective employee is 688. However, net pay is 1215 just because of

payment of higher rate of tax.

Employee 003

Hourly rate 20 Salary:

Pay period Start date: 11 June 2012

End date: 24 June

2012

Forwarded to

head office

Gross wages Hours Rate

Ordinary time 38 1 760

Overtime (1.5*hourly rate) 60 1.5 60

Overtime (2*hourly rate) 2 2 80

Holiday pay (A/L) 760 1 760

Casual loading (25%) 0 0.25 0

Saturday loading (25%) 9.6 0.25 48

Holiday leave loading (17.5%)

(760*17.5%) 131.48 0.175 131.48

Personal leave paid 0 1 0

Total 1839.48

Allowances

Car 100 1939.48

Pre-tax deduction

Superannuation 100

Salary sacrifice

Taxes

PAYG tax 588

HELP

Tax offsets

Total PAYG withholding 688

Deduction

Child support

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

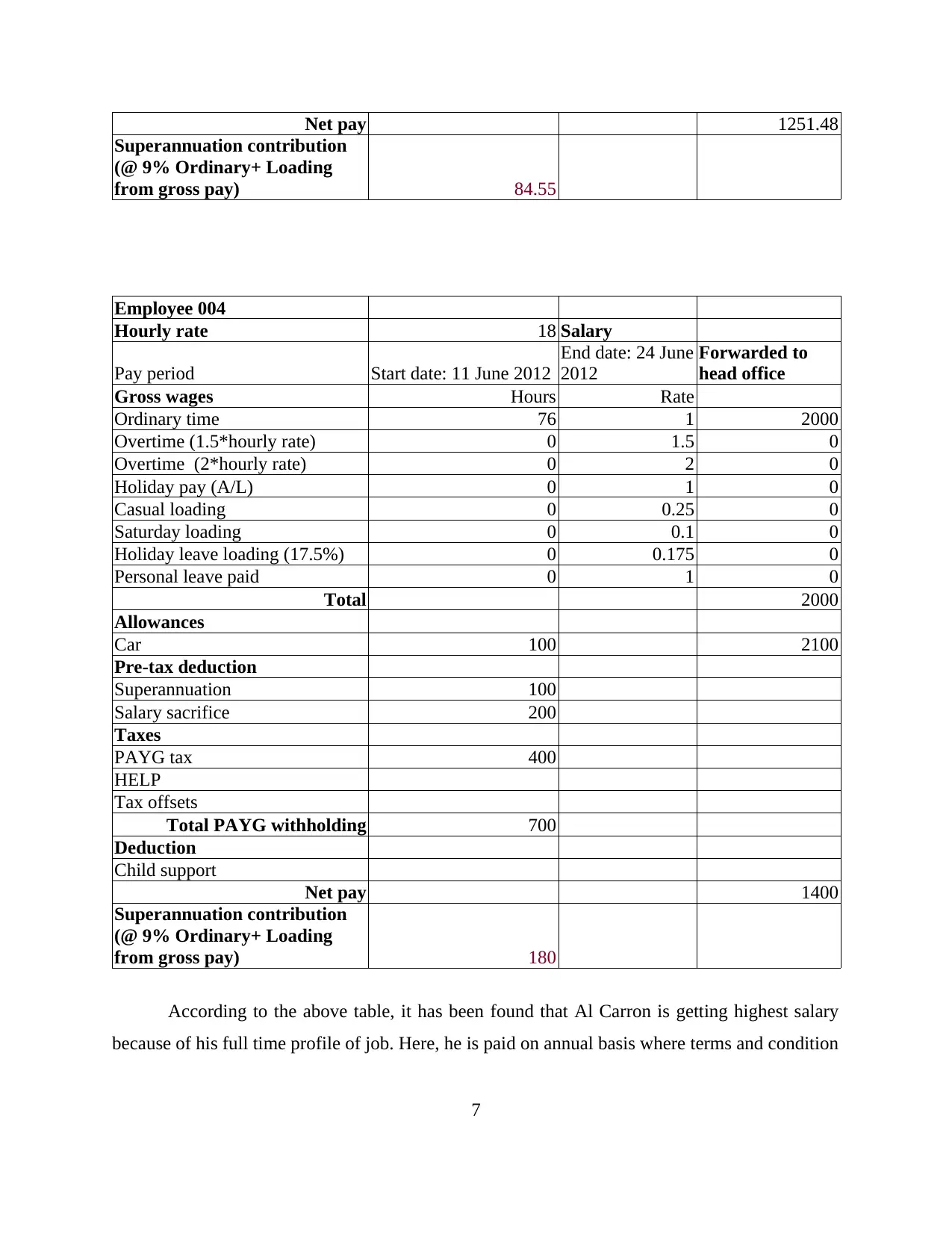

Net pay 1251.48

Superannuation contribution

(@ 9% Ordinary+ Loading

from gross pay) 84.55

Employee 004

Hourly rate 18 Salary

Pay period Start date: 11 June 2012

End date: 24 June

2012

Forwarded to

head office

Gross wages Hours Rate

Ordinary time 76 1 2000

Overtime (1.5*hourly rate) 0 1.5 0

Overtime (2*hourly rate) 0 2 0

Holiday pay (A/L) 0 1 0

Casual loading 0 0.25 0

Saturday loading 0 0.1 0

Holiday leave loading (17.5%) 0 0.175 0

Personal leave paid 0 1 0

Total 2000

Allowances

Car 100 2100

Pre-tax deduction

Superannuation 100

Salary sacrifice 200

Taxes

PAYG tax 400

HELP

Tax offsets

Total PAYG withholding 700

Deduction

Child support

Net pay 1400

Superannuation contribution

(@ 9% Ordinary+ Loading

from gross pay) 180

According to the above table, it has been found that Al Carron is getting highest salary

because of his full time profile of job. Here, he is paid on annual basis where terms and condition

7

Superannuation contribution

(@ 9% Ordinary+ Loading

from gross pay) 84.55

Employee 004

Hourly rate 18 Salary

Pay period Start date: 11 June 2012

End date: 24 June

2012

Forwarded to

head office

Gross wages Hours Rate

Ordinary time 76 1 2000

Overtime (1.5*hourly rate) 0 1.5 0

Overtime (2*hourly rate) 0 2 0

Holiday pay (A/L) 0 1 0

Casual loading 0 0.25 0

Saturday loading 0 0.1 0

Holiday leave loading (17.5%) 0 0.175 0

Personal leave paid 0 1 0

Total 2000

Allowances

Car 100 2100

Pre-tax deduction

Superannuation 100

Salary sacrifice 200

Taxes

PAYG tax 400

HELP

Tax offsets

Total PAYG withholding 700

Deduction

Child support

Net pay 1400

Superannuation contribution

(@ 9% Ordinary+ Loading

from gross pay) 180

According to the above table, it has been found that Al Carron is getting highest salary

because of his full time profile of job. Here, he is paid on annual basis where terms and condition

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

also varies. This employee pays for car uses and other related expenses but also claim for

threshold.

Schedule forwarding of data on worksheet

The data sheet of overall record has been attached in mail. It consists of detail

information related to calculation of pay for fortnight. It proves to be effective to maintain

effective record and meeting expectations of individual in an effectual manner.

TASK B: RECONCILING PAYROLL REGISTOR AND AUTHORIZE

PAYMENT

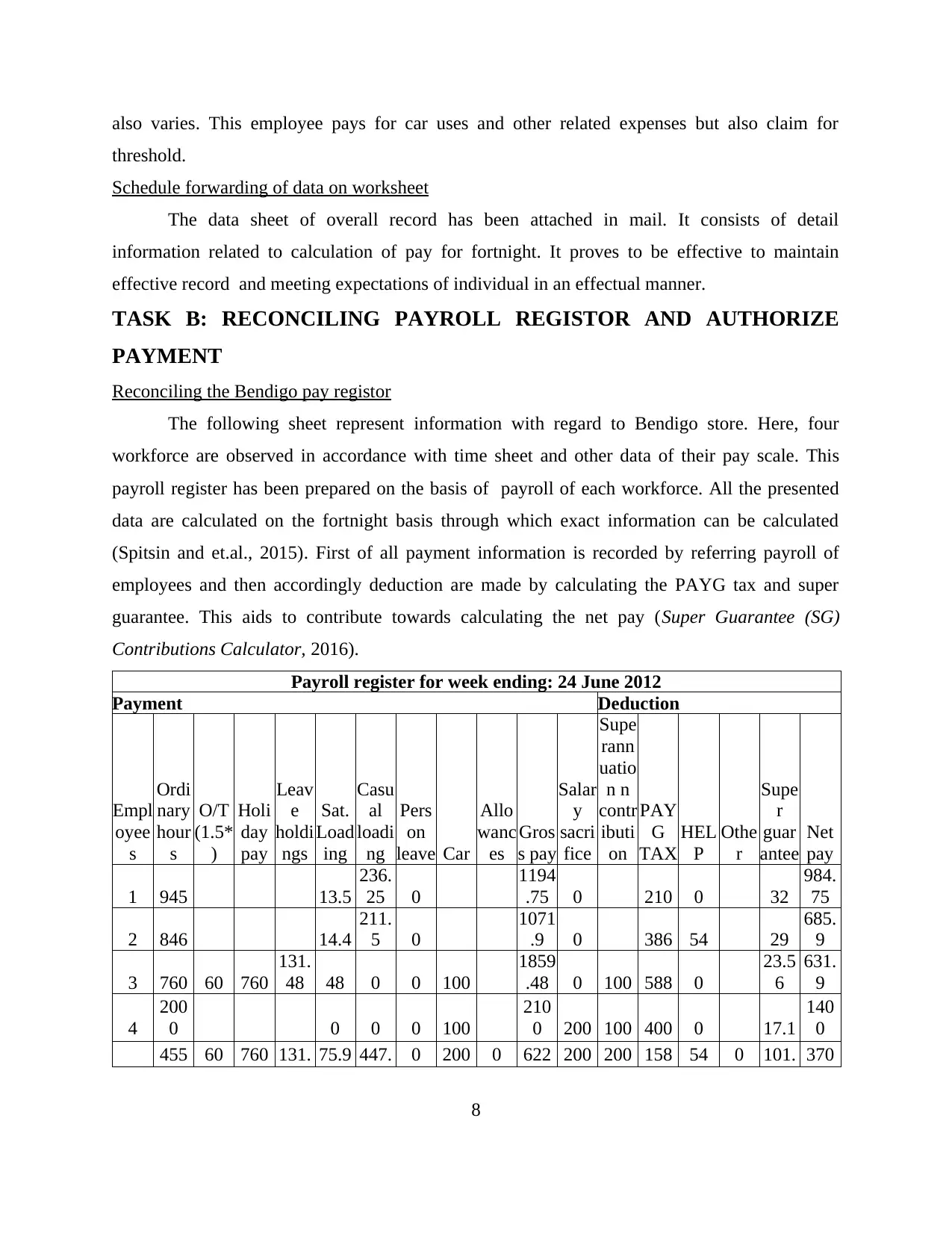

Reconciling the Bendigo pay registor

The following sheet represent information with regard to Bendigo store. Here, four

workforce are observed in accordance with time sheet and other data of their pay scale. This

payroll register has been prepared on the basis of payroll of each workforce. All the presented

data are calculated on the fortnight basis through which exact information can be calculated

(Spitsin and et.al., 2015). First of all payment information is recorded by referring payroll of

employees and then accordingly deduction are made by calculating the PAYG tax and super

guarantee. This aids to contribute towards calculating the net pay (Super Guarantee (SG)

Contributions Calculator, 2016).

Payroll register for week ending: 24 June 2012

Payment Deduction

Empl

oyee

s

Ordi

nary

hour

s

O/T

(1.5*

)

Holi

day

pay

Leav

e

holdi

ngs

Sat.

Load

ing

Casu

al

loadi

ng

Pers

on

leave Car

Allo

wanc

es

Gros

s pay

Salar

y

sacri

fice

Supe

rann

uatio

n n

contr

ibuti

on

PAY

G

TAX

HEL

P

Othe

r

Supe

r

guar

antee

Net

pay

1 945 13.5

236.

25 0

1194

.75 0 210 0 32

984.

75

2 846 14.4

211.

5 0

1071

.9 0 386 54 29

685.

9

3 760 60 760

131.

48 48 0 0 100

1859

.48 0 100 588 0

23.5

6

631.

9

4

200

0 0 0 0 100

210

0 200 100 400 0 17.1

140

0

455 60 760 131. 75.9 447. 0 200 0 622 200 200 158 54 0 101. 370

8

threshold.

Schedule forwarding of data on worksheet

The data sheet of overall record has been attached in mail. It consists of detail

information related to calculation of pay for fortnight. It proves to be effective to maintain

effective record and meeting expectations of individual in an effectual manner.

TASK B: RECONCILING PAYROLL REGISTOR AND AUTHORIZE

PAYMENT

Reconciling the Bendigo pay registor

The following sheet represent information with regard to Bendigo store. Here, four

workforce are observed in accordance with time sheet and other data of their pay scale. This

payroll register has been prepared on the basis of payroll of each workforce. All the presented

data are calculated on the fortnight basis through which exact information can be calculated

(Spitsin and et.al., 2015). First of all payment information is recorded by referring payroll of

employees and then accordingly deduction are made by calculating the PAYG tax and super

guarantee. This aids to contribute towards calculating the net pay (Super Guarantee (SG)

Contributions Calculator, 2016).

Payroll register for week ending: 24 June 2012

Payment Deduction

Empl

oyee

s

Ordi

nary

hour

s

O/T

(1.5*

)

Holi

day

pay

Leav

e

holdi

ngs

Sat.

Load

ing

Casu

al

loadi

ng

Pers

on

leave Car

Allo

wanc

es

Gros

s pay

Salar

y

sacri

fice

Supe

rann

uatio

n n

contr

ibuti

on

PAY

G

TAX

HEL

P

Othe

r

Supe

r

guar

antee

Net

pay

1 945 13.5

236.

25 0

1194

.75 0 210 0 32

984.

75

2 846 14.4

211.

5 0

1071

.9 0 386 54 29

685.

9

3 760 60 760

131.

48 48 0 0 100

1859

.48 0 100 588 0

23.5

6

631.

9

4

200

0 0 0 0 100

210

0 200 100 400 0 17.1

140

0

455 60 760 131. 75.9 447. 0 200 0 622 200 200 158 54 0 101. 370

8

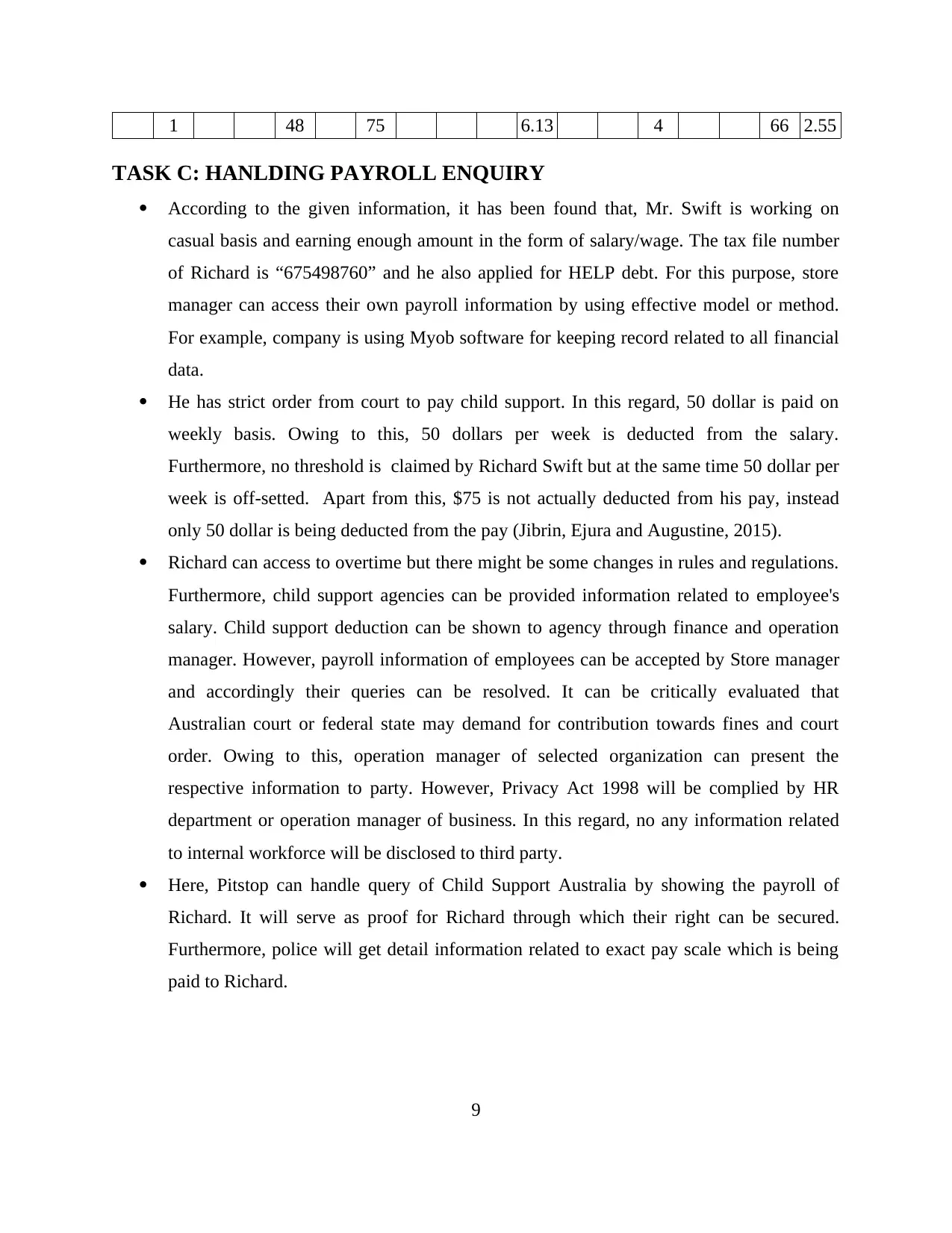

1 48 75 6.13 4 66 2.55

TASK C: HANLDING PAYROLL ENQUIRY

According to the given information, it has been found that, Mr. Swift is working on

casual basis and earning enough amount in the form of salary/wage. The tax file number

of Richard is “675498760” and he also applied for HELP debt. For this purpose, store

manager can access their own payroll information by using effective model or method.

For example, company is using Myob software for keeping record related to all financial

data.

He has strict order from court to pay child support. In this regard, 50 dollar is paid on

weekly basis. Owing to this, 50 dollars per week is deducted from the salary.

Furthermore, no threshold is claimed by Richard Swift but at the same time 50 dollar per

week is off-setted. Apart from this, $75 is not actually deducted from his pay, instead

only 50 dollar is being deducted from the pay (Jibrin, Ejura and Augustine, 2015).

Richard can access to overtime but there might be some changes in rules and regulations.

Furthermore, child support agencies can be provided information related to employee's

salary. Child support deduction can be shown to agency through finance and operation

manager. However, payroll information of employees can be accepted by Store manager

and accordingly their queries can be resolved. It can be critically evaluated that

Australian court or federal state may demand for contribution towards fines and court

order. Owing to this, operation manager of selected organization can present the

respective information to party. However, Privacy Act 1998 will be complied by HR

department or operation manager of business. In this regard, no any information related

to internal workforce will be disclosed to third party.

Here, Pitstop can handle query of Child Support Australia by showing the payroll of

Richard. It will serve as proof for Richard through which their right can be secured.

Furthermore, police will get detail information related to exact pay scale which is being

paid to Richard.

9

TASK C: HANLDING PAYROLL ENQUIRY

According to the given information, it has been found that, Mr. Swift is working on

casual basis and earning enough amount in the form of salary/wage. The tax file number

of Richard is “675498760” and he also applied for HELP debt. For this purpose, store

manager can access their own payroll information by using effective model or method.

For example, company is using Myob software for keeping record related to all financial

data.

He has strict order from court to pay child support. In this regard, 50 dollar is paid on

weekly basis. Owing to this, 50 dollars per week is deducted from the salary.

Furthermore, no threshold is claimed by Richard Swift but at the same time 50 dollar per

week is off-setted. Apart from this, $75 is not actually deducted from his pay, instead

only 50 dollar is being deducted from the pay (Jibrin, Ejura and Augustine, 2015).

Richard can access to overtime but there might be some changes in rules and regulations.

Furthermore, child support agencies can be provided information related to employee's

salary. Child support deduction can be shown to agency through finance and operation

manager. However, payroll information of employees can be accepted by Store manager

and accordingly their queries can be resolved. It can be critically evaluated that

Australian court or federal state may demand for contribution towards fines and court

order. Owing to this, operation manager of selected organization can present the

respective information to party. However, Privacy Act 1998 will be complied by HR

department or operation manager of business. In this regard, no any information related

to internal workforce will be disclosed to third party.

Here, Pitstop can handle query of Child Support Australia by showing the payroll of

Richard. It will serve as proof for Richard through which their right can be secured.

Furthermore, police will get detail information related to exact pay scale which is being

paid to Richard.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Meeting with Mr Swift

Hello, Mr. Swift, I hope you are in good health and spirit. I am here to clear your doubts

on taxation and your payroll structure. Your tax file number is “675498760” that is registered as

per Australian taxation standards. Talking about your child support, it’s around $ 50 per week

that amount to $ 100 for fortnight. As per Australian standards, deduction of child supports is

always made at last that is after tax withheld deductions and salary sacrifice for voluntary

investments. Finally, your overtime is not at all related to your divorce status. Finally, we are

ready to have complete transparency in your deductions for child support to police or concerned

department. You can always visit for any kind of query

CONCLUSION

The aforementioned report concludes that payroll preparation can be done effectively by

using appropriate structure, However, regulatory framework must be kept into account through

which ethical consideration of business can be ensured. It can also be said that, payroll register

can be prepared at last for detail information of each employee working the organization.

10

Hello, Mr. Swift, I hope you are in good health and spirit. I am here to clear your doubts

on taxation and your payroll structure. Your tax file number is “675498760” that is registered as

per Australian taxation standards. Talking about your child support, it’s around $ 50 per week

that amount to $ 100 for fortnight. As per Australian standards, deduction of child supports is

always made at last that is after tax withheld deductions and salary sacrifice for voluntary

investments. Finally, your overtime is not at all related to your divorce status. Finally, we are

ready to have complete transparency in your deductions for child support to police or concerned

department. You can always visit for any kind of query

CONCLUSION

The aforementioned report concludes that payroll preparation can be done effectively by

using appropriate structure, However, regulatory framework must be kept into account through

which ethical consideration of business can be ensured. It can also be said that, payroll register

can be prepared at last for detail information of each employee working the organization.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Journals and books

Chung, D.J., Steenburgh, T. and Sudhir, K., 2013. Do bonuses enhance sales productivity? A

dynamic structural analysis of bonus-based compensation plans. Marketing Science. 33(2).

pp.165-187.

Jibrin, M.S., Ejura, S.B. and Augustine, N.I., 2015. System of Payroll in the Public Sector

Administration. Asian Development Policy Review. 3(1).pp.9-19.

Spitsin, V. and et.al., 2015. Comparative analysis of salary, labor intensity and payroll-

output ratio of Foreign and domestic firms: Case Russian vehicle industry. Ratio. 1500.

p.100.

Jolly, N.A., 2015. Revenue sharing and within-team payroll inequality in Major League

Baseball. Applied Economics Letters. 22(1). pp.80-85.

Lu, B., Liu, C. and Zhao, T., 2015. A three-tier salary management system for higher

vocational colleges. Int. J. Multimed. Ubiq. Eng. 10(4). pp.91-104.

Rockerbie, D.W. and Easton, S.T., 2014. Unsustainable Runs with Revenue Sharing and Salary

Caps. In The Run to the Pennant (pp. 43-51). Springer New York.

Tao, Y.L., Chuang, H.L. and Lin, E.S., 2016. Compensation and performance in Major League

Baseball: Evidence from salary dispersion and team performance. International Review of

Economics & Finance. 43. pp.151-159.

Online

Super Guarantee (SG) Contributions Calculator. 2016. [Online]. Available

through:<http://calculators.ato.gov.au/scripts/net/SGCalculatorWeb/

GetSGContribution.aspx?ms=Businesses>. [Accessed on 30th August 2016].

11

Journals and books

Chung, D.J., Steenburgh, T. and Sudhir, K., 2013. Do bonuses enhance sales productivity? A

dynamic structural analysis of bonus-based compensation plans. Marketing Science. 33(2).

pp.165-187.

Jibrin, M.S., Ejura, S.B. and Augustine, N.I., 2015. System of Payroll in the Public Sector

Administration. Asian Development Policy Review. 3(1).pp.9-19.

Spitsin, V. and et.al., 2015. Comparative analysis of salary, labor intensity and payroll-

output ratio of Foreign and domestic firms: Case Russian vehicle industry. Ratio. 1500.

p.100.

Jolly, N.A., 2015. Revenue sharing and within-team payroll inequality in Major League

Baseball. Applied Economics Letters. 22(1). pp.80-85.

Lu, B., Liu, C. and Zhao, T., 2015. A three-tier salary management system for higher

vocational colleges. Int. J. Multimed. Ubiq. Eng. 10(4). pp.91-104.

Rockerbie, D.W. and Easton, S.T., 2014. Unsustainable Runs with Revenue Sharing and Salary

Caps. In The Run to the Pennant (pp. 43-51). Springer New York.

Tao, Y.L., Chuang, H.L. and Lin, E.S., 2016. Compensation and performance in Major League

Baseball: Evidence from salary dispersion and team performance. International Review of

Economics & Finance. 43. pp.151-159.

Online

Super Guarantee (SG) Contributions Calculator. 2016. [Online]. Available

through:<http://calculators.ato.gov.au/scripts/net/SGCalculatorWeb/

GetSGContribution.aspx?ms=Businesses>. [Accessed on 30th August 2016].

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.