Financial Analysis Report: Financial Feasibility of Pearl Business

VerifiedAdded on 2022/12/05

|27

|5505

|153

Report

AI Summary

This report provides a comprehensive financial analysis of a proposed pearl import business venture. It examines the feasibility of importing pearls from Tahiti and selling them in Zurich, Switzerland, focusing on the financial aspects of the business plan. The analysis includes a detailed breakdown of estimates and assumptions, break-even analysis, profit and loss statements, balance sheets, cash flow projections, and discounted cash flow analysis. Sensitivity analysis is also conducted to assess the impact of various factors on the business's financial performance. The report concludes with recommendations regarding the investment's viability, considering factors such as break-even sales, net profit, cash flow, and net present value. The study also reflects on the financial tools and techniques employed in the assessment, providing valuable insights into the financial management of a new business venture.

0

Running head: FINANCIAL MANAGEMENT

Financial management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Running head: FINANCIAL MANAGEMENT

Financial management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL MANAGEMENT

Executive summary:

The report has been prepared to evaluate the feasibility of the new business venture proposed in

the given case study. The case study presents the business proposal of importing pearl from

Tahiti and selling in Zurich, Switzerland. Felix as an entrepreneur of the proposed business is

concerned about the financial viability of the project and intends to determine its feasibility by

the development of financial plan. The paper presents the application of various financial tools

such as break even analysis, sensitivity analysis and discounted cash flow of capital budgeting

technique in evaluating the worthiness of project with an initial investment of CHF 250000 by

Felix. After conducting a detailed analysis of the facts and all the figures presented in the case

study, it has been inferred that undertaking the investment would be worthy as identified by

different figures such as break even sales, net profit, cash flow and net present value.

FINANCIAL MANAGEMENT

Executive summary:

The report has been prepared to evaluate the feasibility of the new business venture proposed in

the given case study. The case study presents the business proposal of importing pearl from

Tahiti and selling in Zurich, Switzerland. Felix as an entrepreneur of the proposed business is

concerned about the financial viability of the project and intends to determine its feasibility by

the development of financial plan. The paper presents the application of various financial tools

such as break even analysis, sensitivity analysis and discounted cash flow of capital budgeting

technique in evaluating the worthiness of project with an initial investment of CHF 250000 by

Felix. After conducting a detailed analysis of the facts and all the figures presented in the case

study, it has been inferred that undertaking the investment would be worthy as identified by

different figures such as break even sales, net profit, cash flow and net present value.

2

FINANCIAL MANAGEMENT

Table of Contents

Introduction:....................................................................................................................................3

Discussion:.......................................................................................................................................3

Summary of all the estimates and assumptions:..............................................................................3

Evaluating the Break-even analysis:................................................................................................8

Analysis of the profit and loss statement for the first year of operation:........................................9

Analysis of balance sheet for the first year of operation:..............................................................11

Analysis of monthly and annual cash flow for the first year of operation:...................................12

Analysis of the discounted cash flow for the proposed business:.................................................15

Sensitivity analysis:.......................................................................................................................16

Conclusion and recommendation:.................................................................................................20

Critical reflection:..........................................................................................................................21

FINANCIAL MANAGEMENT

Table of Contents

Introduction:....................................................................................................................................3

Discussion:.......................................................................................................................................3

Summary of all the estimates and assumptions:..............................................................................3

Evaluating the Break-even analysis:................................................................................................8

Analysis of the profit and loss statement for the first year of operation:........................................9

Analysis of balance sheet for the first year of operation:..............................................................11

Analysis of monthly and annual cash flow for the first year of operation:...................................12

Analysis of the discounted cash flow for the proposed business:.................................................15

Sensitivity analysis:.......................................................................................................................16

Conclusion and recommendation:.................................................................................................20

Critical reflection:..........................................................................................................................21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL MANAGEMENT

Introduction:

The report is prepared to demonstrate the financial analysis and evaluate the feasibility of

the new business venture that is to be undertaken by Felix after his retirement. The new business

venture is about opening a retail business of natural pearls, which will be imported from Tahiti

and would be sold in Zurich. The viability of the business venture is evaluated by the

development of the financial plan, which involves the use of techniques of capital budgeting and

forecasting of the annual and monthly cash generated from the sales of pearl. Development of the

financial plan incorporates evaluation of the profit and loss statement, balance sheet, annual cash

flow, sensitivity analysis and monthly and annual cash flow of the proposed retail business (Barr

and McClellan 2018). It is essential for the entrepreneur to evaluate the sustainability of the

business in the current market scenario by conducting the feasibility analysis. The overall

accumulation of the assets has been done by preparation and evaluation of the balance sheet. In

addition to this, the estimated overall expenditure of the business is evaluated by analyzing the

monthly cash flow generated by the business. Application of discounted cash flow model has

been done to evaluate the time value of projected profits of the profits proposed by new venture.

Discussion:

Summary of all the estimates and assumptions:

In this section, all the estimates and assumptions that are considered necessary for the

analysis is presented.

The exclusive rights for selling the products in Switzerland has been granted for a period

of five years in exchange for the upfront fee of such rights. It has been assumed for

FINANCIAL MANAGEMENT

Introduction:

The report is prepared to demonstrate the financial analysis and evaluate the feasibility of

the new business venture that is to be undertaken by Felix after his retirement. The new business

venture is about opening a retail business of natural pearls, which will be imported from Tahiti

and would be sold in Zurich. The viability of the business venture is evaluated by the

development of the financial plan, which involves the use of techniques of capital budgeting and

forecasting of the annual and monthly cash generated from the sales of pearl. Development of the

financial plan incorporates evaluation of the profit and loss statement, balance sheet, annual cash

flow, sensitivity analysis and monthly and annual cash flow of the proposed retail business (Barr

and McClellan 2018). It is essential for the entrepreneur to evaluate the sustainability of the

business in the current market scenario by conducting the feasibility analysis. The overall

accumulation of the assets has been done by preparation and evaluation of the balance sheet. In

addition to this, the estimated overall expenditure of the business is evaluated by analyzing the

monthly cash flow generated by the business. Application of discounted cash flow model has

been done to evaluate the time value of projected profits of the profits proposed by new venture.

Discussion:

Summary of all the estimates and assumptions:

In this section, all the estimates and assumptions that are considered necessary for the

analysis is presented.

The exclusive rights for selling the products in Switzerland has been granted for a period

of five years in exchange for the upfront fee of such rights. It has been assumed for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL MANAGEMENT

computation of the figures that the rights have been granted for a period of five years

because it has been assumed that projection would be made for such time period.

The selling price of undrilled pearl in Tahiti is assumed to be at an average value of

14800 XPF each and and Orohena pearls at the discount of 35% would sell the pearls.

Products would be shipped to owner of the business, Felix after the payment is made on

each order. The net purchase price of pearls is XPF 9620 and the amount of air freight

added is XPF 1800. The cost of each pearl after discounting and including freight would

be XPF 11,420. Therefore, the cost price of each pearl in CHF would be then CHF 6372

at the exchange rate of 0.0093. The figures are shown in the table 2.

Furthermore, it is assumed that the salary of employee that is to be paid by Felix is CHF

86400.00 per annum. The salary payable to the assistant hired by Felix from Paula for

delivering and making the pendants would be CHF 350. All the sales made via the

internet or all online sales would be made by credit card and the credit company would

charge 1.2% on the total amount of sales made. It is fifteen days at the end of each

calendar month, the amount would be remitted to Felix .In addition to this, the packaging

and shipping cost per pearl is assumed to be at CHF 15.

It is assumed that Felix would be ordering pearl on monthly basis from Orohena pearls

and a minimum stocks of four week worth of sales is maintained for ensuring that a

suitable range of pearls is supplied to the customers.

The pearls would be stored in a special safe and racking at the cost of CHF 5700 and the

rent would be paid for amount CHF 850 per month for hiring commercial room. Security

deposit for three months and the amount payable monthly is done in advance.

FINANCIAL MANAGEMENT

computation of the figures that the rights have been granted for a period of five years

because it has been assumed that projection would be made for such time period.

The selling price of undrilled pearl in Tahiti is assumed to be at an average value of

14800 XPF each and and Orohena pearls at the discount of 35% would sell the pearls.

Products would be shipped to owner of the business, Felix after the payment is made on

each order. The net purchase price of pearls is XPF 9620 and the amount of air freight

added is XPF 1800. The cost of each pearl after discounting and including freight would

be XPF 11,420. Therefore, the cost price of each pearl in CHF would be then CHF 6372

at the exchange rate of 0.0093. The figures are shown in the table 2.

Furthermore, it is assumed that the salary of employee that is to be paid by Felix is CHF

86400.00 per annum. The salary payable to the assistant hired by Felix from Paula for

delivering and making the pendants would be CHF 350. All the sales made via the

internet or all online sales would be made by credit card and the credit company would

charge 1.2% on the total amount of sales made. It is fifteen days at the end of each

calendar month, the amount would be remitted to Felix .In addition to this, the packaging

and shipping cost per pearl is assumed to be at CHF 15.

It is assumed that Felix would be ordering pearl on monthly basis from Orohena pearls

and a minimum stocks of four week worth of sales is maintained for ensuring that a

suitable range of pearls is supplied to the customers.

The pearls would be stored in a special safe and racking at the cost of CHF 5700 and the

rent would be paid for amount CHF 850 per month for hiring commercial room. Security

deposit for three months and the amount payable monthly is done in advance.

5

FINANCIAL MANAGEMENT

An alarm system would be installed having an initial expenditure of CHF 5500 along

with the monitoring fee of CHF 100 per month.

The pearls would be sold online for, which the site is developed by the website designer,

the total amount spend on planning, and designing the website is CHF 8000. In addition

to this, the amount that would be spend on conducting a market survey is CHF 9000.

The total amount of pearls after the business has been established that would be

demanded monthly is 250 pearls per month.. It is assumed that in the first year of sales,

total units of pearl sold would be 30 units. Packaging and the shipping of pearl within

Switzerland would average CHF 15 per pearl. However, it is further assumed that Felix

would not be charging this price to customers. Therefore, the value of shipping and

packaging cost of pearls in Switzerland would be shown in the income statement, but it

would not be included in the selling price of pearls to customers.

Two students at the cost of CHF 3600 each would run the operation on part time basis.

It is mentioned in the requirement file that any additional amount of money

required in the business can be borrowed by Felix at the rate of 6% per annum.

Felix can borrow an additional amount of CHF 75000 at the rate of 6% per annum.

Felix would also be selling pearls by incorporating into pendants and each pendants

would be sold to Paula at CHF 170. For this purpose, a small drill and jig would be

purchased at the cost of CHF 550 and the clasps and silver chain would cost CHF 25 per

set along with a presentation box at the cost of CHF 7.50 along with hiring an assistant

and cost of delivering the pendant at CHF 350 per month.

It is assumed that the average selling price per pearl in Switzerland would be CHF 270

and the impact of sales tax or VAT is ignored in the calculations.

FINANCIAL MANAGEMENT

An alarm system would be installed having an initial expenditure of CHF 5500 along

with the monitoring fee of CHF 100 per month.

The pearls would be sold online for, which the site is developed by the website designer,

the total amount spend on planning, and designing the website is CHF 8000. In addition

to this, the amount that would be spend on conducting a market survey is CHF 9000.

The total amount of pearls after the business has been established that would be

demanded monthly is 250 pearls per month.. It is assumed that in the first year of sales,

total units of pearl sold would be 30 units. Packaging and the shipping of pearl within

Switzerland would average CHF 15 per pearl. However, it is further assumed that Felix

would not be charging this price to customers. Therefore, the value of shipping and

packaging cost of pearls in Switzerland would be shown in the income statement, but it

would not be included in the selling price of pearls to customers.

Two students at the cost of CHF 3600 each would run the operation on part time basis.

It is mentioned in the requirement file that any additional amount of money

required in the business can be borrowed by Felix at the rate of 6% per annum.

Felix can borrow an additional amount of CHF 75000 at the rate of 6% per annum.

Felix would also be selling pearls by incorporating into pendants and each pendants

would be sold to Paula at CHF 170. For this purpose, a small drill and jig would be

purchased at the cost of CHF 550 and the clasps and silver chain would cost CHF 25 per

set along with a presentation box at the cost of CHF 7.50 along with hiring an assistant

and cost of delivering the pendant at CHF 350 per month.

It is assumed that the average selling price per pearl in Switzerland would be CHF 270

and the impact of sales tax or VAT is ignored in the calculations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL MANAGEMENT

The conversion rate of XPF into CHF is 0.0093 (Xe.com 2019).

The effective income tax rate on the income generated is at 40% and Felix can invest the

additional cash at the rate after tax rate of 4% per annum.

The sales growth rate is decreasing initially and then it has increased in the seventh

month of operation and it is declining subsequently. This has been shown in the table 1.

In the first month of operation, the fixed number of unit of pendant sold would be 30 as

per the contract with Paula. Furthermore, it is assumed that the number of pearls sold

would vary and it stands at 30 units in the first month of operations. This makes total

units sold at the level of 60 units in the first month of operations. However, there is an

increase in the number of unit of pearl sold every month and therefore, it is estimated that

the sales of variable units would grow as per the following table.

Table 1: Projected sales volume

(Source: created by the author)

FINANCIAL MANAGEMENT

The conversion rate of XPF into CHF is 0.0093 (Xe.com 2019).

The effective income tax rate on the income generated is at 40% and Felix can invest the

additional cash at the rate after tax rate of 4% per annum.

The sales growth rate is decreasing initially and then it has increased in the seventh

month of operation and it is declining subsequently. This has been shown in the table 1.

In the first month of operation, the fixed number of unit of pendant sold would be 30 as

per the contract with Paula. Furthermore, it is assumed that the number of pearls sold

would vary and it stands at 30 units in the first month of operations. This makes total

units sold at the level of 60 units in the first month of operations. However, there is an

increase in the number of unit of pearl sold every month and therefore, it is estimated that

the sales of variable units would grow as per the following table.

Table 1: Projected sales volume

(Source: created by the author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL MANAGEMENT

The total cost incurred for purchasing 60 units of pearl in the first year of operation is

XPF 685200 where XPF is the international code of the currency used in Tahiti. In

addition to this, the estimated amount of total investment that is to be made is CHF

88147.36. The figures can be accessed from table 2.

It is assumed that the special safe and the small drill and jig would be depreciated under

straight-line method and the estimated useful life of the two products is assumed to be

five years.

The website designing cost, market research costs and distribution rights would be

amortized for five years.

For the forecasting purpose, it is assumed that the net profit would increase as per the

current sales growth rate that is 17.11% for next three years. It is further assumed that

from forth year, the sale would decrease due to fall in demand which would cause the net

profit to increase at the rate 10% in the fourth year and 5% in the fifth year.

The market interest rate is 6% as per the given case study and therefore, the discount rate

is taken as 6% for the valuation purpose.

It is estimated that the distribution right would be CHF 40000.

The total amount of initial investment is assumed to be at CHF 88147.36 and the amount

of initial investment comprised of airfreight, material cost, packaging cost for sales for 60

units and shipping and packaging cost for 30 units respectively.

FINANCIAL MANAGEMENT

The total cost incurred for purchasing 60 units of pearl in the first year of operation is

XPF 685200 where XPF is the international code of the currency used in Tahiti. In

addition to this, the estimated amount of total investment that is to be made is CHF

88147.36. The figures can be accessed from table 2.

It is assumed that the special safe and the small drill and jig would be depreciated under

straight-line method and the estimated useful life of the two products is assumed to be

five years.

The website designing cost, market research costs and distribution rights would be

amortized for five years.

For the forecasting purpose, it is assumed that the net profit would increase as per the

current sales growth rate that is 17.11% for next three years. It is further assumed that

from forth year, the sale would decrease due to fall in demand which would cause the net

profit to increase at the rate 10% in the fourth year and 5% in the fifth year.

The market interest rate is 6% as per the given case study and therefore, the discount rate

is taken as 6% for the valuation purpose.

It is estimated that the distribution right would be CHF 40000.

The total amount of initial investment is assumed to be at CHF 88147.36 and the amount

of initial investment comprised of airfreight, material cost, packaging cost for sales for 60

units and shipping and packaging cost for 30 units respectively.

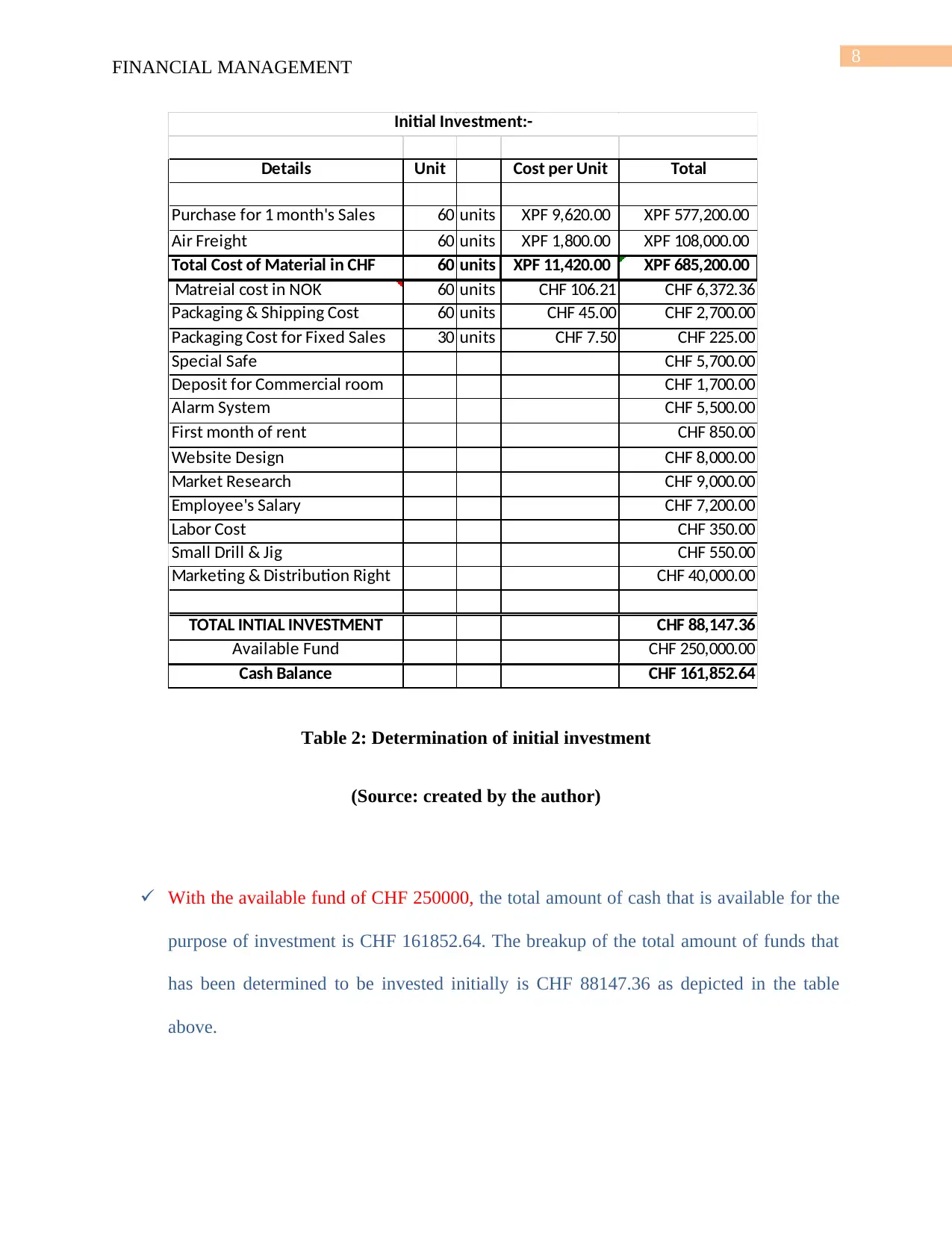

8

FINANCIAL MANAGEMENT

Details Unit Cost per Unit Total

Purchase for 1 month's Sales 60 units XPF 9,620.00 XPF 577,200.00

Air Freight 60 units XPF 1,800.00 XPF 108,000.00

Total Cost of Material in CHF 60 units XPF 11,420.00 XPF 685,200.00

Matreial cost in NOK 60 units CHF 106.21 CHF 6,372.36

Packaging & Shipping Cost 60 units CHF 45.00 CHF 2,700.00

Packaging Cost for Fixed Sales 30 units CHF 7.50 CHF 225.00

Special Safe CHF 5,700.00

Deposit for Commercial room CHF 1,700.00

Alarm System CHF 5,500.00

First month of rent CHF 850.00

Website Design CHF 8,000.00

Market Research CHF 9,000.00

Employee's Salary CHF 7,200.00

Labor Cost CHF 350.00

Small Drill & Jig CHF 550.00

Marketing & Distribution Right CHF 40,000.00

TOTAL INTIAL INVESTMENT CHF 88,147.36

Available Fund CHF 250,000.00

Cash Balance CHF 161,852.64

Initial Investment:-

Table 2: Determination of initial investment

(Source: created by the author)

With the available fund of CHF 250000, the total amount of cash that is available for the

purpose of investment is CHF 161852.64. The breakup of the total amount of funds that

has been determined to be invested initially is CHF 88147.36 as depicted in the table

above.

FINANCIAL MANAGEMENT

Details Unit Cost per Unit Total

Purchase for 1 month's Sales 60 units XPF 9,620.00 XPF 577,200.00

Air Freight 60 units XPF 1,800.00 XPF 108,000.00

Total Cost of Material in CHF 60 units XPF 11,420.00 XPF 685,200.00

Matreial cost in NOK 60 units CHF 106.21 CHF 6,372.36

Packaging & Shipping Cost 60 units CHF 45.00 CHF 2,700.00

Packaging Cost for Fixed Sales 30 units CHF 7.50 CHF 225.00

Special Safe CHF 5,700.00

Deposit for Commercial room CHF 1,700.00

Alarm System CHF 5,500.00

First month of rent CHF 850.00

Website Design CHF 8,000.00

Market Research CHF 9,000.00

Employee's Salary CHF 7,200.00

Labor Cost CHF 350.00

Small Drill & Jig CHF 550.00

Marketing & Distribution Right CHF 40,000.00

TOTAL INTIAL INVESTMENT CHF 88,147.36

Available Fund CHF 250,000.00

Cash Balance CHF 161,852.64

Initial Investment:-

Table 2: Determination of initial investment

(Source: created by the author)

With the available fund of CHF 250000, the total amount of cash that is available for the

purpose of investment is CHF 161852.64. The breakup of the total amount of funds that

has been determined to be invested initially is CHF 88147.36 as depicted in the table

above.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCIAL MANAGEMENT

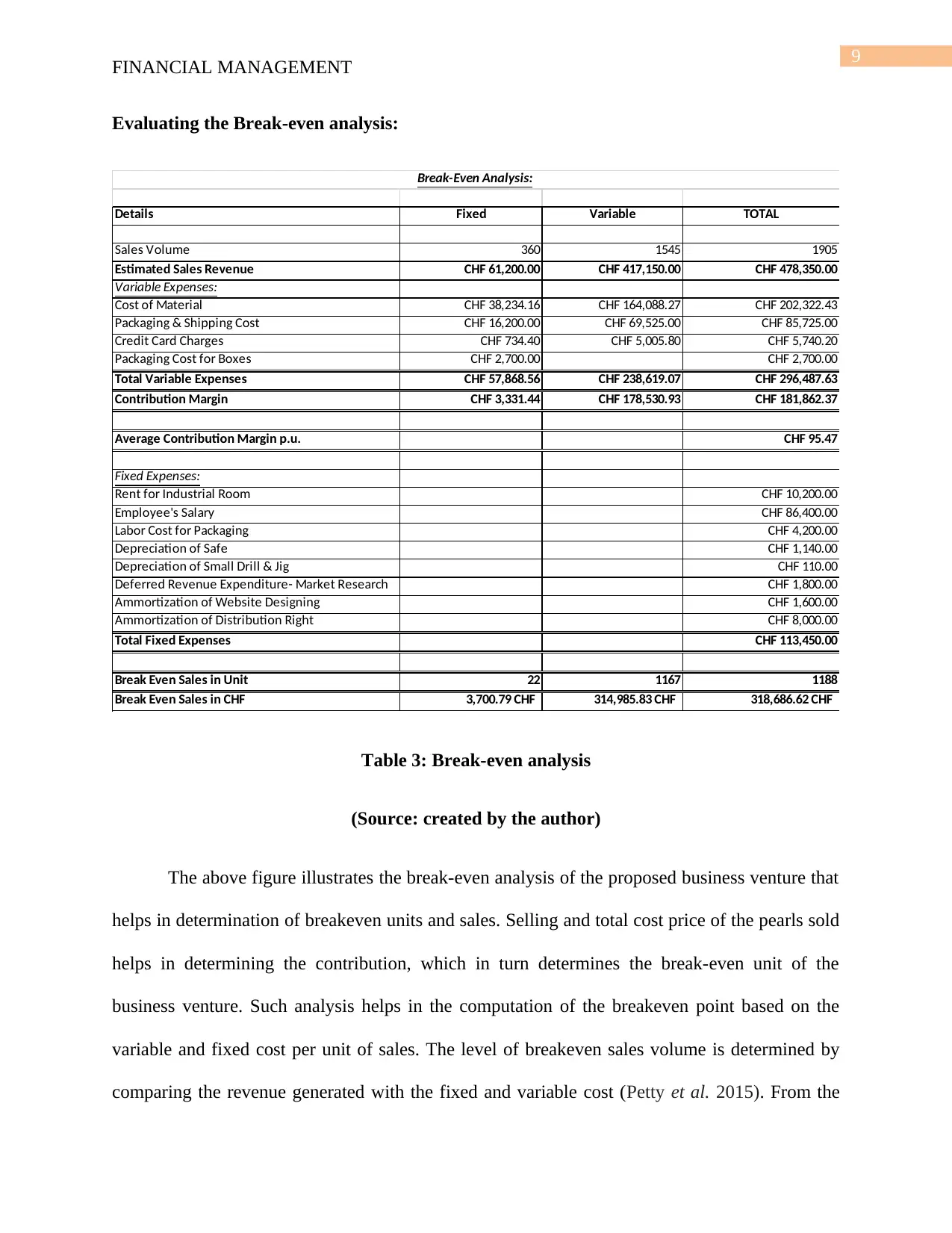

Evaluating the Break-even analysis:

Details Fixed Variable TOTAL

Sales Volume 360 1545 1905

Estimated Sales Revenue CHF 61,200.00 CHF 417,150.00 CHF 478,350.00

Variable Expenses:

Cost of Material CHF 38,234.16 CHF 164,088.27 CHF 202,322.43

Packaging & Shipping Cost CHF 16,200.00 CHF 69,525.00 CHF 85,725.00

Credit Card Charges CHF 734.40 CHF 5,005.80 CHF 5,740.20

Packaging Cost for Boxes CHF 2,700.00 CHF 2,700.00

Total Variable Expenses CHF 57,868.56 CHF 238,619.07 CHF 296,487.63

Contribution Margin CHF 3,331.44 CHF 178,530.93 CHF 181,862.37

Average Contribution Margin p.u. CHF 95.47

Fixed Expenses:

Rent for Industrial Room CHF 10,200.00

Employee's Salary CHF 86,400.00

Labor Cost for Packaging CHF 4,200.00

Depreciation of Safe CHF 1,140.00

Depreciation of Small Drill & Jig CHF 110.00

Deferred Revenue Expenditure- Market Research CHF 1,800.00

Ammortization of Website Designing CHF 1,600.00

Ammortization of Distribution Right CHF 8,000.00

Total Fixed Expenses CHF 113,450.00

Break Even Sales in Unit 22 1167 1188

Break Even Sales in CHF 3,700.79 CHF 314,985.83 CHF 318,686.62 CHF

Break-Even Analysis:

Table 3: Break-even analysis

(Source: created by the author)

The above figure illustrates the break-even analysis of the proposed business venture that

helps in determination of breakeven units and sales. Selling and total cost price of the pearls sold

helps in determining the contribution, which in turn determines the break-even unit of the

business venture. Such analysis helps in the computation of the breakeven point based on the

variable and fixed cost per unit of sales. The level of breakeven sales volume is determined by

comparing the revenue generated with the fixed and variable cost (Petty et al. 2015). From the

FINANCIAL MANAGEMENT

Evaluating the Break-even analysis:

Details Fixed Variable TOTAL

Sales Volume 360 1545 1905

Estimated Sales Revenue CHF 61,200.00 CHF 417,150.00 CHF 478,350.00

Variable Expenses:

Cost of Material CHF 38,234.16 CHF 164,088.27 CHF 202,322.43

Packaging & Shipping Cost CHF 16,200.00 CHF 69,525.00 CHF 85,725.00

Credit Card Charges CHF 734.40 CHF 5,005.80 CHF 5,740.20

Packaging Cost for Boxes CHF 2,700.00 CHF 2,700.00

Total Variable Expenses CHF 57,868.56 CHF 238,619.07 CHF 296,487.63

Contribution Margin CHF 3,331.44 CHF 178,530.93 CHF 181,862.37

Average Contribution Margin p.u. CHF 95.47

Fixed Expenses:

Rent for Industrial Room CHF 10,200.00

Employee's Salary CHF 86,400.00

Labor Cost for Packaging CHF 4,200.00

Depreciation of Safe CHF 1,140.00

Depreciation of Small Drill & Jig CHF 110.00

Deferred Revenue Expenditure- Market Research CHF 1,800.00

Ammortization of Website Designing CHF 1,600.00

Ammortization of Distribution Right CHF 8,000.00

Total Fixed Expenses CHF 113,450.00

Break Even Sales in Unit 22 1167 1188

Break Even Sales in CHF 3,700.79 CHF 314,985.83 CHF 318,686.62 CHF

Break-Even Analysis:

Table 3: Break-even analysis

(Source: created by the author)

The above figure illustrates the break-even analysis of the proposed business venture that

helps in determination of breakeven units and sales. Selling and total cost price of the pearls sold

helps in determining the contribution, which in turn determines the break-even unit of the

business venture. Such analysis helps in the computation of the breakeven point based on the

variable and fixed cost per unit of sales. The level of breakeven sales volume is determined by

comparing the revenue generated with the fixed and variable cost (Petty et al. 2015). From the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINANCIAL MANAGEMENT

table presented above, it is observed that retail business of natural pearls would achieve break

even when 1188 units are sold. Moreover, total amount of break-even sales to be made is CHF

318686.62, whereas total amount of fixed and variable expenses is recorded at CHF 113450.00

and CHF 296487.63 respectively as per the above table.

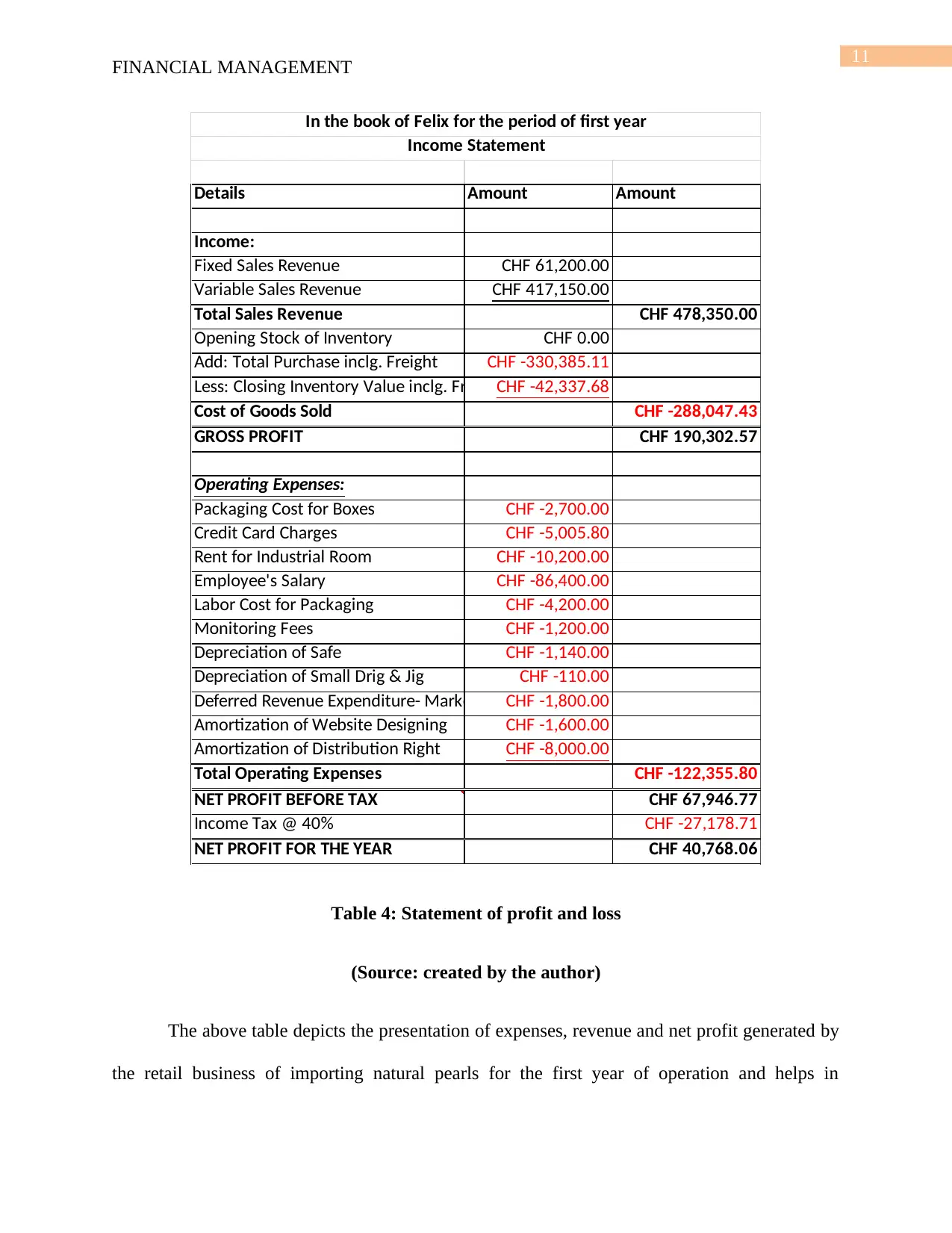

Analysis of the profit and loss statement for the first year of operation:

In the book of Felix for the first year of operations:

FINANCIAL MANAGEMENT

table presented above, it is observed that retail business of natural pearls would achieve break

even when 1188 units are sold. Moreover, total amount of break-even sales to be made is CHF

318686.62, whereas total amount of fixed and variable expenses is recorded at CHF 113450.00

and CHF 296487.63 respectively as per the above table.

Analysis of the profit and loss statement for the first year of operation:

In the book of Felix for the first year of operations:

11

FINANCIAL MANAGEMENT

Details Amount Amount

Income:

Fixed Sales Revenue CHF 61,200.00

Variable Sales Revenue CHF 417,150.00

Total Sales Revenue CHF 478,350.00

Opening Stock of Inventory CHF 0.00

Add: Total Purchase inclg. Freight CHF -330,385.11

Less: Closing Inventory Value inclg. FreightCHF -42,337.68

Cost of Goods Sold CHF -288,047.43

GROSS PROFIT CHF 190,302.57

Operating Expenses:

Packaging Cost for Boxes CHF -2,700.00

Credit Card Charges CHF -5,005.80

Rent for Industrial Room CHF -10,200.00

Employee's Salary CHF -86,400.00

Labor Cost for Packaging CHF -4,200.00

Monitoring Fees CHF -1,200.00

Depreciation of Safe CHF -1,140.00

Depreciation of Small Drig & Jig CHF -110.00

Deferred Revenue Expenditure- Market ResearchCHF -1,800.00

Amortization of Website Designing CHF -1,600.00

Amortization of Distribution Right CHF -8,000.00

Total Operating Expenses CHF -122,355.80

NET PROFIT BEFORE TAX CHF 67,946.77

Income Tax @ 40% CHF -27,178.71

NET PROFIT FOR THE YEAR CHF 40,768.06

Income Statement

In the book of Felix for the period of first year

Table 4: Statement of profit and loss

(Source: created by the author)

The above table depicts the presentation of expenses, revenue and net profit generated by

the retail business of importing natural pearls for the first year of operation and helps in

FINANCIAL MANAGEMENT

Details Amount Amount

Income:

Fixed Sales Revenue CHF 61,200.00

Variable Sales Revenue CHF 417,150.00

Total Sales Revenue CHF 478,350.00

Opening Stock of Inventory CHF 0.00

Add: Total Purchase inclg. Freight CHF -330,385.11

Less: Closing Inventory Value inclg. FreightCHF -42,337.68

Cost of Goods Sold CHF -288,047.43

GROSS PROFIT CHF 190,302.57

Operating Expenses:

Packaging Cost for Boxes CHF -2,700.00

Credit Card Charges CHF -5,005.80

Rent for Industrial Room CHF -10,200.00

Employee's Salary CHF -86,400.00

Labor Cost for Packaging CHF -4,200.00

Monitoring Fees CHF -1,200.00

Depreciation of Safe CHF -1,140.00

Depreciation of Small Drig & Jig CHF -110.00

Deferred Revenue Expenditure- Market ResearchCHF -1,800.00

Amortization of Website Designing CHF -1,600.00

Amortization of Distribution Right CHF -8,000.00

Total Operating Expenses CHF -122,355.80

NET PROFIT BEFORE TAX CHF 67,946.77

Income Tax @ 40% CHF -27,178.71

NET PROFIT FOR THE YEAR CHF 40,768.06

Income Statement

In the book of Felix for the period of first year

Table 4: Statement of profit and loss

(Source: created by the author)

The above table depicts the presentation of expenses, revenue and net profit generated by

the retail business of importing natural pearls for the first year of operation and helps in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.