ESOFT HND Business: Management Accounting Report on Penguin Sportswear

VerifiedAdded on 2022/01/18

|28

|6824

|36

Report

AI Summary

This report provides a comprehensive overview of management accounting practices within Penguin Sportswear (PCT.) Ltd, a Sri Lankan exporter of sportswear. It begins with an introduction to the company, its vision, mission, and operational structure, including its manufacturing processes and key competitors. The report then differentiates between management accounting and financial accounting, highlighting the advantages and disadvantages of management accounting, such as improved decision-making, increased efficiency, and cost control. It delves into the current state of management accounting within Penguin Sportswear, identifying the absence of a formal system and the reliance on MS Excel. Furthermore, the report explores the principles of management accounting, including communication, relevance of information, stewardship, and impact analysis. Finally, it examines various types of management accounting systems, such as cost accounting, job costing, inventory management, and price optimizing systems, along with their respective benefits, and concludes with a discussion of different management accounting reports and their purpose in planning and decision-making.

ACKNOWLEDGEMENT

I would like to extend my gratitude towards everyone who helped me in completing this report

which is a part in HND in business management at ESOFT Metro Campus.

First and foremost, I would like to express my heart full of thanks to my parents who gave this

opportunity to start my higher education at ESOFT Metro Campus.

I would also like to give my heart full of thanks to my lecturer Miss Ruwani Ekanayake, who

supervised me in completing this report as she deserves the word of appreciation.

Thank you …

Sathsarani Gunasekara

I would like to extend my gratitude towards everyone who helped me in completing this report

which is a part in HND in business management at ESOFT Metro Campus.

First and foremost, I would like to express my heart full of thanks to my parents who gave this

opportunity to start my higher education at ESOFT Metro Campus.

I would also like to give my heart full of thanks to my lecturer Miss Ruwani Ekanayake, who

supervised me in completing this report as she deserves the word of appreciation.

Thank you …

Sathsarani Gunasekara

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity 01

Introduction to the penguin’s sportswear (pct.) Ltd

Penguin sportswear is a Sri Lankan exporter of quality products to the global market registered

with the Sri Lankan Export Development Board and it was founded in 1989. Penguin

sportswear is among Srilanka’s leading apparel manufacturers and caters to reputed retailers

across UK and Europe. In penguin sportswear they continuously strive to create value in their

business while constantly innovating their products and services. The pension sportswear is a

medium sized E-turf that manufactures sportswear. It has been registered as a private limited

company in 2010. It manufactures and sells its own brand of sportswear under 3 main

categories namely,

Premium – High end brand for quality conscious customers

Vantage –good quality brands with the medium price range

Regular –Average quality brand with low price range

Apart from the head office, the company has three branches in key locations to manage all the

activities. The main competitor is the Lanka Sportswear.

Vision

“We CREATE value in our business

We make every attempt to INNOVATE our products and services

We strive to EXCEL with our people and processes

With the aspiration to DELIGHT our customers in every way”

Mission

“A great place to work that achieves operational excellence

while ensuring a high degree of social and environmental responsibility”

(Lanka, 2021)

Management Accounting

What is management accounting?

Introduction to the penguin’s sportswear (pct.) Ltd

Penguin sportswear is a Sri Lankan exporter of quality products to the global market registered

with the Sri Lankan Export Development Board and it was founded in 1989. Penguin

sportswear is among Srilanka’s leading apparel manufacturers and caters to reputed retailers

across UK and Europe. In penguin sportswear they continuously strive to create value in their

business while constantly innovating their products and services. The pension sportswear is a

medium sized E-turf that manufactures sportswear. It has been registered as a private limited

company in 2010. It manufactures and sells its own brand of sportswear under 3 main

categories namely,

Premium – High end brand for quality conscious customers

Vantage –good quality brands with the medium price range

Regular –Average quality brand with low price range

Apart from the head office, the company has three branches in key locations to manage all the

activities. The main competitor is the Lanka Sportswear.

Vision

“We CREATE value in our business

We make every attempt to INNOVATE our products and services

We strive to EXCEL with our people and processes

With the aspiration to DELIGHT our customers in every way”

Mission

“A great place to work that achieves operational excellence

while ensuring a high degree of social and environmental responsibility”

(Lanka, 2021)

Management Accounting

What is management accounting?

Management accounting is also known as managerial accounting and can be defined as a

process of providing information and financial resources to managers in making decisions.

Management accounting is only used by the organization's internal team, and this is the only

thing that differentiates it from financial accounting. (Topper-2021) In this process, the

financial information and reports, such as the invoice, the financial balance statement, is shared

by the financial administration with the company's management team. The goal of management

accounting is to use this statistical data and make a better and accurate decision, controlling the

company, business activities and development.

Management accountants work for public companies, private businesses, and government

agencies. Their duties include recording and beating numbers, selecting and managing

company investments, risk management, budgeting, planning, strategizing and decision

making.

Financial Accounting

Financial accounting is a specific branch of accounting that involves a process of recording,

summarizing, and reporting the large number of transactions resulting from business operations

over a period of time. (Will Kenton-2020) These transactions are summarized in the

preparation of financial statements, including the balance sheet, the income statement and the

cash flow statement, which record the operating performance of the company during a specified

period.

(Kenton, 2020)

The advantages and disadvantages of management accounting is explained below in

detailed;

Advantages

1. Better decision making: The management accounting helps in effective decision making for

an organization. It supplies all the required information in the form of charts and forecasts

to the management team. All this information enables managers in performing detailed

analysis and taking correct decisions.

2. Increase efficiency: The management accounting increases the efficiency of operation of the

company. Everything is done in management accounting with a scientific system for

evaluating and comparing the performance with this we find deviations, take promotional

process of providing information and financial resources to managers in making decisions.

Management accounting is only used by the organization's internal team, and this is the only

thing that differentiates it from financial accounting. (Topper-2021) In this process, the

financial information and reports, such as the invoice, the financial balance statement, is shared

by the financial administration with the company's management team. The goal of management

accounting is to use this statistical data and make a better and accurate decision, controlling the

company, business activities and development.

Management accountants work for public companies, private businesses, and government

agencies. Their duties include recording and beating numbers, selecting and managing

company investments, risk management, budgeting, planning, strategizing and decision

making.

Financial Accounting

Financial accounting is a specific branch of accounting that involves a process of recording,

summarizing, and reporting the large number of transactions resulting from business operations

over a period of time. (Will Kenton-2020) These transactions are summarized in the

preparation of financial statements, including the balance sheet, the income statement and the

cash flow statement, which record the operating performance of the company during a specified

period.

(Kenton, 2020)

The advantages and disadvantages of management accounting is explained below in

detailed;

Advantages

1. Better decision making: The management accounting helps in effective decision making for

an organization. It supplies all the required information in the form of charts and forecasts

to the management team. All this information enables managers in performing detailed

analysis and taking correct decisions.

2. Increase efficiency: The management accounting increases the efficiency of operation of the

company. Everything is done in management accounting with a scientific system for

evaluating and comparing the performance with this we find deviations, take promotional

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decisions on this basis. Other employees will also be motivated with this because if their

performance will be favorable, they get reward of this. Thus, management accounting

increases the efficiency.

3. Maximizing the profitability: using the management accounting’s budgetary control and

capital budgeting tool, the company can easily succeed to reduce both the operating and

capital expenditures. After this, company can reduce its price and then company will

receive super profits.

4. Control business cash flow: it is one of the advantage of the management accounting that it

can be used for controlling of the business’s cash flow. We all know that cash in hand is

better than in fixed properties if there is any emergency to pay the loan or debt so, the

management accountant deeply studies from where the money is coming and where it is

going. To check on the misuse of money will surely control of the business cash flow.

The disadvantages

1. Personal bias: the accounting branch is subject to the personal bias and prejudices by the

management. The effectiveness of the management accounting may be affected by the

interpretation and analysis capability of individuals.

2. Lack of specific procedure: Management accounting does not have any specific rules and

principles to follow. In the absence of any guidelines, this branch of accounting may

provide inaccurate data.

3. Costly: the installation of a management accounting system requires huge expenses as they

need to hire a management accountant. such high costs cannot be bear by the small business

organization.

4. Provides only data : It only supplies data to the management but does not provide any plan

of action or decision .Management accounting cannot substitute the role of management and

can only help them in their role by providing the required data . (GOOGLE , n.d.)

performance will be favorable, they get reward of this. Thus, management accounting

increases the efficiency.

3. Maximizing the profitability: using the management accounting’s budgetary control and

capital budgeting tool, the company can easily succeed to reduce both the operating and

capital expenditures. After this, company can reduce its price and then company will

receive super profits.

4. Control business cash flow: it is one of the advantage of the management accounting that it

can be used for controlling of the business’s cash flow. We all know that cash in hand is

better than in fixed properties if there is any emergency to pay the loan or debt so, the

management accountant deeply studies from where the money is coming and where it is

going. To check on the misuse of money will surely control of the business cash flow.

The disadvantages

1. Personal bias: the accounting branch is subject to the personal bias and prejudices by the

management. The effectiveness of the management accounting may be affected by the

interpretation and analysis capability of individuals.

2. Lack of specific procedure: Management accounting does not have any specific rules and

principles to follow. In the absence of any guidelines, this branch of accounting may

provide inaccurate data.

3. Costly: the installation of a management accounting system requires huge expenses as they

need to hire a management accountant. such high costs cannot be bear by the small business

organization.

4. Provides only data : It only supplies data to the management but does not provide any plan

of action or decision .Management accounting cannot substitute the role of management and

can only help them in their role by providing the required data . (GOOGLE , n.d.)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

How the management accounting process is working in

penguin sportswear?

The manufacturing set up was started in January 2011 with a small manufacturing plant but, the

production is multiplied over the years. There is no proper management accounting system in

penguin’s sportswear. The production Manager in charge of the accounting division of the

production unit is Mr. Roy Pereira. He has no background in management accounting and

complies all the management accounting records on MS EXCEL. The reports which has been

prepared do not reflect the exact cost of the manufactured products as they change significantly

every year.

The principles of management accounting

The principles of Management accounting are as follows;

Communication provides insight that is influential

Objective: To drive better decisions about strategy and its execution at all levels

Management accounting begins and ends with conversation, which enhances decision

making ability .Good communication of critical information facilitates cross silos to

management accounting and facilitates integrated thinking .The consequences of actions

in one aspect of the business can be better understood in another area .The most relevant

information can be obtained and analyzed by discussing the requirements of the

decision makers .This means that the recommendations are useful to the decision

makers and can have an impact .When the right people have the right information at the

right time ,it takes a better place to get what they want which will drive long term value

generation .This is how the management accounting influences information based on

decision making. (ESOFT METRO CAMPUS , 2021)

Information is relevant

Objective: to help the organization plan and source the information needed for creating strategy

and tactics for execution

penguin sportswear?

The manufacturing set up was started in January 2011 with a small manufacturing plant but, the

production is multiplied over the years. There is no proper management accounting system in

penguin’s sportswear. The production Manager in charge of the accounting division of the

production unit is Mr. Roy Pereira. He has no background in management accounting and

complies all the management accounting records on MS EXCEL. The reports which has been

prepared do not reflect the exact cost of the manufactured products as they change significantly

every year.

The principles of management accounting

The principles of Management accounting are as follows;

Communication provides insight that is influential

Objective: To drive better decisions about strategy and its execution at all levels

Management accounting begins and ends with conversation, which enhances decision

making ability .Good communication of critical information facilitates cross silos to

management accounting and facilitates integrated thinking .The consequences of actions

in one aspect of the business can be better understood in another area .The most relevant

information can be obtained and analyzed by discussing the requirements of the

decision makers .This means that the recommendations are useful to the decision

makers and can have an impact .When the right people have the right information at the

right time ,it takes a better place to get what they want which will drive long term value

generation .This is how the management accounting influences information based on

decision making. (ESOFT METRO CAMPUS , 2021)

Information is relevant

Objective: to help the organization plan and source the information needed for creating strategy

and tactics for execution

The main role of management accounting is to make relevant information available to the

decision makers on a timely basis. Following communication principle, the decision at hand

and needs of the decision makers are known and understood. This principle therefore involves

in the identification, collection, validation etc. .as it requires achieving an appropriate balance

between the past, present and future related information’s.

Stewardship builds and trust

Objective: To actively manage relationships and sources so that the financial and non-

financial assets, reputation, and value of the organization are protected.

As mentioned before, an effective management accounting function is one where

competent people apply the principles to their practice areas. people who consistently

adhere to good values and best practices become trusted guardians of an organizations

value.

Impact on value is analyzed

Objective: To stimulate different scenarios that demonstrate the cause and effect relationships

between inputs and outputs.

The focus of the principle is on the interaction between management accounting and the

business model by modelling the impact of risks and opportunities, the effect on strategic

outcomes is quantified. This principle requires a thorough understanding of the business model

and the wider macro-economic environment .It involves in analyzing information along the

value generation path ,focus on the risks etc. (ESOFT METRO CAMPUS , 2021)

Different types of Management accounting systems

There are many types of management accounting systems namely,

Cost Accounting systems

decision makers on a timely basis. Following communication principle, the decision at hand

and needs of the decision makers are known and understood. This principle therefore involves

in the identification, collection, validation etc. .as it requires achieving an appropriate balance

between the past, present and future related information’s.

Stewardship builds and trust

Objective: To actively manage relationships and sources so that the financial and non-

financial assets, reputation, and value of the organization are protected.

As mentioned before, an effective management accounting function is one where

competent people apply the principles to their practice areas. people who consistently

adhere to good values and best practices become trusted guardians of an organizations

value.

Impact on value is analyzed

Objective: To stimulate different scenarios that demonstrate the cause and effect relationships

between inputs and outputs.

The focus of the principle is on the interaction between management accounting and the

business model by modelling the impact of risks and opportunities, the effect on strategic

outcomes is quantified. This principle requires a thorough understanding of the business model

and the wider macro-economic environment .It involves in analyzing information along the

value generation path ,focus on the risks etc. (ESOFT METRO CAMPUS , 2021)

Different types of Management accounting systems

There are many types of management accounting systems namely,

Cost Accounting systems

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting is concern with recording, classifying and summarizing costs for the

determination of costs of products or services, planning, controlling and reducing such costs

and furnishing of information to management for decision making. This method helps to

estimate and also takes into account the organization’s probability, inventory and cost control

process.

The objectives of cost accounting are cost reduction, estimation of costs, cost control and

providing basis for operating policy.

The benefits of cost accounting systems are as follows;

1. Classification and sub division controls

2. Control of materials, labor and overhead costs

3. Budgeting

4. Best use of limited resources

5. Expansion (ESOFT METRO CAMPUS , 2021)

Job costing systems

This method assists in assigning production costs to each product in the business, thereby

enabling ordering costs. Job costing is a production cost method adopted by an enterprise that

offers a limited range of unique products. The benefits of job costing systems are as follows;

1. Profitability : The job costing systems allows you to assign costs separately to individual

operations and calculate the profit margin you ‘ll be getting on each job (ESOFT METRO

CAMPUS , 2021) .

2. Performance: a job order costing system also enables you to access the performance of

your employees, job costing provides sufficient information to help you to evaluate

individual performance data in terms of productivity, efficiency and cost control. With the

help of these tools you can identify the employees who fail to meet performance

expectations . (ESOFT METRO CAMPUS , 2021)

3. Accessibility : the system provides access to the expenses incurred on each job ,even during

the manufacturing process .This gives you the opportunity to check the costs one by one ,

identify all the items included ,and understand why they happened .based on your

determination of costs of products or services, planning, controlling and reducing such costs

and furnishing of information to management for decision making. This method helps to

estimate and also takes into account the organization’s probability, inventory and cost control

process.

The objectives of cost accounting are cost reduction, estimation of costs, cost control and

providing basis for operating policy.

The benefits of cost accounting systems are as follows;

1. Classification and sub division controls

2. Control of materials, labor and overhead costs

3. Budgeting

4. Best use of limited resources

5. Expansion (ESOFT METRO CAMPUS , 2021)

Job costing systems

This method assists in assigning production costs to each product in the business, thereby

enabling ordering costs. Job costing is a production cost method adopted by an enterprise that

offers a limited range of unique products. The benefits of job costing systems are as follows;

1. Profitability : The job costing systems allows you to assign costs separately to individual

operations and calculate the profit margin you ‘ll be getting on each job (ESOFT METRO

CAMPUS , 2021) .

2. Performance: a job order costing system also enables you to access the performance of

your employees, job costing provides sufficient information to help you to evaluate

individual performance data in terms of productivity, efficiency and cost control. With the

help of these tools you can identify the employees who fail to meet performance

expectations . (ESOFT METRO CAMPUS , 2021)

3. Accessibility : the system provides access to the expenses incurred on each job ,even during

the manufacturing process .This gives you the opportunity to check the costs one by one ,

identify all the items included ,and understand why they happened .based on your

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

findings ,you can develop specific strategies to control the costs better in future. (ESOFT

METRO CAMPUS , 2021)

4. Continue monitoring : job order costing allows you to monitor the production process

continuously ,giving you the enough time to identify the potential issues and making

corrections to avoid catastrophic situations, such as producing defective items or going

over budget even before the manufacturing process ends . (ESOFT METRO CAMPUS ,

2021)

Inventory Management system

An inventory system is the combination of technology and processes and procedures

that oversee the monitoring and maintenance of stock, whether those products are raw

materials, company assets or finished products ready to be sent to vendors or end

consumers. The objectives of inventory management system are minimizing inventory

investment, provide an acceptable level of customer service and allow cost efficient

operations. The benefits of inventory management systems are as follows;

1. Schedule maintenance

2. Cut costs and increase profits

3. Keep order accurate planning

4. Know thyself (ESOFT METRO CAMPUS , 2021)

Price optimizing systems

This system helps in controlling the price of the resources reeled to the company. This system

helps in making decisions in regard to the prices of different products at the same time. It will

also help in determine the levels of demand of products at changing the levels of prices. Hence,

this helps determining the structures of pricing in order to undertake the promotion pricing and

discounted pricing. The benefits of price optimizing systems are as follows;

1. Automation benefits

2. Speed of decision making

3. Direct financial benefits

METRO CAMPUS , 2021)

4. Continue monitoring : job order costing allows you to monitor the production process

continuously ,giving you the enough time to identify the potential issues and making

corrections to avoid catastrophic situations, such as producing defective items or going

over budget even before the manufacturing process ends . (ESOFT METRO CAMPUS ,

2021)

Inventory Management system

An inventory system is the combination of technology and processes and procedures

that oversee the monitoring and maintenance of stock, whether those products are raw

materials, company assets or finished products ready to be sent to vendors or end

consumers. The objectives of inventory management system are minimizing inventory

investment, provide an acceptable level of customer service and allow cost efficient

operations. The benefits of inventory management systems are as follows;

1. Schedule maintenance

2. Cut costs and increase profits

3. Keep order accurate planning

4. Know thyself (ESOFT METRO CAMPUS , 2021)

Price optimizing systems

This system helps in controlling the price of the resources reeled to the company. This system

helps in making decisions in regard to the prices of different products at the same time. It will

also help in determine the levels of demand of products at changing the levels of prices. Hence,

this helps determining the structures of pricing in order to undertake the promotion pricing and

discounted pricing. The benefits of price optimizing systems are as follows;

1. Automation benefits

2. Speed of decision making

3. Direct financial benefits

4. Ensuring consistency (ESOFT METRO CAMPUS , 2021)

Different management accounting reports

Management accounting reports are also known as cost accounting reports. The purpose of the

management accounting reports is to help in planning, monitoring and determining decisions on

the way forward. The different types of accounting reports are mentioned below;

1. Cost reports : Managerial accounting calculates the costs of items produced .This is done

by taking all the raw products costs ,overhead ,labor and any additional costs into

consideration .The totals are divided by the amounts of the products which are

produced .All of this information’s are summarized in a cost report .This reports helps in

proper identification of the costs ,profits and the expenses in relation to Penguins

sportswear .Thus it provides indication of the aspect of the earnings in penguins sportswear

that is related with one particular product.

2. Order information report:

This provides the information in regard to the operations of penguin’s sportswear thus, it helps

in managing the operations of the company in order to reduce the ordering cost of the products.

3. Budgets: budgets are typically created by using the prior year’s budgets and adjusting to

future projections. A company’s budget list all the sources of revenue and expenses. It helps

in making plans for the company which is the penguins sportswear in order to analyze the

performance of the company and also helps in evaluating the performance of the

departments and cost controlling.

4. Performance report: this report helps in comparison of the actual performance with the

budgeted performance.

Different management accounting reports

Management accounting reports are also known as cost accounting reports. The purpose of the

management accounting reports is to help in planning, monitoring and determining decisions on

the way forward. The different types of accounting reports are mentioned below;

1. Cost reports : Managerial accounting calculates the costs of items produced .This is done

by taking all the raw products costs ,overhead ,labor and any additional costs into

consideration .The totals are divided by the amounts of the products which are

produced .All of this information’s are summarized in a cost report .This reports helps in

proper identification of the costs ,profits and the expenses in relation to Penguins

sportswear .Thus it provides indication of the aspect of the earnings in penguins sportswear

that is related with one particular product.

2. Order information report:

This provides the information in regard to the operations of penguin’s sportswear thus, it helps

in managing the operations of the company in order to reduce the ordering cost of the products.

3. Budgets: budgets are typically created by using the prior year’s budgets and adjusting to

future projections. A company’s budget list all the sources of revenue and expenses. It helps

in making plans for the company which is the penguins sportswear in order to analyze the

performance of the company and also helps in evaluating the performance of the

departments and cost controlling.

4. Performance report: this report helps in comparison of the actual performance with the

budgeted performance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity 02

Apply a range of management accounting techniques and

produce appropriate financial reporting documents

Cost is the expenditure in monetary cost of purchasing various factors of production. The costs

can be classified based on the nature, based on the control and based on the they are as follows;

The costs which can be classified Based on the nature are as follows;

1. Fixed cost: This is the cost which does not change with the level of production.

2. Variable cost: This is the cost which changes with every level of production.

3. Overhead cost: This is a cost which is incurred for another expense of production.

4. marginal cost: This is a cost which is incurred by using one unit of production.

5. material cost: This is a cost which is incurred for the purchase of raw materials.

6. labor cost: This is the amount paid to the workers.

The costs which can be classified based on the basis of control

1. controllable costs

2. uncontrollable costs

The costs which can be classified based on the relevance to decision making

1. opportunity costs

2. real costs

3. sunk costs

4. imputed costs

5. conversion costs

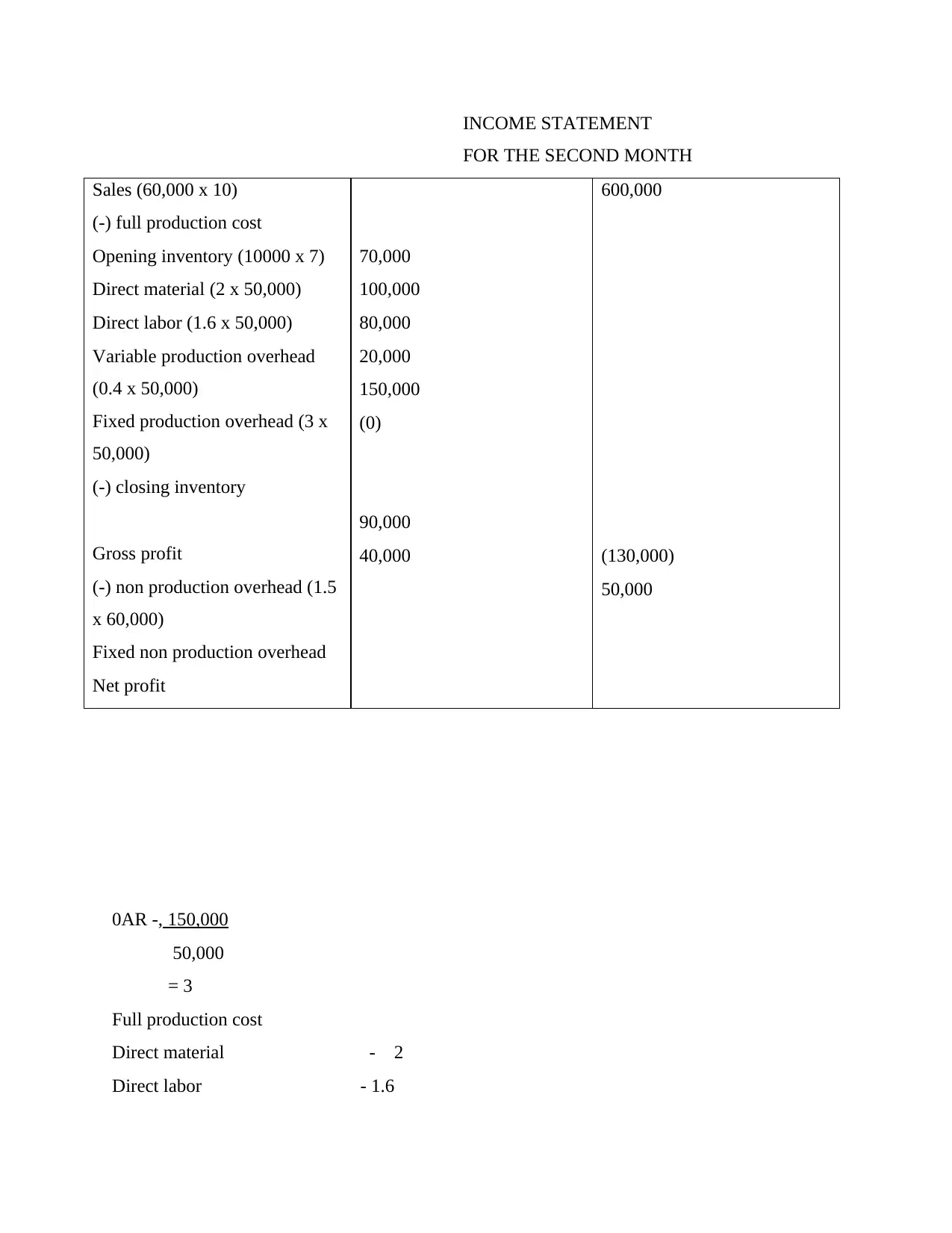

calculate the costs using appropriate techniques of cost

analysis to prepare an income statement using marginal

and absorption costs

PENQUINS SPORTS WEAR LIMITED

Apply a range of management accounting techniques and

produce appropriate financial reporting documents

Cost is the expenditure in monetary cost of purchasing various factors of production. The costs

can be classified based on the nature, based on the control and based on the they are as follows;

The costs which can be classified Based on the nature are as follows;

1. Fixed cost: This is the cost which does not change with the level of production.

2. Variable cost: This is the cost which changes with every level of production.

3. Overhead cost: This is a cost which is incurred for another expense of production.

4. marginal cost: This is a cost which is incurred by using one unit of production.

5. material cost: This is a cost which is incurred for the purchase of raw materials.

6. labor cost: This is the amount paid to the workers.

The costs which can be classified based on the basis of control

1. controllable costs

2. uncontrollable costs

The costs which can be classified based on the relevance to decision making

1. opportunity costs

2. real costs

3. sunk costs

4. imputed costs

5. conversion costs

calculate the costs using appropriate techniques of cost

analysis to prepare an income statement using marginal

and absorption costs

PENQUINS SPORTS WEAR LIMITED

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INCOME STATEMENT

FOR THE SECOND MONTH

Sales (60,000 x 10)

(-) full production cost

Opening inventory (10000 x 7)

Direct material (2 x 50,000)

Direct labor (1.6 x 50,000)

Variable production overhead

(0.4 x 50,000)

Fixed production overhead (3 x

50,000)

(-) closing inventory

Gross profit

(-) non production overhead (1.5

x 60,000)

Fixed non production overhead

Net profit

70,000

100,000

80,000

20,000

150,000

(0)

90,000

40,000

600,000

(130,000)

50,000

0AR -, 150,000

50,000

= 3

Full production cost

Direct material - 2

Direct labor - 1.6

FOR THE SECOND MONTH

Sales (60,000 x 10)

(-) full production cost

Opening inventory (10000 x 7)

Direct material (2 x 50,000)

Direct labor (1.6 x 50,000)

Variable production overhead

(0.4 x 50,000)

Fixed production overhead (3 x

50,000)

(-) closing inventory

Gross profit

(-) non production overhead (1.5

x 60,000)

Fixed non production overhead

Net profit

70,000

100,000

80,000

20,000

150,000

(0)

90,000

40,000

600,000

(130,000)

50,000

0AR -, 150,000

50,000

= 3

Full production cost

Direct material - 2

Direct labor - 1.6

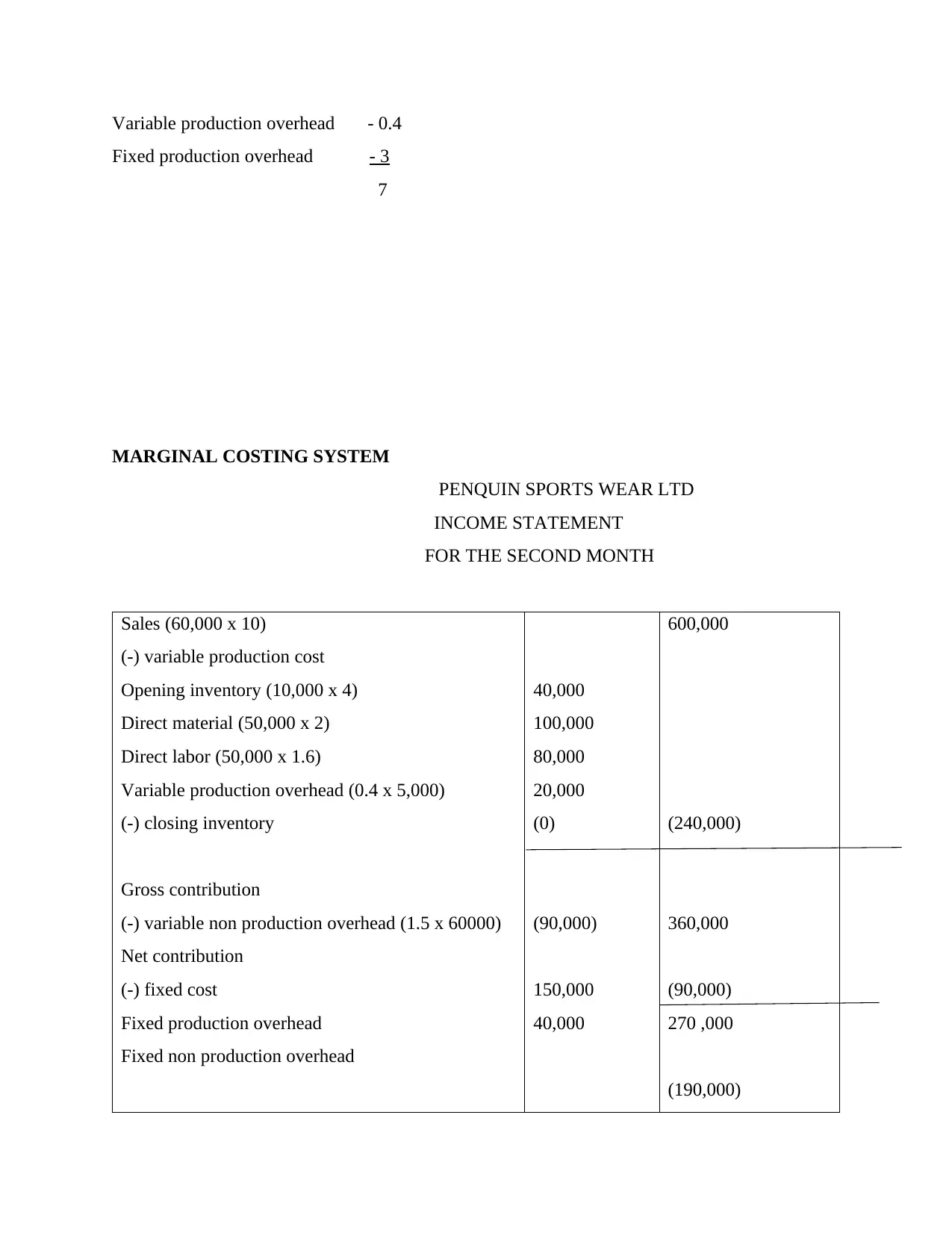

Variable production overhead - 0.4

Fixed production overhead - 3

7

MARGINAL COSTING SYSTEM

PENQUIN SPORTS WEAR LTD

INCOME STATEMENT

FOR THE SECOND MONTH

Sales (60,000 x 10)

(-) variable production cost

Opening inventory (10,000 x 4)

Direct material (50,000 x 2)

Direct labor (50,000 x 1.6)

Variable production overhead (0.4 x 5,000)

(-) closing inventory

Gross contribution

(-) variable non production overhead (1.5 x 60000)

Net contribution

(-) fixed cost

Fixed production overhead

Fixed non production overhead

40,000

100,000

80,000

20,000

(0)

(90,000)

150,000

40,000

600,000

(240,000)

360,000

(90,000)

270 ,000

(190,000)

Fixed production overhead - 3

7

MARGINAL COSTING SYSTEM

PENQUIN SPORTS WEAR LTD

INCOME STATEMENT

FOR THE SECOND MONTH

Sales (60,000 x 10)

(-) variable production cost

Opening inventory (10,000 x 4)

Direct material (50,000 x 2)

Direct labor (50,000 x 1.6)

Variable production overhead (0.4 x 5,000)

(-) closing inventory

Gross contribution

(-) variable non production overhead (1.5 x 60000)

Net contribution

(-) fixed cost

Fixed production overhead

Fixed non production overhead

40,000

100,000

80,000

20,000

(0)

(90,000)

150,000

40,000

600,000

(240,000)

360,000

(90,000)

270 ,000

(190,000)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.