Analysis of a Pension Plan's Bond Portfolio Structure and Strategy

VerifiedAdded on 2023/01/13

|11

|2408

|50

Report

AI Summary

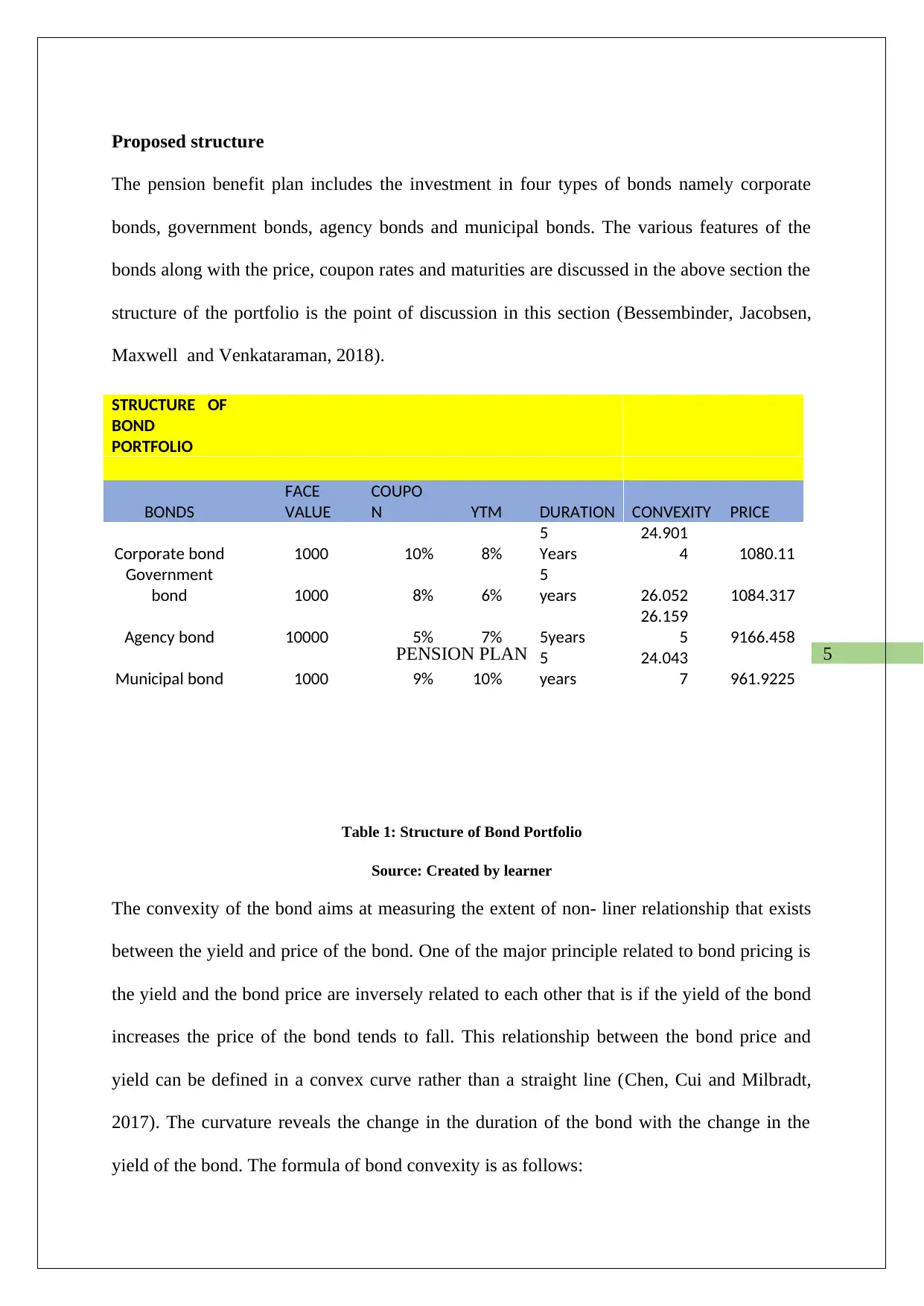

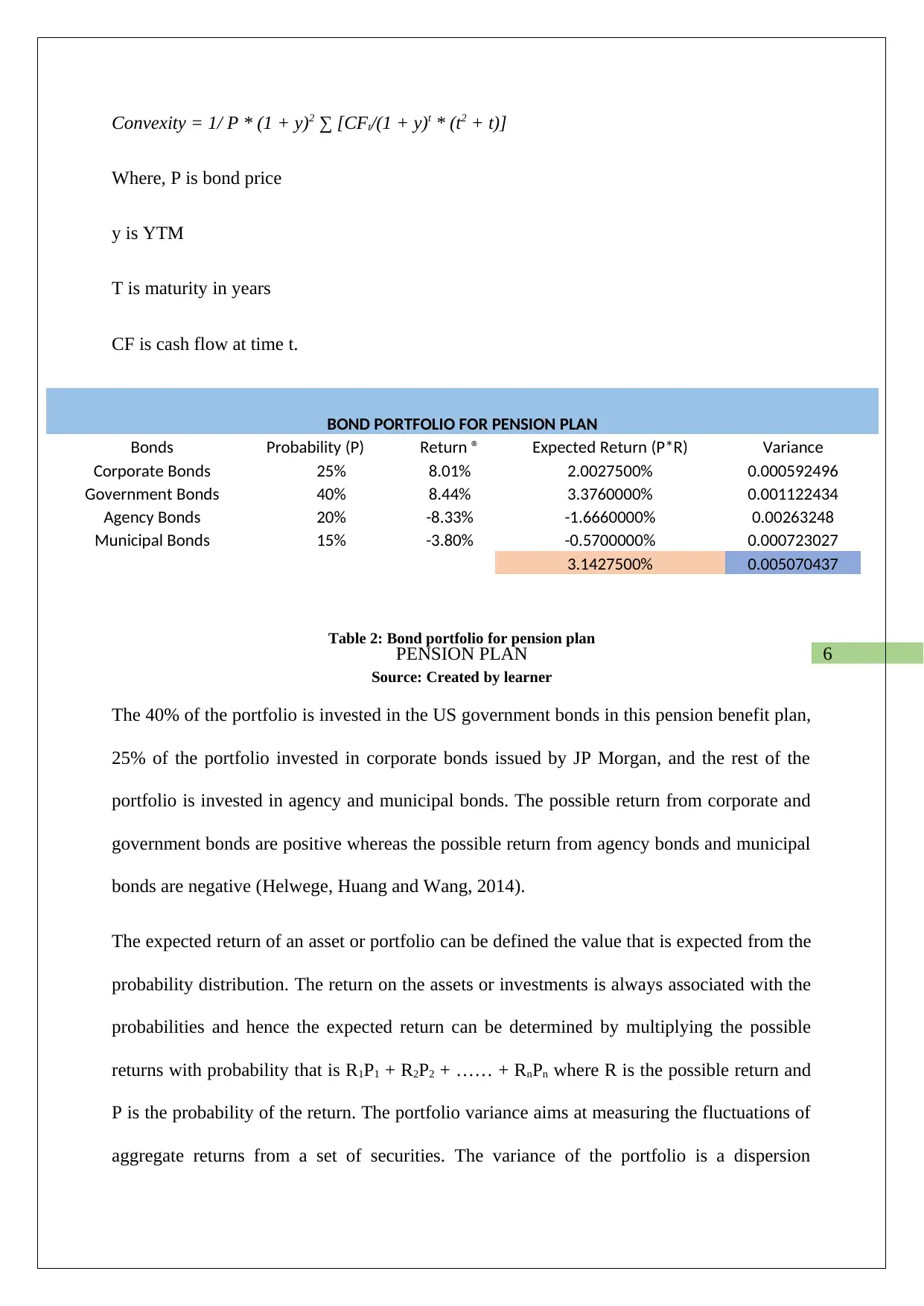

This report presents a comprehensive analysis of a pension plan's bond portfolio. It begins with an introduction to bonds, categorizing them into government, corporate, junk, and municipal bonds. The core of the report focuses on a pension plan's investment in four types of bonds: corporate, government, agency, and municipal. Each bond type is discussed in detail, including the issuer, coupon rate, maturity, and the state of the economy and financial market conditions affecting each. The report then proposes a structure for the bond portfolio, detailing the face value, coupon, yield to maturity, duration, and convexity of each bond. A table summarizes the portfolio's structure, and a second table outlines the bond portfolio for the pension plan, including probabilities, returns, and expected returns. The report concludes with a justification for the inclusion of each bond type in the portfolio, highlighting the benefits and risks associated with each investment. The justification includes aspects such as corporate bonds providing investment opportunities and government bonds offering tax benefits. The report also discusses the importance of diversification and the correlation between different bond types, emphasizing the goal of providing stability and liquidity within the pension plan.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.