Accounting for Pension Plans: Asset, Expense, and Obligation Analysis

VerifiedAdded on 2021/11/15

|8

|1253

|26

Homework Assignment

AI Summary

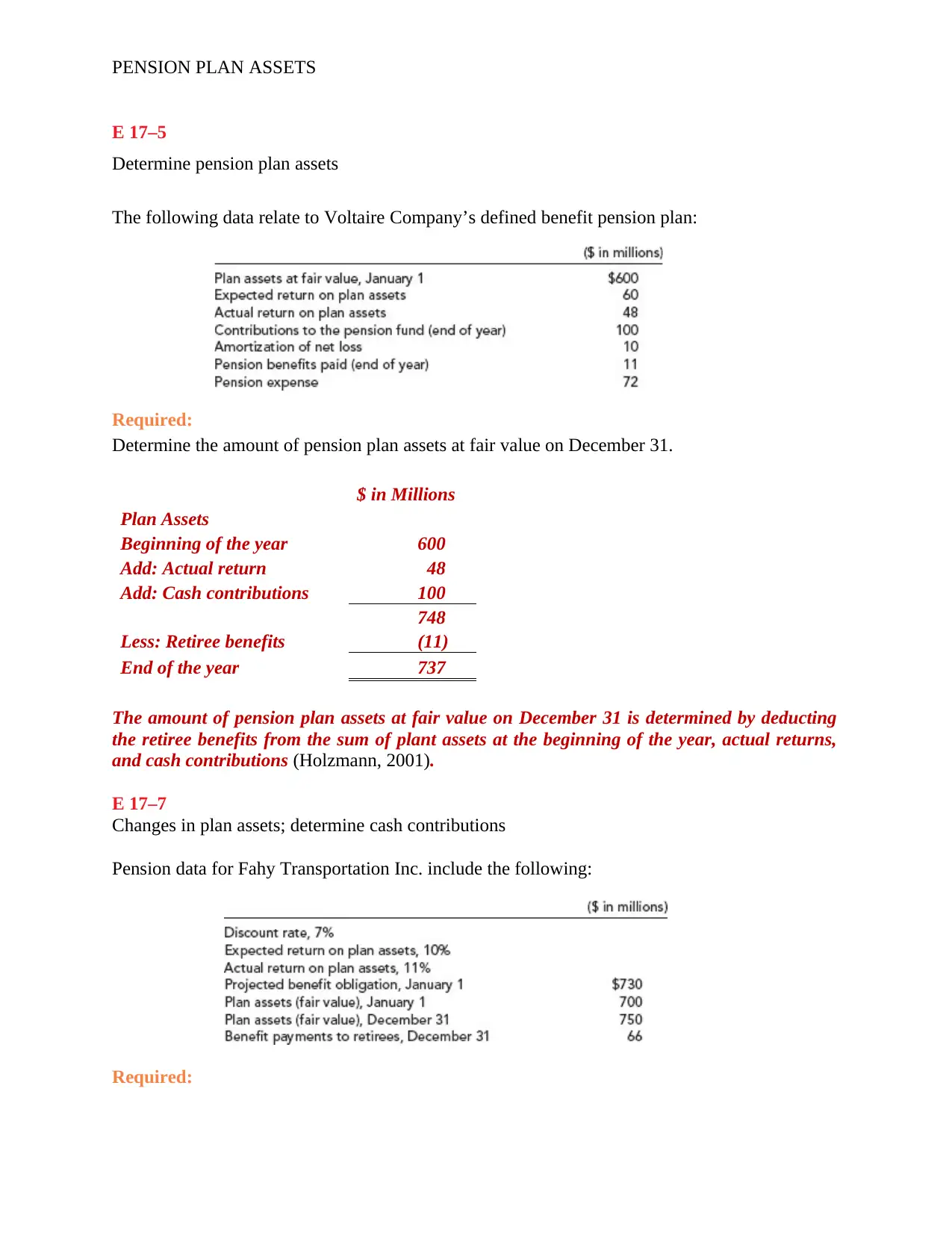

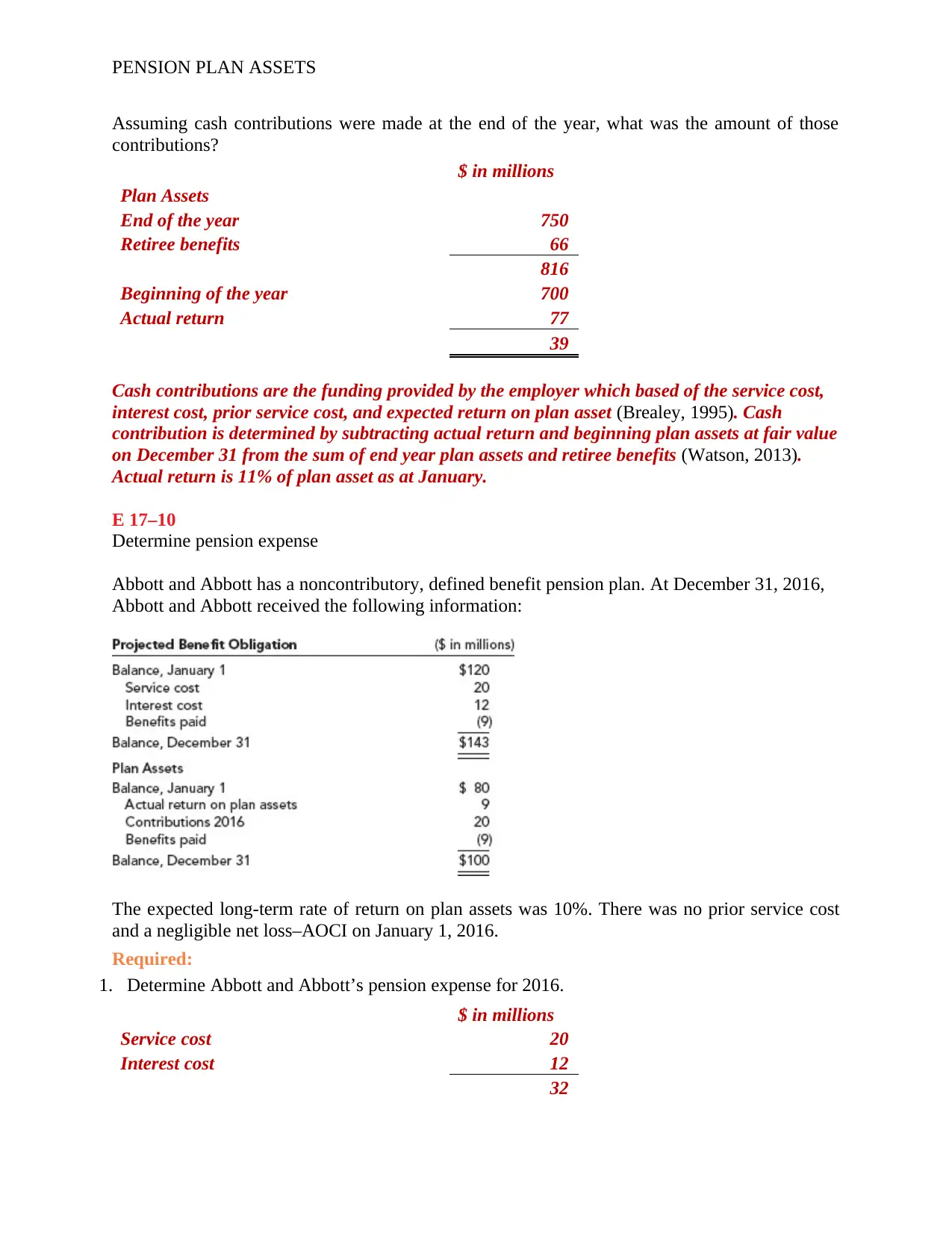

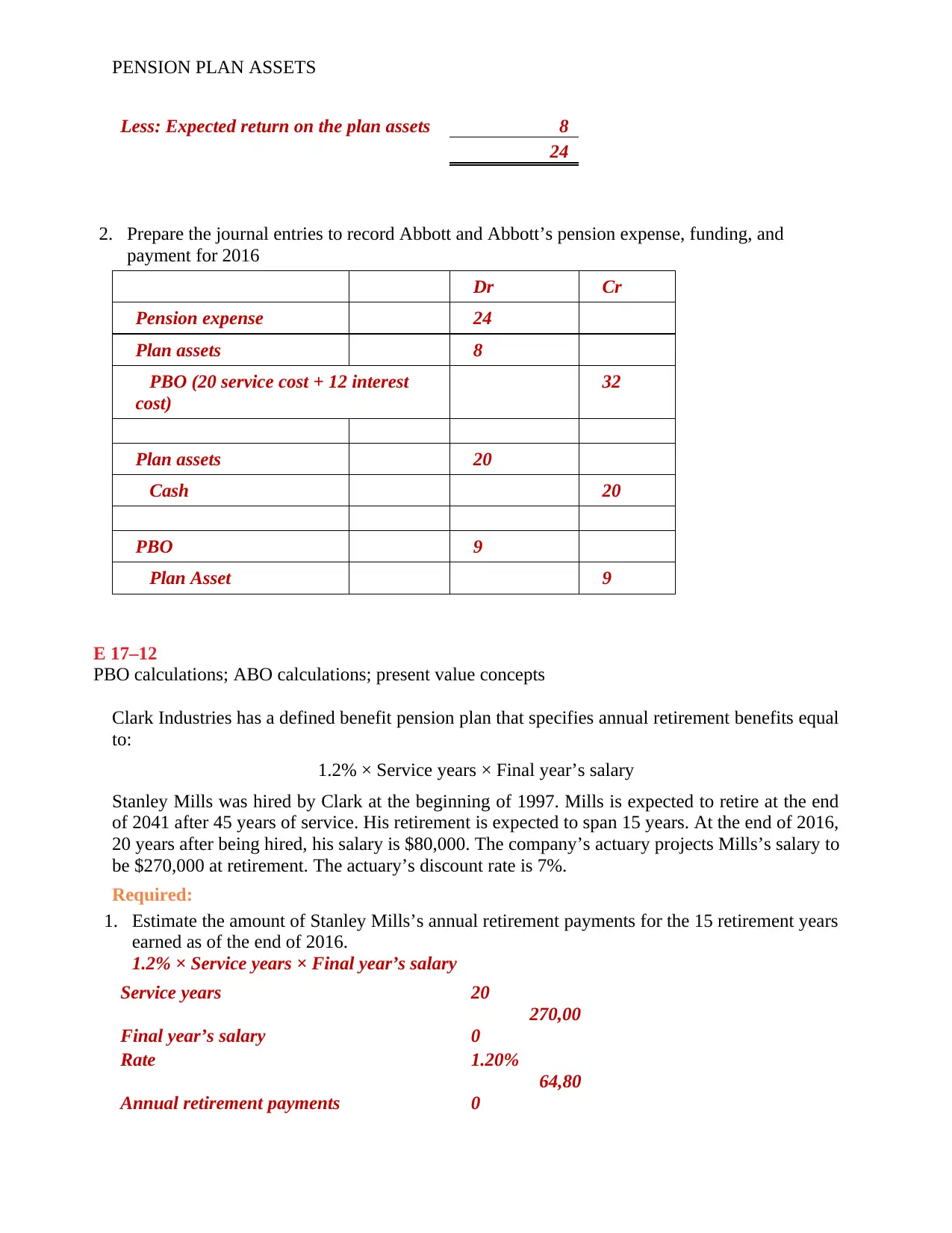

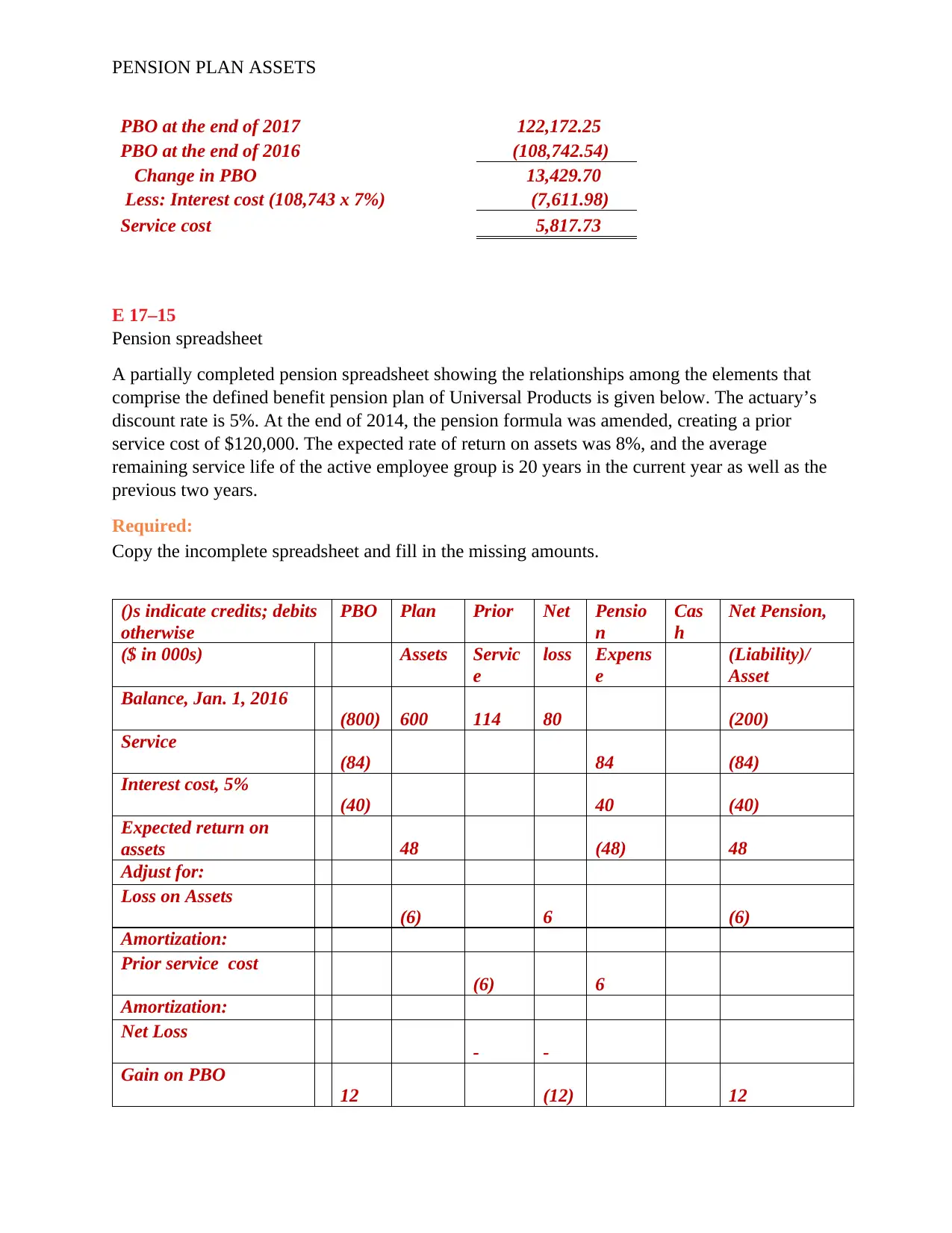

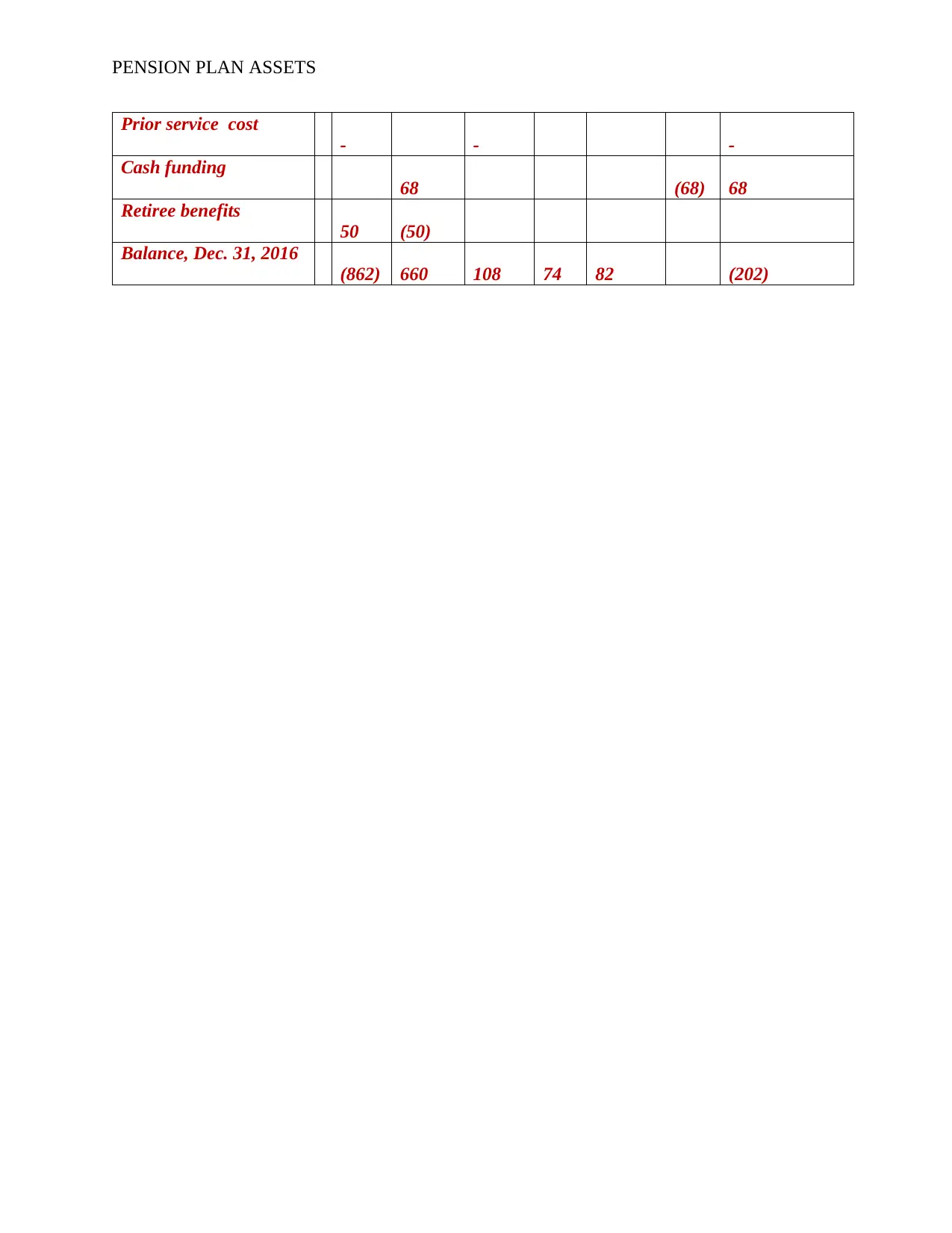

This assignment provides detailed solutions to various pension accounting problems. It begins with determining pension plan assets at fair value, calculating cash contributions, and determining pension expense. The assignment further delves into Projected Benefit Obligation (PBO) and Accumulated Benefit Obligation (ABO) calculations, including estimating annual retirement payments and present values. It includes a spreadsheet analysis demonstrating the relationships among the elements of a defined benefit pension plan, such as service cost, interest cost, and the expected return on assets. The solutions are based on the provided data and relevant accounting principles, with references to established financial accounting resources and concepts.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.