A Comprehensive Guide to Performance Attribution Analysis in Finance

VerifiedAdded on 2022/07/11

|12

|1751

|78

Report

AI Summary

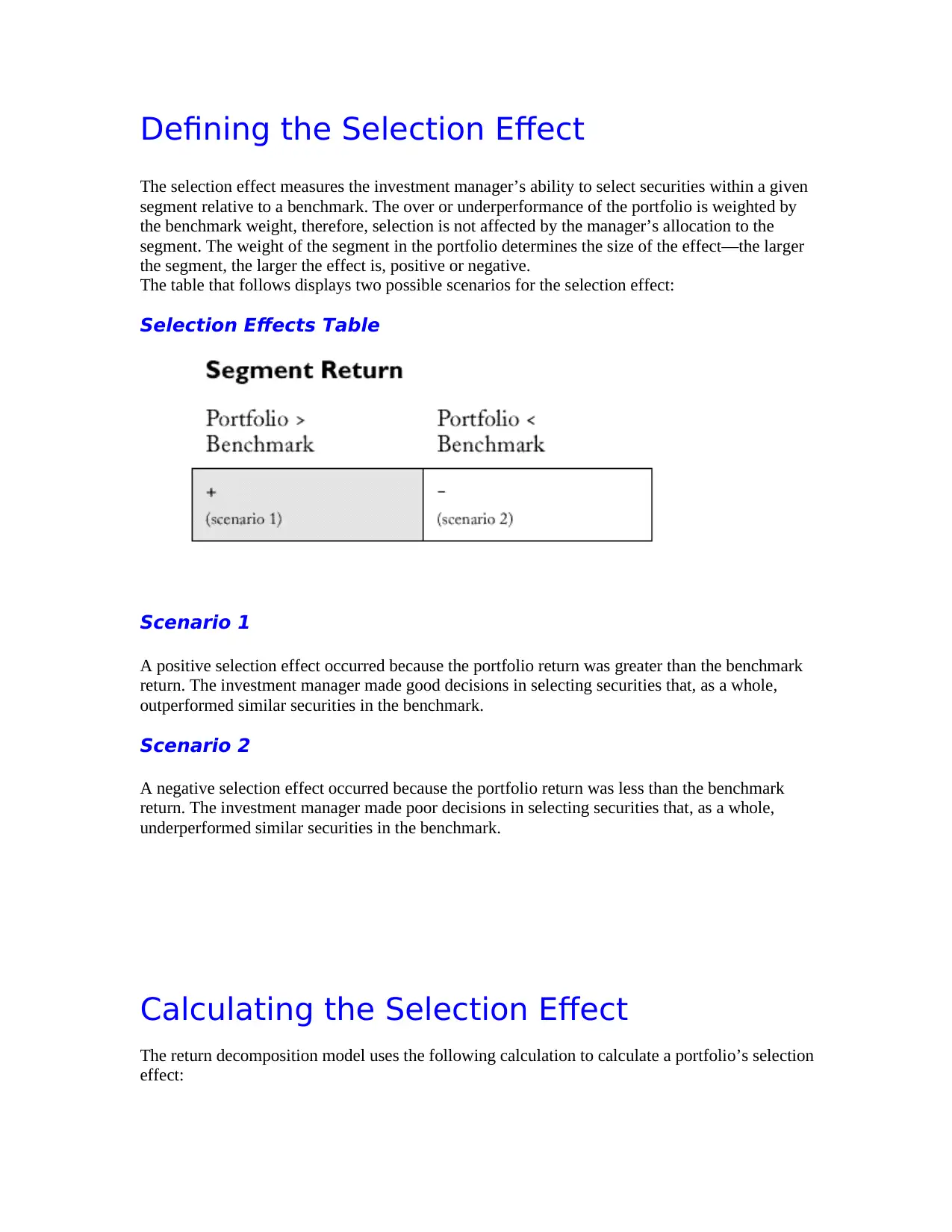

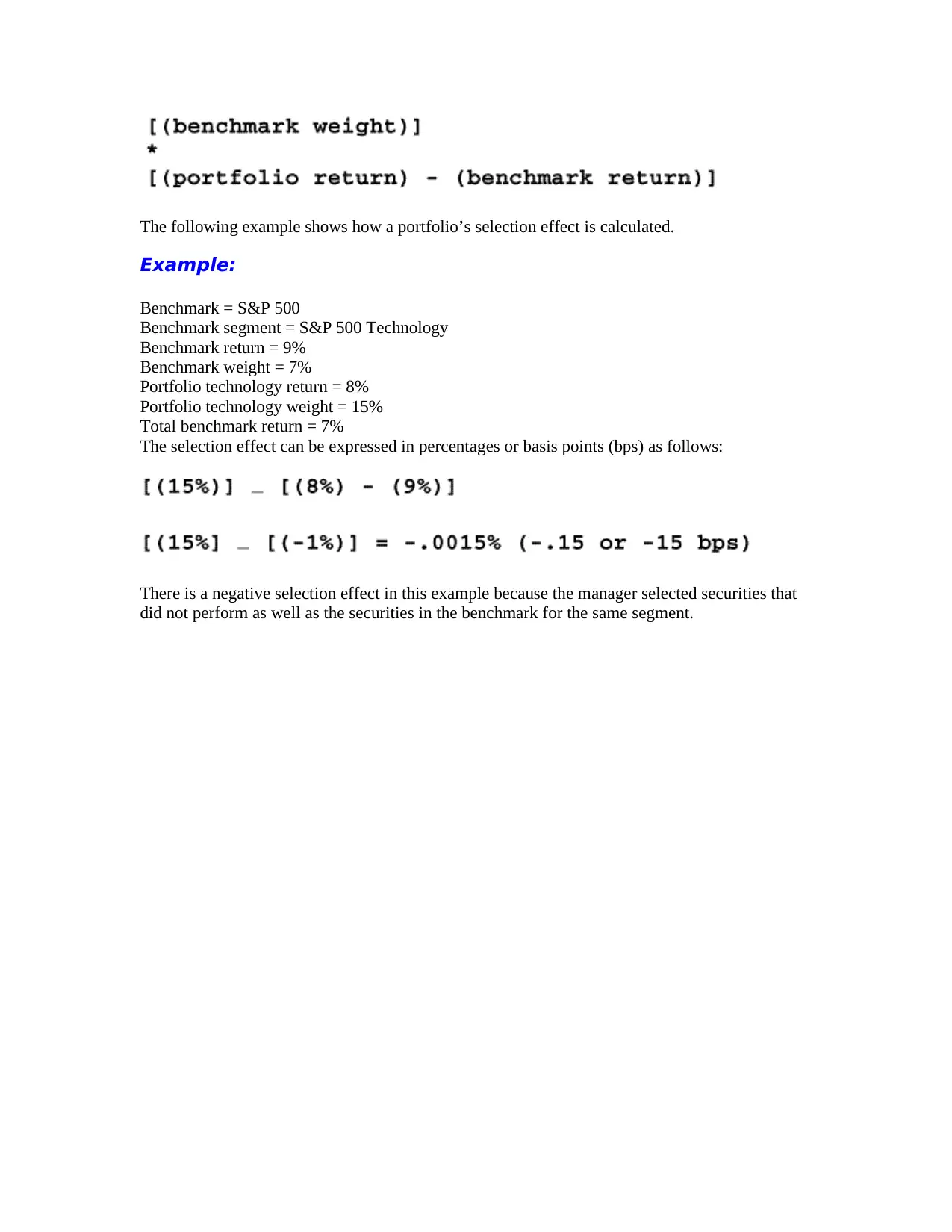

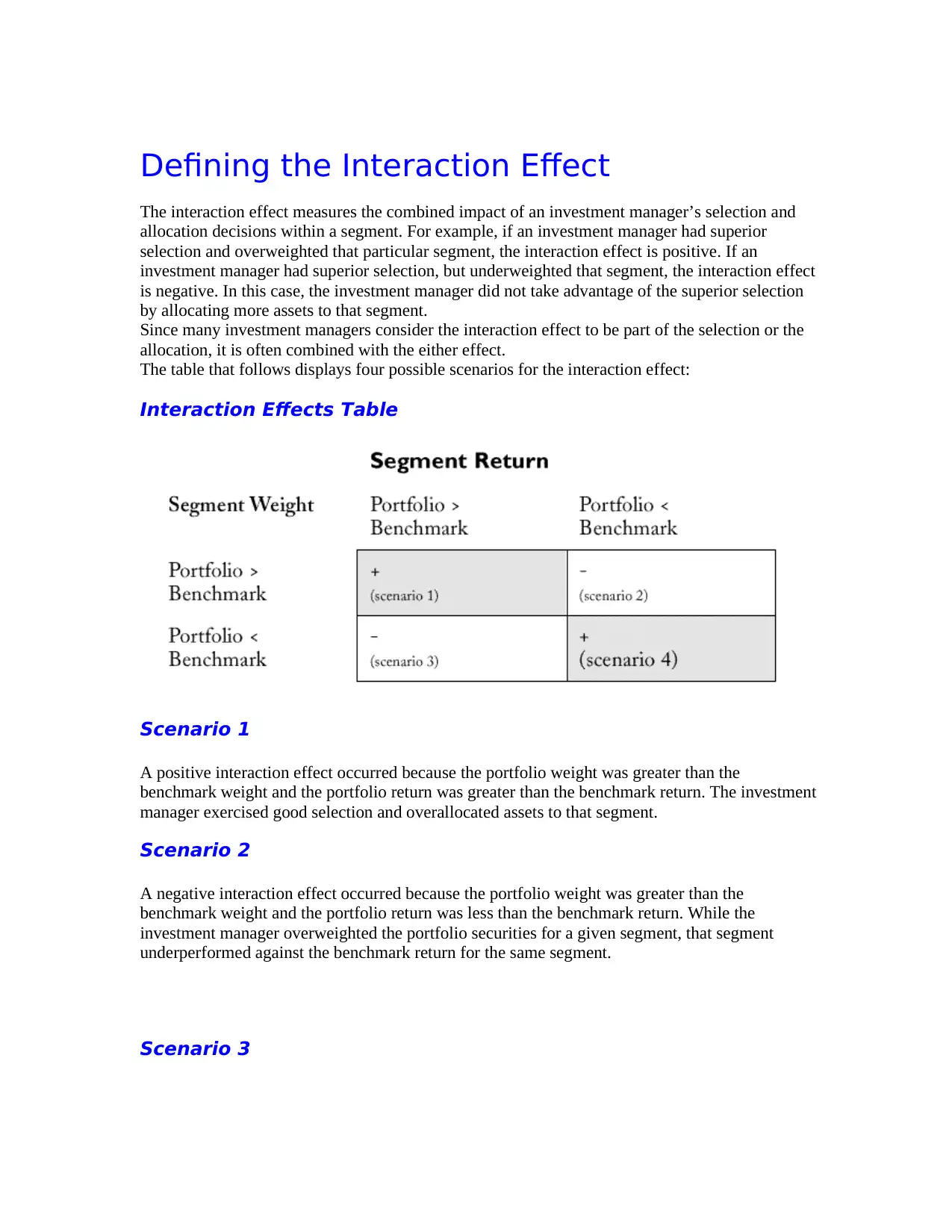

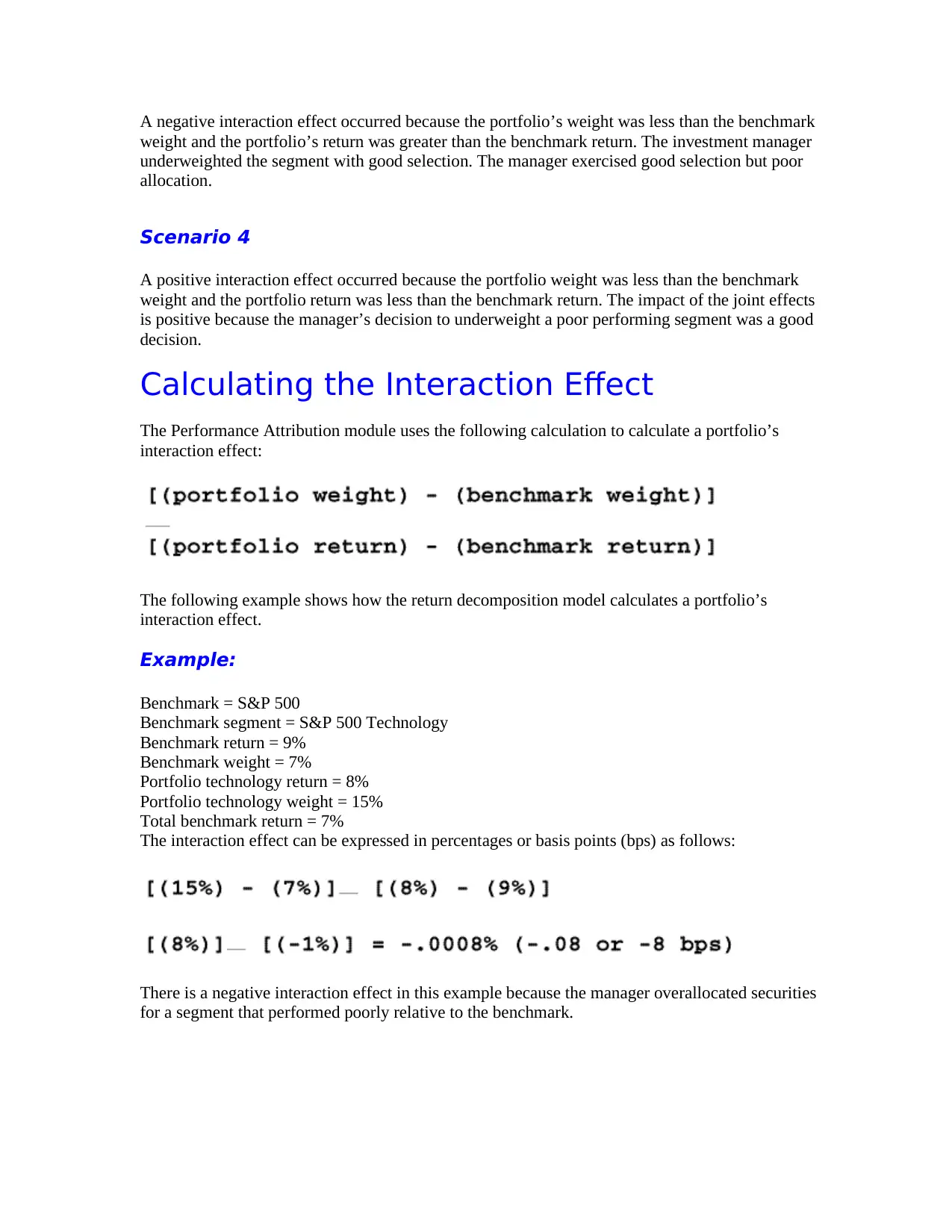

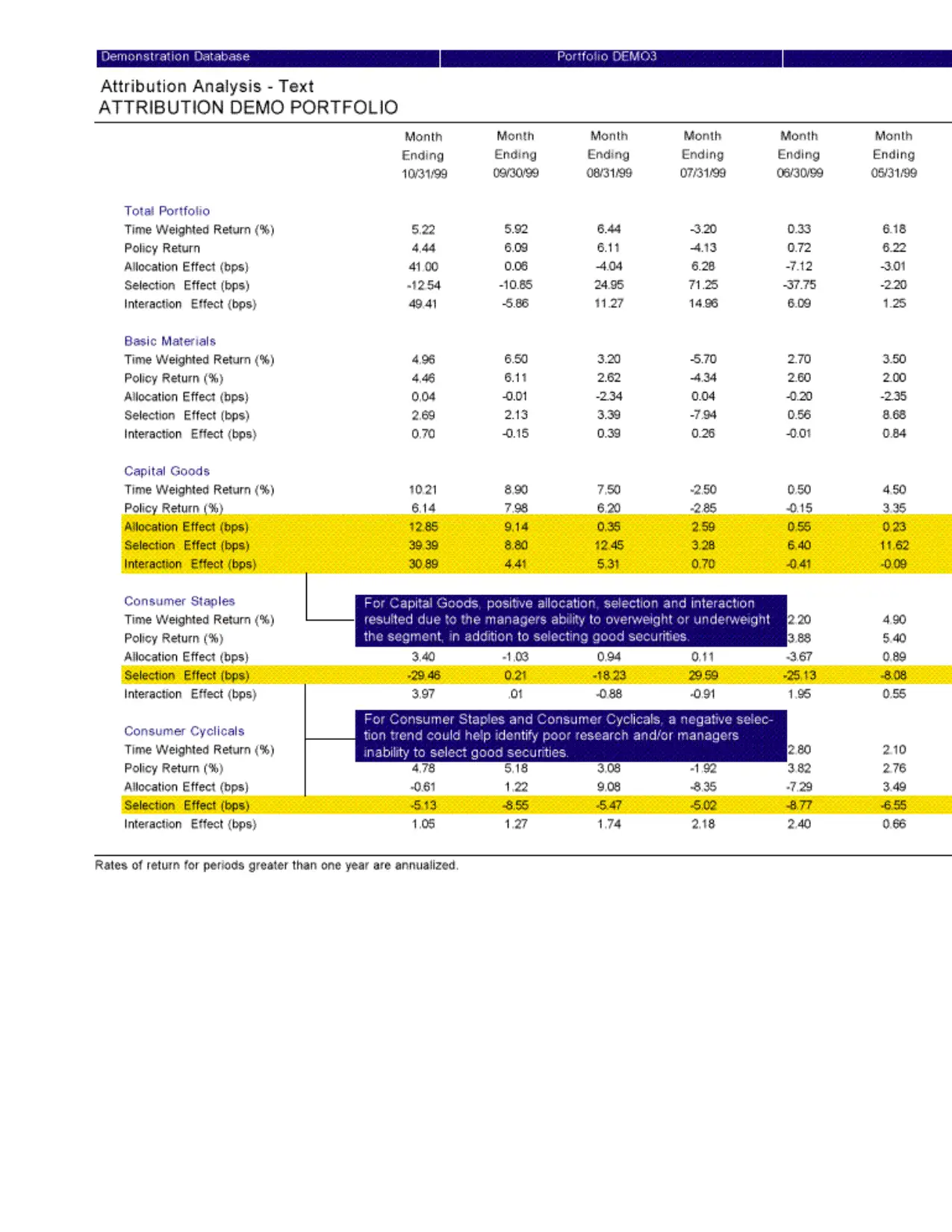

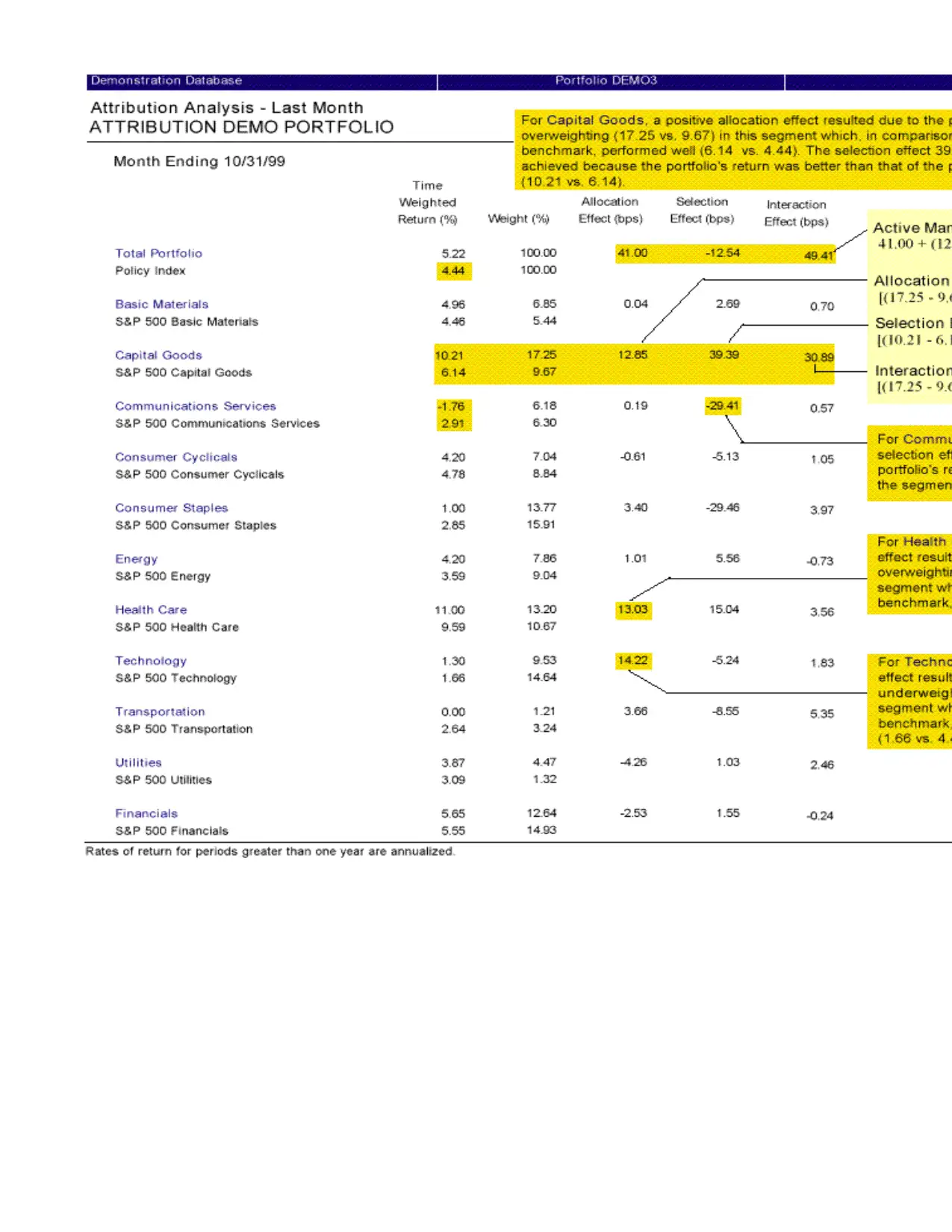

This report provides a comprehensive overview of performance attribution analysis, a crucial method for evaluating investment performance. It delves into the core concepts, including the active management effect and its components: allocation, selection, and interaction effects. The report explains how to calculate each effect using return decomposition analysis, the most widely accepted method in the investment community. The allocation effect assesses an investment manager's ability to effectively distribute assets across different segments, while the selection effect measures the manager's ability to choose successful securities within those segments. The interaction effect combines the impact of both allocation and selection decisions. The report includes scenarios and examples to illustrate how each effect contributes to overall portfolio returns, providing a practical guide for understanding and applying performance attribution in financial analysis. The report also clarifies how to determine if an investment manager has contributed positively to a portfolio’s return. Desklib offers this and other resources to help students excel in their studies.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.