La Trobe Business School ACC3MAC Assignment 1: Budgeting Project

VerifiedAdded on 2023/01/18

|18

|2317

|72

Project

AI Summary

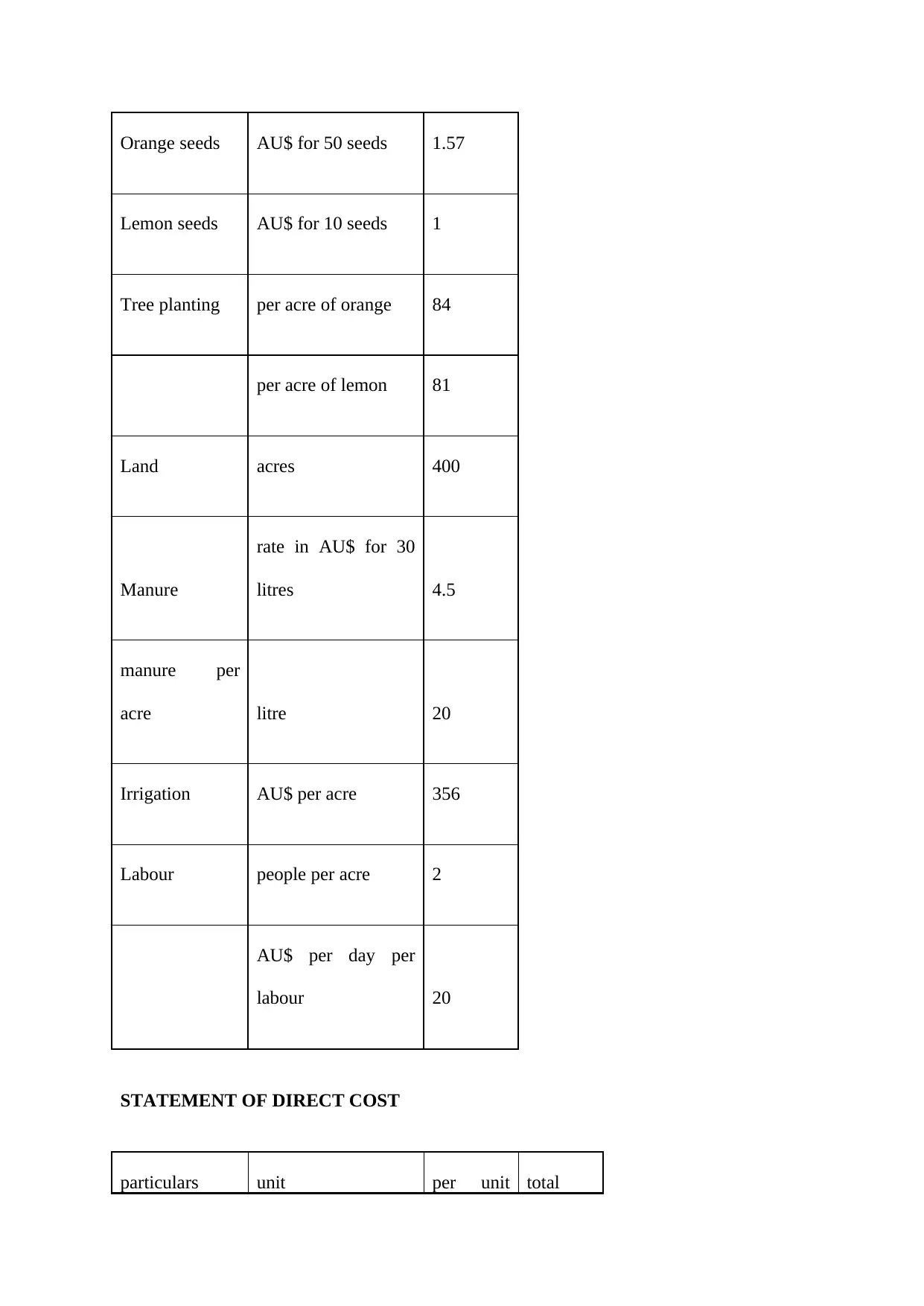

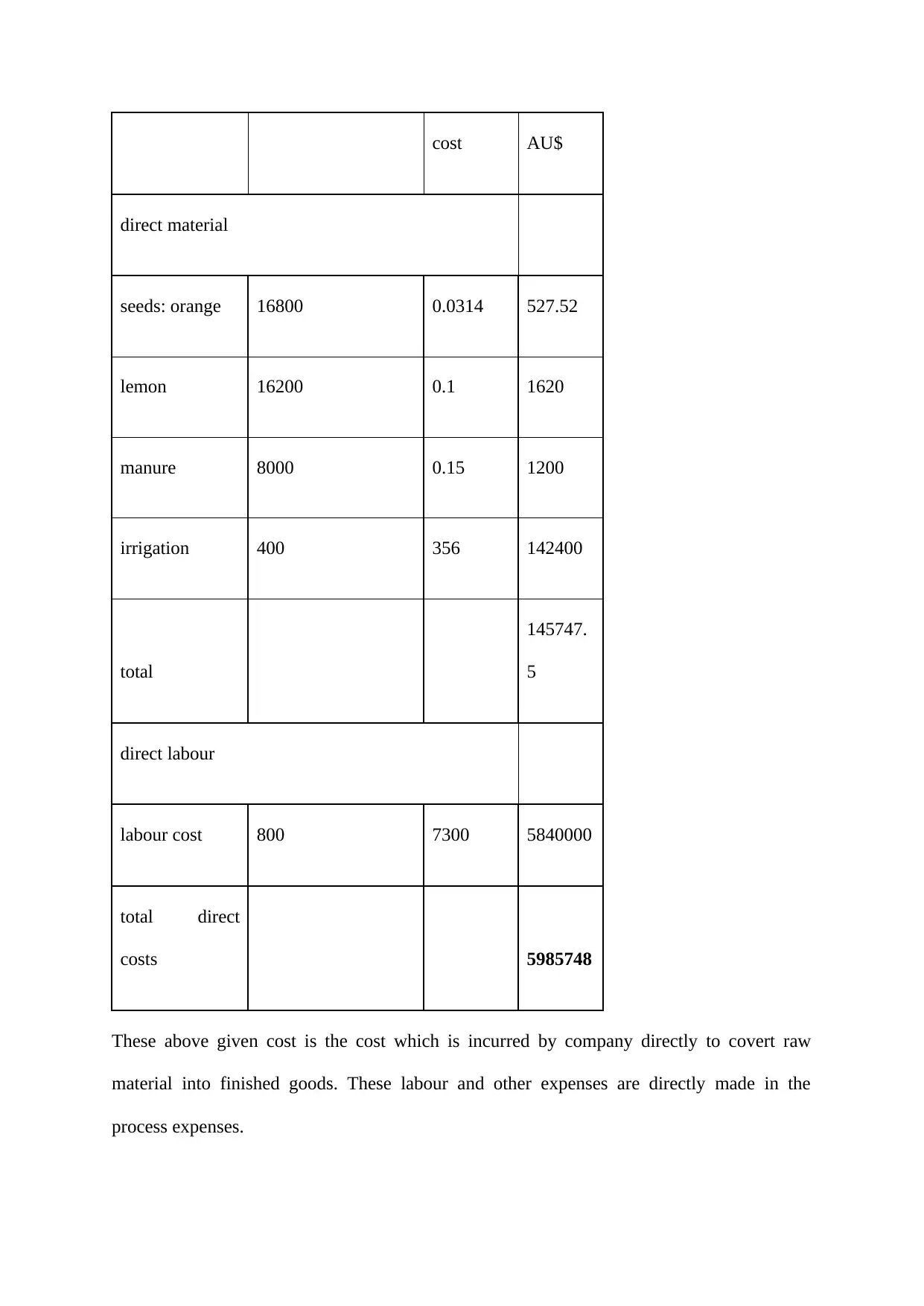

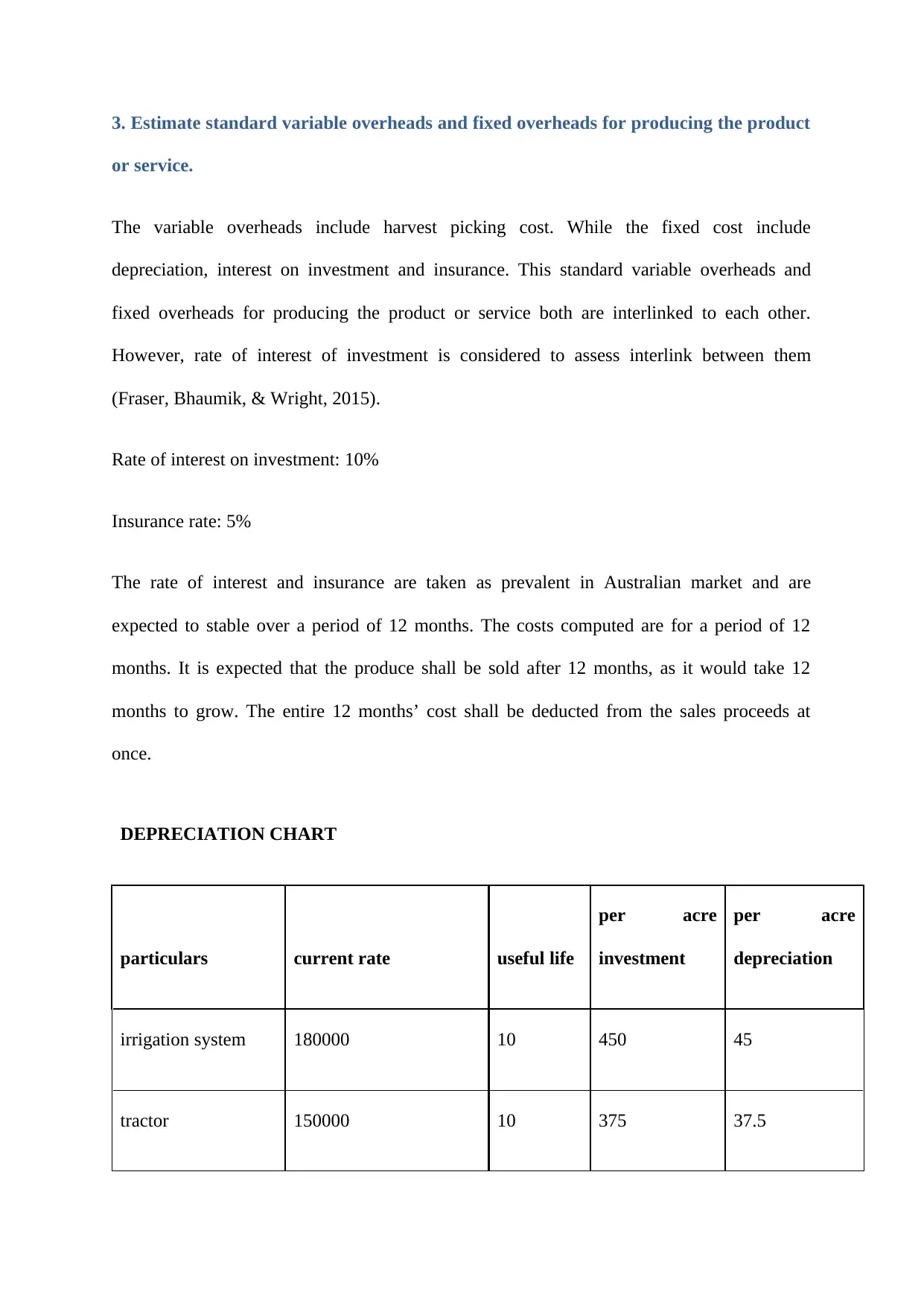

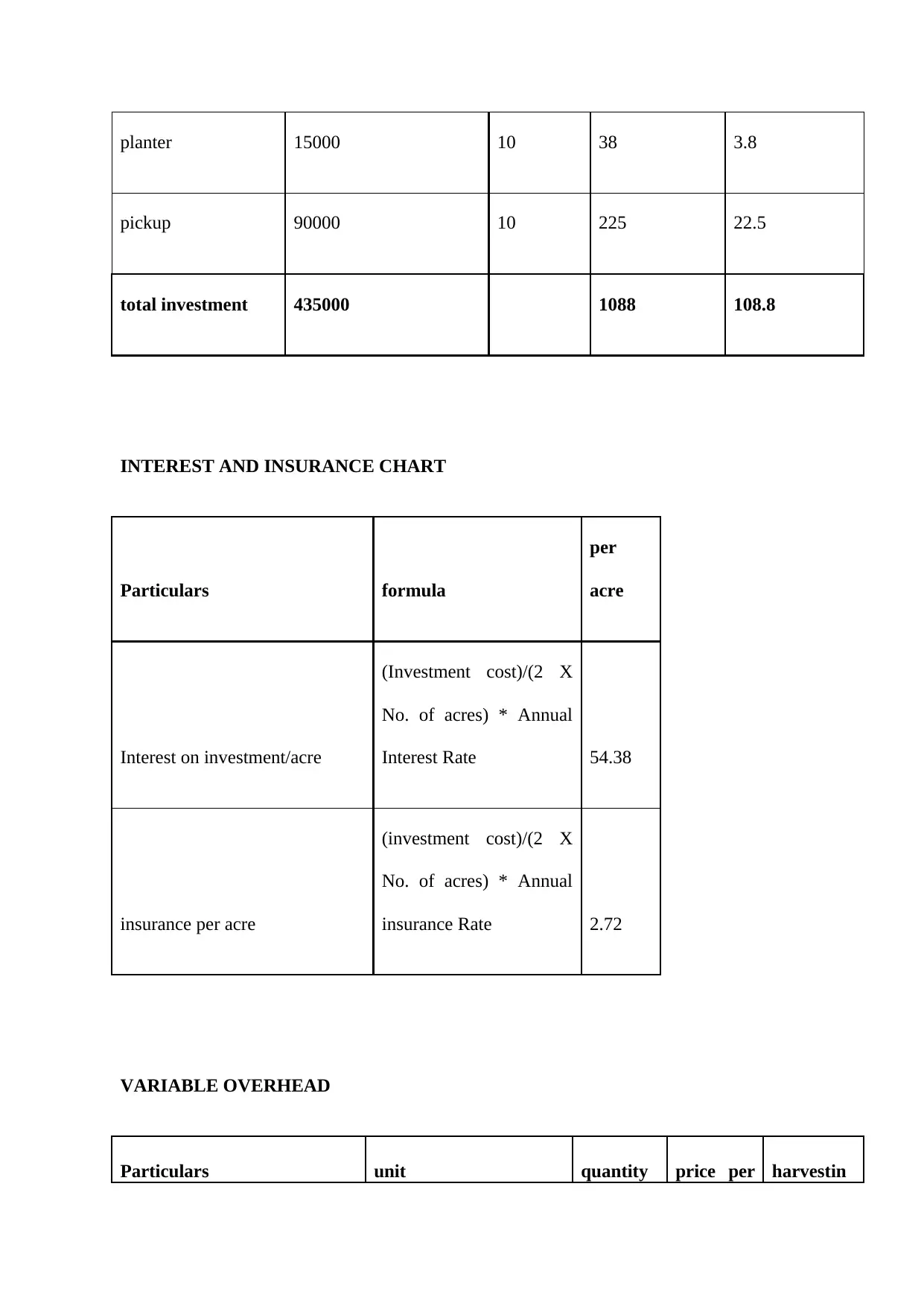

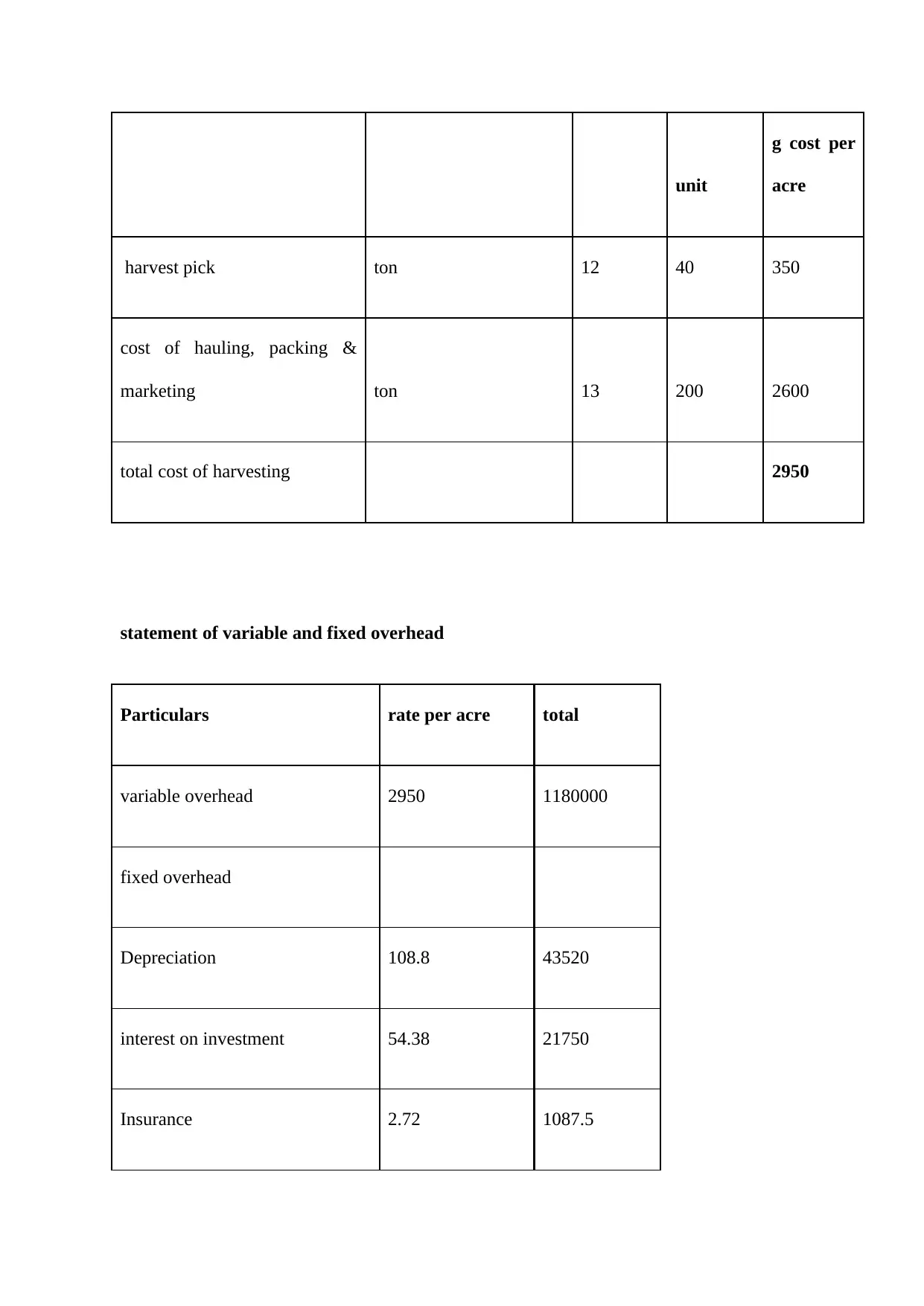

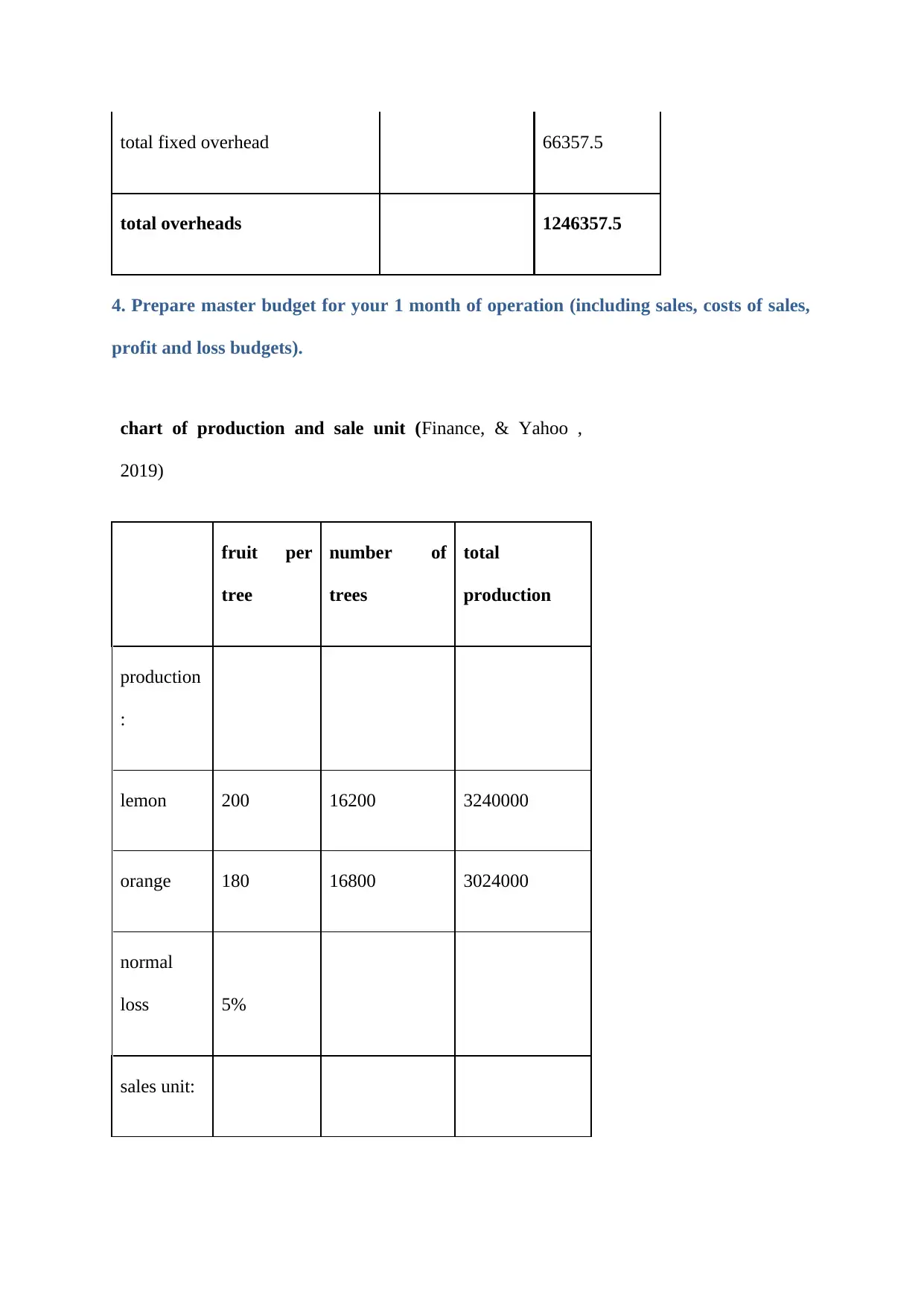

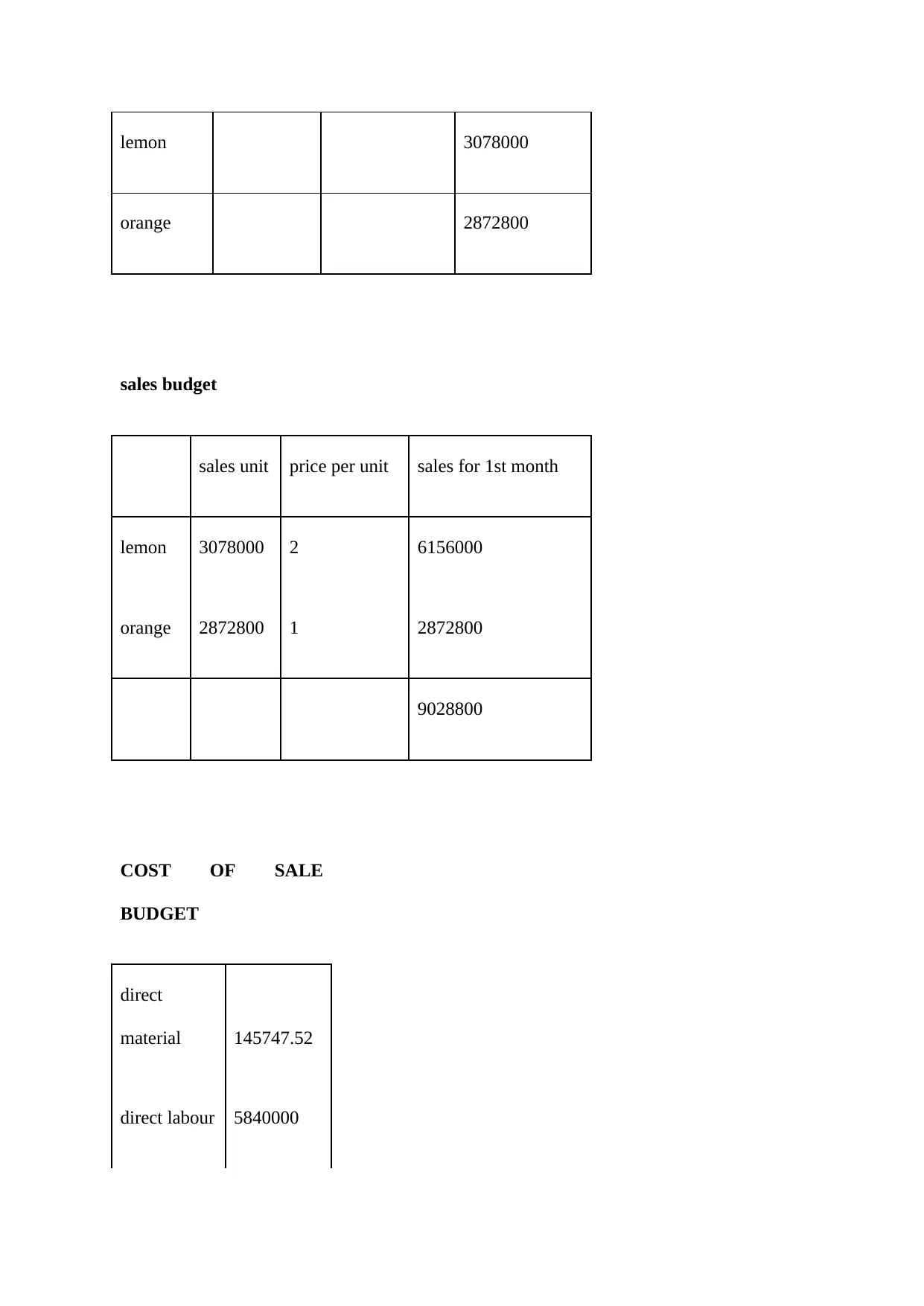

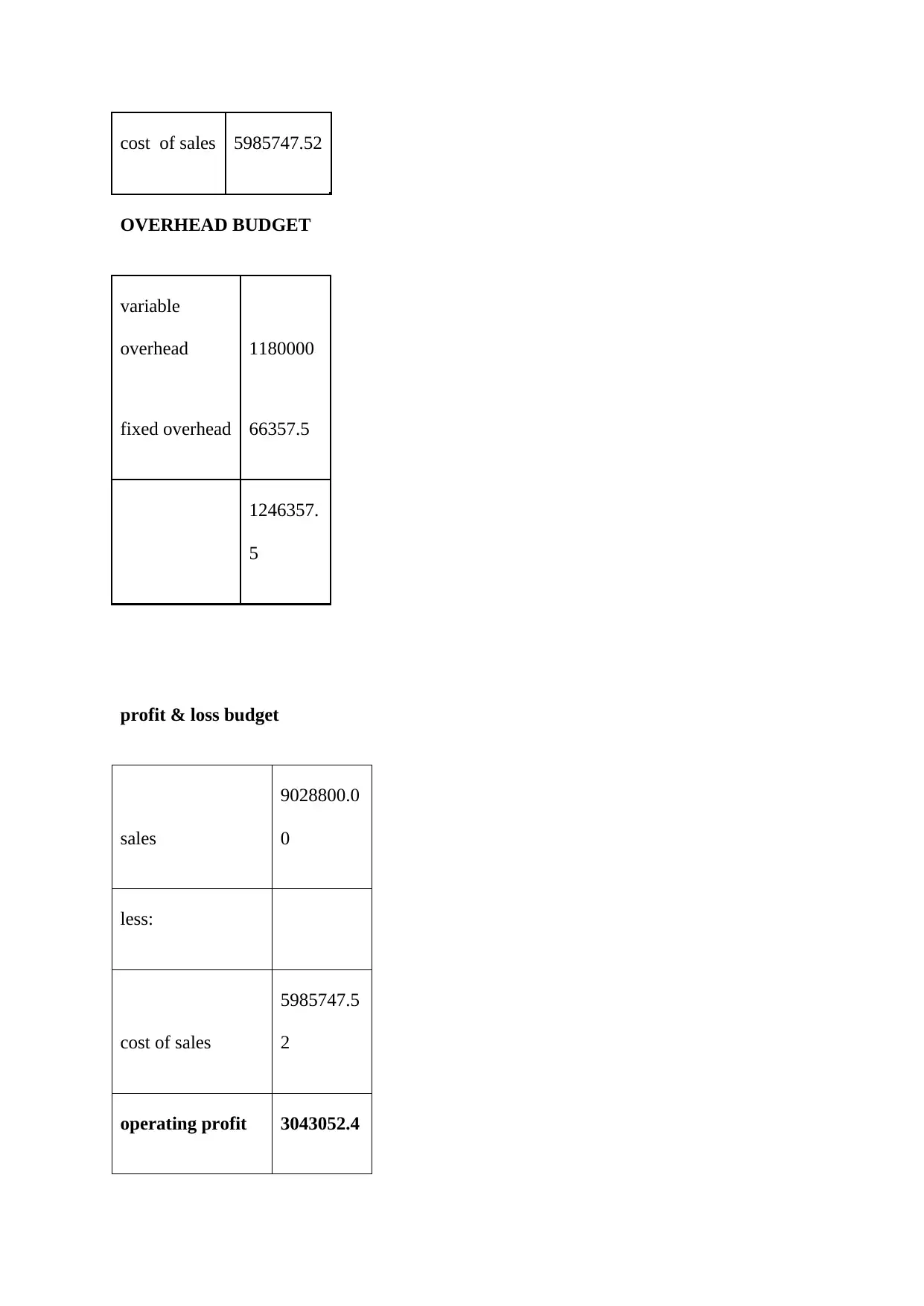

This project focuses on creating a comprehensive budgeting plan for an organic farm producing citrus fruits. The student begins by outlining the vision, purpose, and goals of the business, emphasizing the demand for healthy produce and sustainable agricultural practices. The project then delves into estimating direct material and labor costs, detailing seed, irrigation, manure, and labor expenses for orange and lemon production. Standard variable and fixed overhead costs, including harvesting, depreciation, interest, and insurance, are also calculated. A master budget is prepared, encompassing sales, cost of sales, and profit and loss budgets for the first month of operation. The student reflects on the knowledge and skills gained, highlighting the practical approach to market analysis, cost understanding, and real-time production planning. The assignment demonstrates the application of budgeting principles to assess the costing of a new product and control potential expenses.

1 out of 18

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.