HRM5002D - Case Study: Performance Improvement & Management

VerifiedAdded on 2022/12/01

|15

|3938

|54

Case Study

AI Summary

This case study analyzes performance improvement and management within the health and social care sector, addressing key aspects such as strategic planning models, financial performance measures, and non-financial indicators. Task 1 explores strategic planning models like the Balanced Scorecard and budgeting, evaluating their benefits and drawbacks. Task 2 delves into financial performance analysis, including DuPont analysis and ratio analysis, to assess profitability, liquidity, and efficiency. Task 3 examines non-financial measures and performance appraisal frameworks. The study evaluates the application of these tools in a real-world context, highlighting their importance for organizational effectiveness and improvement in health and social care settings.

Performance Improvement and Management in

Health & Social Care

Health & Social Care

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Task 1...............................................................................................................................................3

Task 2...............................................................................................................................................7

Task 3.............................................................................................................................................10

Task 1...............................................................................................................................................3

Task 2...............................................................................................................................................7

Task 3.............................................................................................................................................10

Task 1

Strategic planning models

1. Balance Scorecard

Organizations use balanced scorecard to link higher perspectives to more detailed points.

Managers can understand how the organization works by showing how daily workouts relate to

hierarchical goals. By analyzing past temporal dimensions such as transactions and creative

ideas, points on the scorecard lead to economic and non-financial terms. The pros and cons of a

fair scorecard depend on how the organization operates its governance structure.

Balanced scorecard views business from four perspectives. The organization sets goals and

emphasizes each point of view. At this point, they strive to achieve these goals by moving and

evaluating progress towards key performance indicators.

Finance: A company usually distributes the company's activities such as transactions, benefits,

and profits. Depending on the organization's goals, the most important thing can be remembered

as the organization's fair indicator system. For example, assuming front-line development is

needed, the scorecard may include monthly offers.

Customers: Viewing company’s organization from a customer perspective can help company’s

company retain customers. This is important because retaining existing customers is cheaper

than acquiring new customers. Evaluating factors such as customer service requirements and

customer satisfaction can help company’s organization retain customers.

Internal Process: Measuring how well company’s organization creates, sells, and manages

products can help company make a profit because productivity determines productivity.

Reference cards help organizations determine where and how far they have implemented the

framework and cycle.

Authoritative Potential: The right scorecard helps organizations determine if they have the right

people, legitimate innovations, and the right culture to achieve their goals.

Benefits

Strategic planning models

1. Balance Scorecard

Organizations use balanced scorecard to link higher perspectives to more detailed points.

Managers can understand how the organization works by showing how daily workouts relate to

hierarchical goals. By analyzing past temporal dimensions such as transactions and creative

ideas, points on the scorecard lead to economic and non-financial terms. The pros and cons of a

fair scorecard depend on how the organization operates its governance structure.

Balanced scorecard views business from four perspectives. The organization sets goals and

emphasizes each point of view. At this point, they strive to achieve these goals by moving and

evaluating progress towards key performance indicators.

Finance: A company usually distributes the company's activities such as transactions, benefits,

and profits. Depending on the organization's goals, the most important thing can be remembered

as the organization's fair indicator system. For example, assuming front-line development is

needed, the scorecard may include monthly offers.

Customers: Viewing company’s organization from a customer perspective can help company’s

company retain customers. This is important because retaining existing customers is cheaper

than acquiring new customers. Evaluating factors such as customer service requirements and

customer satisfaction can help company’s organization retain customers.

Internal Process: Measuring how well company’s organization creates, sells, and manages

products can help company make a profit because productivity determines productivity.

Reference cards help organizations determine where and how far they have implemented the

framework and cycle.

Authoritative Potential: The right scorecard helps organizations determine if they have the right

people, legitimate innovations, and the right culture to achieve their goals.

Benefits

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The biggest advantage of using a balanced scorecard strategy is that when company look at the

four parts of company’s organization's trade show, company can actually see its operations right.

Unlike traditional methods of tracking a company's financial resilience, an appropriate scorecard

provides a complete picture of whether an organization is meeting its goals. Even though the

organization appears financially viable, customer loyalty is diminished, employees may not be

ready, or bikes may be exhausted.

Second, it is not evaluated in the short term using the appropriate control card. When an

accountant sees a major problem in the field of finance (an organization may not go so well), he

often gets a quick idea, but there is no reason to look at the long box. When using a modified

scorecard, the partner first determines the strength of short-, medium-, and long-distance

destinations.

Finally, with a lean metrics system, company can be confident that every important activity

company’s organization performs will achieve flawless results. In the long run, can company

increase the value of company’s product to help company’s organization's maximum interest?

Perhaps if the customer is happy with the item, or if the bike involved is happy with making the

item, the result will be even more surprising.

Disadvantages

There are many benefits to using a balanced scorecard in the accounting tools branch, but there

are some problems with this strategy. First, a good scorecard requires early reflection. It's not a

device that allows company to throw ideas overnight to solve a problem. Since everything is the

same, company will be ordered to hold meetings to determine what goals company’s

organization can achieve in each of the 4 regions above. If company have a clear goal, company

can start to separate it from those that are financially necessary to achieve that goal.

Second, a balanced scorecard gives company an overview of the four areas that are important

when growing and marketing company’s business, but these four areas don't paint the whole

picture. There is a limited amount of money stored on the scorecard. While all others are equal,

in order to be effectively implemented, a fair scorecard must be important to a broad

organizational development process that includes sound accounting strategies.

four parts of company’s organization's trade show, company can actually see its operations right.

Unlike traditional methods of tracking a company's financial resilience, an appropriate scorecard

provides a complete picture of whether an organization is meeting its goals. Even though the

organization appears financially viable, customer loyalty is diminished, employees may not be

ready, or bikes may be exhausted.

Second, it is not evaluated in the short term using the appropriate control card. When an

accountant sees a major problem in the field of finance (an organization may not go so well), he

often gets a quick idea, but there is no reason to look at the long box. When using a modified

scorecard, the partner first determines the strength of short-, medium-, and long-distance

destinations.

Finally, with a lean metrics system, company can be confident that every important activity

company’s organization performs will achieve flawless results. In the long run, can company

increase the value of company’s product to help company’s organization's maximum interest?

Perhaps if the customer is happy with the item, or if the bike involved is happy with making the

item, the result will be even more surprising.

Disadvantages

There are many benefits to using a balanced scorecard in the accounting tools branch, but there

are some problems with this strategy. First, a good scorecard requires early reflection. It's not a

device that allows company to throw ideas overnight to solve a problem. Since everything is the

same, company will be ordered to hold meetings to determine what goals company’s

organization can achieve in each of the 4 regions above. If company have a clear goal, company

can start to separate it from those that are financially necessary to achieve that goal.

Second, a balanced scorecard gives company an overview of the four areas that are important

when growing and marketing company’s business, but these four areas don't paint the whole

picture. There is a limited amount of money stored on the scorecard. While all others are equal,

in order to be effectively implemented, a fair scorecard must be important to a broad

organizational development process that includes sound accounting strategies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finally, many organizations use measures that are not related to their own environment. This is

very important when using custom scorecards to ensure that the tracked information matches

company’s needs. Everything else, measurement is useless.

2. Budgeting

Budget is estimates of income and expenses over a period of time and are usually formulated and

revised from time to time. Financial plans can be created for individuals, groups, companies,

management, or almost anything that generates and sends cash.

A budget is a microeconomic idea that shows the compromises reached when one big thing is

exchanged for another. The main problem (or as a result of this compromise) is that

overspending means the expected profit, so fair spending indicates that revenue will rise to the

cost level, and insufficient spending means that costs increase beyond revenue.

Budget Development Process

The process begins with setting a reservation for the upcoming time frame. These assumptions

are characterized by expected trading patterns, cost patterns, and an overall economic perspective

of the market, industry, or region. Consider and monitor specific factors affecting potential costs.

Budget are distributed as a package showing the principles and methods used to implement them,

including a description of assumptions about the business segment, the associations of key

vendors that set boundaries, and specific estimation methods.

Benefits

1. The plan forces and encourages leaders to investigate problems early and completely. This not

only gives the directors insight and anxiety, but they do a lot of research before making a choice.

2. Plans are “expenditure plans” and therefore provide an important way to manage payments

and business use.

3. The plan provides the tools to periodically evaluate, test, and set management methods and

goals as rules of society as a whole.

4. Planning helps coordinate various capital and assets in the most productive channels.

very important when using custom scorecards to ensure that the tracked information matches

company’s needs. Everything else, measurement is useless.

2. Budgeting

Budget is estimates of income and expenses over a period of time and are usually formulated and

revised from time to time. Financial plans can be created for individuals, groups, companies,

management, or almost anything that generates and sends cash.

A budget is a microeconomic idea that shows the compromises reached when one big thing is

exchanged for another. The main problem (or as a result of this compromise) is that

overspending means the expected profit, so fair spending indicates that revenue will rise to the

cost level, and insufficient spending means that costs increase beyond revenue.

Budget Development Process

The process begins with setting a reservation for the upcoming time frame. These assumptions

are characterized by expected trading patterns, cost patterns, and an overall economic perspective

of the market, industry, or region. Consider and monitor specific factors affecting potential costs.

Budget are distributed as a package showing the principles and methods used to implement them,

including a description of assumptions about the business segment, the associations of key

vendors that set boundaries, and specific estimation methods.

Benefits

1. The plan forces and encourages leaders to investigate problems early and completely. This not

only gives the directors insight and anxiety, but they do a lot of research before making a choice.

2. Plans are “expenditure plans” and therefore provide an important way to manage payments

and business use.

3. The plan provides the tools to periodically evaluate, test, and set management methods and

goals as rules of society as a whole.

4. Planning helps coordinate various capital and assets in the most productive channels.

5. Planning allows managers to transfer responsibilities without losing control over the business.

Defects, errors, and contact deviations can be quickly identified and quickly identified to achieve

the perfect goal.

6. The use of plans in society promotes a 'cost aware' way of thinking, encourages the successful

use of assets, and creates a profit-seeking atmosphere throughout society. Emphasize how much

money company need to spend to achieve company’s goals.

7. Provide standards, standards, or standards for evaluating the performance of offices and

individuals working for the association. Individual leaders can judge their choices and

performance, and find insightful ways to improve their performance.

8. Planning promotes profitable competition, promotes productive work and provides direction

for all members of society. Each of these positive components leads to higher returns and greater

representative profitability.

9. Plans provide a conscious and smart way to deal with social issues.

10. Almost all companies benefit the entire national economy by ensuring operational reliability,

economic use of assets and strong projected losses whenever a plan is carried out.

Disadvantages

1. Organization, planning, or evaluation is certainly not a clear science. Use approximations and

evaluations that can be inaccurate. Financial planning at its best is an indicator. No one knows

what will happen next.

2. The achievement and usefulness of the plan depends on the cooperation and support of all

board members. Everyone must adjust their efforts according to consensus. Top management

must also follow and participate in spending plans. The plan failed for several periods because

members of the board only provided empty requests for execution.

Spending planning is a tool that controls or does not control the board space. Spending plans for

managers cannot be completed, but boards should only use them to meet management

capabilities. Leaders generally feel "wrapped" by financial plans and related figures. They ignore

the understanding that spending plans are designed to provide detailed data, goals, and objectives

that can help company achieve company’s organization's goals.

Defects, errors, and contact deviations can be quickly identified and quickly identified to achieve

the perfect goal.

6. The use of plans in society promotes a 'cost aware' way of thinking, encourages the successful

use of assets, and creates a profit-seeking atmosphere throughout society. Emphasize how much

money company need to spend to achieve company’s goals.

7. Provide standards, standards, or standards for evaluating the performance of offices and

individuals working for the association. Individual leaders can judge their choices and

performance, and find insightful ways to improve their performance.

8. Planning promotes profitable competition, promotes productive work and provides direction

for all members of society. Each of these positive components leads to higher returns and greater

representative profitability.

9. Plans provide a conscious and smart way to deal with social issues.

10. Almost all companies benefit the entire national economy by ensuring operational reliability,

economic use of assets and strong projected losses whenever a plan is carried out.

Disadvantages

1. Organization, planning, or evaluation is certainly not a clear science. Use approximations and

evaluations that can be inaccurate. Financial planning at its best is an indicator. No one knows

what will happen next.

2. The achievement and usefulness of the plan depends on the cooperation and support of all

board members. Everyone must adjust their efforts according to consensus. Top management

must also follow and participate in spending plans. The plan failed for several periods because

members of the board only provided empty requests for execution.

Spending planning is a tool that controls or does not control the board space. Spending plans for

managers cannot be completed, but boards should only use them to meet management

capabilities. Leaders generally feel "wrapped" by financial plans and related figures. They ignore

the understanding that spending plans are designed to provide detailed data, goals, and objectives

that can help company achieve company’s organization's goals.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Significant investments are required to establish a planned investment. Also, sometimes too

much money is normal for the spending plan, and if the assumptions are not met, errors in the

spending plan break. A productive planning program requires skilled people to understand the

thinking, goals, and basics of planning.

5. Overweight in a plan can result in lower-level managers and employees breaking the

framework by making basic estimates of future costs and returns and ignoring climate change in

the light of the fact that this could cause deviances from the plan. It is considered to offset the

spending plan. In a one-sided spending program, representatives tend to overestimate costs and

ignore revenues, resulting in lower costs.

6. The end of the spending period is approaching, and representatives may have to spend a lot to

“manage” spending subsidies, realizing that the actual costs are not as surprising as the financial

plan allows. These exercises have the benefit of being problematic for the organization.

Best Method

The best method among above discussed tools can be budgeting, as this tool can give measures

to control present activities based on future target set by the company as a milestone. This tool

can facilitate variance analyses, which is helpful in identifying gap in present strategy.

Task 2

DuPont Analyses

DuPont Investigation (aka DuPont Character or DuPont Model) is a material performance

analysis framework promoted by DuPont Corporation. DuPont due diligence is a valuable

procedure used to reduce various factors of profitability (ROE). Reduced return on capital allows

sponsors to focus on key performance indicators, recognizing only their strengths and

weaknesses.

DuPont's research is used to estimate a segment's profit share for organizational value (ROE).

This allows sponsors to discover that financial transactions contribute the most to the

advancement of ROE. Financial sponsors can use similar rankings to analyze the results of two

much money is normal for the spending plan, and if the assumptions are not met, errors in the

spending plan break. A productive planning program requires skilled people to understand the

thinking, goals, and basics of planning.

5. Overweight in a plan can result in lower-level managers and employees breaking the

framework by making basic estimates of future costs and returns and ignoring climate change in

the light of the fact that this could cause deviances from the plan. It is considered to offset the

spending plan. In a one-sided spending program, representatives tend to overestimate costs and

ignore revenues, resulting in lower costs.

6. The end of the spending period is approaching, and representatives may have to spend a lot to

“manage” spending subsidies, realizing that the actual costs are not as surprising as the financial

plan allows. These exercises have the benefit of being problematic for the organization.

Best Method

The best method among above discussed tools can be budgeting, as this tool can give measures

to control present activities based on future target set by the company as a milestone. This tool

can facilitate variance analyses, which is helpful in identifying gap in present strategy.

Task 2

DuPont Analyses

DuPont Investigation (aka DuPont Character or DuPont Model) is a material performance

analysis framework promoted by DuPont Corporation. DuPont due diligence is a valuable

procedure used to reduce various factors of profitability (ROE). Reduced return on capital allows

sponsors to focus on key performance indicators, recognizing only their strengths and

weaknesses.

DuPont's research is used to estimate a segment's profit share for organizational value (ROE).

This allows sponsors to discover that financial transactions contribute the most to the

advancement of ROE. Financial sponsors can use similar rankings to analyze the results of two

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

similar companies. Board members can use the DuPont exam to identify qualifications or

deficiencies that need to be addressed.

The three important economic measures that determine profitability (ROE) are labor

productivity, resource efficiency, and economic impact. Labor productivity is determined as net

income or net income divided by the absolute transaction or income. Resource efficiency is

estimated as a percentage of resource turnovers. Impact is assessed using a value multiplier equal

to the average resource allocated as a normal value.

The use of money

The Financial Impact or Value Multiplier is a circular survey of an organization's use of resource

support commitments. The organization's resources are $1,000 and the cost of ownership is

$250. The account item status tells company that the organization also has $750 in red (resource-

liabilities = cost). As organizations free up more resources to purchase resources, their share will

continue to grow.

Most organizations need to use value-added promises to finance their data and development.

Failure to exert influence can put company’s organization in a difficult position compared to its

peers. However, if company put too much effort to Increase Company’s share of company’s

financial power and increase company’s ROE, company can create an imbalance risk.

Calculation:

DuPont Analysis=Net Profit Margin × AT × EM

Where:

Net Profit Margin=Revenue

Net IncomeAT=Asset turnover

Asset Turnover=Average Total Assets

SalesEM=Equity multiplier

Equity Multiplier=Average Shareholders’ EquityAverage Total Assets

DuPont Analyses = 0.035 * 1.5 * 2.5

deficiencies that need to be addressed.

The three important economic measures that determine profitability (ROE) are labor

productivity, resource efficiency, and economic impact. Labor productivity is determined as net

income or net income divided by the absolute transaction or income. Resource efficiency is

estimated as a percentage of resource turnovers. Impact is assessed using a value multiplier equal

to the average resource allocated as a normal value.

The use of money

The Financial Impact or Value Multiplier is a circular survey of an organization's use of resource

support commitments. The organization's resources are $1,000 and the cost of ownership is

$250. The account item status tells company that the organization also has $750 in red (resource-

liabilities = cost). As organizations free up more resources to purchase resources, their share will

continue to grow.

Most organizations need to use value-added promises to finance their data and development.

Failure to exert influence can put company’s organization in a difficult position compared to its

peers. However, if company put too much effort to Increase Company’s share of company’s

financial power and increase company’s ROE, company can create an imbalance risk.

Calculation:

DuPont Analysis=Net Profit Margin × AT × EM

Where:

Net Profit Margin=Revenue

Net IncomeAT=Asset turnover

Asset Turnover=Average Total Assets

SalesEM=Equity multiplier

Equity Multiplier=Average Shareholders’ EquityAverage Total Assets

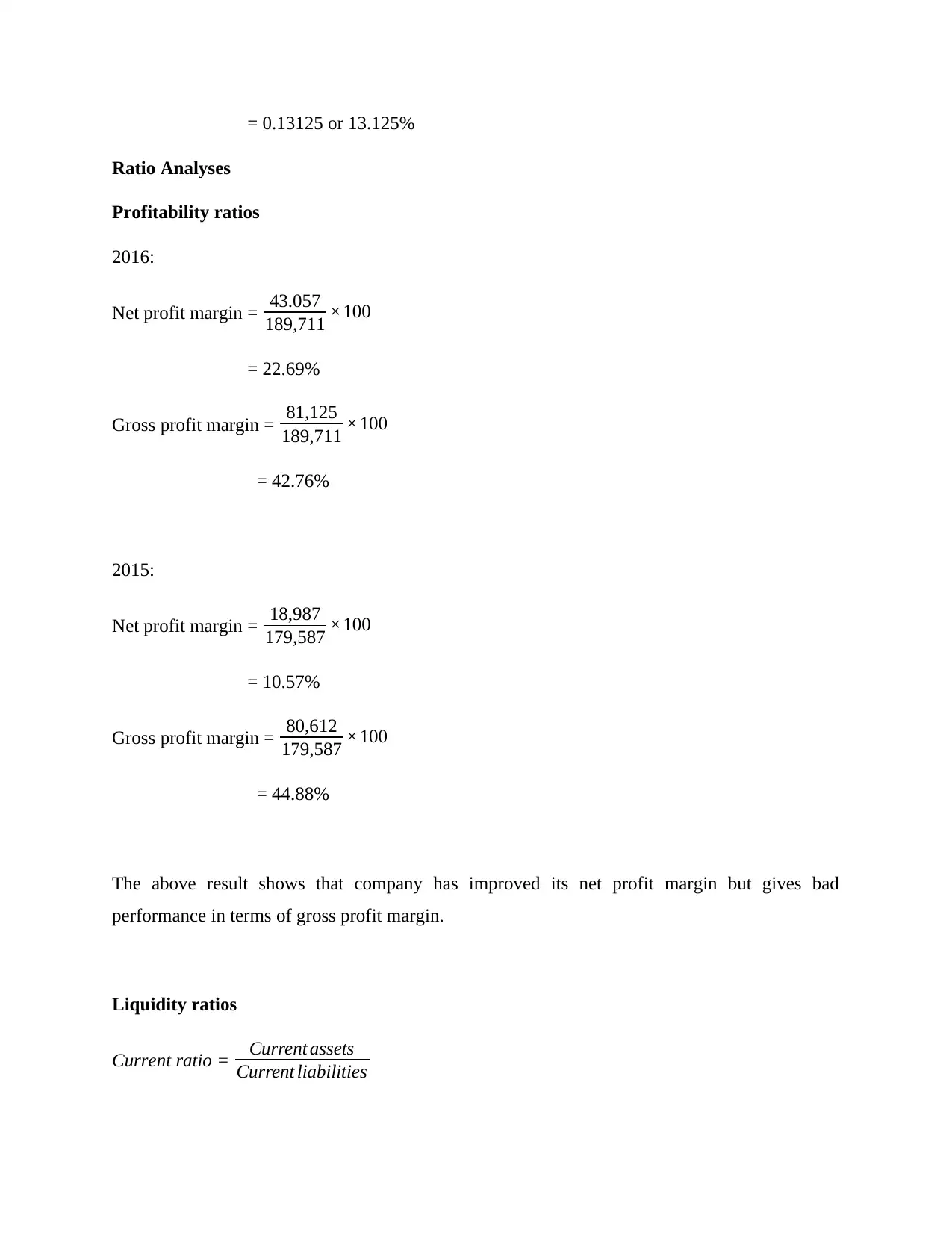

DuPont Analyses = 0.035 * 1.5 * 2.5

= 0.13125 or 13.125%

Ratio Analyses

Profitability ratios

2016:

Net profit margin = 43.057

189,711 ×100

= 22.69%

Gross profit margin = 81,125

189,711 ×100

= 42.76%

2015:

Net profit margin = 18,987

179,587 ×100

= 10.57%

Gross profit margin = 80,612

179,587 ×100

= 44.88%

The above result shows that company has improved its net profit margin but gives bad

performance in terms of gross profit margin.

Liquidity ratios

Current ratio = Current assets

Current liabilities

Ratio Analyses

Profitability ratios

2016:

Net profit margin = 43.057

189,711 ×100

= 22.69%

Gross profit margin = 81,125

189,711 ×100

= 42.76%

2015:

Net profit margin = 18,987

179,587 ×100

= 10.57%

Gross profit margin = 80,612

179,587 ×100

= 44.88%

The above result shows that company has improved its net profit margin but gives bad

performance in terms of gross profit margin.

Liquidity ratios

Current ratio = Current assets

Current liabilities

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

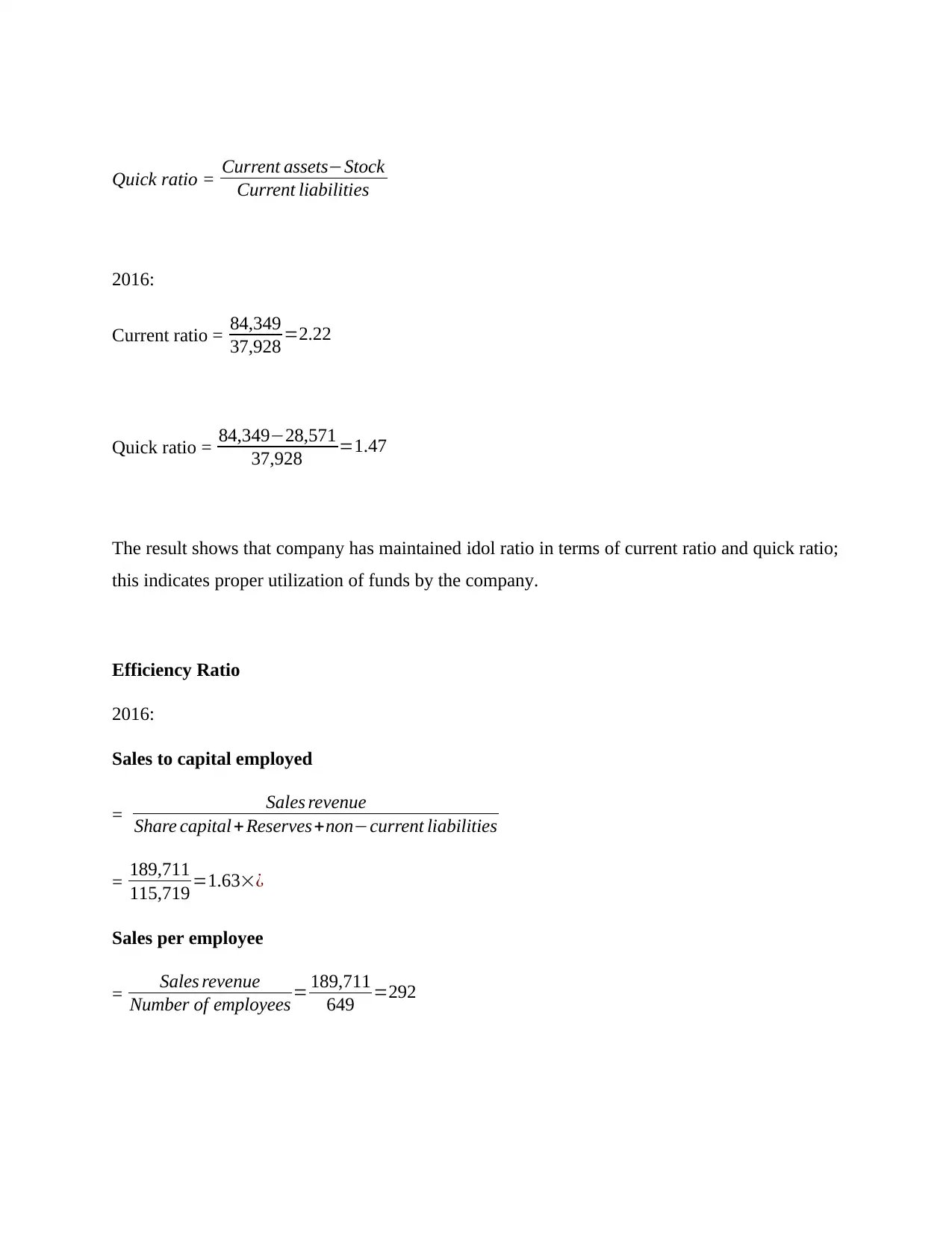

Quick ratio = Current assets−Stock

Current liabilities

2016:

Current ratio = 84,349

37,928 =2.22

Quick ratio = 84,349−28,571

37,928 =1.47

The result shows that company has maintained idol ratio in terms of current ratio and quick ratio;

this indicates proper utilization of funds by the company.

Efficiency Ratio

2016:

Sales to capital employed

= Sales revenue

Share capital +Reserves+non−current liabilities

= 189,711

115,719 =1.63׿

Sales per employee

= Sales revenue

Number of employees = 189,711

649 =292

Current liabilities

2016:

Current ratio = 84,349

37,928 =2.22

Quick ratio = 84,349−28,571

37,928 =1.47

The result shows that company has maintained idol ratio in terms of current ratio and quick ratio;

this indicates proper utilization of funds by the company.

Efficiency Ratio

2016:

Sales to capital employed

= Sales revenue

Share capital +Reserves+non−current liabilities

= 189,711

115,719 =1.63׿

Sales per employee

= Sales revenue

Number of employees = 189,711

649 =292

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 3

Non-financial measures

Performance appraisal frameworks play an important role in creating skills, assessing the

achievement of prestigious goals, and rewarding managers. However, many managers believe

that their existing financial structures are not working satisfactorily now. Most people are

dissatisfied with their pricing plans, according to a new study by U.S. financial authorities. They

recognized that financial measurements are primarily accounting revenues and profits that

highlight important factors such as customer, employee satisfaction, development and quality.

As a result, organizations are adopting a new performance appraisal system. For example, 33%

of financial institutions have significantly improved their performance-performance structure

over the past two years, and 39% of institutions have made significant changes within two years.

The deficit in economic development has shifted from "intangible resources" and "scientific

capital" to non-monetary measures to "adjusted scorecards" for inherent financial and non-

financial measures. This article explores the benefits and barriers of non-financial enforcement

action and provides ideas for action.

Benefits

Non-financial measures offer four distinct advantages over economically dependent pricing

systems. First, it is more closely related to the authoritative long-distance method. In general,

financial frameworks focus on the annual or introductory development of accounting standards.

We do not promote customer or candidate needs or other non-financial goals that may be related

to revenue, constant strength, and long-term life goals. For example, promoting new jobs or

expanding hierarchical opportunities can be an important key task, but it can hinder ad hoc

accounting.

By combining accounting measures with critical non-financial information about the execution

and execution of essential plans, organizations can set goals and motivate board members to use

long-term methodologies.

Second, existing standards experts argue that the driving force of many companies is not the

"hard resources" allowed in the asset statement, but rather the "intangible resources" such as

Non-financial measures

Performance appraisal frameworks play an important role in creating skills, assessing the

achievement of prestigious goals, and rewarding managers. However, many managers believe

that their existing financial structures are not working satisfactorily now. Most people are

dissatisfied with their pricing plans, according to a new study by U.S. financial authorities. They

recognized that financial measurements are primarily accounting revenues and profits that

highlight important factors such as customer, employee satisfaction, development and quality.

As a result, organizations are adopting a new performance appraisal system. For example, 33%

of financial institutions have significantly improved their performance-performance structure

over the past two years, and 39% of institutions have made significant changes within two years.

The deficit in economic development has shifted from "intangible resources" and "scientific

capital" to non-monetary measures to "adjusted scorecards" for inherent financial and non-

financial measures. This article explores the benefits and barriers of non-financial enforcement

action and provides ideas for action.

Benefits

Non-financial measures offer four distinct advantages over economically dependent pricing

systems. First, it is more closely related to the authoritative long-distance method. In general,

financial frameworks focus on the annual or introductory development of accounting standards.

We do not promote customer or candidate needs or other non-financial goals that may be related

to revenue, constant strength, and long-term life goals. For example, promoting new jobs or

expanding hierarchical opportunities can be an important key task, but it can hinder ad hoc

accounting.

By combining accounting measures with critical non-financial information about the execution

and execution of essential plans, organizations can set goals and motivate board members to use

long-term methodologies.

Second, existing standards experts argue that the driving force of many companies is not the

"hard resources" allowed in the asset statement, but rather the "intangible resources" such as

scientific capital and customer engagement. It is difficult to measure intangible resources from a

financial standpoint, but non-financial information can provide an inverse quantitative indicator

of a society's intangible resources.

One study demonstrated the ability of non-monetary “intangible” proposals to account for

differences in financial exchange estimates of US institutions. Campaign-related actions, board

functions, terms of employment, respect for quality and brand have proven very clearly to the

value of the organization, regardless of its accounting resources and obligations. By excluding

these intangible resources, financial valuation can lead managers to make wrong choices and

even make destructive choices.

Third, non-financial measures can be the best indicator of future economic performance. No

matter what your ultimate goal is to strengthen your financial advancement, your current

financial measures may not yield long-term benefits from your current choices. For example,

imagine you are interested in innovative work or customer loyalty programs. U.S. accounting

rules require the use of innovation and demo costs for the period in which they are incurred,

which reduces the benefit. However, beneficial learning generally enhances future benefits if it

can be proven.

Essentially, a commitment to consumer loyalty can improve your ultimate financial performance

by increasing revenue and loyalty to existing customers, attracting new customers, and reducing

call costs. Non-financial information can provide predictable accounting information or stock

performance by providing the missing link between these beneficial events and financial results.

For example, the results of an ad hoc investigation or customer file may indicate future interests

where nothing else can be found.

Finally, the choice of action should be based on information about administrative activities and

the degree of "use" of the action. Anxiety refers to a change in perception beyond the control of a

leader or society and moves from a change in the economy to karma (positive or negative).

Directors need to know how much their achievements have achieved. Otherwise, you don't have

the attributes you need to expand your impact on performance. Since there are many non-

financial measures are less susceptible to external shocks than accounting measures, their use can

provide a more accurate assessment of the results, increasing the perception of management.

This further reduces the risk that managers face when making compensation decisions.

financial standpoint, but non-financial information can provide an inverse quantitative indicator

of a society's intangible resources.

One study demonstrated the ability of non-monetary “intangible” proposals to account for

differences in financial exchange estimates of US institutions. Campaign-related actions, board

functions, terms of employment, respect for quality and brand have proven very clearly to the

value of the organization, regardless of its accounting resources and obligations. By excluding

these intangible resources, financial valuation can lead managers to make wrong choices and

even make destructive choices.

Third, non-financial measures can be the best indicator of future economic performance. No

matter what your ultimate goal is to strengthen your financial advancement, your current

financial measures may not yield long-term benefits from your current choices. For example,

imagine you are interested in innovative work or customer loyalty programs. U.S. accounting

rules require the use of innovation and demo costs for the period in which they are incurred,

which reduces the benefit. However, beneficial learning generally enhances future benefits if it

can be proven.

Essentially, a commitment to consumer loyalty can improve your ultimate financial performance

by increasing revenue and loyalty to existing customers, attracting new customers, and reducing

call costs. Non-financial information can provide predictable accounting information or stock

performance by providing the missing link between these beneficial events and financial results.

For example, the results of an ad hoc investigation or customer file may indicate future interests

where nothing else can be found.

Finally, the choice of action should be based on information about administrative activities and

the degree of "use" of the action. Anxiety refers to a change in perception beyond the control of a

leader or society and moves from a change in the economy to karma (positive or negative).

Directors need to know how much their achievements have achieved. Otherwise, you don't have

the attributes you need to expand your impact on performance. Since there are many non-

financial measures are less susceptible to external shocks than accounting measures, their use can

provide a more accurate assessment of the results, increasing the perception of management.

This further reduces the risk that managers face when making compensation decisions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.