Financial Performance Analysis: CVP, Breakeven, and High-Low Method

VerifiedAdded on 2020/04/29

|23

|4425

|193

Report

AI Summary

This report provides a comprehensive analysis of Cost-Volume-Profit (CVP) analysis, focusing on breakeven points and cost estimation using the high-low method. It begins with an introduction to the objectives, which include analyzing Economist's and Accountant's break even charts, CVP, fixed costs, and the breakeven point of a company. The report differentiates between Economist's and Accountant's break even charts, outlining their fundamental differences and applications. It then delves into the assumptions of CVP analysis, emphasizing the importance of categorizing costs, the impact of volume, and the significance of the breakeven point in units and dollars. The report also includes a detailed analysis using the High-Low method to calculate the breakeven point and margin of safety for a company, including fixed and variable costs, and the limitations of the High-Low method. Finally, the report concludes with a summary of the findings, highlighting the company's financial position based on the margin of safety and breakeven point.

Performance Management 1

Performance Management

Performance Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance Management 2

Table of Contents

Introduction......................................................................................................................................3

Economist’s and Accountant’s break even charts...........................................................................3

Analysis of CVP..............................................................................................................................4

BreakevenPoint and High low method of the company................................................................7

Comparison of the two proposals..................................................................................................11

Recommendations..........................................................................................................................14

Conclusion.....................................................................................................................................18

References......................................................................................................................................19

Appendix........................................................................................................................................21

Table of Contents

Introduction......................................................................................................................................3

Economist’s and Accountant’s break even charts...........................................................................3

Analysis of CVP..............................................................................................................................4

BreakevenPoint and High low method of the company................................................................7

Comparison of the two proposals..................................................................................................11

Recommendations..........................................................................................................................14

Conclusion.....................................................................................................................................18

References......................................................................................................................................19

Appendix........................................................................................................................................21

Performance Management 3

Introduction

This report mainly serves two objectives. This report will help in making an analysis of The

Economist's break even charts and The Accountant's break even charts. Accountant's break even

charts and Economist's break even charts are different from each other but they have same

fundamentals. An Analysis of CVP is also undertaken in this report. An analysis on Fixed cost

does not change with the volume of the output which incurs in the scale of production as fixed by

the management of the organization is also carried out in order to making the analysis that what

is meant by period of time and relevant range. An analysis on Breakeven Point and Margin of

Safety of the company based on its present cost structure for the second half year of 2016, and

of the High-Low method of cost estimation is also carried out. Further a comparison between

two proposals is carried out in order to evaluate the best proposal after comparing all the aspects.

Economist’s and Accountant’s break even charts

The Economist's break even charts

The way of economist’s break even chart has its own advantages for making an analysis of costs

and break even charts. This method involves calculation of costs, profit and volume over

different range of activities. When shown in graph, revenue shows curvilinear trend (Schlicht,

2012).

Organization can increase its sale by making a reduction in its selling price and thus total

revenue do not make an increase simultaneously with the output and thus revenue shows

curvilinear trend. On the other side, variable costs make an increase at the time of low sales and

low production made by the organization and this happens because of increase in the cost of

operations. It is said that once if the business maintains its efficiency in operations, the costs

increases very slowly and thus becomes less steeply and make an increase in linear graph. But, if

Introduction

This report mainly serves two objectives. This report will help in making an analysis of The

Economist's break even charts and The Accountant's break even charts. Accountant's break even

charts and Economist's break even charts are different from each other but they have same

fundamentals. An Analysis of CVP is also undertaken in this report. An analysis on Fixed cost

does not change with the volume of the output which incurs in the scale of production as fixed by

the management of the organization is also carried out in order to making the analysis that what

is meant by period of time and relevant range. An analysis on Breakeven Point and Margin of

Safety of the company based on its present cost structure for the second half year of 2016, and

of the High-Low method of cost estimation is also carried out. Further a comparison between

two proposals is carried out in order to evaluate the best proposal after comparing all the aspects.

Economist’s and Accountant’s break even charts

The Economist's break even charts

The way of economist’s break even chart has its own advantages for making an analysis of costs

and break even charts. This method involves calculation of costs, profit and volume over

different range of activities. When shown in graph, revenue shows curvilinear trend (Schlicht,

2012).

Organization can increase its sale by making a reduction in its selling price and thus total

revenue do not make an increase simultaneously with the output and thus revenue shows

curvilinear trend. On the other side, variable costs make an increase at the time of low sales and

low production made by the organization and this happens because of increase in the cost of

operations. It is said that once if the business maintains its efficiency in operations, the costs

increases very slowly and thus becomes less steeply and make an increase in linear graph. But, if

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Performance Management 4

the production activity is carried beyond the capacity of the plant than it will lead towards

problem of breakdown and costs make an increase and thus it can be analyzed that the business

will have two breakeven points (Osterwalder and Pigneur, 2010).

The Accountant's break even charts

The other method is accountant’s way of making an analysis on costs and revenue and stated that

they have a relationship between them which is linear. It can be analyzed that both the

Accountant's break even charts and Economist's break even charts are different from each other

but they have same fundamentals. The major difference in the accountant’s way is that it put its

focus on prediction of relationship of cost-volume-profit (CVP) in the relevant range where

business is bringing constant returns to scale (Coase, 2012) . This can be stated that both the

methods use costs and revenue in the relevant range.

Analysis of CVP

Assumptions of Analysis of CVP

It can be assumed that all the costs can be categorized into fixed and variable costs. Fixed costs

are the costs that are constant and do not vary with the product ion made by the organization and

the rent of the factory is one of the example. Variable cost can be termed as those cots which are

directly related with the production and changes in proportionate with the output and if the firm

produces more than the variable cost of the firm will increase. Wages of workers is one of the

examples of variable costs. It can also be assumed that the factors which affect revenue and costs

are termed as volume (Foster and Rosenzweig, 2010). CVP is considered important for making

an analysis of CVP. Break even is a calculation to determine the volume of sales at which the

firm will be not making any profits and even not making any losses.

the production activity is carried beyond the capacity of the plant than it will lead towards

problem of breakdown and costs make an increase and thus it can be analyzed that the business

will have two breakeven points (Osterwalder and Pigneur, 2010).

The Accountant's break even charts

The other method is accountant’s way of making an analysis on costs and revenue and stated that

they have a relationship between them which is linear. It can be analyzed that both the

Accountant's break even charts and Economist's break even charts are different from each other

but they have same fundamentals. The major difference in the accountant’s way is that it put its

focus on prediction of relationship of cost-volume-profit (CVP) in the relevant range where

business is bringing constant returns to scale (Coase, 2012) . This can be stated that both the

methods use costs and revenue in the relevant range.

Analysis of CVP

Assumptions of Analysis of CVP

It can be assumed that all the costs can be categorized into fixed and variable costs. Fixed costs

are the costs that are constant and do not vary with the product ion made by the organization and

the rent of the factory is one of the example. Variable cost can be termed as those cots which are

directly related with the production and changes in proportionate with the output and if the firm

produces more than the variable cost of the firm will increase. Wages of workers is one of the

examples of variable costs. It can also be assumed that the factors which affect revenue and costs

are termed as volume (Foster and Rosenzweig, 2010). CVP is considered important for making

an analysis of CVP. Break even is a calculation to determine the volume of sales at which the

firm will be not making any profits and even not making any losses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance Management 5

In analyzing CVP, an influential function is to analyze the breakeven point in units for the

organization (Nicholson and Snyder, 2014). You can compute the breakeven point in dollars by

multiply the sales price for your manufactured goods by the breakeven point in units.

Fixed cost does not change with the volume of the output which incurs in the scale of production

as fixed by the management of the organization. In case if behavior of cost is linked to sales

income, it shows relationship of cost-volume-profit. In net effect, if change is being made in

volume, variable cost makes variation as per the change incurred in the volume. In this case if

selling price is made fixed, fixed remains fixed and then change in the profits incurred (Moulin,

2014).

Being a manager, one on a continuous basis strives to relate these elements in order to make the

maximum profit. Apart from profit projection, the concept of Cost-Volume-Profit (CVP) is

relevant to virtually all decision-making areas mainly in the short run. The relationship among

cost, revenue and profit at different levels can be highlighted in graphs such as breakeven charts,

profit volume graphs, and different other graphs (Cafferky, 2010).

Profit depends on various factors like manufacturing cost and the volume of the sales. These both

the factors are linked with each other. The volume of costs relies upon the market forces and

volume of production which are related to the costs mainly. The management of the organization

does not possess any control over the market. In order to achieve certain level of effectiveness, it

has to use control and management of expenditure, mainly variable cost (Weiss, 2010). This is

because fixed cost cannot be controlled in the organization. But then, cost is based on the

following factors:

Volume of production

Product mix

In analyzing CVP, an influential function is to analyze the breakeven point in units for the

organization (Nicholson and Snyder, 2014). You can compute the breakeven point in dollars by

multiply the sales price for your manufactured goods by the breakeven point in units.

Fixed cost does not change with the volume of the output which incurs in the scale of production

as fixed by the management of the organization. In case if behavior of cost is linked to sales

income, it shows relationship of cost-volume-profit. In net effect, if change is being made in

volume, variable cost makes variation as per the change incurred in the volume. In this case if

selling price is made fixed, fixed remains fixed and then change in the profits incurred (Moulin,

2014).

Being a manager, one on a continuous basis strives to relate these elements in order to make the

maximum profit. Apart from profit projection, the concept of Cost-Volume-Profit (CVP) is

relevant to virtually all decision-making areas mainly in the short run. The relationship among

cost, revenue and profit at different levels can be highlighted in graphs such as breakeven charts,

profit volume graphs, and different other graphs (Cafferky, 2010).

Profit depends on various factors like manufacturing cost and the volume of the sales. These both

the factors are linked with each other. The volume of costs relies upon the market forces and

volume of production which are related to the costs mainly. The management of the organization

does not possess any control over the market. In order to achieve certain level of effectiveness, it

has to use control and management of expenditure, mainly variable cost (Weiss, 2010). This is

because fixed cost cannot be controlled in the organization. But then, cost is based on the

following factors:

Volume of production

Product mix

Performance Management 6

Internal efficiency and the productivity of the factors of production

Methods of production and technology

Batch Size

Plant Size

Thus it can be analyzed that the cost-volume-profit analysis furnishes the complete scenario of

the profit structure. This will help the management to make a differentiation among the effect of

sales, changes in volume and also the changes made to the price of the product. .In other words,

CVP is a tool of management accounting which helps in showing the relationship between sale

volume, cost and profit (Boland, 2014). CVP analysis also helps in answering various analytical

questions which can prove profitable to the organization.

Advantages of CVP analysis

The Managing Director is now aware of various importance of CVP analysis. CVP is quite

useful in making analysis of breakeven point for the firm. CVP is also helpful in making charts

regarding breakeven point in order to make an identification of the profitability of the

organization (Rader, 2014). The relationships between profit, volume and revenue can be

depicted on the charts. CVP analysis will be helpful in budget planning and thus helpful ion

taking decisions regarding pricing, mix of sales and different product mix. CVP analysis is also

important technique for sensitivity analysis. CVP is very effective in calculation of profits and

sales under different situations. The managing director can use the CVP analysis in order to

determine profits and sales when the unit prices of the products being changed. This will help

the managing director to determine the best alternative for the profitability of the organization.

This will also help in profit planning for the organization (Elsner et. al., 2014) CVP is also

Internal efficiency and the productivity of the factors of production

Methods of production and technology

Batch Size

Plant Size

Thus it can be analyzed that the cost-volume-profit analysis furnishes the complete scenario of

the profit structure. This will help the management to make a differentiation among the effect of

sales, changes in volume and also the changes made to the price of the product. .In other words,

CVP is a tool of management accounting which helps in showing the relationship between sale

volume, cost and profit (Boland, 2014). CVP analysis also helps in answering various analytical

questions which can prove profitable to the organization.

Advantages of CVP analysis

The Managing Director is now aware of various importance of CVP analysis. CVP is quite

useful in making analysis of breakeven point for the firm. CVP is also helpful in making charts

regarding breakeven point in order to make an identification of the profitability of the

organization (Rader, 2014). The relationships between profit, volume and revenue can be

depicted on the charts. CVP analysis will be helpful in budget planning and thus helpful ion

taking decisions regarding pricing, mix of sales and different product mix. CVP analysis is also

important technique for sensitivity analysis. CVP is very effective in calculation of profits and

sales under different situations. The managing director can use the CVP analysis in order to

determine profits and sales when the unit prices of the products being changed. This will help

the managing director to determine the best alternative for the profitability of the organization.

This will also help in profit planning for the organization (Elsner et. al., 2014) CVP is also

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Performance Management 7

helpful in making an identification of the profitable products for the organization which can

enhance the profitability of the organization.

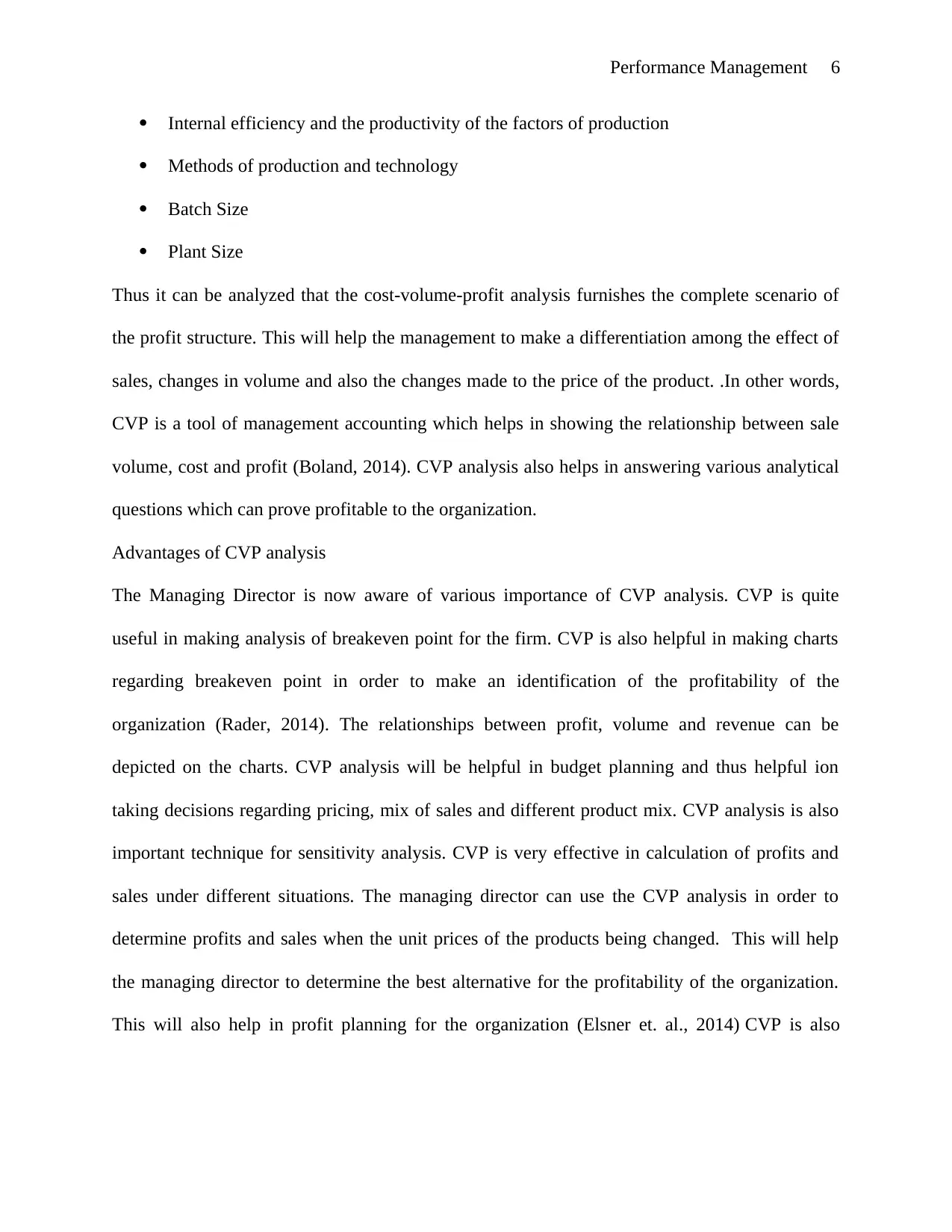

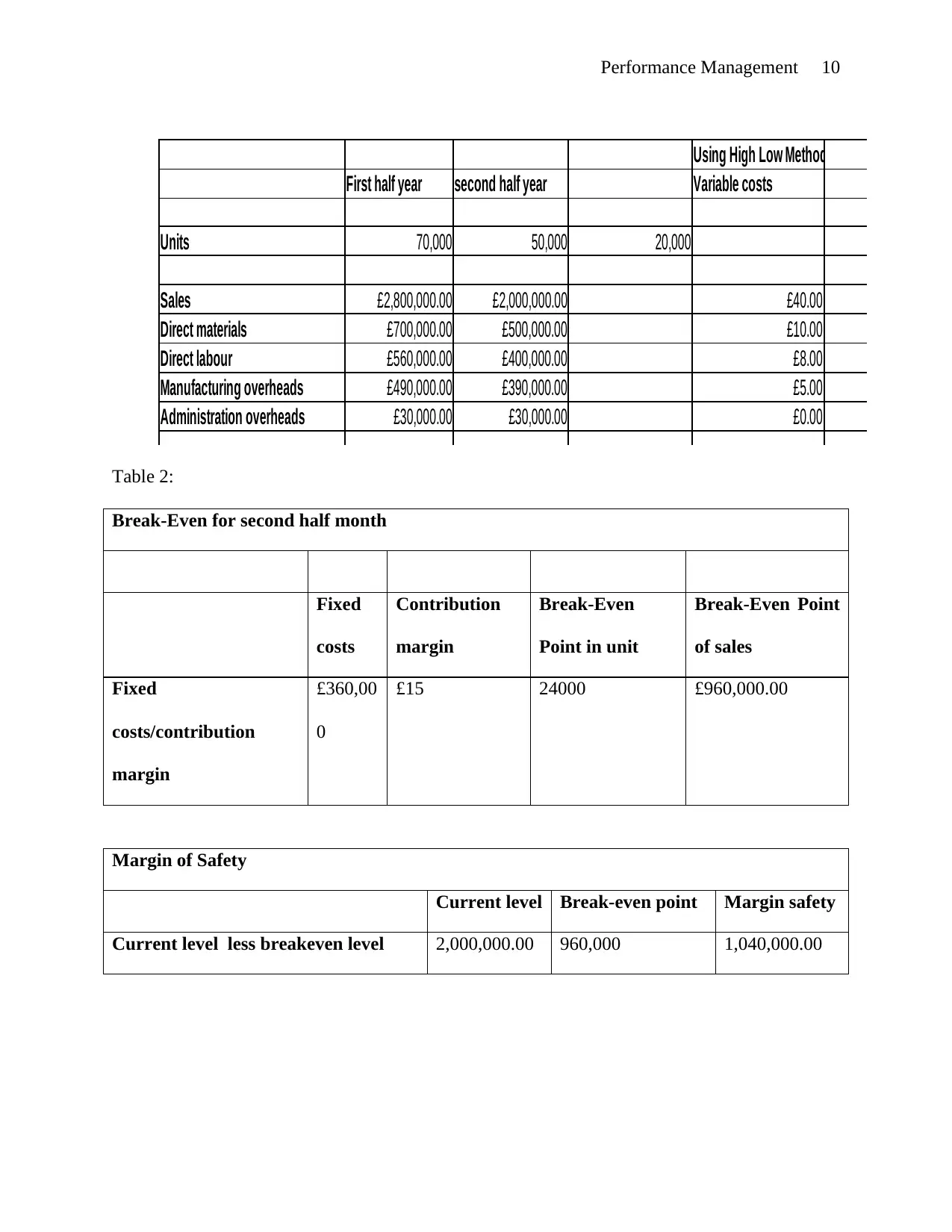

Breakeven Point and High low method of the company

Year 2016

Using High

Low Method

First half

year

second half

year

Variable

costs

Fixed

costs

Units 70,000 50,000 20,000

Sales £2,800,000.

00

£2,000,000.

00

£40.00 £0.00

Direct materials £700,000.0

0

£500,000.00 £10.00 £0.00

Direct labour £560,000.0

0

£400,000.00 £8.00 £0.00

Manufacturing

overheads

£490,000.0

0

£390,000.00 £5.00 £140,000.0

0

Administration

overheads

£30,000.00 £30,000.00 £0.00 £30,000.00

Selling overheads* £330,000.0

0

£290,000.00 £2.00 £190,000.0

0

helpful in making an identification of the profitable products for the organization which can

enhance the profitability of the organization.

Breakeven Point and High low method of the company

Year 2016

Using High

Low Method

First half

year

second half

year

Variable

costs

Fixed

costs

Units 70,000 50,000 20,000

Sales £2,800,000.

00

£2,000,000.

00

£40.00 £0.00

Direct materials £700,000.0

0

£500,000.00 £10.00 £0.00

Direct labour £560,000.0

0

£400,000.00 £8.00 £0.00

Manufacturing

overheads

£490,000.0

0

£390,000.00 £5.00 £140,000.0

0

Administration

overheads

£30,000.00 £30,000.00 £0.00 £30,000.00

Selling overheads* £330,000.0

0

£290,000.00 £2.00 £190,000.0

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

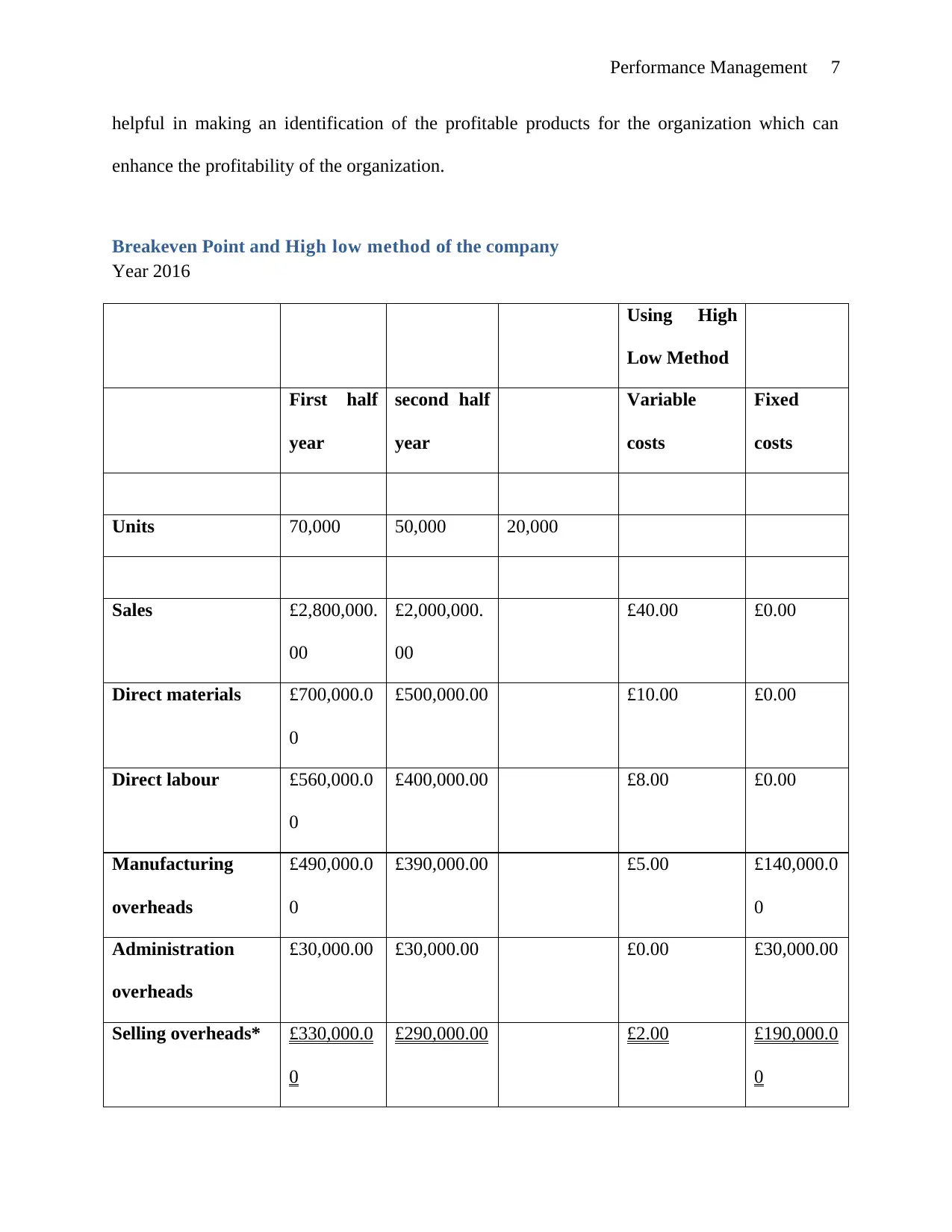

Total Revenue Curve

Total Cost Curve

BEP 1

BEP 1

Economic Profit Zone

Economic Loss Zone

Output in Units

Sales &

Cost

Performance Management 8

Net Profit £690,000.0

0

£390,000.00 £15.00 £360,000.0

0

Break Even Point under Economist Approach:

The following diagram shows the BEP chart under economist approach:

As per the above chart, BEP 1 is the level of sales, after which the company will start earning

profits. At this level of BEP, the company needs to sale 24000 units amounting to £960,000

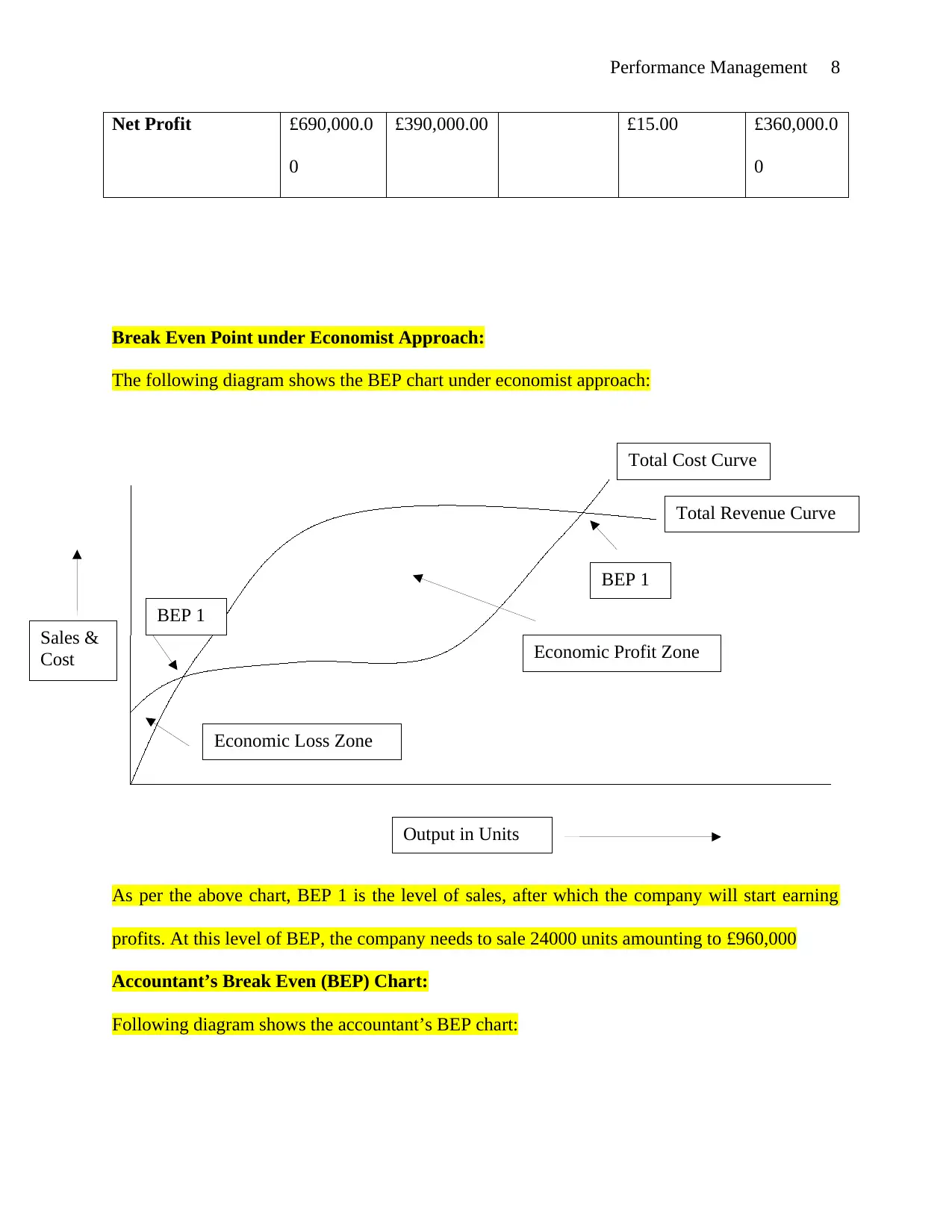

Accountant’s Break Even (BEP) Chart:

Following diagram shows the accountant’s BEP chart:

Total Cost Curve

BEP 1

BEP 1

Economic Profit Zone

Economic Loss Zone

Output in Units

Sales &

Cost

Performance Management 8

Net Profit £690,000.0

0

£390,000.00 £15.00 £360,000.0

0

Break Even Point under Economist Approach:

The following diagram shows the BEP chart under economist approach:

As per the above chart, BEP 1 is the level of sales, after which the company will start earning

profits. At this level of BEP, the company needs to sale 24000 units amounting to £960,000

Accountant’s Break Even (BEP) Chart:

Following diagram shows the accountant’s BEP chart:

Output (in Units)

Cost and Revenue

Break Even Point

24000 Units

BEP sales £960,000

Margin of Safety

Performance Management 9

The graph of Breakeven of the organization indicates the break-even point of organization. The y

axis presents the sales. It indicates the company will achieve break even at 24000units of £

£960,000. The graph also indicates that the margin of safety of the organization is £

1,040,000.00.

Table showing the calculations of HI-LOW method is as below:

Table 1:

Cost and Revenue

Break Even Point

24000 Units

BEP sales £960,000

Margin of Safety

Performance Management 9

The graph of Breakeven of the organization indicates the break-even point of organization. The y

axis presents the sales. It indicates the company will achieve break even at 24000units of £

£960,000. The graph also indicates that the margin of safety of the organization is £

1,040,000.00.

Table showing the calculations of HI-LOW method is as below:

Table 1:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Performance Management 10

Using High Low Method

First half year second half year Variable costs

Units 70,000 50,000 20,000

Sales £2,800,000.00 £2,000,000.00 £40.00

Direct materials £700,000.00 £500,000.00 £10.00

Direct labour £560,000.00 £400,000.00 £8.00

Manufacturing overheads £490,000.00 £390,000.00 £5.00

Administration overheads £30,000.00 £30,000.00 £0.00

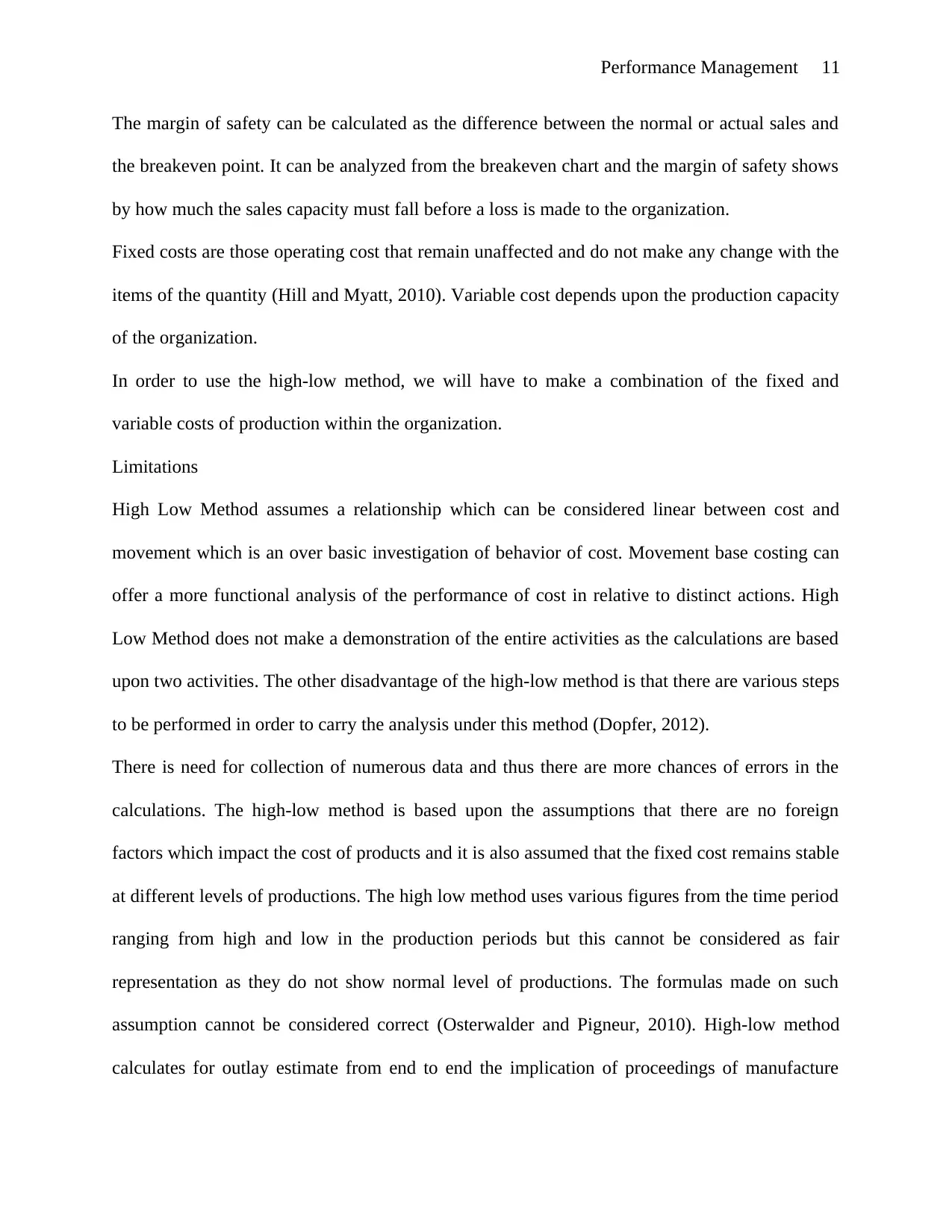

Table 2:

Break-Even for second half month

Fixed

costs

Contribution

margin

Break-Even

Point in unit

Break-Even Point

of sales

Fixed

costs/contribution

margin

£360,00

0

£15 24000 £960,000.00

Margin of Safety

Current level Break-even point Margin safety

Current level less breakeven level 2,000,000.00 960,000 1,040,000.00

Using High Low Method

First half year second half year Variable costs

Units 70,000 50,000 20,000

Sales £2,800,000.00 £2,000,000.00 £40.00

Direct materials £700,000.00 £500,000.00 £10.00

Direct labour £560,000.00 £400,000.00 £8.00

Manufacturing overheads £490,000.00 £390,000.00 £5.00

Administration overheads £30,000.00 £30,000.00 £0.00

Table 2:

Break-Even for second half month

Fixed

costs

Contribution

margin

Break-Even

Point in unit

Break-Even Point

of sales

Fixed

costs/contribution

margin

£360,00

0

£15 24000 £960,000.00

Margin of Safety

Current level Break-even point Margin safety

Current level less breakeven level 2,000,000.00 960,000 1,040,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance Management 11

The margin of safety can be calculated as the difference between the normal or actual sales and

the breakeven point. It can be analyzed from the breakeven chart and the margin of safety shows

by how much the sales capacity must fall before a loss is made to the organization.

Fixed costs are those operating cost that remain unaffected and do not make any change with the

items of the quantity (Hill and Myatt, 2010). Variable cost depends upon the production capacity

of the organization.

In order to use the high-low method, we will have to make a combination of the fixed and

variable costs of production within the organization.

Limitations

High Low Method assumes a relationship which can be considered linear between cost and

movement which is an over basic investigation of behavior of cost. Movement base costing can

offer a more functional analysis of the performance of cost in relative to distinct actions. High

Low Method does not make a demonstration of the entire activities as the calculations are based

upon two activities. The other disadvantage of the high-low method is that there are various steps

to be performed in order to carry the analysis under this method (Dopfer, 2012).

There is need for collection of numerous data and thus there are more chances of errors in the

calculations. The high-low method is based upon the assumptions that there are no foreign

factors which impact the cost of products and it is also assumed that the fixed cost remains stable

at different levels of productions. The high low method uses various figures from the time period

ranging from high and low in the production periods but this cannot be considered as fair

representation as they do not show normal level of productions. The formulas made on such

assumption cannot be considered correct (Osterwalder and Pigneur, 2010). High-low method

calculates for outlay estimate from end to end the implication of proceedings of manufacture

The margin of safety can be calculated as the difference between the normal or actual sales and

the breakeven point. It can be analyzed from the breakeven chart and the margin of safety shows

by how much the sales capacity must fall before a loss is made to the organization.

Fixed costs are those operating cost that remain unaffected and do not make any change with the

items of the quantity (Hill and Myatt, 2010). Variable cost depends upon the production capacity

of the organization.

In order to use the high-low method, we will have to make a combination of the fixed and

variable costs of production within the organization.

Limitations

High Low Method assumes a relationship which can be considered linear between cost and

movement which is an over basic investigation of behavior of cost. Movement base costing can

offer a more functional analysis of the performance of cost in relative to distinct actions. High

Low Method does not make a demonstration of the entire activities as the calculations are based

upon two activities. The other disadvantage of the high-low method is that there are various steps

to be performed in order to carry the analysis under this method (Dopfer, 2012).

There is need for collection of numerous data and thus there are more chances of errors in the

calculations. The high-low method is based upon the assumptions that there are no foreign

factors which impact the cost of products and it is also assumed that the fixed cost remains stable

at different levels of productions. The high low method uses various figures from the time period

ranging from high and low in the production periods but this cannot be considered as fair

representation as they do not show normal level of productions. The formulas made on such

assumption cannot be considered correct (Osterwalder and Pigneur, 2010). High-low method

calculates for outlay estimate from end to end the implication of proceedings of manufacture

Performance Management 12

levels from past periods in the business. This makes the limited scope of applicability of the

method to business with prior account and thus this creates discrimination.

Linear regression analysis will overcome the limitation of the present method by making an

incorporation of all the activities and thus this method is more reliable. Linear regression can be

considered as an alternative for this method (Black et. al., 2012).

Conclusion

Break Even point of sale is £960,000.00 and margin of safety1, 040,000.00. It can be analyzed

from the breakeven chart and the margin of safety shows by how much the sales capacity must

fall before a loss is made to the organization. So, it can be analyzed that the organization is in

good position which can be seen from margin of safety. It can also be analyzed that being a

manager, one on a continuous basis strives to relate these elements in order to make the

maximum profit. Using High Low Method the profit of the company will be £360,000.00.

Comparison of the two proposals

Computations of Proposal 1

Particulars

Second Half

Year 2016

First Half Year

2017

£ £ £ £

Sales

200000

0 2470000

Direct Material

50000

0 475000

Direct Labour 40000 400000

levels from past periods in the business. This makes the limited scope of applicability of the

method to business with prior account and thus this creates discrimination.

Linear regression analysis will overcome the limitation of the present method by making an

incorporation of all the activities and thus this method is more reliable. Linear regression can be

considered as an alternative for this method (Black et. al., 2012).

Conclusion

Break Even point of sale is £960,000.00 and margin of safety1, 040,000.00. It can be analyzed

from the breakeven chart and the margin of safety shows by how much the sales capacity must

fall before a loss is made to the organization. So, it can be analyzed that the organization is in

good position which can be seen from margin of safety. It can also be analyzed that being a

manager, one on a continuous basis strives to relate these elements in order to make the

maximum profit. Using High Low Method the profit of the company will be £360,000.00.

Comparison of the two proposals

Computations of Proposal 1

Particulars

Second Half

Year 2016

First Half Year

2017

£ £ £ £

Sales

200000

0 2470000

Direct Material

50000

0 475000

Direct Labour 40000 400000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.