Performance Management Techniques for Manufacturing Company Report

VerifiedAdded on 2019/12/03

|13

|3882

|214

Report

AI Summary

This report examines performance management techniques for a rapidly growing manufacturing organization facing critical decisions about future growth. It provides an executive summary and an introduction to performance management, emphasizing its importance for organizational goal attainment and effective decision-making. The report delves into various techniques, including budgetary control, cost-volume-profit (CVP) analysis, pricing strategies, limiting factors, investment appraisal, and the balanced scorecard, along with their limitations in the context of the manufacturing company. It explores budgetary control's role in cost monitoring and operational planning, CVP analysis for assessing business opportunities, pricing decisions based on cost considerations, the impact of limiting factors on production, and the use of investment appraisal techniques for evaluating project feasibility. The report provides recommendations to the Board of Directors to aid in making informed decisions regarding cost control, profitability, and production improvement, using techniques such as budgetary control and investment appraisal.

Performance Management

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction to Performance Management .....................................................................................4

Budgetary control ............................................................................................................................4

Pricing .............................................................................................................................................6

Limiting factors ...............................................................................................................................7

Investment appraisal........................................................................................................................7

Balanced scorecard .........................................................................................................................9

Risk ...............................................................................................................................................10

2

Introduction to Performance Management .....................................................................................4

Budgetary control ............................................................................................................................4

Pricing .............................................................................................................................................6

Limiting factors ...............................................................................................................................7

Investment appraisal........................................................................................................................7

Balanced scorecard .........................................................................................................................9

Risk ...............................................................................................................................................10

2

EXECUTIVE SUMMARY

The present report is based on a scenario of a rapidly growing manufacturing

organisation which is faced with important decisions in respect of its’ future growth. The

company is required to take a viable decision which is best for the company. This report is going

to be produced for making Board of Directors understand with the techniques that are available

to making decision regarding future growth. Furthermore, Board is going to be provided with

information and recommendations that will enable them to take the relevant decisions. In the

report, it has been witnessed that techniques are used in business for making decision on cost

controlling, improving profitability and improve production.

3

The present report is based on a scenario of a rapidly growing manufacturing

organisation which is faced with important decisions in respect of its’ future growth. The

company is required to take a viable decision which is best for the company. This report is going

to be produced for making Board of Directors understand with the techniques that are available

to making decision regarding future growth. Furthermore, Board is going to be provided with

information and recommendations that will enable them to take the relevant decisions. In the

report, it has been witnessed that techniques are used in business for making decision on cost

controlling, improving profitability and improve production.

3

You're viewing a preview

Unlock full access by subscribing today!

Introduction

The success of a corporate entity depends on the effectiveness of decisions taken to the

organization. To a general phenomenon, performance management is a system that is used for

identifying improved ways to attain organizational goals as well as constant assessment to the

factors that are helpful in current level of performance in the organisation. The above mentioned

management aspect is quite important for goal-setting and developing metrics to identify

progress and areas of improvements that leads to effective decision making. However, there are

various techniques that are useful in making effective decision among various alternatives. There

is a strong planning and critical thinking behind every decision taken in respect with the future

growth and expansion. Decision making process require an effective technique that can identify

the long-term impacts of such decision. Here, in the reports some of the techniques along with

their limitations in respect with the scenario of a rapidly growing manufacturing organisation.

The discussed techniques are Budgetary control, Issues of CVP, Pricing, Limiting factors,

Investment appraisal, Balanced scorecard and RISK factor.

Range and depth of techniques

Budgetary control

The budgetary control is a technique that is used to identify the effectiveness of using

budgets so as to monitor and control costs and operations in a given accounting period. This

techniques is important for business to identify the future expenses associated with business

operations. To an further extent, budgetary control is said to be a process in which managers set

financial and performance goals using budgets and compare the actual results against the

standard one. The use of this technique is helpful to management for adjusting operational

performance of business. The mentioned manufacturing organization can compare budgeted and

actual figures with the help of aforesaid technique and can find out discrepancies along with

taking remedial measures to improve the performance in proper time. This technique will help

business in making decision over the use of cost controlling techniques. On the other hand,

budgetary control techniques is used for planning and co-ordination between production process.

The company can take decisions regrading improvement in operational performance that will

defiantly support future growth of business. The decision that are to be taken on the basis of

budgetary control technique include future planning along with setting up various budgets,

4

The success of a corporate entity depends on the effectiveness of decisions taken to the

organization. To a general phenomenon, performance management is a system that is used for

identifying improved ways to attain organizational goals as well as constant assessment to the

factors that are helpful in current level of performance in the organisation. The above mentioned

management aspect is quite important for goal-setting and developing metrics to identify

progress and areas of improvements that leads to effective decision making. However, there are

various techniques that are useful in making effective decision among various alternatives. There

is a strong planning and critical thinking behind every decision taken in respect with the future

growth and expansion. Decision making process require an effective technique that can identify

the long-term impacts of such decision. Here, in the reports some of the techniques along with

their limitations in respect with the scenario of a rapidly growing manufacturing organisation.

The discussed techniques are Budgetary control, Issues of CVP, Pricing, Limiting factors,

Investment appraisal, Balanced scorecard and RISK factor.

Range and depth of techniques

Budgetary control

The budgetary control is a technique that is used to identify the effectiveness of using

budgets so as to monitor and control costs and operations in a given accounting period. This

techniques is important for business to identify the future expenses associated with business

operations. To an further extent, budgetary control is said to be a process in which managers set

financial and performance goals using budgets and compare the actual results against the

standard one. The use of this technique is helpful to management for adjusting operational

performance of business. The mentioned manufacturing organization can compare budgeted and

actual figures with the help of aforesaid technique and can find out discrepancies along with

taking remedial measures to improve the performance in proper time. This technique will help

business in making decision over the use of cost controlling techniques. On the other hand,

budgetary control techniques is used for planning and co-ordination between production process.

The company can take decisions regrading improvement in operational performance that will

defiantly support future growth of business. The decision that are to be taken on the basis of

budgetary control technique include future planning along with setting up various budgets,

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

identifying of requirements that are essential to reach expected performance, ways to eliminate

wastes, increase profitability of business, anticipation of capital expenditure for future.

This techniques can also be used by manufacturing unit to centralise control system and

fixation of responsibility. However, there are certain limitations of budgetary control that can

affects the decision making of organization. The major limitation of aforesaid technique is

related to uncertain future. In this method, the budgets are prepared for future, thus, it is possible

that predictions may not come true. Furthermore. The budgets are prepared on assumptions and

continual revision of targets can reduce the value of budgets and involves huge monitory cost.

Nonetheless, application of budgetary control system is totally depends on the support of top

management, hence, lack of support from higher authorities will lead to collapse in entire

system. The manufacturing unit is recommended to use budgetary control tactics to support the

decision of controlling cost and managing financial performance of company in near future.

Issues of CVP (Cost-Volume-Profit Analysis)

The cost volume profit analysis is a tools that is used for making better business

decisions. This tool is also useful for managers in understanding more detailed and objective

ways of a decision so as to assess and predict course of business for the company as well as its

employees. In the mentioned scenario, manufacturing company has to evaluate each and every

decision on the basis of CVP analysis. The tool also provides advantages to answer special

pragmatic questions that are required to assess business opportunities to earn huge profits. The

manufacturing company can decide on company's breakeven point and can also assess how

future spending and production are going to contribute for success and failure. However, this

analysis tool is based on statistical models so provides opportunities to break down the decisions

into probabilities that is helpful in decision-making process. The manufacturing company can

have detailed snapshot of business activities with the help of cost and benefit analysis. This

analysis technique can provide information regarding costs needed to produce a product and final

amount of produced product. The manufacture can determine the future activities in case the

variables are adjusted. The company can also make decision in regard to transportation expenses

as well as possible changes in cost of material. However, it has been witnessed that variable costs

is significantly affected by bottom line and CVP analysis enable managers to establish an idea to

5

wastes, increase profitability of business, anticipation of capital expenditure for future.

This techniques can also be used by manufacturing unit to centralise control system and

fixation of responsibility. However, there are certain limitations of budgetary control that can

affects the decision making of organization. The major limitation of aforesaid technique is

related to uncertain future. In this method, the budgets are prepared for future, thus, it is possible

that predictions may not come true. Furthermore. The budgets are prepared on assumptions and

continual revision of targets can reduce the value of budgets and involves huge monitory cost.

Nonetheless, application of budgetary control system is totally depends on the support of top

management, hence, lack of support from higher authorities will lead to collapse in entire

system. The manufacturing unit is recommended to use budgetary control tactics to support the

decision of controlling cost and managing financial performance of company in near future.

Issues of CVP (Cost-Volume-Profit Analysis)

The cost volume profit analysis is a tools that is used for making better business

decisions. This tool is also useful for managers in understanding more detailed and objective

ways of a decision so as to assess and predict course of business for the company as well as its

employees. In the mentioned scenario, manufacturing company has to evaluate each and every

decision on the basis of CVP analysis. The tool also provides advantages to answer special

pragmatic questions that are required to assess business opportunities to earn huge profits. The

manufacturing company can decide on company's breakeven point and can also assess how

future spending and production are going to contribute for success and failure. However, this

analysis tool is based on statistical models so provides opportunities to break down the decisions

into probabilities that is helpful in decision-making process. The manufacturing company can

have detailed snapshot of business activities with the help of cost and benefit analysis. This

analysis technique can provide information regarding costs needed to produce a product and final

amount of produced product. The manufacture can determine the future activities in case the

variables are adjusted. The company can also make decision in regard to transportation expenses

as well as possible changes in cost of material. However, it has been witnessed that variable costs

is significantly affected by bottom line and CVP analysis enable managers to establish an idea to

5

improve future performance under the range of possibilities nonetheless, this can be seen as a

disadvantage for the manufacturers who are detail-oriented and precise in record data.

There are certain limitations associated with CVP approach. The major limitation

associated with aforesaid tool is of amount of information that is required to multi-product

operation. This is the reason for using this approach for a single product. However, for a

manufacturing organization this is the best decision making tool that is going to be used for

deciding on transportation expenses and possible changes held in cost of material. The issues

associated with cost volume analysis is that the company cannot identify the requirements

associated with multiple production. The limitation of cost benefit analysis is that the tool is

invaluable in demonstrating effect on an organisation's profit that are result of change in volume,

costs and selling prices. The use this method is seen limited because of various assumptions on

which this tools is based upon. The major assumption of these tools is that a single product or

multiple products are to be sold in constant mix.

Break even point

In accordance with this costing approach a point of sales is determined at which entire

costs of the business will be attained. At this point of situation, profit is zero as amount of sales

is equivalent to cost of business. It is the minimum point of sales of the business which is

required to be attained by the business entity. By making use of this analysis, organization can

set targets in order to attain the desired profits in volume as well as amount.

Pricing

Pricing decisions are the most crucial decisions that are to be take by a manufacturing

organisation to cover up the cost of production as well as making profits. The pricing decisions

are based on the cost of production as well as proportion of profits that are to be taken into

consideration. This is an major decision that decide success of an organisation. The

manufacturing organization can take pricing decision on the basis of variable and fixed cost.

This is been evident that the pricing decision are the most crucial for the organization as well as

it is critical decision as per the marketers. This marketing decisions is to be taken by the firm so

as to attain higher profits. However, a major reason for which company calculates total cost of

production and adds some profit figures to make process. This is the major element of marketing

mix and has a crucial impact on success of business. The pricing decision are to be taken while

6

disadvantage for the manufacturers who are detail-oriented and precise in record data.

There are certain limitations associated with CVP approach. The major limitation

associated with aforesaid tool is of amount of information that is required to multi-product

operation. This is the reason for using this approach for a single product. However, for a

manufacturing organization this is the best decision making tool that is going to be used for

deciding on transportation expenses and possible changes held in cost of material. The issues

associated with cost volume analysis is that the company cannot identify the requirements

associated with multiple production. The limitation of cost benefit analysis is that the tool is

invaluable in demonstrating effect on an organisation's profit that are result of change in volume,

costs and selling prices. The use this method is seen limited because of various assumptions on

which this tools is based upon. The major assumption of these tools is that a single product or

multiple products are to be sold in constant mix.

Break even point

In accordance with this costing approach a point of sales is determined at which entire

costs of the business will be attained. At this point of situation, profit is zero as amount of sales

is equivalent to cost of business. It is the minimum point of sales of the business which is

required to be attained by the business entity. By making use of this analysis, organization can

set targets in order to attain the desired profits in volume as well as amount.

Pricing

Pricing decisions are the most crucial decisions that are to be take by a manufacturing

organisation to cover up the cost of production as well as making profits. The pricing decisions

are based on the cost of production as well as proportion of profits that are to be taken into

consideration. This is an major decision that decide success of an organisation. The

manufacturing organization can take pricing decision on the basis of variable and fixed cost.

This is been evident that the pricing decision are the most crucial for the organization as well as

it is critical decision as per the marketers. This marketing decisions is to be taken by the firm so

as to attain higher profits. However, a major reason for which company calculates total cost of

production and adds some profit figures to make process. This is the major element of marketing

mix and has a crucial impact on success of business. The pricing decision are to be taken while

6

You're viewing a preview

Unlock full access by subscribing today!

keeping future profits into consideration. There are two major factors on which pricing decision

can be taken such as objectives of profit maximization and cost of production. The higher cost

lead to high prices on the other hand lower cost defined lower prices. On the basis of market

condition, the company takes effective pricing decisions. In respect with the manufacturing

organization, cost is the major factor that helps in deciding prices of products. There are two

types of cost associated with the manufacturing units such as variable cost and fixed cost. The

pricing decision are based on cost of unit while adding profit margin of the company. The

manufacturing unit is recommended to use cost based pricing which will be beneficial in

covering all types of cost that have been incurred in production process. For example

manufacturing company can set price for the organization by making use of mark up strategy. As

per this approach, percent of profit can be added is total cost in order to attain the desired profit.

Limiting factors

The major issue of production units is associated with limiting factors. It has been

witnessed that the company requires sufficient raw material or resources to compete the

production. The future decisions of business are also associated with availability of resources

with such organization. Limiting factor is known as the factor that restricts a corporate entity for

completing the organizational activities in the most optimal manner. It can also be said that

limiting factor are one that are limited and are not freely available with the manufacturing unit.

The limiting factor is the major issue that is associated with the organization. Within the present

case scenario limiting factor can be labour time, raw material, machine hours and well as space.

For an example , it can be said that in case sales demand excess as compared to production

capacity, there may not be having enough resources so as to produce products to meet the market

demand. The organization can probably remove the production constraints by acquiring

additional resources in case they are available in the external environment. The use of limiting

factor allows company to maximize profits at the time of obtaining the greatest possible

contribution to profit for every time. The use of limiting factor analysis is done in the situation

when only one limiting factor is there, which is the major limitation of business and restricts

organisation's activities. In order to overcome the issue of limited factor and to improve the

production process in future, the manufacturing organization can make use of linear

programming .

7

can be taken such as objectives of profit maximization and cost of production. The higher cost

lead to high prices on the other hand lower cost defined lower prices. On the basis of market

condition, the company takes effective pricing decisions. In respect with the manufacturing

organization, cost is the major factor that helps in deciding prices of products. There are two

types of cost associated with the manufacturing units such as variable cost and fixed cost. The

pricing decision are based on cost of unit while adding profit margin of the company. The

manufacturing unit is recommended to use cost based pricing which will be beneficial in

covering all types of cost that have been incurred in production process. For example

manufacturing company can set price for the organization by making use of mark up strategy. As

per this approach, percent of profit can be added is total cost in order to attain the desired profit.

Limiting factors

The major issue of production units is associated with limiting factors. It has been

witnessed that the company requires sufficient raw material or resources to compete the

production. The future decisions of business are also associated with availability of resources

with such organization. Limiting factor is known as the factor that restricts a corporate entity for

completing the organizational activities in the most optimal manner. It can also be said that

limiting factor are one that are limited and are not freely available with the manufacturing unit.

The limiting factor is the major issue that is associated with the organization. Within the present

case scenario limiting factor can be labour time, raw material, machine hours and well as space.

For an example , it can be said that in case sales demand excess as compared to production

capacity, there may not be having enough resources so as to produce products to meet the market

demand. The organization can probably remove the production constraints by acquiring

additional resources in case they are available in the external environment. The use of limiting

factor allows company to maximize profits at the time of obtaining the greatest possible

contribution to profit for every time. The use of limiting factor analysis is done in the situation

when only one limiting factor is there, which is the major limitation of business and restricts

organisation's activities. In order to overcome the issue of limited factor and to improve the

production process in future, the manufacturing organization can make use of linear

programming .

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Investment appraisal

Investment appraisal techniques are also called as capital budgeting techniques that are

the most famous in corporate world for supporting effective decisions of a business. Wherever,

company thinks about investment, it can go for search available profitable options. The above

mentioned techniques are used to identify the best project among various alternatives. In other

words, investment appraisal techniques are used to evaluate the feasibility of business projects.

In respect with the present case scenario, manufacturing organizations can identify the feasibility

of investment by using traditional payback period (PB) or more sophisticated appraisal tactics

such as discounted cash flow (DCF) methods. There are to in net present value (NPV), internal

rate of return (IRR), profitability index. The importance of investment appraisal technique is to

identify the optimal product in which business can done investments. Among various techniques

discounted cash flows are the most important tactics of investment appraisal. This is an

important approach that is used to identify a ways of valuing future returns from an investment

through assessing the values of returns from today's value. It can be said that the cost of funds

are to be tied within a possible project through considering timing of cash flows. The

manufacturing company can take decision of business expansion by using investment appraisal

methods as well as the use of such methods helps in undertaking a capital allocation process. The

available projects are ranked under such valuation tactic which is helpful in selecting the best

project for the company. However, the limitation of such tactics is that discounting value

methods involve opportunity cost of those projects that add significant value to the company but

they cannot be financed because of lack of sufficient funds to undertake such projects.

In respect with the present case, the company can take decision in respect with opening

manufacturing units to available locations. The future decision can be taken in terms of choosing

location for the business. The best tactics of assessing a project on the basis of time value and

money is Net present value method. NPV is the famous method to take investment decision. In

respect with the present case a scenario is chosen in which an manufacturing company is going

to identify the locations for business expansion. Illustration : The possible case flow from both

the investment in different years is as follows :

Project table :

Year Location A Location B

2015 10000 10000

8

Investment appraisal techniques are also called as capital budgeting techniques that are

the most famous in corporate world for supporting effective decisions of a business. Wherever,

company thinks about investment, it can go for search available profitable options. The above

mentioned techniques are used to identify the best project among various alternatives. In other

words, investment appraisal techniques are used to evaluate the feasibility of business projects.

In respect with the present case scenario, manufacturing organizations can identify the feasibility

of investment by using traditional payback period (PB) or more sophisticated appraisal tactics

such as discounted cash flow (DCF) methods. There are to in net present value (NPV), internal

rate of return (IRR), profitability index. The importance of investment appraisal technique is to

identify the optimal product in which business can done investments. Among various techniques

discounted cash flows are the most important tactics of investment appraisal. This is an

important approach that is used to identify a ways of valuing future returns from an investment

through assessing the values of returns from today's value. It can be said that the cost of funds

are to be tied within a possible project through considering timing of cash flows. The

manufacturing company can take decision of business expansion by using investment appraisal

methods as well as the use of such methods helps in undertaking a capital allocation process. The

available projects are ranked under such valuation tactic which is helpful in selecting the best

project for the company. However, the limitation of such tactics is that discounting value

methods involve opportunity cost of those projects that add significant value to the company but

they cannot be financed because of lack of sufficient funds to undertake such projects.

In respect with the present case, the company can take decision in respect with opening

manufacturing units to available locations. The future decision can be taken in terms of choosing

location for the business. The best tactics of assessing a project on the basis of time value and

money is Net present value method. NPV is the famous method to take investment decision. In

respect with the present case a scenario is chosen in which an manufacturing company is going

to identify the locations for business expansion. Illustration : The possible case flow from both

the investment in different years is as follows :

Project table :

Year Location A Location B

2015 10000 10000

8

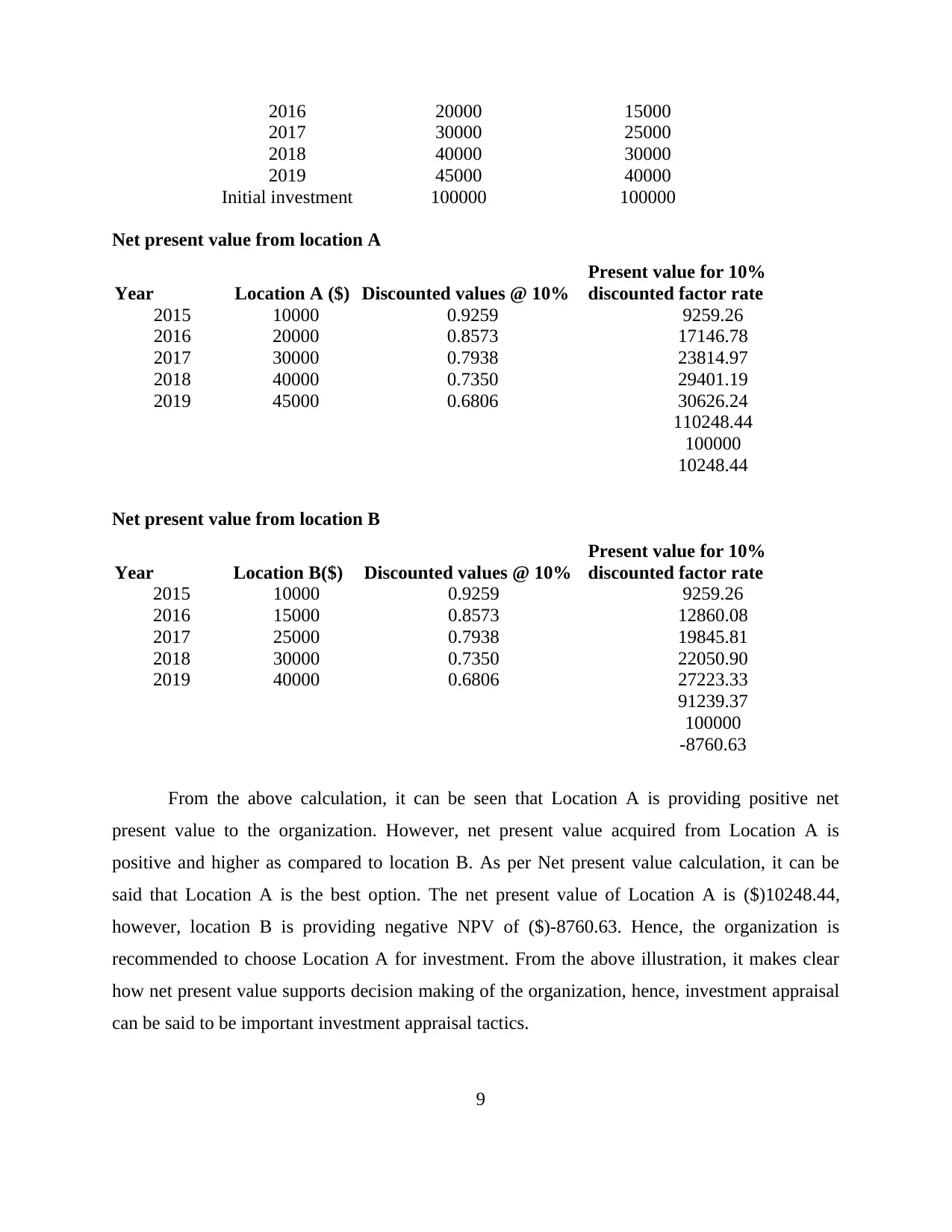

2016 20000 15000

2017 30000 25000

2018 40000 30000

2019 45000 40000

Initial investment 100000 100000

Net present value from location A

Year Location A ($) Discounted values @ 10%

Present value for 10%

discounted factor rate

2015 10000 0.9259 9259.26

2016 20000 0.8573 17146.78

2017 30000 0.7938 23814.97

2018 40000 0.7350 29401.19

2019 45000 0.6806 30626.24

110248.44

100000

10248.44

Net present value from location B

Year Location B($) Discounted values @ 10%

Present value for 10%

discounted factor rate

2015 10000 0.9259 9259.26

2016 15000 0.8573 12860.08

2017 25000 0.7938 19845.81

2018 30000 0.7350 22050.90

2019 40000 0.6806 27223.33

91239.37

100000

-8760.63

From the above calculation, it can be seen that Location A is providing positive net

present value to the organization. However, net present value acquired from Location A is

positive and higher as compared to location B. As per Net present value calculation, it can be

said that Location A is the best option. The net present value of Location A is ($)10248.44,

however, location B is providing negative NPV of ($)-8760.63. Hence, the organization is

recommended to choose Location A for investment. From the above illustration, it makes clear

how net present value supports decision making of the organization, hence, investment appraisal

can be said to be important investment appraisal tactics.

9

2017 30000 25000

2018 40000 30000

2019 45000 40000

Initial investment 100000 100000

Net present value from location A

Year Location A ($) Discounted values @ 10%

Present value for 10%

discounted factor rate

2015 10000 0.9259 9259.26

2016 20000 0.8573 17146.78

2017 30000 0.7938 23814.97

2018 40000 0.7350 29401.19

2019 45000 0.6806 30626.24

110248.44

100000

10248.44

Net present value from location B

Year Location B($) Discounted values @ 10%

Present value for 10%

discounted factor rate

2015 10000 0.9259 9259.26

2016 15000 0.8573 12860.08

2017 25000 0.7938 19845.81

2018 30000 0.7350 22050.90

2019 40000 0.6806 27223.33

91239.37

100000

-8760.63

From the above calculation, it can be seen that Location A is providing positive net

present value to the organization. However, net present value acquired from Location A is

positive and higher as compared to location B. As per Net present value calculation, it can be

said that Location A is the best option. The net present value of Location A is ($)10248.44,

however, location B is providing negative NPV of ($)-8760.63. Hence, the organization is

recommended to choose Location A for investment. From the above illustration, it makes clear

how net present value supports decision making of the organization, hence, investment appraisal

can be said to be important investment appraisal tactics.

9

You're viewing a preview

Unlock full access by subscribing today!

Balanced scorecard

Balance scorecard is a a tool that helps measuring the performance of company measured

in accordance with four major prescriptive such as financial, Internal business process

perspective, Learning and growth perspective as well as customer perspective. This is an helpful

tool to identify the factors that helps in transforming the strategy of an corporate entity into real

actions. However, it has been witnessed that balance scorecard is helpful measuring performance

of business intro various aspects. On the basis of balance score card, organization can take

decision on key performance indicators of business. For a corporate entity, balance score card is

seen to be an matrix that is used for evaluating factors that are crucial to attain success. It can be

seen that organizations have their own KPIs that are significantly based on goals and objectives

of business. In respect with the manufacturing organization, this tool can be helpful in tracking

out the objectives, targets, measures and initiatives of the company under four perspectives that

are mentioned in above points. The organization can make effective decisions on financial

objectives and can decide the action plan that is crucial to meet them. The decision regarding

capital allocation to the manufacturing activities can be decide on through using balance score

cared as a tactic. In other words, the strategies of company implementation and execution

process are to be measured and specific decision regarding improving bottom line operation can

be taken out. In regard to the customers perspective, this tool is useful in measuring the segment

of the market and target groups for which product are to be manufactured. However, the internal

process of the business and associated growth is to be measured. The organization can use such

strategy to make decision in regard to operations management, product safety, innovation,

community development and customers needs etc. From the perspective of learning and growth,

the corporate entity can improve learning and making as well as can improve production process

so as to make optimal products. However, it can be said that with the help of balance score card

organization can take effective decision to improve operating efficiency as well as can penetrate

the market.

Risk

Description of risk

Risk is the major factor that have been witnessed a base of decision making. The risk

associated with the investment projects is the major factor that affects decision making process

10

Balance scorecard is a a tool that helps measuring the performance of company measured

in accordance with four major prescriptive such as financial, Internal business process

perspective, Learning and growth perspective as well as customer perspective. This is an helpful

tool to identify the factors that helps in transforming the strategy of an corporate entity into real

actions. However, it has been witnessed that balance scorecard is helpful measuring performance

of business intro various aspects. On the basis of balance score card, organization can take

decision on key performance indicators of business. For a corporate entity, balance score card is

seen to be an matrix that is used for evaluating factors that are crucial to attain success. It can be

seen that organizations have their own KPIs that are significantly based on goals and objectives

of business. In respect with the manufacturing organization, this tool can be helpful in tracking

out the objectives, targets, measures and initiatives of the company under four perspectives that

are mentioned in above points. The organization can make effective decisions on financial

objectives and can decide the action plan that is crucial to meet them. The decision regarding

capital allocation to the manufacturing activities can be decide on through using balance score

cared as a tactic. In other words, the strategies of company implementation and execution

process are to be measured and specific decision regarding improving bottom line operation can

be taken out. In regard to the customers perspective, this tool is useful in measuring the segment

of the market and target groups for which product are to be manufactured. However, the internal

process of the business and associated growth is to be measured. The organization can use such

strategy to make decision in regard to operations management, product safety, innovation,

community development and customers needs etc. From the perspective of learning and growth,

the corporate entity can improve learning and making as well as can improve production process

so as to make optimal products. However, it can be said that with the help of balance score card

organization can take effective decision to improve operating efficiency as well as can penetrate

the market.

Risk

Description of risk

Risk is the major factor that have been witnessed a base of decision making. The risk

associated with the investment projects is the major factor that affects decision making process

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of an organization. Within in decision making process the risk is evaluated under conditions of

risk in the forms of high, moderate and low. However, the returns of an investment project

always associated with a project. In respect with the project, it has been evident that quantity of

risk is equal to the sum of probabilities of occurring risky outcomes. With a high level of risk,

there are high returns associated which are further multiplied by anticipated loss on such

investment.

Types of risk

Risk for manufacturing companies can be bifurcated into operational risks, technological,

financial and social risks. Operation risk is related to the production process. Example of

operational risk is mechanical failure which can make reduction in the productivity of business.

Technological risks refer to the failure in applied techniques in the business organization. For

example, applicability of inappropriate technology can lead to the high faulty products that will

have adverse impact on the profitability. Financial risks are considered to be pure risks that can

be occurred in any business entity. Example of financial risk is increase in inflation rate and

interest rates of loans. Social risk is linked to the market risk. Example of this risk is change in

taste and preference of customers.

Risk management

The organization always tries to reduce the risk that are associated with the different

projects and try to chose the project that ate having low risk and higher returns. In respect with

the present case of manufacturing company, risk is assassinated with each and every decision,

hence, it is the major factor that decide the returns of business. The management's risk appetite

ability is said to the maker factor of company to absorb, transfer, and manage risk after

identification of risk hence, decisions are to be taken while identifying the extent of risk

assassinated with the projects

Performance management

Financial performance indicators

Financial performance indicators are those through which company can measure its

performance in terms of finance. It thus, helps in effective performance management. Through

this company can assess their growth and progress in term of finance. Some of the financial

performance indicators are describes below:

11

risk in the forms of high, moderate and low. However, the returns of an investment project

always associated with a project. In respect with the project, it has been evident that quantity of

risk is equal to the sum of probabilities of occurring risky outcomes. With a high level of risk,

there are high returns associated which are further multiplied by anticipated loss on such

investment.

Types of risk

Risk for manufacturing companies can be bifurcated into operational risks, technological,

financial and social risks. Operation risk is related to the production process. Example of

operational risk is mechanical failure which can make reduction in the productivity of business.

Technological risks refer to the failure in applied techniques in the business organization. For

example, applicability of inappropriate technology can lead to the high faulty products that will

have adverse impact on the profitability. Financial risks are considered to be pure risks that can

be occurred in any business entity. Example of financial risk is increase in inflation rate and

interest rates of loans. Social risk is linked to the market risk. Example of this risk is change in

taste and preference of customers.

Risk management

The organization always tries to reduce the risk that are associated with the different

projects and try to chose the project that ate having low risk and higher returns. In respect with

the present case of manufacturing company, risk is assassinated with each and every decision,

hence, it is the major factor that decide the returns of business. The management's risk appetite

ability is said to the maker factor of company to absorb, transfer, and manage risk after

identification of risk hence, decisions are to be taken while identifying the extent of risk

assassinated with the projects

Performance management

Financial performance indicators

Financial performance indicators are those through which company can measure its

performance in terms of finance. It thus, helps in effective performance management. Through

this company can assess their growth and progress in term of finance. Some of the financial

performance indicators are describes below:

11

Profits: If the profits of the company is growing than it is a good indicator for the firm

that performance is going in an effective manner. While, the downfall of profit indicates

that performance is not up to the mark and performance management need to take extra

concern.

Stock Turnover Ratio: If the ratio is lower than it indicated that firm sells the inventory

on a faster rate and thus, this is good indicator and company is financially sound. On the

other hand, ratio level is high than company's financial status is not good.

Non financial performance indicators

Those indicators which are not in quantifiable terms are termed as non financial

performance indicators. Some of them are described below:

Employee Performance: The effective performance of all the employees leads to better

performance of a firm and it shows the good sign for the company's progress.

Quality: If the quality of products are of utmost quality then it shows a good sign for the

company's progress.

Customer Satisfaction: High satisfaction among customer can be measured through

feedbacks and through this performance of a manufacturing unit can be measured.

Divisional performance management

For the management of performance of manufacturing company in an effective manner

entities are required to implement approach of divisional performance management. In this

aspect, divisional managers are only responsible for the controllable factors. With this approach,

divisional managers will be held accountable for the factors that can be influenced by others. It

will provide better structure for the accomplishment of operational activities. In addition to this,

there will be better performance indicators for the measure of performance.

Transfer pricing

Transfer pricing is approach of setting price for goods and services sold by organization

to their controlled entities or by one department to the another department. Main objective of this

approach to determine separate profits for the each division. With the applicability of this

12

that performance is going in an effective manner. While, the downfall of profit indicates

that performance is not up to the mark and performance management need to take extra

concern.

Stock Turnover Ratio: If the ratio is lower than it indicated that firm sells the inventory

on a faster rate and thus, this is good indicator and company is financially sound. On the

other hand, ratio level is high than company's financial status is not good.

Non financial performance indicators

Those indicators which are not in quantifiable terms are termed as non financial

performance indicators. Some of them are described below:

Employee Performance: The effective performance of all the employees leads to better

performance of a firm and it shows the good sign for the company's progress.

Quality: If the quality of products are of utmost quality then it shows a good sign for the

company's progress.

Customer Satisfaction: High satisfaction among customer can be measured through

feedbacks and through this performance of a manufacturing unit can be measured.

Divisional performance management

For the management of performance of manufacturing company in an effective manner

entities are required to implement approach of divisional performance management. In this

aspect, divisional managers are only responsible for the controllable factors. With this approach,

divisional managers will be held accountable for the factors that can be influenced by others. It

will provide better structure for the accomplishment of operational activities. In addition to this,

there will be better performance indicators for the measure of performance.

Transfer pricing

Transfer pricing is approach of setting price for goods and services sold by organization

to their controlled entities or by one department to the another department. Main objective of this

approach to determine separate profits for the each division. With the applicability of this

12

You're viewing a preview

Unlock full access by subscribing today!

approach, manufacturing company can make better decisions in timely manner because of the

proximity of local conditions. In addition to this, top managers of the company will not be

distracted by local decision problems and routines. Motivation level of managerial persons will

be increased as they will have better control on the results.

13

proximity of local conditions. In addition to this, top managers of the company will not be

distracted by local decision problems and routines. Motivation level of managerial persons will

be increased as they will have better control on the results.

13

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.