Personal Finance Assignment, Course Name, Semester 2017, University

VerifiedAdded on 2020/03/02

|14

|2469

|47

Homework Assignment

AI Summary

This personal finance assignment delves into various aspects of financial management, starting with an overview of financial literacy in Canada and the need for public education on the subject. The assignment then addresses debt and taxation, providing guidance on how to avoid tax scams and protect personal information. It further explores fiscal goals, illustrating the importance of planning major investments with a cost-benefit analysis and adaptation strategies. The assignment also covers retirement planning, including financial needs estimation, savings plans, and investment avenues. Finally, it reflects on the course's impact, highlighting key learnings in planning, forecasting, taxation, and investment strategies to achieve maximum results with minimal resources. The document includes references to relevant financial literature.

2017

Personal Finance Assignment

Personal Finance Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 20August, 2017.

1 | P a g e

By student name

Professor

University

Date: 20August, 2017.

1 | P a g e

2

Contents

Answer to Question No 1……………………………………………………...3

Answer to Question No 2……………………………………………………...4

Answer to Question No 4……………………………………………………...6

Answer to Question No 5……………………………………………………...8

Answer to Question No 7……………………………………………………...10

References...........................................................................................................12

2 | P a g e

Contents

Answer to Question No 1……………………………………………………...3

Answer to Question No 2……………………………………………………...4

Answer to Question No 4……………………………………………………...6

Answer to Question No 5……………………………………………………...8

Answer to Question No 7……………………………………………………...10

References...........................................................................................................12

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Section One – Financial Literacy in Canada

Understanding Personal Finance is the need of the hour. Not only understanding, but

thorough implementation and learning is required, to implement it effectively in real life. Most of

the Canadian population lacks financial literacy. They need to be trained at the right time such

that they are able to set out personal objectives and are able to take their decisions, based on the

present circumstances. It will help them from not getting cheated and will keep their finances

safe. For this a radical change is required throughout the country. It can be achieved with the

Federal government and several NGO organizations joining hands together and working in this

sector. They can start with educating the people the about the need of it and can teach them ways

of handling the personal finance, its planning and execution. Voluntary self-education is difficult

and hence the need arises to motivate them through some incentive, which can be rewards and

awards in various forms. People need to be educated about the “budget” and how to use it in the

personal life such that people use the limited resources available with them in an effective way.

Moreover, they should be trained at young age only so that with passing age, they are able to

plan better for their post retirement and hence are not dependent on others for finances. Also,

most of the population is unaware of what exactly “insurance” is all about; they need to be made

aware of the same. Moreover, it is the responsibility of the government to bring the information

to the people from the trusted sources in order to improve the financial and economic status of

the individuals. Besides this, every other situation or the transaction has a concept of trade off or

opportunity cost involved. They need to well-trained about these terms so that they make the

right choices.1 It is thus important that people apply efforts from their end to understand the

1 (Luu, Lowe, Butler, & Byme, 2017)

3 | P a g e

Section One – Financial Literacy in Canada

Understanding Personal Finance is the need of the hour. Not only understanding, but

thorough implementation and learning is required, to implement it effectively in real life. Most of

the Canadian population lacks financial literacy. They need to be trained at the right time such

that they are able to set out personal objectives and are able to take their decisions, based on the

present circumstances. It will help them from not getting cheated and will keep their finances

safe. For this a radical change is required throughout the country. It can be achieved with the

Federal government and several NGO organizations joining hands together and working in this

sector. They can start with educating the people the about the need of it and can teach them ways

of handling the personal finance, its planning and execution. Voluntary self-education is difficult

and hence the need arises to motivate them through some incentive, which can be rewards and

awards in various forms. People need to be educated about the “budget” and how to use it in the

personal life such that people use the limited resources available with them in an effective way.

Moreover, they should be trained at young age only so that with passing age, they are able to

plan better for their post retirement and hence are not dependent on others for finances. Also,

most of the population is unaware of what exactly “insurance” is all about; they need to be made

aware of the same. Moreover, it is the responsibility of the government to bring the information

to the people from the trusted sources in order to improve the financial and economic status of

the individuals. Besides this, every other situation or the transaction has a concept of trade off or

opportunity cost involved. They need to well-trained about these terms so that they make the

right choices.1 It is thus important that people apply efforts from their end to understand the

1 (Luu, Lowe, Butler, & Byme, 2017)

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

situation and puts in their own efforts and the government needs to provide the necessary

guidance as and when needed.

Section Two – Debt and Taxes: Answer to Question 3

There have been a large number of people being subject to the tax scams these days in

Canada via an email message or a fake phone call. The foremost reason for being cheated is the

unawareness and lack of the subject knowledge on the taxation front. They are generally

fraudsters impersonating themselves to be from Canada Revenue Agency and will either be

using the link to be clicked by the user to pay the balance tax or there would be calls from

unknown numbers to share the private banking or credit card information in order to complete

the yearly tax filing procedure. Here is few ways to protect you:

1. CRA never asks for the personal data via a phone call or an email link, there would be

proper communication via the letter. So people should take note of the same and try not

to fall prey to such calls.

2. They would never demand the penalty or the left over tax in the form of gift cards, or

goods or exactly credit card.

3. They would never inquire the Social Insurance Number. It is a private number and is not

needed by the CRA agents when it comes to tax filling.

4. There would be a confirmation window for the present tax status before further tax

payment is asked for. So the users must look for the validity of the same and then take

important decision to pay.

4 | P a g e

situation and puts in their own efforts and the government needs to provide the necessary

guidance as and when needed.

Section Two – Debt and Taxes: Answer to Question 3

There have been a large number of people being subject to the tax scams these days in

Canada via an email message or a fake phone call. The foremost reason for being cheated is the

unawareness and lack of the subject knowledge on the taxation front. They are generally

fraudsters impersonating themselves to be from Canada Revenue Agency and will either be

using the link to be clicked by the user to pay the balance tax or there would be calls from

unknown numbers to share the private banking or credit card information in order to complete

the yearly tax filing procedure. Here is few ways to protect you:

1. CRA never asks for the personal data via a phone call or an email link, there would be

proper communication via the letter. So people should take note of the same and try not

to fall prey to such calls.

2. They would never demand the penalty or the left over tax in the form of gift cards, or

goods or exactly credit card.

3. They would never inquire the Social Insurance Number. It is a private number and is not

needed by the CRA agents when it comes to tax filling.

4. There would be a confirmation window for the present tax status before further tax

payment is asked for. So the users must look for the validity of the same and then take

important decision to pay.

4 | P a g e

5

5. In case inadvertently the bank account information is shared over the mail to a suspicious

recipient, the person should take help of the bank to block his/her account so that the

access is restricted2. This will help in keeping the account safe and also help the

government in getting hold of these fake imperators.

2 (Melvin & Norrbin, 2017)

5 | P a g e

5. In case inadvertently the bank account information is shared over the mail to a suspicious

recipient, the person should take help of the bank to block his/her account so that the

access is restricted2. This will help in keeping the account safe and also help the

government in getting hold of these fake imperators.

2 (Melvin & Norrbin, 2017)

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Section Three – Fiscal Goals: Answer to Question 4

Once a major investment or expenditure is to be incurred, planning is a pre requisite. It is

important to properly plan all the things, beforehand so that the results are effective and as per

the required standards. There can be multiple investments examples from real life, like

investment for a course, buying a new house or a major capital expenditure for the business. A

lot of money is needed for any of such activity. Thus it is important that before investing the

same, proper planning must be done to avoid discrepancies. The aim should be to make the most

profitable investment that will help in getting the best results. An illustrative example of such

plan is earmarked below:

1. A statement of goal: A machinery is to be purchased for use in business, the same is

to be imported from outside Canada and a down payment of 50% of the total cost is

required to be made upfront. The same can be paid through Letter of Credit or direct

wire transfer. A cost benefit analysis needs to be done.

2. Expected cost of purchase: The machinery will cost at around CAD 200,000 out of

which a total of CAD 100,000 will needs to be paid as advance through the bank.

3. Savings plan with the estimates and expected rate of return: The expected rate of

return from the project investment is expected to be 20-22% over the period of 5

years from initial investment. The investment will break even in the 3rd year using the

estimated discounted rate of 10%. Since this is an integral investment to the whole

project, it will results in economies of scale and the productivity and the revenue will

increase on account of it. The rest 50% of the amount is to be paid in the equal

installment amount over the time horizon of next 3 years. In the calculation attached

6 | P a g e

Section Three – Fiscal Goals: Answer to Question 4

Once a major investment or expenditure is to be incurred, planning is a pre requisite. It is

important to properly plan all the things, beforehand so that the results are effective and as per

the required standards. There can be multiple investments examples from real life, like

investment for a course, buying a new house or a major capital expenditure for the business. A

lot of money is needed for any of such activity. Thus it is important that before investing the

same, proper planning must be done to avoid discrepancies. The aim should be to make the most

profitable investment that will help in getting the best results. An illustrative example of such

plan is earmarked below:

1. A statement of goal: A machinery is to be purchased for use in business, the same is

to be imported from outside Canada and a down payment of 50% of the total cost is

required to be made upfront. The same can be paid through Letter of Credit or direct

wire transfer. A cost benefit analysis needs to be done.

2. Expected cost of purchase: The machinery will cost at around CAD 200,000 out of

which a total of CAD 100,000 will needs to be paid as advance through the bank.

3. Savings plan with the estimates and expected rate of return: The expected rate of

return from the project investment is expected to be 20-22% over the period of 5

years from initial investment. The investment will break even in the 3rd year using the

estimated discounted rate of 10%. Since this is an integral investment to the whole

project, it will results in economies of scale and the productivity and the revenue will

increase on account of it. The rest 50% of the amount is to be paid in the equal

installment amount over the time horizon of next 3 years. In the calculation attached

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

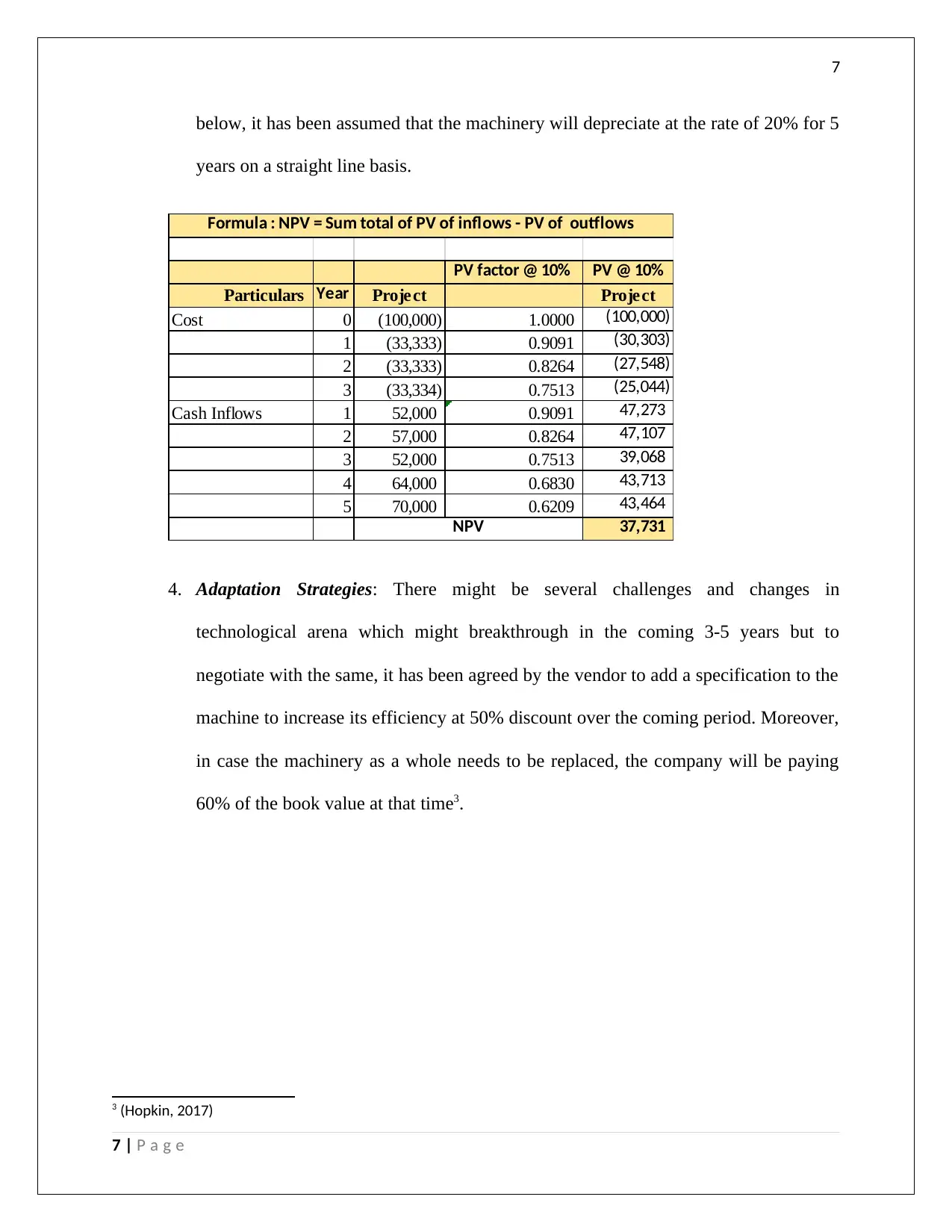

below, it has been assumed that the machinery will depreciate at the rate of 20% for 5

years on a straight line basis.

PV factor @ 10% PV @ 10%

Particulars Year Project Project

Cost 0 (100,000) 1.0000 (100,000)

1 (33,333) 0.9091 (30,303)

2 (33,333) 0.8264 (27,548)

3 (33,334) 0.7513 (25,044)

Cash Inflows 1 52,000 0.9091 47,273

2 57,000 0.8264 47,107

3 52,000 0.7513 39,068

4 64,000 0.6830 43,713

5 70,000 0.6209 43,464

37,731

Formula : NPV = Sum total of PV of inflows - PV of outflows

NPV

4. Adaptation Strategies: There might be several challenges and changes in

technological arena which might breakthrough in the coming 3-5 years but to

negotiate with the same, it has been agreed by the vendor to add a specification to the

machine to increase its efficiency at 50% discount over the coming period. Moreover,

in case the machinery as a whole needs to be replaced, the company will be paying

60% of the book value at that time3.

3 (Hopkin, 2017)

7 | P a g e

below, it has been assumed that the machinery will depreciate at the rate of 20% for 5

years on a straight line basis.

PV factor @ 10% PV @ 10%

Particulars Year Project Project

Cost 0 (100,000) 1.0000 (100,000)

1 (33,333) 0.9091 (30,303)

2 (33,333) 0.8264 (27,548)

3 (33,334) 0.7513 (25,044)

Cash Inflows 1 52,000 0.9091 47,273

2 57,000 0.8264 47,107

3 52,000 0.7513 39,068

4 64,000 0.6830 43,713

5 70,000 0.6209 43,464

37,731

Formula : NPV = Sum total of PV of inflows - PV of outflows

NPV

4. Adaptation Strategies: There might be several challenges and changes in

technological arena which might breakthrough in the coming 3-5 years but to

negotiate with the same, it has been agreed by the vendor to add a specification to the

machine to increase its efficiency at 50% discount over the coming period. Moreover,

in case the machinery as a whole needs to be replaced, the company will be paying

60% of the book value at that time3.

3 (Hopkin, 2017)

7 | P a g e

8

Section four: Answer to Question 5

Retirement is inevitable in a salaried person’s life and it has to be planned really well in

advance in order to avoid future contingencies and risks. The retirement strategy needs to be

planned ideally at the age of 25-30 years and a planned investment is needed to yield the best

return. Considering the investment avenues & the best rates available in the Canadian market,

following is the proposed proposition to save for retirement:

i. I am planning to retire at around 55-58 years, this would be the ideal time because

the family would be well established and the public policy on retirement would

also be in effect at that time as per the law. In case I retire anytime before that, I

would like to move towards social service and make a step ahead in the personal

handicraft works, which needs minimal investment but would require skilled

hands and marketing. In this way I will keep myself occupied and will also retain

that sense of independence.

ii. Estimation of the financial needs and expenses post retirement: On the outset, the

basic requirements can be fulfilled in approximately CAD 500, other social

requirements may vary from CAD 200-300, besides all this, and there may be an

ad requirement like medical expenses, one time expenditure which again may be

tune of CAD 200-300. To plan other personal business, a short term investment of

CAD 1000-2000 may be required to open the start up. Since, everything would be

specifically machine made, investment in machinery would be required and there

would be less of lab our costs.

8 | P a g e

Section four: Answer to Question 5

Retirement is inevitable in a salaried person’s life and it has to be planned really well in

advance in order to avoid future contingencies and risks. The retirement strategy needs to be

planned ideally at the age of 25-30 years and a planned investment is needed to yield the best

return. Considering the investment avenues & the best rates available in the Canadian market,

following is the proposed proposition to save for retirement:

i. I am planning to retire at around 55-58 years, this would be the ideal time because

the family would be well established and the public policy on retirement would

also be in effect at that time as per the law. In case I retire anytime before that, I

would like to move towards social service and make a step ahead in the personal

handicraft works, which needs minimal investment but would require skilled

hands and marketing. In this way I will keep myself occupied and will also retain

that sense of independence.

ii. Estimation of the financial needs and expenses post retirement: On the outset, the

basic requirements can be fulfilled in approximately CAD 500, other social

requirements may vary from CAD 200-300, besides all this, and there may be an

ad requirement like medical expenses, one time expenditure which again may be

tune of CAD 200-300. To plan other personal business, a short term investment of

CAD 1000-2000 may be required to open the start up. Since, everything would be

specifically machine made, investment in machinery would be required and there

would be less of lab our costs.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

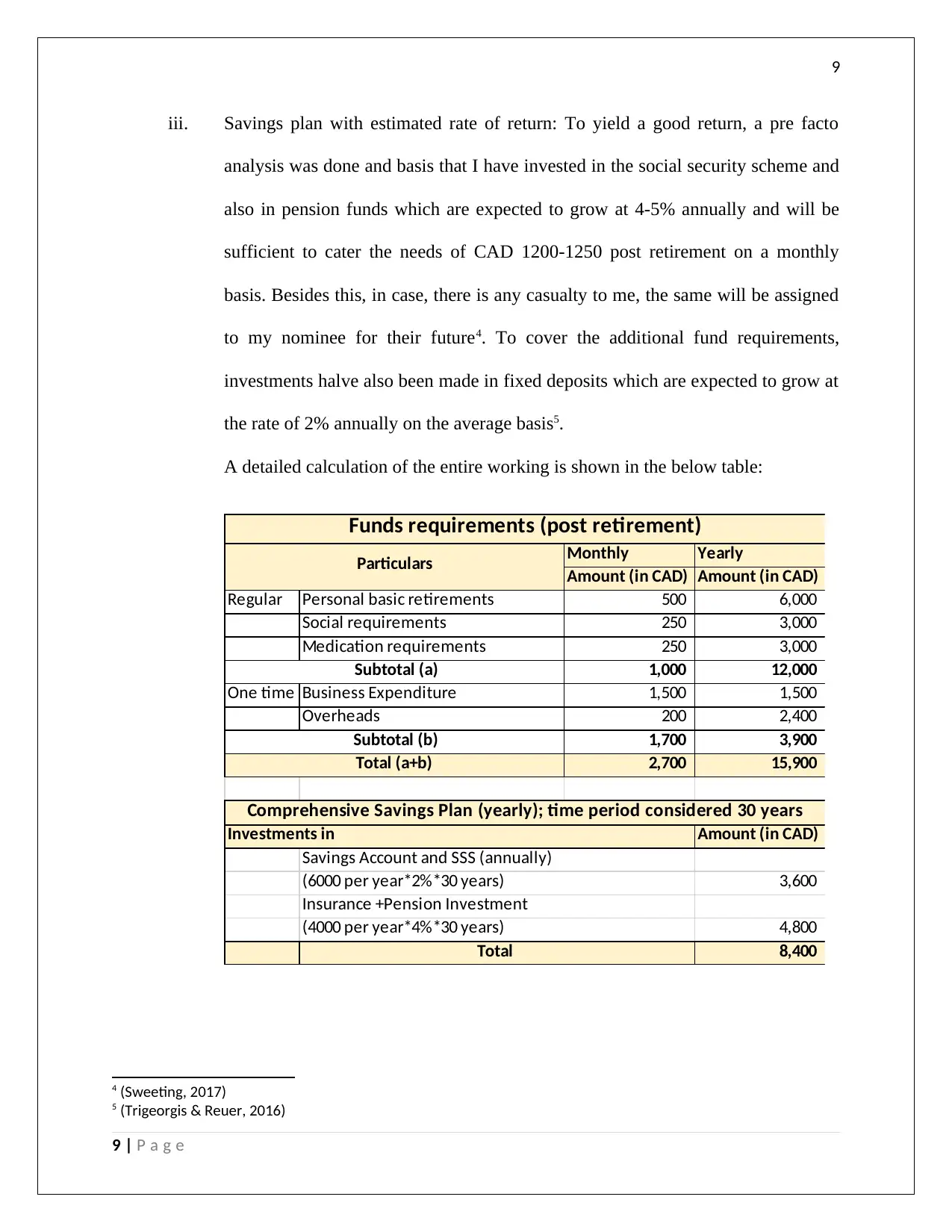

iii. Savings plan with estimated rate of return: To yield a good return, a pre facto

analysis was done and basis that I have invested in the social security scheme and

also in pension funds which are expected to grow at 4-5% annually and will be

sufficient to cater the needs of CAD 1200-1250 post retirement on a monthly

basis. Besides this, in case, there is any casualty to me, the same will be assigned

to my nominee for their future4. To cover the additional fund requirements,

investments halve also been made in fixed deposits which are expected to grow at

the rate of 2% annually on the average basis5.

A detailed calculation of the entire working is shown in the below table:

Monthly Yearly

Amount (in CAD) Amount (in CAD)

Regular Personal basic retirements 500 6,000

Social requirements 250 3,000

Medication requirements 250 3,000

1,000 12,000

One time Business Expenditure 1,500 1,500

Overheads 200 2,400

1,700 3,900

2,700 15,900

Amount (in CAD)

3,600

4,800

8,400

Insurance +Pension Investment

(4000 per year*4%*30 years)

Total

Investments in

Funds requirements (post retirement)

Comprehensive Savings Plan (yearly); time period considered 30 years

Savings Account and SSS (annually)

(6000 per year*2%*30 years)

Subtotal (a)

Subtotal (b)

Total (a+b)

Particulars

4 (Sweeting, 2017)

5 (Trigeorgis & Reuer, 2016)

9 | P a g e

iii. Savings plan with estimated rate of return: To yield a good return, a pre facto

analysis was done and basis that I have invested in the social security scheme and

also in pension funds which are expected to grow at 4-5% annually and will be

sufficient to cater the needs of CAD 1200-1250 post retirement on a monthly

basis. Besides this, in case, there is any casualty to me, the same will be assigned

to my nominee for their future4. To cover the additional fund requirements,

investments halve also been made in fixed deposits which are expected to grow at

the rate of 2% annually on the average basis5.

A detailed calculation of the entire working is shown in the below table:

Monthly Yearly

Amount (in CAD) Amount (in CAD)

Regular Personal basic retirements 500 6,000

Social requirements 250 3,000

Medication requirements 250 3,000

1,000 12,000

One time Business Expenditure 1,500 1,500

Overheads 200 2,400

1,700 3,900

2,700 15,900

Amount (in CAD)

3,600

4,800

8,400

Insurance +Pension Investment

(4000 per year*4%*30 years)

Total

Investments in

Funds requirements (post retirement)

Comprehensive Savings Plan (yearly); time period considered 30 years

Savings Account and SSS (annually)

(6000 per year*2%*30 years)

Subtotal (a)

Subtotal (b)

Total (a+b)

Particulars

4 (Sweeting, 2017)

5 (Trigeorgis & Reuer, 2016)

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Section Five – Class and Pedagogy: Answer to Question 7

The course and the sessions imparted on the personal financing front have been and will

be ultra essential. The fact that the present has huge arena of investment avenues, in the

professional world makes it much more essential. Major teachings and learning has been

undertaken in the course, to make use of planning and forecasting strategies in order to reap the

maximum returns with minimal risks. To plan well, the knowledge on the subject is necessary as

well as a good research on the topic.

Also, it has helped to get some insights into the taxation front, in order to how adequate

guard needs to be insured to avoid fraudsters and prevent oneself from being cheated. Not only

personal knowledge is essential, but to create awareness in order to prevent others from being

deceived or defrauded is essential. Besides all this, this course has given helped some

investments strategies and how to do pre facto analysis that by what period the initial investment

would be recovered, what would be the breakeven point, what would be ROI and the final

profits. It has given lessons of planning the debts well in order to avoid crisis, this can be done

by paying the installments bi-monthly rather than monthly, avoiding the purchases which are

based on option of “buy today, pay later” and interest free loans as it always increases the

liability. Also, negotiation skills play a great deal in major investments as it needs to be on par to

get the maximum benefit out of the financial situation6.

All in all, this course is explicitly aimed at achieving the maximum results out of the

minimum available resources and the same can be achieved with aggressive planning and

accurate execution7.

6 (Gerrans & Hershey, 2016)

7 (King & Carey, 2017)

10 | P a g e

Section Five – Class and Pedagogy: Answer to Question 7

The course and the sessions imparted on the personal financing front have been and will

be ultra essential. The fact that the present has huge arena of investment avenues, in the

professional world makes it much more essential. Major teachings and learning has been

undertaken in the course, to make use of planning and forecasting strategies in order to reap the

maximum returns with minimal risks. To plan well, the knowledge on the subject is necessary as

well as a good research on the topic.

Also, it has helped to get some insights into the taxation front, in order to how adequate

guard needs to be insured to avoid fraudsters and prevent oneself from being cheated. Not only

personal knowledge is essential, but to create awareness in order to prevent others from being

deceived or defrauded is essential. Besides all this, this course has given helped some

investments strategies and how to do pre facto analysis that by what period the initial investment

would be recovered, what would be the breakeven point, what would be ROI and the final

profits. It has given lessons of planning the debts well in order to avoid crisis, this can be done

by paying the installments bi-monthly rather than monthly, avoiding the purchases which are

based on option of “buy today, pay later” and interest free loans as it always increases the

liability. Also, negotiation skills play a great deal in major investments as it needs to be on par to

get the maximum benefit out of the financial situation6.

All in all, this course is explicitly aimed at achieving the maximum results out of the

minimum available resources and the same can be achieved with aggressive planning and

accurate execution7.

6 (Gerrans & Hershey, 2016)

7 (King & Carey, 2017)

10 | P a g e

11

References

Gerrans, P., & Hershey, D. (2016). Financial Adviser Anxiety, Financial Literacy, and Financial Advice

Seeking. Journal of Consumer Affairs , 51 (1), 54-90.

(http://onlinelibrary.wiley.com/doi/10.1111/joca.12120/full)

Hopkin, P. (2017). Fundamentals of Risk Management: Understanding, evaluating and implementing

(Fourth ed.). London: The Institute of Risk Management. (https://books.google.co.in/books?

11 | P a g e

References

Gerrans, P., & Hershey, D. (2016). Financial Adviser Anxiety, Financial Literacy, and Financial Advice

Seeking. Journal of Consumer Affairs , 51 (1), 54-90.

(http://onlinelibrary.wiley.com/doi/10.1111/joca.12120/full)

Hopkin, P. (2017). Fundamentals of Risk Management: Understanding, evaluating and implementing

(Fourth ed.). London: The Institute of Risk Management. (https://books.google.co.in/books?

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.