Personal Finance Report: Retirement Planning for Alastair and Wendy

VerifiedAdded on 2022/11/26

|25

|4361

|468

Report

AI Summary

This report, prepared for Alastair and Wendy Windsor, focuses on their retirement planning, outlining their financial objectives, both short-term and long-term, and proposing strategies to achieve them. It analyzes their pension schemes, including the impact of UK pension reforms introduced in 2014/15, and considers the implications of taxation on their income and wealth. The report details the couple's income projections, savings plans, and investment options, while also addressing the financial responsibilities they have towards their dependents and the potential impact of inheritance tax. It provides a comprehensive financial assessment, offering recommendations to ensure a secure financial future for Alastair and Wendy, considering various scenarios and key assumptions related to their retirement age and income sources. The report also analyzes Wendy's pension contributions and the couple's overall tax liabilities, providing a complete financial overview.

Running head: PERSONAL FINANCE

Personal Finance

Name of the Student:

Name of the University:

Authors Note:

Personal Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

PERSONAL FINANCE

Contents

Introduction:....................................................................................................................................2

Part A:..............................................................................................................................................2

Part B:..............................................................................................................................................6

Part C:..............................................................................................................................................8

Part D:............................................................................................................................................10

Part E:............................................................................................................................................12

Conclusion:....................................................................................................................................13

References:....................................................................................................................................14

PERSONAL FINANCE

Contents

Introduction:....................................................................................................................................2

Part A:..............................................................................................................................................2

Part B:..............................................................................................................................................6

Part C:..............................................................................................................................................8

Part D:............................................................................................................................................10

Part E:............................................................................................................................................12

Conclusion:....................................................................................................................................13

References:....................................................................................................................................14

2

PERSONAL FINANCE

Introduction:

As a consultant firm we are obliged to provide our clients with best possible suggestions

to help them to achieve their financial objectives. In this documents we shall help Alastair and

Wendy Windsor of North East England to plan their retirement in a manner suitable to their

financial requirements in the future. Once retired the primary source of income of a person is his

or her pension. It is important to plan the retirement effectively to ensure that the pensions to be

received in the future shall be enough to meet the future expenses and other needs of the elderly

people. The detailed discussion and the suggestive course of action for Alastair and Wendy

outlined below.

Part A:

Financial objectives of Alastair and Wendy in the short and long run:

Financial objectives of clients are dependent on number of things including their age, financial

needs, income, quality of life in the future and others. The financial objectives are mainly of two

categories, firstly short term objectives and secondly long term objectives. Alastair and Wendy

aged 56 years and 49 years respectively are elderly couple looking to secure their future.

Short term objectives:

In the short run the objective of the couple is to ensure that the pension income of theirs will be

sufficient to meet their family expenditures. The pensions that would be received after paying

necessary taxes shall be enough to meet the family expenditures of the couple subsequent to their

retirement is the main short term objective.

Medium term objective:

PERSONAL FINANCE

Introduction:

As a consultant firm we are obliged to provide our clients with best possible suggestions

to help them to achieve their financial objectives. In this documents we shall help Alastair and

Wendy Windsor of North East England to plan their retirement in a manner suitable to their

financial requirements in the future. Once retired the primary source of income of a person is his

or her pension. It is important to plan the retirement effectively to ensure that the pensions to be

received in the future shall be enough to meet the future expenses and other needs of the elderly

people. The detailed discussion and the suggestive course of action for Alastair and Wendy

outlined below.

Part A:

Financial objectives of Alastair and Wendy in the short and long run:

Financial objectives of clients are dependent on number of things including their age, financial

needs, income, quality of life in the future and others. The financial objectives are mainly of two

categories, firstly short term objectives and secondly long term objectives. Alastair and Wendy

aged 56 years and 49 years respectively are elderly couple looking to secure their future.

Short term objectives:

In the short run the objective of the couple is to ensure that the pension income of theirs will be

sufficient to meet their family expenditures. The pensions that would be received after paying

necessary taxes shall be enough to meet the family expenditures of the couple subsequent to their

retirement is the main short term objective.

Medium term objective:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

PERSONAL FINANCE

Covering the University fees of one of the dependents of the couple along with saving for the

America trip are part of medium term objectives of the couple. In order to achieve the medium

term objectives the funds must be invested in profitable investment options.

Long term objectives:

The primary financial objective of the both is to invest in stable sources to secure their future.

The dependents are Harry and Holly as Alastair and Wendy do not have any children from their

marriage (Ellison, 2011). In addition to meeting the short term objectives ensuring that the part

of net income of the couple subsequent to the retirement shall gone towards securing their future

is also to be noted.

The financial objectives of Alastair and Wendy thus, include that the income in the future should

be enough to meet their budgeted expenditures as well as to make savings for their future.

Meeting the family expenditures and providing for their dependants in case anything happens to

Alastair and Wendy is the main financial objective of the couple (Farrar, Moizer & Hyde, 2012).

Plans to achieve the objectives of the couple:

Pensions are received by both Alastair and Wendy from their respective employers in the form of

lump sum and annuity. In addition to the current employment income and pension both have also

inherited properties from their ancestors. Both their income and wealth are increased due to these

inherited properties from their grandparents.

From the facts it is clear that the main source of income to the couple is the respective income

from different pension schemes. With both having two or more pension schemes to earn income

in the future in the form of annuity and in lump sum. However, the amount of lump sum payment

PERSONAL FINANCE

Covering the University fees of one of the dependents of the couple along with saving for the

America trip are part of medium term objectives of the couple. In order to achieve the medium

term objectives the funds must be invested in profitable investment options.

Long term objectives:

The primary financial objective of the both is to invest in stable sources to secure their future.

The dependents are Harry and Holly as Alastair and Wendy do not have any children from their

marriage (Ellison, 2011). In addition to meeting the short term objectives ensuring that the part

of net income of the couple subsequent to the retirement shall gone towards securing their future

is also to be noted.

The financial objectives of Alastair and Wendy thus, include that the income in the future should

be enough to meet their budgeted expenditures as well as to make savings for their future.

Meeting the family expenditures and providing for their dependants in case anything happens to

Alastair and Wendy is the main financial objective of the couple (Farrar, Moizer & Hyde, 2012).

Plans to achieve the objectives of the couple:

Pensions are received by both Alastair and Wendy from their respective employers in the form of

lump sum and annuity. In addition to the current employment income and pension both have also

inherited properties from their ancestors. Both their income and wealth are increased due to these

inherited properties from their grandparents.

From the facts it is clear that the main source of income to the couple is the respective income

from different pension schemes. With both having two or more pension schemes to earn income

in the future in the form of annuity and in lump sum. However, the amount of lump sum payment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

PERSONAL FINANCE

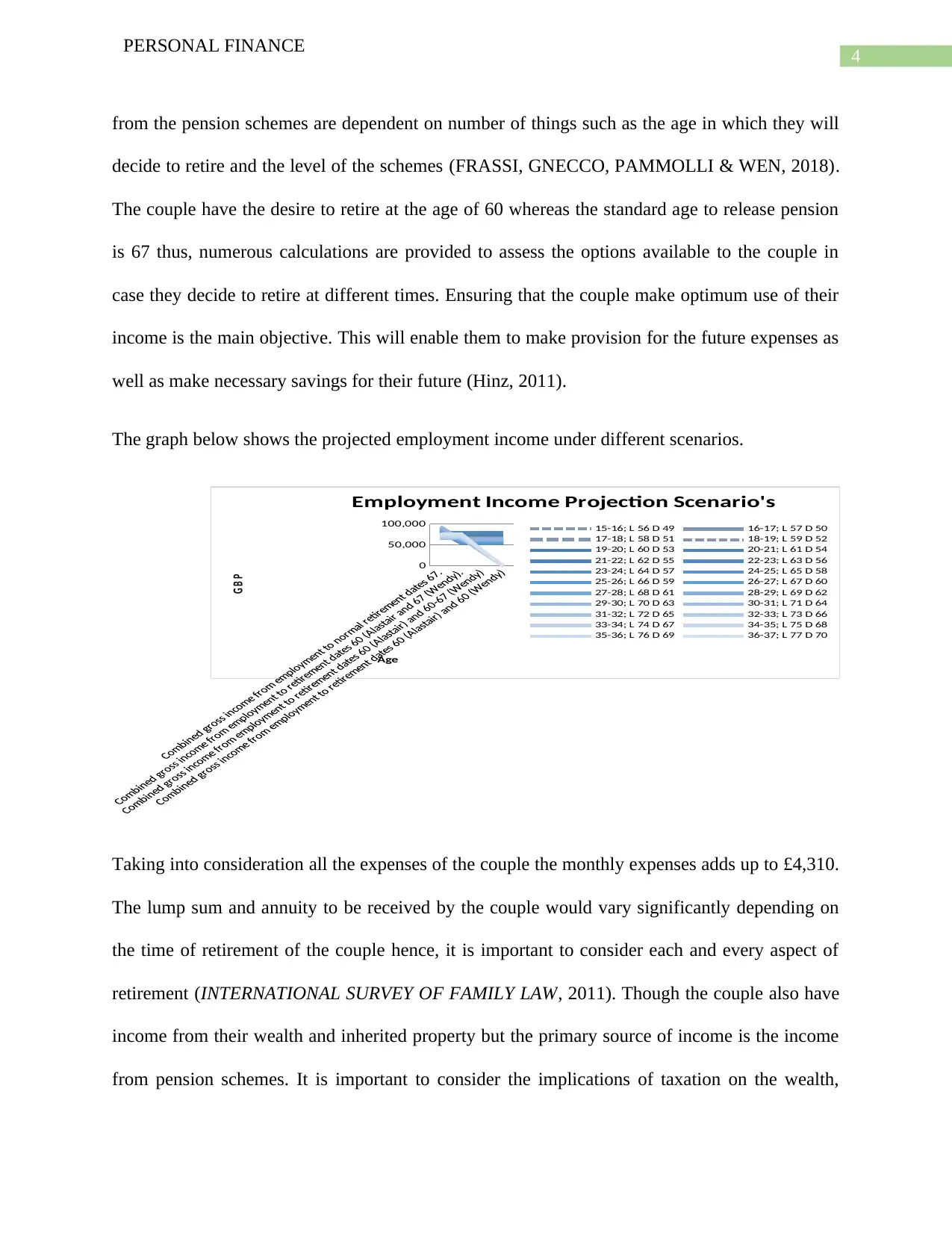

from the pension schemes are dependent on number of things such as the age in which they will

decide to retire and the level of the schemes (FRASSI, GNECCO, PAMMOLLI & WEN, 2018).

The couple have the desire to retire at the age of 60 whereas the standard age to release pension

is 67 thus, numerous calculations are provided to assess the options available to the couple in

case they decide to retire at different times. Ensuring that the couple make optimum use of their

income is the main objective. This will enable them to make provision for the future expenses as

well as make necessary savings for their future (Hinz, 2011).

The graph below shows the projected employment income under different scenarios.

0

50,000

100,000

Employment Income Projection Scenario's

15-16; L 56 D 49 16-17; L 57 D 50

17-18; L 58 D 51 18-19; L 59 D 52

19-20; L 60 D 53 20-21; L 61 D 54

21-22; L 62 D 55 22-23; L 63 D 56

23-24; L 64 D 57 24-25; L 65 D 58

25-26; L 66 D 59 26-27; L 67 D 60

27-28; L 68 D 61 28-29; L 69 D 62

29-30; L 70 D 63 30-31; L 71 D 64

31-32; L 72 D 65 32-33; L 73 D 66

33-34; L 74 D 67 34-35; L 75 D 68

35-36; L 76 D 69 36-37; L 77 D 70

Age

G B P

Taking into consideration all the expenses of the couple the monthly expenses adds up to £4,310.

The lump sum and annuity to be received by the couple would vary significantly depending on

the time of retirement of the couple hence, it is important to consider each and every aspect of

retirement (INTERNATIONAL SURVEY OF FAMILY LAW, 2011). Though the couple also have

income from their wealth and inherited property but the primary source of income is the income

from pension schemes. It is important to consider the implications of taxation on the wealth,

PERSONAL FINANCE

from the pension schemes are dependent on number of things such as the age in which they will

decide to retire and the level of the schemes (FRASSI, GNECCO, PAMMOLLI & WEN, 2018).

The couple have the desire to retire at the age of 60 whereas the standard age to release pension

is 67 thus, numerous calculations are provided to assess the options available to the couple in

case they decide to retire at different times. Ensuring that the couple make optimum use of their

income is the main objective. This will enable them to make provision for the future expenses as

well as make necessary savings for their future (Hinz, 2011).

The graph below shows the projected employment income under different scenarios.

0

50,000

100,000

Employment Income Projection Scenario's

15-16; L 56 D 49 16-17; L 57 D 50

17-18; L 58 D 51 18-19; L 59 D 52

19-20; L 60 D 53 20-21; L 61 D 54

21-22; L 62 D 55 22-23; L 63 D 56

23-24; L 64 D 57 24-25; L 65 D 58

25-26; L 66 D 59 26-27; L 67 D 60

27-28; L 68 D 61 28-29; L 69 D 62

29-30; L 70 D 63 30-31; L 71 D 64

31-32; L 72 D 65 32-33; L 73 D 66

33-34; L 74 D 67 34-35; L 75 D 68

35-36; L 76 D 69 36-37; L 77 D 70

Age

G B P

Taking into consideration all the expenses of the couple the monthly expenses adds up to £4,310.

The lump sum and annuity to be received by the couple would vary significantly depending on

the time of retirement of the couple hence, it is important to consider each and every aspect of

retirement (INTERNATIONAL SURVEY OF FAMILY LAW, 2011). Though the couple also have

income from their wealth and inherited property but the primary source of income is the income

from pension schemes. It is important to consider the implications of taxation on the wealth,

5

PERSONAL FINANCE

property and overall income of the couple. After deducting all necessary taxes on income and

applicable taxes on wealth the available income should be sufficient to meet the monthly

expenditures of the family in addition to make necessary savings for the future. It is important to

note that the income of the couple in the future should not only be sufficient to meet their

expenditures but they have dependents including the parents of Alastair who are at the advanced

age and are sickly. Thus medical bills for his parents are also quite significant. Ensuring the

future incomes of the couple is sufficient to meet all these expenditures and provide for the

security of the couple is the primary financial objective of the couple (Kira & Eijnatten, 2011).

Apart from the above financing the University fees of Holly and to make provision for the

American trip will be fulfilled by investing certain percentage of total funds in lucrative

investment options such as Real Estate Investments Trusts and other such lucrative but less risky

investment options.

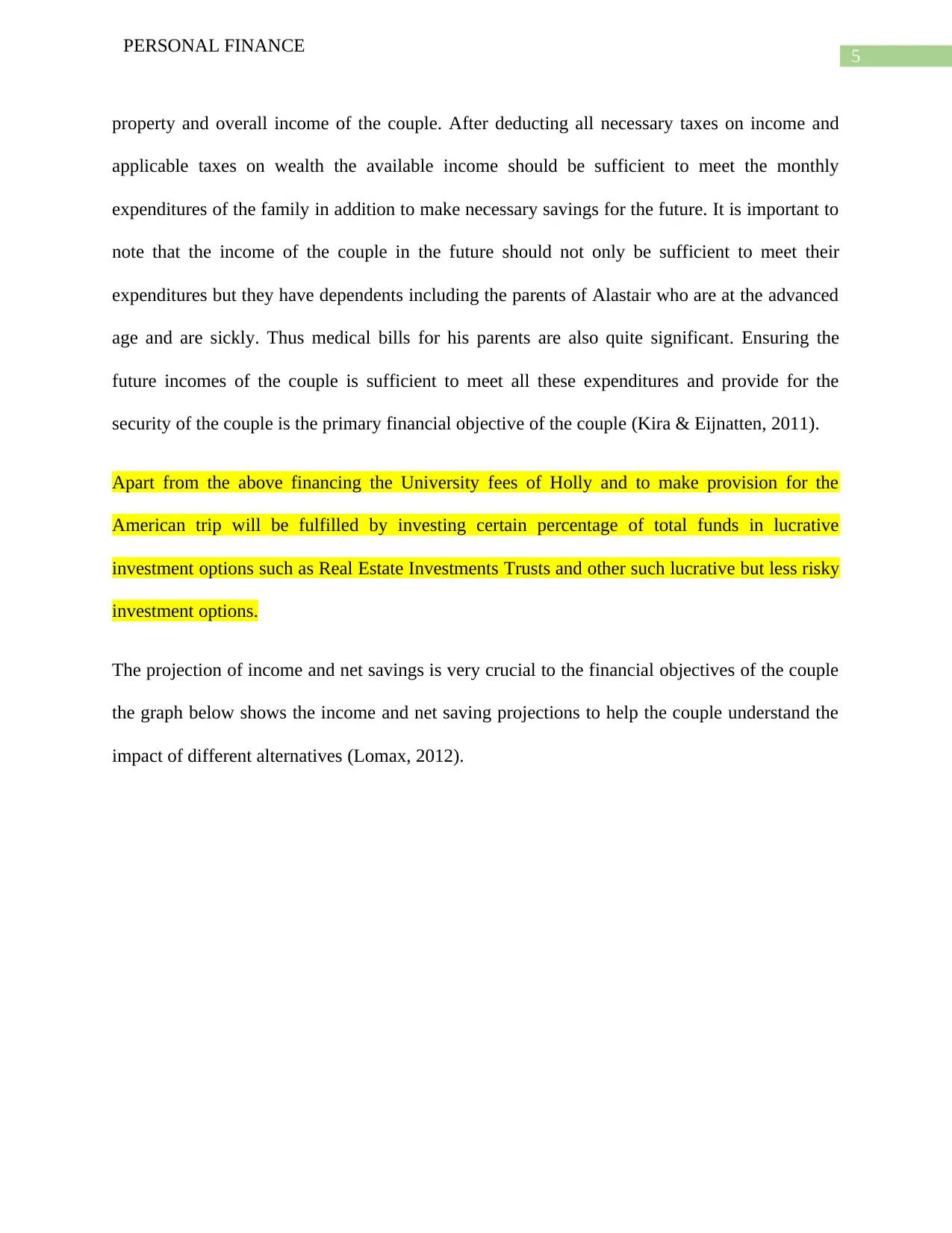

The projection of income and net savings is very crucial to the financial objectives of the couple

the graph below shows the income and net saving projections to help the couple understand the

impact of different alternatives (Lomax, 2012).

PERSONAL FINANCE

property and overall income of the couple. After deducting all necessary taxes on income and

applicable taxes on wealth the available income should be sufficient to meet the monthly

expenditures of the family in addition to make necessary savings for the future. It is important to

note that the income of the couple in the future should not only be sufficient to meet their

expenditures but they have dependents including the parents of Alastair who are at the advanced

age and are sickly. Thus medical bills for his parents are also quite significant. Ensuring the

future incomes of the couple is sufficient to meet all these expenditures and provide for the

security of the couple is the primary financial objective of the couple (Kira & Eijnatten, 2011).

Apart from the above financing the University fees of Holly and to make provision for the

American trip will be fulfilled by investing certain percentage of total funds in lucrative

investment options such as Real Estate Investments Trusts and other such lucrative but less risky

investment options.

The projection of income and net savings is very crucial to the financial objectives of the couple

the graph below shows the income and net saving projections to help the couple understand the

impact of different alternatives (Lomax, 2012).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

PERSONAL FINANCE

15-16; L 56 D 49

17-18; L 58 D 51

19-20; L 60 D 53

21-22; L 62 D 55

23-24; L 64 D 57

25-26; L 66 D 59

27-28; L 68 D 61

29-30; L 70 D 63

31-32; L 72 D 65

33-34; L 74 D 67

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Income & Net Savings Projections

Alastair Pension Income

Alastair Employment Income

Wendy Employment Income

Wendy Pension Income

Net Annual Savings

Age

GBP

From the above graph the income and net savings projections can be understood clearly.

Key assumptions to the above part are outlined below:

I. Alastair wants to retire at an early age and if possible even now.

II. The company in which Alastair works however pays pension at the age of 60 years.

III. The couple would be responsible to take care of Alastair’s parents.

IV. Harry and Holly both are dependents on the couple and the couple wants to provide

equally for both of them.

V. No will has been made to plan the estate of the couple yet.

VI. It has been assumed that salaries of Alastair and Wendy have increased.

VII. New reforms of pension schemes have been availed by the couple.

VIII. Inheritance tax shall be paid at 40% (Marotta, 2011).

PERSONAL FINANCE

15-16; L 56 D 49

17-18; L 58 D 51

19-20; L 60 D 53

21-22; L 62 D 55

23-24; L 64 D 57

25-26; L 66 D 59

27-28; L 68 D 61

29-30; L 70 D 63

31-32; L 72 D 65

33-34; L 74 D 67

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Income & Net Savings Projections

Alastair Pension Income

Alastair Employment Income

Wendy Employment Income

Wendy Pension Income

Net Annual Savings

Age

GBP

From the above graph the income and net savings projections can be understood clearly.

Key assumptions to the above part are outlined below:

I. Alastair wants to retire at an early age and if possible even now.

II. The company in which Alastair works however pays pension at the age of 60 years.

III. The couple would be responsible to take care of Alastair’s parents.

IV. Harry and Holly both are dependents on the couple and the couple wants to provide

equally for both of them.

V. No will has been made to plan the estate of the couple yet.

VI. It has been assumed that salaries of Alastair and Wendy have increased.

VII. New reforms of pension schemes have been availed by the couple.

VIII. Inheritance tax shall be paid at 40% (Marotta, 2011).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

PERSONAL FINANCE

Part B:

Reforms introduced in pension related provisions in the UK during the fiscal year 2014/15 have

significant impact on the quantum of income in the future. The new reforms shall help the couple

to take advantage to enhance their pensionable income. Since the primary source of income to

the couple is pension hence, maximizing their pension income is the main objective as this will

enable them to meet their family expenditures and make savings at the same time for the future.

Finalizing the most beneficial pension scheme will enable the couple to earn maximum amount

of income in the future to make provision for their future. The beneficial provisions introduced in

the reforms shall be used properly to extract maximum benefits out of the pension schemes to

achieve the financial objectives of the couple in the future (Novella & Olivera, 2014).

Since the reforms introduced in 2014/15 has reduced the applicable taxes on pension income and

allowed the pensioners to cash their lump sum dues with reduced tax liability it is important for

the couple to use these reforms effectively to increase their income from pension schemes. In

contrast to the earlier provision of allowing 25% lump sum payment of pension funds now the

pensioners have the option to take number of small lump sums thus, pensioners can decide

whether to take small lump sums or take lump sum amount of pension at one go. People

investing in pension schemes if aged 55 years or above will have the option to take small lump

sums from pension funds according to his or her needs (Rutledge, Wu & Vitagliano, 2014).

With this reform Alastair aged 56 years can straight away start receiving pension income if he

desires to retire now instead of waiting for 60 years of age. Thus, by using the reform he does not

have to wait to be 60 to 67 years old to avail the benefits of pension. Also the 40% tax on lump

sum payment received from pension schemes need not be paid under the new reforms hence,

Alastair will be able to reduce his tax liability and start receiving pension from now. The new

PERSONAL FINANCE

Part B:

Reforms introduced in pension related provisions in the UK during the fiscal year 2014/15 have

significant impact on the quantum of income in the future. The new reforms shall help the couple

to take advantage to enhance their pensionable income. Since the primary source of income to

the couple is pension hence, maximizing their pension income is the main objective as this will

enable them to meet their family expenditures and make savings at the same time for the future.

Finalizing the most beneficial pension scheme will enable the couple to earn maximum amount

of income in the future to make provision for their future. The beneficial provisions introduced in

the reforms shall be used properly to extract maximum benefits out of the pension schemes to

achieve the financial objectives of the couple in the future (Novella & Olivera, 2014).

Since the reforms introduced in 2014/15 has reduced the applicable taxes on pension income and

allowed the pensioners to cash their lump sum dues with reduced tax liability it is important for

the couple to use these reforms effectively to increase their income from pension schemes. In

contrast to the earlier provision of allowing 25% lump sum payment of pension funds now the

pensioners have the option to take number of small lump sums thus, pensioners can decide

whether to take small lump sums or take lump sum amount of pension at one go. People

investing in pension schemes if aged 55 years or above will have the option to take small lump

sums from pension funds according to his or her needs (Rutledge, Wu & Vitagliano, 2014).

With this reform Alastair aged 56 years can straight away start receiving pension income if he

desires to retire now instead of waiting for 60 years of age. Thus, by using the reform he does not

have to wait to be 60 to 67 years old to avail the benefits of pension. Also the 40% tax on lump

sum payment received from pension schemes need not be paid under the new reforms hence,

Alastair will be able to reduce his tax liability and start receiving pension from now. The new

8

PERSONAL FINANCE

pension policy suits Alastair as the overall cost of accessing pension funds and tax liability

towards pension fund will reduce significantly. Alastair will also be benefitted with the scheme

of transferring final salary to the pension scheme. This would increase the pension income

significantly. There are number of other benefits including transferring to defined contribution

scheme from current defined benefit scheme (Selin, 2016).

Workings:

Alastair’s pension:

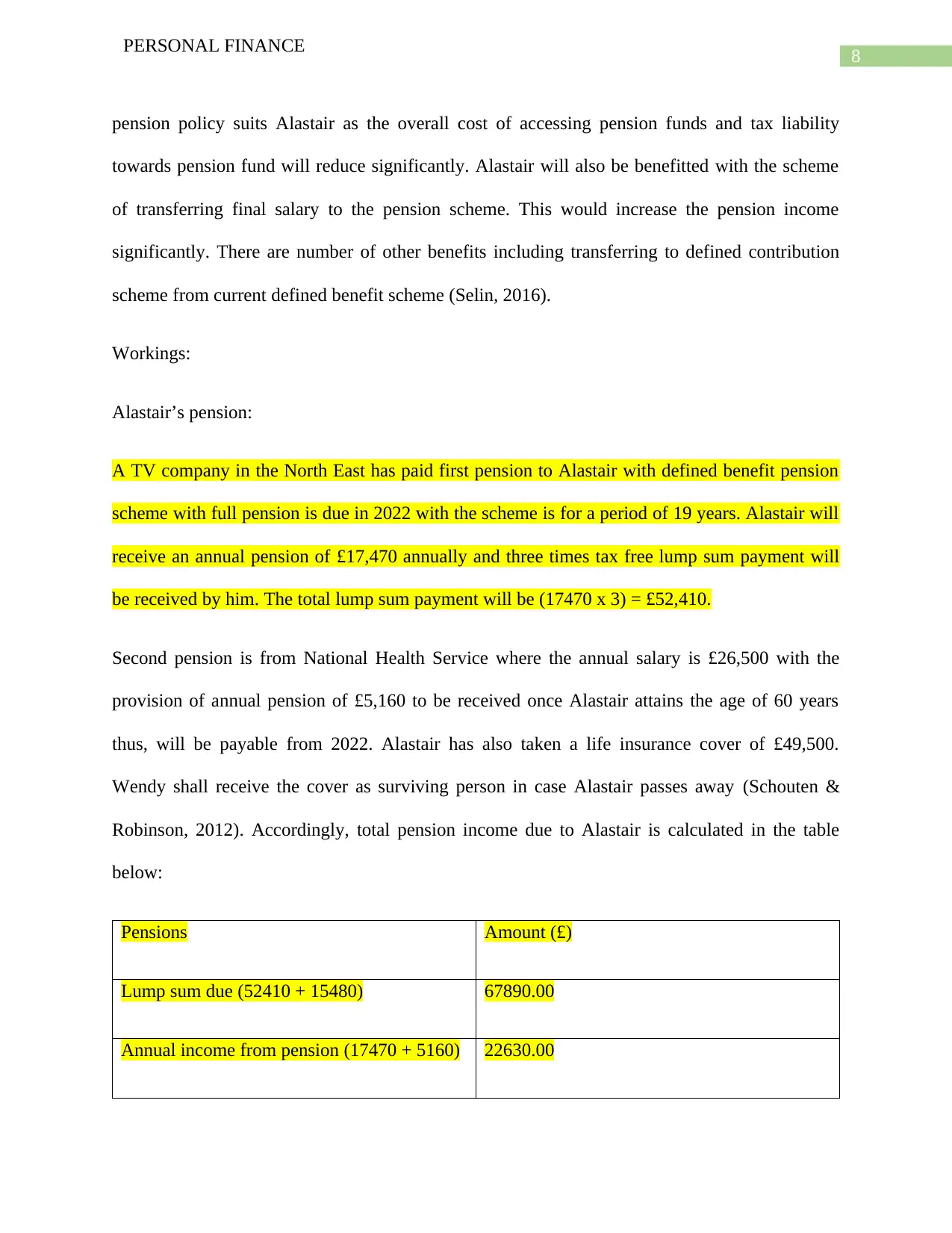

A TV company in the North East has paid first pension to Alastair with defined benefit pension

scheme with full pension is due in 2022 with the scheme is for a period of 19 years. Alastair will

receive an annual pension of £17,470 annually and three times tax free lump sum payment will

be received by him. The total lump sum payment will be (17470 x 3) = £52,410.

Second pension is from National Health Service where the annual salary is £26,500 with the

provision of annual pension of £5,160 to be received once Alastair attains the age of 60 years

thus, will be payable from 2022. Alastair has also taken a life insurance cover of £49,500.

Wendy shall receive the cover as surviving person in case Alastair passes away (Schouten &

Robinson, 2012). Accordingly, total pension income due to Alastair is calculated in the table

below:

Pensions Amount (£)

Lump sum due (52410 + 15480) 67890.00

Annual income from pension (17470 + 5160) 22630.00

PERSONAL FINANCE

pension policy suits Alastair as the overall cost of accessing pension funds and tax liability

towards pension fund will reduce significantly. Alastair will also be benefitted with the scheme

of transferring final salary to the pension scheme. This would increase the pension income

significantly. There are number of other benefits including transferring to defined contribution

scheme from current defined benefit scheme (Selin, 2016).

Workings:

Alastair’s pension:

A TV company in the North East has paid first pension to Alastair with defined benefit pension

scheme with full pension is due in 2022 with the scheme is for a period of 19 years. Alastair will

receive an annual pension of £17,470 annually and three times tax free lump sum payment will

be received by him. The total lump sum payment will be (17470 x 3) = £52,410.

Second pension is from National Health Service where the annual salary is £26,500 with the

provision of annual pension of £5,160 to be received once Alastair attains the age of 60 years

thus, will be payable from 2022. Alastair has also taken a life insurance cover of £49,500.

Wendy shall receive the cover as surviving person in case Alastair passes away (Schouten &

Robinson, 2012). Accordingly, total pension income due to Alastair is calculated in the table

below:

Pensions Amount (£)

Lump sum due (52410 + 15480) 67890.00

Annual income from pension (17470 + 5160) 22630.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

PERSONAL FINANCE

Total pension income 90520.00

Note:

I. The lump sum payment of payment is taxable ta the rate of 40%.

II. With taxation pension income is 20%.

Wendy’s pension:

Wendy has taught 8 years in private sector and 8 years Further Education with 4 years from

Higher Education. Contribution to pension fund was 10.2% of £ 49000, i.e. £ 4998. In addition

entitled pension of £ 4500 and £ 11700 as lump sum.

Total pension of Wendy’s will be £6,568 (Wang, 2018).

Part C:

Taxation matters and issues affecting the couple:

The net earnings of the couple will be dependent to a large extent on the taxation provisions

applicable to their incomes. Thus, it is important to consider the effects of taxation on the net

income of the couple. Though the primary sources of income of the couple is pension income

however, there are other incomes such as income from property and wealth. Impact of taxation

provisions on these income would determine the net income in the hands of the couple.

Especially considering the inheritance of property and wealth the impact of capital gain tax shall

be ascertained to determine actual impact on the net income of the couple. The capital gain tax

on the apartment Wendy has decide to sale will have to be calculated to determine the impact of

PERSONAL FINANCE

Total pension income 90520.00

Note:

I. The lump sum payment of payment is taxable ta the rate of 40%.

II. With taxation pension income is 20%.

Wendy’s pension:

Wendy has taught 8 years in private sector and 8 years Further Education with 4 years from

Higher Education. Contribution to pension fund was 10.2% of £ 49000, i.e. £ 4998. In addition

entitled pension of £ 4500 and £ 11700 as lump sum.

Total pension of Wendy’s will be £6,568 (Wang, 2018).

Part C:

Taxation matters and issues affecting the couple:

The net earnings of the couple will be dependent to a large extent on the taxation provisions

applicable to their incomes. Thus, it is important to consider the effects of taxation on the net

income of the couple. Though the primary sources of income of the couple is pension income

however, there are other incomes such as income from property and wealth. Impact of taxation

provisions on these income would determine the net income in the hands of the couple.

Especially considering the inheritance of property and wealth the impact of capital gain tax shall

be ascertained to determine actual impact on the net income of the couple. The capital gain tax

on the apartment Wendy has decide to sale will have to be calculated to determine the impact of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

PERSONAL FINANCE

the same on the net income of the couple. Rate of capital gain tax on capital gain arising from

sale of residential properties is 28% in 2018 however, the rate reduced to 18 for sale of properties

inherited from deceased persons (Natali, 2009).

In case of property inherited the Govt. imposes certain percentage of tax on such inheritance,

known as inheritance tax. Inheritance tax has to be paid by the inheritor subsequent to the

transfer of the property to the inheritor. Applicable rate of inheritance tax in UK is 40% in 2018.

A similar percentage of tax shall be imposed on inheritance income received by the couple in

2018. Estate planning is one of the most effective ways to deal with tax related matters thus, one

should make an effective estate plan to minimize tax liability on such properties. The parents and

grandparents of Alastair and Wendy have done that however, no such planning has been made

the couple who believe that their properties and wealth shall be transferred to Harry and Holly

(Kira & van Eijnatten, 2012).

Considering the advanced stage of Alastair’s parents and their sickly health the couple need

health cover for Alastair’s parents and insurance cover for themselves. The health cover would

protect the couple from expensive medical bills for different types of diseases including cancer.

Thus, using health cover for Alastair’s parents and insurance cover for the couple would help

them to reduce the burden on the future income of the couple (Kira & Eijnatten, 2011).

Workings:

Capital gain tax:

Particulars Amount (£) Amount (£)

PERSONAL FINANCE

the same on the net income of the couple. Rate of capital gain tax on capital gain arising from

sale of residential properties is 28% in 2018 however, the rate reduced to 18 for sale of properties

inherited from deceased persons (Natali, 2009).

In case of property inherited the Govt. imposes certain percentage of tax on such inheritance,

known as inheritance tax. Inheritance tax has to be paid by the inheritor subsequent to the

transfer of the property to the inheritor. Applicable rate of inheritance tax in UK is 40% in 2018.

A similar percentage of tax shall be imposed on inheritance income received by the couple in

2018. Estate planning is one of the most effective ways to deal with tax related matters thus, one

should make an effective estate plan to minimize tax liability on such properties. The parents and

grandparents of Alastair and Wendy have done that however, no such planning has been made

the couple who believe that their properties and wealth shall be transferred to Harry and Holly

(Kira & van Eijnatten, 2012).

Considering the advanced stage of Alastair’s parents and their sickly health the couple need

health cover for Alastair’s parents and insurance cover for themselves. The health cover would

protect the couple from expensive medical bills for different types of diseases including cancer.

Thus, using health cover for Alastair’s parents and insurance cover for the couple would help

them to reduce the burden on the future income of the couple (Kira & Eijnatten, 2011).

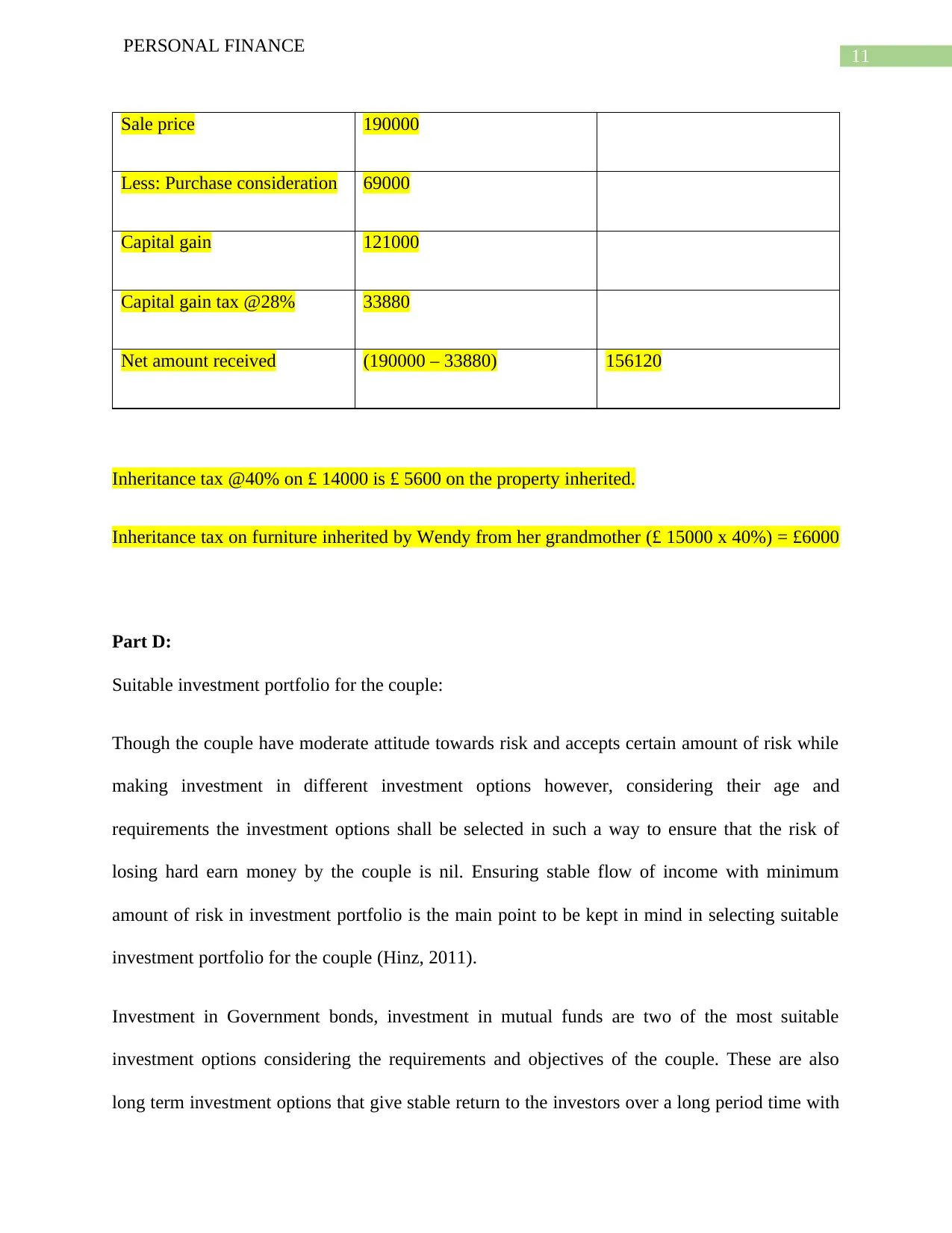

Workings:

Capital gain tax:

Particulars Amount (£) Amount (£)

11

PERSONAL FINANCE

Sale price 190000

Less: Purchase consideration 69000

Capital gain 121000

Capital gain tax @28% 33880

Net amount received (190000 – 33880) 156120

Inheritance tax @40% on £ 14000 is £ 5600 on the property inherited.

Inheritance tax on furniture inherited by Wendy from her grandmother (£ 15000 x 40%) = £6000

Part D:

Suitable investment portfolio for the couple:

Though the couple have moderate attitude towards risk and accepts certain amount of risk while

making investment in different investment options however, considering their age and

requirements the investment options shall be selected in such a way to ensure that the risk of

losing hard earn money by the couple is nil. Ensuring stable flow of income with minimum

amount of risk in investment portfolio is the main point to be kept in mind in selecting suitable

investment portfolio for the couple (Hinz, 2011).

Investment in Government bonds, investment in mutual funds are two of the most suitable

investment options considering the requirements and objectives of the couple. These are also

long term investment options that give stable return to the investors over a long period time with

PERSONAL FINANCE

Sale price 190000

Less: Purchase consideration 69000

Capital gain 121000

Capital gain tax @28% 33880

Net amount received (190000 – 33880) 156120

Inheritance tax @40% on £ 14000 is £ 5600 on the property inherited.

Inheritance tax on furniture inherited by Wendy from her grandmother (£ 15000 x 40%) = £6000

Part D:

Suitable investment portfolio for the couple:

Though the couple have moderate attitude towards risk and accepts certain amount of risk while

making investment in different investment options however, considering their age and

requirements the investment options shall be selected in such a way to ensure that the risk of

losing hard earn money by the couple is nil. Ensuring stable flow of income with minimum

amount of risk in investment portfolio is the main point to be kept in mind in selecting suitable

investment portfolio for the couple (Hinz, 2011).

Investment in Government bonds, investment in mutual funds are two of the most suitable

investment options considering the requirements and objectives of the couple. These are also

long term investment options that give stable return to the investors over a long period time with

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.