Taxation Law Assessment: Personal Income Tax and Insurance Needs

VerifiedAdded on 2022/09/18

|7

|1047

|28

Homework Assignment

AI Summary

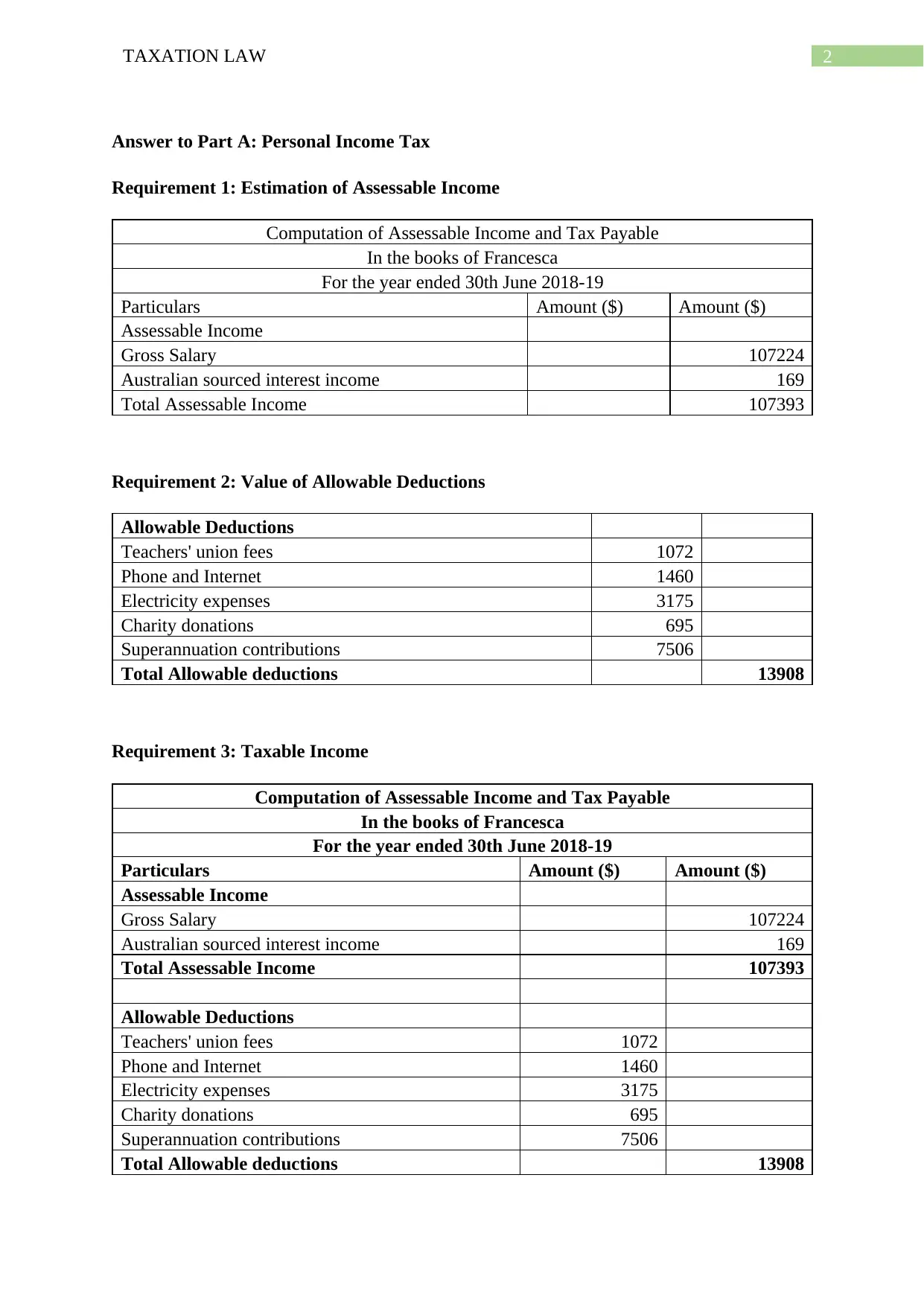

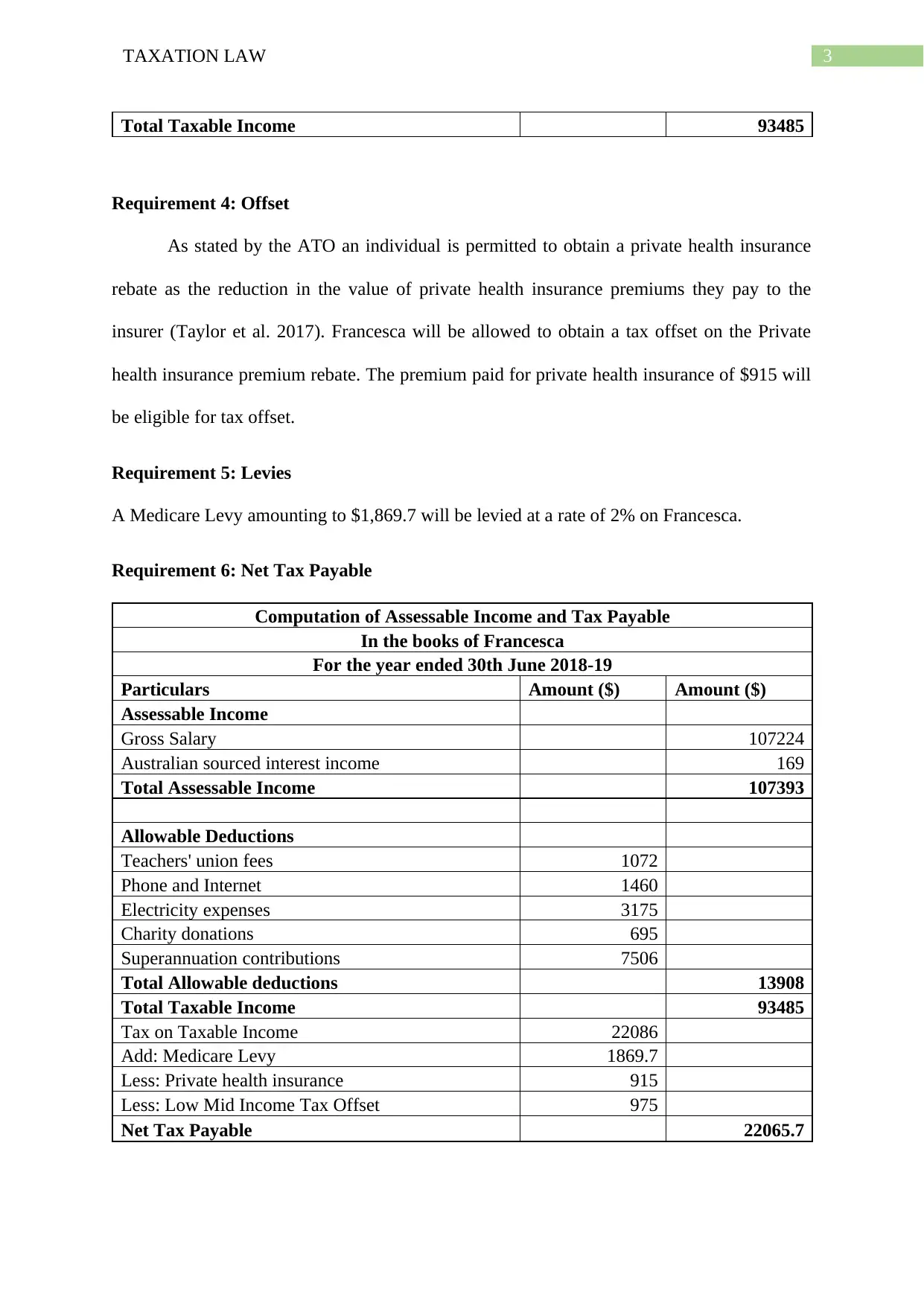

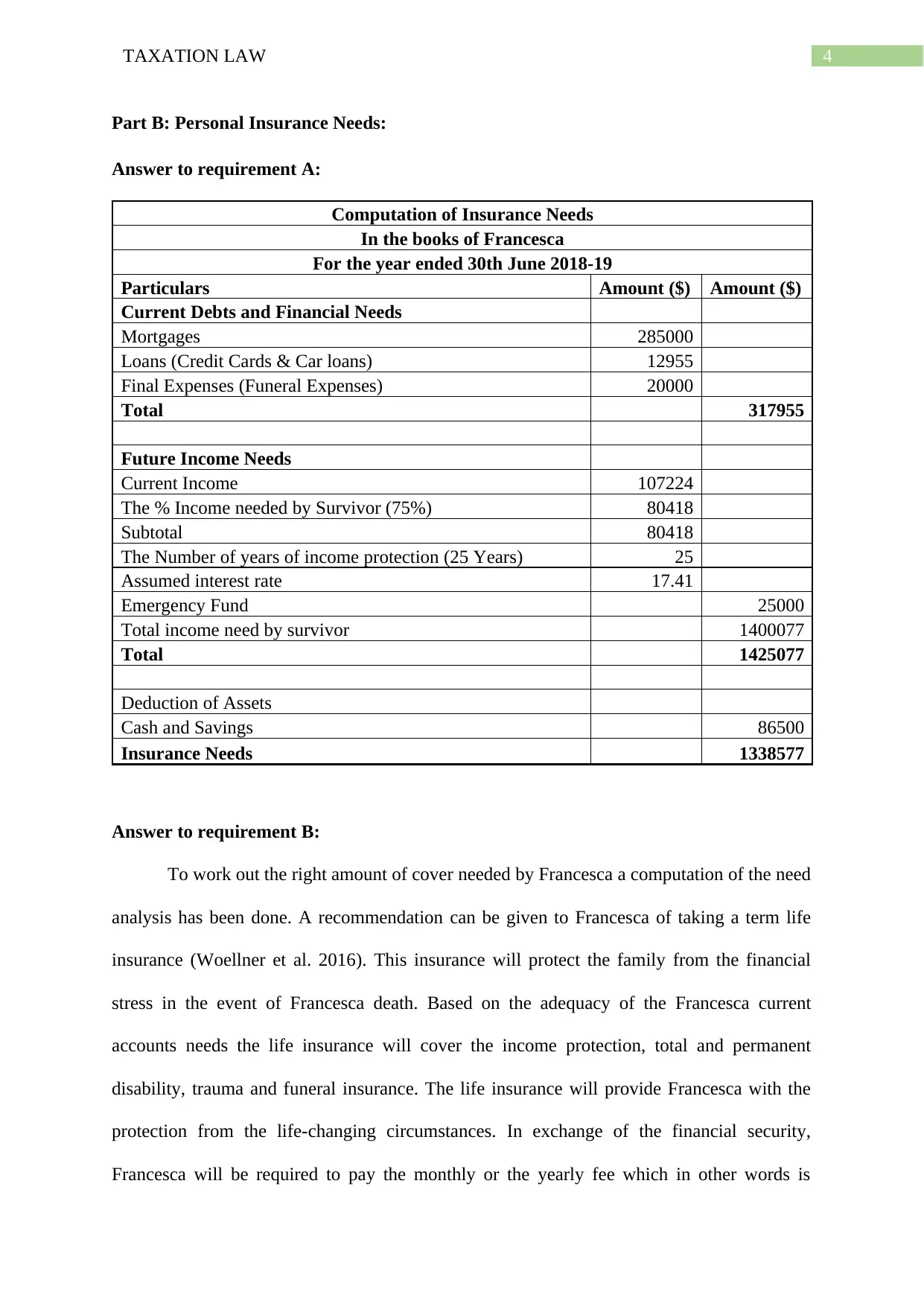

This assignment presents a comprehensive solution to a Taxation Law assessment, focusing on personal income tax and insurance needs. The assignment begins with the calculation of assessable income, incorporating gross salary and Australian sourced interest income. It then proceeds to determine allowable deductions, including teachers' union fees, phone and internet expenses, electricity costs, charitable donations, and superannuation contributions. Following this, the taxable income is calculated, leading to the determination of the tax payable, considering tax offsets like the private health insurance rebate and the low-mid income tax offset, along with the Medicare levy. The second part of the assignment addresses personal insurance needs, calculating current debts, financial needs, and future income requirements to estimate the necessary insurance coverage, recommending term life insurance, and detailing the benefits of life insurance, trauma cover, and income protection. The solution provides a complete analysis, incorporating relevant calculations and recommendations based on the provided scenario.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.