Taxation Law Assignment: Calculating Personal Tax Liability 2019

VerifiedAdded on 2020/10/22

|5

|516

|308

Homework Assignment

AI Summary

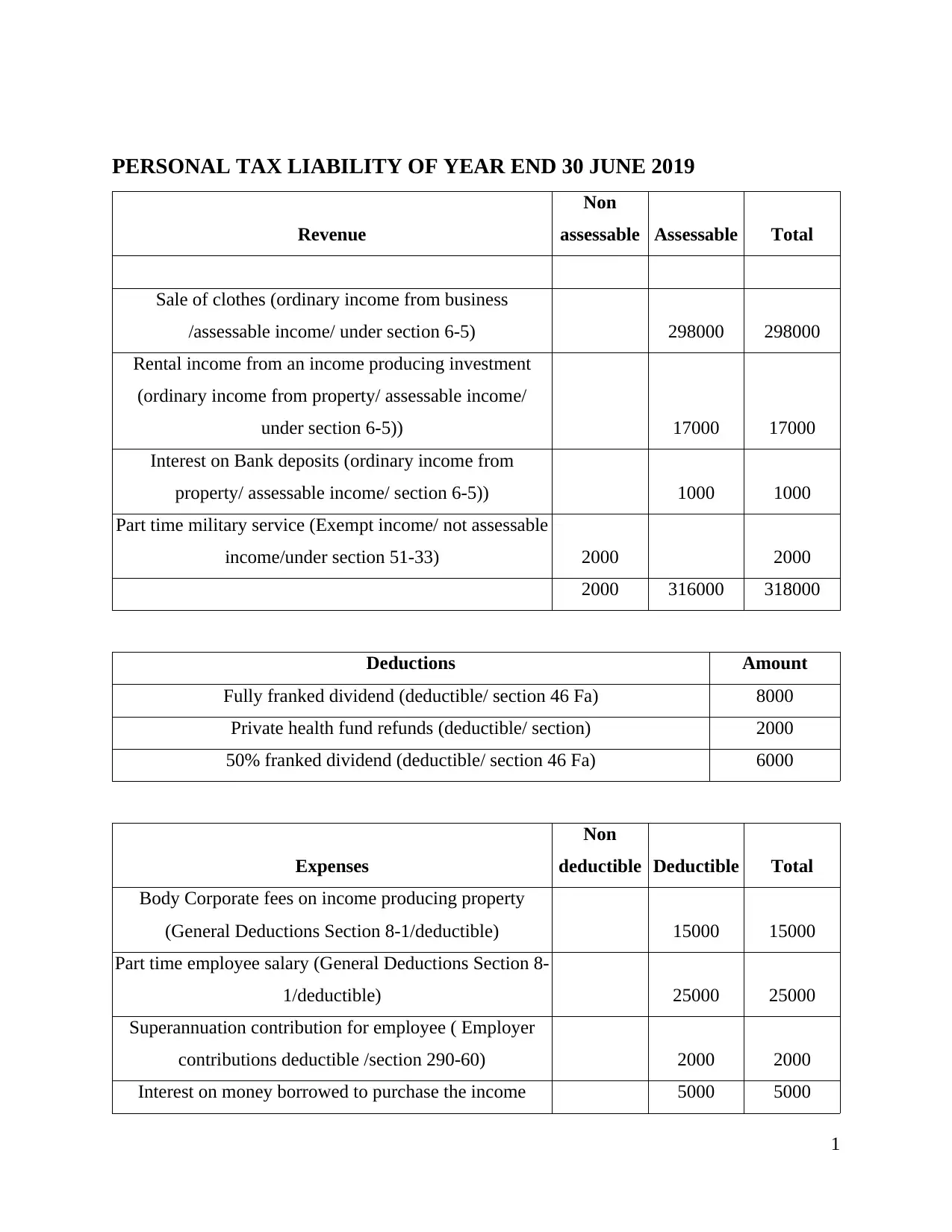

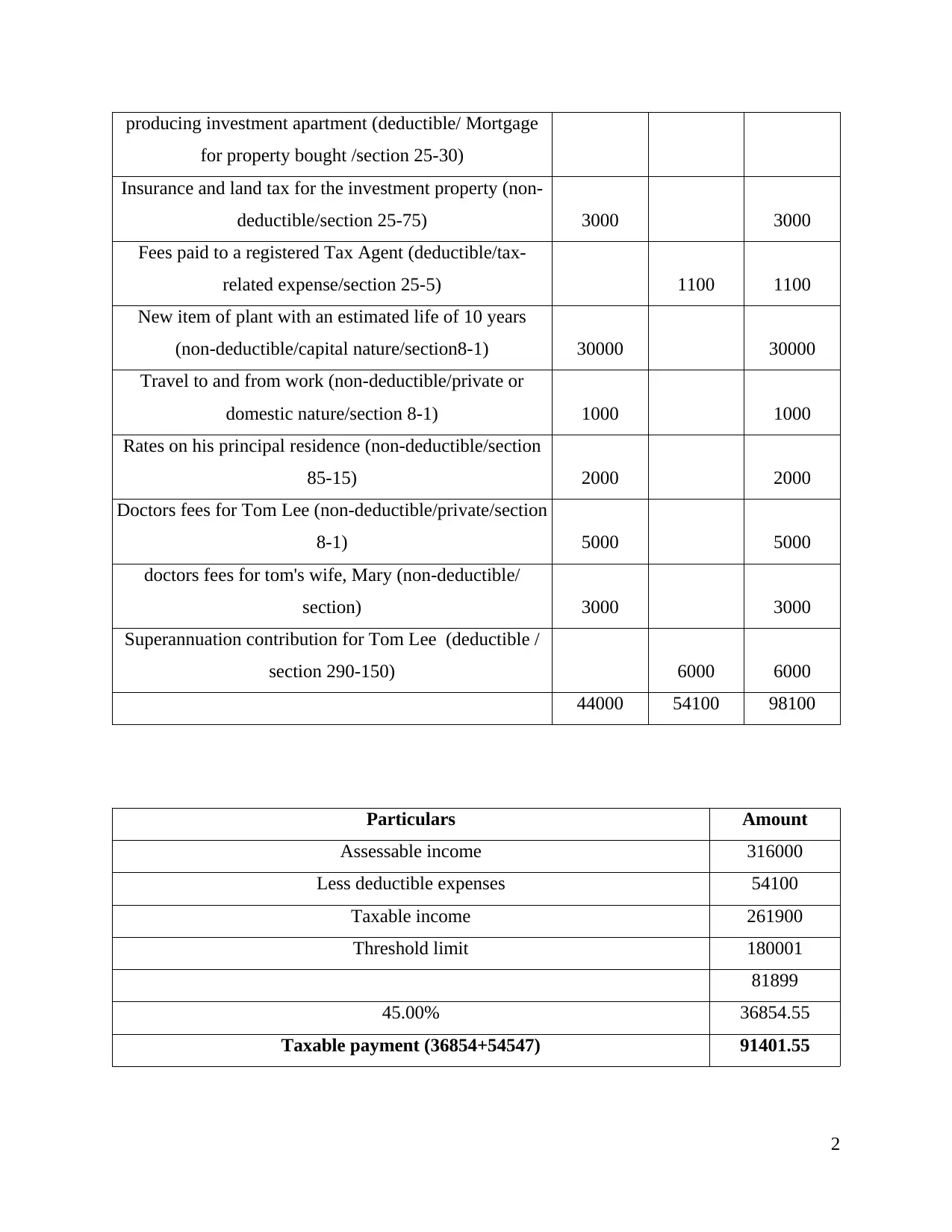

This document presents a detailed solution to a taxation law assignment focusing on calculating personal tax liability for the year ending June 30, 2019. The solution begins with a table outlining various revenue sources, categorizing them as assessable or non-assessable income, and providing corresponding amounts. Key income components include the sale of clothes (business income), rental income, and interest on bank deposits. Exempt income from part-time military service is also identified. The document then details deductible and non-deductible expenses, such as fully and partially franked dividends, body corporate fees, employee salaries, superannuation contributions, interest on investment loans, and various non-deductible expenses. The final section calculates the taxable income by subtracting total deductible expenses from assessable income, and then calculates the tax payable based on the provided threshold and tax rates. The assignment provides a comprehensive analysis of income, deductions, and tax calculation under relevant sections of the taxation law.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.