University Tax Assignment: ACC400 Advanced Taxation Analysis

VerifiedAdded on 2022/09/14

|13

|1222

|10

Homework Assignment

AI Summary

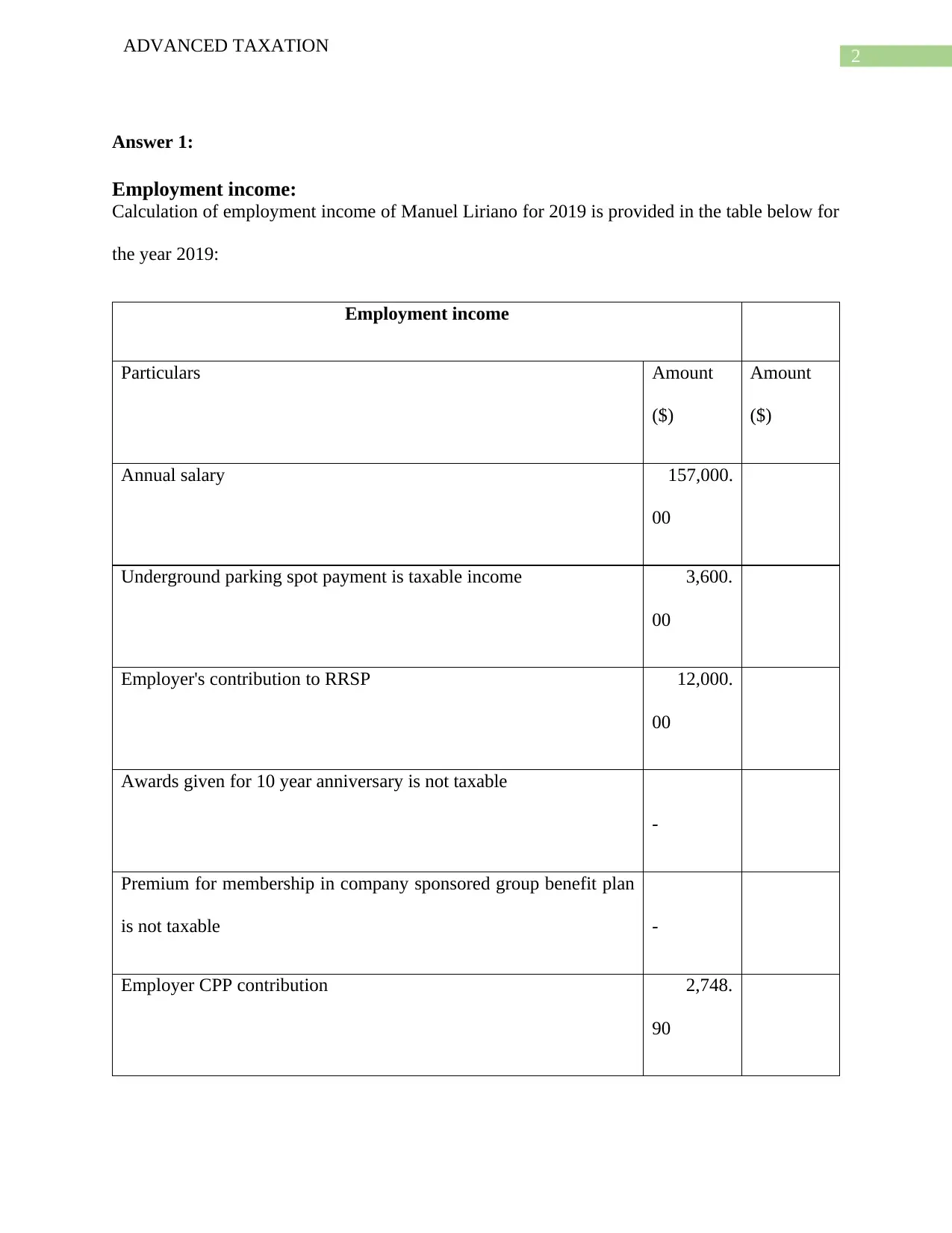

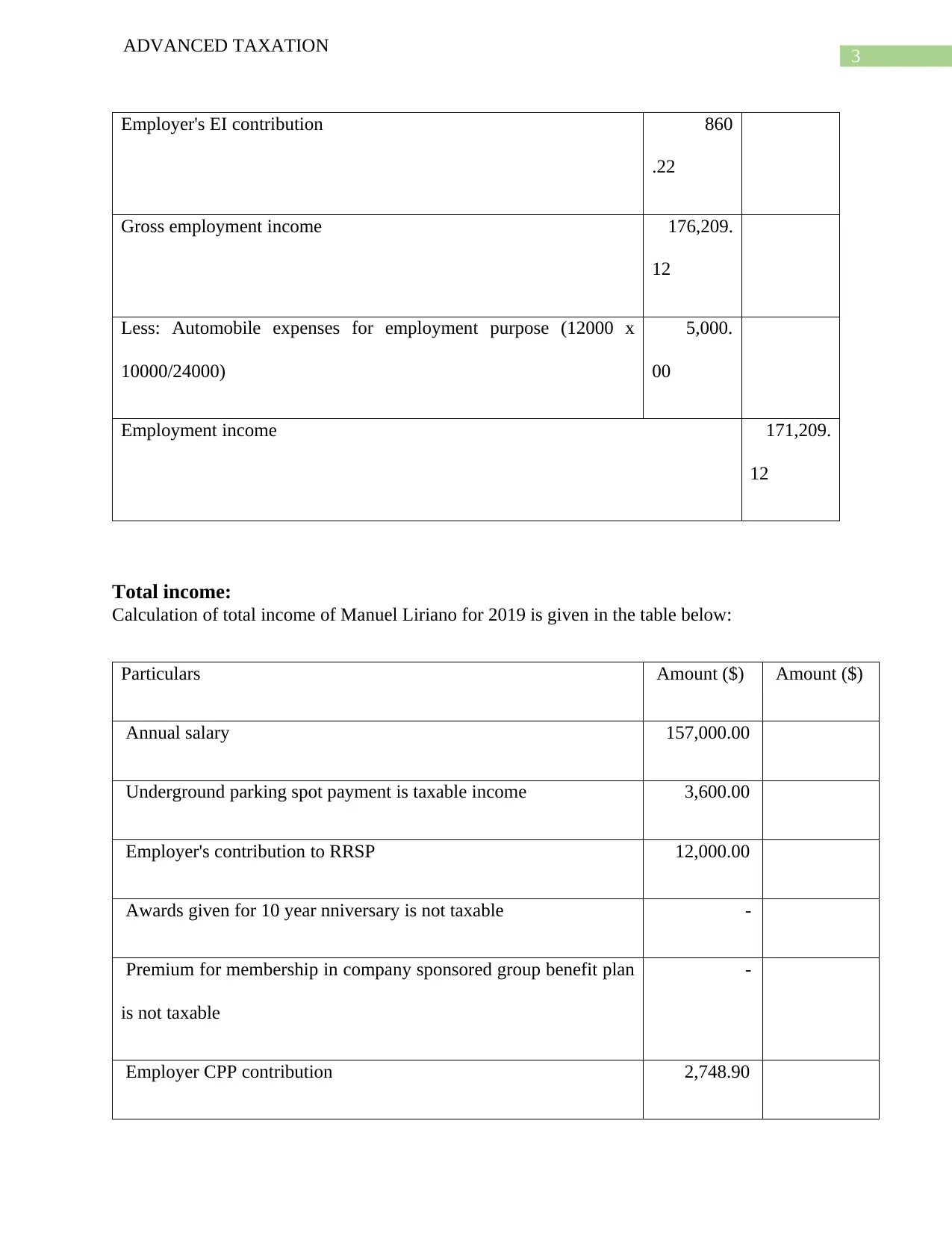

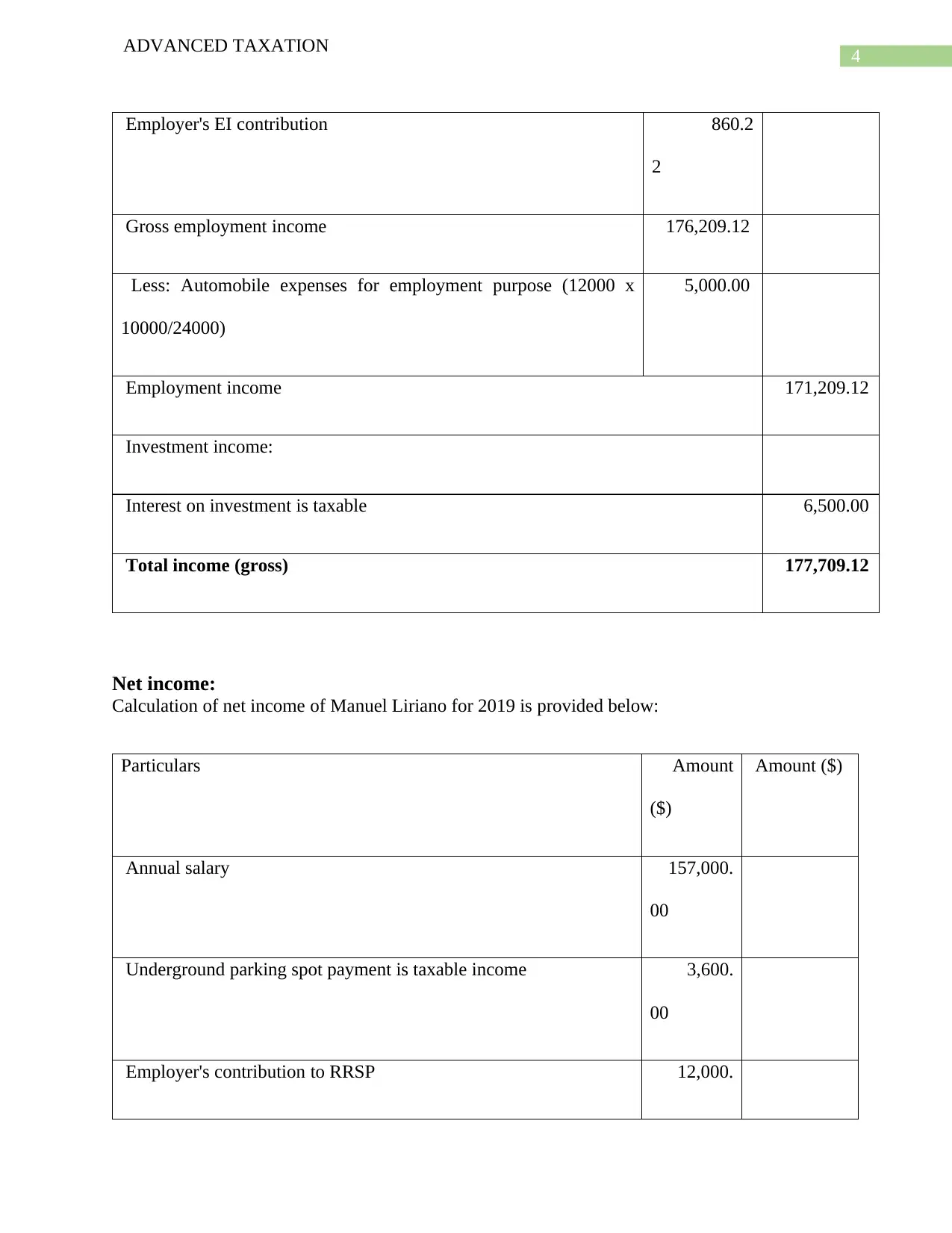

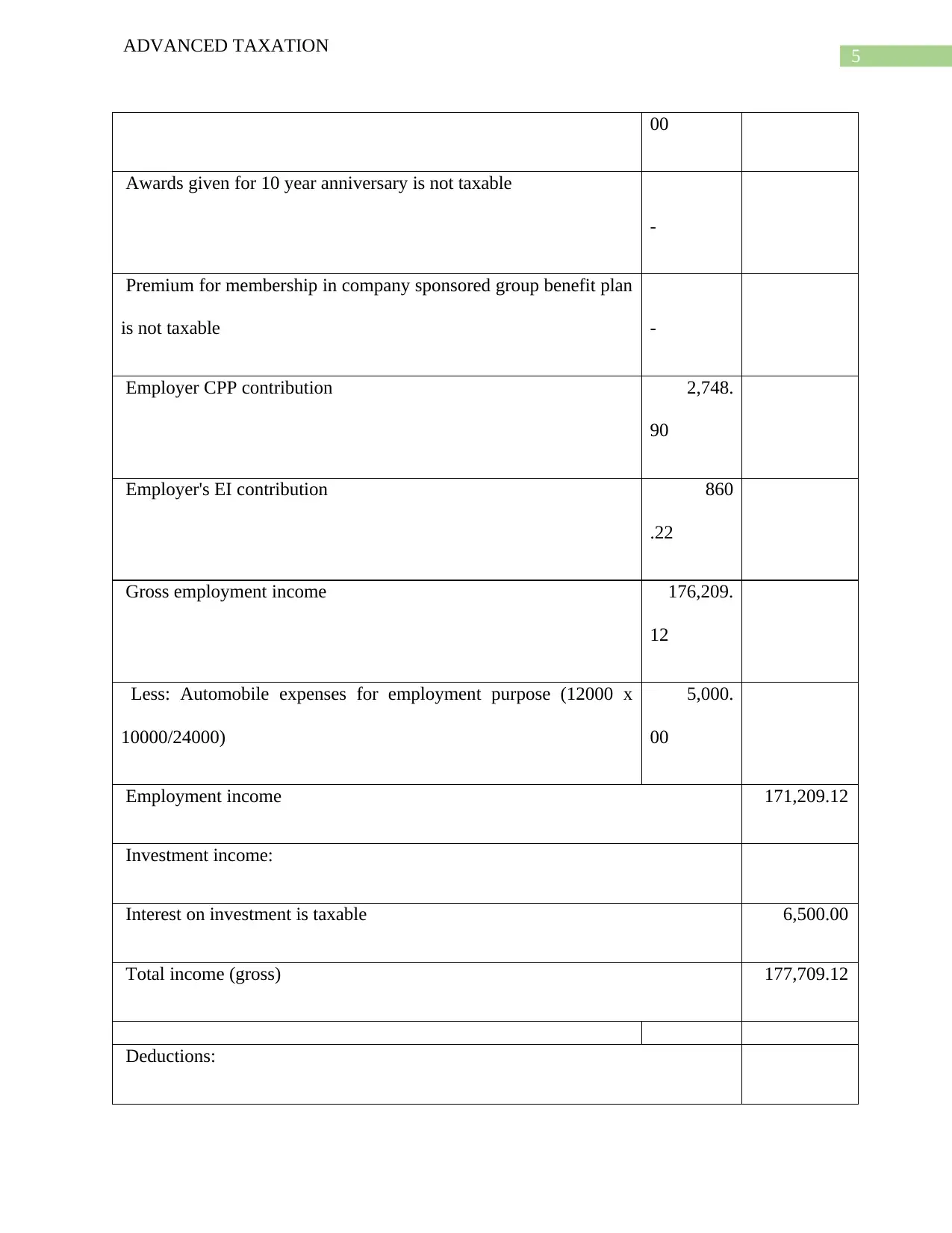

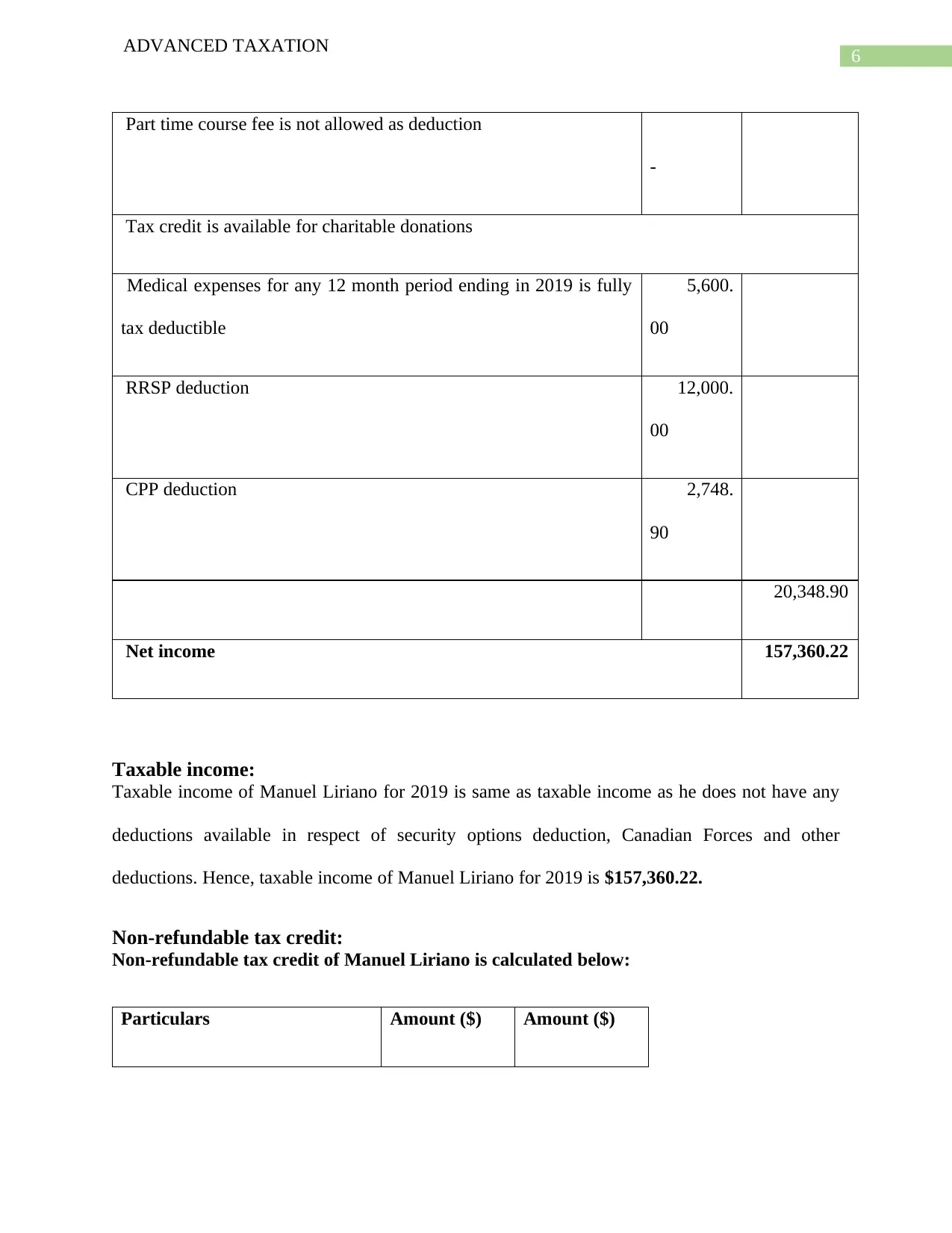

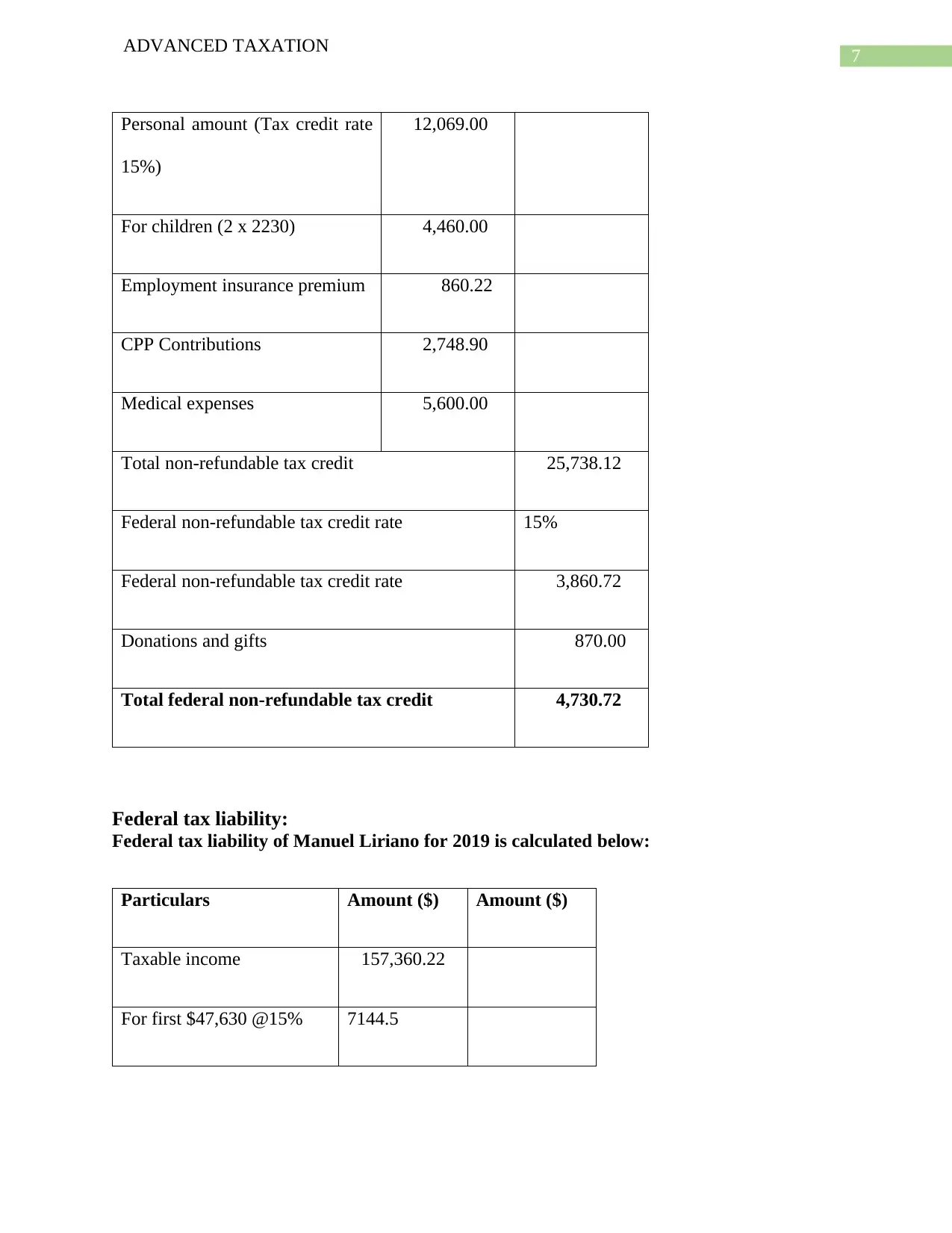

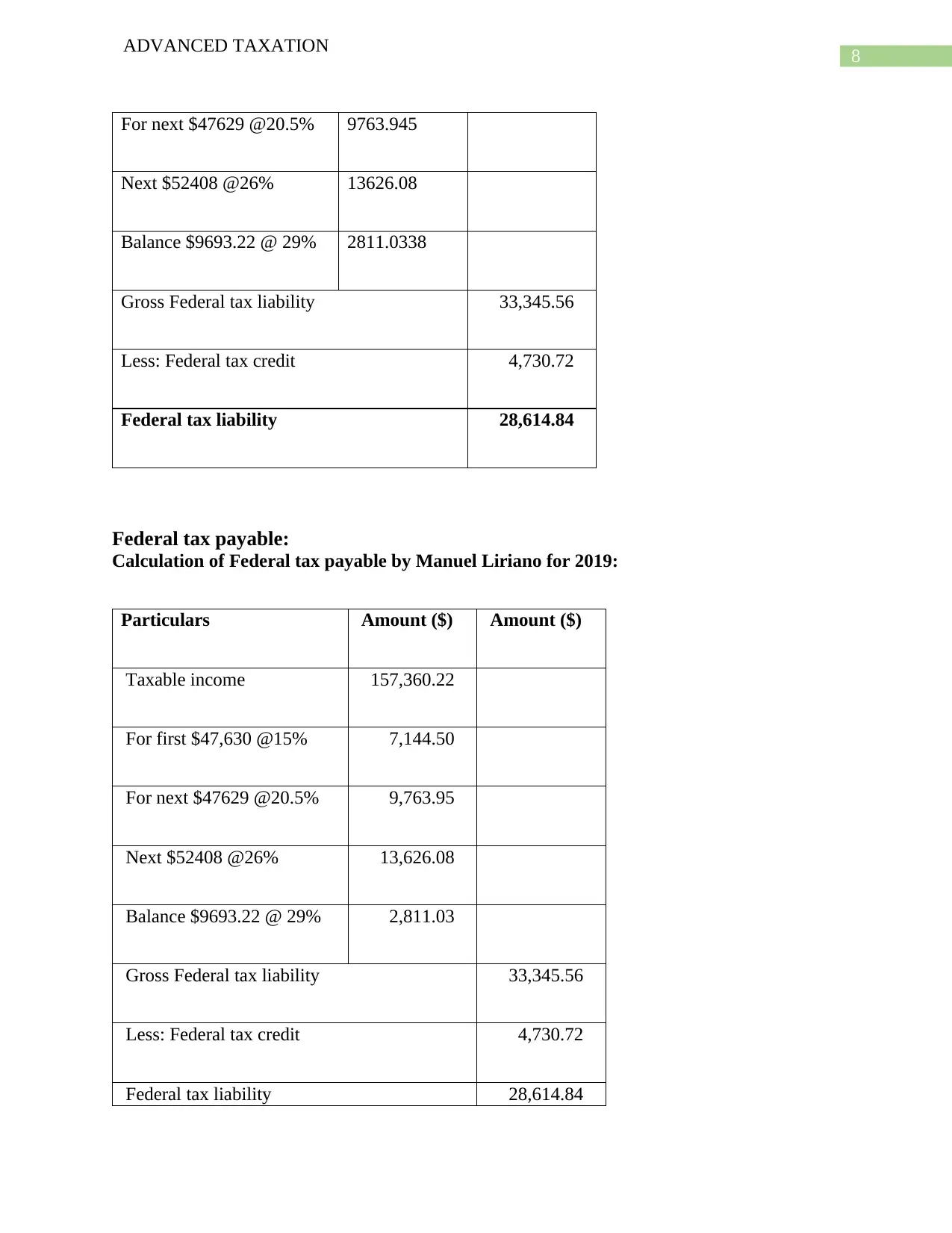

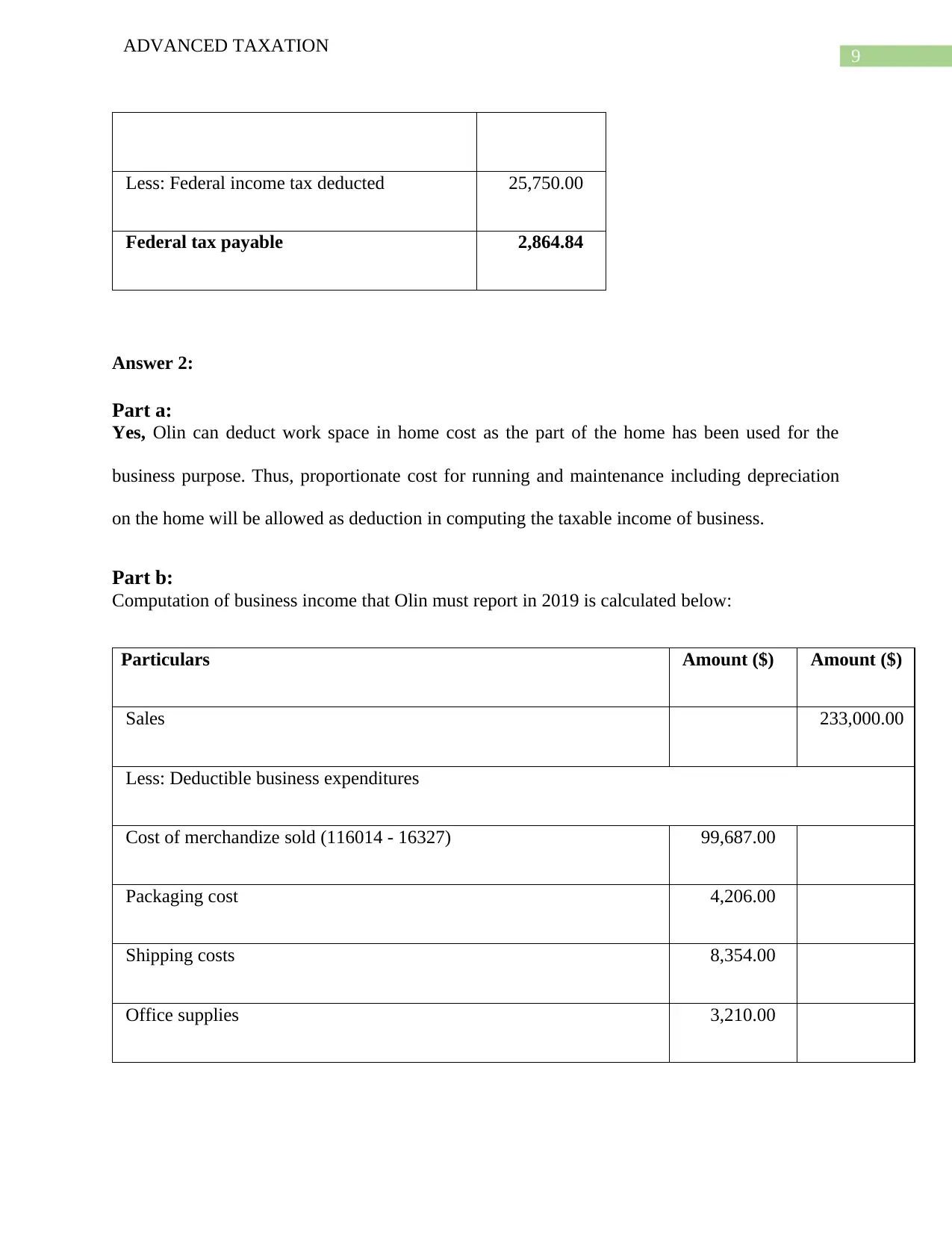

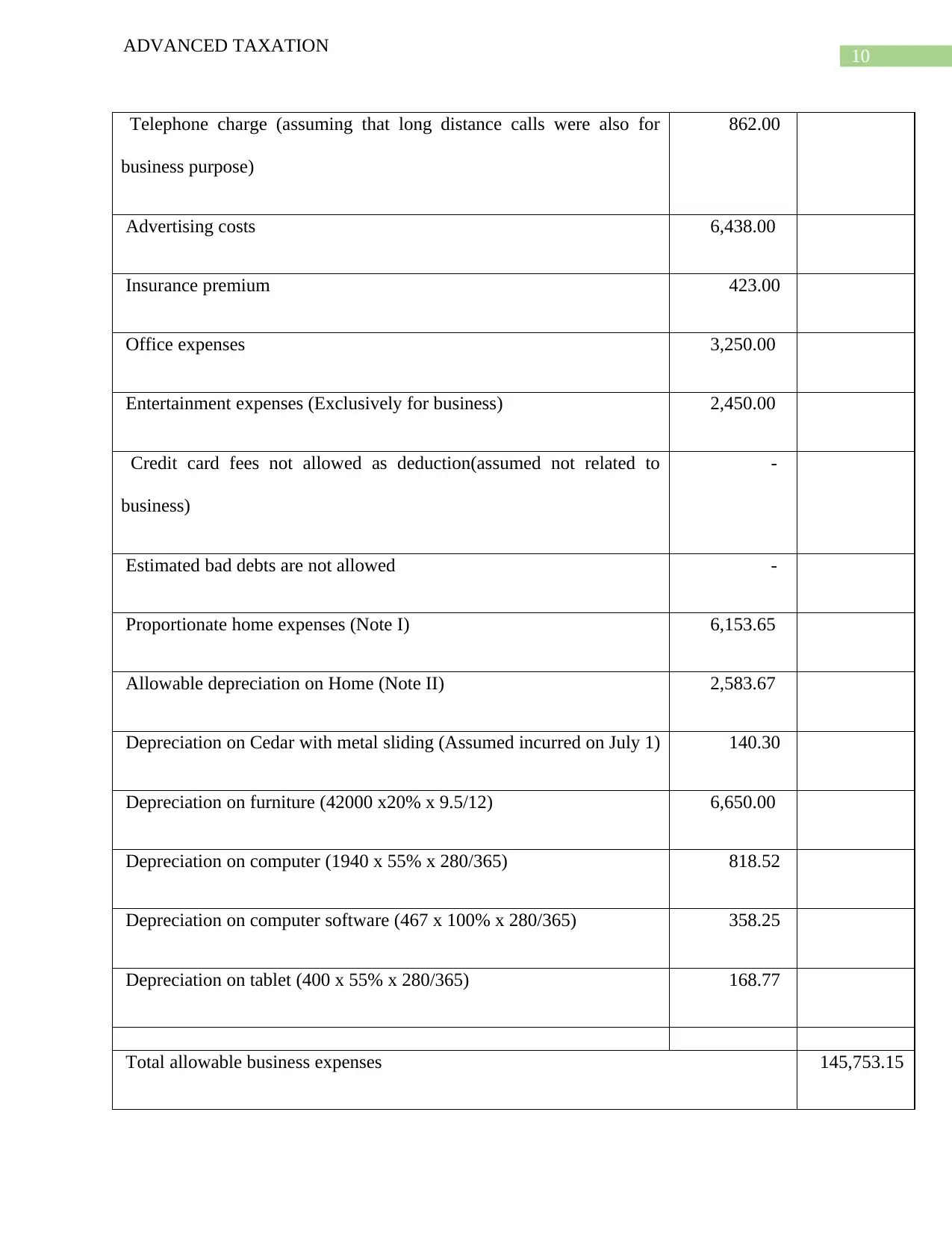

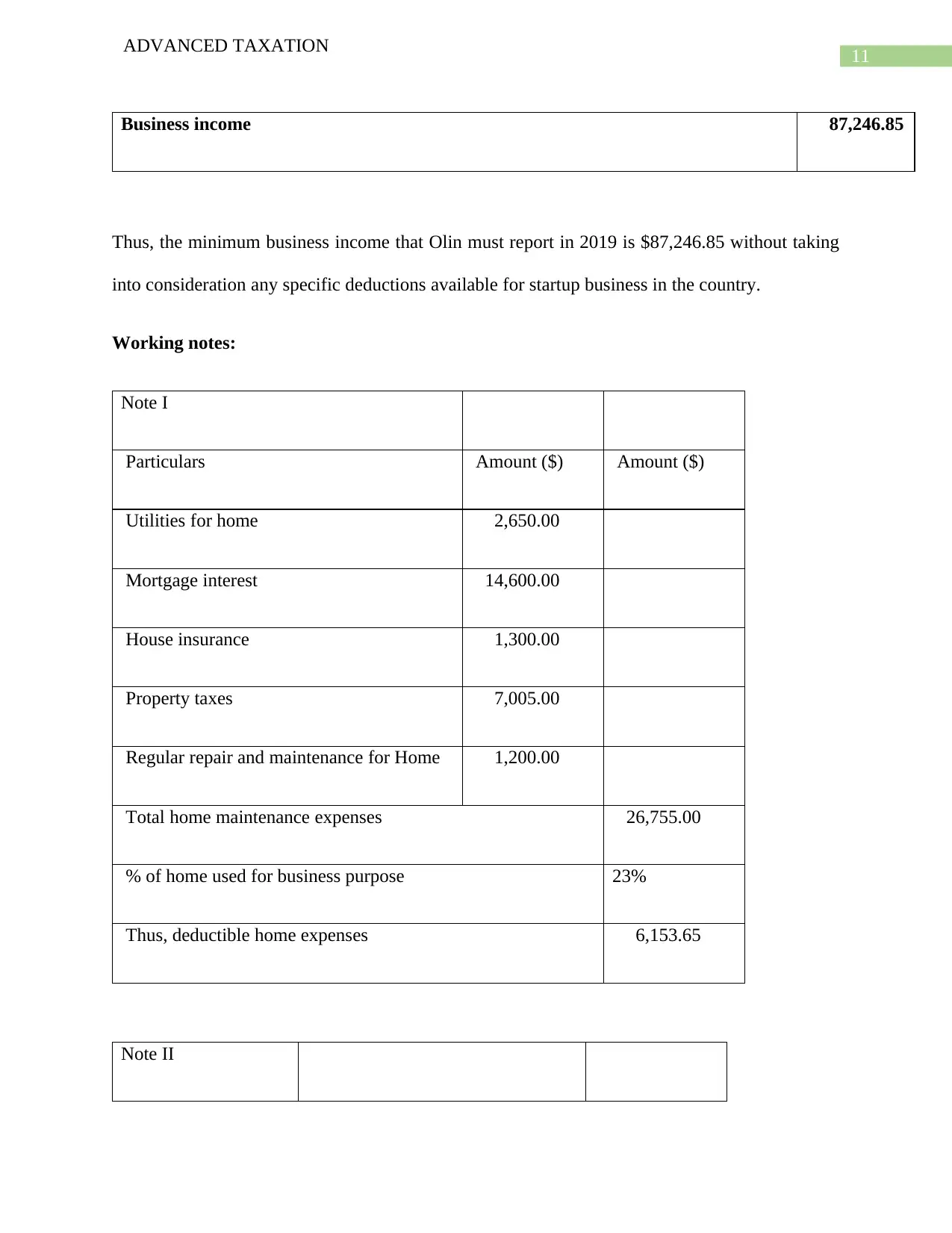

This document presents a detailed solution to an advanced taxation assignment, addressing both personal and business tax scenarios. The solution meticulously calculates Manuel Liriano's employment income, total income, net income, taxable income, non-refundable tax credits, federal tax liability, and federal tax payable for the year 2019. It incorporates various income components, deductions, and tax credits based on the provided information. The assignment also includes an analysis of Olin's business income, determining deductible business expenses, and calculating the final business income. The solution addresses the deductibility of home office expenses, including depreciation and proportionate costs. Furthermore, the solution details the tax implications of various employment benefits, investment income, and business expenditures, providing a comprehensive understanding of the tax calculations involved. The solution adheres to the assignment brief, providing a clear and organized breakdown of the calculations and analysis required for the assignment.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.