Taxation Assessment: Analyzing Peter Smith's Tax Situation

VerifiedAdded on 2022/11/30

|11

|1925

|391

Homework Assignment

AI Summary

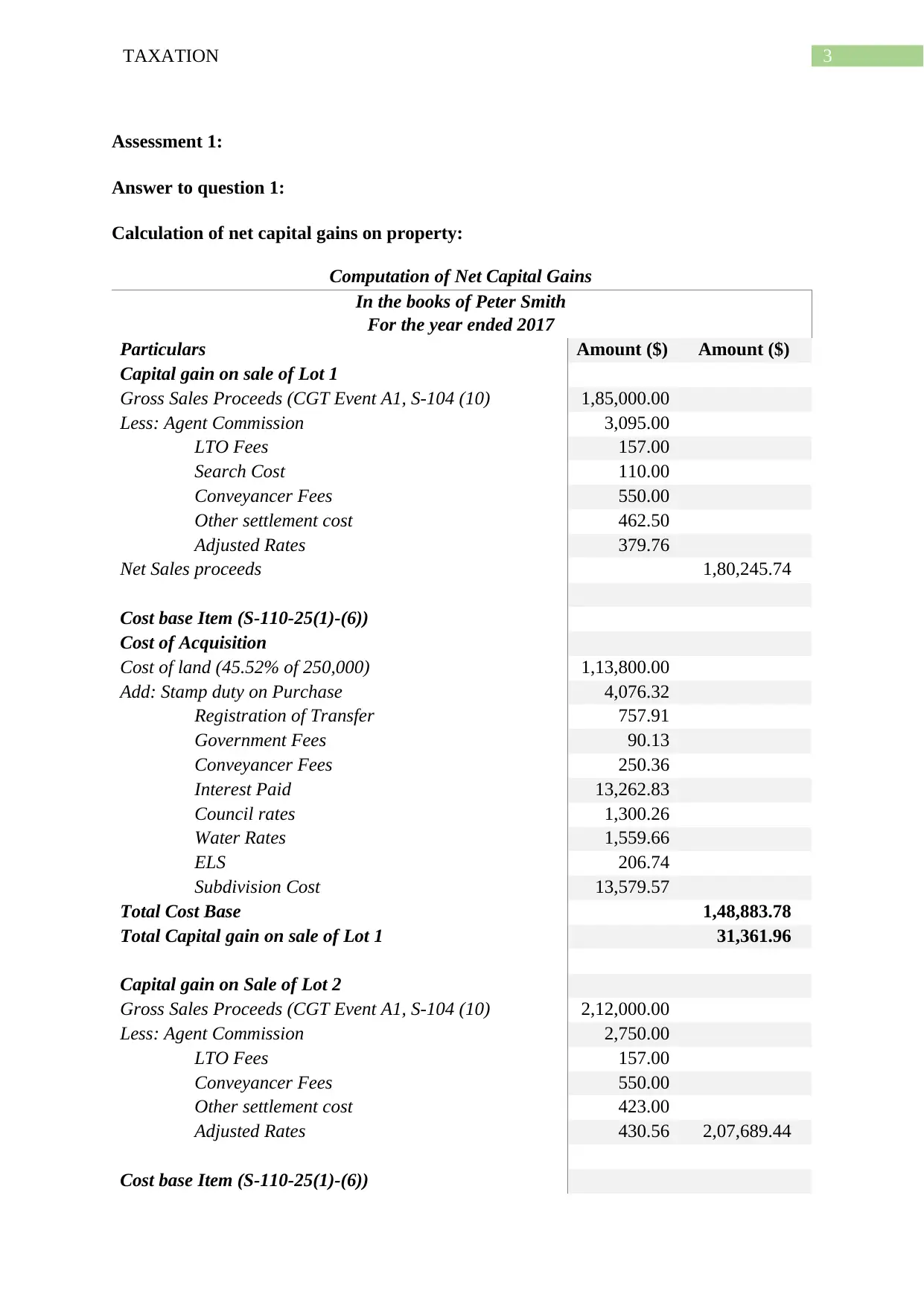

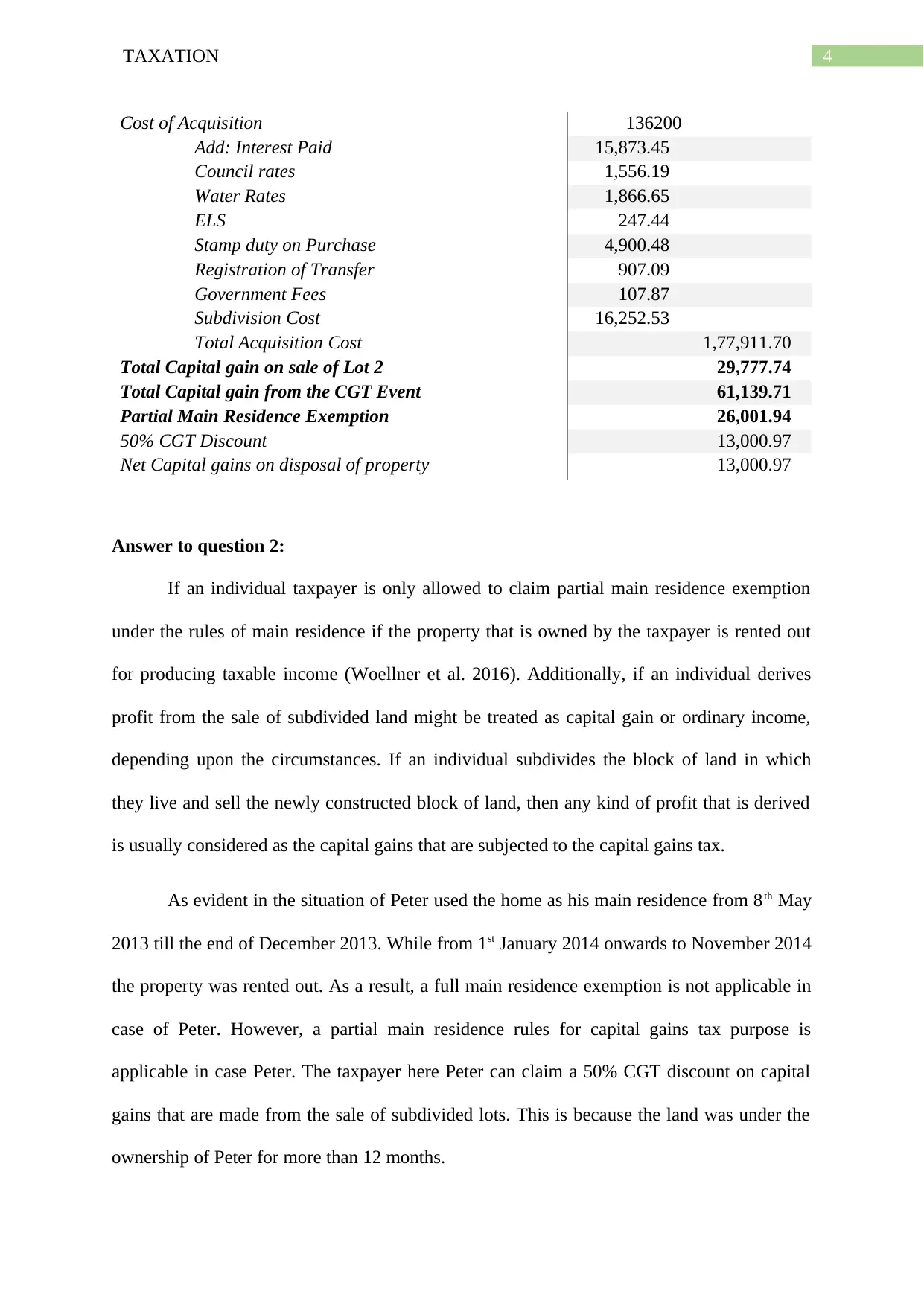

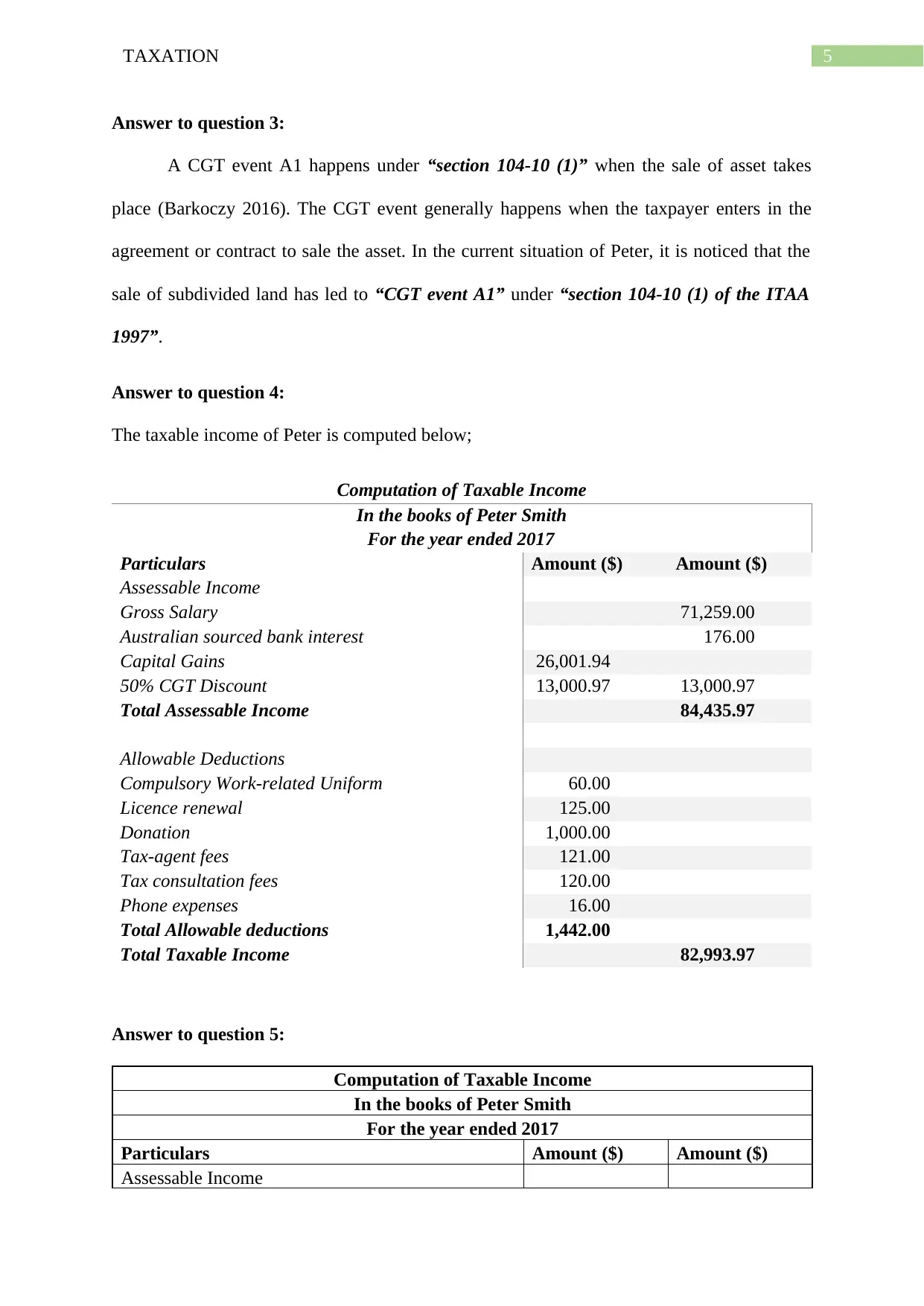

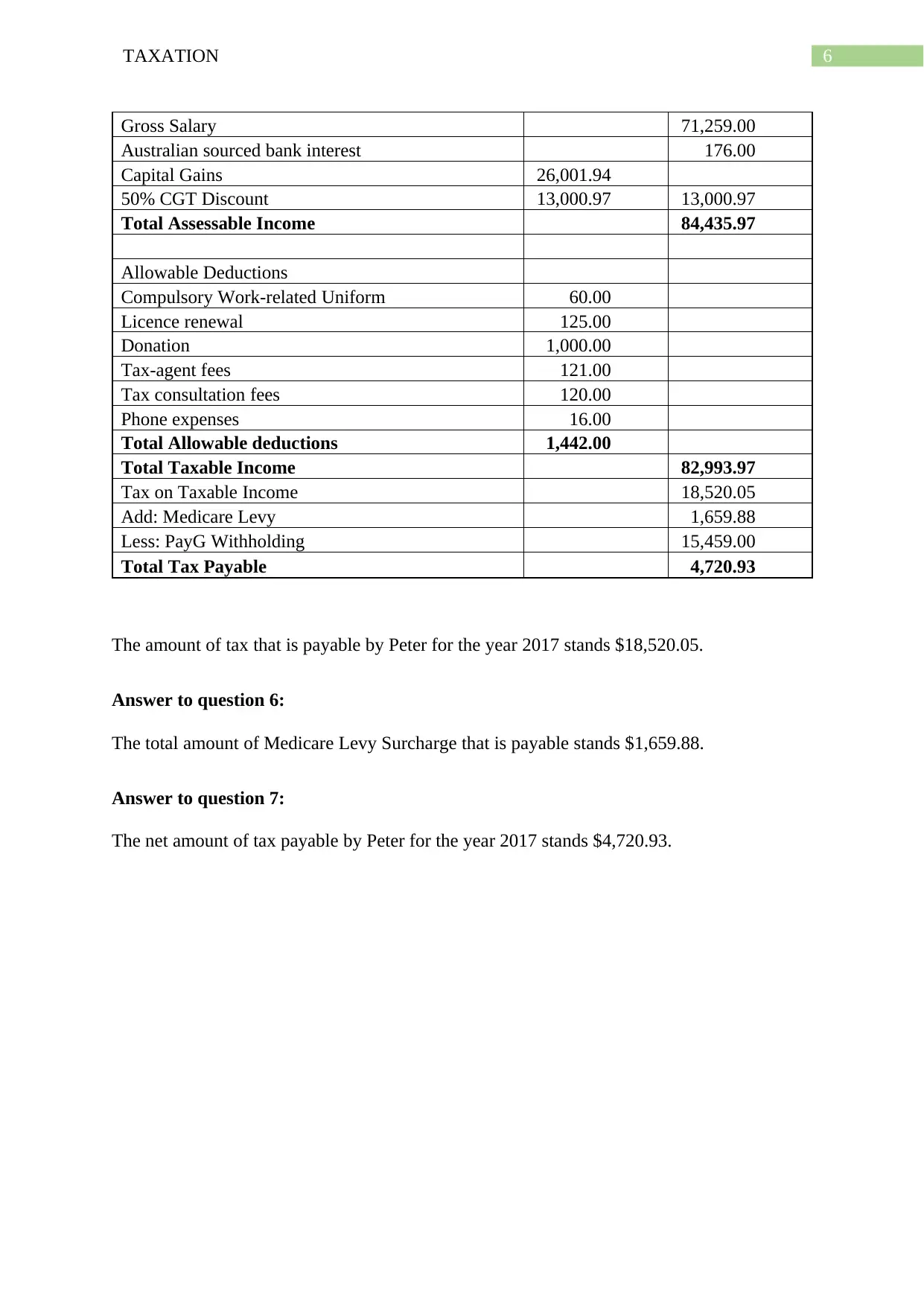

This assignment solution provides a comprehensive analysis of Peter Smith's tax situation, addressing two assessments. Assessment 1 focuses on calculating net capital gains from property sales, determining taxable income, and computing tax payable, including Medicare levy and PAYG. It covers relevant expenses, deductions, and the application of CGT rules, including partial main residence exemption and the 50% CGT discount. Assessment 2 builds upon the initial scenario by incorporating the purchase of an air conditioner and its depreciation, exploring capital allowances and their impact on the capital gains calculation and overall tax position. The solution also discusses capital allowance regimes, tax planning, and avoidance strategies, and provides detailed calculations and explanations based on the provided facts and Australian taxation law. The analysis considers the implications of job loss and rental income, offering tax advice and outlining the differences between tax planning and avoidance.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.