Financial Analysis of Petrochina: A Detailed Report

VerifiedAdded on 2021/04/16

|19

|4459

|22

Report

AI Summary

This report provides a comprehensive financial analysis of Petrochina, evaluating its performance over two years. It examines profitability, liquidity, and solvency ratios, revealing a decline in profitability and challenges in liquidity due to falling market demand and increasing obligations. The analysis highlights Petrochina's strong solvency position, achieved through equity financing. The report also discusses the importance of independent audits, referencing Price Water House Coopers' audit of Petrochina. Furthermore, it explores the impact of the 2007/08 financial crisis on the company and draws lessons for international organizations. The report concludes that while Petrochina faces profitability and liquidity challenges, its solvency remains stable due to its financial strategies.

Running head: INTERNATIONAL ACCOUNTING AND FINANCE ISSUES

International Accounting and Finance Issues

Name of the University:

Name of the Student:

Author’s Note:

Course ID:

International Accounting and Finance Issues

Name of the University:

Name of the Student:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1INTERNATIONAL ACCOUNTING AND FINANCE ISSUES

Executive Summary

The report is deemed to provide with an opportunity to develop written communication

skills along with working with global finance and accounting issues. From the evaluation

of ratios, it has been found that Petrochina is struggling in terms of profitability, liquidity

and working capital due to falling demand in the market and increasing short-term dues

and obligations. However, it has effective solvency position in the market, since it has

placed additional emphasis on raising funds through issuance of equity shares, instead

of relying on debt financing. This is the reason for which several unconventional oil and

gas organisations along with Petrochina have dealt with constant bankruptcy in foreign

lands.

Executive Summary

The report is deemed to provide with an opportunity to develop written communication

skills along with working with global finance and accounting issues. From the evaluation

of ratios, it has been found that Petrochina is struggling in terms of profitability, liquidity

and working capital due to falling demand in the market and increasing short-term dues

and obligations. However, it has effective solvency position in the market, since it has

placed additional emphasis on raising funds through issuance of equity shares, instead

of relying on debt financing. This is the reason for which several unconventional oil and

gas organisations along with Petrochina have dealt with constant bankruptcy in foreign

lands.

2INTERNATIONAL ACCOUNTING AND FINANCE ISSUES

Table of Contents

Introduction:.......................................................................................................................3

Background:.......................................................................................................................3

Financial Statement Analysis:...........................................................................................3

Independent Audit and Assurance:...................................................................................8

Impact on Financial Crisis on Petrochina Globally:.........................................................10

Conclusion:......................................................................................................................12

References:......................................................................................................................14

Appendices:.....................................................................................................................17

Table of Contents

Introduction:.......................................................................................................................3

Background:.......................................................................................................................3

Financial Statement Analysis:...........................................................................................3

Independent Audit and Assurance:...................................................................................8

Impact on Financial Crisis on Petrochina Globally:.........................................................10

Conclusion:......................................................................................................................12

References:......................................................................................................................14

Appendices:.....................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3INTERNATIONAL ACCOUNTING AND FINANCE ISSUES

Introduction:

The report is deemed to provide with an opportunity to develop written

communication skills along with working with global finance and accounting issues.

Petrochina has established its business as a joint stock organization along with less

liability within the Company law of the People’s Republic of China as an aspect of

restructuring “China National Petroleum Corporation” (Unda, 2015). The objective of the

paper is to evaluate the financial situation of Petrochina Company for the past two

years. Moreover, the report will also evaluate the independent audit of the organizations

is a vital aspect of maintaining assurance and confidence. Moreover, it will also explain

the extent to which the financial crisis of 2007/08 impacts the company’s business

internationally. Additionally, it will also explain the lessons regarding the crisis for

international organizations like Petrochina.

Background:

Petrochina Company is selected for the reason that it is positioned as the

renowned oil and gas manufacturer and seller attaining a major position within the oil

and gas sector. The company is positioned as among the oil companies all through the

world. The objective of the paper is to evaluate the financial situation of Petrochina

Company for the past two years. Ratio analysis will be carried out to understand the

financial position of the organization that will include ratios such as liquidity, solvency,

working capital, profitability and performance.

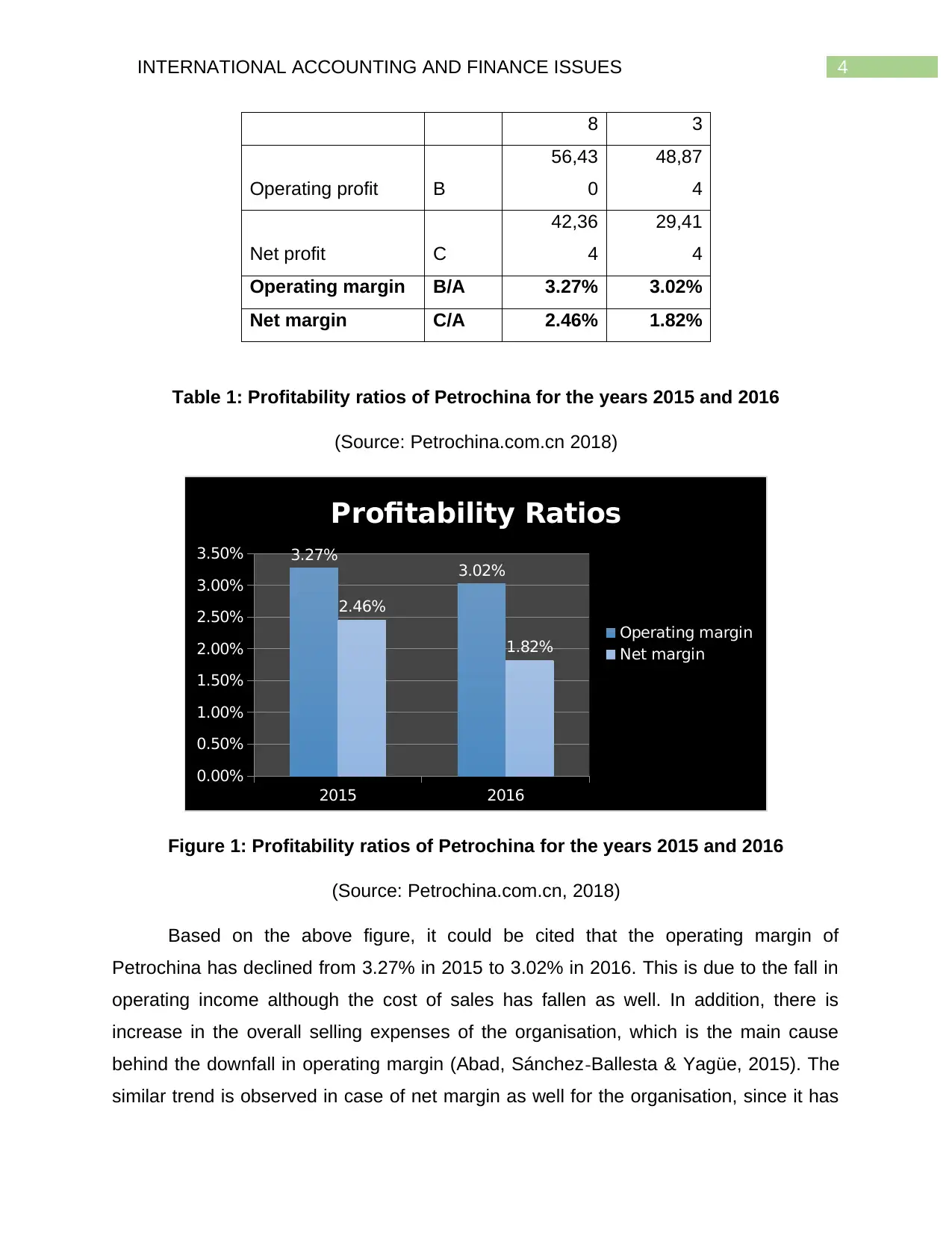

Financial Statement Analysis:

Profitability analysis:

The profitability analysis of Petrochina has been carried out with the help of the

following ratios, which are presented in the form of a table as follows:

Profitability Ratios:-

Particulars

Detail

s 2015 2016

Sales A 17,25,42 16,16,90

Introduction:

The report is deemed to provide with an opportunity to develop written

communication skills along with working with global finance and accounting issues.

Petrochina has established its business as a joint stock organization along with less

liability within the Company law of the People’s Republic of China as an aspect of

restructuring “China National Petroleum Corporation” (Unda, 2015). The objective of the

paper is to evaluate the financial situation of Petrochina Company for the past two

years. Moreover, the report will also evaluate the independent audit of the organizations

is a vital aspect of maintaining assurance and confidence. Moreover, it will also explain

the extent to which the financial crisis of 2007/08 impacts the company’s business

internationally. Additionally, it will also explain the lessons regarding the crisis for

international organizations like Petrochina.

Background:

Petrochina Company is selected for the reason that it is positioned as the

renowned oil and gas manufacturer and seller attaining a major position within the oil

and gas sector. The company is positioned as among the oil companies all through the

world. The objective of the paper is to evaluate the financial situation of Petrochina

Company for the past two years. Ratio analysis will be carried out to understand the

financial position of the organization that will include ratios such as liquidity, solvency,

working capital, profitability and performance.

Financial Statement Analysis:

Profitability analysis:

The profitability analysis of Petrochina has been carried out with the help of the

following ratios, which are presented in the form of a table as follows:

Profitability Ratios:-

Particulars

Detail

s 2015 2016

Sales A 17,25,42 16,16,90

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4INTERNATIONAL ACCOUNTING AND FINANCE ISSUES

8 3

Operating profit B

56,43

0

48,87

4

Net profit C

42,36

4

29,41

4

Operating margin B/A 3.27% 3.02%

Net margin C/A 2.46% 1.82%

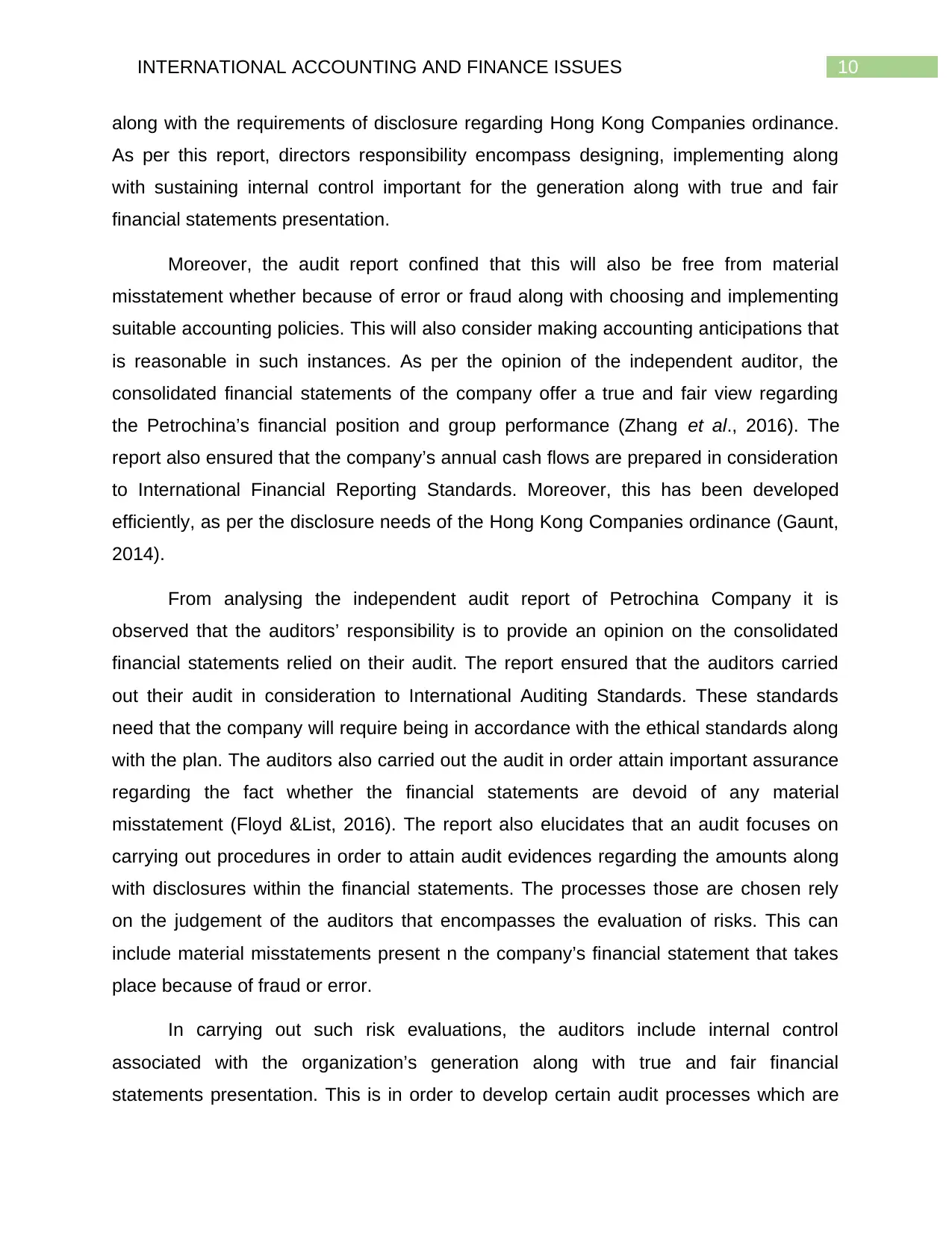

Table 1: Profitability ratios of Petrochina for the years 2015 and 2016

(Source: Petrochina.com.cn 2018)

2015 2016

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50% 3.27%

3.02%

2.46%

1.82%

Profitability Ratios

Operating margin

Net margin

Figure 1: Profitability ratios of Petrochina for the years 2015 and 2016

(Source: Petrochina.com.cn, 2018)

Based on the above figure, it could be cited that the operating margin of

Petrochina has declined from 3.27% in 2015 to 3.02% in 2016. This is due to the fall in

operating income although the cost of sales has fallen as well. In addition, there is

increase in the overall selling expenses of the organisation, which is the main cause

behind the downfall in operating margin (Abad, Sánchez‐Ballesta & Yagüe, 2015). The

similar trend is observed in case of net margin as well for the organisation, since it has

8 3

Operating profit B

56,43

0

48,87

4

Net profit C

42,36

4

29,41

4

Operating margin B/A 3.27% 3.02%

Net margin C/A 2.46% 1.82%

Table 1: Profitability ratios of Petrochina for the years 2015 and 2016

(Source: Petrochina.com.cn 2018)

2015 2016

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50% 3.27%

3.02%

2.46%

1.82%

Profitability Ratios

Operating margin

Net margin

Figure 1: Profitability ratios of Petrochina for the years 2015 and 2016

(Source: Petrochina.com.cn, 2018)

Based on the above figure, it could be cited that the operating margin of

Petrochina has declined from 3.27% in 2015 to 3.02% in 2016. This is due to the fall in

operating income although the cost of sales has fallen as well. In addition, there is

increase in the overall selling expenses of the organisation, which is the main cause

behind the downfall in operating margin (Abad, Sánchez‐Ballesta & Yagüe, 2015). The

similar trend is observed in case of net margin as well for the organisation, since it has

5INTERNATIONAL ACCOUNTING AND FINANCE ISSUES

dropped to 1.82% in 2016 from 2.46% in 2015. The possible reasons identified behind

this downfall include the fall in market demand, increase in non-operating expense and

decline in non-operating income as well (Contessotto & Moroney, 2014). Hence, from

the profitability point of view, Petrochina is not in a healthy position in the oil and gas

sector of the nation.

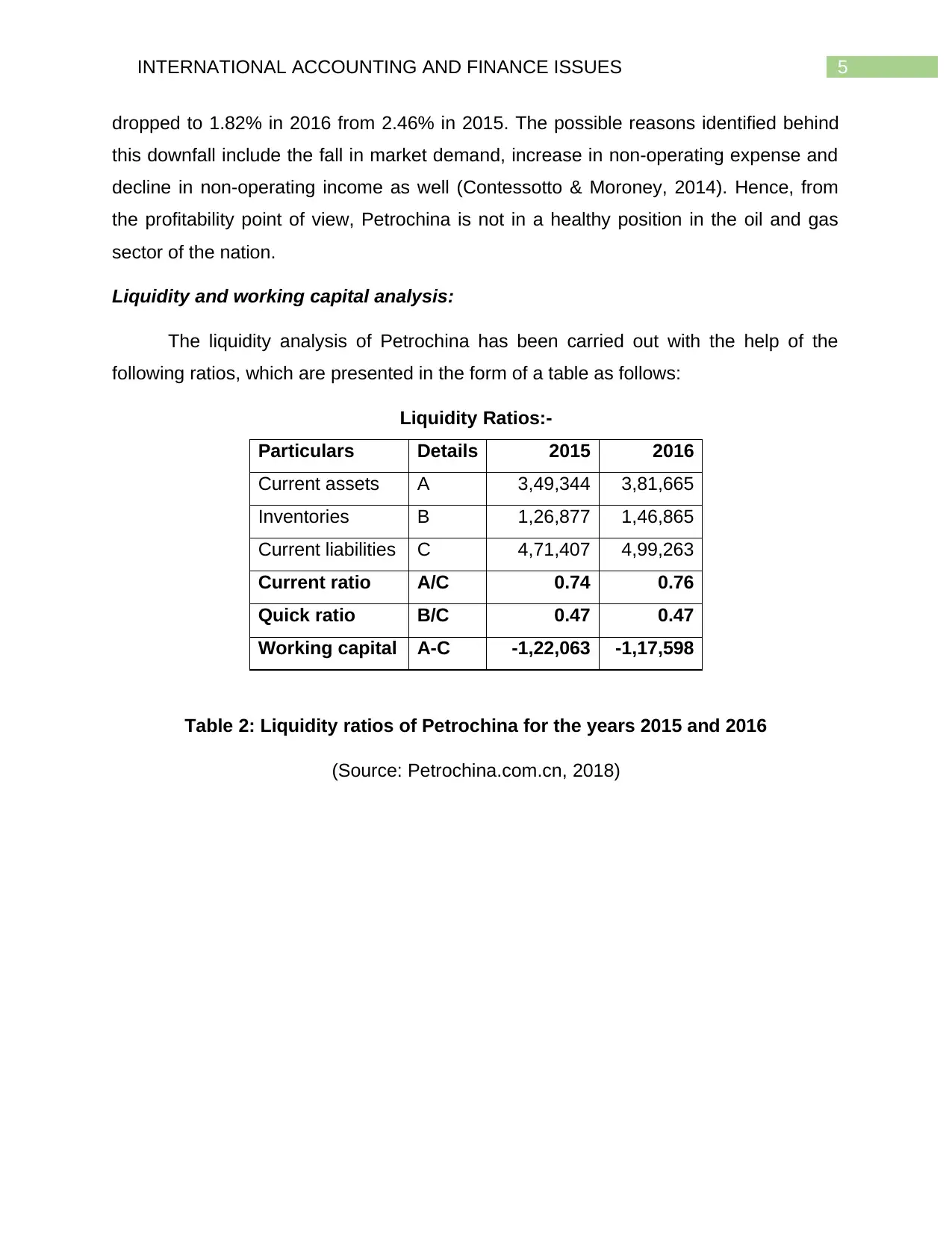

Liquidity and working capital analysis:

The liquidity analysis of Petrochina has been carried out with the help of the

following ratios, which are presented in the form of a table as follows:

Liquidity Ratios:-

Particulars Details 2015 2016

Current assets A 3,49,344 3,81,665

Inventories B 1,26,877 1,46,865

Current liabilities C 4,71,407 4,99,263

Current ratio A/C 0.74 0.76

Quick ratio B/C 0.47 0.47

Working capital A-C -1,22,063 -1,17,598

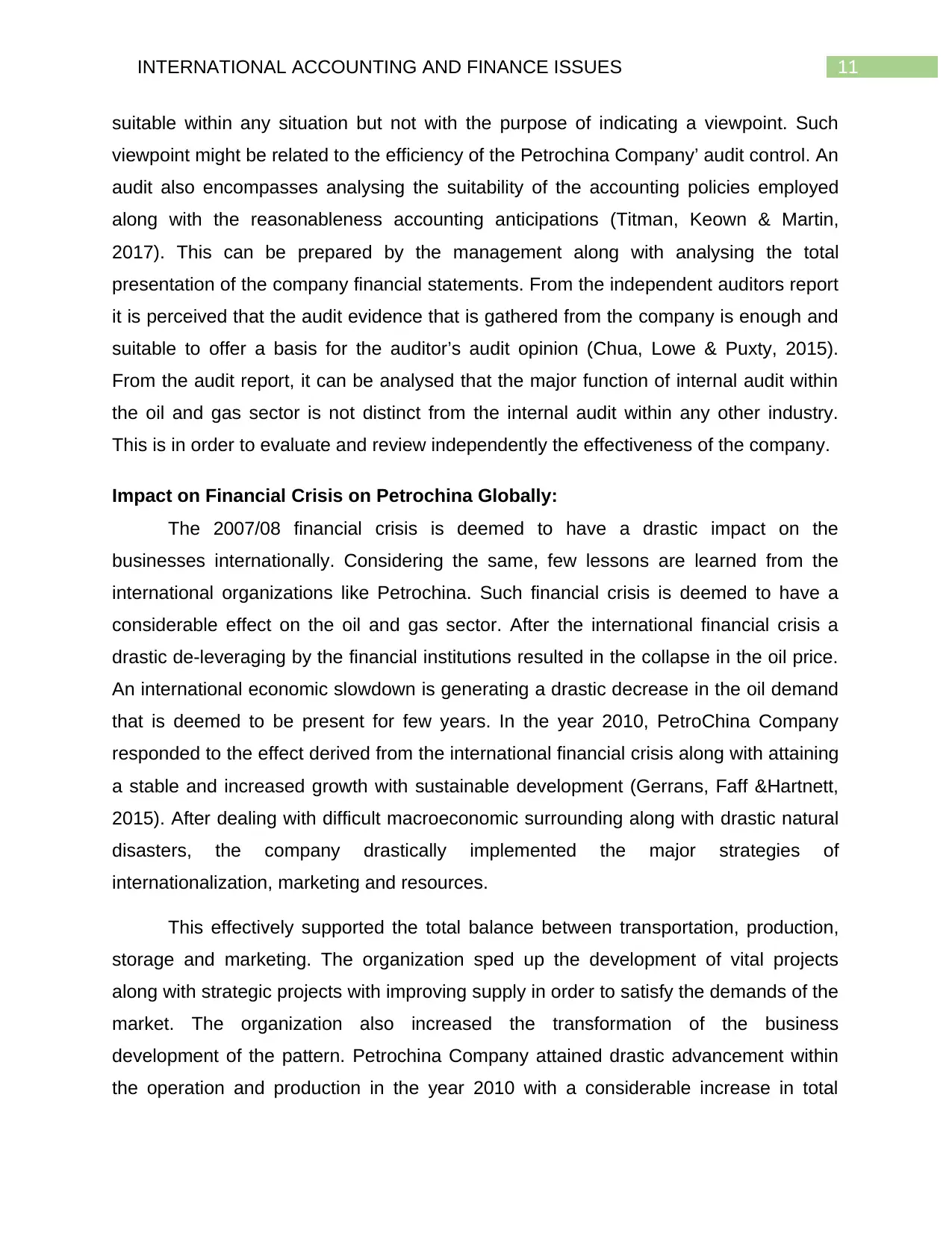

Table 2: Liquidity ratios of Petrochina for the years 2015 and 2016

(Source: Petrochina.com.cn, 2018)

dropped to 1.82% in 2016 from 2.46% in 2015. The possible reasons identified behind

this downfall include the fall in market demand, increase in non-operating expense and

decline in non-operating income as well (Contessotto & Moroney, 2014). Hence, from

the profitability point of view, Petrochina is not in a healthy position in the oil and gas

sector of the nation.

Liquidity and working capital analysis:

The liquidity analysis of Petrochina has been carried out with the help of the

following ratios, which are presented in the form of a table as follows:

Liquidity Ratios:-

Particulars Details 2015 2016

Current assets A 3,49,344 3,81,665

Inventories B 1,26,877 1,46,865

Current liabilities C 4,71,407 4,99,263

Current ratio A/C 0.74 0.76

Quick ratio B/C 0.47 0.47

Working capital A-C -1,22,063 -1,17,598

Table 2: Liquidity ratios of Petrochina for the years 2015 and 2016

(Source: Petrochina.com.cn, 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6INTERNATIONAL ACCOUNTING AND FINANCE ISSUES

2015 2016

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

0.74 0.76

0.47 0.47

Liquidity Ratios

Current ratio

Quick ratio

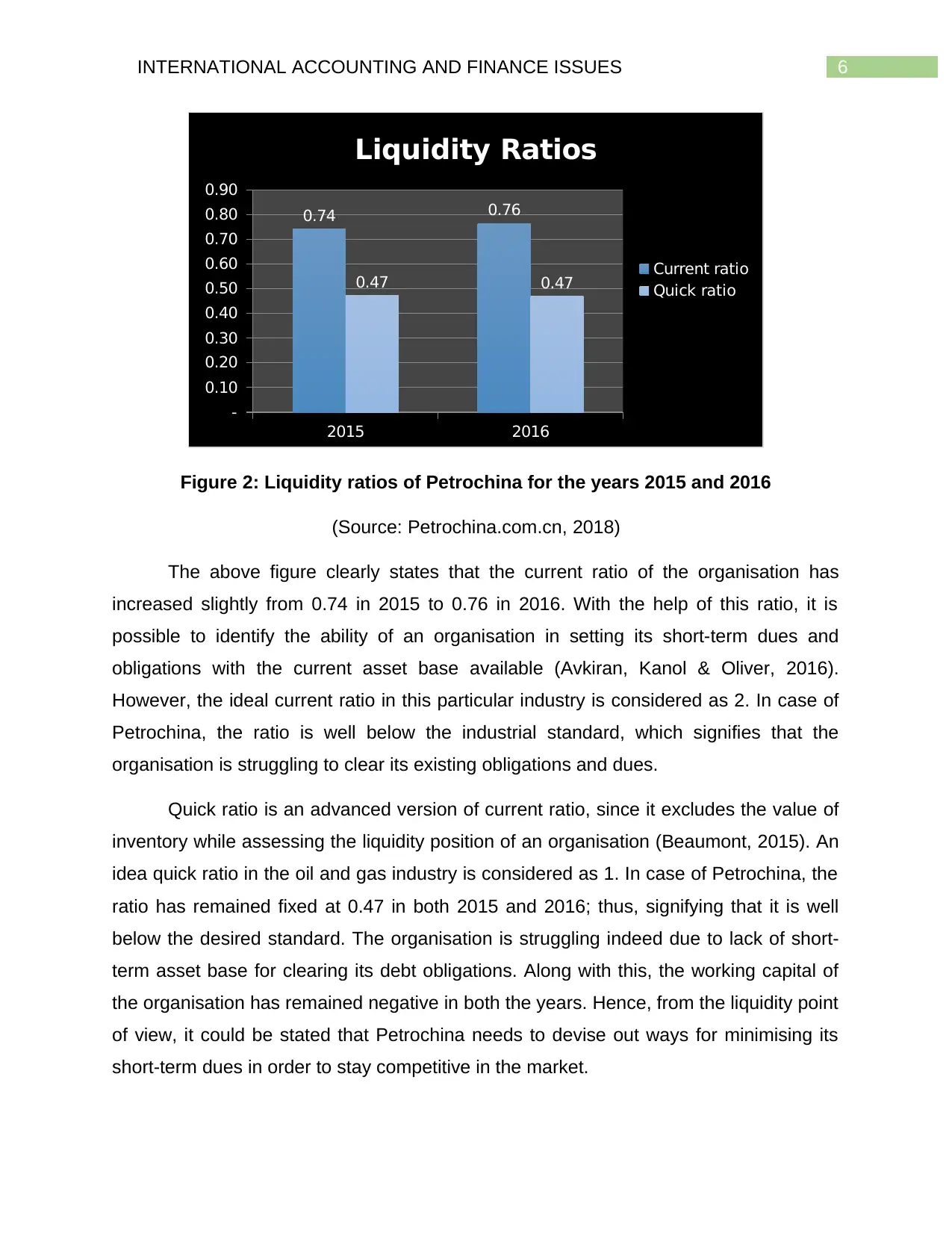

Figure 2: Liquidity ratios of Petrochina for the years 2015 and 2016

(Source: Petrochina.com.cn, 2018)

The above figure clearly states that the current ratio of the organisation has

increased slightly from 0.74 in 2015 to 0.76 in 2016. With the help of this ratio, it is

possible to identify the ability of an organisation in setting its short-term dues and

obligations with the current asset base available (Avkiran, Kanol & Oliver, 2016).

However, the ideal current ratio in this particular industry is considered as 2. In case of

Petrochina, the ratio is well below the industrial standard, which signifies that the

organisation is struggling to clear its existing obligations and dues.

Quick ratio is an advanced version of current ratio, since it excludes the value of

inventory while assessing the liquidity position of an organisation (Beaumont, 2015). An

idea quick ratio in the oil and gas industry is considered as 1. In case of Petrochina, the

ratio has remained fixed at 0.47 in both 2015 and 2016; thus, signifying that it is well

below the desired standard. The organisation is struggling indeed due to lack of short-

term asset base for clearing its debt obligations. Along with this, the working capital of

the organisation has remained negative in both the years. Hence, from the liquidity point

of view, it could be stated that Petrochina needs to devise out ways for minimising its

short-term dues in order to stay competitive in the market.

2015 2016

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

0.74 0.76

0.47 0.47

Liquidity Ratios

Current ratio

Quick ratio

Figure 2: Liquidity ratios of Petrochina for the years 2015 and 2016

(Source: Petrochina.com.cn, 2018)

The above figure clearly states that the current ratio of the organisation has

increased slightly from 0.74 in 2015 to 0.76 in 2016. With the help of this ratio, it is

possible to identify the ability of an organisation in setting its short-term dues and

obligations with the current asset base available (Avkiran, Kanol & Oliver, 2016).

However, the ideal current ratio in this particular industry is considered as 2. In case of

Petrochina, the ratio is well below the industrial standard, which signifies that the

organisation is struggling to clear its existing obligations and dues.

Quick ratio is an advanced version of current ratio, since it excludes the value of

inventory while assessing the liquidity position of an organisation (Beaumont, 2015). An

idea quick ratio in the oil and gas industry is considered as 1. In case of Petrochina, the

ratio has remained fixed at 0.47 in both 2015 and 2016; thus, signifying that it is well

below the desired standard. The organisation is struggling indeed due to lack of short-

term asset base for clearing its debt obligations. Along with this, the working capital of

the organisation has remained negative in both the years. Hence, from the liquidity point

of view, it could be stated that Petrochina needs to devise out ways for minimising its

short-term dues in order to stay competitive in the market.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTERNATIONAL ACCOUNTING AND FINANCE ISSUES

Long-term solvency analysis:

The long-term solvency analysis of Petrochina has been carried out with the help

of the following ratios, which are presented in the form of a table as follows:

Long-Term Solvency Ratios:-

Particulars Details 2015 2016

Non-current liabilities A

5,78,39

9

5,24,65

9

Total shareholders'

equity B

13,44,28

8

13,73,02

8

Operating profit C

56,43

0

48,87

4

Interest expense D

23,82

6

20,65

2

Gearing ratio

A/

(A+B)

0.3

0

0.2

8

Interest cover ratio C/D

2.3

7

2.3

7

Table 3: Long-term solvency ratios of Petrochina for the years 2015 and 2016

(Source: Petrochina.com.cn, 2018)

Long-term solvency analysis:

The long-term solvency analysis of Petrochina has been carried out with the help

of the following ratios, which are presented in the form of a table as follows:

Long-Term Solvency Ratios:-

Particulars Details 2015 2016

Non-current liabilities A

5,78,39

9

5,24,65

9

Total shareholders'

equity B

13,44,28

8

13,73,02

8

Operating profit C

56,43

0

48,87

4

Interest expense D

23,82

6

20,65

2

Gearing ratio

A/

(A+B)

0.3

0

0.2

8

Interest cover ratio C/D

2.3

7

2.3

7

Table 3: Long-term solvency ratios of Petrochina for the years 2015 and 2016

(Source: Petrochina.com.cn, 2018)

8INTERNATIONAL ACCOUNTING AND FINANCE ISSUES

2015 2016

-

0.50

1.00

1.50

2.00

2.50

0.30 0.28

2.37 2.37

Long-Term Solvency Ratios

Gearing ratio

Interest cover ratio

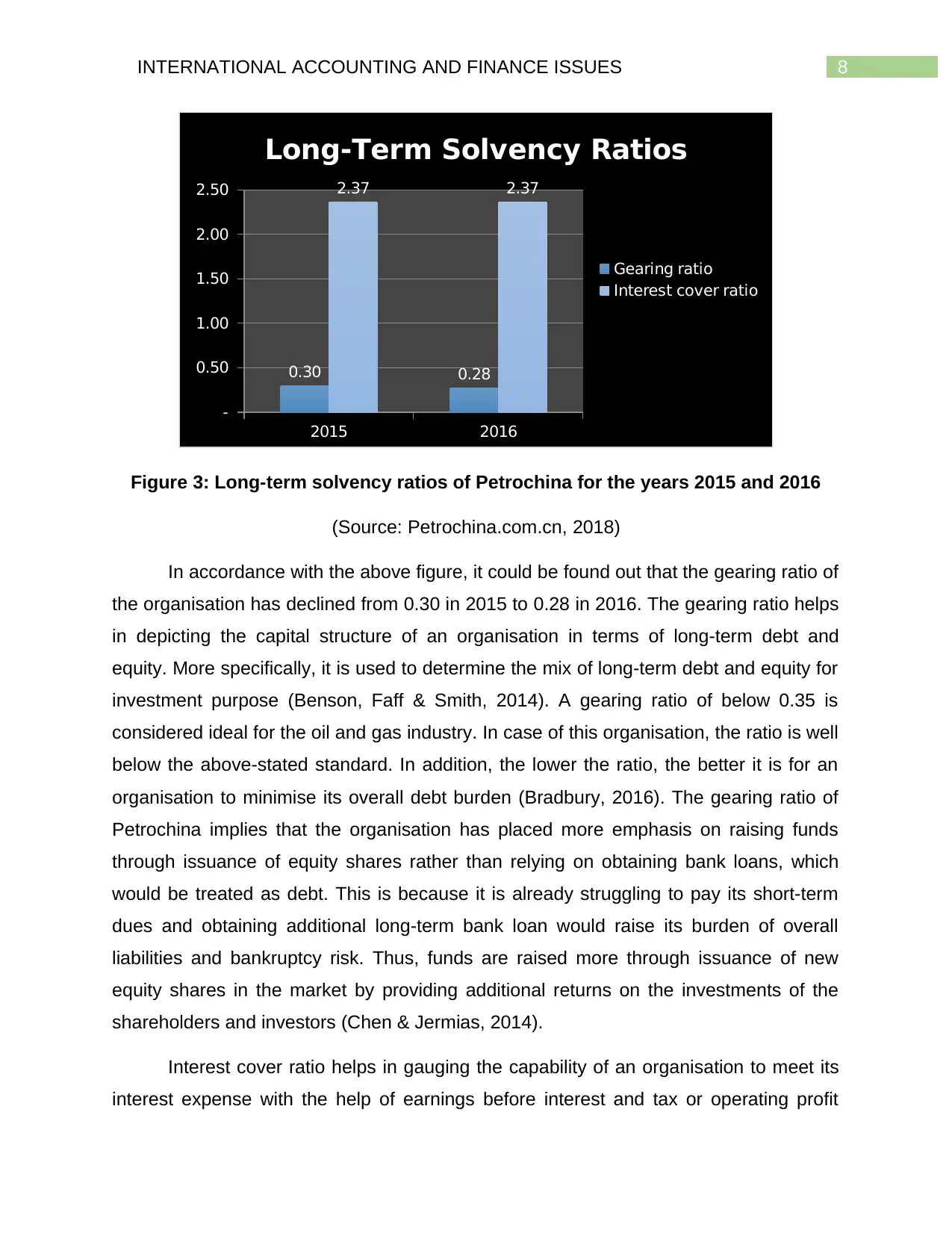

Figure 3: Long-term solvency ratios of Petrochina for the years 2015 and 2016

(Source: Petrochina.com.cn, 2018)

In accordance with the above figure, it could be found out that the gearing ratio of

the organisation has declined from 0.30 in 2015 to 0.28 in 2016. The gearing ratio helps

in depicting the capital structure of an organisation in terms of long-term debt and

equity. More specifically, it is used to determine the mix of long-term debt and equity for

investment purpose (Benson, Faff & Smith, 2014). A gearing ratio of below 0.35 is

considered ideal for the oil and gas industry. In case of this organisation, the ratio is well

below the above-stated standard. In addition, the lower the ratio, the better it is for an

organisation to minimise its overall debt burden (Bradbury, 2016). The gearing ratio of

Petrochina implies that the organisation has placed more emphasis on raising funds

through issuance of equity shares rather than relying on obtaining bank loans, which

would be treated as debt. This is because it is already struggling to pay its short-term

dues and obtaining additional long-term bank loan would raise its burden of overall

liabilities and bankruptcy risk. Thus, funds are raised more through issuance of new

equity shares in the market by providing additional returns on the investments of the

shareholders and investors (Chen & Jermias, 2014).

Interest cover ratio helps in gauging the capability of an organisation to meet its

interest expense with the help of earnings before interest and tax or operating profit

2015 2016

-

0.50

1.00

1.50

2.00

2.50

0.30 0.28

2.37 2.37

Long-Term Solvency Ratios

Gearing ratio

Interest cover ratio

Figure 3: Long-term solvency ratios of Petrochina for the years 2015 and 2016

(Source: Petrochina.com.cn, 2018)

In accordance with the above figure, it could be found out that the gearing ratio of

the organisation has declined from 0.30 in 2015 to 0.28 in 2016. The gearing ratio helps

in depicting the capital structure of an organisation in terms of long-term debt and

equity. More specifically, it is used to determine the mix of long-term debt and equity for

investment purpose (Benson, Faff & Smith, 2014). A gearing ratio of below 0.35 is

considered ideal for the oil and gas industry. In case of this organisation, the ratio is well

below the above-stated standard. In addition, the lower the ratio, the better it is for an

organisation to minimise its overall debt burden (Bradbury, 2016). The gearing ratio of

Petrochina implies that the organisation has placed more emphasis on raising funds

through issuance of equity shares rather than relying on obtaining bank loans, which

would be treated as debt. This is because it is already struggling to pay its short-term

dues and obtaining additional long-term bank loan would raise its burden of overall

liabilities and bankruptcy risk. Thus, funds are raised more through issuance of new

equity shares in the market by providing additional returns on the investments of the

shareholders and investors (Chen & Jermias, 2014).

Interest cover ratio helps in gauging the capability of an organisation to meet its

interest expense with the help of earnings before interest and tax or operating profit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9INTERNATIONAL ACCOUNTING AND FINANCE ISSUES

(Chua, Lowe & Puxty, 2015). A ratio above 2 is considered as ideal for this particular

industry. In case of Petrochina, the ratio has remained constant at 2.37 in both 2015

and 2016. This denotes that despite the fall in overall revenues, it has managed to

minimise various expenses; thus, enabling the organisation to maintain the same rate.

Moreover, the ratio is above the stated ideal standard implying the overall efficacy of the

organisation to strike an appropriate balance between revenue and expenditure. Hence,

from the solvency point of view, Petrochina is enjoying stable position in the oil and gas

sector of the nation.

Independent Audit and Assurance:

Independent audit that is also referred as external audit oaf the organisations is a

vital part of assurance and confidence. With every new fraud as well as audit failure

present in the financial statements of any company, several direct questions are asked

regarding the independent audit value. It can be said that, it is vital for the auditors to

remain positioned to offer assurance on financial reporting based on the global

standards. This is related to auditing, accounting and independence (Vogel, 2014).

Additionally, the importance of independent audit will continue to enhance the impact as

an aspect of properly operating international capital markets that impacts investors all

through the world. This concept can be explained in a better manner through taking the

example of Petrochina Company. Price Water House Coopers is observed to provide an

independent audit report on the company for all its shareholders to consider it. This

audit report is established within the People’s Republic of China with decreased liability.

This independent audit report of the company has audited the company’s financial

statements that include consolidated balance sheets, cash flow statements, profit and

loss amount along with changes in equity statement (Floyd & List, 2016).

The independent audit report also checked assurance regarding directors’

responsibility in consideration to the financial statements, auditors’ responsibility,

auditor’s opinion along with other matters. The audit report explained assured that the

directors of Petrochina Company are accountable for the development along with true

and fair presentation of the consolidated financial statements (Vogel, 2016). It is also

assured that this is conducted in accordance with the Financial Reporting Standards

(Chua, Lowe & Puxty, 2015). A ratio above 2 is considered as ideal for this particular

industry. In case of Petrochina, the ratio has remained constant at 2.37 in both 2015

and 2016. This denotes that despite the fall in overall revenues, it has managed to

minimise various expenses; thus, enabling the organisation to maintain the same rate.

Moreover, the ratio is above the stated ideal standard implying the overall efficacy of the

organisation to strike an appropriate balance between revenue and expenditure. Hence,

from the solvency point of view, Petrochina is enjoying stable position in the oil and gas

sector of the nation.

Independent Audit and Assurance:

Independent audit that is also referred as external audit oaf the organisations is a

vital part of assurance and confidence. With every new fraud as well as audit failure

present in the financial statements of any company, several direct questions are asked

regarding the independent audit value. It can be said that, it is vital for the auditors to

remain positioned to offer assurance on financial reporting based on the global

standards. This is related to auditing, accounting and independence (Vogel, 2014).

Additionally, the importance of independent audit will continue to enhance the impact as

an aspect of properly operating international capital markets that impacts investors all

through the world. This concept can be explained in a better manner through taking the

example of Petrochina Company. Price Water House Coopers is observed to provide an

independent audit report on the company for all its shareholders to consider it. This

audit report is established within the People’s Republic of China with decreased liability.

This independent audit report of the company has audited the company’s financial

statements that include consolidated balance sheets, cash flow statements, profit and

loss amount along with changes in equity statement (Floyd & List, 2016).

The independent audit report also checked assurance regarding directors’

responsibility in consideration to the financial statements, auditors’ responsibility,

auditor’s opinion along with other matters. The audit report explained assured that the

directors of Petrochina Company are accountable for the development along with true

and fair presentation of the consolidated financial statements (Vogel, 2016). It is also

assured that this is conducted in accordance with the Financial Reporting Standards

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10INTERNATIONAL ACCOUNTING AND FINANCE ISSUES

along with the requirements of disclosure regarding Hong Kong Companies ordinance.

As per this report, directors responsibility encompass designing, implementing along

with sustaining internal control important for the generation along with true and fair

financial statements presentation.

Moreover, the audit report confined that this will also be free from material

misstatement whether because of error or fraud along with choosing and implementing

suitable accounting policies. This will also consider making accounting anticipations that

is reasonable in such instances. As per the opinion of the independent auditor, the

consolidated financial statements of the company offer a true and fair view regarding

the Petrochina’s financial position and group performance (Zhang et al., 2016). The

report also ensured that the company’s annual cash flows are prepared in consideration

to International Financial Reporting Standards. Moreover, this has been developed

efficiently, as per the disclosure needs of the Hong Kong Companies ordinance (Gaunt,

2014).

From analysing the independent audit report of Petrochina Company it is

observed that the auditors’ responsibility is to provide an opinion on the consolidated

financial statements relied on their audit. The report ensured that the auditors carried

out their audit in consideration to International Auditing Standards. These standards

need that the company will require being in accordance with the ethical standards along

with the plan. The auditors also carried out the audit in order attain important assurance

regarding the fact whether the financial statements are devoid of any material

misstatement (Floyd &List, 2016). The report also elucidates that an audit focuses on

carrying out procedures in order to attain audit evidences regarding the amounts along

with disclosures within the financial statements. The processes those are chosen rely

on the judgement of the auditors that encompasses the evaluation of risks. This can

include material misstatements present n the company’s financial statement that takes

place because of fraud or error.

In carrying out such risk evaluations, the auditors include internal control

associated with the organization’s generation along with true and fair financial

statements presentation. This is in order to develop certain audit processes which are

along with the requirements of disclosure regarding Hong Kong Companies ordinance.

As per this report, directors responsibility encompass designing, implementing along

with sustaining internal control important for the generation along with true and fair

financial statements presentation.

Moreover, the audit report confined that this will also be free from material

misstatement whether because of error or fraud along with choosing and implementing

suitable accounting policies. This will also consider making accounting anticipations that

is reasonable in such instances. As per the opinion of the independent auditor, the

consolidated financial statements of the company offer a true and fair view regarding

the Petrochina’s financial position and group performance (Zhang et al., 2016). The

report also ensured that the company’s annual cash flows are prepared in consideration

to International Financial Reporting Standards. Moreover, this has been developed

efficiently, as per the disclosure needs of the Hong Kong Companies ordinance (Gaunt,

2014).

From analysing the independent audit report of Petrochina Company it is

observed that the auditors’ responsibility is to provide an opinion on the consolidated

financial statements relied on their audit. The report ensured that the auditors carried

out their audit in consideration to International Auditing Standards. These standards

need that the company will require being in accordance with the ethical standards along

with the plan. The auditors also carried out the audit in order attain important assurance

regarding the fact whether the financial statements are devoid of any material

misstatement (Floyd &List, 2016). The report also elucidates that an audit focuses on

carrying out procedures in order to attain audit evidences regarding the amounts along

with disclosures within the financial statements. The processes those are chosen rely

on the judgement of the auditors that encompasses the evaluation of risks. This can

include material misstatements present n the company’s financial statement that takes

place because of fraud or error.

In carrying out such risk evaluations, the auditors include internal control

associated with the organization’s generation along with true and fair financial

statements presentation. This is in order to develop certain audit processes which are

11INTERNATIONAL ACCOUNTING AND FINANCE ISSUES

suitable within any situation but not with the purpose of indicating a viewpoint. Such

viewpoint might be related to the efficiency of the Petrochina Company’ audit control. An

audit also encompasses analysing the suitability of the accounting policies employed

along with the reasonableness accounting anticipations (Titman, Keown & Martin,

2017). This can be prepared by the management along with analysing the total

presentation of the company financial statements. From the independent auditors report

it is perceived that the audit evidence that is gathered from the company is enough and

suitable to offer a basis for the auditor’s audit opinion (Chua, Lowe & Puxty, 2015).

From the audit report, it can be analysed that the major function of internal audit within

the oil and gas sector is not distinct from the internal audit within any other industry.

This is in order to evaluate and review independently the effectiveness of the company.

Impact on Financial Crisis on Petrochina Globally:

The 2007/08 financial crisis is deemed to have a drastic impact on the

businesses internationally. Considering the same, few lessons are learned from the

international organizations like Petrochina. Such financial crisis is deemed to have a

considerable effect on the oil and gas sector. After the international financial crisis a

drastic de-leveraging by the financial institutions resulted in the collapse in the oil price.

An international economic slowdown is generating a drastic decrease in the oil demand

that is deemed to be present for few years. In the year 2010, PetroChina Company

responded to the effect derived from the international financial crisis along with attaining

a stable and increased growth with sustainable development (Gerrans, Faff &Hartnett,

2015). After dealing with difficult macroeconomic surrounding along with drastic natural

disasters, the company drastically implemented the major strategies of

internationalization, marketing and resources.

This effectively supported the total balance between transportation, production,

storage and marketing. The organization sped up the development of vital projects

along with strategic projects with improving supply in order to satisfy the demands of the

market. The organization also increased the transformation of the business

development of the pattern. Petrochina Company attained drastic advancement within

the operation and production in the year 2010 with a considerable increase in total

suitable within any situation but not with the purpose of indicating a viewpoint. Such

viewpoint might be related to the efficiency of the Petrochina Company’ audit control. An

audit also encompasses analysing the suitability of the accounting policies employed

along with the reasonableness accounting anticipations (Titman, Keown & Martin,

2017). This can be prepared by the management along with analysing the total

presentation of the company financial statements. From the independent auditors report

it is perceived that the audit evidence that is gathered from the company is enough and

suitable to offer a basis for the auditor’s audit opinion (Chua, Lowe & Puxty, 2015).

From the audit report, it can be analysed that the major function of internal audit within

the oil and gas sector is not distinct from the internal audit within any other industry.

This is in order to evaluate and review independently the effectiveness of the company.

Impact on Financial Crisis on Petrochina Globally:

The 2007/08 financial crisis is deemed to have a drastic impact on the

businesses internationally. Considering the same, few lessons are learned from the

international organizations like Petrochina. Such financial crisis is deemed to have a

considerable effect on the oil and gas sector. After the international financial crisis a

drastic de-leveraging by the financial institutions resulted in the collapse in the oil price.

An international economic slowdown is generating a drastic decrease in the oil demand

that is deemed to be present for few years. In the year 2010, PetroChina Company

responded to the effect derived from the international financial crisis along with attaining

a stable and increased growth with sustainable development (Gerrans, Faff &Hartnett,

2015). After dealing with difficult macroeconomic surrounding along with drastic natural

disasters, the company drastically implemented the major strategies of

internationalization, marketing and resources.

This effectively supported the total balance between transportation, production,

storage and marketing. The organization sped up the development of vital projects

along with strategic projects with improving supply in order to satisfy the demands of the

market. The organization also increased the transformation of the business

development of the pattern. Petrochina Company attained drastic advancement within

the operation and production in the year 2010 with a considerable increase in total

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.