Individual Assignment Report: PetroChina for Non-Financial Directors

VerifiedAdded on 2021/02/22

|19

|4532

|68

Report

AI Summary

This individual assignment report analyzes the financial performance of PetroChina, a state-owned energy giant, focusing on key financial ratios such as liquidity, solvency, profitability, and performance. The report compares PetroChina's performance with its peer, SINOPEC, and examines trends from 2015 to 2016. It delves into the company's challenges, including declining profits and stock performance, and explores the impact of the 2007/2008 financial crisis. The report also discusses the role of independent audits, audit expectations, and the assurance they provide. Furthermore, it provides insights into the global effects of the financial crisis and lessons learned by PetroChina. The report is structured into three parts: ratio analysis, independent audit, and the financial crisis, offering a comprehensive view of PetroChina's financial health and strategic considerations.

Individual Assignment Report to the

Non-Financial Directors of PetroChina

Name:

P Number:

Module Code: ACFI3424

Word Count: 2997

Non-Financial Directors of PetroChina

Name:

P Number:

Module Code: ACFI3424

Word Count: 2997

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Part A..................................................................................................3

Ratio Analysis.................................................................................3

1.1 Liquidity....................................................................................4

1.2 Working Capital.........................................................................4

1.3 Solvency...................................................................................5

1.4 Profitability................................................................................6

1.5 Performance.............................................................................7

Part B..................................................................................................8

2.1 The definition of Independent Audit...............................................8

2.2 The assurance of independent audit.............................................9

2.3 The confidence of independent audit............................................9

2.4 Audit expectations gap..............................................................10

Part C................................................................................................12

3.1 The global effect of 2007/2008 financial crisis..............................12

3.2 Lesson learned from the financial crisis by PetroChina..................13

Reference..........................................................................................14

Part A

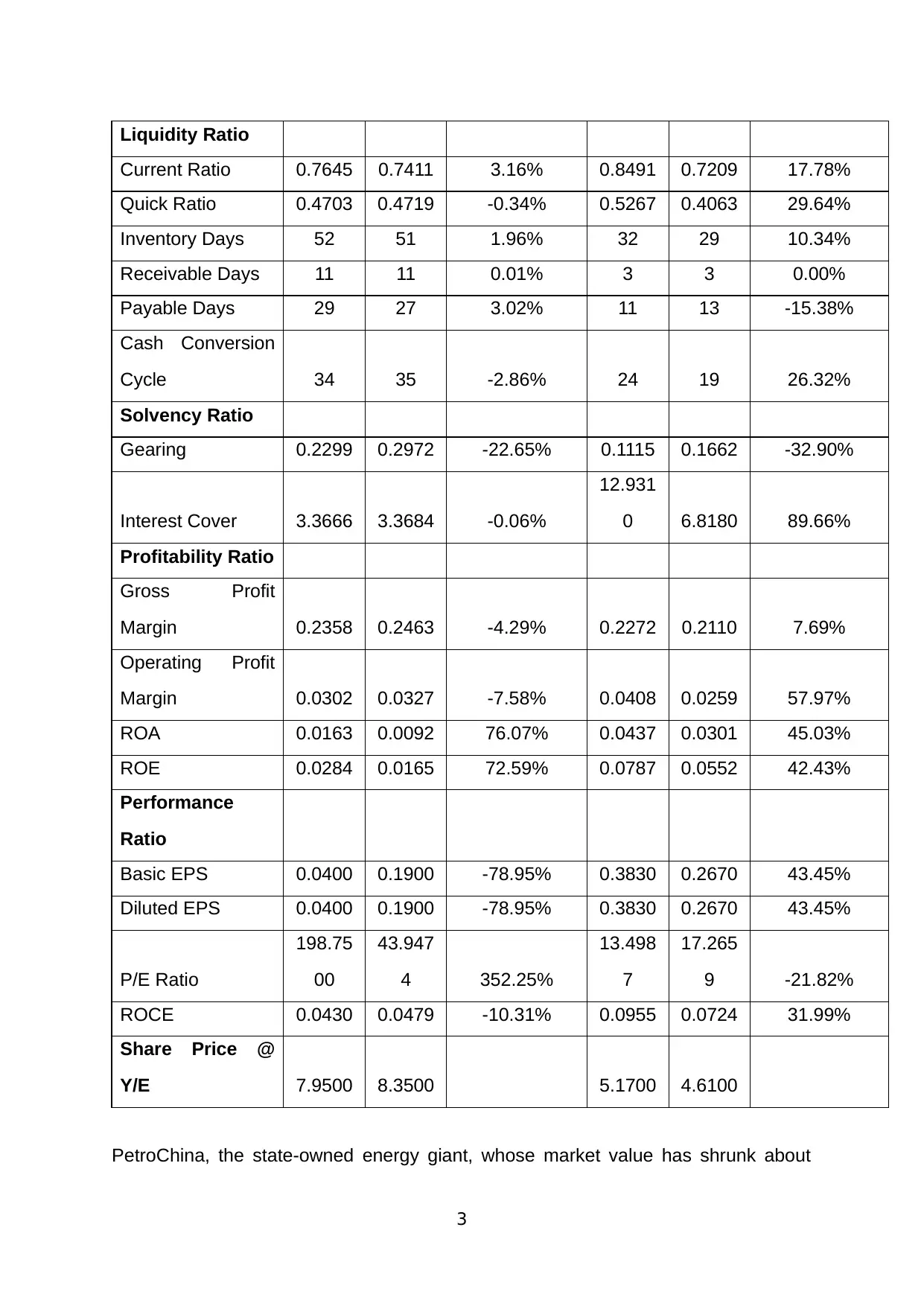

Ratio Analysis

PetroChina SINOPEC

2016 2015 Change Rate 2016 2015 Change Rate

2

Part A..................................................................................................3

Ratio Analysis.................................................................................3

1.1 Liquidity....................................................................................4

1.2 Working Capital.........................................................................4

1.3 Solvency...................................................................................5

1.4 Profitability................................................................................6

1.5 Performance.............................................................................7

Part B..................................................................................................8

2.1 The definition of Independent Audit...............................................8

2.2 The assurance of independent audit.............................................9

2.3 The confidence of independent audit............................................9

2.4 Audit expectations gap..............................................................10

Part C................................................................................................12

3.1 The global effect of 2007/2008 financial crisis..............................12

3.2 Lesson learned from the financial crisis by PetroChina..................13

Reference..........................................................................................14

Part A

Ratio Analysis

PetroChina SINOPEC

2016 2015 Change Rate 2016 2015 Change Rate

2

Liquidity Ratio

Current Ratio 0.7645 0.7411 3.16% 0.8491 0.7209 17.78%

Quick Ratio 0.4703 0.4719 -0.34% 0.5267 0.4063 29.64%

Inventory Days 52 51 1.96% 32 29 10.34%

Receivable Days 11 11 0.01% 3 3 0.00%

Payable Days 29 27 3.02% 11 13 -15.38%

Cash Conversion

Cycle 34 35 -2.86% 24 19 26.32%

Solvency Ratio

Gearing 0.2299 0.2972 -22.65% 0.1115 0.1662 -32.90%

Interest Cover 3.3666 3.3684 -0.06%

12.931

0 6.8180 89.66%

Profitability Ratio

Gross Profit

Margin 0.2358 0.2463 -4.29% 0.2272 0.2110 7.69%

Operating Profit

Margin 0.0302 0.0327 -7.58% 0.0408 0.0259 57.97%

ROA 0.0163 0.0092 76.07% 0.0437 0.0301 45.03%

ROE 0.0284 0.0165 72.59% 0.0787 0.0552 42.43%

Performance

Ratio

Basic EPS 0.0400 0.1900 -78.95% 0.3830 0.2670 43.45%

Diluted EPS 0.0400 0.1900 -78.95% 0.3830 0.2670 43.45%

P/E Ratio

198.75

00

43.947

4 352.25%

13.498

7

17.265

9 -21.82%

ROCE 0.0430 0.0479 -10.31% 0.0955 0.0724 31.99%

Share Price @

Y/E 7.9500 8.3500 5.1700 4.6100

PetroChina, the state-owned energy giant, whose market value has shrunk about

3

Current Ratio 0.7645 0.7411 3.16% 0.8491 0.7209 17.78%

Quick Ratio 0.4703 0.4719 -0.34% 0.5267 0.4063 29.64%

Inventory Days 52 51 1.96% 32 29 10.34%

Receivable Days 11 11 0.01% 3 3 0.00%

Payable Days 29 27 3.02% 11 13 -15.38%

Cash Conversion

Cycle 34 35 -2.86% 24 19 26.32%

Solvency Ratio

Gearing 0.2299 0.2972 -22.65% 0.1115 0.1662 -32.90%

Interest Cover 3.3666 3.3684 -0.06%

12.931

0 6.8180 89.66%

Profitability Ratio

Gross Profit

Margin 0.2358 0.2463 -4.29% 0.2272 0.2110 7.69%

Operating Profit

Margin 0.0302 0.0327 -7.58% 0.0408 0.0259 57.97%

ROA 0.0163 0.0092 76.07% 0.0437 0.0301 45.03%

ROE 0.0284 0.0165 72.59% 0.0787 0.0552 42.43%

Performance

Ratio

Basic EPS 0.0400 0.1900 -78.95% 0.3830 0.2670 43.45%

Diluted EPS 0.0400 0.1900 -78.95% 0.3830 0.2670 43.45%

P/E Ratio

198.75

00

43.947

4 352.25%

13.498

7

17.265

9 -21.82%

ROCE 0.0430 0.0479 -10.31% 0.0955 0.0724 31.99%

Share Price @

Y/E 7.9500 8.3500 5.1700 4.6100

PetroChina, the state-owned energy giant, whose market value has shrunk about

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

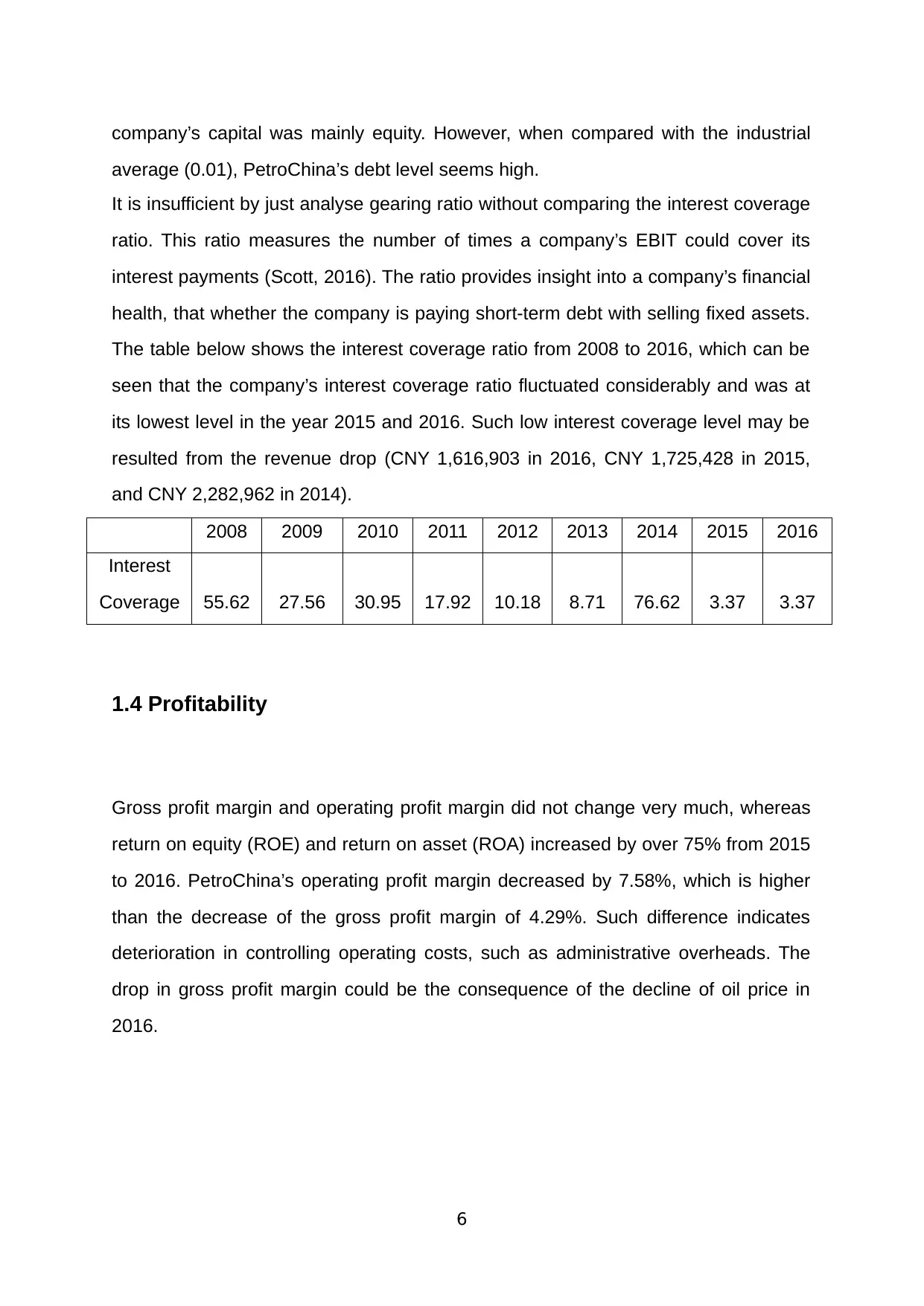

$800 billion (around £573 billion), experienced its biggest stock collapse 10 years

after listing. Its profits declined by over 30 percent to RMB 29 billion. Among its

peers in the world, PetroChina has plunged the most in terms of stock returns since

its first peak in 2007. The economic in China when PetroChina listed in Shanghai

Stock Exchange, there were bubbles in both oil industry and Chinese stock market.

The company was clearly overvalued by the market and hence, bubbles were

deemed to burst, not even mention the global financial crisis was just around the

corner.

1.1 Liquidity

Liquidity ratios provide insight on the ability that a company can meet its short-term

obligations. Liquidity on its own meaning how quick a company can convert assets

into cash and pay out its current liabilities. Liquidity ratios vary from one industry to

another. PetroChina, the largest energy company in China, did a good job in keeping

its liquidity ratios stable comparing to its peer SINOPEC.

PetroChina had less than one in both current and quick ratios lower than its major

competitor SINOPEC. The industrial average of current ratio and quick ratio are 0.87

and 0.79 respectively (Moneycontrol.com, 2018). PetroChina’s current ratio in 2016

was slightly lower than the average, which indicates that the company did well in

maintaining liquidity level. However, PetroChina’s quick ratio was 0.47 that was 0.3

lower than the industrial average. The quick ratio removed the possible effect of

inventory, which may not be easy to sell at its carrying value quickly. Given that

inventories in the energy industry have high liquidity and constant demand,

PetroChina’s quick ratio was unsatisfying.

PetroChina also had longer cash conversion cycle (CCC) (34 days in 2016) than the

industrial average of 20 days (Moneycontrol.com, 2018). Long inventory turnover

period was the main cause of such long CCC of PetroChina. It gives the same

4

after listing. Its profits declined by over 30 percent to RMB 29 billion. Among its

peers in the world, PetroChina has plunged the most in terms of stock returns since

its first peak in 2007. The economic in China when PetroChina listed in Shanghai

Stock Exchange, there were bubbles in both oil industry and Chinese stock market.

The company was clearly overvalued by the market and hence, bubbles were

deemed to burst, not even mention the global financial crisis was just around the

corner.

1.1 Liquidity

Liquidity ratios provide insight on the ability that a company can meet its short-term

obligations. Liquidity on its own meaning how quick a company can convert assets

into cash and pay out its current liabilities. Liquidity ratios vary from one industry to

another. PetroChina, the largest energy company in China, did a good job in keeping

its liquidity ratios stable comparing to its peer SINOPEC.

PetroChina had less than one in both current and quick ratios lower than its major

competitor SINOPEC. The industrial average of current ratio and quick ratio are 0.87

and 0.79 respectively (Moneycontrol.com, 2018). PetroChina’s current ratio in 2016

was slightly lower than the average, which indicates that the company did well in

maintaining liquidity level. However, PetroChina’s quick ratio was 0.47 that was 0.3

lower than the industrial average. The quick ratio removed the possible effect of

inventory, which may not be easy to sell at its carrying value quickly. Given that

inventories in the energy industry have high liquidity and constant demand,

PetroChina’s quick ratio was unsatisfying.

PetroChina also had longer cash conversion cycle (CCC) (34 days in 2016) than the

industrial average of 20 days (Moneycontrol.com, 2018). Long inventory turnover

period was the main cause of such long CCC of PetroChina. It gives the same

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

picture as quick ratio, that PetroChina had difficulties in converting inventory into

cash. Both receivable days and payable days were longer than other companies in

this industry. One possible reason is that PetroChina as the largest energy company

in China has great bargaining power and reputation. Hence, the company can gain

better terms on trade receivables and payables.

1.2 Working Capital

PetroChina also had longer cash conversion cycle (CCC) (34 days in 2016) than the

industrial average of 20 days (Moneycontrol.com, 2018). Long inventory turnover

period was the main cause of such long CCC of PetroChina. It gives the same

picture as quick ratio, that PetroChina had difficulties in converting inventory into

cash. Both receivable days and payable days were longer than other companies in

this industry. One possible reason is that PetroChina as the largest energy company

in China has great bargaining power and reputation. Hence, the company can gain

better terms on trade receivables and payables.

1.3 Solvency

Solvency refers to the ability than one company can pay off its long-term obligations

(Scott, 2016). The major two ratios for determining the solvency of a company are

debt-to-equity ratio and interest cover ratio. Gearing ratio measures the capital

structure of a company and the higher ratio, the weaker solvency. There are

arguments saying that market values can be a better indicator than book value.

However, the market value of PetroChina’s debt was missing, therefore book values

of debt and equity were used for the purpose of consistency. PetroChina had lower

than 1 leverage ratio which did not change materially. Such result shows that the

5

cash. Both receivable days and payable days were longer than other companies in

this industry. One possible reason is that PetroChina as the largest energy company

in China has great bargaining power and reputation. Hence, the company can gain

better terms on trade receivables and payables.

1.2 Working Capital

PetroChina also had longer cash conversion cycle (CCC) (34 days in 2016) than the

industrial average of 20 days (Moneycontrol.com, 2018). Long inventory turnover

period was the main cause of such long CCC of PetroChina. It gives the same

picture as quick ratio, that PetroChina had difficulties in converting inventory into

cash. Both receivable days and payable days were longer than other companies in

this industry. One possible reason is that PetroChina as the largest energy company

in China has great bargaining power and reputation. Hence, the company can gain

better terms on trade receivables and payables.

1.3 Solvency

Solvency refers to the ability than one company can pay off its long-term obligations

(Scott, 2016). The major two ratios for determining the solvency of a company are

debt-to-equity ratio and interest cover ratio. Gearing ratio measures the capital

structure of a company and the higher ratio, the weaker solvency. There are

arguments saying that market values can be a better indicator than book value.

However, the market value of PetroChina’s debt was missing, therefore book values

of debt and equity were used for the purpose of consistency. PetroChina had lower

than 1 leverage ratio which did not change materially. Such result shows that the

5

company’s capital was mainly equity. However, when compared with the industrial

average (0.01), PetroChina’s debt level seems high.

It is insufficient by just analyse gearing ratio without comparing the interest coverage

ratio. This ratio measures the number of times a company’s EBIT could cover its

interest payments (Scott, 2016). The ratio provides insight into a company’s financial

health, that whether the company is paying short-term debt with selling fixed assets.

The table below shows the interest coverage ratio from 2008 to 2016, which can be

seen that the company’s interest coverage ratio fluctuated considerably and was at

its lowest level in the year 2015 and 2016. Such low interest coverage level may be

resulted from the revenue drop (CNY 1,616,903 in 2016, CNY 1,725,428 in 2015,

and CNY 2,282,962 in 2014).

2008 2009 2010 2011 2012 2013 2014 2015 2016

Interest

Coverage 55.62 27.56 30.95 17.92 10.18 8.71 76.62 3.37 3.37

1.4 Profitability

Gross profit margin and operating profit margin did not change very much, whereas

return on equity (ROE) and return on asset (ROA) increased by over 75% from 2015

to 2016. PetroChina’s operating profit margin decreased by 7.58%, which is higher

than the decrease of the gross profit margin of 4.29%. Such difference indicates

deterioration in controlling operating costs, such as administrative overheads. The

drop in gross profit margin could be the consequence of the decline of oil price in

2016.

6

average (0.01), PetroChina’s debt level seems high.

It is insufficient by just analyse gearing ratio without comparing the interest coverage

ratio. This ratio measures the number of times a company’s EBIT could cover its

interest payments (Scott, 2016). The ratio provides insight into a company’s financial

health, that whether the company is paying short-term debt with selling fixed assets.

The table below shows the interest coverage ratio from 2008 to 2016, which can be

seen that the company’s interest coverage ratio fluctuated considerably and was at

its lowest level in the year 2015 and 2016. Such low interest coverage level may be

resulted from the revenue drop (CNY 1,616,903 in 2016, CNY 1,725,428 in 2015,

and CNY 2,282,962 in 2014).

2008 2009 2010 2011 2012 2013 2014 2015 2016

Interest

Coverage 55.62 27.56 30.95 17.92 10.18 8.71 76.62 3.37 3.37

1.4 Profitability

Gross profit margin and operating profit margin did not change very much, whereas

return on equity (ROE) and return on asset (ROA) increased by over 75% from 2015

to 2016. PetroChina’s operating profit margin decreased by 7.58%, which is higher

than the decrease of the gross profit margin of 4.29%. Such difference indicates

deterioration in controlling operating costs, such as administrative overheads. The

drop in gross profit margin could be the consequence of the decline of oil price in

2016.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The ROE ratio measures return earned by a company on its equity capital (Scott,

2016). In the case of PetroChina, ROA and ROE were not very much different

because the major part of assets was financed by equity capital. ROE can help

PetroChina to investigate what drives the income, operating activities or non-

operating activities. There are have two kinds of ways: three-way and five-way:

• ROE = Net profit margin × Total asset turnover × Leverage

• ROE = Tax burden × Interest burden × EBIT margin × Total asset turnover ×

Leverage

By analysing ROE with three-way and five-way DuPont analysis, PetroChina’s

revenue was drriven mainly by operating activities, which supported by assets.

1.5 Performance

EPS of PetroChina decreased severely by nearly 80% in 2016 meaning the

company attributed fewer earnings to each share of common stock. One reason is

that the big drop in earnings Low produce was the primary cause of profit decline.

7

2016). In the case of PetroChina, ROA and ROE were not very much different

because the major part of assets was financed by equity capital. ROE can help

PetroChina to investigate what drives the income, operating activities or non-

operating activities. There are have two kinds of ways: three-way and five-way:

• ROE = Net profit margin × Total asset turnover × Leverage

• ROE = Tax burden × Interest burden × EBIT margin × Total asset turnover ×

Leverage

By analysing ROE with three-way and five-way DuPont analysis, PetroChina’s

revenue was drriven mainly by operating activities, which supported by assets.

1.5 Performance

EPS of PetroChina decreased severely by nearly 80% in 2016 meaning the

company attributed fewer earnings to each share of common stock. One reason is

that the big drop in earnings Low produce was the primary cause of profit decline.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total crude oil output in the first three quarters declined by 3.6%, to 697m barrels of

oil (Megaw, 2016). Like its peers, PetroChina has cut high-cost production in order to

stay profitable. However, such actions met political difficulties due to Beijing prioritise

production targets.

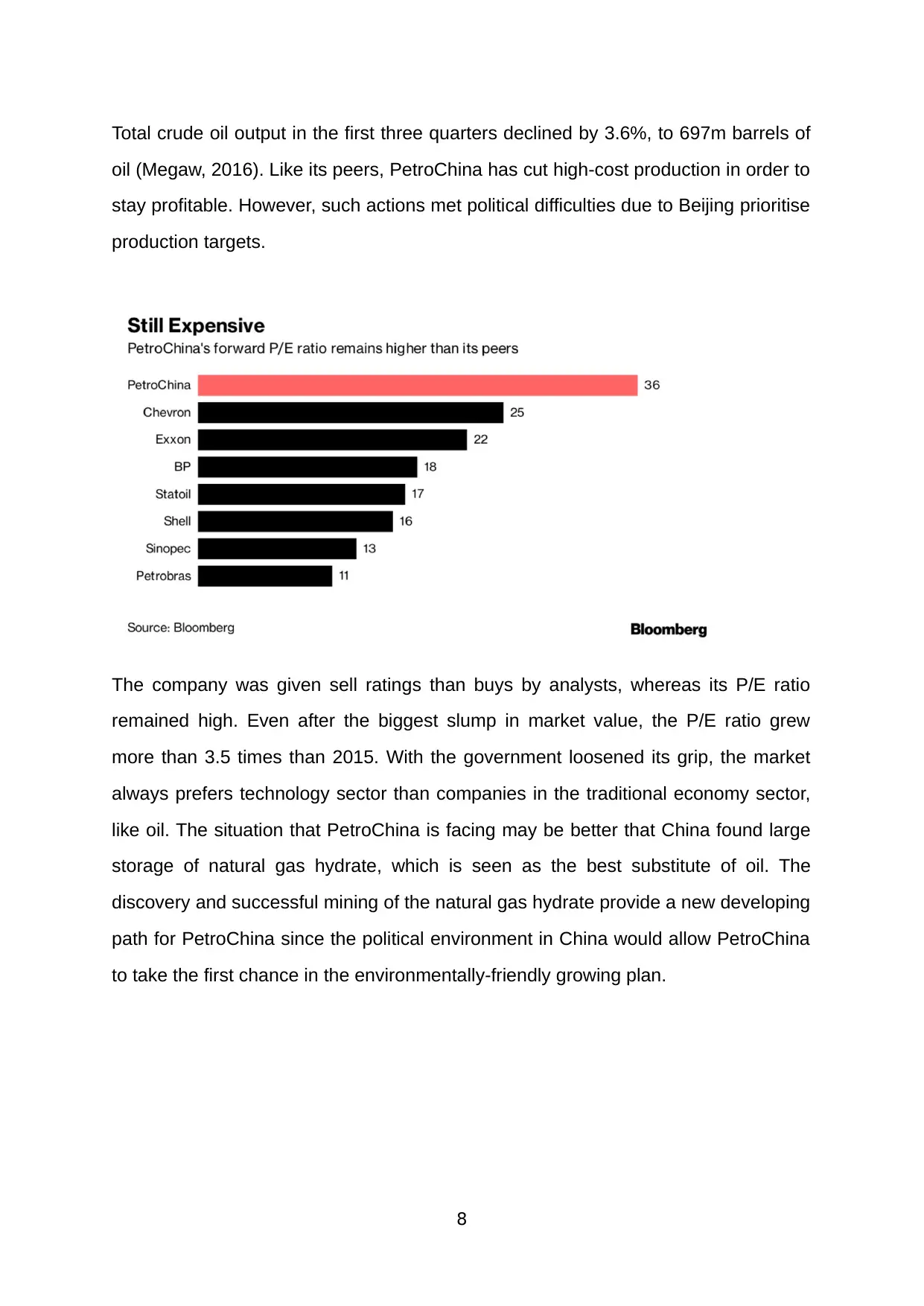

The company was given sell ratings than buys by analysts, whereas its P/E ratio

remained high. Even after the biggest slump in market value, the P/E ratio grew

more than 3.5 times than 2015. With the government loosened its grip, the market

always prefers technology sector than companies in the traditional economy sector,

like oil. The situation that PetroChina is facing may be better that China found large

storage of natural gas hydrate, which is seen as the best substitute of oil. The

discovery and successful mining of the natural gas hydrate provide a new developing

path for PetroChina since the political environment in China would allow PetroChina

to take the first chance in the environmentally-friendly growing plan.

8

oil (Megaw, 2016). Like its peers, PetroChina has cut high-cost production in order to

stay profitable. However, such actions met political difficulties due to Beijing prioritise

production targets.

The company was given sell ratings than buys by analysts, whereas its P/E ratio

remained high. Even after the biggest slump in market value, the P/E ratio grew

more than 3.5 times than 2015. With the government loosened its grip, the market

always prefers technology sector than companies in the traditional economy sector,

like oil. The situation that PetroChina is facing may be better that China found large

storage of natural gas hydrate, which is seen as the best substitute of oil. The

discovery and successful mining of the natural gas hydrate provide a new developing

path for PetroChina since the political environment in China would allow PetroChina

to take the first chance in the environmentally-friendly growing plan.

8

Part B

2.1 The definition of Independent Audit

Independent auditors are expected to provide the expression of an opinion on the

fairness of a company’s financial reporting with accounting standards, which requires

auditors to state opinions on whether the company’s financial reporting comply with

accounting principles independently. Auditors do not have the responsibility to

prepare financial statements for the company. However, the independent auditor

may utilise his professional knowledge to make comments on the form or content of

the financial reporting. It relies on the auditor himself to decide which auditing

procedure needed to be exercise and his judgements should not be affected in any

circumstances. In the US, audit reports are legally required for statements provided

to SEC. Many companies who are not subject to rules of SEC also prepare audit

report to enhance the credibility of their statements.

Evidence shows that companies who get their reports audited can get loans at lower

interest rates than their peer otherwise (Blackwell, Noland, and Winters, 1998). That

is because auditors, especially independent auditors, serve the purpose of

increasing stakeholders’ confidence in the reliability of financial statements and the

company’s stability. Hence, creditors do not require high interest to cover the risk of

loss. Requirements for getting the professional qualification including certain amount

and level of education and defined the length of practical experience give

independent auditors credibility. Independent auditors are often nominated by the

audit committee that is appointed by the board of directors, which is consist of

shareholders and represent the interests of shareholders.

The audit process starts before accepting an engagement. The auditor needs to

assess the potential risks, the nature and complexity of client’s business and

whether the firm has required resources and expertise to perform required activities.

9

2.1 The definition of Independent Audit

Independent auditors are expected to provide the expression of an opinion on the

fairness of a company’s financial reporting with accounting standards, which requires

auditors to state opinions on whether the company’s financial reporting comply with

accounting principles independently. Auditors do not have the responsibility to

prepare financial statements for the company. However, the independent auditor

may utilise his professional knowledge to make comments on the form or content of

the financial reporting. It relies on the auditor himself to decide which auditing

procedure needed to be exercise and his judgements should not be affected in any

circumstances. In the US, audit reports are legally required for statements provided

to SEC. Many companies who are not subject to rules of SEC also prepare audit

report to enhance the credibility of their statements.

Evidence shows that companies who get their reports audited can get loans at lower

interest rates than their peer otherwise (Blackwell, Noland, and Winters, 1998). That

is because auditors, especially independent auditors, serve the purpose of

increasing stakeholders’ confidence in the reliability of financial statements and the

company’s stability. Hence, creditors do not require high interest to cover the risk of

loss. Requirements for getting the professional qualification including certain amount

and level of education and defined the length of practical experience give

independent auditors credibility. Independent auditors are often nominated by the

audit committee that is appointed by the board of directors, which is consist of

shareholders and represent the interests of shareholders.

The audit process starts before accepting an engagement. The auditor needs to

assess the potential risks, the nature and complexity of client’s business and

whether the firm has required resources and expertise to perform required activities.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In addition, audit firms also conduct detailed due diligence checks on senior

managements and the audit committee as part of client acceptance procedure,

which further increases the accountability of their final products (Kueppers and

Sullivan, 2010). The auditor takes many movements to analysis the company’s

present and past reports, press releases, and its industry in order to gain a whole

picture of the company and to shed light on the risks and material misstatements.

Movements also include consideration of new transactions which are unusual or

significantly different from the past as well as consideration of past audit report on

misstatements.

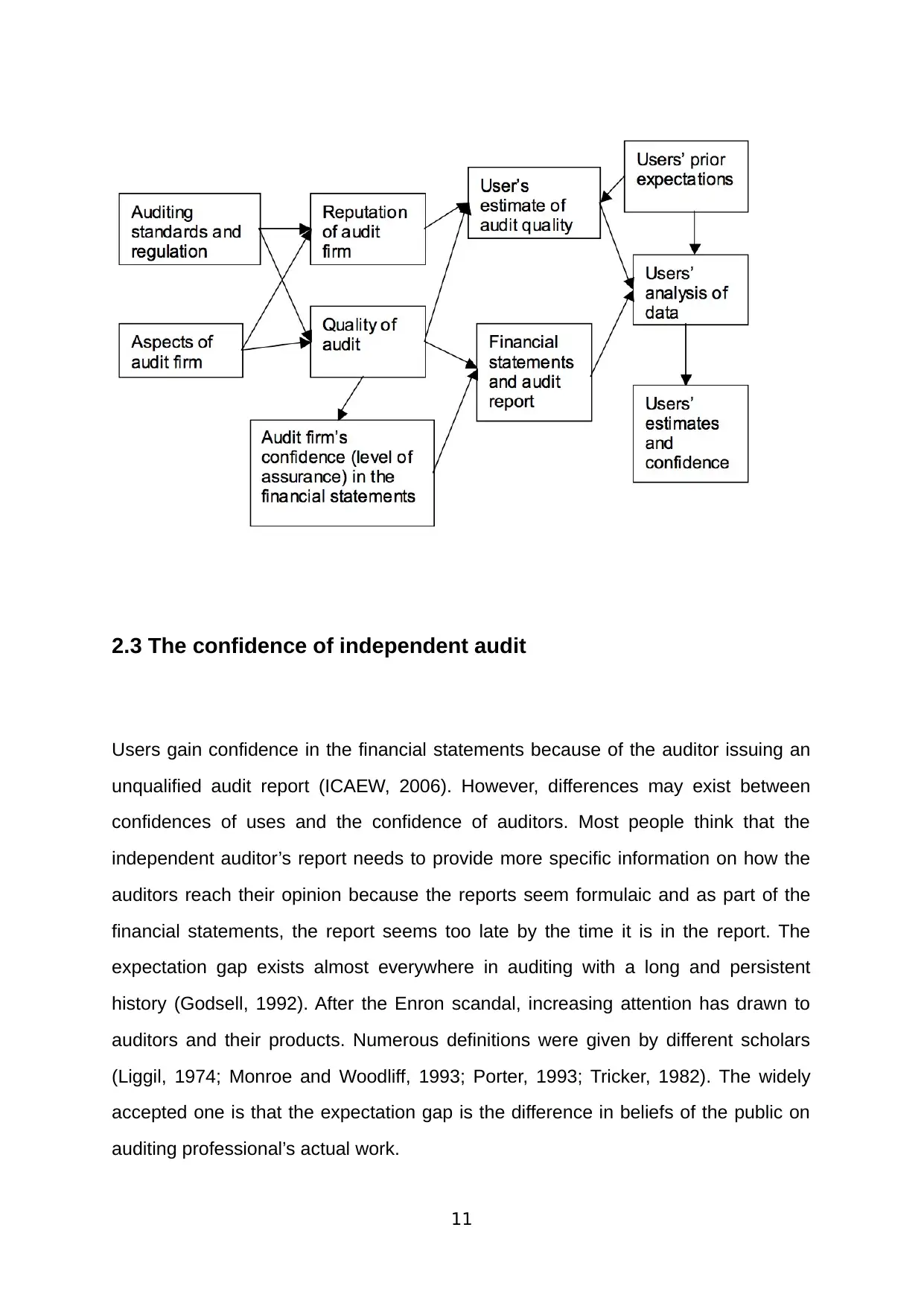

2.2 The assurance of independent audit

According to the PCAOB (1972), an auditor is required to plan and perform audit ‘to

obtain reasonable assurance about whether the financial statements are free of

material misstatement, whether caused by error or fraud’. Reasonable assurance

means a high level, but not absolute, of assurance. Absolute assurance is

considered impossible due to the fact that auditors cannot test every detail of the

company because there is not enough time or budget. The confidence that an

auditor attains is subjective and is the foundation for expressing an audit opinion,

whereas users of financial statements derive their own confidence in the audited

financial statements. Users of financial statements may gain confidence in the

management of a company that they are operating with knowledge of

consequences.

10

managements and the audit committee as part of client acceptance procedure,

which further increases the accountability of their final products (Kueppers and

Sullivan, 2010). The auditor takes many movements to analysis the company’s

present and past reports, press releases, and its industry in order to gain a whole

picture of the company and to shed light on the risks and material misstatements.

Movements also include consideration of new transactions which are unusual or

significantly different from the past as well as consideration of past audit report on

misstatements.

2.2 The assurance of independent audit

According to the PCAOB (1972), an auditor is required to plan and perform audit ‘to

obtain reasonable assurance about whether the financial statements are free of

material misstatement, whether caused by error or fraud’. Reasonable assurance

means a high level, but not absolute, of assurance. Absolute assurance is

considered impossible due to the fact that auditors cannot test every detail of the

company because there is not enough time or budget. The confidence that an

auditor attains is subjective and is the foundation for expressing an audit opinion,

whereas users of financial statements derive their own confidence in the audited

financial statements. Users of financial statements may gain confidence in the

management of a company that they are operating with knowledge of

consequences.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.3 The confidence of independent audit

Users gain confidence in the financial statements because of the auditor issuing an

unqualified audit report (ICAEW, 2006). However, differences may exist between

confidences of uses and the confidence of auditors. Most people think that the

independent auditor’s report needs to provide more specific information on how the

auditors reach their opinion because the reports seem formulaic and as part of the

financial statements, the report seems too late by the time it is in the report. The

expectation gap exists almost everywhere in auditing with a long and persistent

history (Godsell, 1992). After the Enron scandal, increasing attention has drawn to

auditors and their products. Numerous definitions were given by different scholars

(Liggil, 1974; Monroe and Woodliff, 1993; Porter, 1993; Tricker, 1982). The widely

accepted one is that the expectation gap is the difference in beliefs of the public on

auditing professional’s actual work.

11

Users gain confidence in the financial statements because of the auditor issuing an

unqualified audit report (ICAEW, 2006). However, differences may exist between

confidences of uses and the confidence of auditors. Most people think that the

independent auditor’s report needs to provide more specific information on how the

auditors reach their opinion because the reports seem formulaic and as part of the

financial statements, the report seems too late by the time it is in the report. The

expectation gap exists almost everywhere in auditing with a long and persistent

history (Godsell, 1992). After the Enron scandal, increasing attention has drawn to

auditors and their products. Numerous definitions were given by different scholars

(Liggil, 1974; Monroe and Woodliff, 1993; Porter, 1993; Tricker, 1982). The widely

accepted one is that the expectation gap is the difference in beliefs of the public on

auditing professional’s actual work.

11

2.4 Audit expectations gap

Most of the studies determine the gap between auditors’ and public’s view of the

responsibilities of auditors via surveys. Findings show that the public expects

auditors to be more active in detecting and reporting wrongdoings and frauds, which

are not in the principals of audit work. The level of assurance an audit is expected to

provide is also significantly different. The public hold auditors to provide a very high

level of assurance which is simply unable to achieve (Epstein and Geiger, 1994).

Other aspects such as the extent of auditors’ responsibilities to third parties, the

nature of balance sheet assessments, and the validation of and on-going hazards to

auditors’ independence also contain differences.

Several ways can be taken to reduce the expectation gap: expanding audit report,

education, structuring audit methodologies, expansion of auditor’s responsibilities

and enhancement of auditor independence, and so on (Chye Koh and Woo, 1998),

among which education is believed to be the most effective solution. Users tend to

have a higher expectation in auditors’ responsibilities than what auditors themselves

believe reasonable. Such difference resulted in dissatisfaction and criticism on

auditing work. One major criticism addresses the issue that auditors spend extremely

long time with their clients. Hence many suspects the actual independence of

external auditors. The accounting professions have taken measures to address such

gap to the public and try to narrow down the gap by increasing audit quality.

Taking the audit reports of PetroChina’s financial statement as an example, KPMG

issued qualified audit report saying that the company’s 2016 financial statements

present fairly, in all material respects, in accordance with the requirements of

Accounting Standards for Business Enterprises issued by the Ministry of Finance of

the People’s Republic of China. The reports also gave opinions on issues that need

to be noticed by stakeholders along with why the auditor think those issues matter.

The audit report allows users of the financial statement to develop a rather

comprehensive idea of how useful is the financial statement and what issues require

12

Most of the studies determine the gap between auditors’ and public’s view of the

responsibilities of auditors via surveys. Findings show that the public expects

auditors to be more active in detecting and reporting wrongdoings and frauds, which

are not in the principals of audit work. The level of assurance an audit is expected to

provide is also significantly different. The public hold auditors to provide a very high

level of assurance which is simply unable to achieve (Epstein and Geiger, 1994).

Other aspects such as the extent of auditors’ responsibilities to third parties, the

nature of balance sheet assessments, and the validation of and on-going hazards to

auditors’ independence also contain differences.

Several ways can be taken to reduce the expectation gap: expanding audit report,

education, structuring audit methodologies, expansion of auditor’s responsibilities

and enhancement of auditor independence, and so on (Chye Koh and Woo, 1998),

among which education is believed to be the most effective solution. Users tend to

have a higher expectation in auditors’ responsibilities than what auditors themselves

believe reasonable. Such difference resulted in dissatisfaction and criticism on

auditing work. One major criticism addresses the issue that auditors spend extremely

long time with their clients. Hence many suspects the actual independence of

external auditors. The accounting professions have taken measures to address such

gap to the public and try to narrow down the gap by increasing audit quality.

Taking the audit reports of PetroChina’s financial statement as an example, KPMG

issued qualified audit report saying that the company’s 2016 financial statements

present fairly, in all material respects, in accordance with the requirements of

Accounting Standards for Business Enterprises issued by the Ministry of Finance of

the People’s Republic of China. The reports also gave opinions on issues that need

to be noticed by stakeholders along with why the auditor think those issues matter.

The audit report allows users of the financial statement to develop a rather

comprehensive idea of how useful is the financial statement and what issues require

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.