BSMAN3009 - Financial Ratio Analysis of Petronas for 2016 and 2017

VerifiedAdded on 2023/06/03

|23

|4207

|231

Report

AI Summary

This report provides a financial ratio analysis of Petronas, a Malaysian oil and gas company, for the years 2016 and 2017. The analysis encompasses profitability ratios (net profit, return on assets, and return on equity), asset efficiency ratios (average collection period and days inventory outstanding), liquidity analysis (current and quick ratios), capital structure analysis (debt-to-equity ratio), and market performance. The study reveals a significant improvement in Petronas' financial performance in 2017 compared to 2016, with increases in profitability and asset efficiency, indicating effective resource management. The report highlights the importance and limitations of ratio analysis, providing valuable insights into Petronas' financial health and operational effectiveness. Data is presented in RM million, and the report references relevant financial accounting literature.

1

Assessment task 2: Individual report

Assessment task 2: Individual report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive Summary

Financial ratio analysis is the most important part of accounting and finance as it is used

to analyse the performance of entity and also allow the comparison between companies present

report has been drafted to perform the ratio analysis of Petronas, a famous company in Malaysia

that deals in oil and gas production and exploration. In this report, profitability, liquidity

position, capital structure, market performance, and efficiency of company has been evaluated

through use of ratios. It has been found that Petronas has very strong financial performance in

year 2017 as compared to year 2016.

Executive Summary

Financial ratio analysis is the most important part of accounting and finance as it is used

to analyse the performance of entity and also allow the comparison between companies present

report has been drafted to perform the ratio analysis of Petronas, a famous company in Malaysia

that deals in oil and gas production and exploration. In this report, profitability, liquidity

position, capital structure, market performance, and efficiency of company has been evaluated

through use of ratios. It has been found that Petronas has very strong financial performance in

year 2017 as compared to year 2016.

3

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Financial Ratio Analysis of Petronas for year 2016 and 2017........................................................4

Meaning, importance and limitations of ratio analysis....................................................................4

Profitability Analysis of Petronas (All data has been presented in RM million)............................5

Asset Efficiency Analysis (All data has been presented in RM million)........................................8

Liquidity Analysis (Short term solvency analysis) (All data has been presented in RM million) 10

Capital Structure Analysis (All data has been presented in RM million)......................................12

Market Performance (All data has been presented in RM million)...............................................14

Conclusion.....................................................................................................................................15

References......................................................................................................................................17

Appendix........................................................................................................................................18

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Financial Ratio Analysis of Petronas for year 2016 and 2017........................................................4

Meaning, importance and limitations of ratio analysis....................................................................4

Profitability Analysis of Petronas (All data has been presented in RM million)............................5

Asset Efficiency Analysis (All data has been presented in RM million)........................................8

Liquidity Analysis (Short term solvency analysis) (All data has been presented in RM million) 10

Capital Structure Analysis (All data has been presented in RM million)......................................12

Market Performance (All data has been presented in RM million)...............................................14

Conclusion.....................................................................................................................................15

References......................................................................................................................................17

Appendix........................................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Introduction

This report is developed for carrying out financial analysis of a recognized public-listed

company by adopting the use of its recently published annual reports. The financial analysis of

the selected company is undertaken with the use of ratio analysis technique that helps in carrying

out an evaluation of the profitability, asset efficiency, liquidity, and capital structure and market

performance. In this context, the company selected is Petronas, an integrated oil and gas

multinational company of Malaysia that has attained higher position within the Fortune Global

list. The financial ratio analysis of the company has been calculated with the use of financial

reports of the company over the last two financial years.

Financial Ratio Analysis of Petronas for year 2016 and 2017

Meaning, importance and limitations of ratio analysis

Ratio analysis is the important method in accounting and finance used to evaluate the

financial performance of an entity through examining and comparing the financial information

provided in the annual report of such entity. The information gathered through performing the

ratio analysis is used by management and investor to make useful decisions. Management use

ratio analysis to evaluate their efficiency, liquidity performance, leverage position and market

performance during the particular period. On the other had investors use information gathered

from the ratio analysis to make investment decisions. Investors are mainly concerned for

organization profitability, holding period return and market performance as main motive is to

maximize their own wealth. So it can be said that ratio analysis is one of best tool measure the

profitability, operational efficiency, liquidity performance, financial strength, and market

performance of the company and also allow the comparison.

There are numerous uses of ratio analysis in business as it helps in simplifying the

complex accounting statement and other financial data into simple ratio that can be easily

understood by the management and investor to take the required decision. Through the

application or use of ratio analysis management can identify the problems and issues in various

areas. In this way management can take appropriate steps to solve the issues at proper time. Ratio

Introduction

This report is developed for carrying out financial analysis of a recognized public-listed

company by adopting the use of its recently published annual reports. The financial analysis of

the selected company is undertaken with the use of ratio analysis technique that helps in carrying

out an evaluation of the profitability, asset efficiency, liquidity, and capital structure and market

performance. In this context, the company selected is Petronas, an integrated oil and gas

multinational company of Malaysia that has attained higher position within the Fortune Global

list. The financial ratio analysis of the company has been calculated with the use of financial

reports of the company over the last two financial years.

Financial Ratio Analysis of Petronas for year 2016 and 2017

Meaning, importance and limitations of ratio analysis

Ratio analysis is the important method in accounting and finance used to evaluate the

financial performance of an entity through examining and comparing the financial information

provided in the annual report of such entity. The information gathered through performing the

ratio analysis is used by management and investor to make useful decisions. Management use

ratio analysis to evaluate their efficiency, liquidity performance, leverage position and market

performance during the particular period. On the other had investors use information gathered

from the ratio analysis to make investment decisions. Investors are mainly concerned for

organization profitability, holding period return and market performance as main motive is to

maximize their own wealth. So it can be said that ratio analysis is one of best tool measure the

profitability, operational efficiency, liquidity performance, financial strength, and market

performance of the company and also allow the comparison.

There are numerous uses of ratio analysis in business as it helps in simplifying the

complex accounting statement and other financial data into simple ratio that can be easily

understood by the management and investor to take the required decision. Through the

application or use of ratio analysis management can identify the problems and issues in various

areas. In this way management can take appropriate steps to solve the issues at proper time. Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

analysis allows comparing the financial data with competitors or industry average that helps the

management to rank the company in the respective sector and take steps to improve the

performance (Higgins, 2012).

There are limitations of ratio analysis that comes across while making analysis of

financial statements. Ratio analysis uses historical data to make interpretation of financial

performance. It does not mean that same values of ratio will be carried forward in next year. For

this purpose, forecast financial statement can be used for performing ratio analysis and results

derived can be compared with the historical results for consistency.

Ratio analysis can be divided into five major segments that are underline below:

Profitability analysis

Asset efficiency analysis

Liquidity Analysis

Capital Structure Analysis

Market performance

Profitability Analysis of Petronas (All data has been presented in RM million)

Profitability analysis is the most important ratio analysis that measures the entity ability

to earn the profits in relation to sales, assets and equity. The purpose of profitability analysis is to

check the ability of company to earn the revenue in relation to some metric. Purpose is to check

how much resources have used by the company to earn the revenue. Some of important

profitability ratios are net profit ratio, return on assets, return on equity and return on capital

employed. It means profitability analysis helps to analysis how well company is performing in

generating the profits in relation to certain measure like amount of investment.

Ratios Formula 2016 2017

Profitability Ratios

Net profit Ratio Net profit (After tax)

/Revenue or sales 12.18% 20.35%

Return on assets Net profit (After tax) /

Average Total Assets 3.98% 7.57%

analysis allows comparing the financial data with competitors or industry average that helps the

management to rank the company in the respective sector and take steps to improve the

performance (Higgins, 2012).

There are limitations of ratio analysis that comes across while making analysis of

financial statements. Ratio analysis uses historical data to make interpretation of financial

performance. It does not mean that same values of ratio will be carried forward in next year. For

this purpose, forecast financial statement can be used for performing ratio analysis and results

derived can be compared with the historical results for consistency.

Ratio analysis can be divided into five major segments that are underline below:

Profitability analysis

Asset efficiency analysis

Liquidity Analysis

Capital Structure Analysis

Market performance

Profitability Analysis of Petronas (All data has been presented in RM million)

Profitability analysis is the most important ratio analysis that measures the entity ability

to earn the profits in relation to sales, assets and equity. The purpose of profitability analysis is to

check the ability of company to earn the revenue in relation to some metric. Purpose is to check

how much resources have used by the company to earn the revenue. Some of important

profitability ratios are net profit ratio, return on assets, return on equity and return on capital

employed. It means profitability analysis helps to analysis how well company is performing in

generating the profits in relation to certain measure like amount of investment.

Ratios Formula 2016 2017

Profitability Ratios

Net profit Ratio Net profit (After tax)

/Revenue or sales 12.18% 20.35%

Return on assets Net profit (After tax) /

Average Total Assets 3.98% 7.57%

6

Return on equity

Net profit (After tax) /

Average Shareholder's

Equity

5.66% 10.63%

(Annual Report, 2017 and Annual Report, 2016)

(Note: Financial Data can be located at appendix section of this report)

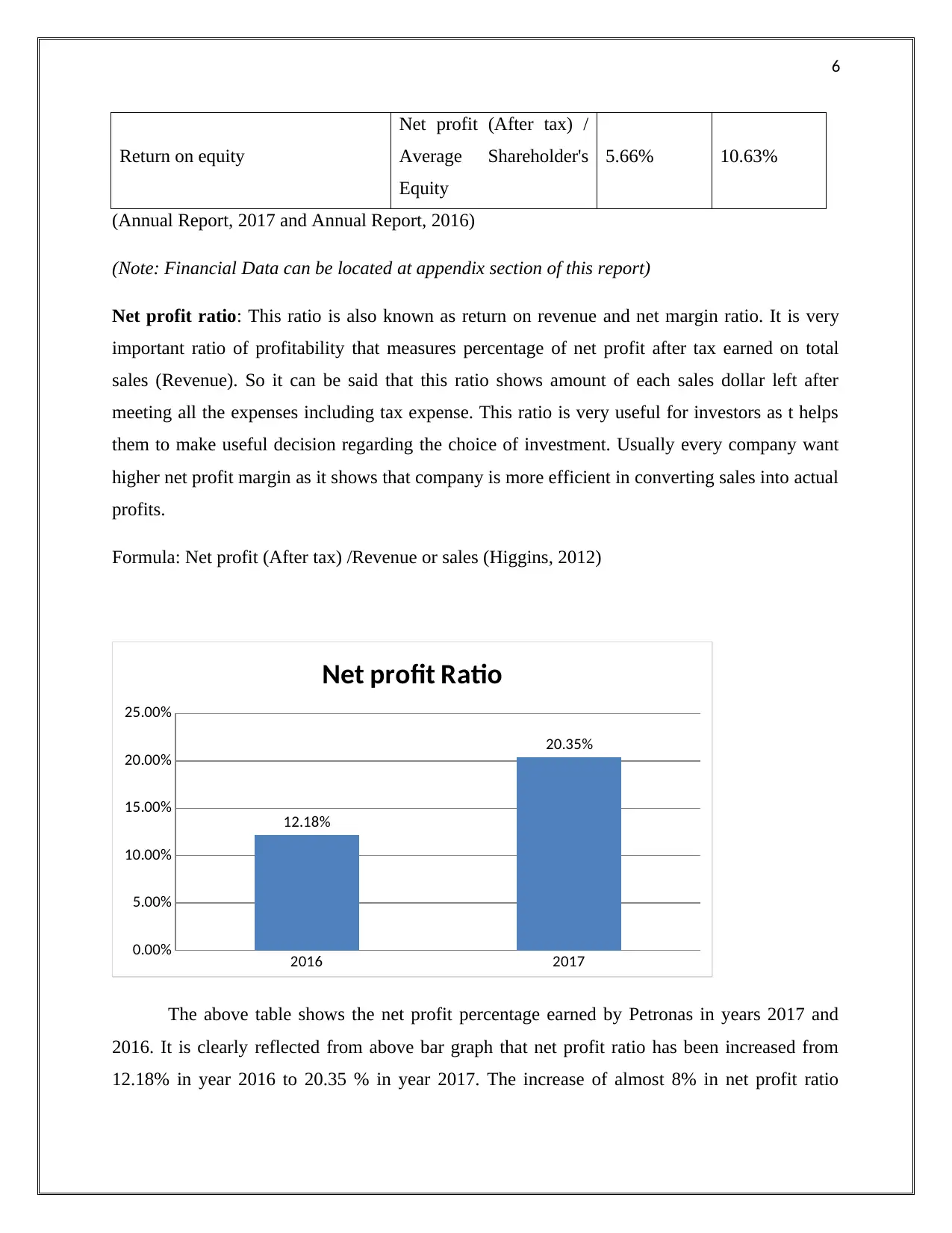

Net profit ratio: This ratio is also known as return on revenue and net margin ratio. It is very

important ratio of profitability that measures percentage of net profit after tax earned on total

sales (Revenue). So it can be said that this ratio shows amount of each sales dollar left after

meeting all the expenses including tax expense. This ratio is very useful for investors as t helps

them to make useful decision regarding the choice of investment. Usually every company want

higher net profit margin as it shows that company is more efficient in converting sales into actual

profits.

Formula: Net profit (After tax) /Revenue or sales (Higgins, 2012)

2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

12.18%

20.35%

Net profit Ratio

The above table shows the net profit percentage earned by Petronas in years 2017 and

2016. It is clearly reflected from above bar graph that net profit ratio has been increased from

12.18% in year 2016 to 20.35 % in year 2017. The increase of almost 8% in net profit ratio

Return on equity

Net profit (After tax) /

Average Shareholder's

Equity

5.66% 10.63%

(Annual Report, 2017 and Annual Report, 2016)

(Note: Financial Data can be located at appendix section of this report)

Net profit ratio: This ratio is also known as return on revenue and net margin ratio. It is very

important ratio of profitability that measures percentage of net profit after tax earned on total

sales (Revenue). So it can be said that this ratio shows amount of each sales dollar left after

meeting all the expenses including tax expense. This ratio is very useful for investors as t helps

them to make useful decision regarding the choice of investment. Usually every company want

higher net profit margin as it shows that company is more efficient in converting sales into actual

profits.

Formula: Net profit (After tax) /Revenue or sales (Higgins, 2012)

2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

12.18%

20.35%

Net profit Ratio

The above table shows the net profit percentage earned by Petronas in years 2017 and

2016. It is clearly reflected from above bar graph that net profit ratio has been increased from

12.18% in year 2016 to 20.35 % in year 2017. The increase of almost 8% in net profit ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

during year 2017 reflects great improvement in ability of management to utilize resources in

optimum manner earn the revenue. Net profit ratio shows an increasing trend in profitability

performance of Petronas.

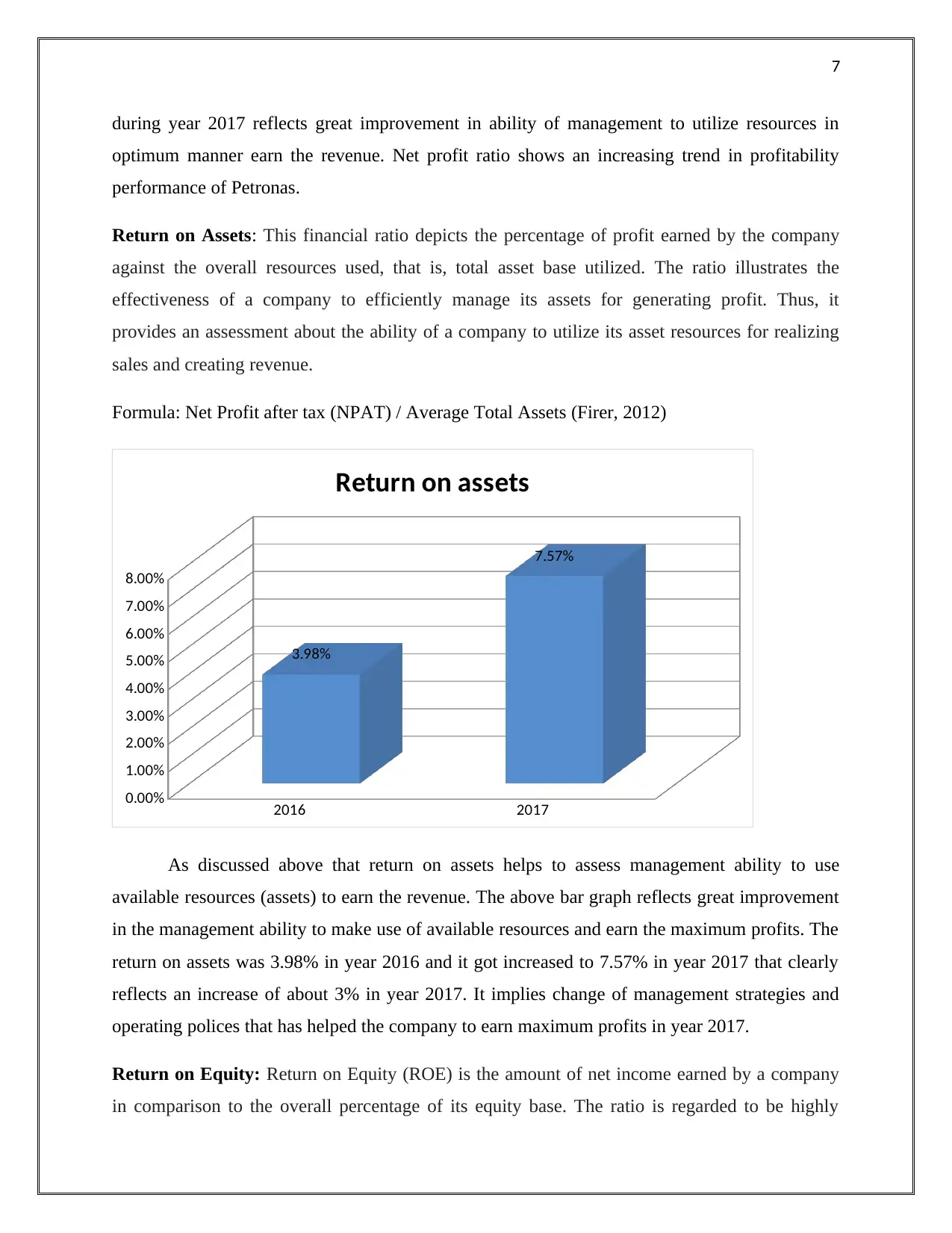

Return on Assets: This financial ratio depicts the percentage of profit earned by the company

against the overall resources used, that is, total asset base utilized. The ratio illustrates the

effectiveness of a company to efficiently manage its assets for generating profit. Thus, it

provides an assessment about the ability of a company to utilize its asset resources for realizing

sales and creating revenue.

Formula: Net Profit after tax (NPAT) / Average Total Assets (Firer, 2012)

2016 2017

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

3.98%

7.57%

Return on assets

As discussed above that return on assets helps to assess management ability to use

available resources (assets) to earn the revenue. The above bar graph reflects great improvement

in the management ability to make use of available resources and earn the maximum profits. The

return on assets was 3.98% in year 2016 and it got increased to 7.57% in year 2017 that clearly

reflects an increase of about 3% in year 2017. It implies change of management strategies and

operating polices that has helped the company to earn maximum profits in year 2017.

Return on Equity: Return on Equity (ROE) is the amount of net income earned by a company

in comparison to the overall percentage of its equity base. The ratio is regarded to be highly

during year 2017 reflects great improvement in ability of management to utilize resources in

optimum manner earn the revenue. Net profit ratio shows an increasing trend in profitability

performance of Petronas.

Return on Assets: This financial ratio depicts the percentage of profit earned by the company

against the overall resources used, that is, total asset base utilized. The ratio illustrates the

effectiveness of a company to efficiently manage its assets for generating profit. Thus, it

provides an assessment about the ability of a company to utilize its asset resources for realizing

sales and creating revenue.

Formula: Net Profit after tax (NPAT) / Average Total Assets (Firer, 2012)

2016 2017

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

3.98%

7.57%

Return on assets

As discussed above that return on assets helps to assess management ability to use

available resources (assets) to earn the revenue. The above bar graph reflects great improvement

in the management ability to make use of available resources and earn the maximum profits. The

return on assets was 3.98% in year 2016 and it got increased to 7.57% in year 2017 that clearly

reflects an increase of about 3% in year 2017. It implies change of management strategies and

operating polices that has helped the company to earn maximum profits in year 2017.

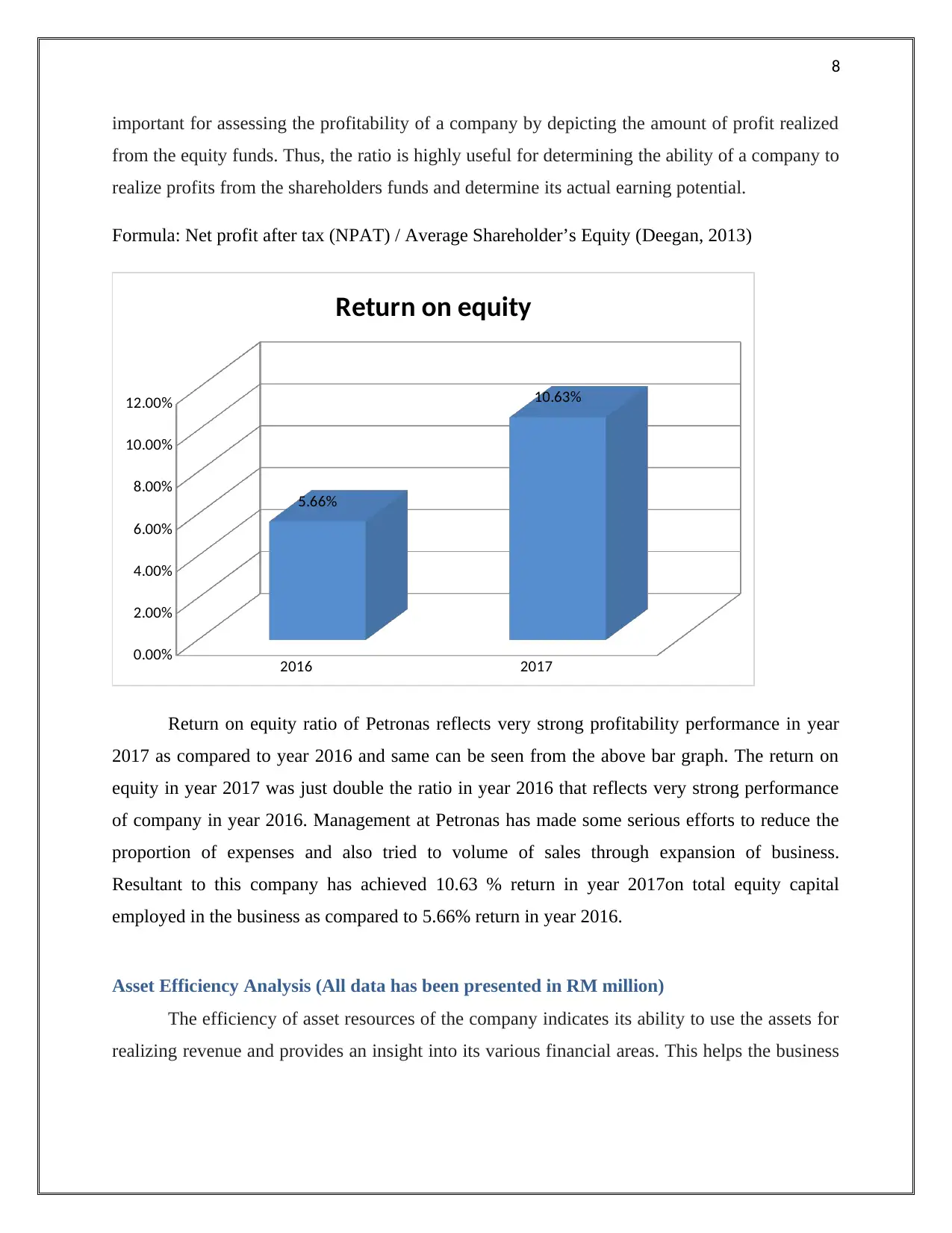

Return on Equity: Return on Equity (ROE) is the amount of net income earned by a company

in comparison to the overall percentage of its equity base. The ratio is regarded to be highly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

important for assessing the profitability of a company by depicting the amount of profit realized

from the equity funds. Thus, the ratio is highly useful for determining the ability of a company to

realize profits from the shareholders funds and determine its actual earning potential.

Formula: Net profit after tax (NPAT) / Average Shareholder’s Equity (Deegan, 2013)

2016 2017

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

5.66%

10.63%

Return on equity

Return on equity ratio of Petronas reflects very strong profitability performance in year

2017 as compared to year 2016 and same can be seen from the above bar graph. The return on

equity in year 2017 was just double the ratio in year 2016 that reflects very strong performance

of company in year 2016. Management at Petronas has made some serious efforts to reduce the

proportion of expenses and also tried to volume of sales through expansion of business.

Resultant to this company has achieved 10.63 % return in year 2017on total equity capital

employed in the business as compared to 5.66% return in year 2016.

Asset Efficiency Analysis (All data has been presented in RM million)

The efficiency of asset resources of the company indicates its ability to use the assets for

realizing revenue and provides an insight into its various financial areas. This helps the business

important for assessing the profitability of a company by depicting the amount of profit realized

from the equity funds. Thus, the ratio is highly useful for determining the ability of a company to

realize profits from the shareholders funds and determine its actual earning potential.

Formula: Net profit after tax (NPAT) / Average Shareholder’s Equity (Deegan, 2013)

2016 2017

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

5.66%

10.63%

Return on equity

Return on equity ratio of Petronas reflects very strong profitability performance in year

2017 as compared to year 2016 and same can be seen from the above bar graph. The return on

equity in year 2017 was just double the ratio in year 2016 that reflects very strong performance

of company in year 2016. Management at Petronas has made some serious efforts to reduce the

proportion of expenses and also tried to volume of sales through expansion of business.

Resultant to this company has achieved 10.63 % return in year 2017on total equity capital

employed in the business as compared to 5.66% return in year 2016.

Asset Efficiency Analysis (All data has been presented in RM million)

The efficiency of asset resources of the company indicates its ability to use the assets for

realizing revenue and provides an insight into its various financial areas. This helps the business

9

manager to identify the particular areas of financial strength and weakness so that asset resources

can be utilized in an effective manner for realizing sales.

Ratios Formula 2016 2017

Asset Efficiency Ratios

Average Collection period in

days (Day Sales Outstanding)

(365*Average

accounts

receivable)/Net

Receivables Sales

85.11 73.47

Day’s inventory outstanding (365*Average

Inventory)/Sales 25.03 23.91

(Annual Report, 2017 and Annual Report, 2016)

(Note: Financial Data can be located at appendix section of this report)

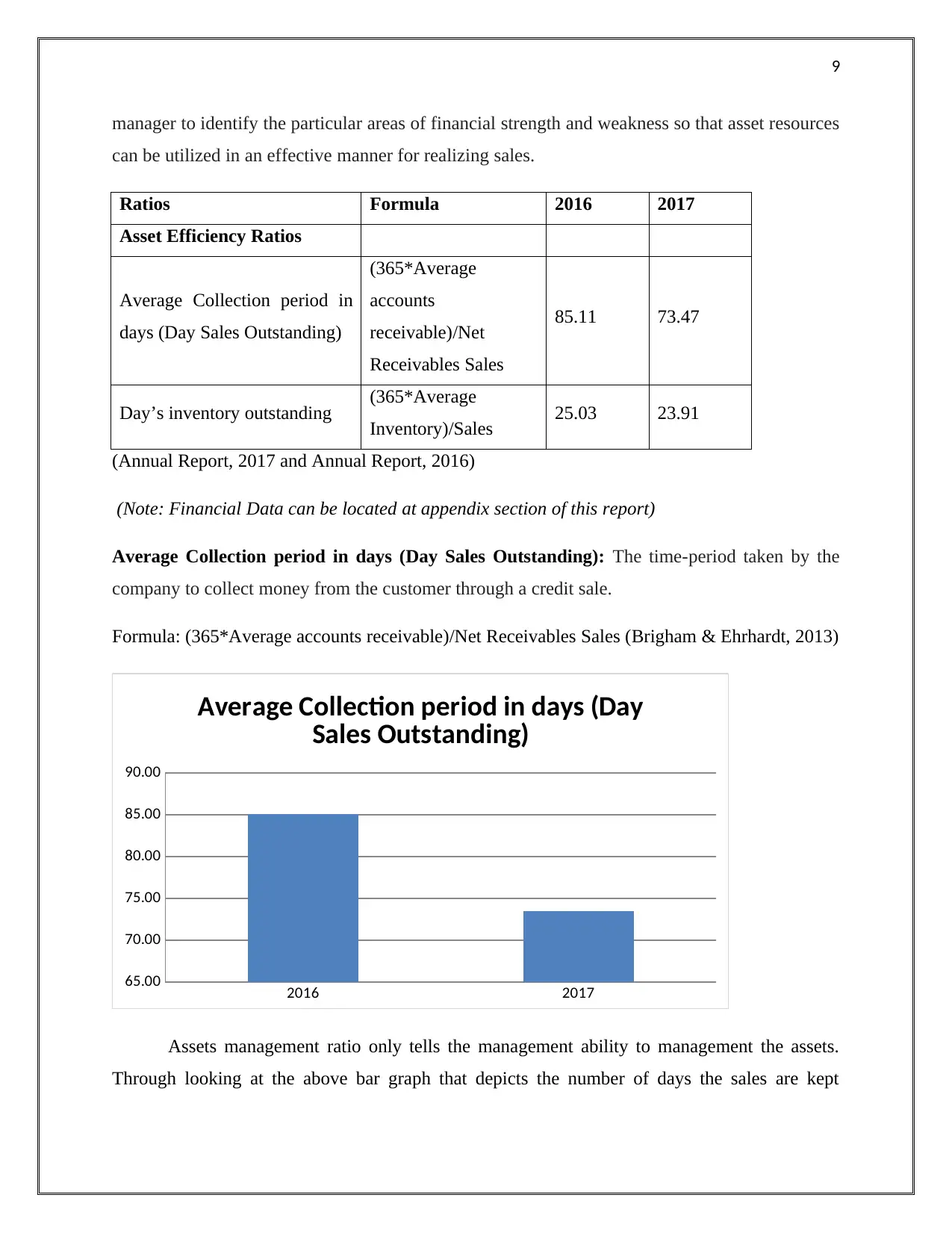

Average Collection period in days (Day Sales Outstanding): The time-period taken by the

company to collect money from the customer through a credit sale.

Formula: (365*Average accounts receivable)/Net Receivables Sales (Brigham & Ehrhardt, 2013)

2016 2017

65.00

70.00

75.00

80.00

85.00

90.00

Average Collection period in days (Day

Sales Outstanding)

Assets management ratio only tells the management ability to management the assets.

Through looking at the above bar graph that depicts the number of days the sales are kept

manager to identify the particular areas of financial strength and weakness so that asset resources

can be utilized in an effective manner for realizing sales.

Ratios Formula 2016 2017

Asset Efficiency Ratios

Average Collection period in

days (Day Sales Outstanding)

(365*Average

accounts

receivable)/Net

Receivables Sales

85.11 73.47

Day’s inventory outstanding (365*Average

Inventory)/Sales 25.03 23.91

(Annual Report, 2017 and Annual Report, 2016)

(Note: Financial Data can be located at appendix section of this report)

Average Collection period in days (Day Sales Outstanding): The time-period taken by the

company to collect money from the customer through a credit sale.

Formula: (365*Average accounts receivable)/Net Receivables Sales (Brigham & Ehrhardt, 2013)

2016 2017

65.00

70.00

75.00

80.00

85.00

90.00

Average Collection period in days (Day

Sales Outstanding)

Assets management ratio only tells the management ability to management the assets.

Through looking at the above bar graph that depicts the number of days the sales are kept

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

outstanding, it can be said that efficiency of management at Petronas has improved as there has

been decrease in this ratio. The analysis of above bar graph says that in year 2016, management

requires 85 days to collect the outstanding sales and in year 2017 it got reduced to 73 days. So it

can be said that management has tried to improve the policies of asset management and also get

success. The decrease in days sales outstanding will helps the company to collect cash from

customer far early as expected and also helps to increase the working capital within the business.

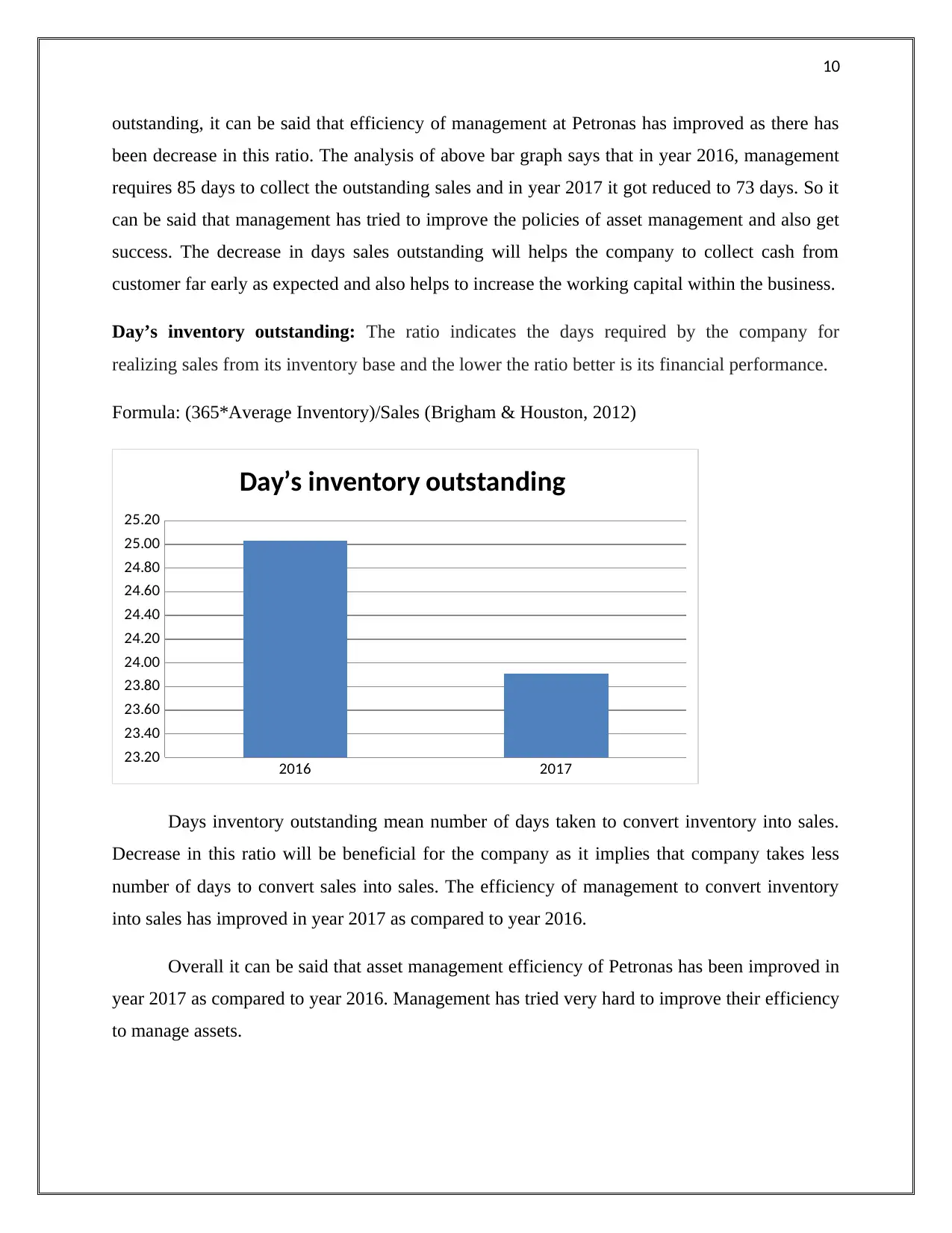

Day’s inventory outstanding: The ratio indicates the days required by the company for

realizing sales from its inventory base and the lower the ratio better is its financial performance.

Formula: (365*Average Inventory)/Sales (Brigham & Houston, 2012)

2016 2017

23.20

23.40

23.60

23.80

24.00

24.20

24.40

24.60

24.80

25.00

25.20

Day’s inventory outstanding

Days inventory outstanding mean number of days taken to convert inventory into sales.

Decrease in this ratio will be beneficial for the company as it implies that company takes less

number of days to convert sales into sales. The efficiency of management to convert inventory

into sales has improved in year 2017 as compared to year 2016.

Overall it can be said that asset management efficiency of Petronas has been improved in

year 2017 as compared to year 2016. Management has tried very hard to improve their efficiency

to manage assets.

outstanding, it can be said that efficiency of management at Petronas has improved as there has

been decrease in this ratio. The analysis of above bar graph says that in year 2016, management

requires 85 days to collect the outstanding sales and in year 2017 it got reduced to 73 days. So it

can be said that management has tried to improve the policies of asset management and also get

success. The decrease in days sales outstanding will helps the company to collect cash from

customer far early as expected and also helps to increase the working capital within the business.

Day’s inventory outstanding: The ratio indicates the days required by the company for

realizing sales from its inventory base and the lower the ratio better is its financial performance.

Formula: (365*Average Inventory)/Sales (Brigham & Houston, 2012)

2016 2017

23.20

23.40

23.60

23.80

24.00

24.20

24.40

24.60

24.80

25.00

25.20

Day’s inventory outstanding

Days inventory outstanding mean number of days taken to convert inventory into sales.

Decrease in this ratio will be beneficial for the company as it implies that company takes less

number of days to convert sales into sales. The efficiency of management to convert inventory

into sales has improved in year 2017 as compared to year 2016.

Overall it can be said that asset management efficiency of Petronas has been improved in

year 2017 as compared to year 2016. Management has tried very hard to improve their efficiency

to manage assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Liquidity Analysis (Short term solvency analysis) (All data has been presented in RM

million)

The liquidity analysis depicts the ability of a company to meet its financial obligations

from its asset base. This can be assessed by the calculation of the current as well as quick ratio

by the company that determines its ability to generate sufficient cash inflows for avoiding the

financial risk of insolvency.

Ratios Formula 2016 2017

Liquidity Analysis (Short

term solvency ratios)

Current Ratio

Current

Assets/Current

liabilities

2.57 2.93

Quick Ratio: Quick Assets/Current

liabilities 2.38 2.71

(Annual Report, 2017 and Annual Report, 2016)

(Note: Financial Data can be located at appendix section of this report)

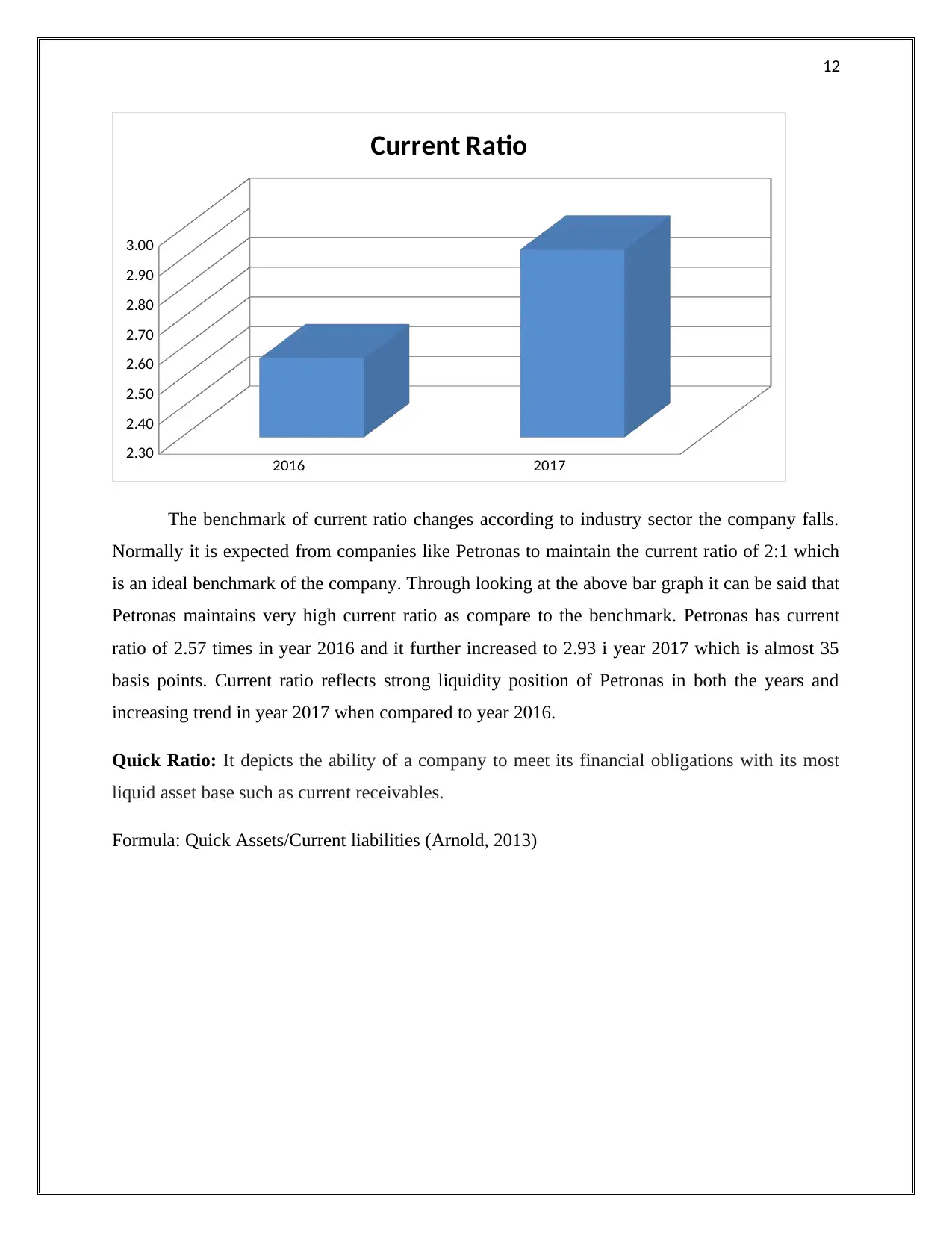

Current Ratio: The ratio depicts the ability of a company to meet its short-term financial

obligations with its current asset base such as cash equivalents, marketable securities that can

easily transferred into cash within short-term period of time.

Formula: Current Assets/Current liabilities (Baker & Nofsinger, 2010)

Liquidity Analysis (Short term solvency analysis) (All data has been presented in RM

million)

The liquidity analysis depicts the ability of a company to meet its financial obligations

from its asset base. This can be assessed by the calculation of the current as well as quick ratio

by the company that determines its ability to generate sufficient cash inflows for avoiding the

financial risk of insolvency.

Ratios Formula 2016 2017

Liquidity Analysis (Short

term solvency ratios)

Current Ratio

Current

Assets/Current

liabilities

2.57 2.93

Quick Ratio: Quick Assets/Current

liabilities 2.38 2.71

(Annual Report, 2017 and Annual Report, 2016)

(Note: Financial Data can be located at appendix section of this report)

Current Ratio: The ratio depicts the ability of a company to meet its short-term financial

obligations with its current asset base such as cash equivalents, marketable securities that can

easily transferred into cash within short-term period of time.

Formula: Current Assets/Current liabilities (Baker & Nofsinger, 2010)

12

2016 2017

2.30

2.40

2.50

2.60

2.70

2.80

2.90

3.00

Current Ratio

The benchmark of current ratio changes according to industry sector the company falls.

Normally it is expected from companies like Petronas to maintain the current ratio of 2:1 which

is an ideal benchmark of the company. Through looking at the above bar graph it can be said that

Petronas maintains very high current ratio as compare to the benchmark. Petronas has current

ratio of 2.57 times in year 2016 and it further increased to 2.93 i year 2017 which is almost 35

basis points. Current ratio reflects strong liquidity position of Petronas in both the years and

increasing trend in year 2017 when compared to year 2016.

Quick Ratio: It depicts the ability of a company to meet its financial obligations with its most

liquid asset base such as current receivables.

Formula: Quick Assets/Current liabilities (Arnold, 2013)

2016 2017

2.30

2.40

2.50

2.60

2.70

2.80

2.90

3.00

Current Ratio

The benchmark of current ratio changes according to industry sector the company falls.

Normally it is expected from companies like Petronas to maintain the current ratio of 2:1 which

is an ideal benchmark of the company. Through looking at the above bar graph it can be said that

Petronas maintains very high current ratio as compare to the benchmark. Petronas has current

ratio of 2.57 times in year 2016 and it further increased to 2.93 i year 2017 which is almost 35

basis points. Current ratio reflects strong liquidity position of Petronas in both the years and

increasing trend in year 2017 when compared to year 2016.

Quick Ratio: It depicts the ability of a company to meet its financial obligations with its most

liquid asset base such as current receivables.

Formula: Quick Assets/Current liabilities (Arnold, 2013)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.